Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor

$950

$760

$570

$380

$190

$0

$937

$170

Growth of real wealth

1988 1994

Nexus

CPI

1999 2004 2009 2013

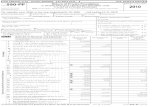

Building Value for ClientsSince its establishment in 1988, Nexus has pursued an investment approach which concentrates on real growth inclient wealth over the long term. The chart illustrates the impact of this long-term investment thinking – a $100 investment in a balanced portfolio in 1989 has grown to $937 at December 31, 2013.

March 2004Volume 9, Issue 1

Inside Articles The BIg ChIllSITTIng on The SIdelIneS WhAT ClIenTS Are ASkIng USPeArlS of WISdom

Nexus Investment Management Inc. Portfolio Management & Financial Counsel

$100 Investment with nexus in 1989

March 2014Vol.19 No. 1

notes

from the editor

The Big Chill

The after-effects of the crisis – low interest rates, unemployment and undervalued assets – have been a dominant influence on the markets since then. 2013 was a welcome change for investors, with its more positive outlook for economic growth and robust stock market returns, especially in the U.S. 2014, however, has had a mixed start to the year with many people having reservations that the good times were too good to be true. New political worries have surfaced in the emerging markets in general and in the Ukraine in particular. There have also been softer than expected economic reports – slack sales, weak employment data and poor industrial output. Apparently, we can blame this on the weather. According to reports from official government agencies, private surveys and corporations, it has been the colder-than-normal weather and heavy snowfall across large sections of the U.S. (and Canada) that have been responsible for this economic news. A big chill indeed!

With every chill comes investor anxiety. While there will be a thaw in the weather for sure, investor anxiety isn’t as easily alleviated. The best way to combat anxiety and stay invested despite troubling news is to find the right investment approach that works in good times and bad. You have heard us say many times that timing the market and trying to predict short-term market movements is a ‘mug’s game’. It is our belief that the best approach for investors is to stick to a long-term discipline and avoid the temptation of market timing. Nexus’s disciplined investment approach seeks to achieve the “Holy Grail” of investing. This being lower-than-market volatility, outperformance in down markets (capital preservation), and superior long-term returns. In November of last year, we hosted our annual client

event and presented on this very topic. For those unable to attend, the presentation, complete with references to military strategy, a surprise appearance from Carnac the Magnificent and a pinch of Monty Python, is available for viewing on our website, www.nexusinvestments.com, under the Publications heading. Our clients always ask interesting questions at this event. In this issue of Nexus Notes we have included two questions that were asked by our clients: Is it a good idea to use ETFs? and What is Nexus’s most aggressive holding?

One of the signs of the times is how much cash investors have on hand. When investors are anxious, they will hold cash despite the fact that it earns next to nothing. In this issue of Nexus Notes, our new investment analyst, Devin Crago, has penned an article on what it means for an investor to be sitting on the sidelines holding cash. Cash can be useful to fund short-term spending needs, but cash alone will not fund your retirement. The Nexus North American Income Fund (NNAIF) provides one way to step carefully off the sidelines without having to plunge headlong into the stock market.

Here’s hoping that Spring and the “big thaw” are just around the corner!

It is amazing that five years have already passed since the financial crisis.

DCW

Sitting on the SidelinesA recent survey from investment management firm BlackRock concluded that 35% of affluent investors’ assets are sitting in cash and savings accounts.A mountAin of cAshA separate survey from UBS stated a modestly lower number of 28%1. Either way, when compared to the norm (about 5% of a portfolio allocated to cash), these high percentages illustrate a mood of heightened anxiety that has produced a willingness on the part of investors to hold cash instruments that yield almost no return. The markets are in uncharted waters and many have chosen to sail with caution.To help put these numbers in context, consider this figure from the U.S. Federal Reserve: U.S. investors have some $10.8 trillion sitting in cash and cash-like investments. That’s a big number – roughly two thirds of U.S. Gross Domestic Product (GDP). This mountain of cash has given rise to the phrase, “there is a lot of cash on the sidelines”, an expression which is being bandied about on Wall Street, Bay Street and in the financial media to describe the phenomenon of investors seeking safety in cash rather than investing in stocks, bonds or other investments. While we are strong believers in the idea that holding some cash provides valuable “optionality” (meaning that keeping cash on hand today affords you the option to buy when bargains become available tomorrow), today’s elevated cash levels are intriguing and warrant further discussion.

WhAt does “the sidelines” meAn? And WhAt does it meAn for mArkets?Not everyone agrees as to just what “cash on the sidelines” really means. In an amusing and insightful article entitled “My Top 10 Peeves”, Cliff Asness of AQR Capital Management takes exception to the loose use of the phrase:

Every time someone says, “There is a lot of cash on the sidelines,” a tiny part of my soul dies. There are no sidelines. Those saying this seem to envision a seller of stocks moving her money to

iNVeStmeNtS

1 “Cash is Still King for Affluent Investors.” Financial Times. December 6, 2013.

2 Clifford S. Asness, “My Top 10 Peeves.” Financial Analysts Journal Vol 70 (2014).

3 In 2013 Canadian investors received an average rate of 0.78% on 1-year GICs.

cash and awaiting a chance to return. But they always ignore that this seller sold to somebody, who presumably moved a precisely equal amount of cash off the sidelines.2

If this popular phrase simply isn’t true and cash can’t, in fact, move on and off the sidelines, does it really matter that investors are holding high levels of cash? In a word, yes, and one of the main consequences could be higher future equity prices. Over time, as more investors decide that they want to reduce their cash holdings and get back into the markets, the demand for stocks will rise while the supply of stocks will stay more or less the same, exerting upward pressure on stock prices.Using a simple example, imagine what would happen to the price of a coveted ticket to the Olympic gold medal hockey game if fans who had been waiting to buy suddenly came out in droves. The seller would increase the price of the ticket in response to that demand and sell to the highest bidder. For equity markets, a similar dynamic is likely to play out when investors begin to collectively show a greater appetite for investing in equities – the amount of cash won’t change but the demand for scarce assets (stocks) will increase.

A Whole lottA nuthin’...Putting aside the debate on the validity of the phrase “cash on the sidelines” for the moment, let’s just focus on the fact that investors are holding an awful lot of cash. So, what are investors earning on this cash that is sitting on the proverbial sidelines?For Canadians the answer is, unfortunately, next to nothing or, more specifically, about 0.78%3. While returns on cash for Canadians have been paltry, the issue is even more acute in the U.S. market. We can see from the chart below that the amount a U.S. investor earned

Sitting on the Sidelines cont.’d

iNVeStmeNtS

4 In 2013 U.S. investors received an average rate of 0.27% on 6-month negotiable certificates of deposit. This compares to an average rate of about 6% during the period 1964 to 2012.

5 Klarman, Seth. “Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor” (1991).

in 2013 on US$100,000 invested in 6-month certificates of deposit was an appalling US$270 (yes, you read that correctly). In 2006, prior to the financial crisis, that same investment would have generated US$5,240 of income per year4.

In addition to the slim returns investors can earn in cash instruments, bond investors are also facing much lower income streams than were available historically — again due to the low level of interest rates. That subject was covered in our last edition of Nexus Notes, so we won’t go into it any further here, but suffice it to say that investors are facing the very real prospect of interest rates that are “lower for longer” and correspondingly low income streams.

in the long term, it’s tough to Win the gAme from the sidelines

So, what are individual investors to do? Over the long term, most individuals simply cannot fund their retirements by maintaining such high allocations to low yielding cash and bonds. Nor should they engage in speculative market timing, entering and exiting the markets according to the news of the day. In some respects, the current focus on whether an investor is on or off the sidelines is reminiscent of exactly that: a debate over when is the right time to jump in or out of the market. Respected value investor Seth Klarman eloquently dismisses that strategy with this statement: “In reality, no one knows what the market will do; trying to predict

it is a waste of time, and investing based upon that prediction is a speculative undertaking”5.

Rather, what each investor needs is a financial plan containing strategies to achieve their long-term goals. Although it’s never easy, it is important to ignore the noise of the market and concentrate on the ingredients for long-term success:

Invest in high quality businesses...

... and buy those businesses at good prices

Intelligently diversify your portfolio

Manage risk

Apply a strategic asset allocation mix that addresses your specific needs

Try to keep your emotions in check and stick to the plan

the sWing mAy hAve AlreAdy stArted

One of the most dependable patterns in the financial markets is the pendulum of human emotion that swings from extremes of fear and risk aversion to extremes of greed and optimism. As we pointed out earlier, today’s investment climate is marked by a significant amount of investor anxiety, with the result that investors have been happy to hold cash that yields next to nothing.

As residual fear from the financial crisis fades and the pendulum swings back towards optimism, we expect investors will collectively attempt to reduce their cash holdings and rotate back towards equities. As this happens, the dynamics described above should increase demand for stocks and provide a tailwind for equity prices. Indeed, judging by the remarkable rise in markets in 2013, it can be argued with some conviction that this process may have already begun.

1986 1996 20061991 2001 2011

2013$270

2006$5,240

$ 10,000$9,000$8,000$7,000$6,000$5,000$4,000$3,000$2,000$1,000

$0

Annual Income Generated by $100,000 Investmentin a 6-month CD (US$)

DMC

fiNaNcial PlaNNiNg

What Clients Are Asking Us

Below, we highlight two questions which we feel may be of interest to our readers that came up in our annual client presentation in November.

1. Are pAssive index funds And etfs risky for investors?

Passive index funds and exchange-traded funds (ETFs) are designed to perform in-line with a particular index or sector or specialty theme. They allow investors the opportunity to get broad market exposure through a single investment vehicle. There are billions of dollars invested in the hundreds of ETFs available to investors in Canada; they offer exposure to everything from the TSX 60 Index to global infrastructure stocks to an index of Canadian junior oil stocks. While these investment vehicles may appear attractive on the surface, we suggest that they are not suitable for all investors. Embedded fees and expenses can be quite high, particularly for smaller ETFs with specialty and/or global exposure. In addition, the “passive” nature of the funds means that investors get exposure to equities that are included for quantitative rather than qualitative reasons. This resulted in Nortel’s stock making up more than one-third of the value of the TSE ETF in August 2000, and mining scam Bre-X Minerals being included in the TSE index before it vaporised in 1997.

We see the proliferation of these passive investment vehicles as an advantage to Nexus and our clients. We find that there is less fundamental research being done on companies and that passive fund re-balancing, by its nature, causes passive fund managers to buy high and sell low. This creates advantages for us and allows us the opportunity to add value.

As an active manager, Nexus believes that our investment decision-making will meaningfully improve investment

outcomes. In fact, as we demonstrated in this year’s presentation, Nexus’s “active share” at September 30, 2013 was 73%. That means that 73% of the holdings in the Nexus Equity Fund differed from its benchmark. ETFs can be useful in certain circumstances, but we think that emphasizing them too much risks creating unwelcome consequences.

2. WhAt is our most Aggressive holding?

In terms of the stock in our portfolios with the highest price-earnings multiple, it is likely Gilead Sciences. Gilead is a biotechnology company that researches, develops and commercializes pharmaceuticals primarily focussing on HIV/AIDS, liver diseases such as hepatitis B and C, and cardiovascular and respiratory conditions. One of the more recognizable products developed by Gilead is Tamiflu1, which was widely used (as well as stockpiled by various governments) during the global outbreak of H5N1 avian flu in 2005.

While the stock trades at a P-E multiple in excess of 30 times, versus the S&P 500 at approximately 17 times, we feel that it is justified based on the company’s strong record of growth and the pending launch of highly profitable new drug therapies. We are particularly enthusiastic about two drug compounds which have shown well in late stage clinical trials addressing hepatitis C and leukemia.

On its own, Gilead appears “aggressive”, but because its business is so different from our other holdings it actually helps to diversify the portfolio. However, simply being different is insufficient justification for purchase. In fact, Gilead has a future earnings profit that we believe will justify today’s valuation.

Whenever we host client events, like the annual event at the National Club or our regular pooled fund lunches in the office, it gives us a good opportunity to hear what is on our clients’ minds and to answer questions at the end of our presentations.

1 Tamiflu is marketed by Roche today.

JEH

“I’ ll put it back to work someday, but right now it feels great to have it lying around in humongous clumps.”

We don’t normally trumpet our performance. But a recent survey shows that the Nexus North American Income Fund’s return numbers, over both the short and long term, have been rather, well, remarkable.

Nexus North American Income Fund Performs

NeWS flaSh

Morningstar Canada publishes a performance survey of various mutual funds based on their respective investment mandates. The Nexus North American Income Fund, which is a pooled fund offered only to Nexus clients (with whom we have a “managed account” relationship), is not included in the survey. Nevertheless, it is interesting to compare it to its closest Morningstar peer group – the “Canadian Core Fixed Income” category. The Nexus Fund returns compare very favourably to the mutual fund returns in the survey for each of the 1-, 2-, 3-, 5- and 10-year periods ending December 31, 2013. Two things bear highlighting, however. First, not all of the mutual funds in the peer group have an allocation to “income-oriented equities” as the Nexus fund does. Second,

Source – Morningstar Canada, Nexus - Period ending December 31, 2013.

the Nexus fund returns are presented before the deduction of investment management fees, while the peer group returns are presented after deducting such fees. (This is because Nexus’s fees are different for each client, being based on the value of the client’s family portfolio.) Even after accounting for these factors, the Nexus North American Income Fund performance stands out in comparison.

As Devin Crago points out in an accompanying Nexus Notes article, “It’s tough to win the game from the sidelines”, but there are plenty of reasons why a quality fixed income component is an important part of a disciplined financial plan. Compared to the returns currently available from cash, GICs and many other fixed income alternatives, the Nexus North American Income Fund could provide an attractive alternative.

The Fund invests in a combination of money market securities, investment grade bonds and up to 20% of its assets in Canadian and U.S. income-generating equities. Distributions of interest and dividends from the fund are made monthly and, in most cases, re-invested in additional units of the fund.

If you would like to discuss how we might help you make the most of your sidelined assets, please don’t hesitate to contact us.

5th Percentile Return (after fees)

Median Return (after fees)

Fund Count

4.6% 5.9%5.2% 7.3% 6.4%

Annualized Returns

1-Year 2-Year 3-Year 5-Year 10-Year

Nexus Income Fund (before fees)

1.5%

-1.5%

501

3.6%

0.9%

371

4.8%

3.0%

314

6.6%

4.3%

216

5.1%

4.0%

101

Morningstar Bond Funds

JEH

• CBC News recently conducted a survey of Canadian retirement plans. The results are certainly interesting, and in some aspects, deeply disturbing for the future of many baby boomers. 89% of respondents said they would be relying on CPP, and of those, 51% said they would rely “heavily” on CPP. Since CPP tops out at $1,000 per month there obviously needs to be some other source of income to even reach the poverty line. 59% of people said they would likely take a part-time job to support retirement. 49% said they would sell their home or other real estate. 40% said they were counting on an inheritance. The most frightening insight, however, is that 34% of respondents claim to be counting on a lottery win to make their retirement plan work. (www.cbc.ca, posted January 20, 2014 at 11:22 a.m.)

• Many will have read about the concept of “Peak Oil”, which is the idea that the world’s ability to grow the daily production of oil has peaked and will steadily decline over the decades to come. Bloomberg borrowed this concept in a recent article about “Peak Car”. Most people assume that the automobile market will continue to grow, or even accelerate, as the wealth in many emerging economies like China allows a growing segment of its population to afford such a luxury. A recent PriceWaterhouse survey, however, points out that half the world’s population today lives in an urban area, but this is likely to grow by 25% to 50% over the next decade. The result will be urban gridlock which means that fewer people will opt for cars and will seek other ways to get around. Public transit and car sharing are likely to represent a significantly larger share of urban transportation than they do today. In fact, the Bloomberg article points out that some underlying trends supporting this idea already are in place. In 1983, 87% of 19-year-olds in the U.S. had a drivers license.

In 2010 the number had fallen to less than 70%. More kids live in cities and fewer have the need or the opportunity to drive around. No one is predicting a precipitous decline in the demand for cars. But over the decades ahead, the forces of urbanization may eventually result in fewer cars rolling off the assembly line. (Jeff Green and Keith Naughton, Bloomberg, February 24, 2014.)

• The designer handbag is an important accessory for many women in Hong Kong. For some, however, the passion to accessorize outstrips their ability to finance it. The Wall Street Journal recently reported about the rise of certain non-bank lenders that actually offer loans based on the collateral of a woman’s handbag. “Yes Lady Finance Co.” is willing to lend up to 80% of the value of a bag by Gucci, Chanel, Hermès or Louis Vuitton. Sometimes it will consider Prada. While this business is essentially a pawnbroker, pawnbrokers typically target poorer residents and foreign domestic workers. Yes Lady targets the affluent Hong Kong woman who wants to quickly access financing to acquire the latest “must have” bag. And with interest rates well below 10%, what is not to like? In order to get the purse back, the loan must be repaid in four months. Apparently, almost all clients do exactly that. Perhaps by borrowing against another bag? (The Wall Street Journal, August 13, 2013.)

• Who would have thought love and emotion were economically cyclical? Turns out that couples think twice about breaking up when times are tough. Divorce in the U.S. fell to a 40-year low in 2009 during the depths of the recession, but has rebounded sharply along with the economic recovery since then. (Barron’s, February 24, 2014.)

Pearls of WisdomReading is one of the principal occupations in our profession. As we digest a wide range of material, interesting ideas and surprising facts – some serious and some light-hearted – rise to the surface. We attempt to share a few of those with you in each of our issues of Nexus Notes.

JCAS

miScellaNeouS

Tel: (416) 360-0580 or 1 (888) 756-9999Fax:(416) 360-8289email: [email protected]: nexusinvestments.com

William W. BerghuisR. Denys Calvin, CFA Geoffrey J. Gouinlock, CFAFergus W. Gould, CFAJames E. HoustonJohn C.A. Stevenson, CFADianne C. White, CA, CFP, TEP

Nexus Investment Management Inc.111 Richmond Street West, Suite 801 Toronto, Ontario M5H 2G4

Portfolio Management & Financial Counsel

Exceptional client service and objective advice: tailored to the client’s individual needs.

Superior investment performance1: long-term record of superior after-tax returns and capital preservation.

Disciplined investment approach: “Growth at a Reasonable Price” philosophy, using research and patience.

Alignment with clients’ interests: as the Firm is wholly owned by its principals, we are committed to your financial success.

Cost-effective management: our services are accessible directly, without the costs of branding and distribution.

Nexus Investment Management Inc. provides discretionary investment management and financial counselling services to private clients, trusts, estates and foundations.

The Nexus Notes newsletter is published and distributed by the principals of Nexus Investment Management Inc. for the purpose of providing relevant information to our clients and other interested parties. For additional copies, or to be removed from our mailing list, please contact our office.Publication Mail Agreement 40033917. A composite of Nexus accounts, managed to a balanced mandate, has earned 8.1% per annum, pre-fees for 10 years. A composite of notional returns from a weighted average of the following indices: T-Bill (5%), Bonds (35%), TSX (35%) and S&P 500 (25%) earned a return of 6.3% over the same period.

1