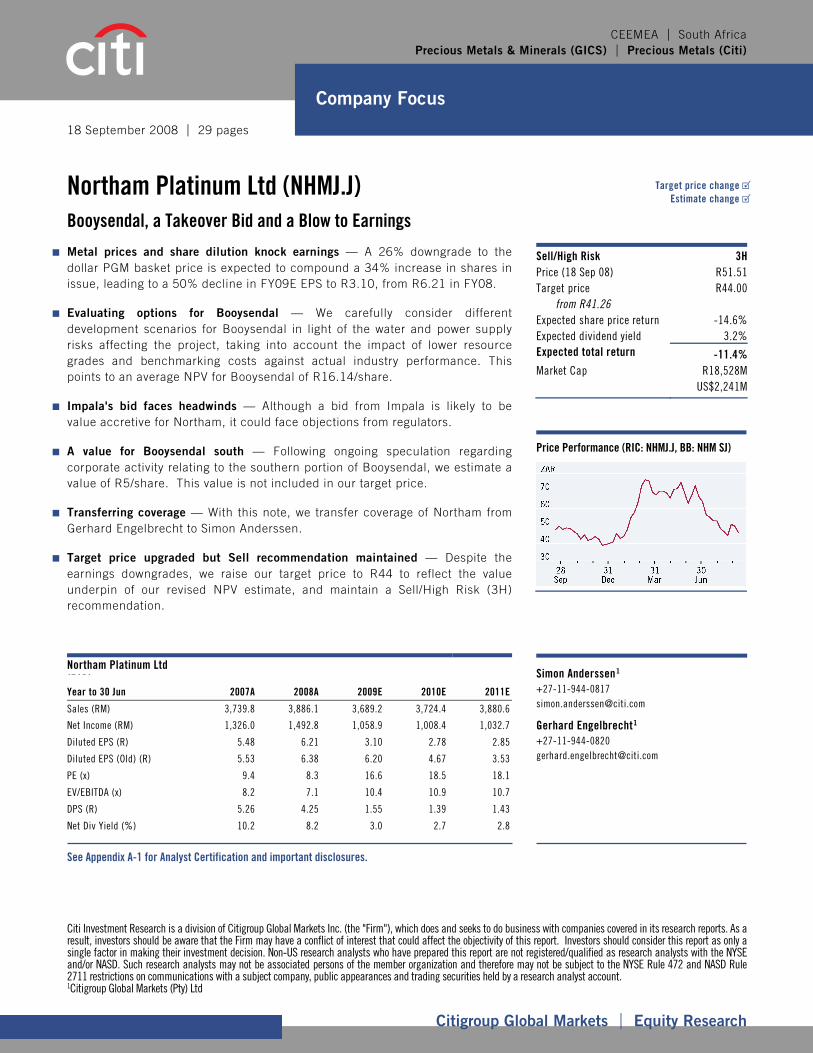

Northam Platinum Ltd (NHMJ.J) - Marble Arch Research · Risk (3H) recommendation on Northam. This...

29

Citi Investment Research is a division of Citigroup Global Markets Inc. (the "Firm"), which does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Non-US research analysts who have prepared this report are not registered/qualified as research analysts with the NYSE and/or NASD. Such research analysts may not be associated persons of the member organization and therefore may not be subject to the NYSE Rule 472 and NASD Rule 2711 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. 1 Citigroup Global Markets (Pty) Ltd Citigroup Global Markets Equity Research CEEMEA South Africa Precious Metals & Minerals (GICS) Precious Metals (Citi) Company Focus 18 September 2008 29 pages Northam Platinum Ltd (NHMJ.J) Booysendal, a Takeover Bid and a Blow to Earnings Metal prices and share dilution knock earnings — A 26% downgrade to the dollar PGM basket price is expected to compound a 34% increase in shares in issue, leading to a 50% decline in FY09E EPS to R3.10, from R6.21 in FY08. Evaluating options for Booysendal — We carefully consider different development scenarios for Booysendal in light of the water and power supply risks affecting the project, taking into account the impact of lower resource grades and benchmarking costs against actual industry performance. This points to an average NPV for Booysendal of R16.14/share. Impala's bid faces headwinds — Although a bid from Impala is likely to be value accretive for Northam, it could face objections from regulators. A value for Booysendal south — Following ongoing speculation regarding corporate activity relating to the southern portion of Booysendal, we estimate a value of R5/share. This value is not included in our target price. Transferring coverage — With this note, we transfer coverage of Northam from Gerhard Engelbrecht to Simon Anderssen. Target price upgraded but Sell recommendation maintained — Despite the earnings downgrades, we raise our target price to R44 to reflect the value underpin of our revised NPV estimate, and maintain a Sell/High Risk (3H) recommendation. Northam Platinum Ltd (ZAR) Year to 30 Jun 2007A 2008A 2009E 2010E 2011E Sales (RM) 3,739.8 3,886.1 3,689.2 3,724.4 3,880.6 Net Income (RM) 1,326.0 1,492.8 1,058.9 1,008.4 1,032.7 Diluted EPS (R) 5.48 6.21 3.10 2.78 2.85 Diluted EPS (Old) (R) 5.53 6.38 6.20 4.67 3.53 PE (x) 9.4 8.3 16.6 18.5 18.1 EV/EBITDA (x) 8.2 7.1 10.4 10.9 10.7 DPS (R) 5.26 4.25 1.55 1.39 1.43 Net Div Yield (%) 10.2 8.2 3.0 2.7 2.8 Sell/High Risk 3H Price (18 Sep 08) R51.51 Target price R44.00 from R41.26 Expected share price return -14.6% Expected dividend yield 3.2% Expected total return -11.4% Market Cap R18,528M US$2,241M Price Performance (RIC: NHMJ.J, BB: NHM SJ) See Appendix A-1 for Analyst Certification and important disclosures. Simon Anderssen 1 +27-11-944-0817 [email protected] Gerhard Engelbrecht 1 +27-11-944-0820 [email protected] Target price change Estimate change

Transcript of Northam Platinum Ltd (NHMJ.J) - Marble Arch Research · Risk (3H) recommendation on Northam. This...

Citi Investment Research is a division of Citigroup Global Markets Inc. (the "Firm"), which does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Non-US research analysts who have prepared this report are not registered/qualified as research analysts with the NYSE and/or NASD. Such research analysts may not be associated persons of the member organization and therefore may not be subject to the NYSE Rule 472 and NASD Rule 2711 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. 1Citigroup Global Markets (Pty) Ltd

Citigroup Global Markets Equity Research

CEEMEA South Africa Precious Metals & Minerals (GICS) Precious Metals (Citi)

Company Focus

18 September 2008 29 pages

Northam Platinum Ltd (NHMJ.J) Booysendal, a Takeover Bid and a Blow to Earnings

Metal prices and share dilution knock earnings — A 26% downgrade to the dollar PGM basket price is expected to compound a 34% increase in shares in issue, leading to a 50% decline in FY09E EPS to R3.10, from R6.21 in FY08.

Evaluating options for Booysendal — We carefully consider different development scenarios for Booysendal in light of the water and power supply risks affecting the project, taking into account the impact of lower resource grades and benchmarking costs against actual industry performance. This points to an average NPV for Booysendal of R16.14/share.

Impala's bid faces headwinds — Although a bid from Impala is likely to be value accretive for Northam, it could face objections from regulators.

A value for Booysendal south — Following ongoing speculation regarding corporate activity relating to the southern portion of Booysendal, we estimate a value of R5/share. This value is not included in our target price.

Transferring coverage — With this note, we transfer coverage of Northam from Gerhard Engelbrecht to Simon Anderssen.

Target price upgraded but Sell recommendation maintained — Despite the earnings downgrades, we raise our target price to R44 to reflect the value underpin of our revised NPV estimate, and maintain a Sell/High Risk (3H) recommendation.

Northam Platinum Ltd (ZAR)

Year to 30 Jun 2007A 2008A 2009E 2010E 2011E

Sales (RM) 3,739.8 3,886.1 3,689.2 3,724.4 3,880.6

Net Income (RM) 1,326.0 1,492.8 1,058.9 1,008.4 1,032.7

Diluted EPS (R) 5.48 6.21 3.10 2.78 2.85

Diluted EPS (Old) (R) 5.53 6.38 6.20 4.67 3.53

PE (x) 9.4 8.3 16.6 18.5 18.1

EV/EBITDA (x) 8.2 7.1 10.4 10.9 10.7

DPS (R) 5.26 4.25 1.55 1.39 1.43

Net Div Yield (%) 10.2 8.2 3.0 2.7 2.8

Sell/High Risk 3HPrice (18 Sep 08) R51.51Target price R44.00

from R41.26 Expected share price return -14.6%Expected dividend yield 3.2%Expected total return -11.4%Market Cap R18,528M US$2,241M

Price Performance (RIC: NHMJ.J, BB: NHM SJ)

See Appendix A-1 for Analyst Certification and important disclosures.

Simon Anderssen1 +27-11-944-0817 [email protected]

Gerhard Engelbrecht1 +27-11-944-0820 [email protected]

Target price change Estimate change

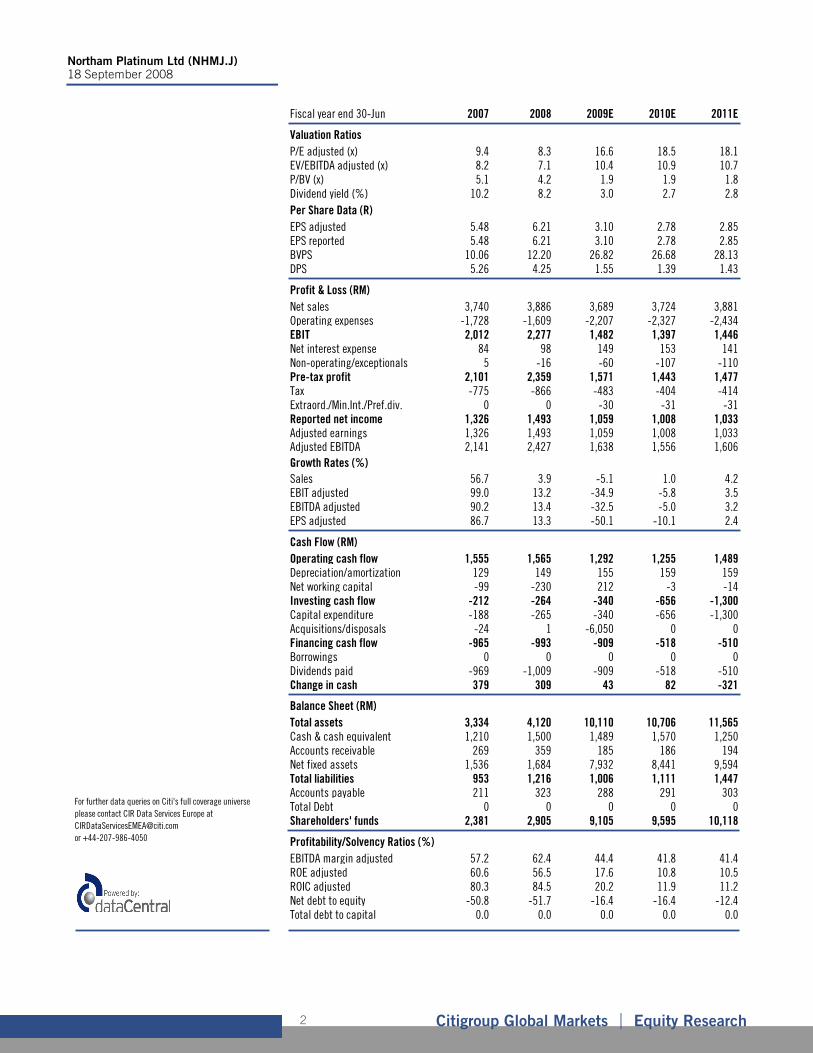

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 2

Fiscal year end 30-Jun 2007 2008 2009E 2010E 2011E

Valuation RatiosP/E adjusted (x) 9.4 8.3 16.6 18.5 18.1EV/EBITDA adjusted (x) 8.2 7.1 10.4 10.9 10.7P/BV (x) 5.1 4.2 1.9 1.9 1.8Dividend yield (%) 10.2 8.2 3.0 2.7 2.8Per Share Data (R)EPS adjusted 5.48 6.21 3.10 2.78 2.85EPS reported 5.48 6.21 3.10 2.78 2.85BVPS 10.06 12.20 26.82 26.68 28.13DPS 5.26 4.25 1.55 1.39 1.43

Profit & Loss (RM)Net sales 3,740 3,886 3,689 3,724 3,881Operating expenses -1,728 -1,609 -2,207 -2,327 -2,434EBIT 2,012 2,277 1,482 1,397 1,446Net interest expense 84 98 149 153 141Non-operating/exceptionals 5 -16 -60 -107 -110Pre-tax profit 2,101 2,359 1,571 1,443 1,477Tax -775 -866 -483 -404 -414Extraord./Min.Int./Pref.div. 0 0 -30 -31 -31Reported net income 1,326 1,493 1,059 1,008 1,033Adjusted earnings 1,326 1,493 1,059 1,008 1,033Adjusted EBITDA 2,141 2,427 1,638 1,556 1,606Growth Rates (%)Sales 56.7 3.9 -5.1 1.0 4.2EBIT adjusted 99.0 13.2 -34.9 -5.8 3.5EBITDA adjusted 90.2 13.4 -32.5 -5.0 3.2EPS adjusted 86.7 13.3 -50.1 -10.1 2.4

Cash Flow (RM)Operating cash flow 1,555 1,565 1,292 1,255 1,489Depreciation/amortization 129 149 155 159 159Net working capital -99 -230 212 -3 -14Investing cash flow -212 -264 -340 -656 -1,300Capital expenditure -188 -265 -340 -656 -1,300Acquisitions/disposals -24 1 -6,050 0 0Financing cash flow -965 -993 -909 -518 -510Borrowings 0 0 0 0 0Dividends paid -969 -1,009 -909 -518 -510Change in cash 379 309 43 82 -321

Balance Sheet (RM)Total assets 3,334 4,120 10,110 10,706 11,565Cash & cash equivalent 1,210 1,500 1,489 1,570 1,250Accounts receivable 269 359 185 186 194Net fixed assets 1,536 1,684 7,932 8,441 9,594Total liabilities 953 1,216 1,006 1,111 1,447Accounts payable 211 323 288 291 303Total Debt 0 0 0 0 0Shareholders' funds 2,381 2,905 9,105 9,595 10,118

Profitability/Solvency Ratios (%)EBITDA margin adjusted 57.2 62.4 44.4 41.8 41.4ROE adjusted 60.6 56.5 17.6 10.8 10.5ROIC adjusted 80.3 84.5 20.2 11.9 11.2Net debt to equity -50.8 -51.7 -16.4 -16.4 -12.4Total debt to capital 0.0 0.0 0.0 0.0 0.0

For further data queries on Citi's full coverage universe please contact CIR Data Services Europe at [email protected] or +44-207-986-4050

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 3

Evaluating Options for Booysendal 4 Impala’s bid for Mvela and Northam 4 Booysendal – 5

Degrading 6 Benchmarking Costs 7 Estimating NPVs 9 1 – Original 11 2 – Scaled-up 13 3 – Modular 15 Booysendal: What about the south? 16

Northam Mine 19 Earnings Forecasts 21 Valuation 24 Recommendation 25 Northam Platinum Ltd 26

Company description 26 Investment strategy 26 Valuation 26 Risks 26

Appendix A-1 27 Analyst Certification 27

Contents

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 4

This report evaluates, in detail, both Northam Mine and various options available to develop the company’s Booysendal project. We establish NPVs for these assets of R25.29/share and R16.14/share respectively, and an NPV for the company of R43.96. We set our target price at R44. In addition, we estimate corporate activity relating to the southern section of Booysendal could add a further R5/share to this value. We highlight that the 26% downgrade to the PGM basket price is expected to contribute to a 50% decline in EPS to R3.10 in FY09 and maintain a Sell/High Risk (3H) recommendation on Northam.

This report contains a detailed analysis of various development options for Booysendal, followed by a review of Northam Mine and the company’s financial position. However, we begin by addressing Impala’s pending bid for Northam and its parent Mvela Resources, and possible headwinds such an offer could face from regulators.

Impala’s bid for Mvela and Northam

On Friday 12 September, Impala Platinum, Mvela Resources (Mvela) and Northam Platinum issued cautionary announcements indicating that they were in discussions which could lead to Impala acquiring the entire share capital of Mvela and Northam. No further details were provided. Northam’s share price jumped 18.8% on the day, but has retracted slightly and currently trades at R51.51, a 12% premium to its closing level on Thursday 11 September.

Northam’s shares therefore trade at a premium to our target price (R44) and since an offer from Impala is likely to be at a premium to the current market price, a bid from Impala would probably be value accretive to Northam shareholders.

However, any transaction will need competition and DME approval and we anticipate the following factors will be relevant considerations:

Security of Anglo Platinum’s mining rights: Mvela Resources’ acquisition of Booysendal was subject to specific undertakings limiting changes to the company’s shareholder structure that could compromise Anglo Platinum’s security of tenure for its remaining mineral rights. It is unclear whether Anglo Platinum’s new order mining licences granted in April 2008, partly a result of the discounted sale of assets (including Booysendal) to HDP entities (including Mvela Resources), have been legally secured.

If Mvela were to breach any of its undertakings, it will be deemed to offer 50% of its Northam shares to Anglo Platinum at a 25-50% discount to their market value.

Competition and market concentration: Impala’s proposed acquisition would increase the concentration of control of PGM resources (and production) held by the industry’s three largest producers: Anglo Platinum, Impala and Lonmin. We estimate that the transaction would increase Impala’s control of PGM resources from 19% to 27% and the concentration of resource held by the three largest companies from 75% to 82%.

Evaluating Options for Booysendal

Mvela holds 62.8% of Northam

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 5

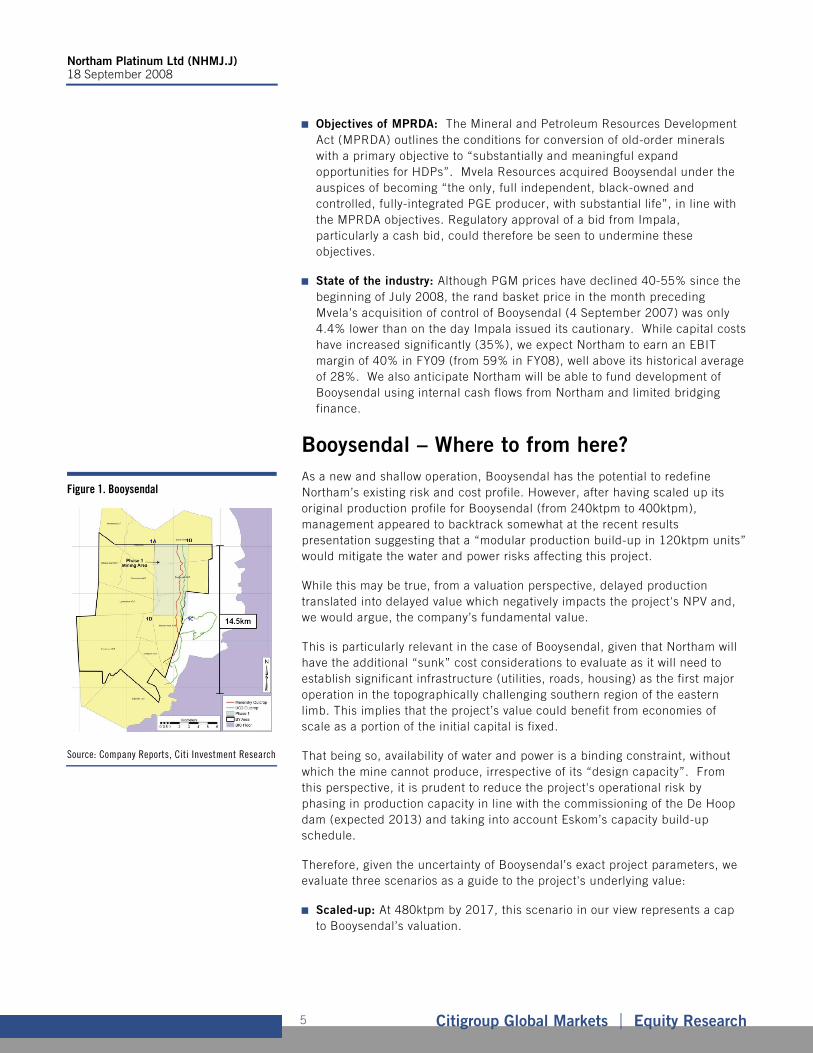

Objectives of MPRDA: The Mineral and Petroleum Resources Development Act (MPRDA) outlines the conditions for conversion of old-order minerals with a primary objective to “substantially and meaningful expand opportunities for HDPs”. Mvela Resources acquired Booysendal under the auspices of becoming “the only, full independent, black-owned and controlled, fully-integrated PGE producer, with substantial life”, in line with the MPRDA objectives. Regulatory approval of a bid from Impala, particularly a cash bid, could therefore be seen to undermine these objectives.

State of the industry: Although PGM prices have declined 40-55% since the beginning of July 2008, the rand basket price in the month preceding Mvela’s acquisition of control of Booysendal (4 September 2007) was only 4.4% lower than on the day Impala issued its cautionary. While capital costs have increased significantly (35%), we expect Northam to earn an EBIT margin of 40% in FY09 (from 59% in FY08), well above its historical average of 28%. We also anticipate Northam will be able to fund development of Booysendal using internal cash flows from Northam and limited bridging finance.

Booysendal – Where to from here?

As a new and shallow operation, Booysendal has the potential to redefine Northam’s existing risk and cost profile. However, after having scaled up its original production profile for Booysendal (from 240ktpm to 400ktpm), management appeared to backtrack somewhat at the recent results presentation suggesting that a “modular production build-up in 120ktpm units” would mitigate the water and power risks affecting this project.

While this may be true, from a valuation perspective, delayed production translated into delayed value which negatively impacts the project's NPV and, we would argue, the company’s fundamental value.

This is particularly relevant in the case of Booysendal, given that Northam will have the additional “sunk” cost considerations to evaluate as it will need to establish significant infrastructure (utilities, roads, housing) as the first major operation in the topographically challenging southern region of the eastern limb. This implies that the project’s value could benefit from economies of scale as a portion of the initial capital is fixed.

That being so, availability of water and power is a binding constraint, without which the mine cannot produce, irrespective of its “design capacity”. From this perspective, it is prudent to reduce the project's operational risk by phasing in production capacity in line with the commissioning of the De Hoop dam (expected 2013) and taking into account Eskom’s capacity build-up schedule.

Therefore, given the uncertainty of Booysendal’s exact project parameters, we evaluate three scenarios as a guide to the project's underlying value:

Scaled-up: At 480ktpm by 2017, this scenario in our view represents a cap to Booysendal’s valuation.

Figure 1. Booysendal

Source: Company Reports, Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 6

Original: Follows Northam’s initial guidance for a 240ktpm operation.

Modular: As mentioned above, Northam’s management recently alluded to a modular-type production build-up and we simulate such a scenario.

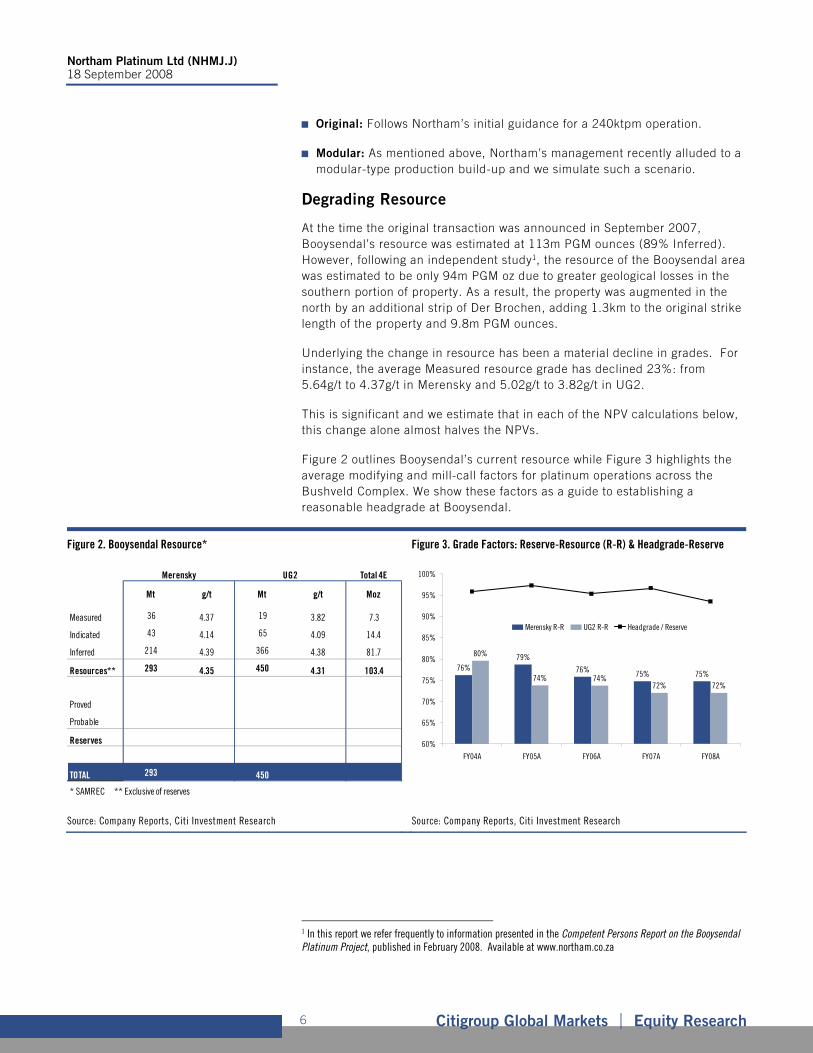

Degrading Resource

At the time the original transaction was announced in September 2007, Booysendal’s resource was estimated at 113m PGM ounces (89% Inferred). However, following an independent study1, the resource of the Booysendal area was estimated to be only 94m PGM oz due to greater geological losses in the southern portion of property. As a result, the property was augmented in the north by an additional strip of Der Brochen, adding 1.3km to the original strike length of the property and 9.8m PGM ounces.

Underlying the change in resource has been a material decline in grades. For instance, the average Measured resource grade has declined 23%: from 5.64g/t to 4.37g/t in Merensky and 5.02g/t to 3.82g/t in UG2.

This is significant and we estimate that in each of the NPV calculations below, this change alone almost halves the NPVs.

Figure 2 outlines Booysendal’s current resource while Figure 3 highlights the average modifying and mill-call factors for platinum operations across the Bushveld Complex. We show these factors as a guide to establishing a reasonable headgrade at Booysendal.

Figure 2. Booysendal Resource* Figure 3. Grade Factors: Reserve-Resource (R-R) & Headgrade-Reserve

Total 4E

Mt g/t Mt g/t Moz

Measured 36 4.37 19 3.82 7.3

Indicated 43 4.14 65 4.09 14.4

Inferred 214 4.39 366 4.38 81.7

Resources** 293 4.35 450 4.31 103.4

Proved

Probable

Reserves

TOTAL 293 450

* SAMREC ** Exclusive of reserves

Merensky UG2

76%79%

76% 75% 75%

80%

74% 74%72% 72%

60%

65%

70%

75%

80%

85%

90%

95%

100%

FY04A FY05A FY06A FY07A FY08A

Merensky R-R UG2 R-R Headgrade / Reserve

Source: Company Reports, Citi Investment Research Source: Company Reports, Citi Investment Research

1 In this report we refer frequently to information presented in the Competent Persons Report on the Booysendal Platinum Project, published in February 2008. Available at www.northam.co.za

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 7

For instance, in FY08 the average Merensky (UG2) reserve grade was only 75% (72%) of the resource grade and the headgrade was diluted by a further 6% (compared to the implied reserve grade). Therefore, if the average Merensky resource grade was 5g/t, the average headgrade would be only 3.53g/t.

Benchmarking Costs

Operating and capital costs are crucial considerations when calculating NPVs for the above scenarios. Although it is simplistic to commoditise concentrators or other capital items, we have little alternative given that a bankable feasibility study is only due 2H09. As such, we benchmark the three significant cost categories against recent performance and published information in order to estimate achievable costs targets. The three categories are: operating costs, ongoing capex and expansion capex.

Operating Costs

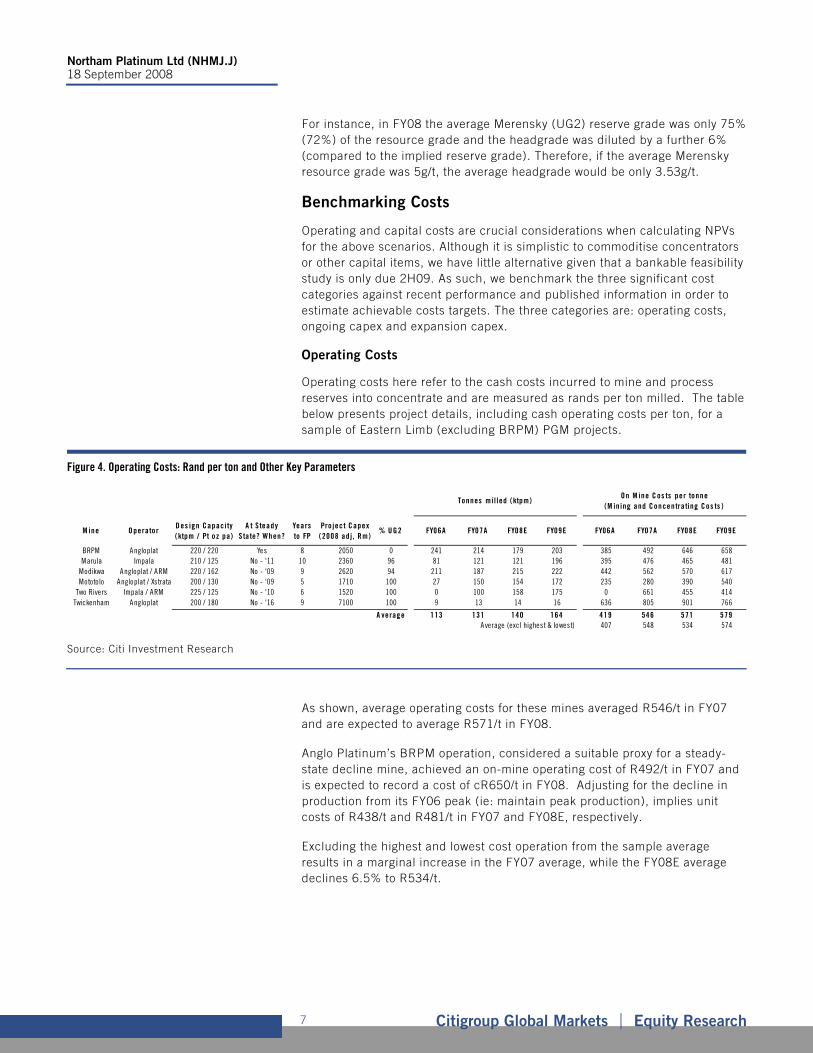

Operating costs here refer to the cash costs incurred to mine and process reserves into concentrate and are measured as rands per ton milled. The table below presents project details, including cash operating costs per ton, for a sample of Eastern Limb (excluding BRPM) PGM projects.

Figure 4. Operating Costs: Rand per ton and Other Key Parameters

M ine O peratorD es ign Capacity (ktpm / Pt oz pa)

A t S teady State? When?

Years to FP

Project Capex ( 2008 ad j, Rm)

% U G2 FY06A FY07A FY08E FY09E FY06A FY07A FY08E FY09E

BRPM Angloplat 220 / 220 Yes 8 2050 0 241 214 179 203 385 492 646 658Marula Impala 210 / 125 No - '11 10 2360 96 81 121 121 196 395 476 465 481

Modikwa Angloplat / ARM 220 / 162 No - '09 9 2620 94 211 187 215 222 442 562 570 617Mototolo Angloplat / Xstrata 200 / 130 No - '09 5 1710 100 27 150 154 172 235 280 390 540

Two Rivers Impala / ARM 225 / 125 No - '10 6 1520 100 0 100 158 175 0 661 455 414Twickenham Angloplat 200 / 180 No - '16 9 7100 100 9 13 14 16 636 805 901 766

A verage 113 131 140 164 419 546 571 579Average (excl highest & lowest) 407 548 534 574

On M ine C os ts per tonne (M in ing and Concentrating Cos ts )

Tonnes mi l led (ktpm)

Source: Citi Investment Research

As shown, average operating costs for these mines averaged R546/t in FY07 and are expected to average R571/t in FY08.

Anglo Platinum’s BRPM operation, considered a suitable proxy for a steady-state decline mine, achieved an on-mine operating cost of R492/t in FY07 and is expected to record a cost of cR650/t in FY08. Adjusting for the decline in production from its FY06 peak (ie: maintain peak production), implies unit costs of R438/t and R481/t in FY07 and FY08E, respectively.

Excluding the highest and lowest cost operation from the sample average results in a marginal increase in the FY07 average, while the FY08E average declines 6.5% to R534/t.

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 8

In presentations outlining the original (240ktpm) and then the 400ktpm proposed operations at Booysendal, Northam guided towards operating costs (in 2007 real terms) of R301/t and R378/t (including smelting and refining), respectively.

From the table above, these costs appear out of line with actual costs of production achieved across similar operations. We therefore suggest that realistic operating costs are likely to be higher than those indicated by the company.

We also highlight that the time from project approval to full production is typically longer than six years and that the average standalone operation is designed to operate at a capacity between 200 and 250ktpm.

Ongoing Capex

Ongoing, or maintenance, capex is capital expenditure on infrastructure or equipment necessary to sustain output at existing levels.

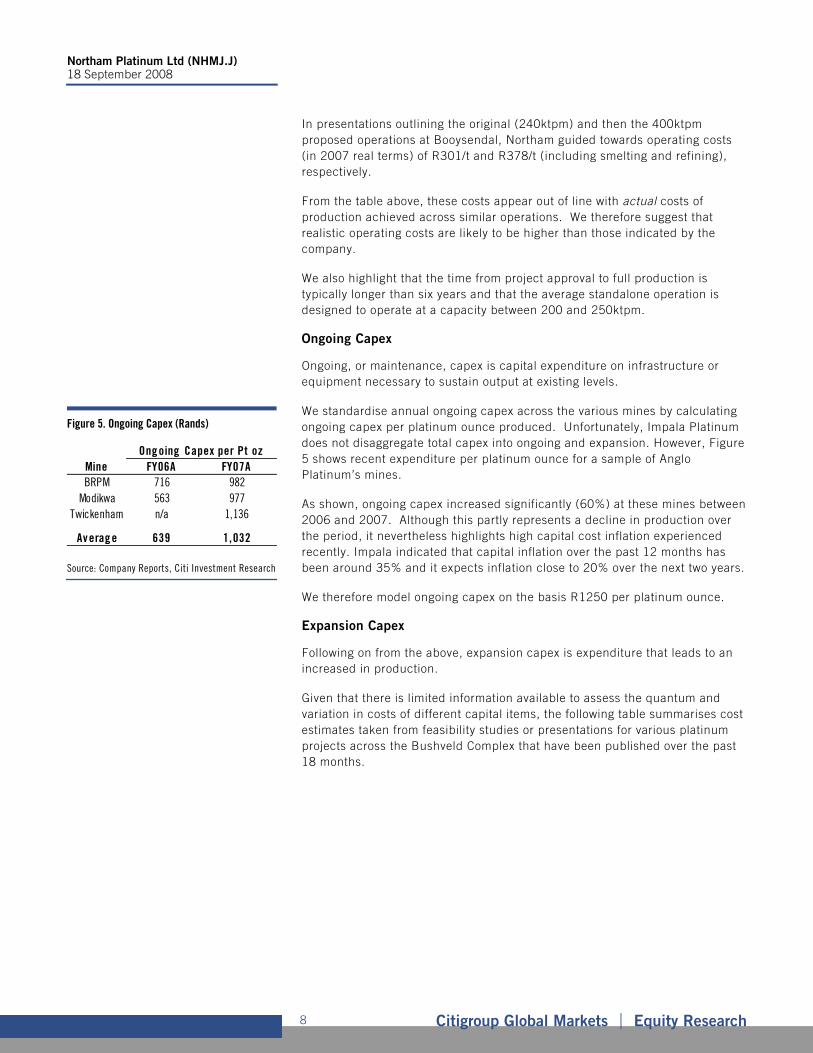

We standardise annual ongoing capex across the various mines by calculating ongoing capex per platinum ounce produced. Unfortunately, Impala Platinum does not disaggregate total capex into ongoing and expansion. However, Figure 5 shows recent expenditure per platinum ounce for a sample of Anglo Platinum’s mines.

As shown, ongoing capex increased significantly (60%) at these mines between 2006 and 2007. Although this partly represents a decline in production over the period, it nevertheless highlights high capital cost inflation experienced recently. Impala indicated that capital inflation over the past 12 months has been around 35% and it expects inflation close to 20% over the next two years.

We therefore model ongoing capex on the basis R1250 per platinum ounce.

Expansion Capex

Following on from the above, expansion capex is expenditure that leads to an increased in production.

Given that there is limited information available to assess the quantum and variation in costs of different capital items, the following table summarises cost estimates taken from feasibility studies or presentations for various platinum projects across the Bushveld Complex that have been published over the past 18 months.

Figure 5. Ongoing Capex (Rands)

Mine FY06A FY07ABRPM 716 982

Modikwa 563 977Twickenham n/a 1,136

Averag e 639 1,032

Ong oing Capex per Pt oz

Source: Company Reports, Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 9

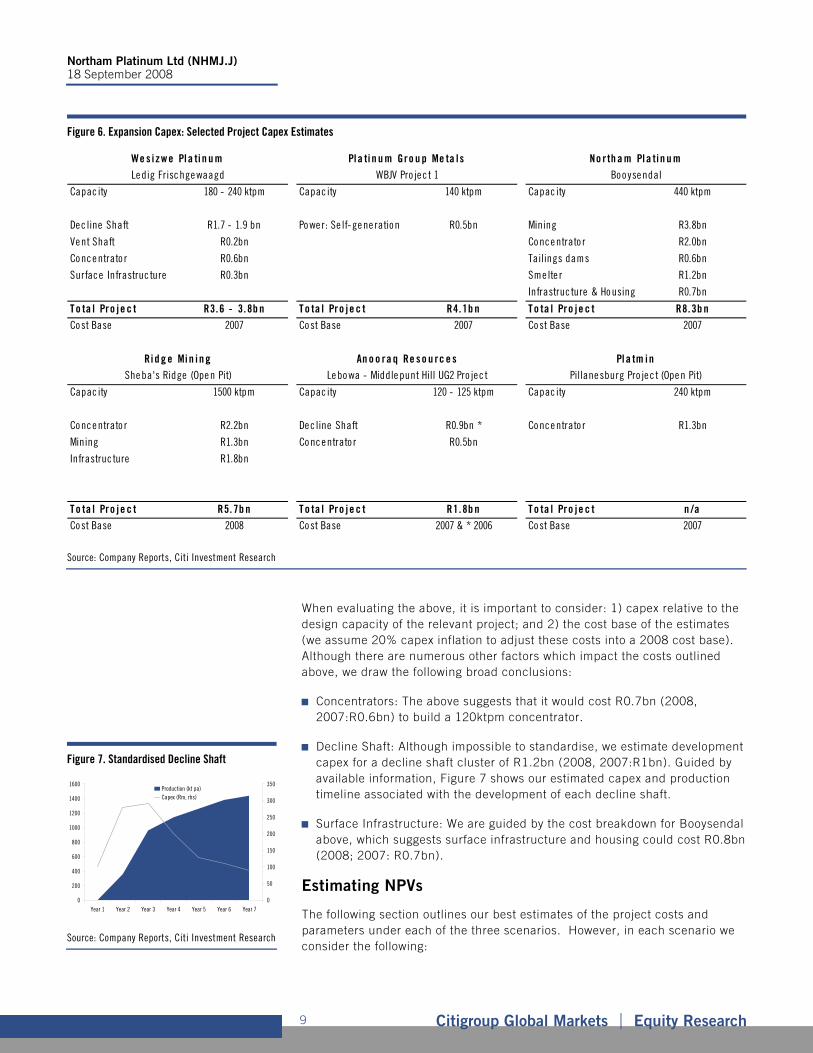

Figure 6. Expansion Capex: Selected Project Capex Estimates

Capac ity 180 - 240 ktpm Capac ity 140 ktpm Capac ity 440 ktpm

Dec line Shaft R1.7 - 1.9 bn Po we r: Se lf-ge ne ration R0.5bn Mining R3.8bn

Vent Shaft R0.2bn Co nce ntrato r R2.0bn

Conc e ntrato r R0.6bn Tailings dams R0.6bn

Surface Infrastruc ture R0.3bn Sme lte r R1.2bn

Infrastruc ture & Ho using R0.7bn

T o ta l Pro j e c t R3.6 - 3.8b n T o ta l Pro j e c t R4.1b n T o ta l Pro je c t R8.3b nCost Base 2007 Co st Base 2007 Co st Base 2007

Capac ity 1500 ktpm Capac ity 120 - 125 ktpm Capac ity 240 ktpm

Conc e ntrato r R2.2bn De c line Shaft R0.9bn * Co nce ntrato r R1.3bn

Mining R1.3bn Co nc e ntrato r R0.5bn

Infrastruc ture R1.8bn

T o ta l Pro j e c t R5. 7b n T o ta l Pro j e c t R1.8b n T o ta l Pro je c t n /aCost Base 2008 Co st Base 2007 & * 2006 Co st Base 2007

Pl a tm i nPillanesburg Pro je c t (Ope n Pit)

No rth a m Pl a tin u mBoo yse ndal

Ri d g e Mi n i n gShe ba's Ridge (Ope n Pit)

An o o ra q Re s o u rc e sLe bo wa - Middle punt Hill UG2 Pro jec t

We s iz we Pla ti n u mLe dig Frisc hge waagd

Pla ti n u m Gro u p Me ta l sWBJV Pro je c t 1

Source: Company Reports, Citi Investment Research

When evaluating the above, it is important to consider: 1) capex relative to the design capacity of the relevant project; and 2) the cost base of the estimates (we assume 20% capex inflation to adjust these costs into a 2008 cost base). Although there are numerous other factors which impact the costs outlined above, we draw the following broad conclusions:

Concentrators: The above suggests that it would cost R0.7bn (2008, 2007:R0.6bn) to build a 120ktpm concentrator.

Decline Shaft: Although impossible to standardise, we estimate development capex for a decline shaft cluster of R1.2bn (2008, 2007:R1bn). Guided by available information, Figure 7 shows our estimated capex and production timeline associated with the development of each decline shaft.

Surface Infrastructure: We are guided by the cost breakdown for Booysendal above, which suggests surface infrastructure and housing could cost R0.8bn (2008; 2007: R0.7bn).

Estimating NPVs

The following section outlines our best estimates of the project costs and parameters under each of the three scenarios. However, in each scenario we consider the following:

Figure 7. Standardised Decline Shaft

0

200

400

600

800

1000

1200

1400

1600

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 70

50

100

150

200

250

300

350Production (kt pa)Capex (Rm, rhs)

Source: Company Reports, Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 10

Smelter and refining costs: Northam will have insufficient smelting capacity at its Northam processing plant to treat concentrate from Booysendal, in addition to concentrate from its Northam Mine and from Platmin’s Pilanesberg Project (as per a recently concluded concentrate off-take agreement). To avoid the uncertainty inherent in forecasting the timing and cost of additional smelter capacity, we assume Northam enters into an off-take agreement of its own for Booysendal concentrate. We estimate that the terms of these contracts typically vary between 10% and 15% of the concentrates’ refined market value. However, given Northam’s refining relationship with Heraeus, we believe it may be able to achieve preferential terms and we therefore believe Northam could earn 92% of the prevailing spot metal price, in lieu of refining charges.

Royalties: We assume Northam pays royalties on refined mineral sales. This caps the royalty payable to 5% of gross revenue.

Preference for UG2: As stated at its FY08 results presentation, we take into account the preference towards mining UG2 ore over Merensky. Notwithstanding, Merensky’s higher resource grade (4.37g/t vs 3.82g/t), the UG2 reef is more amenable to on-reef development and mechanisation, thus allowing for a smaller capital footprint.

Infrastructure: As noted earlier, development of Booysendal will require expenditure on broader infrastructure, such as: roads, utilities and housing. We include capex of R800m in each scenario to account for this.

Mining Life: We model each scenario over a 33-year period, from 2009 to 2041.

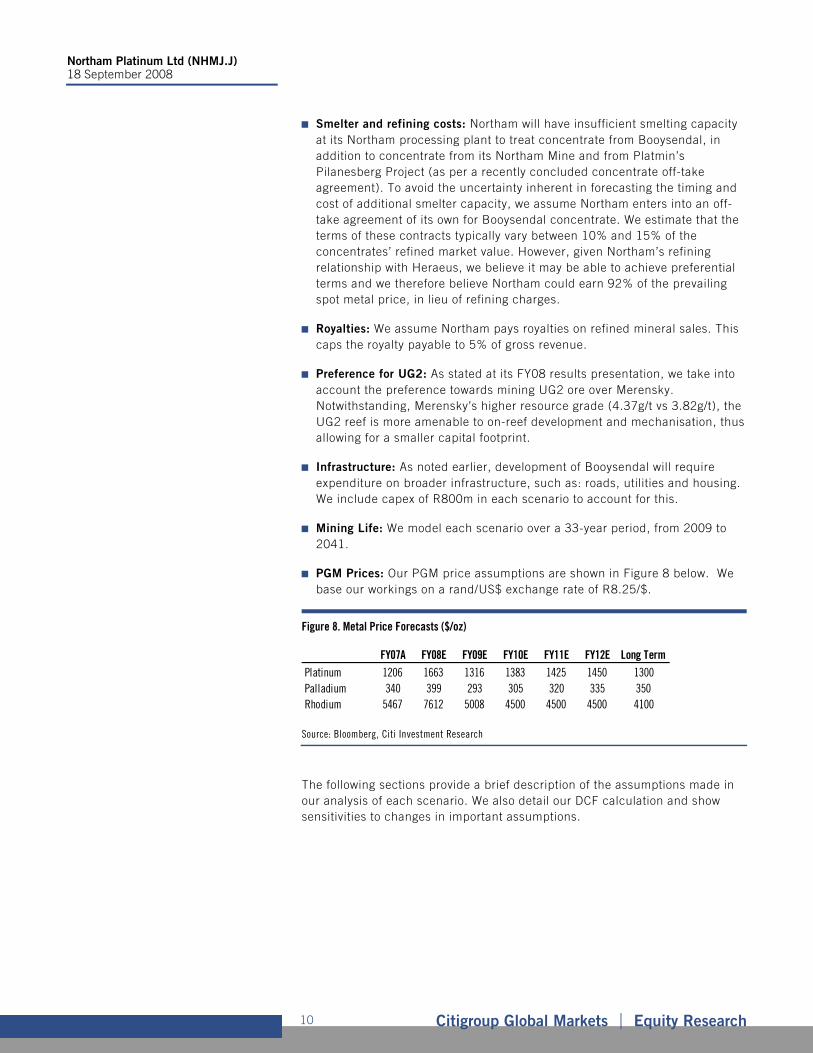

PGM Prices: Our PGM price assumptions are shown in Figure 8 below. We base our workings on a rand/US$ exchange rate of R8.25/$.

Figure 8. Metal Price Forecasts ($/oz)

FY07A FY08E FY09E FY10E FY11E FY12E Long TermPlatinum 1206 1663 1316 1383 1425 1450 1300Palladium 340 399 293 305 320 335 350Rhodium 5467 7612 5008 4500 4500 4500 4100

Source: Bloomberg, Citi Investment Research

The following sections provide a brief description of the assumptions made in our analysis of each scenario. We also detail our DCF calculation and show sensitivities to changes in important assumptions.

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 11

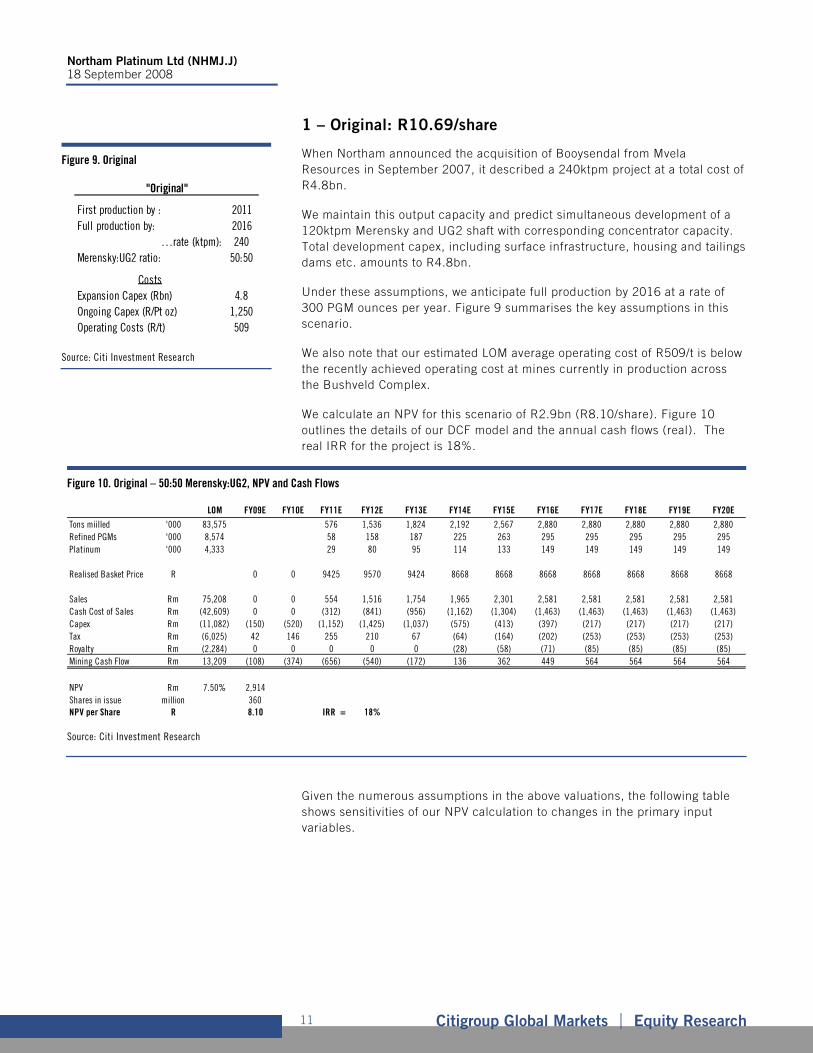

1 – Original: R10.69/share

When Northam announced the acquisition of Booysendal from Mvela Resources in September 2007, it described a 240ktpm project at a total cost of R4.8bn.

We maintain this output capacity and predict simultaneous development of a 120ktpm Merensky and UG2 shaft with corresponding concentrator capacity. Total development capex, including surface infrastructure, housing and tailings dams etc. amounts to R4.8bn.

Under these assumptions, we anticipate full production by 2016 at a rate of 300 PGM ounces per year. Figure 9 summarises the key assumptions in this scenario.

We also note that our estimated LOM average operating cost of R509/t is below the recently achieved operating cost at mines currently in production across the Bushveld Complex.

We calculate an NPV for this scenario of R2.9bn (R8.10/share). Figure 10 outlines the details of our DCF model and the annual cash flows (real). The real IRR for the project is 18%.

Figure 10. Original – 50:50 Merensky:UG2, NPV and Cash Flows

LOM FY09E FY10E FY11E FY12E FY13E FY14E FY15E FY16E FY17E FY18E FY19E FY20E

Tons miilled '000 83,575 576 1,536 1,824 2,192 2,567 2,880 2,880 2,880 2,880 2,880Refined PGMs '000 8,574 58 158 187 225 263 295 295 295 295 295Platinum '000 4,333 29 80 95 114 133 149 149 149 149 149

Realised Basket Price R 0 0 9425 9570 9424 8668 8668 8668 8668 8668 8668 8668

Sales Rm 75,208 0 0 554 1,516 1,754 1,965 2,301 2,581 2,581 2,581 2,581 2,581Cash Cost of Sales Rm (42,609) 0 0 (312) (841) (956) (1,162) (1,304) (1,463) (1,463) (1,463) (1,463) (1,463)Capex Rm (11,082) (150) (520) (1,152) (1,425) (1,037) (575) (413) (397) (217) (217) (217) (217)Tax Rm (6,025) 42 146 255 210 67 (64) (164) (202) (253) (253) (253) (253)Royalty Rm (2,284) 0 0 0 0 0 (28) (58) (71) (85) (85) (85) (85)Mining Cash Flow Rm 13,209 (108) (374) (656) (540) (172) 136 362 449 564 564 564 564

NPV Rm 7.50% 2,914Shares in issue million 360NPV per Share R 8.10 IRR = 18%

Source: Citi Investment Research

Given the numerous assumptions in the above valuations, the following table shows sensitivities of our NPV calculation to changes in the primary input variables.

Figure 9. Original

First production by : 2011Full production by: 2016

…rate (ktpm): 240Merensky:UG2 ratio: 50:50

CostsExpansion Capex (Rbn) 4.8Ongoing Capex (R/Pt oz) 1,250Operating Costs (R/t) 509

"Original"

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 12

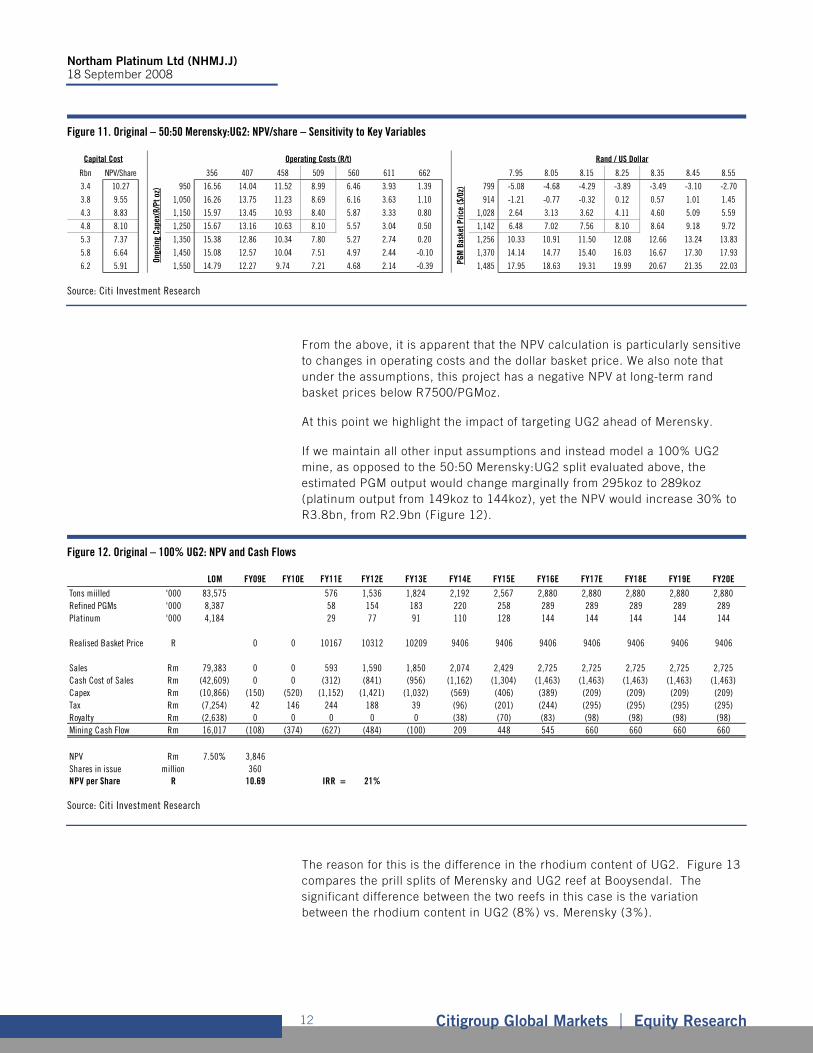

Figure 11. Original – 50:50 Merensky:UG2: NPV/share – Sensitivity to Key Variables

Rbn NPV/Share 356 407 458 509 560 611 662 7.95 8.05 8.15 8.25 8.35 8.45 8.55

3.4 10.27 950 16.56 14.04 11.52 8.99 6.46 3.93 1.39 799 -5.08 -4.68 -4.29 -3.89 -3.49 -3.10 -2.70

3.8 9.55 1,050 16.26 13.75 11.23 8.69 6.16 3.63 1.10 914 -1.21 -0.77 -0.32 0.12 0.57 1.01 1.45

4.3 8.83 1,150 15.97 13.45 10.93 8.40 5.87 3.33 0.80 1,028 2.64 3.13 3.62 4.11 4.60 5.09 5.59

4.8 8.10 1,250 15.67 13.16 10.63 8.10 5.57 3.04 0.50 1,142 6.48 7.02 7.56 8.10 8.64 9.18 9.72

5.3 7.37 1,350 15.38 12.86 10.34 7.80 5.27 2.74 0.20 1,256 10.33 10.91 11.50 12.08 12.66 13.24 13.83

5.8 6.64 1,450 15.08 12.57 10.04 7.51 4.97 2.44 -0.10 1,370 14.14 14.77 15.40 16.03 16.67 17.30 17.93

6.2 5.91 1,550 14.79 12.27 9.74 7.21 4.68 2.14 -0.39 1,485 17.95 18.63 19.31 19.99 20.67 21.35 22.03

Capital CostOn

goin

g Ca

pex(

R/Pt

oz)

Operating Costs (R/t) Rand / US Dollar

PGM

Bas

ket P

rice

($/0

z)

Source: Citi Investment Research

From the above, it is apparent that the NPV calculation is particularly sensitive to changes in operating costs and the dollar basket price. We also note that under the assumptions, this project has a negative NPV at long-term rand basket prices below R7500/PGMoz.

At this point we highlight the impact of targeting UG2 ahead of Merensky.

If we maintain all other input assumptions and instead model a 100% UG2 mine, as opposed to the 50:50 Merensky:UG2 split evaluated above, the estimated PGM output would change marginally from 295koz to 289koz (platinum output from 149koz to 144koz), yet the NPV would increase 30% to R3.8bn, from R2.9bn (Figure 12).

Figure 12. Original – 100% UG2: NPV and Cash Flows

LOM FY09E FY10E FY11E FY12E FY13E FY14E FY15E FY16E FY17E FY18E FY19E FY20E

Tons miilled '000 83,575 576 1,536 1,824 2,192 2,567 2,880 2,880 2,880 2,880 2,880Refined PGMs '000 8,387 58 154 183 220 258 289 289 289 289 289Platinum '000 4,184 29 77 91 110 128 144 144 144 144 144

Realised Basket Price R 0 0 10167 10312 10209 9406 9406 9406 9406 9406 9406 9406

Sales Rm 79,383 0 0 593 1,590 1,850 2,074 2,429 2,725 2,725 2,725 2,725 2,725Cash Cost of Sales Rm (42,609) 0 0 (312) (841) (956) (1,162) (1,304) (1,463) (1,463) (1,463) (1,463) (1,463)Capex Rm (10,866) (150) (520) (1,152) (1,421) (1,032) (569) (406) (389) (209) (209) (209) (209)Tax Rm (7,254) 42 146 244 188 39 (96) (201) (244) (295) (295) (295) (295)Royalty Rm (2,638) 0 0 0 0 0 (38) (70) (83) (98) (98) (98) (98)Mining Cash Flow Rm 16,017 (108) (374) (627) (484) (100) 209 448 545 660 660 660 660

NPV Rm 7.50% 3,846Shares in issue million 360NPV per Share R 10.69 IRR = 21%

Source: Citi Investment Research

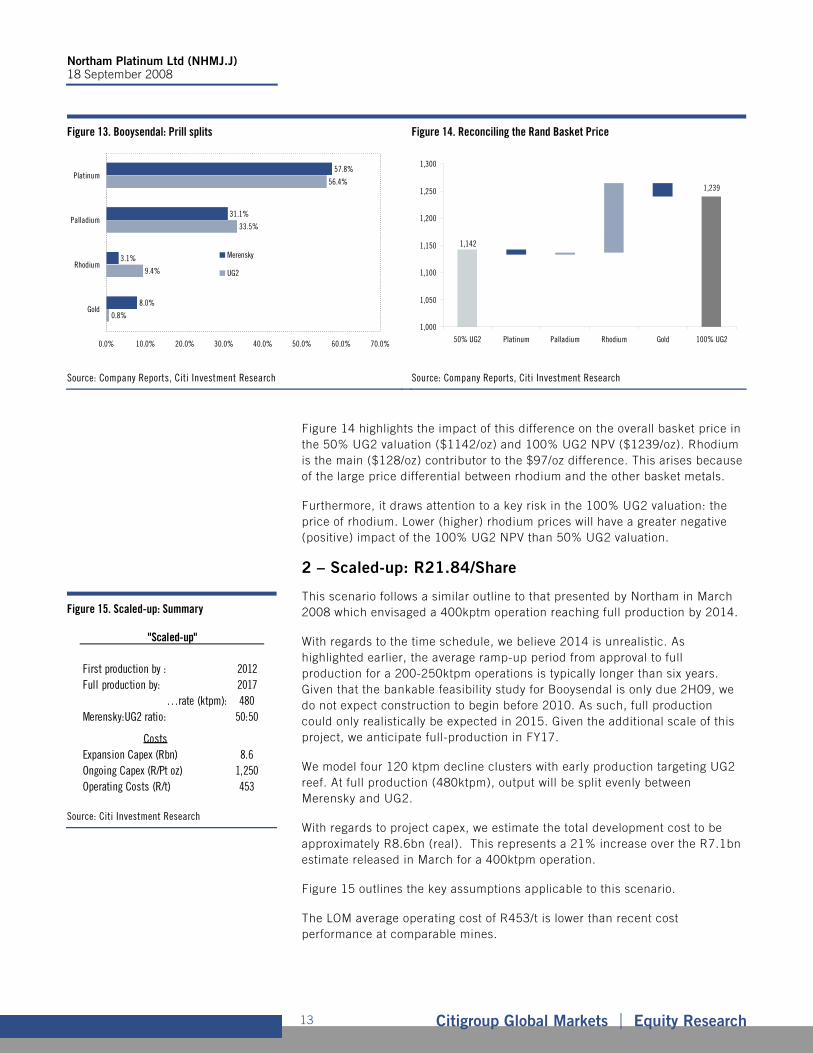

The reason for this is the difference in the rhodium content of UG2. Figure 13 compares the prill splits of Merensky and UG2 reef at Booysendal. The significant difference between the two reefs in this case is the variation between the rhodium content in UG2 (8%) vs. Merensky (3%).

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 13

Figure 13. Booysendal: Prill splits Figure 14. Reconciling the Rand Basket Price

57.8%

31.1%

3.1%

8.0%

56.4%

33.5%

9.4%

0.8%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Platinum

Palladium

Rhodium

Gold

Merensky

UG2

1,142

1,239

1,000

1,050

1,100

1,150

1,200

1,250

1,300

50% UG2 Platinum Palladium Rhodium Gold 100% UG2

Source: Company Reports, Citi Investment Research Source: Company Reports, Citi Investment Research

Figure 14 highlights the impact of this difference on the overall basket price in the 50% UG2 valuation ($1142/oz) and 100% UG2 NPV ($1239/oz). Rhodium is the main ($128/oz) contributor to the $97/oz difference. This arises because of the large price differential between rhodium and the other basket metals.

Furthermore, it draws attention to a key risk in the 100% UG2 valuation: the price of rhodium. Lower (higher) rhodium prices will have a greater negative (positive) impact of the 100% UG2 NPV than 50% UG2 valuation.

2 – Scaled-up: R21.84/Share

This scenario follows a similar outline to that presented by Northam in March 2008 which envisaged a 400kptm operation reaching full production by 2014.

With regards to the time schedule, we believe 2014 is unrealistic. As highlighted earlier, the average ramp-up period from approval to full production for a 200-250ktpm operations is typically longer than six years. Given that the bankable feasibility study for Booysendal is only due 2H09, we do not expect construction to begin before 2010. As such, full production could only realistically be expected in 2015. Given the additional scale of this project, we anticipate full-production in FY17.

We model four 120 ktpm decline clusters with early production targeting UG2 reef. At full production (480ktpm), output will be split evenly between Merensky and UG2.

With regards to project capex, we estimate the total development cost to be approximately R8.6bn (real). This represents a 21% increase over the R7.1bn estimate released in March for a 400ktpm operation.

Figure 15 outlines the key assumptions applicable to this scenario.

The LOM average operating cost of R453/t is lower than recent cost performance at comparable mines.

Figure 15. Scaled-up: Summary

First production by : 2012Full production by: 2017

…rate (ktpm): 480Merensky:UG2 ratio: 50:50

CostsExpansion Capex (Rbn) 8.6Ongoing Capex (R/Pt oz) 1,250Operating Costs (R/t) 453

"Scaled-up"

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 14

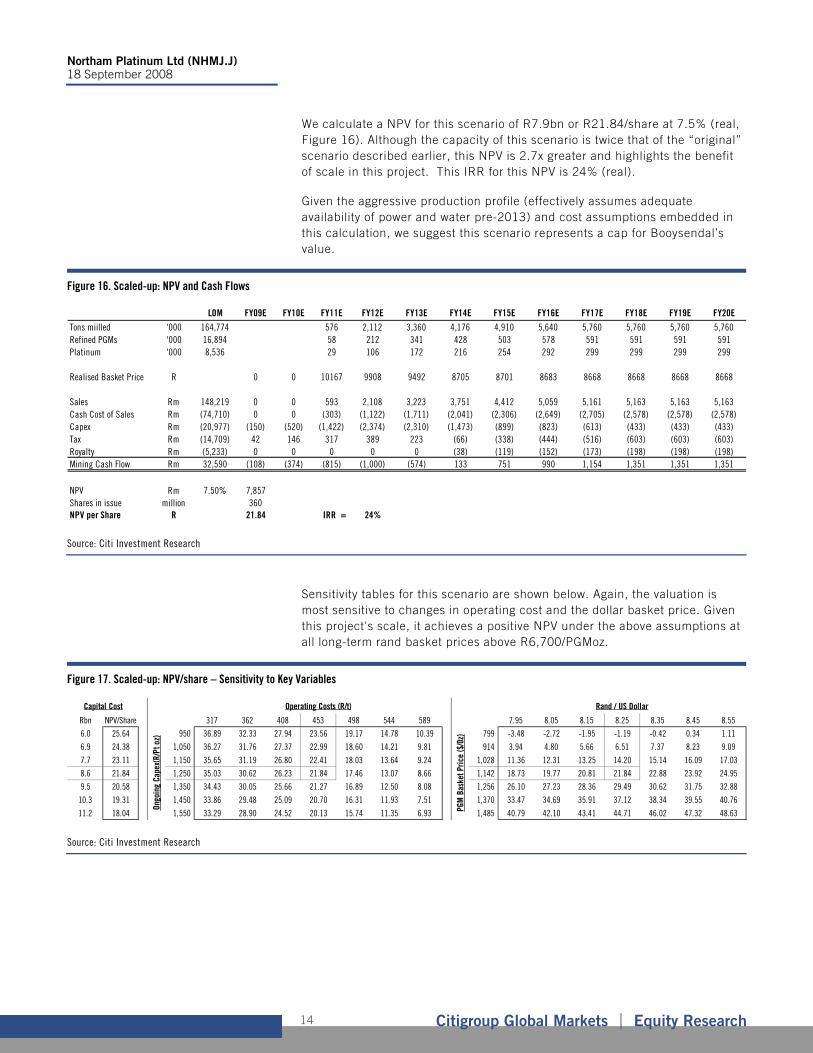

We calculate a NPV for this scenario of R7.9bn or R21.84/share at 7.5% (real, Figure 16). Although the capacity of this scenario is twice that of the “original” scenario described earlier, this NPV is 2.7x greater and highlights the benefit of scale in this project. This IRR for this NPV is 24% (real).

Given the aggressive production profile (effectively assumes adequate availability of power and water pre-2013) and cost assumptions embedded in this calculation, we suggest this scenario represents a cap for Booysendal’s value.

Figure 16. Scaled-up: NPV and Cash Flows

LOM FY09E FY10E FY11E FY12E FY13E FY14E FY15E FY16E FY17E FY18E FY19E FY20E

Tons miilled '000 164,774 576 2,112 3,360 4,176 4,910 5,640 5,760 5,760 5,760 5,760Refined PGMs '000 16,894 58 212 341 428 503 578 591 591 591 591Platinum '000 8,536 29 106 172 216 254 292 299 299 299 299

Realised Basket Price R 0 0 10167 9908 9492 8705 8701 8683 8668 8668 8668 8668

Sales Rm 148,219 0 0 593 2,108 3,223 3,751 4,412 5,059 5,161 5,163 5,163 5,163Cash Cost of Sales Rm (74,710) 0 0 (303) (1,122) (1,711) (2,041) (2,306) (2,649) (2,705) (2,578) (2,578) (2,578)Capex Rm (20,977) (150) (520) (1,422) (2,374) (2,310) (1,473) (899) (823) (613) (433) (433) (433)Tax Rm (14,709) 42 146 317 389 223 (66) (338) (444) (516) (603) (603) (603)Royalty Rm (5,233) 0 0 0 0 0 (38) (119) (152) (173) (198) (198) (198)Mining Cash Flow Rm 32,590 (108) (374) (815) (1,000) (574) 133 751 990 1,154 1,351 1,351 1,351

NPV Rm 7.50% 7,857Shares in issue million 360NPV per Share R 21.84 IRR = 24%

Source: Citi Investment Research

Sensitivity tables for this scenario are shown below. Again, the valuation is most sensitive to changes in operating cost and the dollar basket price. Given this project's scale, it achieves a positive NPV under the above assumptions at all long-term rand basket prices above R6,700/PGMoz.

Figure 17. Scaled-up: NPV/share – Sensitivity to Key Variables

Rbn NPV/Share 317 362 408 453 498 544 589 7.95 8.05 8.15 8.25 8.35 8.45 8.55

6.0 25.64 950 36.89 32.33 27.94 23.56 19.17 14.78 10.39 799 -3.48 -2.72 -1.95 -1.19 -0.42 0.34 1.11

6.9 24.38 1,050 36.27 31.76 27.37 22.99 18.60 14.21 9.81 914 3.94 4.80 5.66 6.51 7.37 8.23 9.09

7.7 23.11 1,150 35.65 31.19 26.80 22.41 18.03 13.64 9.24 1,028 11.36 12.31 13.25 14.20 15.14 16.09 17.03

8.6 21.84 1,250 35.03 30.62 26.23 21.84 17.46 13.07 8.66 1,142 18.73 19.77 20.81 21.84 22.88 23.92 24.95

9.5 20.58 1,350 34.43 30.05 25.66 21.27 16.89 12.50 8.08 1,256 26.10 27.23 28.36 29.49 30.62 31.75 32.88

10.3 19.31 1,450 33.86 29.48 25.09 20.70 16.31 11.93 7.51 1,370 33.47 34.69 35.91 37.12 38.34 39.55 40.76

11.2 18.04 1,550 33.29 28.90 24.52 20.13 15.74 11.35 6.93 1,485 40.79 42.10 43.41 44.71 46.02 47.32 48.63

Capital Cost

Ongo

ing

Cape

x(R/

Pt o

z)

Operating Costs (R/t) Rand / US Dollar

PGM

Bas

ket P

rice

($/0

z)

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 15

3 – Modular: R15.65/share

At the company’s recent results presentation, management discussed the possibility of adopting a modular approach to develop Booysendal in order to mitigate the risk of insufficient power and water. It indicated this may involve phased construction of 120ktpm “units” with a bias towards UG2 production.

Our model follows this approach. Given that power and water availability is only likely to be “secure” beyond 2013, we assume Northam will only have adequate power and water (partly from allocations granted by Anglo Platinum) to develop and bring into production one decline shaft, which will stockpile ore until a concentrator is commissioned in 2013. Beyond this, additional capacity will be added and the mine will ramp up to 480ktpm by FY21.

The average operating cost of R477/t is greater than the “Scaled-up” scenario, yet still well below recently achieved cost targets. Real capex for this project is estimated at R8.8bn.

We calculate an NPV of R5.6bn or R15.65/share under this scenario (Figure 19). The real IRR is 20%.

Figure 19. Modular: NPV and Cash Flows

LOM FY09E FY10E FY11E FY12E FY13E FY14E FY15E FY16E FY17E FY18E FY19E FY20E

Tons miilled '000 150,770 0 1,200 1,931 2,678 3,660 4,320 5,100 5,400 5,580Refined PGMs '000 15,436 0 120 194 269 369 439 520 552 572Platinum '000 7,793 0 60 97 135 185 221 262 279 289

Realised Basket Price R 0 0 10209 9406 9222 9019 8893 8763 8717 8692

Sales Rm 135,690 0 0 0 0 1,217 1,827 2,489 3,350 3,926 4,589 4,853 5,007Cash Cost of Sales Rm (71,455) 0 0 0 0 (611) (994) (1,323) (1,808) (2,134) (2,519) (2,667) (2,621)Capex Rm (20,101) 0 (320) (810) (960) (1,147) (1,080) (1,215) (1,249) (1,340) (1,190) (864) (639)Tax Rm (12,358) 0 90 227 269 151 69 14 (82) (127) (246) (370) (489)Royalty Rm (4,424) 0 0 0 0 0 0 (9) (40) (56) (93) (130) (165)Mining Cash Flow Rm 27,353 0 (230) (583) (691) (390) (178) (44) 171 270 540 821 1,094

NPV Rm 7.50% 5,630Shares in issue million 360NPV per Share R 15.65 IRR = 20%

Source: Citi Investment Research

The sensitivity of this NPV to important input variables is shown below. The project has a negative NPV at long-term rand basket prices below R7,020/PGMoz.

Figure 18. Modular: Summary

First production by : 2013Full production by: 2021

…rate (ktpm): 480Merensky:UG2 ratio: 50:50Steady-State Headgrade (g/t)

CostsExpansion Capex (Rbn) 8.8Ongoing Capex (R/Pt oz) 1,250Operating Costs (R/t) 477

"Modular"

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 16

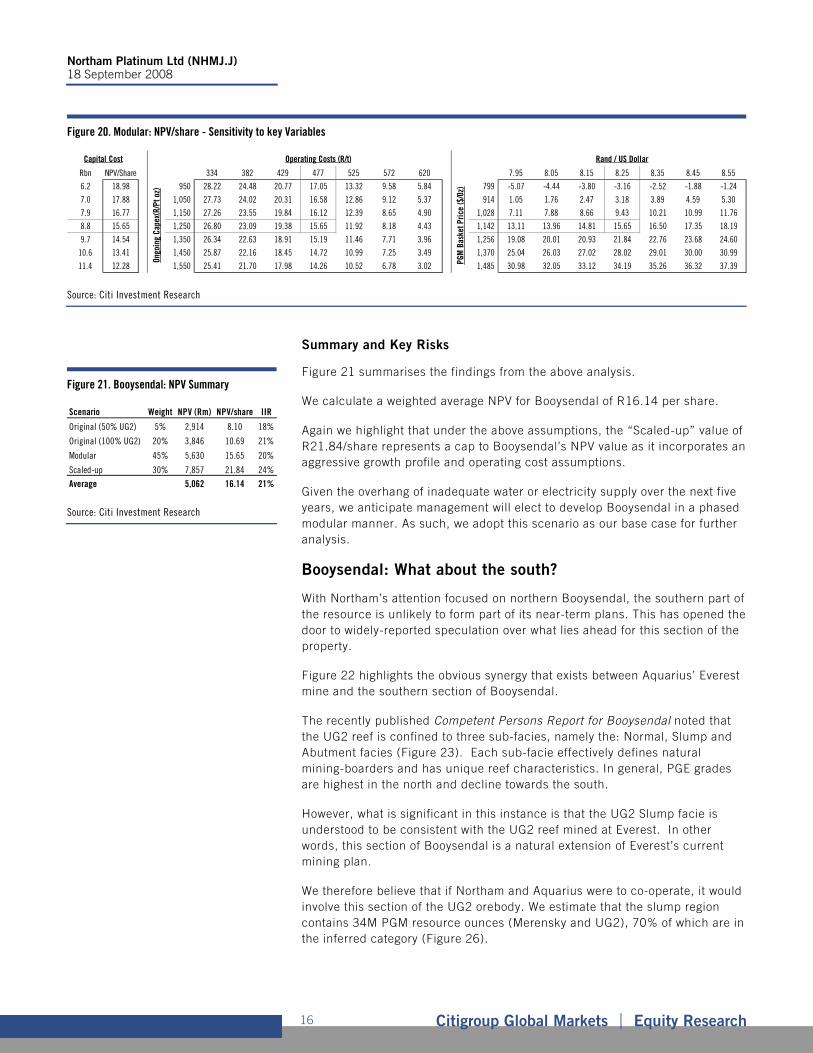

Figure 20. Modular: NPV/share - Sensitivity to key Variables

Rbn NPV/Share 334 382 429 477 525 572 620 7.95 8.05 8.15 8.25 8.35 8.45 8.55

6.2 18.98 950 28.22 24.48 20.77 17.05 13.32 9.58 5.84 799 -5.07 -4.44 -3.80 -3.16 -2.52 -1.88 -1.24

7.0 17.88 1,050 27.73 24.02 20.31 16.58 12.86 9.12 5.37 914 1.05 1.76 2.47 3.18 3.89 4.59 5.30

7.9 16.77 1,150 27.26 23.55 19.84 16.12 12.39 8.65 4.90 1,028 7.11 7.88 8.66 9.43 10.21 10.99 11.76

8.8 15.65 1,250 26.80 23.09 19.38 15.65 11.92 8.18 4.43 1,142 13.11 13.96 14.81 15.65 16.50 17.35 18.19

9.7 14.54 1,350 26.34 22.63 18.91 15.19 11.46 7.71 3.96 1,256 19.08 20.01 20.93 21.84 22.76 23.68 24.60

10.6 13.41 1,450 25.87 22.16 18.45 14.72 10.99 7.25 3.49 1,370 25.04 26.03 27.02 28.02 29.01 30.00 30.99

11.4 12.28 1,550 25.41 21.70 17.98 14.26 10.52 6.78 3.02 1,485 30.98 32.05 33.12 34.19 35.26 36.32 37.39

Capital CostOn

goin

g Ca

pex(

R/Pt

oz)

Operating Costs (R/t) Rand / US Dollar

PGM

Bas

ket P

rice

($/0

z)

Source: Citi Investment Research

Summary and Key Risks

Figure 21 summarises the findings from the above analysis.

We calculate a weighted average NPV for Booysendal of R16.14 per share.

Again we highlight that under the above assumptions, the “Scaled-up” value of R21.84/share represents a cap to Booysendal’s NPV value as it incorporates an aggressive growth profile and operating cost assumptions.

Given the overhang of inadequate water or electricity supply over the next five years, we anticipate management will elect to develop Booysendal in a phased modular manner. As such, we adopt this scenario as our base case for further analysis.

Booysendal: What about the south?

With Northam’s attention focused on northern Booysendal, the southern part of the resource is unlikely to form part of its near-term plans. This has opened the door to widely-reported speculation over what lies ahead for this section of the property.

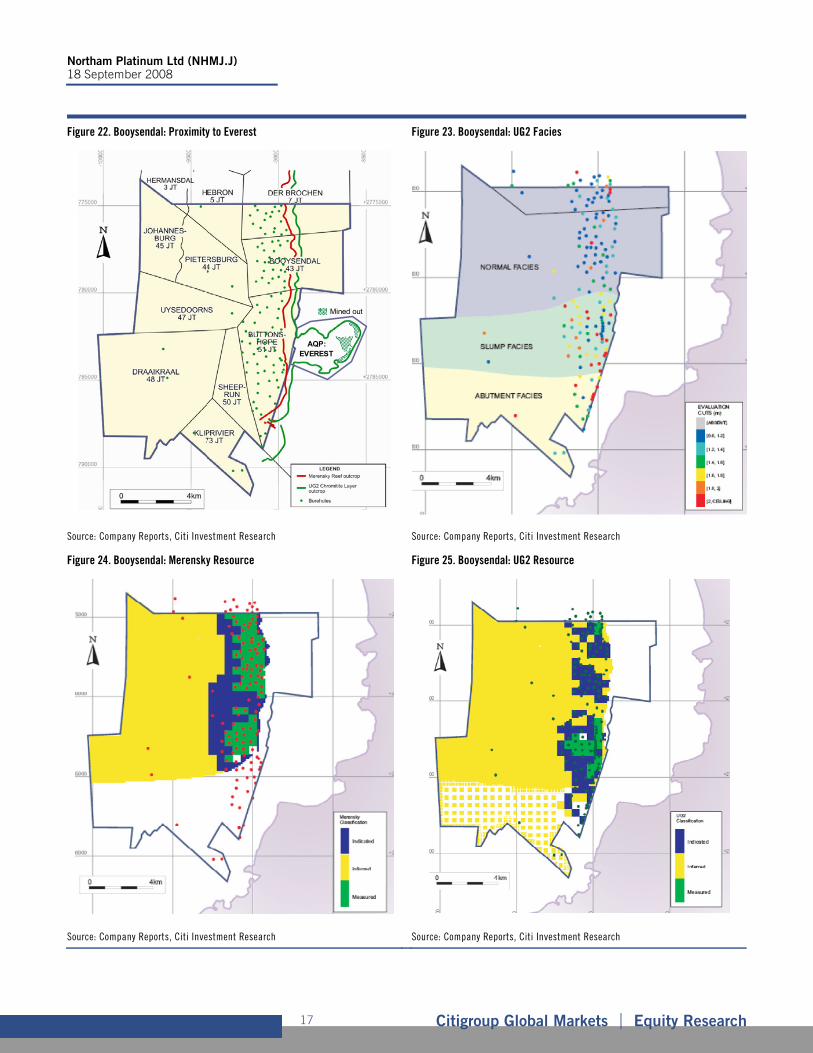

Figure 22 highlights the obvious synergy that exists between Aquarius’ Everest mine and the southern section of Booysendal.

The recently published Competent Persons Report for Booysendal noted that the UG2 reef is confined to three sub-facies, namely the: Normal, Slump and Abutment facies (Figure 23). Each sub-facie effectively defines natural mining-boarders and has unique reef characteristics. In general, PGE grades are highest in the north and decline towards the south.

However, what is significant in this instance is that the UG2 Slump facie is understood to be consistent with the UG2 reef mined at Everest. In other words, this section of Booysendal is a natural extension of Everest’s current mining plan.

We therefore believe that if Northam and Aquarius were to co-operate, it would involve this section of the UG2 orebody. We estimate that the slump region contains 34M PGM resource ounces (Merensky and UG2), 70% of which are in the inferred category (Figure 26).

Figure 21. Booysendal: NPV Summary

Scenario Weight NPV (Rm) NPV/share IIR

Original (50% UG2) 5% 2,914 8.10 18%

Original (100% UG2) 20% 3,846 10.69 21%

Modular 45% 5,630 15.65 20%

Scaled-up 30% 7,857 21.84 24%

Average 5,062 16.14 21%

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 17

Figure 22. Booysendal: Proximity to Everest Figure 23. Booysendal: UG2 Facies

AQP: EVEREST

Mined out

Source: Company Reports, Citi Investment Research Source: Company Reports, Citi Investment Research

Figure 24. Booysendal: Merensky Resource Figure 25. Booysendal: UG2 Resource

Source: Company Reports, Citi Investment Research Source: Company Reports, Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 18

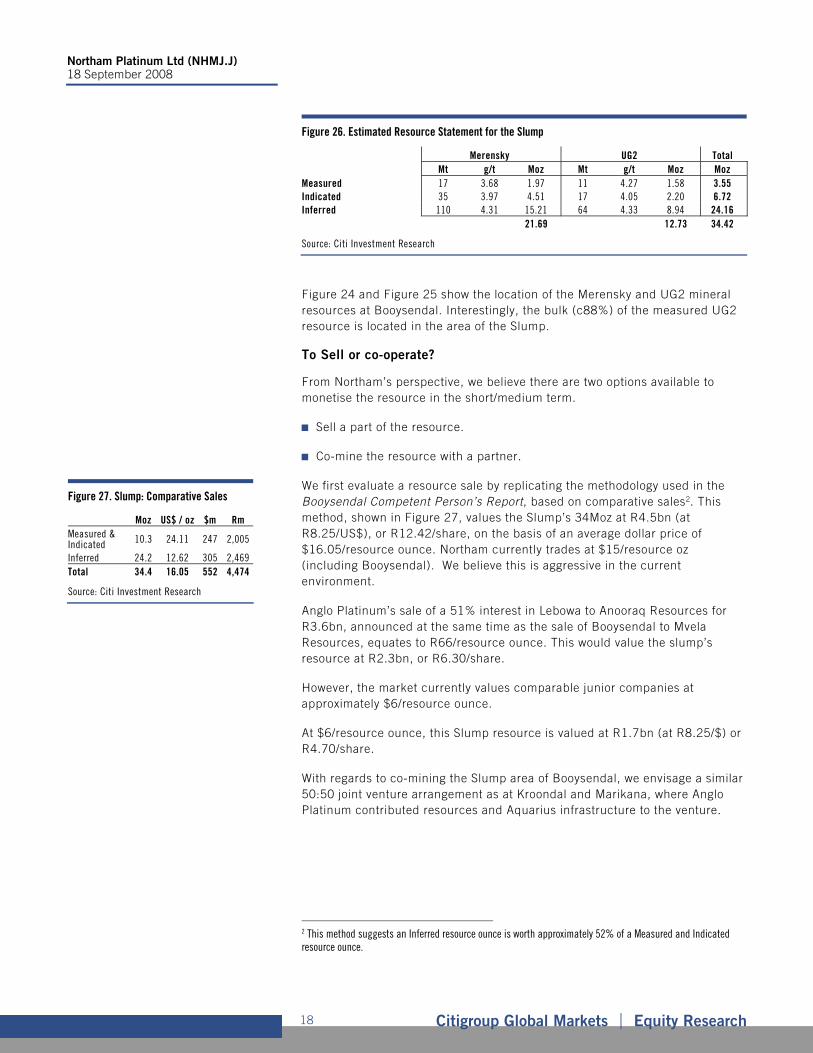

Figure 26. Estimated Resource Statement for the Slump

Merensky UG2 Total Mt g/t Moz Mt g/t Moz Moz Measured 17 3.68 1.97 11 4.27 1.58 3.55 Indicated 35 3.97 4.51 17 4.05 2.20 6.72 Inferred 110 4.31 15.21 64 4.33 8.94 24.16 21.69 12.73 34.42

Source: Citi Investment Research

Figure 24 and Figure 25 show the location of the Merensky and UG2 mineral resources at Booysendal. Interestingly, the bulk (c88%) of the measured UG2 resource is located in the area of the Slump.

To Sell or co-operate?

From Northam’s perspective, we believe there are two options available to monetise the resource in the short/medium term.

Sell a part of the resource.

Co-mine the resource with a partner.

We first evaluate a resource sale by replicating the methodology used in the Booysendal Competent Person’s Report, based on comparative sales2. This method, shown in Figure 27, values the Slump’s 34Moz at R4.5bn (at R8.25/US$), or R12.42/share, on the basis of an average dollar price of $16.05/resource ounce. Northam currently trades at $15/resource oz (including Booysendal). We believe this is aggressive in the current environment.

Anglo Platinum’s sale of a 51% interest in Lebowa to Anooraq Resources for R3.6bn, announced at the same time as the sale of Booysendal to Mvela Resources, equates to R66/resource ounce. This would value the slump’s resource at R2.3bn, or R6.30/share.

However, the market currently values comparable junior companies at approximately $6/resource ounce.

At $6/resource ounce, this Slump resource is valued at R1.7bn (at R8.25/$) or R4.70/share.

With regards to co-mining the Slump area of Booysendal, we envisage a similar 50:50 joint venture arrangement as at Kroondal and Marikana, where Anglo Platinum contributed resources and Aquarius infrastructure to the venture.

2 This method suggests an Inferred resource ounce is worth approximately 52% of a Measured and Indicated resource ounce.

Figure 27. Slump: Comparative Sales

Moz US$ / oz $m Rm Measured & Indicated 10.3 24.11 247 2,005

Inferred 24.2 12.62 305 2,469 Total 34.4 16.05 552 4,474

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 19

Given the shorter strike length, the slump region is likely to support a smaller mine than the northern section (i.e. c240ktpm). Therefore using the above calculations as a guide, we suggest the NPV of such a joint venture would approximate the Original scenarios evaluated earlier. In other words, the NPV could be between R3bn and R4bn. Northam’s 50% share in this venture could be worth cR4.20/share and R5.55/share.

Therefore, both options point to a value of approximately R5/share for a transaction on this section of Booysendal.

Northam Mine

FY08 Operational Review

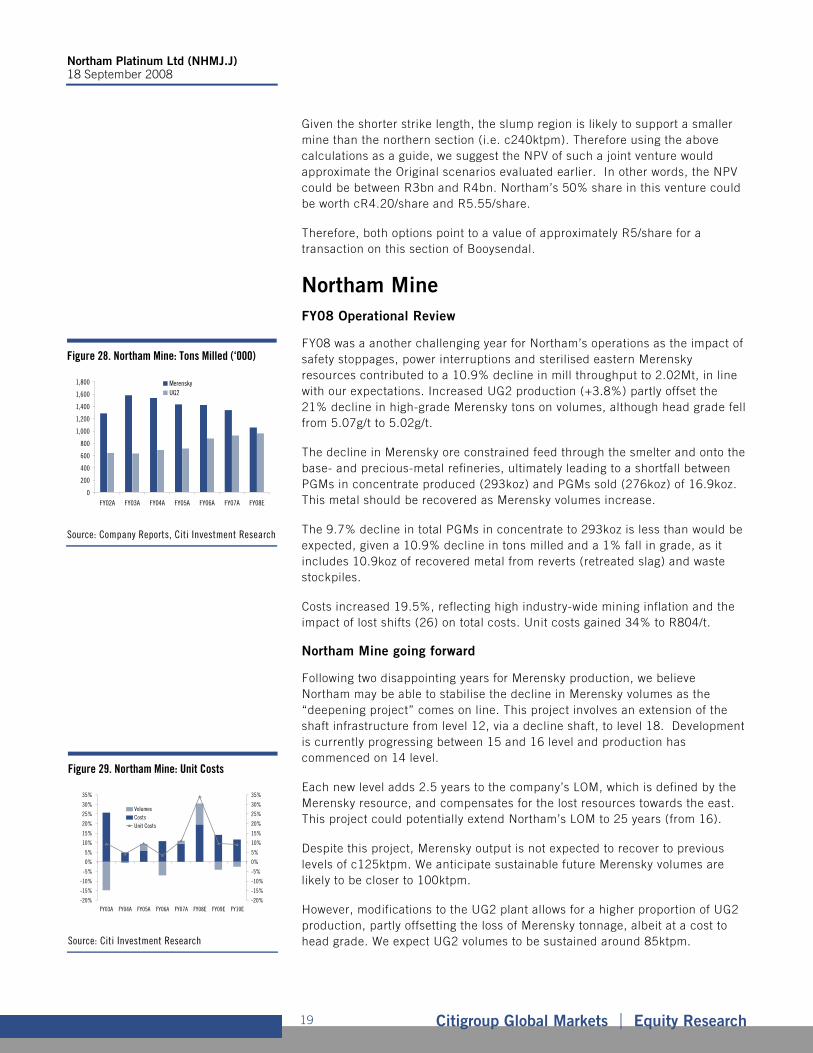

FY08 was a another challenging year for Northam’s operations as the impact of safety stoppages, power interruptions and sterilised eastern Merensky resources contributed to a 10.9% decline in mill throughput to 2.02Mt, in line with our expectations. Increased UG2 production (+3.8%) partly offset the 21% decline in high-grade Merensky tons on volumes, although head grade fell from 5.07g/t to 5.02g/t.

The decline in Merensky ore constrained feed through the smelter and onto the base- and precious-metal refineries, ultimately leading to a shortfall between PGMs in concentrate produced (293koz) and PGMs sold (276koz) of 16.9koz. This metal should be recovered as Merensky volumes increase.

The 9.7% decline in total PGMs in concentrate to 293koz is less than would be expected, given a 10.9% decline in tons milled and a 1% fall in grade, as it includes 10.9koz of recovered metal from reverts (retreated slag) and waste stockpiles.

Costs increased 19.5%, reflecting high industry-wide mining inflation and the impact of lost shifts (26) on total costs. Unit costs gained 34% to R804/t.

Northam Mine going forward

Following two disappointing years for Merensky production, we believe Northam may be able to stabilise the decline in Merensky volumes as the “deepening project” comes on line. This project involves an extension of the shaft infrastructure from level 12, via a decline shaft, to level 18. Development is currently progressing between 15 and 16 level and production has commenced on 14 level.

Each new level adds 2.5 years to the company’s LOM, which is defined by the Merensky resource, and compensates for the lost resources towards the east. This project could potentially extend Northam’s LOM to 25 years (from 16).

Despite this project, Merensky output is not expected to recover to previous levels of c125ktpm. We anticipate sustainable future Merensky volumes are likely to be closer to 100ktpm.

However, modifications to the UG2 plant allows for a higher proportion of UG2 production, partly offsetting the loss of Merensky tonnage, albeit at a cost to head grade. We expect UG2 volumes to be sustained around 85ktpm.

Figure 28. Northam Mine: Tons Milled (‘000)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY02A FY03A FY04A FY05A FY06A FY07A FY08E

MerenskyUG2

Source: Company Reports, Citi Investment Research

Figure 29. Northam Mine: Unit Costs

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

FY03A FY04A FY05A FY06A FY07A FY08E FY09E FY10E-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

VolumesCostsUnit Costs

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 20

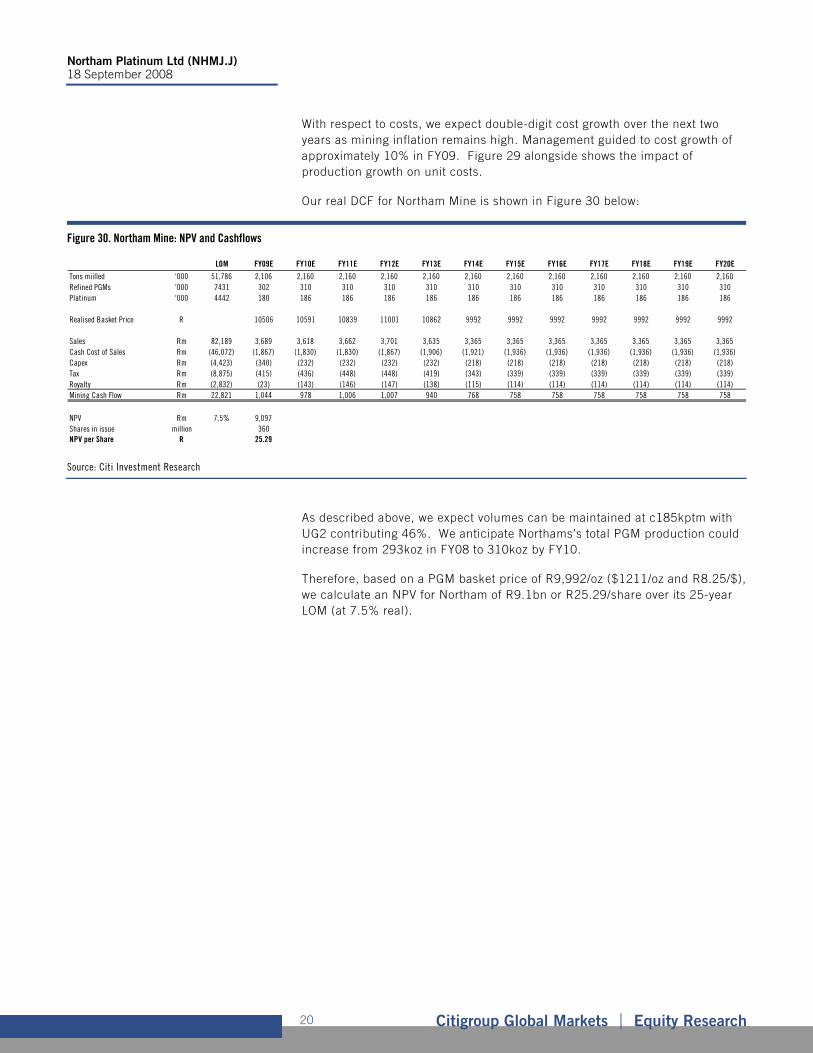

With respect to costs, we expect double-digit cost growth over the next two years as mining inflation remains high. Management guided to cost growth of approximately 10% in FY09. Figure 29 alongside shows the impact of production growth on unit costs.

Our real DCF for Northam Mine is shown in Figure 30 below:

Figure 30. Northam Mine: NPV and Cashflows

LOM FY09E FY10E FY11E FY12E FY13E FY14E FY15E FY16E FY17E FY18E FY19E FY20E

Tons miilled '000 51,786 2,106 2,160 2,160 2,160 2,160 2,160 2,160 2,160 2,160 2,160 2,160 2,160Refined PGMs '000 7431 302 310 310 310 310 310 310 310 310 310 310 310Platinum '000 4442 180 186 186 186 186 186 186 186 186 186 186 186

Realised Basket Price R 10506 10591 10839 11001 10862 9992 9992 9992 9992 9992 9992 9992

Sales Rm 82,189 3,689 3,618 3,662 3,701 3,635 3,365 3,365 3,365 3,365 3,365 3,365 3,365Cash Cost of Sales Rm (46,072) (1,867) (1,830) (1,830) (1,867) (1,906) (1,921) (1,936) (1,936) (1,936) (1,936) (1,936) (1,936)Capex Rm (4,423) (340) (232) (232) (232) (232) (218) (218) (218) (218) (218) (218) (218)Tax Rm (8,875) (415) (436) (448) (448) (419) (343) (339) (339) (339) (339) (339) (339)Royalty Rm (2,832) (23) (143) (146) (147) (138) (115) (114) (114) (114) (114) (114) (114)Mining Cash Flow Rm 22,821 1,044 978 1,006 1,007 940 768 758 758 758 758 758 758

NPV Rm 7.5% 9,097Shares in issue million 360NPV per Share R 25.29

Source: Citi Investment Research

As described above, we expect volumes can be maintained at c185kptm with UG2 contributing 46%. We anticipate Northams’s total PGM production could increase from 293koz in FY08 to 310koz by FY10.

Therefore, based on a PGM basket price of R9,992/oz ($1211/oz and R8.25/$), we calculate an NPV for Northam of R9.1bn or R25.29/share over its 25-year LOM (at 7.5% real).

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 21

Earnings Forecasts

The following considers the impact of our operational view (above) on earnings. Again, we anticipate Booysendal to be developed in a phased modular manner and base the following forecasts on the Modular scenario outlined above.

Figure 31 summarises our forecasts for combined production over the next four years and highlights that we anticipate no growth from Booysendal before FY12.

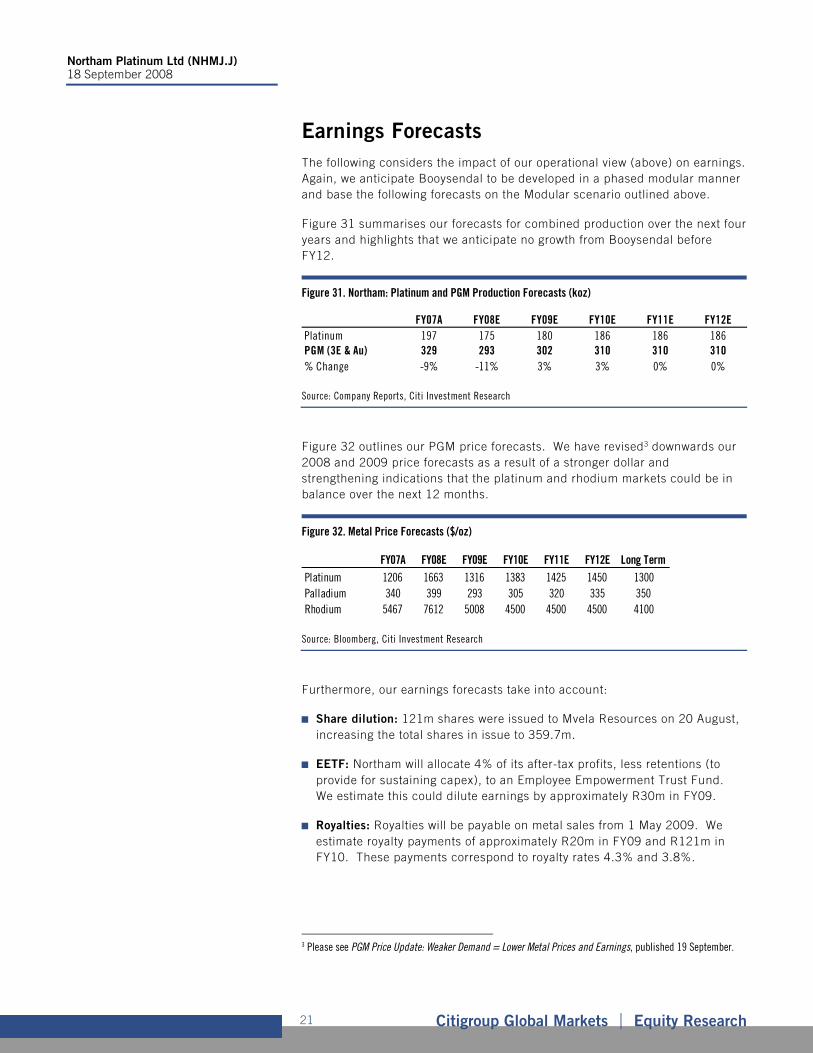

Figure 31. Northam: Platinum and PGM Production Forecasts (koz)

FY07A FY08E FY09E FY10E FY11E FY12EPlatinum 197 175 180 186 186 186PGM (3E & Au) 329 293 302 310 310 310% Change -9% -11% 3% 3% 0% 0%

Source: Company Reports, Citi Investment Research

Figure 32 outlines our PGM price forecasts. We have revised3 downwards our 2008 and 2009 price forecasts as a result of a stronger dollar and strengthening indications that the platinum and rhodium markets could be in balance over the next 12 months.

Figure 32. Metal Price Forecasts ($/oz)

FY07A FY08E FY09E FY10E FY11E FY12E Long TermPlatinum 1206 1663 1316 1383 1425 1450 1300Palladium 340 399 293 305 320 335 350Rhodium 5467 7612 5008 4500 4500 4500 4100

Source: Bloomberg, Citi Investment Research

Furthermore, our earnings forecasts take into account:

Share dilution: 121m shares were issued to Mvela Resources on 20 August, increasing the total shares in issue to 359.7m.

EETF: Northam will allocate 4% of its after-tax profits, less retentions (to provide for sustaining capex), to an Employee Empowerment Trust Fund. We estimate this could dilute earnings by approximately R30m in FY09.

Royalties: Royalties will be payable on metal sales from 1 May 2009. We estimate royalty payments of approximately R20m in FY09 and R121m in FY10. These payments correspond to royalty rates 4.3% and 3.8%.

3 Please see PGM Price Update: Weaker Demand = Lower Metal Prices and Earnings, published 19 September.

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 22

Pandora: The Pandora project is a venture between Anglo Platinum (42.5%), Lonmin (42.5%), Ba Bo Mogale (7.5%) and Mvela Resources (7.5%). Mvela will transfer its interest to Northam during FY09. The project produced 98k PGM ounces in the year ending September 2007 and 54k PGM oz during the nine months to end-June 2008. Pandora is managed by Lonmin, which purchases 100% of the ore mined for further processing.

A summary of our new earnings forecasts (reduced by 50% for FY09, 40% for FY10 and 195 for FY11) is given below.

Figure 33. Northam: Summarised Income Statement

FY07A FY08A FY09E FY10E FY11ESales Rm 3,740 3,886 3,689 3,724 3,881Cost of Sales Rm (1,728) (1,609) (2,207) (2,327) (2,434)Profit before tax Rm 2,101 2,359 1,571 1,443 1,477Tax Rm (775) (866) (483) (404) (414)Profit after tax Rm 1,326 1,493 1,089 1,039 1,064Attributable Profits Rm 1,326 1,493 1,059 1,008 1,033

Dividend Rm 1,245 1,011 529 504 516

Weighted average shares - diluted m 240 241 342 362 362

EPS R 5.53 6.21 3.10 2.78 2.85% Change 88% 12% -50% -10% 2%DPS R 5.26 4.25 1.55 1.39 1.43

Source: Company Reports, Citi Investment Research

As shown, we expect EPS to fall 50% to R3.10 in FY09. Figure 35 disaggregates this decline into the main factors affecting EPS.

Figure 34. Northam EPS (Rands) Figure 35. EPS: Reconciling FY08 EPS with FY09E

R 5.48

R 6.21

R 3.10R 2.78

3

4

5

6

7

FY07A FY08A FY09E FY10E

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

FY08

Inte

rest

& O

ther

STC

Reco

vere

d Sa

les

EETF

Cost

s

Pand

ora

Roya

lties

Prod

uctio

n

Met

al P

rices FX

New

Shar

es

FY09

Source: Company Reports, Citi Investment Research Source: Company Reports, Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 23

The primary reason for the fall in EPS is an anticipated 26% decline in the dollar PGM basket price and the impact of 121m new shares issued to Mvela Resources that increase the total shares in issue from 238m to 359m. In other words, these new shares automatically dilute earnings by 36%.

If we were to adjust for: shares in issue, metal prices and the rand/US dollar exchange rate (i.e. set their variables at FY08 levels), our FY09 EPS forecast would increase 4.5% to R6.49.

Cash Balance and Dividends

A decision to stagger expansion at Booysendal would not only mitigate some of the associated project risks but, by delaying development and therefore capital expenditure, also limit the company’s need to raise additional capital. We previously anticipated Northam would need to raise as much as R3bn to fund the expansion.

Under the Modular scenario outlined above, our cash flow model suggests that positive cash flows from Northam (Figure 36) will be sufficient to subsidise Booysendal’s expected capex requirements, with limited bridge funding (R1.6bn).

Furthermore, we expect Northam to continue paying dividends, albeit at a lower payout ratio while it funds Booysendal.

Figure 37 outlines our expected capex and dividend cash flows and their impact on the cash balance.

Figure 36. Northam Mine: Free Cash Flow (R million) Figure 37. Northam: Cash Flows (R millions)

0

100

200

300

400

500

600

700

800

900

1,000

FY09E FY10E FY11E FY12E FY13E FY14E FY15E

0

500

1,000

1,500

2,000

2,500

FY07A FY08A FY09E FY10E FY11E FY12E

Capex

Dividend

Cash Balance

Source: Citi Investment Research Source: Company Reports, Citi Investment Research

Mvela shares automatically dilute EPS by

36%

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 24

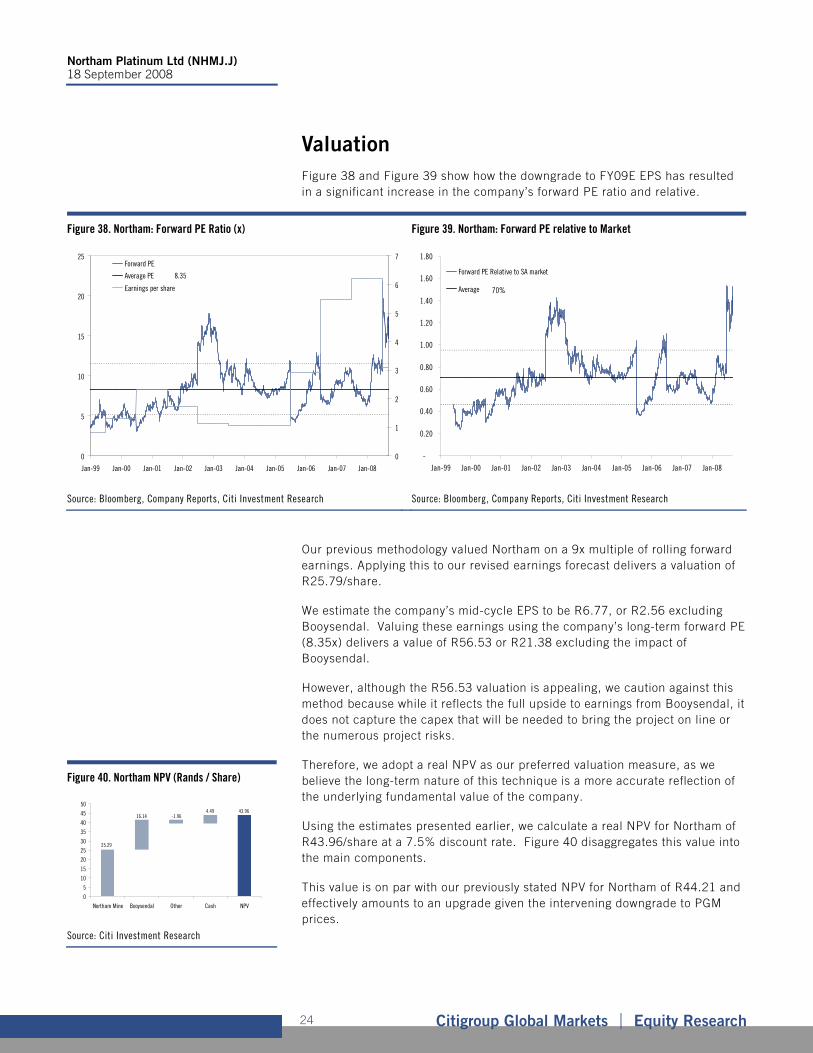

Valuation

Figure 38 and Figure 39 show how the downgrade to FY09E EPS has resulted in a significant increase in the company’s forward PE ratio and relative.

Figure 38. Northam: Forward PE Ratio (x) Figure 39. Northam: Forward PE relative to Market

8.35

0

5

10

15

20

25

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

0

1

2

3

4

5

6

7Forward PE

Average PE

Earnings per share 70%

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Forward PE Relative to SA market

Average

Source: Bloomberg, Company Reports, Citi Investment Research Source: Bloomberg, Company Reports, Citi Investment Research

Our previous methodology valued Northam on a 9x multiple of rolling forward earnings. Applying this to our revised earnings forecast delivers a valuation of R25.79/share.

We estimate the company’s mid-cycle EPS to be R6.77, or R2.56 excluding Booysendal. Valuing these earnings using the company’s long-term forward PE (8.35x) delivers a value of R56.53 or R21.38 excluding the impact of Booysendal.

However, although the R56.53 valuation is appealing, we caution against this method because while it reflects the full upside to earnings from Booysendal, it does not capture the capex that will be needed to bring the project on line or the numerous project risks.

Therefore, we adopt a real NPV as our preferred valuation measure, as we believe the long-term nature of this technique is a more accurate reflection of the underlying fundamental value of the company.

Using the estimates presented earlier, we calculate a real NPV for Northam of R43.96/share at a 7.5% discount rate. Figure 40 disaggregates this value into the main components.

This value is on par with our previously stated NPV for Northam of R44.21 and effectively amounts to an upgrade given the intervening downgrade to PGM prices.

Figure 40. Northam NPV (Rands / Share)

0

5

10

15

20

25

30

35

40

45

50

Northam Mine Booysendal Other Cash NPV

25.29

16.14 -1.964.49 43.96

Source: Citi Investment Research

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 25

The DCF does not include proceeds from any transaction relating to the southern part of Booysendal. We estimated this could potentially add R5/share to our valuation.

We set our new target price at R44, in line with our DCF valuation.

Recommendation

The following table summarises the factors impacting our recommendation:

Negative Positive

Earnings momentum: A significant decline in earnings in the current market environment may add a further risk premium to Northam’s valuation.

Attractive P/NPV: Amongst its peers, Northam trades at the lowest premium to NPV.

NPV at Spot: At spot prices, Northam’s NPV is R29.67/share, 42% lower than current market prices.

Takeover Premium: The overhang of a bid from Impala is likely to support near-term prices.

Dividends to be cut: Northam’s dividend is likely to suffer the double blow of lower earnings and a higher dividend cover multiple.

Booysendal South: We estimate the southern section of Booysendal could add R5/share to Northam’s valuation.

Booysendal fully priced in: We believe the full upside of Booysendal is priced into Northam’s valuation. This is aggressive given the risks and uncertainties of this project.

We are not convinced the above supports an upgrade to our recommendation while Northam’s near-term earnings remain dependent on a single operation. We therefore maintain our Sell/High Risk (3H) recommendation on Northam.

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 26

Northam Platinum Ltd

Company description

Northam Platinum is South Africa's fifth-largest platinum producer and operates the world's deepest platinum mine on the western limb of the Bushveld Complex. The company has its own processing capacity and outsources final refining under a long-term agreement to a third party.

Investment strategy

Northam's earnings are driven by international PGM metal prices and the rand/US dollar exchange rate. PGM prices have increased significantly over the past six years and, while we expect long-term prices to remain high, we believe the industry is discounting current spot prices. It is our view that this is unsustainable and that prices will moderate over the next three to four years. Furthermore, higher commodity prices have led Northam's earnings to cyclical highs while the company's earnings multiples, relative to the overall South African market, are in line with long-term averages. We therefore believe that earnings are at the top of their cycle while the market is showing mid-cycle valuations. We rate Northam Sell/High Risk (3H).

Valuation

We base our valuation of Northam on separate real discounted cash flow models for its Northam (R25.29/share) and Booysendal operations (R16.14/share). In our view, this method takes into account the long-term nature of a mining project. The DCF is discounted at 7.5% pa.

We also value Northam based on forward multiples of rolling earnings 12 months forward and mid-cycle earnings. However, we suggest this methodology fails to capture: (1) the benefit of future earnings from Booysendal; or (2) the capex necessary to bring Booysendal into production.

Risks

We rate Northam High Risk. As a single mine operation, Northam is exposed to numerous operational risk factors that may negatively impact the company's ability to maintain or grow production. Furthermore the company is the industry's highest-cost producer and is therefore vulnerable to falling commodity prices or an appreciation of the rand against the US dollar. While Northam is expected to start development of a new mine, Booysendal, which will in the long term diversify its operations and reduce overall costs, it is our opinion that the near-term execution risk outweighs these long-term benefits. The key risk to our target price would be PGM prices significantly above our forecasts or a weaker rand than expected.

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 27

Appendix A-1 Analyst Certification

Each research analyst(s) principally responsible for the preparation and content of all or any identified portion of this research report hereby certifies that, with respect to each issuer or security or any identified portion of the report with respect to an issuer or security that the research analyst covers in this research report, all of the views expressed in this research report accurately reflect their personal views about those issuer(s) or securities. Each research analyst(s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendation(s) or view(s) expressed by that research analyst in this research report.

IMPORTANT DISCLOSURES

0

20

40

60

80

O N D J2006

F M A M J J A S O N D J2007

F M A M J J A S O N D J2008

F M A M J J A S

12 3

4 56

78

9

10

# Date RatingTargetPrice

ClosingPrice

1: 18 Oct 05 3H *15.22 17.202: 8 Nov 05 3H *16.31 17.103: 16 Jan 06 3H *17.40 24.004: 25 Jan 06 3H *19.93 23.155: 31 Mar 06 *2H *29.45 31.006: 11 May 06 2H *40.46 38.007: 14 Jul 06 *3H *44.00 42.348: 1 Sep 06 Coverage suspended9: 4 Oct 07 *3H *38.95 47.97

10: 14 Apr 08 3H *41.26 69.50*Indicates change.

Northam Platinum Ltd (NHMJ.J)Ratings and Target Price History - Fundamental ResearchAnalyst: Gerhard Engelbrecht (covered since October 5 2007) ZAR

CoveredNot covered Rating/target price changes above reflect Eastern Standard Time

Chart current as of 13 S

eptember 2008

Analysts' compensation is determined based upon activities and services intended to benefit the investor clients of Citigroup Global Markets Inc. and its affiliates ("the Firm"). Like all Firm employees, analysts receive compensation that is impacted by overall firm profitability, which includes revenues from, among other business units, the Private Client Division, Institutional Sales and Trading, and Investment Banking.

For important disclosures (including copies of historical disclosures) regarding the companies that are the subject of this Citi Investment Research product ("the Product"), please contact Citi Investment Research, 388 Greenwich Street, 29th Floor, New York, NY, 10013, Attention: Legal/Compliance. In addition, the same important disclosures, with the exception of the Valuation and Risk assessments and historical disclosures, are contained on the Firm's disclosure website at www.citigroupgeo.com. Private Client Division clients should refer to www.smithbarney.com/research. Valuation and Risk assessments can be found in the text of the most recent research note/report regarding the subject company. Historical disclosures (for up to the past three years) will be provided upon request.

Citi Investment Research Ratings Distribution Data current as of 30 June 2008 Buy Hold SellCiti Investment Research Global Fundamental Coverage (3096) 50% 36% 14%

% of companies in each rating category that are investment banking clients 53% 52% 42%Guide to Fundamental Research Investment Ratings: Citi Investment Research's stock recommendations include a risk rating and an investment rating. Risk ratings, which take into account both price volatility and fundamental criteria, are: Low (L), Medium (M), High (H), and Speculative (S). Investment ratings are a function of Citi Investment Research's expectation of total return (forecast price appreciation and dividend yield within the next 12 months) and risk rating. For securities in emerging markets (Asia Pacific, Emerging Europe/Middle East/Africa, and Latin America), investment ratings are: Buy (1) (expected total return of 15% or more for Low-Risk stocks, 20% or more for Medium-Risk stocks, 30% or more for High-Risk stocks, and 40% or more for Speculative stocks); Hold (2) (5%-15% for Low-Risk stocks, 10%-20% for Medium-Risk stocks, 15%-30% for High-Risk stocks, and 20%-40% for Speculative stocks); and Sell (3) (5% or less for Low-Risk stocks, 10% or less for Medium-Risk stocks, 15% or less for High-Risk stocks, and 20% or less for Speculative stocks). Investment ratings are determined by the ranges described above at the time of initiation of coverage, a change in investment and/or risk rating, or a change in target price (subject to limited management discretion). At other times, the expected total returns may fall outside of these ranges because of market price movements and/or other short-term volatility or trading patterns. Such interim deviations from specified ranges will be permitted but will become subject to review by Research Management. Your decision to buy or sell a security should be based upon your personal investment objectives and should be made only after evaluating the stock's expected performance and risk.

Guide to Corporate Bond Research Credit Opinions and Investment Ratings: Citi Investment Research's corporate bond research issuer publications include a fundamental credit opinion of Improving, Stable or Deteriorating and a complementary risk rating of Low (L), Medium (M), High (H) or Speculative (S) regarding the credit risk of the company featured in the report. The fundamental credit opinion reflects the CIR analyst's opinion of the direction of credit fundamentals of the issuer without respect to securities market vagaries. The fundamental credit opinion is not geared to, but should be viewed in the context of, debt ratings issued by major public debt ratings companies such as Moody's Investors Service, Standard and Poor's, and Fitch Ratings. CBR risk ratings are approximately equivalent to the following matrix: Low Risk -- Triple A to Low Double A; Low to Medium Risk -- High Single A through High Triple B; Medium to High Risk -- Mid Triple B through High Double B; High to Speculative

Northam Platinum Ltd (NHMJ.J) 18 September 2008

Citigroup Global Markets Equity Research 28

Risk -- Mid Double B and Below. The risk rating element illustrates the analyst's opinion of the relative likelihood of loss of principal when a fixed income security issued by a company is held to maturity, based upon both fundamental and market risk factors. Certain reports published by Citi Investment Research will also include investment ratings on specific issues of companies under coverage which have been assigned fundamental credit opinions and risk ratings. Investment ratings are a function of Citi Investment Research's expectations for total return, relative return (relative to the performance of relevant Citi bond indices), and risk rating. These investment ratings are: Buy/Overweight -- the bond is expected to outperform the relevant Citigroup bond market sector index (Broad Investment Grade, High Yield Market or Emerging Market); Hold/Neutral Weight -- the bond is expected to perform in line with the relevant Citigroup bond market sector index; or Sell/Underweight -- the bond is expected to underperform the relevant Citigroup bond market sector index. Performance data for Citi bond indices are updated monthly, are available upon request and can also be viewed at http://sd.ny.ssmb.com/ using the "Indexes" tab.

OTHER DISCLOSURES The subject company's share price set out on the front page of this Product is quoted as at 18 September 2008 01:19 PM on the issuer's primary market.

For securities recommended in the Product in which the Firm is not a market maker, the Firm is a liquidity provider in the issuers' financial instruments and may act as principal in connection with such transactions. The Firm is a regular issuer of traded financial instruments linked to securities that may have been recommended in the Product. The Firm regularly trades in the securities of the subject company(ies) discussed in the Product. The Firm may engage in securities transactions in a manner inconsistent with the Product and, with respect to securities covered by the Product, will buy or sell from customers on a principal basis.

Securities recommended, offered, or sold by the Firm: (i) are not insured by the Federal Deposit Insurance Corporation; (ii) are not deposits or other obligations of any insured depository institution (including Citibank); and (iii) are subject to investment risks, including the possible loss of the principal amount invested. Although information has been obtained from and is based upon sources that the Firm believes to be reliable, we do not guarantee its accuracy and it may be incomplete and condensed. Note, however, that the Firm has taken all reasonable steps to determine the accuracy and completeness of the disclosures made in the Important Disclosures section of the Product. The Firm's research department has received assistance from the subject company(ies) referred to in this Product including, but not limited to, discussions with management of the subject company(ies). Firm policy prohibits research analysts from sending draft research to subject companies. However, it should be presumed that the author of the Product has had discussions with the subject company to ensure factual accuracy prior to publication. All opinions, projections and estimates constitute the judgment of the author as of the date of the Product and these, plus any other information contained in the Product, are subject to change without notice. Prices and availability of financial instruments also are subject to change without notice. Notwithstanding other departments within the Firm advising the companies discussed in this Product, information obtained in such role is not used in the preparation of the Product. Although Citi Investment Research does not set a predetermined frequency for publication, if the Product is a fundamental research report, it is the intention of Citi Investment Research to provide research coverage of the/those issuer(s) mentioned therein, including in response to news affecting this issuer, subject to applicable quiet periods and capacity constraints. The Product is for informational purposes only and is not intended as an offer or solicitation for the purchase or sale of a security. Any decision to purchase securities mentioned in the Product must take into account existing public information on such security or any registered prospectus.

Investing in non-U.S. securities, including ADRs, may entail certain risks. The securities of non-U.S. issuers may not be registered with, nor be subject to the reporting requirements of the U.S. Securities and Exchange Commission. There may be limited information available on foreign securities. Foreign companies are generally not subject to uniform audit and reporting standards, practices and requirements comparable to those in the U.S. Securities of some foreign companies may be less liquid and their prices more volatile than securities of comparable U.S. companies. In addition, exchange rate movements may have an adverse effect on the value of an investment in a foreign stock and its corresponding dividend payment for U.S. investors. Net dividends to ADR investors are estimated, using withholding tax rates conventions, deemed accurate, but investors are urged to consult their tax advisor for exact dividend computations. Investors who have received the Product from the Firm may be prohibited in certain states or other jurisdictions from purchasing securities mentioned in the Product from the Firm. Smith Barney clients can ask their Financial Advisor for additional details. Citigroup Global Markets Inc. takes responsibility for the Product in the United States. Any orders by US investors resulting from the information contained in the Product may be placed only through Citigroup Global Markets Inc.