Not Without Its Charms - colliers.com · Korean peninsula and the summit between US President ......

18

Colliers Radar Seoul sProperty 19 June 2018 Not Without Its Charms Seoul office property offers good value for tenants, and near-term attractions for investors

Transcript of Not Without Its Charms - colliers.com · Korean peninsula and the summit between US President ......

Colliers Radar

Seoul sProperty 19 June 2018

Not Without Its Charms Seoul office property offers good value for tenants, and near-term attractions for investors

Judy Jang Associate Director | Research | Seoul

Andrew Haskins Executive Director | Research | Asia

Robust demand in most Asian office

markets is driving up rents. Seoul is

more favourable to tenants, and should

see marginal rent growth and rising

vacancy over the next few years. We

advise tenants to take advantage of this

situation to negotiate new leases now.

Hong Kong and Tokyo were the top

Asian investment markets in Q1, with

Seoul third. We expect volumes in Seoul

to stay firm in H2 and 2019. Looking

further ahead, rapprochement between

South and North Korea improves

prospects for Seoul, and justifies further

reduction in the market's cap rate.

Flexible workspace is growing across

Asia. In Seoul, landlords use flexible

workspace as a tool to cut vacancy.

They should choose operator partners

and plan future strategies carefully to

exploit the concept more successfully.

Executive Summary Conditions in most Asian office leasing markets are firm.

Hong Kong, Singapore and big Chinese and Indian cities

are seeing strong demand from existing and new tenant

sectors, notably technology and flexible workspace

operators. We therefore expect prime grade office rent to

rise further in many cities in 2018, with Singapore likely

to record growth of 10-12%. Seoul is more favourable to

tenants than many other markets, with rent growth set to

be marginal and vacancy to rise over the next few years.

In our view, tenants in Seoul should take advantage of

these conditions to negotiate new leases now.

Investment property markets in Asia remain strong, and

aggregate transactions in Q1 2018 rose 24% YOY, to

USD37.4 billion, based on RCA figures. Hong Kong and

Tokyo were the top two urban investment markets. Seoul

came third, confirming firm investment demand despite

the dull occupier market. Solid yields (4.3% for Grade A

office, 4-5% for retail, 6-7% for logistics) and high sales

listings suggest demand will stay firm in H2 and 2019.

Long-run prospects for Seoul as an investment target

have improved after this year's rapprochement on the

Korean peninsula and the summit between US President

Trump and North Korea's Chairman Kim. Cap rates for

Seoul office property have declined since the GFC, but

may well fall further if financial markets remove the risk

premium traditionally applied to South Korean assets. In

the near term, political reconciliation should boost capital

values in northern Gyeonggi Province in particular.

Flexible workspace is now an integral part of the Asian

commercial property market. It accounts for 3-11% of

Grade A office space in large Asian cities, but for a much

higher proportion of new take-up, and the market should

grow further. Seoul landlords use flexible workspace

largely as a tool to lower vacancy. In our view, landlords

need to choose operator partners and devise future

strategies for flexible workspace carefully, in order to

exploit the concept more profitably and avoid pitfalls

such as the loss of an anchor tenant.

Figure 1: Summary of Asia Prime Grade office market

City Rental growth City vacancy City vacancy

Net income yld*

10 year govt Spread

(2017-21 avg pa) (Q1 2018) (2021E) (Q1 2018) bond yld

Seoul 3.3% 11.8% 14.7% 4.3% 2.7% 1.6pp

Hong Kong 2.1% 5.1% 5.0% 2.4% 2.2% 0.2pp

Singapore 4.1% 5.8% 6.4% 3.6% 2.6% 1.0pp

Shanghai 0.5% 13.6% 12.7% 3.6% 3.6% 0.0pp

Beijing -0.3% 8.7% 14.7% 4.0% 3.6% 0.4pp

Shenzhen 1.1% 11.1% 20.4% 3.9% 3.6% 0.3pp

Taipei 0.6% 12.9% 5.9% 2.8% 0.9% 1.9pp

Bangalore 4.9% 9.1% 7.0% 8.0-8.5% 7.9% 0.1-0.6pp

Source: Colliers International Research, Bloomberg

3 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Contents Seoul market at a glance .................... 4

Asian Office Market Trends ............... 5

Strong conditions in most markets .................. 5

Key market snapshots Q1 2018 ...................... 6

Seoul Office Q1: Higher vacancy due to YBD ................................................. 8

Forecast at a glance ........................................ 8

Leasing Market ................................................ 8

Supply ............................................................. 8

Vacancy Rate and Rent ................................... 9

Outlook ............................................................ 9

Asian Investment Market Trends ..... 10

Market conditions remain firm in Q1 .............. 10

Korean market strong in Q1 2018 ................. 11

Seoul yields above Asian averages ............... 11

Long-run prospects less attractive ................. 12

Rapprochement between the two Koreas a positive surprise ............................................ 13

Implications of reconciliation .......................... 13

Seoul Investment Q1: Still Active .... 14

Forecast at a glance ...................................... 14

Capital Markets: transactions active .............. 14

Asian Flexible Workspace Trends ... 15

Flexible workspace impacts the Seoul office market ..................................... 16

Flexible workspace business status .............. 16

Transaction market impact ............................ 16

4 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Seoul market at a

glance Office market

Seoul Office Market: Demand and Supply

Source: Colliers International Korea

Seoul Office Market: Grade A Rent and Vacancy

Source: Colliers International Korea

Seoul Office Market: Supply Forecasts

Source: Colliers International Korea

Investment market

Asia property transaction volumes by country in Q1 2018 (USD, YOY)

Note. These totals exclude undeveloped land. Source: RCA as of 8

May 2017; calculations by Colliers

Asia property transaction volumes by urban centre in Q1 2018 (USD, YOY)

Note. These totals exclude undeveloped land. Source: RCA as of 8

May 2017; calculations by Colliers

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

(50)

-

50

100

150

200

GLA

('000 s

qm

)

New Supply Net Absorption Vacancy

0%

5%

10%

15%

20%

0

5,000

10,000

15,000

20,000

25,000

30,000

Vacancy

Rate

(%

)

Rent

(KR

W/s

q.m

./m

o)

Overall Rent Vacancy Rate (%)

0

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

000

sqm

CBD GBD YBD Others

Investment Property Transactions in Asian Cities

US$ million Q1 2017 Q1 2018 YoY

Japan 11,715 13,148 12%

China 7,415 9,222 24%

Hong Kong 4,195 7,877 88%

South Korea 2,783 4,404 58%

Singapore 1,587 995 -37%

Taiwan 500 515 3%

India 289 441 53%

Malaysia 369 107 -71%

Thailand 618 33 -95%

Vietnam 78 17 -78%

Investment Property Transactions in Asian Cities

US$ million Q1 2017 Q1 2018 YoY

Hong Kong 4,195 7,877 88%

Tokyo 4,594 6,864 49%

Seoul 1,793 3,613 102%

Shanghai 4,436 1,065 -76%

Nagoya 196 1,006 413%

Singapore 1,587 995 -37%

Guangzhou 179 958 435%

Beijing 917 675 -26%

Yokohama 1,453 566 -61%

Fukuoka 172 291 69%

5 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

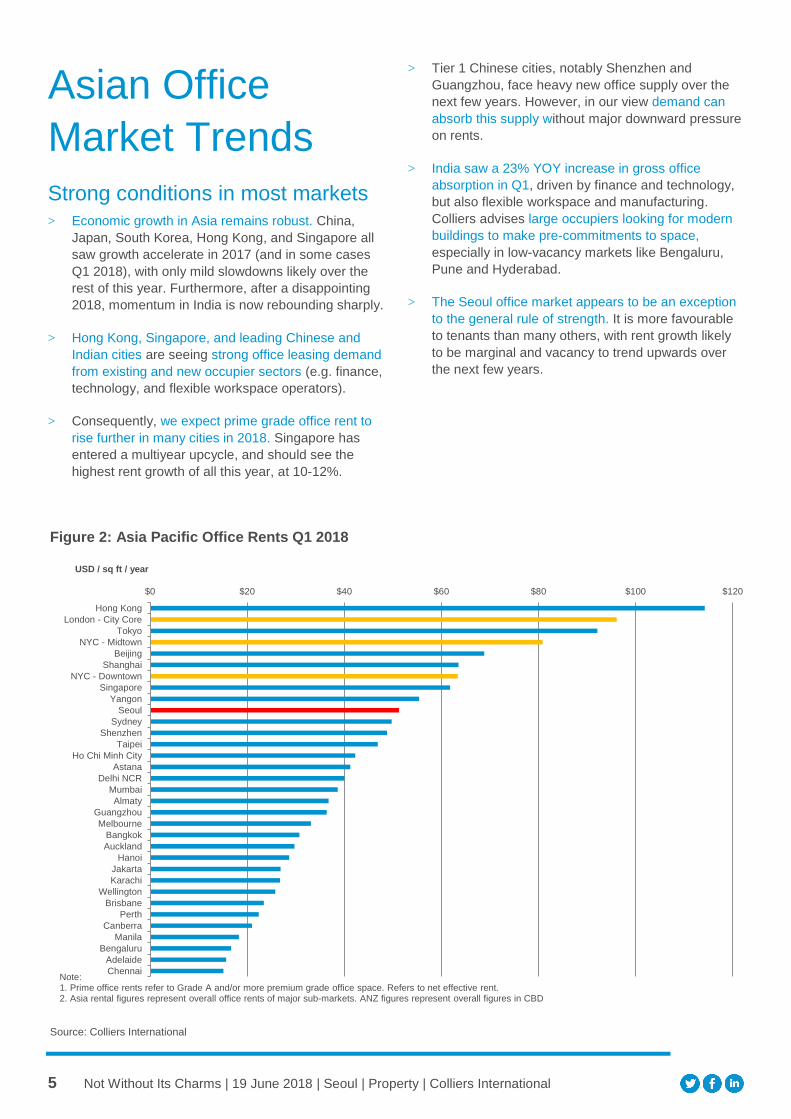

Asian Office

Market Trends

Strong conditions in most markets

> Economic growth in Asia remains robust. China,

Japan, South Korea, Hong Kong, and Singapore all

saw growth accelerate in 2017 (and in some cases

Q1 2018), with only mild slowdowns likely over the

rest of this year. Furthermore, after a disappointing

2018, momentum in India is now rebounding sharply.

> Hong Kong, Singapore, and leading Chinese and

Indian cities are seeing strong office leasing demand

from existing and new occupier sectors (e.g. finance,

technology, and flexible workspace operators).

> Consequently, we expect prime grade office rent to

rise further in many cities in 2018. Singapore has

entered a multiyear upcycle, and should see the

highest rent growth of all this year, at 10-12%.

> Tier 1 Chinese cities, notably Shenzhen and

Guangzhou, face heavy new office supply over the

next few years. However, in our view demand can

absorb this supply without major downward pressure

on rents.

> India saw a 23% YOY increase in gross office

absorption in Q1, driven by finance and technology,

but also flexible workspace and manufacturing.

Colliers advises large occupiers looking for modern

buildings to make pre-commitments to space,

especially in low-vacancy markets like Bengaluru,

Pune and Hyderabad.

> The Seoul office market appears to be an exception

to the general rule of strength. It is more favourable

to tenants than many others, with rent growth likely

to be marginal and vacancy to trend upwards over

the next few years.

Figure 2: Asia Pacific Office Rents Q1 2018

Source: Colliers International

$0 $20 $40 $60 $80 $100 $120

Hong Kong

London - City Core

Tokyo

NYC - Midtown

Beijing

Shanghai

NYC - Downtown

Singapore

Yangon

Seoul

Sydney

Shenzhen

Taipei

Ho Chi Minh City

Astana

Delhi NCR

Mumbai

Almaty

Guangzhou

Melbourne

Bangkok

Auckland

Hanoi

Jakarta

Karachi

Wellington

Brisbane

Perth

Canberra

Manila

Bengaluru

Adelaide

Chennai

USD / sq ft / year

Note: 1. Prime office rents refer to Grade A and/or more premium grade office space. Refers to net effective rent.2. Asia rental figures represent overall office rents of major sub-markets. ANZ figures represent overall figures in CBD

6 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Key market snapshots Q1 2018

Hong Kong

Singapore

Source: Colliers International

Source: Colliers International

7 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Shanghai

Bengaluru

Source: Colliers International

Source: Colliers International

8 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Seoul Office Q1:

Higher vacancy

due to YBD Despite sustained demand in the CBD and GBD due

to economic strength, overall Grade A vacancy in

Seoul increased due to new supply in the YBD.

Although serviced office providers are in expansion

mode, we expect the tenant-oriented market to

persist until 2020 due to new supply. Therefore,

occupiers should take advantage of the tenant-

oriented market conditions to negotiate new leases.

Forecast at a glance

Demand Leasing demand in the IT sector

should be sustained due to economic

strength. In addition, we think demand

for flexible workspace will grow.

Supply In the CBD, Centropolis Building (4%

of total surveyed stock in CBD) will be

completed in H2 2018. In the GBD,

Luchen Tower and Gangnam N

Tower will be completed in H2. These

will boost total stock in the GBD by

4%. Over the next three years, we

expect total new supply in prime

areas to exceed 1.3 million sq m (14.9

million sq ft).

Vacancy rate The overall Grade A vacancy rate will

continue to increase due to the LG

Group's relocation and new supply.

We expect vacancy to rise to a peak

of nearly 17.0% in 2020 due to heavy

new supply in YBD and, but to fall

back to 14.0% by end-2022.

Rent Face rent has increased due to

cyclically adjusted terms as some

buildings increased the rent level at

the start of 2018. We estimate a 2%

rent increase in Seoul this year linked

to the CPI. We expect rental growth

over the next few years to be

marginal, there could be an increase

of 2-3% per annum on average.

Leasing Market

Demand

Net absorption in the Seoul Grade A office market fell by

27,928 sq m (300,610 sq ft) in Q1 2018 QOQ due to the

YBD market. CBD and GBD increased by 10,913 sq m

(117,464 sq ft) and 8,300 sq m (89,340 sq ft),

respectively, while the YBD fell by 47,140 sq m.

(507,415 sq ft).

Certain companies are actively upgrading and signing

new lease contracts as they expand their business due

to economic strength. The CBD area's Seoul City Tower

resolved 514 sq m (5,530 sq ft) of vacancy after

completing lease expansion contracts with BNP Paribas

and NH Insurance. In addition, Shinhan Life Insurance

and Shinhan Data system took up about 1,300 sq m

(13,995 sq ft) of office space in Shinhan L Tower. Oil

Hub Korea leased 2,023 sq m (21,775 sq ft) in the Seoul

Square building, moving from the B Grade Building

where it was previously resident.

There is strong demand from growth sectors in the IT

industry. Tera Fintech, the local crowd-funding company,

leased 1,523 sq m (16,395sq ft) in the SI Tower, to

relocate headquarters. South Korea’s cryptocurrency

exchange, Bithumb, leased 2,878 sq m (30,980 sq ft) in

the KT&G Dachie Tower to expand its call centre in the

GBD area. Meanwhile, Amazon Korea leased 2,768 sq

m (29,795 sq ft) in the Pine Avenue A building to open a

new call centre in the CBD area.

Supply

The Korean Teachers Credit Union (KTCU) building, with

83,381 sq m (897,505 sq ft) of gross floor area, was

finished in Q1 2018. About 40% of KTCU is dedicated to

self-use and the other 60% is leased to KB Securities.

Fig. 3: Seoul Office Market: Demand and Supply

Source: Colliers International Korea.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

(50)

-

50

100

150

200

GLA

('000 s

qm

)

New Supply Net Absorption Vacancy

9 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Vacancy Rate and Rent

The average vacancy rate in the CBD stood at 11.3% at

end-Q1, a slight decrease from end-2017. The expected

relocation from the CBD to other areas of companies

including Daewoo Construction and public institutions

will push up the CBD’s vacancy rate in H2 2018. We

predict 15.0% for end-2018.

The GBD vacancy rate fell by 0.3 percentage points to

6.0%, thanks to the limited supply and increased

demand in the IT industry.

The YBD vacancy rate increased by 8.3 percentage

points to 22.3% due to vacant storeys in the newly

completed KTCU and the relocations of some

companies out of the YBD. As LG CNS relocated to LG

Science Park in Magok, FKI Tower's vacant area was

added to the YBD market. In addition, the relocation of

KTCU created backfill space in 63 Building after KTCU

moved out.

The average asking rent of overall Grade A offices

increased to KRW27,182 (USD25.2) per sq m per

month, a 2% increase from Q4 2017 as most office

buildings adjusted their rates similar to the CPI level at

the start of 2018.

Fig. 4: Seoul Office: Grade A Rent and Vacancy

Source: Colliers International Korea

Figure 5: Q1 2018 Vacancy and Rent Level

Source: Colliers International Korea

Outlook

The economic indices of South Korea are showing

hopeful signs of strength. Although demand for Grade A

office space in Seoul is recovering, the upward trend in

vacancy rates in the market is likely to continue due to

the emergence of backfill spaces by new supply.

In the CBD area, Summit Tower and Seosomun Building

(6% of total surveyed stock in the CBD) are due to be

completed in 2019. If Daewoo E&C, which is developer

of the building, relocates to Summit Tower, the Daewoo

E&C headquarter will become available. Thus, the rise in

the CBD vacancy rate should continue in 2019.

Meanwhile, the expected new supply will be quickly filled

due to the limited prime office supply and increasing

flexible workspace tenants in the GBD.

In the YBD area, the Parc 1, with 336,610 sq m.

(897,505 sq ft) of gross floor area, will enter the market

in 2020. The KB Finance’s headquarters building and the

Korea Post office building are also expected to be

completed in 2020. Moreover, the Private School

Pension Building is expected to start its re-construction

in 2018 with completion slated in 2022. Although some

areas of new completions will likely be owner-occupied,

the relocation of headquarters from existing buildings to

new supply will create some backfill space. Currently,

market conditions favour tenants, and we assume that

this will remain the case until 2020.

Figure 6: Seoul Office Market: Supply Forecasts

Source: Colliers International Korea

0%

5%

10%

15%

20%

0

5,000

10,000

15,000

20,000

25,000

30,000

Vacancy

Rate

(%

)

Rent

(KR

W/s

q.m

./m

o)

Overall Rent Vacancy Rate (%) 0

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

000

sqm

CBD GBD YBD Others

SUBMARKET VACANCY (%) RENT(KRW/SQM/MO)

CBD 11.3% 31,328

GBD 5.95% 26,800

YBD 22.3% 23,416

OVERALL 11.8% 27,182

10 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Asian Investment

Market Trends

Market conditions remain firm in Q1

> Property investment in Asia maintained the strength

of recent years and hit the highest Q1 level since

2007 in Q1 2018, with completed property

transactions reaching USD37.4bn, up by 24% YOY.

> Hong Kong and Tokyo were the most active cities,

recording transactions of completed properties worth

USD7.9bn (+88% YoY) and USD6.9bn (+49% YoY)

in Q1 2018, respectively.

> Looking ahead, we expect the investment market in

India (+53% YOY) to continue maturing, while Japan

should recover further from dull volumes in 2017.

> Valuations of most categories of investment property

look rich, with yield spreads over ten-year bonds for

prime-grade office property mostly in a range of 0-2

percentage points. However, according to our

Valuations team's latest Asia Cap Rates report1

capitalisation rates in Asia are mostly either stable or

still declining.

> We therefore now assume around 10% growth in

transaction volumes for completed properties in

2018. The chief risk to this view is not weak demand

or availability of capital, but potential lack of high-

quality properties available for sale.

1 Valuation & Advisory Services | Asia "Asia Cap Rates" Q1 18

Figure 8: Investment Property Transactions in Asia

Source: Real Capital Analytics (as of 15 May 2018) for closed deals of

properties over USD10 million, excluding land development sites

0

20

40

60

80

100

120

140

US

$ b

illio

ns

Figure 7: Summary of Asia Prime Grade office market

City Rental growth City vacancy City vacancy

Net income yld*

10 yr govt. Spread

(2017-21 avg pa) (Q1 2018) (2021E) (Q1 2018) bond yield

Seoul 3.3% 11.8% 14.7% 4.3% 2.7% 1.6pp

Hong Kong 2.1% 5.1% 5.0% 2.4% 2.2% 0.2pp

Singapore 4.1% 5.8% 6.4% 3.6% 2.6% 1.0pp

Shanghai 0.5% 13.6% 12.7% 3.6% 3.6% 0.0pp

Beijing -0.3% 8.7% 14.7% 4.0% 3.6% 0.4pp

Shenzhen 1.1% 11.1% 20.4% 3.9% 3.6% 0.3pp

Taipei 0.6% 12.9% 5.9% 2.8% 0.9% 1.9pp

Bangalore 4.9% 9.1% 7.0% 8.0-8.5% 7.9% 0.1-0.6pp

Note. This table is repeated from Figure 1 above. Source: Colliers International Research, Bloomberg

11 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Korean market strong in Q1 2018

According to RCA, total property transaction volumes for

South Korea increased by 58% YOY in Q1 2018, to

USD4.4 billion. This represents a significantly stronger

outcome than over 2017 as a whole, for which the

increase was just 7% (to USD14.3 billion). RCA notes

that domestic capital was the driving force behind the

high deal volumes in South Korea in the period.

It is noteworthy that Seoul accounted for over 80% of

total transactions in South Korea: deals in the capital

more than doubled YOY in Q1 2018, to USD3.6 billion.

Accordingly, Seoul ranked as the no.3 urban investment

market in Asia in Q1 after Hong Kong and Tokyo.

Seoul yields above Asian averages

Above-average property yields make Seoul attractive as

a near-term investment target. As shown in Figure 6,

Grade A office property in Seoul offers a net yield of

4.3%, compared to no higher than 4.0% for most other

leading Asian cities except Bangalore, and as low as

2.4% for Hong Kong. Moreover, Seoul office property

offers a spread over ten-year government bonds of 1.5

percentage points, versus very narrow spreads for Hong

Kong and Tier 1 Chinese cities.

Looking at other categories of investment property, retail

property in Seoul yields 4.0-5.0%, compared to 2.3-2.5%

in Hong Kong but a similar range of 4.2-5.0% in

Singapore. Logistics property around Seoul yields 6.0-

7.0%, far above Hong Kong on 3.5-3.7% and above

most leading Chinese cities in a range of 5.0-6.7%.

Figure 8: Asia property transaction volumes by country in Q1 2018 (USD, YOY)

Investment Property Transactions in Asian Countries

US$ million Q1 2017 Q1 2018 YoY

Japan 11,715 13,148 12%

China 7,415 9,222 24%

Hong Kong 4,195 7,877 88%

South Korea 2,783 4,404 58%

Singapore 1,587 995 -37%

Taiwan 500 515 3%

India 289 441 53%

Malaysia 369 107 -71%

Thailand 618 33 -95%

Vietnam 78 17 -78%

Note. These totals exclude undeveloped land. Source: RCA as of 8 May 2017; calculations by Colliers

Figure 9: Asia property transaction volumes by urban centre in Q1 2018 (USD, YOY)

Investment Property Transactions in Asian Cities

US$ million Q1 2017 Q1 2018 YoY

Hong Kong 4,195 7,877 88%

Tokyo 4,594 6,864 49%

Seoul 1,793 3,613 102%

Shanghai 4,436 1,065 -76%

Nagoya 196 1,006 413%

Singapore 1,587 995 -37%

Guangzhou 179 958 435%

Beijing 917 675 -26%

Yokohama 1,453 566 -61%

Fukuoka 172 291 69%

Note. These totals exclude undeveloped land. Source: RCA as of 8 May 2017; calculations by Colliers

12 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

In our opinion, high transaction volumes in Seoul partly

reflect interest in the market from foreign institutional

investors looking to diversify their portfolios who perceive

South Korea as a relatively stable market providing solid

investment yields. As noted, Grade A office property in

Seoul offers a net yield 1.6 percentage points above ten-

year government bonds, and 1.8 percentage points

above the five-year government bonds (currently yielding

2.5%) which some Korean investment institutions seem

to use as a benchmark. Investment property in Seoul

therefore offers good value to both foreign and domestic

institutions.

We see little chance that capital values will decline in the

near term, with the result that property that offers good

value now offers significantly better value in a few

months' time. The key reason for this is that the pace of

monetary tightening in South Korea looks set to be very

gradual. The Bank of Korea tightened interest rates for

the first time in six years in November 2017, when it

raised the seven-day repurchase rate from 1.25% to

1.5%. However, not only is the outlook for inflation

benign, but also the government seems likely to retain

an accommodative bias in fiscal policy as President

Moon pushes ahead with a domestic agenda of job

creation and increased welfare provision.

Oxford Economics predicts that the short-term nominal

interest rate will rise gradually to 3.5% by end-2021.

Between Q2 2018 and Q4 2021, it predicts that CPI

inflation will only increase from 1.7% to 2.0%2. On the

basis of these forecasts, real (i.e. inflation-adjusted)

short-term interest rates, which stand at about zero now,

will stay below about 1% until end-2020. Persistent low

real interest rates should support capital values and

investment activity in the property market.

Long-run prospects less attractive

The attractions of relatively high yields in Seoul are

offset by lower long-run economic growth and poorer

demographic prospects than for many other Asian cities.

While the South Korean economy is performing well right

now, for the country as a whole Oxford Economics

projects average real GDP growth over 2017-2021 at

2.7%, and over 2022-2026 at 2.3%. Such growth rates

are well below those of developing markets such as

India, Indonesia and, indeed, China, for which Oxford

Economics predicts average real GDP growth over

2017-2021 of 6.1%, and over 2022-2026 of 4.9%.

The contrast in terms of economic growth is most

evident at the city level. Figure 9 below compares real

2 Please see "Country Economic Forecast, South Korea" by Oxford

Economics (9 May 2018).

GDP growth rates over the next five years for major Asia

Pacific investment centres. Bangalore is at the top, and

Seoul is second from last. Seoul does outperform Tokyo,

a city with which comparisons are obvious.

Figure 9: Real GDP growth (%), 2018-2022

Source: Oxford Economics. HK = Hong Kong, SG = Singapore, BG =

Bangalore

Incidentally, it should be clear from Figure 9 that Seoul

will only be growing at about 1.5-2.5% over the next five

years, compared to Oxford Economics' forecast for

average real GDP growth for South Korea as a whole

over 2017-2021 of 2.7%. The reason why Seoul is

underperforming the national average is that South

Korea has a strong competitive advantage in advanced

manufacturing, but is less strong in services, and the

economy of Seoul is mostly services-based.

In addition, weaker long-run economic growth prospects

for Seoul partly reflect a weak demographic profile. The

population of Seoul is currently shrinking, although

Oxford Economics expects the rate of decline to

moderate over the next few years.

Fig. 10: Average population growth, 2018-2022

Source: Oxford Economics. HK = Hong Kong, SG = Singapore, BG =

Bangalore

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2018 2019 2020 2021 2022

Seoul HK SG ShanghaiBeijing Shenzhen Taipei BGSydney Tokyo

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

13 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Rapprochement between the two Koreas a positive surprise

An important positive surprise for investors in the Seoul

property market has come from the recent easing of

tensions between North Korea and South Korea.

Investors in financial assets in South Korea – whether

equities, bonds or property – have lived within the

possibility of conflict on the peninsula ever since the

Korean War ended with an armistice in 1953.

The summit held in late April 2018 in Panmunjom

between President Moon Jae-in of South Korea and

Chairman Kim Jong-un of North Korea marked the first

time that a North Korean leader had entered the South

since the end of the war. Immediately after this summit,

optimism increased about the scope for broader

reconciliation between the two Koreas, and perhaps

eventual reunification. The fact that President Donald

Trump of the US and President Xi Xinping of China had

made a significant contribution to the peace process was

perceived as another factor encouraging factor.

Optimism has increased further following the summit

held in Singapore on 12 June between US President

Trump and North Korea's Chairman Kim. In the wake of

the decision by the US in early May to withdraw from an

international nuclear agreement with Iran, we had

become sceptical about prospects for a further major

diplomatic breakthrough on the Korean peninsula. In the

event, we were too cautious. One could argue that the

Singapore summit resulted only in a commitment on

North Korea's part to the denuclearisation of the Korean

peninsula. Nevertheless, this is a major step forward;

and it is encouraging that the US and North Korea are

talking and negotiating with each other.

Overall, the degree of rapprochement between North

Korea on the one hand and South Korea and the US on

the other so far in 2018 has positively surprised most

international observers. It seems reasonable to hope for

continued progress towards reconciliation between the

two Koreas. Such progress should reduce concern

among foreign investors and property occupiers about

exposure to Seoul – a city which lies only about 55

kilometres from the border with North Korea.

If the perception spreads that the risk of conflict on the

Korean peninsula has permanently diminished, the

consequence might be the removal of the "risk premium"

traditionally applied to South Korean financial assets.

While capitalisation rates for Seoul office property have

been declining steadily ever since the Global Financial

Crisis of 2007-2008 to the present 4-5% range, we have

observed that they remain higher than in much of the

rest of Asia. For property investors, removal of the risk

premium might imply a permanent reduction in perceived

appropriate cap rates and a consequent increase in

capital values.

Implications of reconciliation

Interest in real estate investment in the Paju and

Yeoncheon districts, which border on Panmunjeon

where the Moon-Kim summit took place, continues to

increase. We expect that the rise of property prices in

some areas, especially in the northern part of Gyeonggi

Province, will affect the overall real estate market in

Seoul. The investment demand of liquid funds that has

been focused up to now on the housing market in central

Seoul will probably extend to other places such as the

land market skirting around Seoul. During his election

campaign, President Moon made a pledge to link Paju,

Kaesong, and Haeju into a unified economic zone. The

special economic zone of Tongil specialises in

developing border areas such as industrial complexes

and multiple cities by linking Paju, Gaeseong, and Haeju.

If the development of the Special Economic Zone comes

to fruition, real estate investors' attention will be

concentrated on the Gyeonggi region.

Looking further ahead, it is reasonable to expect political

reconciliation to contribute to a modest acceleration of

economic growth in South Korea compared to existing

estimates, to an improvement in consumer sentiment,

and to further growth in tourist arrivals. All these factors

ought to support the property market in Seoul and South

Korea in general.

It is probably too early to speculate about the

implications of eventual Korean reunification for the

Seoul property market. However, it may be instructive to

compare Seoul with Berlin. After the reunification of

Germany in 1990, it took 15-20 years for Berlin to

develop into a major international city attracting investors

and multinational corporate occupiers from around the

world. For investors in Seoul commercial property, that

may suggest a long wait ahead. However, at least the

start of the road now appears to be in sight.

14 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Seoul Investment

Q1: Still Active Based on Colliers' figures for nine major office

buildings, total transaction volume in Seoul in Q1

2018 stood at KRW2.4 trillion (USD2.3 billion).

Looking ahead, we expect that total market

transaction size for 2018 will exceed KRW7.0 trillion

(USD7.0 billion) as many properties will be put up for

sale. We expect the Seoul office investment market

to continue to thrive for as long as the real interest

rate stays low.

Forecast at a glance

Demand

Actual 2017 aggregate transaction

size was about KRW7.0 trillion

(USD7.0 billion). If expected sales are

completed successfully, the office

transaction volume in 2018 will equal

or exceed the total transacted volume

in 2017.

Foreign Investors

Foreign investors’ inbound investment

led Seoul office deals in 2016, with

44% coming from foreign investors. In

2017, total office transaction volume

stood at KRW7.0 trillion (USD7.0

billion), of which total only15% came

from foreign investors. For investment

portfolio diversification, we expect

foreign investors to expand their

investment in Korea again.

Price

The average sales value rose in Q1,

thanks to prime building transactions

like the K-Twin Tower, representing

the highest unit price transacted for

buildings sold in Seoul. We expect the

sale price of Grade A buildings to stay

broadly stable until 2020, reflecting

low real interest rates but competitive

conditions in the occupier market.

While investors' appetite for office

buildings is high, vacancy remains a

critical issue, and we expect funding

to stay challenging for buildings with

high vacancy rates.

Capital Markets: transactions active

In Q1 2018, the K-Twin Tower (83,878 sq m by GFA),

previously owned by KKR and LIM, was purchased by

Samsung SRA Asset Management for KRW714 billion

(USD664 million), implying a unit price of KRW28 million

per pyeong (USD7,926 per sq m). The sale of this

property broke the record for unit prices in Seoul.

Investors are now increasing their focus on major

investment areas such as Pangyo, which currently

enjoys a low vacancy rate. Pangyo has emerged as a

viable alternative office location. Mirae Asset

Management has acquired the ALPHADOM 6-3 Tower

from Hana Asset Management for KRW460 billion

(USD429 million). In addition, LH plans to sell the

ALPHADOM 6-4 Tower, located near the ALPHADOM 6-

3 Tower, to a public REITs Elsewhere, East Central

Tower, which is located in the Gangdong area, was

purchased by Millinium Inmark Asset for KRW340 billion

(USD316 million).

Value-added strategies are increasingly being adopted in

the Seoul investment property market. Pebble Stone

Asset Management has purchased the Hana Card HQ

building for KRW73 billion (USD61 million). As Hana

Card is moving out, the Hana Card HQ building remains

vacant. However, Pebble Stone was able to close trhe

deal successfully by implementing a value-added

strategy. A consortium of Mastern Investment

Management and Angelo Gordon purchased KB Bank

Myeongdong HQ building for KRW241 billion (USD 202

million). The investors plan to redevelop the property into

a retail and hotel site.

Looking ahead, many Grade A buildings, including the

Centropolis building, the Samsung C&T Corporation's

headquarters, and KDB Life insurance Tower are due to

be put on the market. In addition, major conglomerates

like Samsung Group continue to put up their real estate

holdings for sale. Despite concerns over high vacancy

rates, institutional investors appear to be investing

actively in alternative assets due to the environment of

prolonged low interest rates. The majority of domestic

investors still prefer stable assets that guarantee long-

term tenants. Unlike domestic investors, foreign

investors are taking a long-term perspective even

regarding high vacancy rates. Foreign investors with

ample operating experience are buying buildings with a

vacancy rate of 50% or more, attracting tenants, and

pursuing strategies to return the assets to domestic

institutional investors. Thus, foreign investors are

increasing their exposure to property holdings for their

investment portfolio diversification in Korea. We have

seen that there is also increasing interest among

investors in value-add investment strategies, and we

expect this interest to persist.

15 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Asian Flexible

Workspace

Trends "Flexible workspace is no longer a disruptor, nor a

complementary sub-sector to the office market. It is a

fundamental part of the commercial real estate market

and a sector in its own right, growing in size and

importance to landlords and occupiers. The average

flexible workspace leasing term is now over 24 months,

up from 12 months in 2013, demonstrating that it is now

competition to traditional office space.

We have seen continued growth in the sector…. This

growth has been fuelled by the thirst for flexibility from

multinational corporations, evidenced by the percentage

of deals for 15 desks or more increasing to 48% in 2017

from 32% in 2016, which in turn was up from 12% in

2014." From "The Flexible Workspace Outlook Report 2018 (APAC)"

(March 2018), by Colliers International

The flexible workspace market in Asia has become far

more sophisticated, and now spans a wide range of

products lying between coworking and traditional

serviced offices. Since flexible workspace is a low-

margin business with low barriers to entry, flexible

workspace operators need to continue to enhance their

offerings. There has been a movement away from banks

of cellular offices to larger, more customised spaces.

Increased sophistication is driving increased popularity.

The flexible workspace market therefore continues to

expand across Asia. In the CBDs of most major cities,

flexible workspace still accounts for less than about 5%

of occupied prime grade office space; exceptions include

Bangalore and Chengdu, on 11% and 9% respectively.

However, flexible workspace operators have become an

important source of demand for new leased space. In

Shanghai, for example, flexible workspace operators

presently account for 4% of aggregate Grade A office

space, but for about 8% of new take-up of leased space.

Tenant mix, Shanghai Grade A office (end-2017)

Source: Colliers International

Tenant mix of new take-up Shanghai Grade A office (2017)

Source: Colliers International

Finance, 42%

Professional Service, 16%

TMT, 9%

Flexible workspace,

4%

Manufacturing, 8%

Medical & Health, 5%

Trading, 8%

Fashion, 3%FMCG, 2%Others, 3%

Finance, 35%

Professional Service, 21%

TMT, 12%

Flexible workspace,

8%

Manufacturing, 7%

Medical & Health, 5%

Trading, 4%

Fashion, 2%FMCG, 2% Others, 5%

Flexible Workspace in Asia: Market Indicators

Source: Colliers International

16 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

Flexible workspace

impacts the Seoul

office market The expansion of the flexible workspace has an

influence not only on the office leasing market but also

on the transaction market. In a market favouring tenants,

landlords use the flexible office operators as a new tool

to lower vacancy rates. Flexible workspace is also used

as a means to raise the value of buildings in order to

close sales successfully. In a market situation favouring

tenants, we expect that flexible workspace operators will

be able to earn higher profits with favourable lease

terms. However, if the area occupied by the flexible

workspace operator is large, depending on its strategy

the landlord may not benefit. The landlord will not be

able to change the term conditions due to the long-term

contract.

We expect demand for flexible workspace to continue to

expand. However, since both domestic companies and

major companies which own buildings are entering the

flexible workspace market together, competition between

domestic and overseas companies is likely to become

intense. Therefore, in order to be a win-win partner for a

flexible workspace operator and a landlord, it is

necessary to consider effective leasing strategies based

on market forecasts.

Flexible workspace business status

The expansion of the flexible workspace market has had

a major impact on the office leasing market and the

investment market in Seoul since WeWork, the global

flexible workspace operator, entered the domestic

market in 2016.

The leasing demand for large Grade A office-space was

stable due to major companies' increased demand for

headquarters relocation in 2014. However, the vacancy

rate has continued to rise since 2015 due to the

economic downturn and new office supply. The demand

for leased office space has been recovering over 2017

and 2018, with Gangnam as the centre of the flexible

workspace sector driven by WeWork since 2016. Due to

the rise of tech-related start-ups, which prefer cost-

effective office space, flexible workspace has emerged

as an alternative method to lower vacancy rates.

In particular, as of April 2018, WeWork has opened 10

branches in Seoul within two years of entering the

market. WeWork has had a significant impact on

lowering office vacancy rates by leasing ten or more

floors in major buildings with high vacancy rates. For

example, in the case of the HP building in the Yeoido

area, in which seven floors were vacant, WeWork leased

tall the vacant floors and reduced vacancy in the building

to zero.

Preference for flexible workspace has expanded beyond

Gangnam, a region which IT ventures or start-ups prefer,

and now to Gangbuk. Recently, WeWork leased eight

floors of Jongno Tower and plans to open its tenth

branch in September. This is because demand for start-

ups as well as domestic large companies is increasing.

Not only global but also domestic flexible workspace

operators are actively opening new branches. A

representative flexible workspace company in Korea is

FastFive, which was launched in March 2015. As of

November 2017, it operates 12 branches and recently

opened a Hongdae branch.

In addition, large companies are entering the shared

office market to decrease vacancy in their buildings and

to discover new business opportunities. In fact, Hanwha

Life recently opened a 'Dream Plus Gangnam' shared

office of 15 stories in the Hanwha Life Seocho Building.

In addition, the Hyundai Card has a 'Studio black' and

A-ju group operates ‘Spacrap’.

Present state of WeWork in Seoul

Building Submarket Area (SQM) Open date

Hongwoo GBD 6,500 Aug. 2016

Dashin Security CBD 20,000 Feb. 2017

Ilsong Building GBD 13,080 Aug. 2017

Arc Place GBD 5,801 Dec. 2017

K-Twin Tower CBD 6,930 Mar. 2018

HP Building YBD 12,356 April. 2018

Seoul Square CBD 17,852 May. 2018

Daese Building GBD 9,205 June. 2018

PCA Life Tower GBD 11,918 July. 2018

Jongro Tower CBD 12,742 Sep. 2018

Total Operating 10 locations

Source: Colliers International

Transaction market impact

Flexible workspace also has a significant impact on the

successful closure of commercial real estate

transactions. Flexible workspace operations can involve

the leasing of large areas of office space for long

periods, and so can increase the value of buildings by

17 Not Without Its Charms | 19 June 2018 | Seoul | Property | Colliers International

lowering vacancy. In fact, KTB Asset Management was

recently able to close the Ilsong Building (WeWork

Building) acquisition by securing WeWork as a key

tenant and attracted investors in a timely manner when

Seoul’s office vacancy rate is high.

In addition, the K-Twin Tower was the first Korean

commercial real estate that Kohlberg Kravis Roberts

(KKR) invested in, and has recorded the highest unit

price at KRW310 billion (USD289 million) so far in 2018,

purchased by Samsung SRA Asset Management.

Although the building was vacant when the KTCU first

invested, it was able to close the deal successfully by

effectively managing the vacancy rate by leasing to

Microsoft and WeWork. Meanwhile, NC Tower 2 was

able to complete a successful sale of Igis Asset

Management, as Fast Five leased the vacant space

where Cupang had moved out.

The asset manager uses the flexible workspace as a

marketing point to attract institutional investors. In fact,

most of the 10 branches which WeWork has leased are

owned by asset management companies. Arc Place is

owned by Blackstone. Seoul Square and Jongno Tower

are owned by Alpha Investment. In addition, HP Building

is owned by CBRE Global Investor Asset Management

and is put on the market.

Looking ahead, we expect flexible workspace to continue

to have an impact on office leasing and investment

markets, as high growth continues. Flexible workspace

companies are taking advantage of the current market

situation, which is favourable to tenants. In order to

attract flexible workspace operators, the building owners

offer various benefits such as rent-free periods, interior

subsidy support and rent reduction. In addition, there is

an increasing number of buildings that change the

signboard of the building to the name of the flexible

workspace operator. The reason why the landlord

changes the image of the building and leases the office

is that the vacancy rate in the Seoul office is getting

higher and use of flexible workspace helps solve the

vacancy rate in a short time.

However, for a building investor, a single anchor tenant

can be a risk. In particular, if the lease adjustment is not

flexible when the building is sold, the yield may

decrease. In addition, real estate funds must secure a

fixed cash flow for regular dividends. Leasing the same

area to several tenants may result in a more stable cash

rental income stream.

In addition, as the expansion of the domestic flexible

workspace as well as the global flexible workspace

market is accelerating, competition among the flexible

space operators will become more intense, and there is

a possibility that some flexible workspaces may be shut

down and that a single tenant may leave the building.

The departure of a single tenant can cause a bigger loss

to a landlord than the departure of multiple small tenants,

if early tenant benefits are irrecoverable.

Therefore, the building owners need to analyse the

market prospects, and negotiate lease terms when

dealing with flexible workspace operators based on long-

term strategies, and monitor the creditworthiness and

growth potential of the flexible workspaces.

Copyright © 2018 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

413 offices in

69 countries on

6 continents United States: 145

Canada: 28

Latin America: 23

Asia Pacific: 86

EMEA: 131

$2.7 billion in annual revenue

2 billion square feet under management

15,400 professionals and staff

Primary Authors:

Judy Jang

Associate Director | Research | Korea

+82 2 6325 1900

Judy.Jang @colliers.com

Regional Authors:

Andrew Haskins

Executive Director | Research | Asia

+852 2 2822 0511

Andrew.Haskins @colliers.com

Colliers International | <Korea>

14F, S Tower, 82, Saemunan-ro

Jongno-gu,Seoul 03185| Korea

+ 82 2 6325 1900

About Colliers International Group Inc.

Colliers International Group Inc. (NASDAQ & TSX: CIGI) is an industry-leading real estate services

company with a global brand operating in 69 countries and a workforce of more than 12,000 skilled

professionals serving clients in the world’s most important markets. Colliers is the fastest-growing

publicly listed global real estate services company, with 2017 corporate revenues of $2.3 billion ($2.7

billion including affiliates). With an enterprising culture and significant employee ownership and

control, Colliers professionals provide a full range of services to real estate occupiers, owners and

investors worldwide. Services include strategic advice and execution for property sales, leasing and

finance; global corporate solutions; property, facility and project management; workplace solutions;

appraisal, valuation and tax consulting; customized research; and thought leadership consulting.

Colliers professionals think differently, share great ideas and offer thoughtful and innovative advice

that help clients accelerate their success. Colliers has been ranked among the top 100 global

outsourcing firms by the International Association of Outsourcing Professionals for 13 consecutive

years, more than any other real estate services firm. Colliers has also been ranked the number one

property manager in the world by Commercial Property Executive for two years in a row.

For the latest news from Colliers, visit Colliers.com or follow us on Twitter: @Colliers and LinkedIn.