North American Nitrogen Outlook - Fertilizer Industry … 2016 - North... · · 2017-01-16North...

27

North American Nitrogen Outlook TFI Outlook November 2016 Doug Hoadley Hoadley Consulting

Transcript of North American Nitrogen Outlook - Fertilizer Industry … 2016 - North... · · 2017-01-16North...

North American

Nitrogen Outlook

TFI Outlook

November 2016

Doug Hoadley

Hoadley Consulting

Hoadley Consulting: Over 25 years of

experience in the fertilizer industry

Expert on the nitrogen, phosphates and potash industries

Detailed knowledge of the competitive situation for North

America

Global competitive costs analysis for N, P & K

Feasibility studies for new projects, expansions and M&A

Strategic planning

Economic and marketing analysis

+1-847-636-1747

Agenda

Demand Outlook

Changes to Capacity

Ammonia Outlook

Urea Outlook

UAN Outlook

Summary

Hoadley Consulting

Key Nitrogen Drivers

Low grain prices = slow demand growth

New nitrogen capacity puts pressures prices

Collapse in energy values plus currency devaluations results in lower costs for marginal producers

Cash costs for most producers have fallen

Cheap freight shrinks the globe

China, China, China

Hoadley Consulting

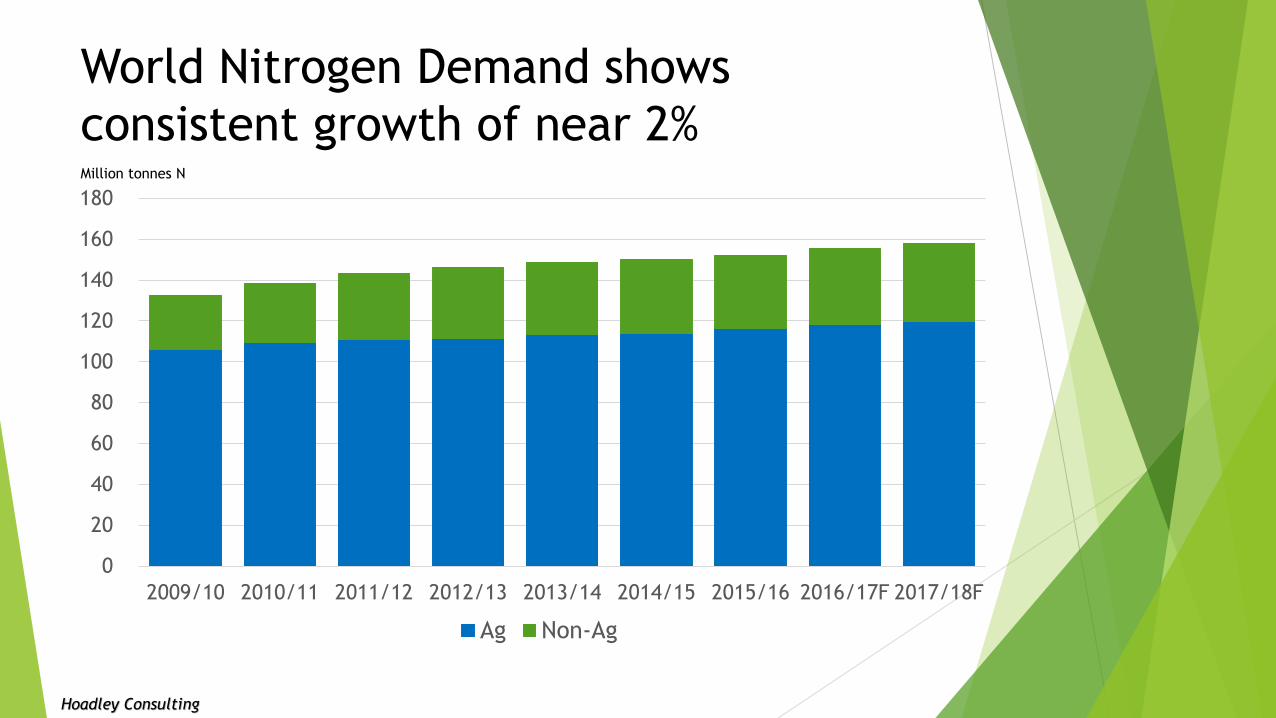

World Nitrogen Demand shows

consistent growth of near 2%

0

20

40

60

80

100

120

140

160

180

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F 2017/18F

Ag Non-Ag

Million tonnes N

Hoadley Consulting

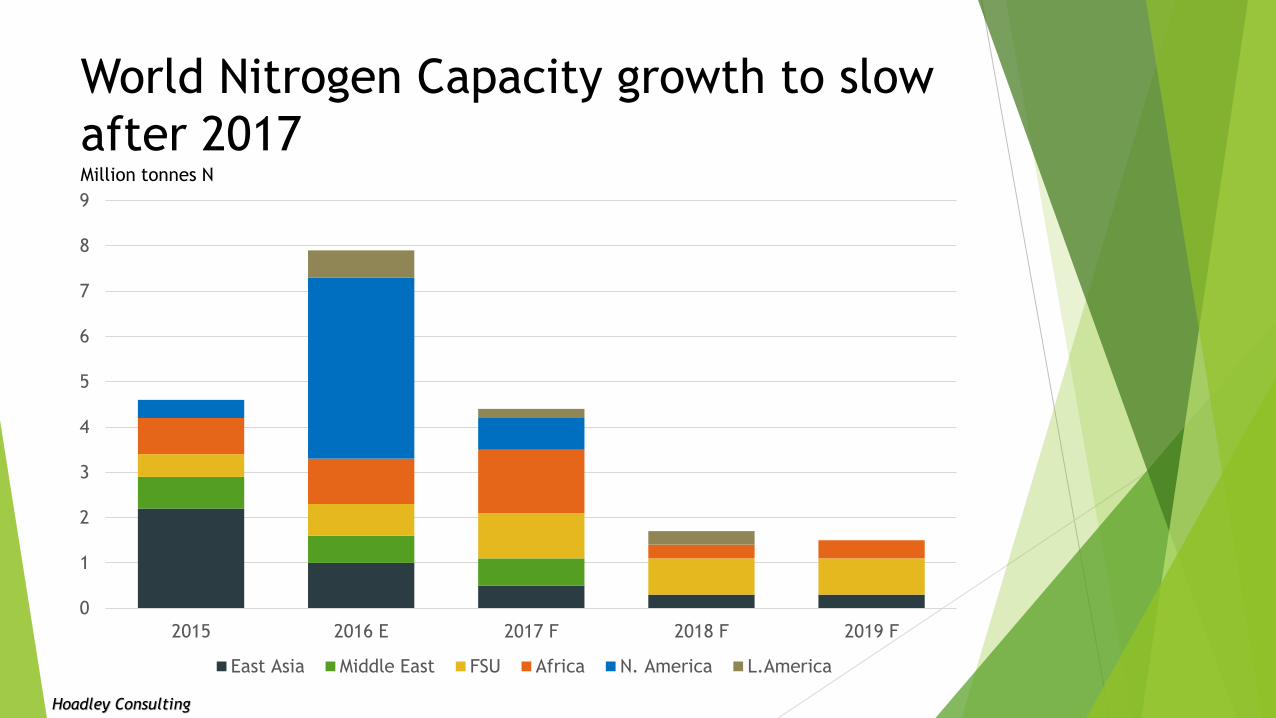

World Nitrogen Capacity growth to slow

after 2017

0

1

2

3

4

5

6

7

8

9

2015 2016 E 2017 F 2018 F 2019 F

East Asia Middle East FSU Africa N. America L.America

Hoadley Consulting

Million tonnes N

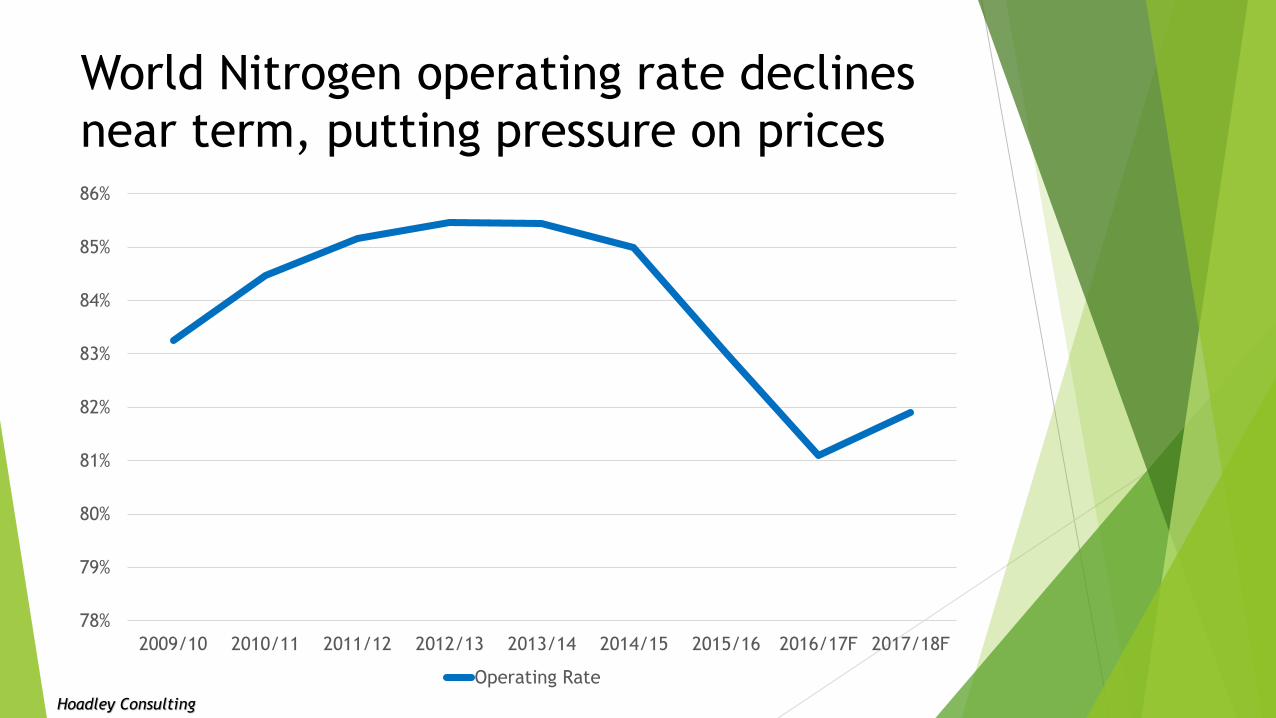

World Nitrogen operating rate declines

near term, putting pressure on prices

78%

79%

80%

81%

82%

83%

84%

85%

86%

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F 2017/18F

Operating Rate

Hoadley Consulting

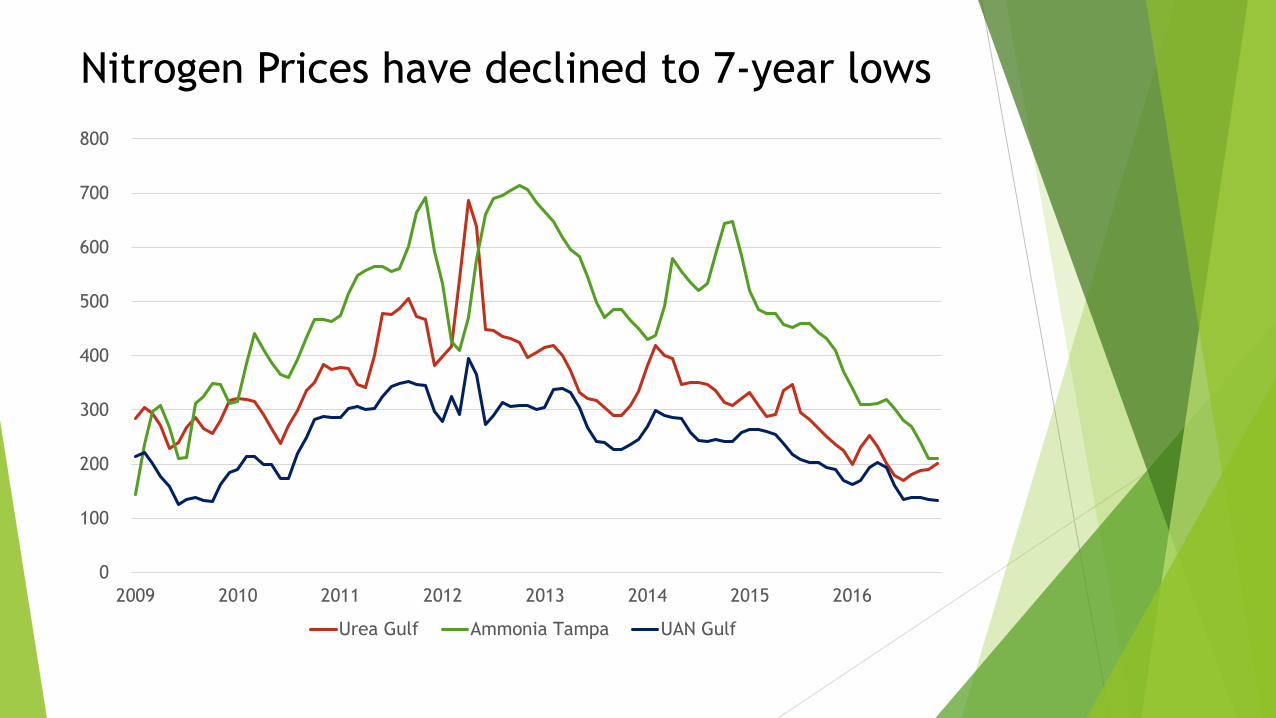

Nitrogen Prices have declined to 7-year lows

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013 2014 2015 2016

Urea Gulf Ammonia Tampa UAN Gulf

USA nitrogen fertilizer demand forecast

to decline 1% to 2% next year

0

2

4

6

8

10

12

14

2013/14 2014/15 2015/16E 2016/17F

Ammonia Urea UAN Other

Million tons N

Hoadley Consulting

North American Nitrogen Capacity

growth peaks in 2016/17

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Ammonia Urea UAN

2015/16 2016/17F 2017/18F

Hoadley Consulting

Million tons

Ammonia Situation and Outlook

Hoadley Consulting

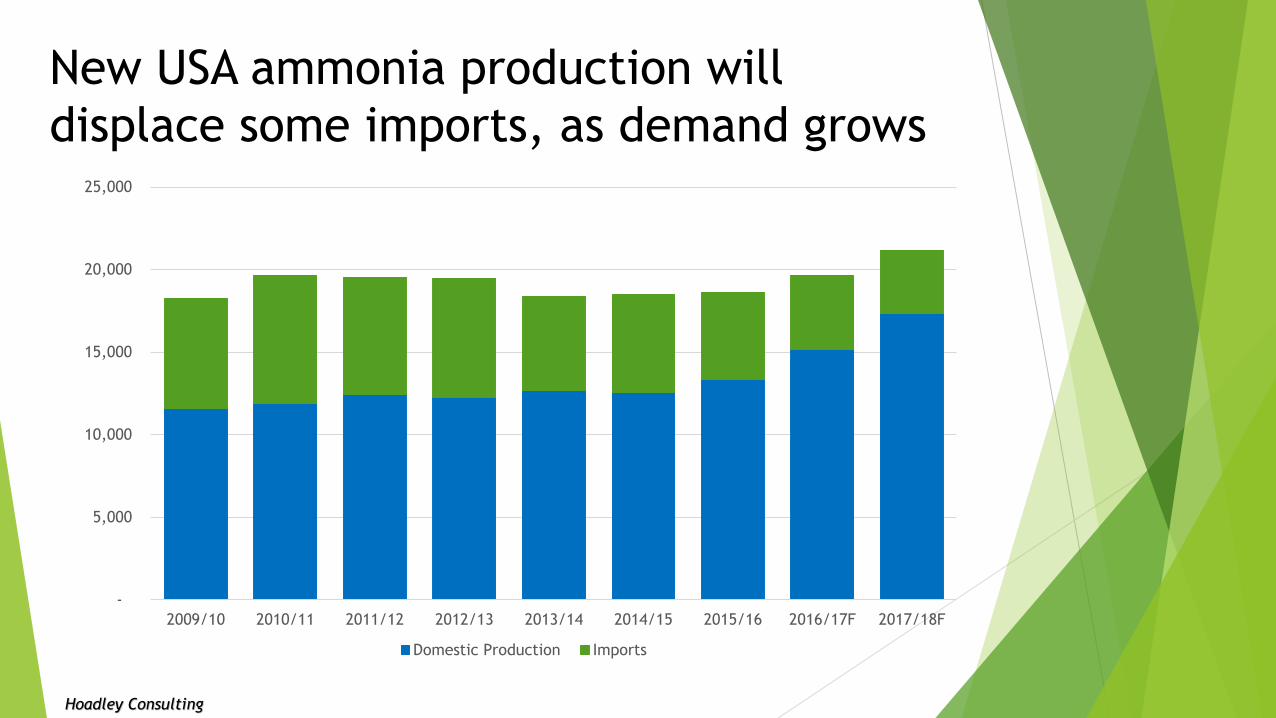

New USA ammonia production will

displace some imports, as demand grows

-

5,000

10,000

15,000

20,000

25,000

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F 2017/18F

Domestic Production Imports

Hoadley Consulting

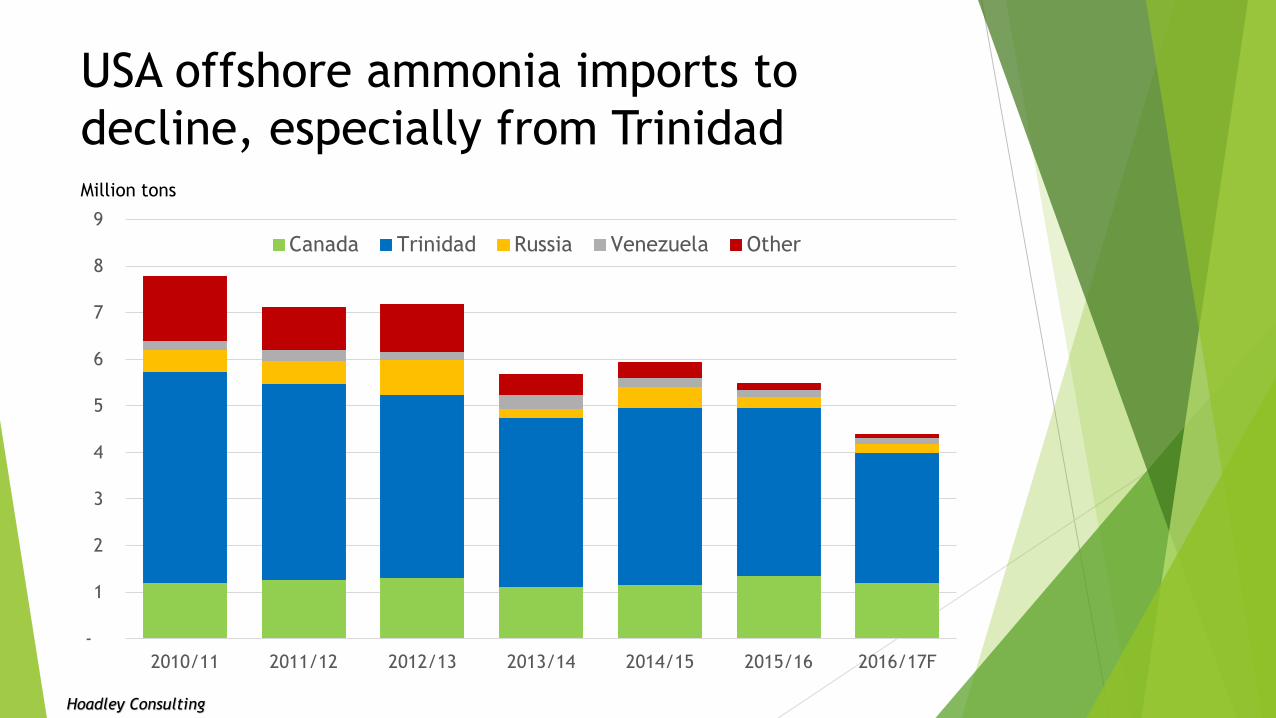

USA offshore ammonia imports to

decline, especially from Trinidad

-

1

2

3

4

5

6

7

8

9

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F

Canada Trinidad Russia Venezuela Other

Million tons

Hoadley Consulting

2015/16 Ammonia Cost Curve based on

USA supply

Hoadley Consulting

USA Production

Trinidad

imports

How high will offshore USA Ammonia

exports grow?

-

50

100

150

200

250

300

2012/13 2013/14 2014/15 2015/16 2016/17F

Latin America Canada W. Europe Morocco Other

Hoadley Consulting

Urea Situation and Outlook

Hoadley Consulting

New USA urea production will displace about

half of current imports by 2017/18

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F 2017/18F

Domestic Production Imports

Hoadley Consulting

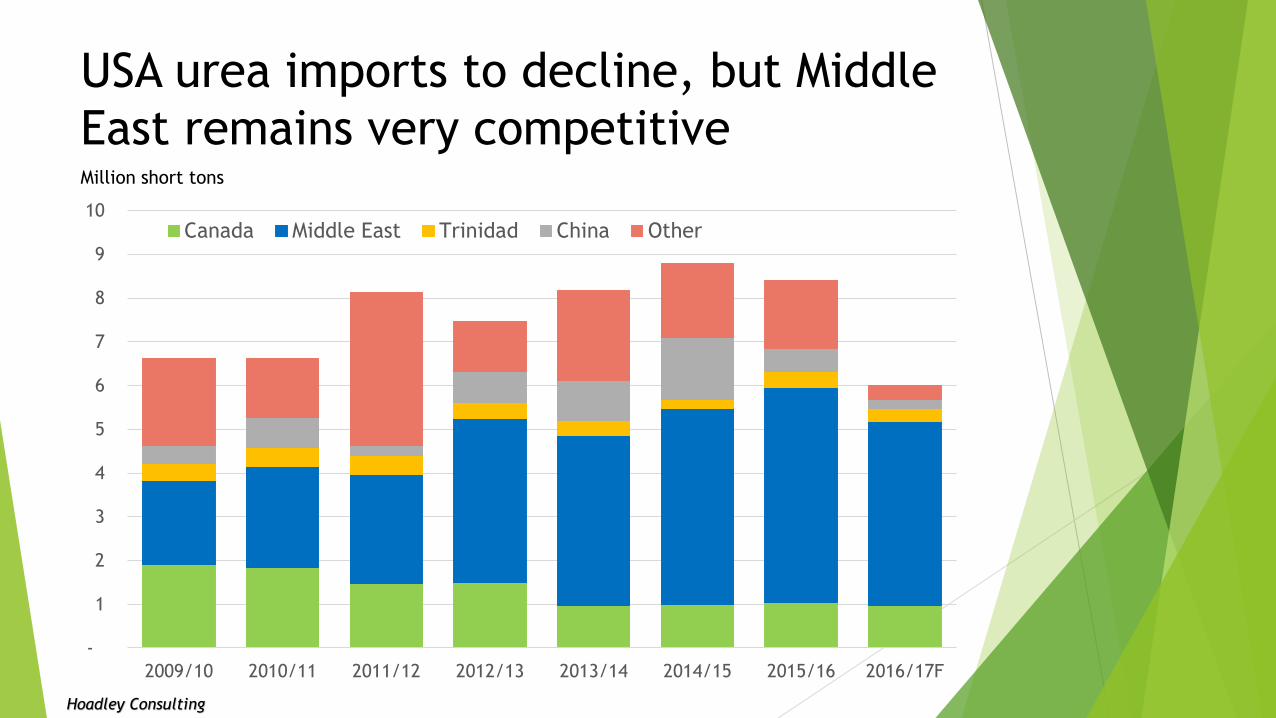

USA urea imports to decline, but Middle

East remains very competitive

-

1

2

3

4

5

6

7

8

9

10

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F

Canada Middle East Trinidad China Other

Million short tons

Hoadley Consulting

2015/16 Urea Cost Curve based on

USA supply

Hoadley Consulting

USA

productionMiddle East

imports

Will Offshore USA Urea exports increase?

-

50

100

150

200

250

300

350

400

450

2012/13 2013/14 2014/15 2015/16

Latin America Canada W. Europe Other

Hoadley Consulting

UAN Situation and Outlook

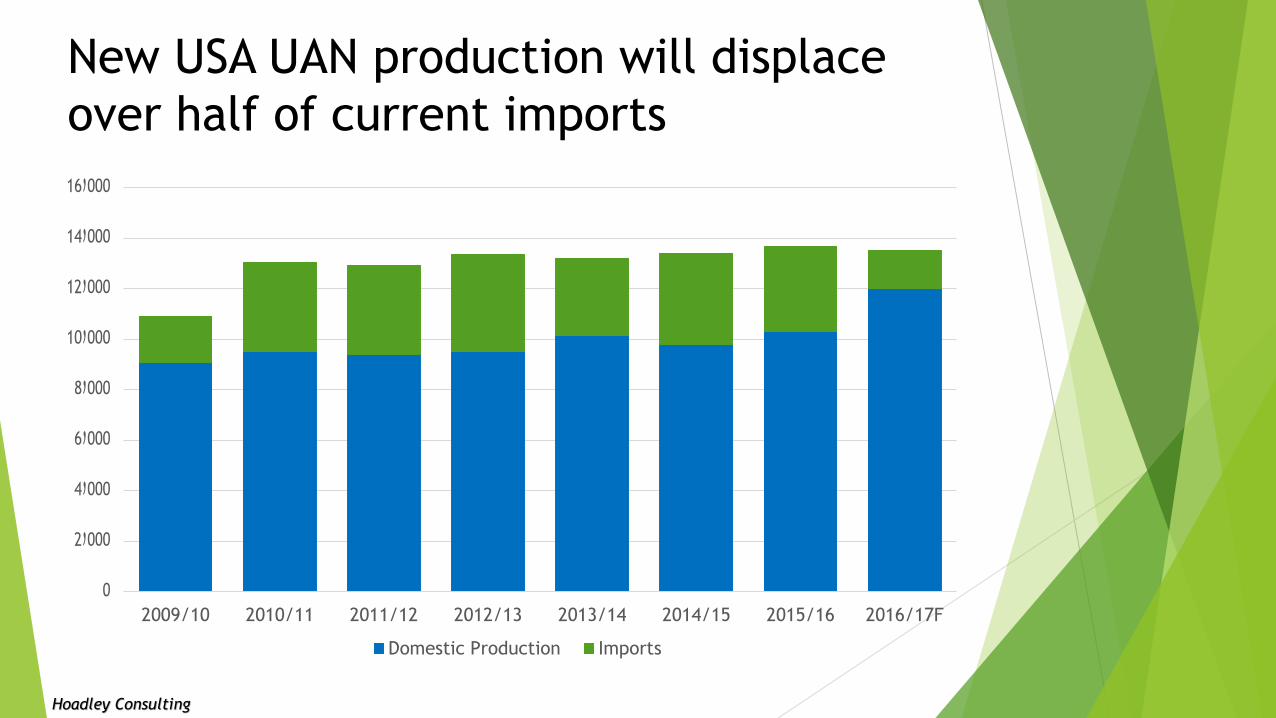

New USA UAN production will displace

over half of current imports

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F

Domestic Production Imports

Hoadley Consulting

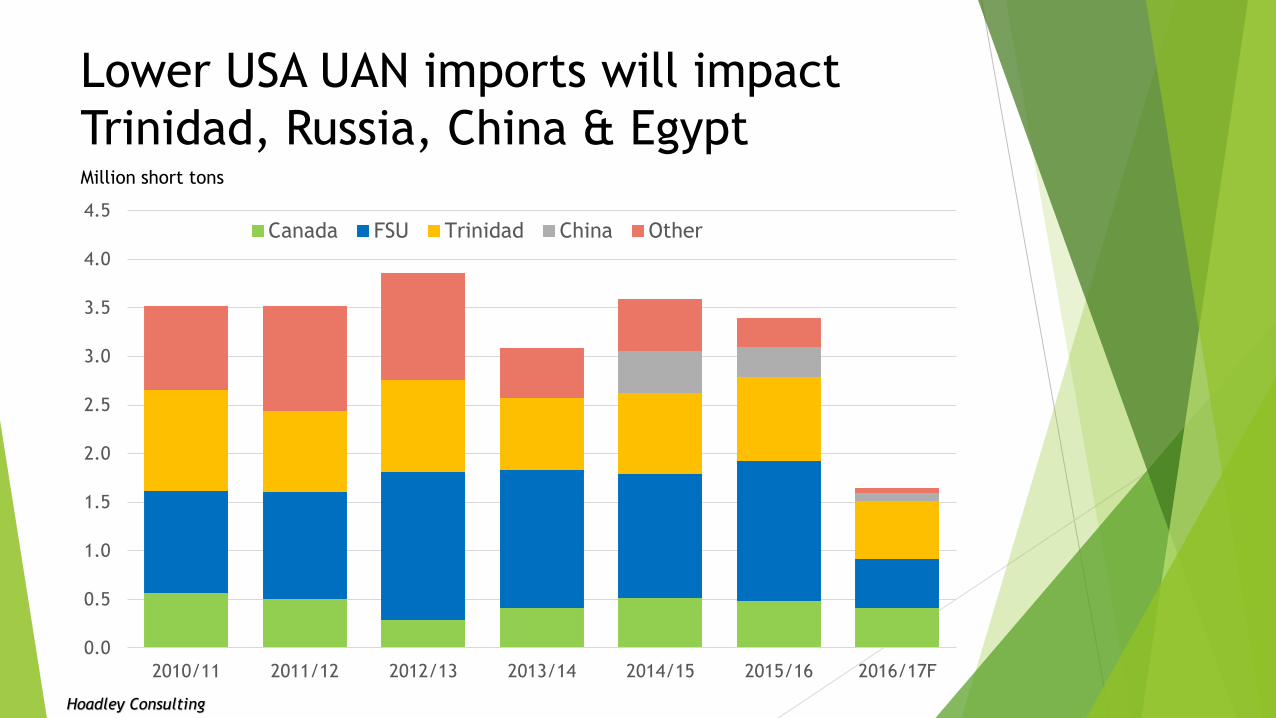

Lower USA UAN imports will impact

Trinidad, Russia, China & Egypt

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F

Canada FSU Trinidad China Other

Million short tons

Hoadley Consulting

2015/16 UAN Cost Curve based on supply

to North America

Hoadley Consulting

North American production

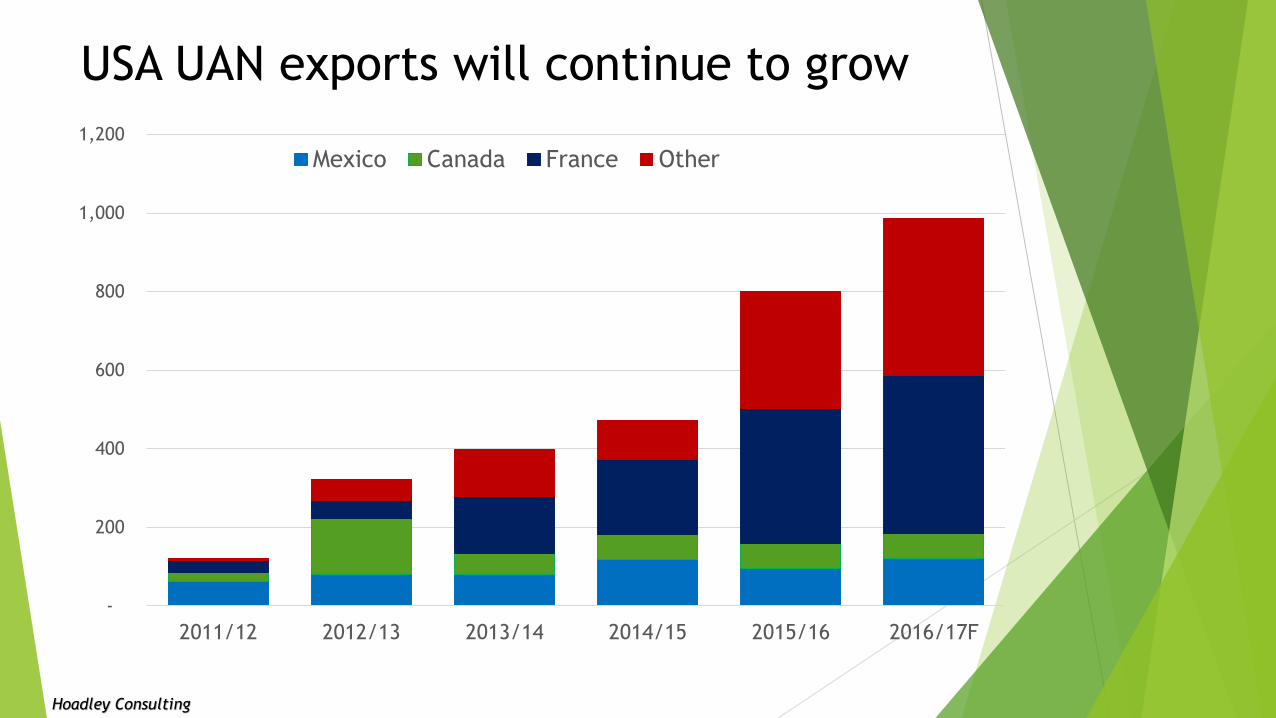

USA UAN exports will continue to grow

-

200

400

600

800

1,000

1,200

2011/12 2012/13 2013/14 2014/15 2015/16 2016/17F

Mexico Canada France Other

Hoadley Consulting

Summary

New nitrogen capacity peaks in 2016; the global balance starts to return in

2018 and 2019

Fertilizer demand growth will be slow unless grain prices rally; industrial

growth should remain strong

New capacity, lower energy values and currency devaluations has put pressure

on nitrogen fertilizer prices

The cash cost of the marginal supplier to the USA will decline as high-cost

suppliers are no longer competitive

New North American production will result in lower ammonia, urea and UAN

offshore imports, but….imports will continue

USA offshore exports will expand for UAN & ammonia and probably urea

Hoadley Consulting

Appendix Sources are mainly TFI, IFA, & Company Reports

Forecasts are by Hoadley Consulting

Years are USA fertilizer years (July-June)

Data are short tons, mostly in ‘000 except where noted otherwise

Costs are US$/ton, delivered to US Gulf for Offshore suppliers

We do not guarantee the accuracy of any assumptions, data or forecasts

More questions? Call Doug at +1-847-636-1747

Go Cubs!

Hoadley Consulting