Norad Report Bmmp

60

Private Sector Development Program in Bangladesh Assessment of Business Conditions and Sector Potentials

-

Upload

mosannef-hossain-bhuiya -

Category

Documents

-

view

54 -

download

1

Transcript of Norad Report Bmmp

PrivateSectorDevelopmentPrograminBangladesh

AssessmentofBusinessConditionsandSectorPotentials

2

ACKNOWLEDGEMENTS.................................................................................................................................4

LISTOFACRONYMS .......................................................................................................................................4

EXECUTIVESUMMARY..................................................................................................................................6

1.0INTRODUCTION .......................................................................................................................................81.2METHODOLOGY ............................................................................................................................................9

2.0THEBUSINESSFRAMEWORKINBANGLADESH.......................................................................... 102.1CORPORATESOCIALRESPONSIBILITY(CSR) .......................................................................................... 102.2PUBLICPRIVATEPARTNERSHIP(PPP)................................................................................................... 12

3.0SECTORSPECIFICISSUES ................................................................................................................... 13

3.1ICT ............................................................................................................................................................. 133.1.1ABOUTTHEMARKET.............................................................................................................................. 133.1.2BENEFITSANDCHALLENGES .................................................................................................................. 143.1.3DOINGBUSINESSINTHEICTSECTOR ................................................................................................... 153.1.4INTERNETCONNECTION ......................................................................................................................... 163.1.5OUTSOURCINGOFSERVICES................................................................................................................... 16

3.2ENERGYANDPOWERPRODUCTION.............................................................................................. 173.2.1REHABILITATIONOFOLDPOWERPLANTS .......................................................................................... 193.2.3OIL,GASANDCOAL................................................................................................................................ 193.2.4RENEWABLEENERGY............................................................................................................................. 213.2.5GOVERNMENTPOLICIES......................................................................................................................... 223.2.6THETYPICALINVESTMENTROUTEFORPOWERGENERATION .......................................................... 223.2.7BUSINESSOPPORTUNITIESINTHEPOWERANDENERGYSECTOR...................................................... 23

3.3SHIPBUILDINGANDMARITIMERELATEDACTIVITIES ........................................................... 233.3.1PLANSFORTHEBANGLADESHISHIPBUILDINGSECTOR ...................................................................... 233.3.2ENTERINGTHEINTERNATIONALMARKET ............................................................................................ 243.3.3WHATCANBANGLADESHOFFER?......................................................................................................... 243.3.4BUSINESSOPPORTUNITIES .................................................................................................................... 25

3.4MARINEACTIVITIES ............................................................................................................................ 253.4.1MARINECAPTUREFISHERIES................................................................................................................. 263.4.2SHRIMPS ................................................................................................................................................. 273.4.3FISHFEEDANDHEALTHANDSAFETYISSUES ........................................................................................ 283.4.4BUSINESSOPPORTUNITIES .................................................................................................................... 28

3.5TRADEOFMANUFACTUREDGOODS.............................................................................................. 293.5.1TRANSPORTANDSHIPMENT.................................................................................................................. 293.5.2READYMADEGARMENTS(RMG) .......................................................................................................... 293.5.3HOMETEXTILES ..................................................................................................................................... 303.5.4PHARMACEUTICALS ............................................................................................................................... 313.5.5OTHERSECTORS ..................................................................................................................................... 31

3

4.0THEB2BPROGRAM............................................................................................................................. 324.1TELENORASA“HANDHOLDER”................................................................................................................ 324.2LEARNINGEXPERIENCEFROMTHEDANISHB2B .................................................................................... 32

5.0CONCLUSIONSANDRECOMMENDATIONS.................................................................................... 335.1BUSINESSFRAMEWORK ............................................................................................................................ 335.2 SECTORISSUES ....................................................................................................................................... 345.2.1ICT................................................................................................................................................................................ 345.2.2ENERGYANDPOWERPRODUCTION ........................................................................................................................ 345.2.3SHIPBUILDING............................................................................................................................................................ 355.2.4MARINEACTIVITIES................................................................................................................................................... 355.2.5TRADINGWITHMANUFACTUREDGOODS............................................................................................................... 365.3PROGRAMISSUES ....................................................................................................................................... 36

6.0REFERENCESANDINFORMATION: ................................................................................................. 38TENDERINFO .................................................................................................................................................... 38REFERENCESMADETOWEBSITESANDPUBLICATIONS................................................................................... 38

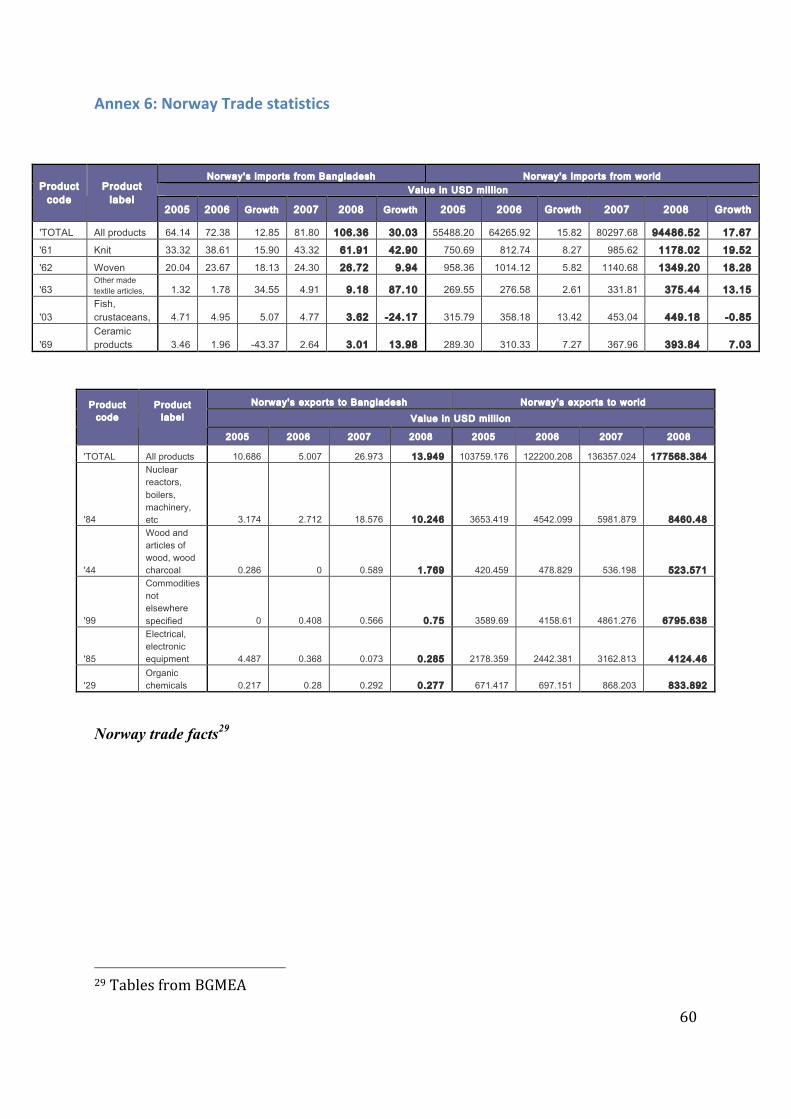

7.0ANNEXES ................................................................................................................................................. 40ANNEX1INFORMATIONGATHERING .............................................................................................................. 40ANNEX2TERMSOFREFERENCE ...................................................................................................................... 43ANNEX3:ROADMAPFORBUSINESSENTRYINBANGLADESH........................................................................ 46APRACTICALROUTEFORNORWEGIANBUSINESSES....................................................................................... 46INCORPORATINGACOMPANY ............................................................................................................................................. 46LIMITEDCOMPANIES............................................................................................................................................................ 47REGISTRATION.................................................................................................................................................. 47TIMEFRAMEANDCOSTSINVOLVEDINOBTAININGREGISTRATIONANDCOMMONLICENCES ................................ 50REGISTRATIONWITHBOARDOFINVESTMENT(BOI)................................................................................................... 50REGISTERINGWITHENVIRONMENTALLEGISLATION .................................................................................................... 50OBTAININGWORKPERMITFORFOREIGNNATIONALS................................................................................................. 51IMPORTANDEXPORTLICENSE........................................................................................................................................... 51SECTORSPECIFICREGULATIONSANDINFORMATION...................................................................................... 52COSTESTIMATESFROMTHEICTINDUSTRY ................................................................................................................... 52SPECIFICAGREEMENTSFORTHEPOWERSECTOR........................................................................................................... 52ISSUESTOBECOVEREDWHILEFORMINGASHIPYARD/SHIPBUILDING .................................................................... 53MARINEACTIVITIES.............................................................................................................................................................. 53TAXRATE(ASSESSMENTYEAR200809) .................................................................................................. 54INCENTIVESFORFOREIGNINVESTMENT.......................................................................................................... 55TAXHOLIDAY ......................................................................................................................................................................... 56OTHERIMPORTANTINCENTIVES........................................................................................................................................ 56EXPORTPROCESSINGZONES(EPZS) ............................................................................................................................... 56INVESTMENTS,REMITTANCESOUTOFBANGLADESH ..................................................................................... 56ANNEX4:PREVIOUSSUPPORTFROMTHENORWEGIANGOVERNMENTTOECONOMICDEVELOPMENTINBANGLADESH .................................................................................................................................................... 58ANNEX5:ECONOMICDEVELOPMENTOFBANGLADESH................................................................................. 58ANNEX6:NORWAYTRADESTATISTICS .......................................................................................................... 60

4

AcknowledgementsIthasbeenapleasuretoconductthestudy”Private Sector Development Programme in Bangladesh – assessment of business conditions and sector potential”. Much progress have taken place since I last visited Bangladesh few years ago, perhaps especially in the business sector. I would like to express my gratitude to Bangladesh Enterprise Institute (BEI), for setting up an interesting program and accompanying me to the different institutions for the field interviews. I would also like to thank all individuals and institutions that have generously shared knowledge and experience responding openly to all sorts of questions. A special thank to individuals that have assisted in the final quality assurance of sector and other information.

Oslo 12th October 2009

Åsa Sildnes

Listofacronyms AD Authorized Dealer

ADB Asian Development Bank

AGM Annual General Meeting

AOA Articles of Association

B2B Business to business

BASIS Bangladesh Association of Software and Information Services

BBBF Bangladesh Better Business Forum

BDT Bangladeshi Taka (1 NOK = 11 BDT)

BGMEA The Bangladesh Garment Manufacturers and Exporter Association

BOI Board of Investment

BOO Build Own and Operate

BOT Build Operate and Transfer

BPDB Bangladesh Power Development Board

CDM The Clean Development Mechanism

CMMI Capability Maturity Model Integration

5

CNG Compressed Natural Gas

CSR Corporate Social Responsibility

DCC Dhaka Corporate Council

DOE DepartmentofEnvironment

DWT Dead Weight Ton

EGM Extraordinary General Meeting

EPB Export Promotion Bureau

EPZ Export Processing Zones

ERC Export Registration Certificate

FICCI Foreign Investors Chamber of Commerce and Industries

FIQC Fish Inspection and Quality Control

GDP Gross domestic product

HACCP Hazard Analysis (and) Critical Control Point

HFO Heavy Furnace Oil

IFC International Finance Corporation

IPP Independent Power Plants

LNG Liquefied Natural Gas

LPG Liquid Petroleum Gas

MOA Memorandum of Association

NBR National Board of Revenue

NCG Nordic Consulting Group

NG Natural Gas

PDB Power Development Board

PPPP Public Private Power Plants

PSD Private Sector Development

PSDSP Private Sector Development Support Program

REB Rural Electrification Board

REP Request for Proposal

RJSCF The Registrar for Joint-Stock Companies & Firms

6

RMG Ready made garments

SEDF South Asia Enterprise Development Facility

SRO Statuary rules and order

TCF Trillion Cubic Feet

TIN Tax Identification Number

USC Utility Service Cell

VAT ValueAddedTax

WB World Bank

ExecutivesummaryDoingbusinessinBangladeshisnotcommonplaceforNorwegiancompanies,butseveralmaybeencouragedbythebusinessopportunitiespickedupbyanumberofforeigninvestorsinBangladeshlately.Thisstudyhasbeencarriedoutaspartofaprocesstoincreaseregularbusinesscollaborationandtradebetweenourtwocountries.ThesuccessofGrameenPhone,ajointventurebetweenNorwegianandBangladeshipartners,hasproventhatitispossibletodogoodbusinessinBangladesh.Attractionsincludeamarketthatconsistsof150millionpeople,andthefactthatlowsalariesandawell‐trainedandEnglishspeakinglabourforcemakeitagoodlocationforoutsourcingofproduction.Businessrisksarehigh,butsoareprospectsofgoodprofitmargins.

Companies that would like to do business in Bangladesh are likely to meet regulatory hurdles and compliance problems and should expect that getting the required licences in place might take more time than indicated from the authorities. Digitalising company registration is under way and is expected to reduce irregularities and promote transparency in the registration process.

It is relatively easy to invest 100% as a foreign company in Bangladesh. For an investor this might be an advantage in cases with no obvious local partner to add value to the project, although collaboration with a local company in most cases is likely to make the entrance into Bangladesh easier. Other incentives are tax holidays and Export Processing Zones. Access to enough and reliable electricity is seen as one of the biggest obstacles to industrial development in Bangladesh today and therefore the power situation at location should be assessed in the planning phase of any project.

All sectors identified in the first study have potential for business development between Bangladesh and Norway. In the ICT sector, the costofhumanresourceandtheavailabilityofcompetencearereasonsforBangladeshtoberatedasoneoftheupcomingoutsourcingdestinations.Internetcapacityneedstobedevelopedtokeepabreastwiththeneedsofthesector.TheconstructionofasecondinternationallineforinternetconnectionmightbeimportantforBangladesh’sattractionasanoutsourcingdestination.

Theenergysectorhasmanychallengesaswellasopportunities.Thegapbetweendemandandsupplyforelectricityisfirstlyabottleneckforbusinessdevelopmentbut

7

alsoanopportunityfordoingbusinessintheenergysector.Thedevelopmentoftheenergysectorrequiresmassiveinvolvementfromthegovernmenttoimplementthenationalstrategyandtocarryouttransparenttenderingprocessesresultinginconstructionofnewprojects.Thegovernmenthastoproveitsabilitytoactandimprovethecriticalpowersituation,unlessitsambitiousannualGDPgrowthobjectivetowards2020islikelytofail.Thereishugepotentialincoal,gasandrenewableenergy,butimplementationdependsontheabilityofpoliticianstoact.Withregardtorenewableenergy,theGovernmenthasgivenemphasisonsolarpoweronly,declaringallocationsforruralelectrification.Atthemomentofeditingthisreport,littlehasbeendonefromthegovernmentonthefundingside.NGOsandothersmallfirmsareextendingtheiractivitiesandaretheonesthathavecontributedtoruralelectrification.

Despitethepresentfinancialcrisisaffectingtheshippingsector,Bangladeshientrepreneursshowgreatenthusiasmtogetintointernationalshipbuildingandanumberofinvestorspositionthemselvesforpartneringwithforeigninvestors.Somecompanieshavealreadysetupmodernshipyardsandgotinternationalorders;e.g.incollaborationwithDanishcompaniesthroughDanida`sB2Bprogram.LabourcostischeapinBangladeshandthesameshipcansupposedlybebuiltinBangladeshforhalfthepriceofthatinChina.TheBangladeshishipbuildingindustryisdevelopingtheirnicheonshipsbetween3000‐6000DWT,mainlysmallertankersandcargoships.Thisisduetofutureexpectationsondemandforthesetypesofvessels.Besides,locationsalongtheriverbanksrestrictthesizeoftheconstruction.

WhenNorwegiancontractorschoosealocationforhullbuilding,criteriasuchasqualityandpriceareimportant.OccupationalHealthandSafetymeasuresmustbeinplacetoavoidaccidentsandabadreputation.Offshorevesselsareparticularlydemandingshipstoconstructsincetheyareloadedwithequipment.ItmightthereforetakesometimebeforeBangladeshbuildsoffshorevessels.

Fish–andshrimpfarmingislikelytopresentbusinessopportunitiestoNorwegiancompaniesinterestedineitherfishfarmingorsellingofequipment.AquacultureinBangladeshisdeveloped,buthasmanychallengeswhenitcomestoqualityimprovement,accesstonewtechnologyandbetterenvironmentalstandardofthefarms.Productionoffishandshrimpfeedisabusinessopportunity.

Thefishingfleetispartlyoldandinneedforreinvestments.Energyefficiencyofenginesisgenerallylowandinvestinginmodernfishingequipmentaswellasenergyefficientmotorsarelikelytopayoff.

TradingwithgarmentsisthemainbusinessconnectionbetweenNorwayandBangladeshtoday,with5%oftheknitwearand2%ofthewovenmaterialimportstoNorwayfromBangladesh.TheInternationaltextilebrandsbuyinggarmentsfromBangladeshandtheNGOshaveworkedtomakethesectorcleanwhenitcomestochildlabour,violatingoflabourlaws,humanrightsandenvironmentalhazardsandmostfactoriesinBangladeshtodayrespectinternationallyacceptedbusinessprinciples.

FocusonmorehighvalueproductsbothingarmentsandhometextilesmightincreaseimportstoNorway.GarmentsmadefromexpensivefabricsfromathirdcountrybutwiththemainprocessinginBangladeshcanbeimporteddutyfreetoNorway.Thisopportunityitseemshasnotyetbeenfullyutilised.Thehometextilefactorieshavelong

8

waitinglistsforproductionandindicateaninterestinginvestmentpossibilitythatcouldbefurtherinvestigated.

A B2B program between Norway and Bangladesh should start with a pilot phase with the aim of reaching a limited number of companies in the prioritised sectors (5-10 companies). The experience from this first phase should then form the continuation of the program. It will be advantageous for the program to be linked to the Norwegian Embassy, e.g. with offices in the Embassy. This will give the program credibility and standing both in the Norwegian and the Bangladeshi business environment. Further, it is seen as important to have a Norwegian national as a programme director, to enable easy communication with Norwegian companies and marketing of the program in Norway. This does not prevent close collaboration with local institutions, e.g. on services such as quality assurance of Bangladeshi companies entering into the program as well as preparing local companies for the program.

In the pilot phase, the program director should closely follow each company entering into the program and give tailor made support. Based on experiences in the pilot phase, conclusion to be made on what service level to provide and what approach to follow for the continuation of the B2B. The support (both in the form of follow up by a program director and in monetary support) should be generous in the pilot phase. The program should aim at a limited number of companies participating in the program, maybe up to 50 companies over the life span of the program. Bangladesh is presently not well known to Norwegian businesses and there are many other PSD programs competing for a few companies looking for business opportunities in emerging and challenging markets.

The recruitment of Norwegian companies should be strict and should be selected on criteria such as a good business idea and commitment to succeed. The company must have the right motivation, realistic plans and they should also set aside the necessary human resources for the project. On the Bangladeshi side, there is no shortage of committed companies as potential local partners. To avoid disappointment and misunderstanding these companies might be offered preparatory training on how to do business with Norwegians. Cluster entry might create synergies and areas for collaboration, e.g. in terms of sharing premises, mutual learning, experiences and benefitting from coordinated contact with government and other bodies.

1.0IntroductionA team from Norad/NCG carried out the study “Identification and Feasibility: Private Sector Development Programme Bangladesh” in 2008/2009 with the purpose to assess if a Norwegian sponsored PSD program should be planned as part of the development partnership between Norway and Bangladesh. The study identified specific sectors of interest for collaboration between Norwegian and Bangladeshi companies. Norad wanted a follow up of the study to further increase knowledge about the business conditions in general and the chosen sectors in particular.

”Private Sector Development Program in Bangladesh – assessment of business conditions and sector potential” aims at digging deeper into the sectors identified by the first study as well as describing the general business framework in Bangladesh. Specific conditions such as licences and requirements for each sector are listed. Companies that would like to start

9

business in Bangladesh, are advised to carry out project specific feasibility studies to assure updated and detailed information of the sector of interest.

”Private Sector Development Program in Bangladesh – assessment of business conditions and sector potential” builds on the mentioned Norad/NCG study from 08/09 and attempts not to duplicate information already presented there. The “Identification and feasibility –“ should therefore be referred to for general country information and the reasoning behind planning a B2B program.

Thefirstpartofthereportlooksatthegeneralbusinessframework;whataretherequirementstostartbusinessinBangladesh,howtoregisteracompany,whattimeframeandcostsareinvolved,whatkindoflicencesmustbeinplace,taxratesandincentivesaswellasregulationsforremittances.Mostofthisinformationiscompiledinannex3:RoadmapforbusinessentryinBangladesh.

Themiddlepartfocusonsectorspecificissues;wherespecialattentionisgiventotheICTsector,marineactivities,shipbuilding,energyandtrade,allidentifiedassectorswithpotentialforcollaborationbetweenNorwegianandBangladeshicompanies.Anumberofcompaniesandsectorspecificinstitutionshavebeenvisitedandinterviewedtogiveabroadpictureofeachsector.TradingwithgarmentsispresentlythemaintradegoingonbetweenNorwayandBangladeshandisanactivitythatcangrowe.g.intohighervaluegarmentsandhometextiles.Thenormalprocedurefortradingwithgarmentsisdescribed.Theenergysector,especiallypowerproduction,ishighlyinterestingwithhugegrowthpotential,butalsouncertainasitdependscompletelyonpoliticaldecisionsandthegovernments`abilitytoimplementitsenergypolicy.

ThelastpartlooksbrieflyatexperiencesfromtheDanishB2Bprogram.Itcontainsconclusionsandrecommendationdividedintothreesections;issuesrelatedtothebusinessframework,tosectorissuesandtoissuesconcerningafutureB2BprogrambetweenNorwegianandBangladeshibusinesses.

1.2Methodology

In collaboration with Bangladesh Enterprise Institute, a program for the fieldwork was set up aiming at meeting representatives for sectors of special interest and institutions involved in private sector development in Bangladesh. Preparations for the study included interview with a representative of the Danish B2B program. A number of studies carried out for private sector development in Bangladesh have been perused and references made to issues of doing business in Bangladesh that might be of interest for the potential investor. Further, documents and websites providing information to investors from the government and authorities have been studied and often quoted. Areas and procedures where information on routines does not correspond with experience of investors are mentioned. A number of meetings have been conducted with resource persons from companies, authorities and sector professionals1. The study report might be seen as a practical guide to do business in Bangladesh with introductory information of interesting sectors.

1Annex1Informationgathering

10

2.0ThebusinessframeworkinBangladeshThebusinessframeworkiswelldescribedinthebooklet”BangladeshInvestmentHandbook”,publishedbyBOIin2007.Theinformationfrom2007isstillcorrectexceptfromsomechangesintaxlawsaswellasincentivesforcompanies.TheBOIwebpage;www.boi.gov.bdprovidesinformationtocompanieslookingtoBangladeshforbusiness.Thatsaid,mostinvestorswillexperiencethatproceduresdescribedasquitestraightforwardandeasytoaccess,inreallifesituationtakestime,iscumbersomeanddifficulttopushthroughthesystem.Acommonreasonfordelaysandproblemsisthewidelyexpectedhandlingfees(speedmoney)requestedbyofficersatdifferentlevels.

Unfortunately,themaybemostimportantinstitutionsforhandlingapplicationsforforeignbusinesses;TheBoardofInvestment(BOI),DhakaCityCorporation(DCC)andTheRegistrarforJoint‐StockCompaniesandFirms(RJSCF)areknownfor“unofficial”practicesandfordelayingtheprocessiftheirrequestsarerejected.ThereareongoingprogramssuchasPrivateSectorDevelopmentSupportProgram(PSDSP)andSouthAsiaEnterpriseDevelopmentFacility(SEDF)thatworkdirectlywithinstitutionslikeBOItobecomemoreefficient,butitisstillawaytogo.ThereisapressureonthenewgovernmenttoimplementtheplanforrestructuringBOI,aplanthatwasapprovedbythecaretakergovernment.BOIseemstoneedafullmakeovertobecomeanefficientandtransparentorganisationpromotingbusinessinBangladesh.

ThepreviousgovernmentstartedBangladeshBetterBusinessForum(BBBF)withthepurposetoimplementreformstoimprovethebusinessenvironment.ThisforumisputonholdbutthePrimeMinisterhasindicatedthattheworkoftheforumshallcontinue.Theforumhasbeenwellreceivedbytheprivatesector.Itsachievementsduringthe1.5yearsinoperationarevisible.

Detailsaboutcompanyregistration,taxissuesandremittancesarefoundinAnnex3:RoadmapforBusinessentryinBangladesh.

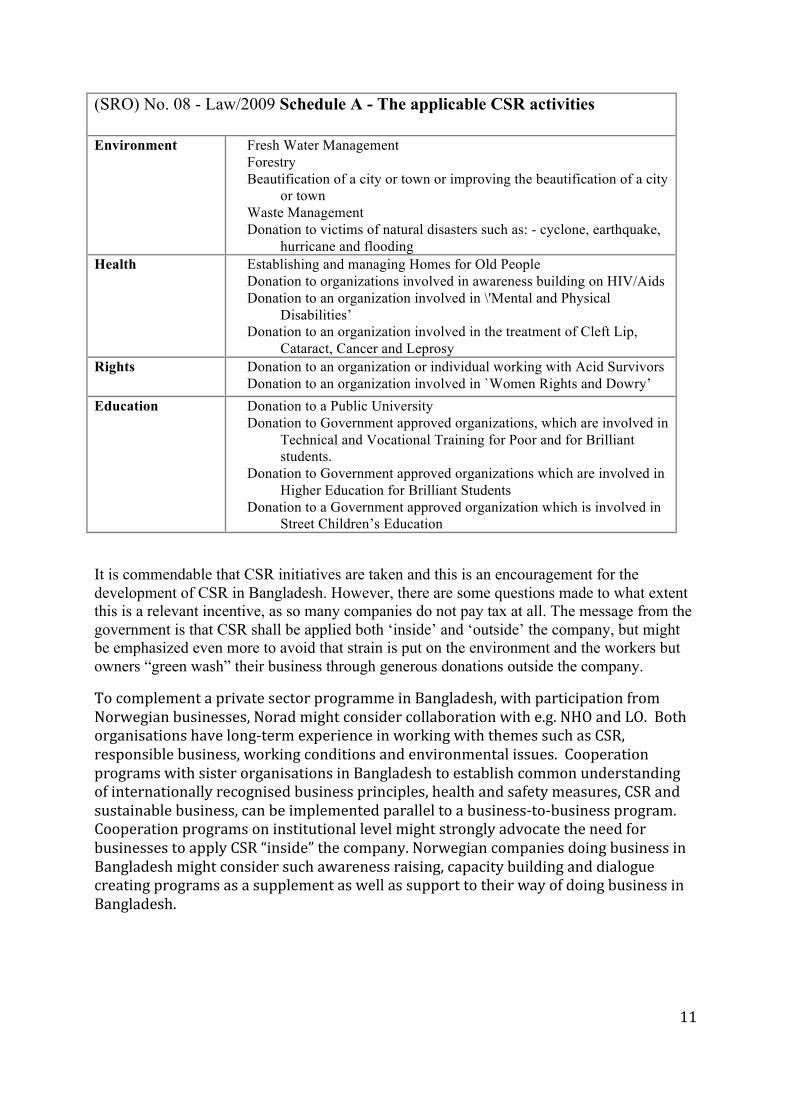

2.1CorporateSocialResponsibility(CSR)The Ministry of Finance through the National Board of Revenue (NBR) has provided a significant incentive to companies in Bangladesh to increase and to formalise their corporate philanthropy and other CSR activities.2

The Statuary rules and order (SRO) has decided to grant a 10 % Tax Exemption of actual expenses for organizations involved in the listed Corporate Social Responsibility (CSR) activities and meeting the compliance conditions specified.

2http://www.ficci.org.bd/monthly_bulletins_view.php?bu_id=B-004

11

(SRO) No. 08 - Law/2009 Schedule A - The applicable CSR activities

Environment

Fresh Water Management Forestry Beautification of a city or town or improving the beautification of a city

or town Waste Management Donation to victims of natural disasters such as: - cyclone, earthquake,

hurricane and flooding Health

Establishing and managing Homes for Old People Donation to organizations involved in awareness building on HIV/Aids Donation to an organization involved in \'Mental and Physical

Disabilities’ Donation to an organization involved in the treatment of Cleft Lip,

Cataract, Cancer and Leprosy Rights Donation to an organization or individual working with Acid Survivors

Donation to an organization involved in `Women Rights and Dowry’ Education

Donation to a Public University Donation to Government approved organizations, which are involved in

Technical and Vocational Training for Poor and for Brilliant students.

Donation to Government approved organizations which are involved in Higher Education for Brilliant Students

Donation to a Government approved organization which is involved in Street Children’s Education

It is commendable that CSR initiatives are taken and this is an encouragement for the development of CSR in Bangladesh. However, there are some questions made to what extent this is a relevant incentive, as so many companies do not pay tax at all. The message from the government is that CSR shall be applied both ‘inside’ and ‘outside’ the company, but might be emphasized even more to avoid that strain is put on the environment and the workers but owners “green wash” their business through generous donations outside the company.

TocomplementaprivatesectorprogrammeinBangladesh,withparticipationfromNorwegianbusinesses,Noradmightconsidercollaborationwithe.g.NHOandLO.Bothorganisationshavelong‐termexperienceinworkingwiththemessuchasCSR,responsiblebusiness,workingconditionsandenvironmentalissues.CooperationprogramswithsisterorganisationsinBangladeshtoestablishcommonunderstandingofinternationallyrecognisedbusinessprinciples,healthandsafetymeasures,CSRandsustainablebusiness,canbeimplementedparalleltoabusiness‐to‐businessprogram.CooperationprogramsoninstitutionallevelmightstronglyadvocatetheneedforbusinessestoapplyCSR“inside”thecompany.NorwegiancompaniesdoingbusinessinBangladeshmightconsidersuchawarenessraising,capacitybuildinganddialoguecreatingprogramsasasupplementaswellassupporttotheirwayofdoingbusinessinBangladesh.

12

2.2PublicPrivatePartnership(PPP)Public-private partnership is not a new invention in Bangladesh. From the mid nineties, PPP commenced in Bangladesh resulting in 50 projects in telecommunication, port construction and other physical infrastructure projects. The budget proposal indicates increased focus on PPP in order to boost the economy and increase local and foreign investments. The government has ambitious goals for gross domestic product (GDP) growth, aiming at a growth rate between 8 and 10 % sustained till 2021. To attain this growth, they foresee investments in power production, energy, ports, communication, drinking water, waste management, education and health. The government realises that it alone cannot provide such huge amount of resources but will team up with private sector investors to invest alongside the government. The government will provide three new budget lines focussing on the following:

• PPP Technical Assistance to cover expenditure related to pre feasibility studies and preparatory work before asking the private sector to submit their bids for PPP projects.

• Viability gap funding as a subsidy or seed money to attract private initiatives for the construction of power plants, hospitals, schools, roads and highways which are non-profitable but essential for the society.

• Infrastructure investment fund from where the government can provide equity or loan to private investors to ensure Government participation.

The government plans to set up an institution for preparation and implementation of the PPP budget and indicates that the PPP facilities should be in operation from September 2009. At the time of final editing of the report (Oct. 2009), there are no signs of this facility. When it comes to renewable energy, the Government has given emphasis to solar power only, but despite its declaration of ambitious plans, there is no trace of the promised funds to be disbursed through commercial banks for the purpose. The World Bank has declared credit to the Bangladesh Government for supporting rural people for solar solutions but there is no known progress in this project. Investors in the sector should follow the development of the governments PPP plans closely, although it is likely that interested investors has to go through the usual practice of political lobby. Advantages as well as possible disadvantages to invest alongside the government should be assessed. The position paper PPP: “Invigorating Investment Initiative through Public Private Partnership” was published in June 09.3

3www.mof.gov.bd/en/budget/09_10/ppp/ppp_09_10_en.pdf

13

3.0Sectorspecificissues

3.1ICT

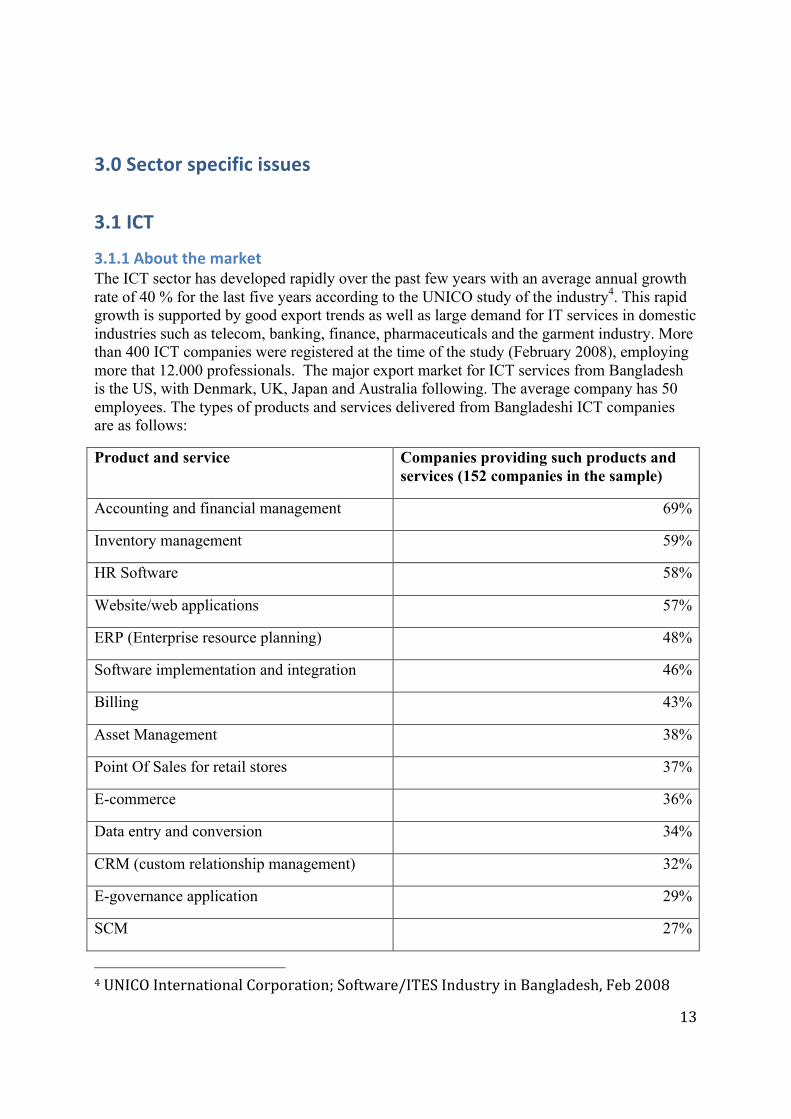

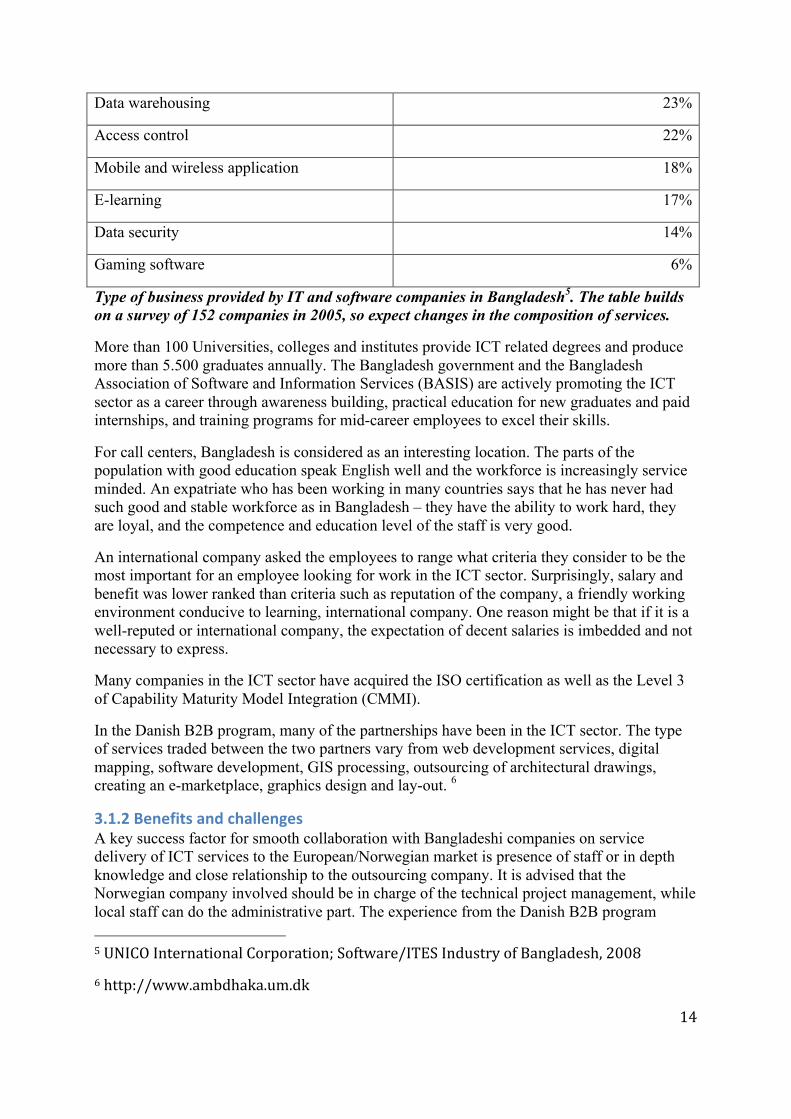

3.1.1AboutthemarketThe ICT sector has developed rapidly over the past few years with an average annual growth rate of 40 % for the last five years according to the UNICO study of the industry4. This rapid growth is supported by good export trends as well as large demand for IT services in domestic industries such as telecom, banking, finance, pharmaceuticals and the garment industry. More than 400 ICT companies were registered at the time of the study (February 2008), employing more that 12.000 professionals. The major export market for ICT services from Bangladesh is the US, with Denmark, UK, Japan and Australia following. The average company has 50 employees. The types of products and services delivered from Bangladeshi ICT companies are as follows:

Product and service Companies providing such products and services (152 companies in the sample)

Accounting and financial management 69%

Inventory management 59%

HR Software 58%

Website/web applications 57%

ERP (Enterprise resource planning) 48%

Software implementation and integration 46%

Billing 43%

Asset Management 38%

Point Of Sales for retail stores 37%

E-commerce 36%

Data entry and conversion 34%

CRM (custom relationship management) 32%

E-governance application 29%

SCM 27%

4UNICOInternationalCorporation;Software/ITESIndustryinBangladesh,Feb2008

14

Data warehousing 23%

Access control 22%

Mobile and wireless application 18%

E-learning 17%

Data security 14%

Gaming software 6%

Type of business provided by IT and software companies in Bangladesh5. The table builds on a survey of 152 companies in 2005, so expect changes in the composition of services.

More than 100 Universities, colleges and institutes provide ICT related degrees and produce more than 5.500 graduates annually. The Bangladesh government and the Bangladesh Association of Software and Information Services (BASIS) are actively promoting the ICT sector as a career through awareness building, practical education for new graduates and paid internships, and training programs for mid-career employees to excel their skills.

For call centers, Bangladesh is considered as an interesting location. The parts of the population with good education speak English well and the workforce is increasingly service minded. An expatriate who has been working in many countries says that he has never had such good and stable workforce as in Bangladesh – they have the ability to work hard, they are loyal, and the competence and education level of the staff is very good.

An international company asked the employees to range what criteria they consider to be the most important for an employee looking for work in the ICT sector. Surprisingly, salary and benefit was lower ranked than criteria such as reputation of the company, a friendly working environment conducive to learning, international company. One reason might be that if it is a well-reputed or international company, the expectation of decent salaries is imbedded and not necessary to express.

Many companies in the ICT sector have acquired the ISO certification as well as the Level 3 of Capability Maturity Model Integration (CMMI).

In the Danish B2B program, many of the partnerships have been in the ICT sector. The type of services traded between the two partners vary from web development services, digital mapping, software development, GIS processing, outsourcing of architectural drawings, creating an e-marketplace, graphics design and lay-out. 6

3.1.2BenefitsandchallengesA key success factor for smooth collaboration with Bangladeshi companies on service delivery of ICT services to the European/Norwegian market is presence of staff or in depth knowledge and close relationship to the outsourcing company. It is advised that the Norwegian company involved should be in charge of the technical project management, while local staff can do the administrative part. The experience from the Danish B2B program 5UNICOInternationalCorporation;Software/ITESIndustryofBangladesh,2008

6http://www.ambdhaka.um.dk

15

indicates that the main challenges in project collaboration are project management and communication. These frustrations can be overcome by presence from the Norwegian company. It is likely that presence in the country is needed for a longer period than expected in the start up of a joint project. It can take more than a year before project management and communication runs smoothly between the two partners, according to Danish experiences. Personal abilities and capabilities of the representative of the Norwegian company can make or break the success of the collaboration between the partners. Careful selection of the right employee is crucial and personal abilities are seen as more important than technical skills.

Prices of human resource are still low in Bangladesh, with prices as low as 200 NOK per hour for software development, and for data mining prices vary from NOK 100 to NOK 160 per hour based on experience of staff. A document from BASIS promoting Bangladesh as outsourcing destination for ICT compares costs in Bangladesh with other Asian destinations:

WhyoutsourcetoBangladesh?

BangladeshofferssignificantcostadvantagesforIToutsourcing‐bothintermsof

worker‐wagesaswellascostofinfrastructure

SalaryofprogrammersinBangladeshis50%ofthatinIndia,40%ofPhilippines

and70%oftheVietnam

RentforofficespaceinDhaka(Capital)isbelow20%ofthatinDelhiand40%of

Manila

Software and IT services have been declared by the Government as a `High

priority’exportsector

All Software and IT Services companies including those having foreign

ownershipshavebeenexemptedfromIncomeTaxuntil2011

3.1.3DoingbusinessintheICTsectorIt might be easier to set up IT companies in Bangladesh than other types of companies. The reason is that there is not much transport of goods across borders, raw materials to import or cumbersome work getting goods out of the customs. When the business is established and properly registered, and the trade licence is obtained, the business is running without too much interaction with government bodies. However, when a contract is signed with an overseas customer, the local company need to obtain an Export Registration Certificate (ERC). The ERC must be made for each order. When the remittance (money transfer) arrive in the company’s bank, the company will have to present the ERC, as well as a work order invoice, the registration certificate of the company and Form C; Declaration of remittance to the Central Bank. When this paperwork is through, your bank will transfer the money in local currency to your local currency account. A company in the export business will be granted to keep 40% of the remittance in foreign currency and it will be deposited in the company’s foreign currency account.

16

3.1.4InternetconnectionThe development of the ICT sector is hampered by Internet capacity. The edge system is available whereas many are looking forward to the development of 3G systems. Access to 3G will mean 10 times the speed of the present system to a cheaper price. However, the 3G do not meet the security requirements to transfer of data that many clients need. The government owned Telecommunication Company is presently the only provider of Internet services. There are no known plans to change the monopoly system and open for private concessions. However, the Telecommunication Company is looking at possibilities to open one more international line to increase the stability and reliability of international Internet lines. With a second line in place, Bangladesh is likely to attract more business as an outsourcing destination. Many companies will shy away from Bangladesh as long as they depend on only one line. It is seen as risky. Services are relatively expensive. Dedicated bandwidth of 3 MB per second will cost approximately NOK 11000 per month. There are restrictions on services via the Internet and e.g. Skype calls are not permitted, but this restriction is difficult to enforce.

3.1.5OutsourcingofservicesOutsourcingofICTservicestakeplaceinmostpartsoftheICTbusiness.Often,theendcustomerdoesnotknowwheretheactualserviceiscarriedoutastheydealwithaonestopsupplierservingthecompany`stotaldemandforICTservices.Whenmultinationalactorschoosecountriesforwheretooutsourceservices,theyevaluatearangeofcriteriasuchaslanguageandeducationlevelaswellasgeopoliticalissues.Longtermperspectiveofstabilityisimportanttomakeinvestmentsinthesectorinanewcountry.Twostablelinesoutofthecountryinplaceareimportant.BangladeshconsiderstoinstallonemorelinewhichislikelytoincreasetheinterestforBangladeshasanoutsourcingdestination.

Outsourcingofsoftwaredevelopmentisworkingwellwithintechnicalfields,especiallywhereEnglishlanguageiscommonlyused.However,softwaredevelopmentforNorwegiancustomersoftenrequireknowledgeoftheNorwegianlanguageandcultureonfunctionallevelandwillthusdependonclosecollaborationbetweenpeoplewithdifferentskills.

CommoncountriesforoutsourcingofICTforNorwegianbusinessesareIndia,Ukraina,PolandandotherpreviousEasternEuropecountries.

EDBBusinessPartnerhaspublishedareportonglobalsourcingavailableontheInternetwheremuchinformationonoutsourcingisfound.7

7http://www.edb.com/Documents/Corporate%20Documents/Report_Global_Sourcing_2007.pdf

17

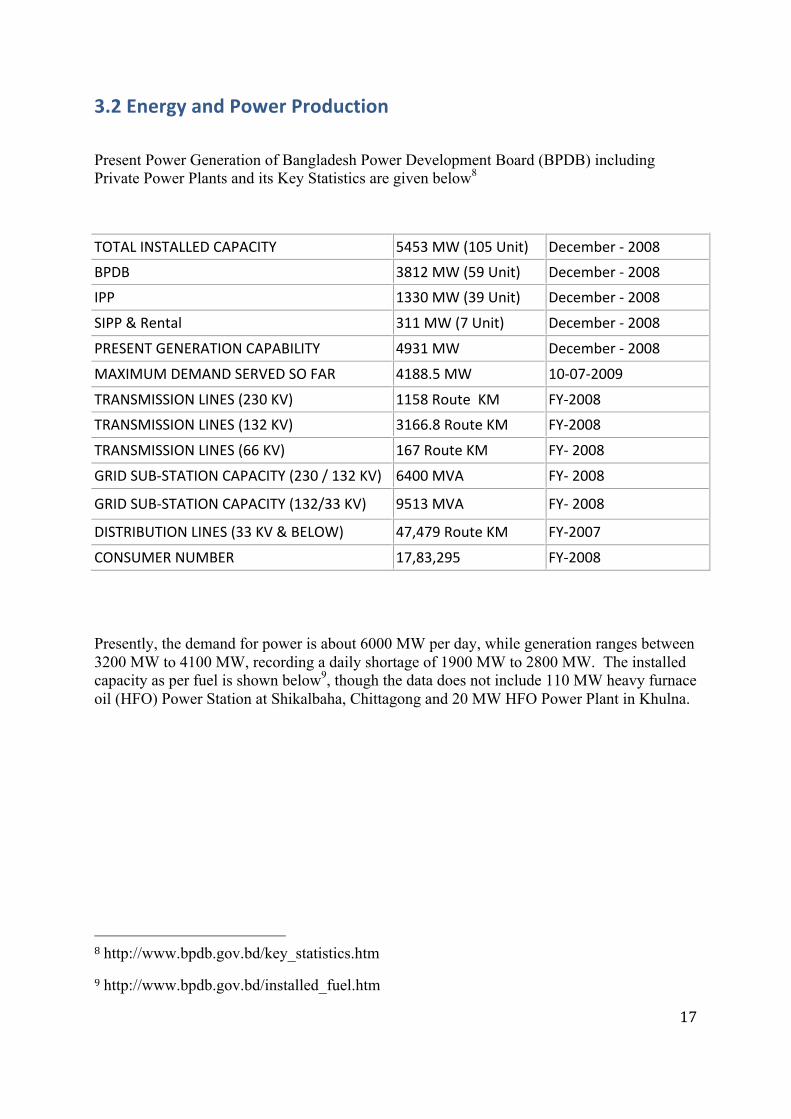

3.2EnergyandPowerProduction

Present Power Generation of Bangladesh Power Development Board (BPDB) including Private Power Plants and its Key Statistics are given below8

TOTALINSTALLEDCAPACITY 5453MW(105Unit) December‐2008

BPDB 3812MW(59Unit) December‐2008

IPP 1330MW(39Unit) December‐2008

SIPP&Rental 311MW(7Unit) December‐2008

PRESENTGENERATIONCAPABILITY 4931MW December‐2008

MAXIMUMDEMANDSERVEDSOFAR 4188.5MW 10‐07‐2009

TRANSMISSIONLINES(230KV) 1158RouteKM FY‐2008

TRANSMISSIONLINES(132KV) 3166.8RouteKM FY‐2008

TRANSMISSIONLINES(66KV) 167RouteKM FY‐2008

GRIDSUB‐STATIONCAPACITY(230/132KV) 6400MVA FY‐2008

GRIDSUB‐STATIONCAPACITY(132/33KV) 9513MVA FY‐2008

DISTRIBUTIONLINES(33KV&BELOW) 47,479RouteKM FY‐2007

CONSUMERNUMBER 17,83,295 FY‐2008

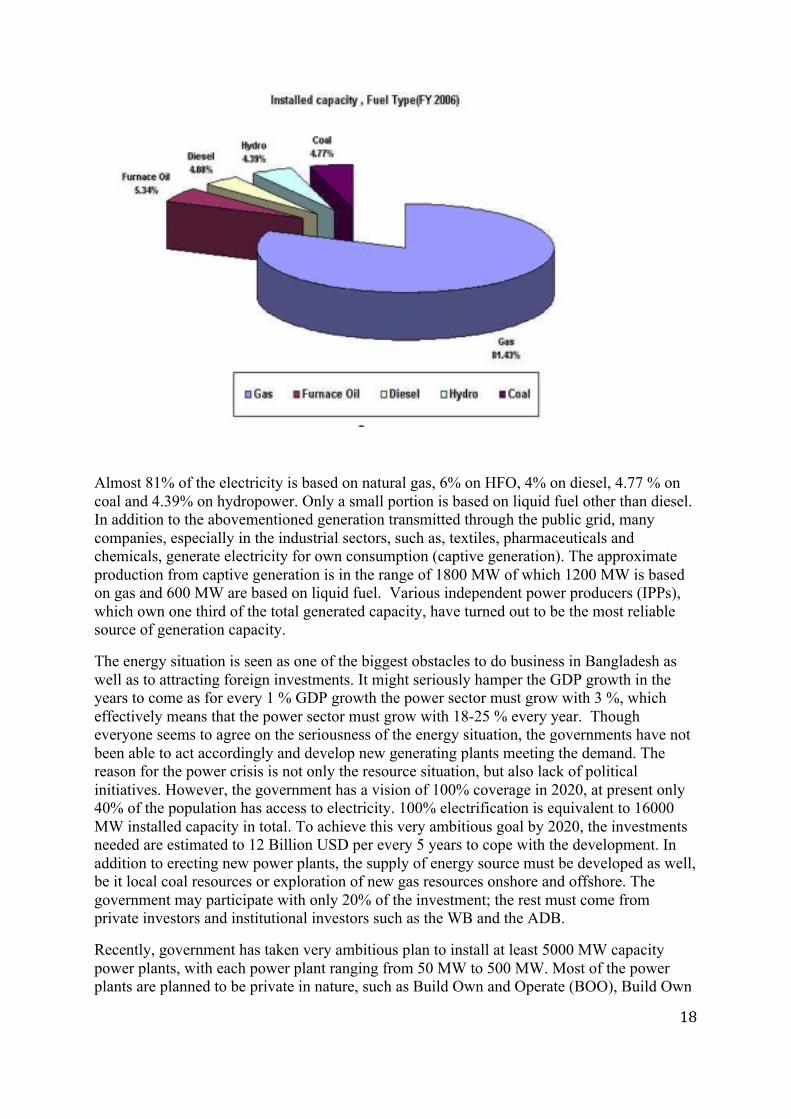

Presently, the demand for power is about 6000 MW per day, while generation ranges between 3200 MW to 4100 MW, recording a daily shortage of 1900 MW to 2800 MW. The installed capacity as per fuel is shown below9, though the data does not include 110 MW heavy furnace oil (HFO) Power Station at Shikalbaha, Chittagong and 20 MW HFO Power Plant in Khulna.

8http://www.bpdb.gov.bd/key_statistics.htm

9http://www.bpdb.gov.bd/installed_fuel.htm

18

Almost 81% of the electricity is based on natural gas, 6% on HFO, 4% on diesel, 4.77 % on coal and 4.39% on hydropower. Only a small portion is based on liquid fuel other than diesel. In addition to the abovementioned generation transmitted through the public grid, many companies, especially in the industrial sectors, such as, textiles, pharmaceuticals and chemicals, generate electricity for own consumption (captive generation). The approximate production from captive generation is in the range of 1800 MW of which 1200 MW is based on gas and 600 MW are based on liquid fuel. Various independent power producers (IPPs), which own one third of the total generated capacity, have turned out to be the most reliable source of generation capacity.

The energy situation is seen as one of the biggest obstacles to do business in Bangladesh as well as to attracting foreign investments. It might seriously hamper the GDP growth in the years to come as for every 1 % GDP growth the power sector must grow with 3 %, which effectively means that the power sector must grow with 18-25 % every year. Though everyone seems to agree on the seriousness of the energy situation, the governments have not been able to act accordingly and develop new generating plants meeting the demand. The reason for the power crisis is not only the resource situation, but also lack of political initiatives. However, the government has a vision of 100% coverage in 2020, at present only 40% of the population has access to electricity. 100% electrification is equivalent to 16000 MW installed capacity in total. To achieve this very ambitious goal by 2020, the investments needed are estimated to 12 Billion USD per every 5 years to cope with the development. In addition to erecting new power plants, the supply of energy source must be developed as well, be it local coal resources or exploration of new gas resources onshore and offshore. The government may participate with only 20% of the investment; the rest must come from private investors and institutional investors such as the WB and the ADB.

Recently, government has taken very ambitious plan to install at least 5000 MW capacity power plants, with each power plant ranging from 50 MW to 500 MW. Most of the power plants are planned to be private in nature, such as Build Own and Operate (BOO), Build Own

19

and Transfer (BOT), Independent Power Plants (IPP), Public Private Power Plants (PPPP) and some of them are rental power. Out of 3500 MW Power Projects 2000 MW will be generated from coal, 1400 MW from HFO and only 100 MW from natural gas. It is also learned that other power projects under planning either may be coal or HFO. This is the first time government is not giving any assurance of supply of fuel/source of energy; moreover, it is well declared that the project owner must arrange the energy source for new power projects. Most of the projects are private power projects, such as rental (1-3 years), BOOs, IPPs and the PPPs, where government will have maximum 20% of shares.

With such huge and growing power deficit there is large business scope both for domestic and foreign companies in the power sector. The Government’s plans and policies for the power sector still seem not very clear though The National Energy Policy from 2004 indicates strong focus on the power sector, but till now, implementation is hampered and little action has been taken. Rehabilitation of older power plants will also become increasingly important in the future.

3.2.1RehabilitationofOldPowerPlants40% of the power plants are more than 20-25 years old and already due for major overhaul. They are running well below capacity due to efficiency problems. With the present power situation, it is not realistic to replace them with new and more environmentally friendly power generating technology in a short-term perspective. The need for rehabilitation of old and inefficient plants is obvious, but so far the Government have put even lesser emphasis on rehabilitation than on construction of new plants. However, it is likely that rehabilitation of old plants will become an interesting business in the future with another series of power plants due for overhaul, installed in early and late 1990s. The rental power plants as well as company owned power plants (captive generation) are seen as very inefficient (maybe as much as 50%) with need of rehabilitation. It might be feasible to invest in rehabilitation of power plants and get shares as a partly payment for technology installation. The increase in efficiency and following increase in profitability should make such model interesting.

3.2.3Oil,GasandCoalOwn energy sector of Bangladesh is largely concentrated around natural gas. Bangladesh has substantial resources of natural gas with natural gas wells opened in the 1960s, the 1970s and only a few were added during the 1980s. Development of new gas wells as well as renovation of old wells have stagnated and hampered the production of gas. Often the pressure of the national gas distribution system goes low and resulting in unreliable production. New gas connections to the industries become a difficult issue. The natural gas (NG) is distributed in pipes to most of the Eastern Districts and some of the Western Districts and still the Southern part and Northern part have no gas connections. Domestic cooking largely depends on gas in the urban areas where gas connection is available. People living in areas without gas distributions through pipes use locally available biomass (fire woods), kerosene or LPG (Liquid Petroleum Gas) in cylinders for cooking. From 2003 the natural gas is being compressed and used in vehicles as Compressed Natural Gas (CNG). The use of CNG has been largely increased due to lower cost than liquid fuels (petrol, octane and diesel). Two stroke engines had been banned in Dhaka and Chittagong City in 2002 and all three wheelers and cars have been converted to use CNG. This makes a tremendous difference on the air

20

quality in the crowded streets of the cities, but use of gas in vehicles has increased tremendously and thereby caused another reason for lower gas pressure in the national distribution gas pipelines.

Most private owned industries power stations run on natural gas, but recently there are restrictions for using NG as the sole source for power generators. Now, the government insists on dual fuel system generators which can run both on gas and diesel or gas and furnace oil.

At present, the remaining deposit of explored sources of gas is approximately 6 Trillion Cubic Feet (TCF). Analysts have been estimating remaining sources of gas to 32 TCF at a 50% probability10. Despite the potentially good news, new gas explorations, if any, are likely to be started at least 5-6 years ahead. No drilling has been done to confirm these estimates.

Due to the country’s urgent need for gas the government is considering to buy Liquefied Natural Gas (LNG). The plan is then to degasify the liquid gas to feed into the gas transmission pipe system. Professionals in the energy sector argue that gas should be prioritised for industrial purposes and not so much for producing electricity. Many industries depend on gas in their industrial process, such as the fertiliser industry. The production suffers when access to gas is limited. At the moment Petrobangla (Bangladesh State Owned Oil and Gas Company) loose BDT 27 (ca NOK 2,7) on each MCF (1000 square ft) NG they provide to the gas transmission system. The gas provision is thus heavily subsidized.

Coal is well suited for power generation and Bangladesh has an estimated 67 TCF in coal reserves. Mainly due to controversy on the exploitation of the coal deposits, the government has not been able to make decisions on how to utilise the resource. Instead, there has been a discussion whether Bangladesh should invest in coal power based on import of Australian coal. Estimates show that costs of Australian based coal energy will be 5 BDT per KWH, while cost of local coal will be 3 BDT per KWH. Import of coal from Australia also forces Bangladesh to build a deep-sea port that can receive vessels above 5000 DWT, which is adding further costs to this alternative.

Professionals in the energy sector argue that coal mining must start immediately and construction of coal-based power plants must start simultaneously. A plan for development of coal resources must be in place to remove or mitigate social and physical issues related to the mining, through collaboration between stakeholders like government, affected population, miners etc. The coal resources are in abundance and can solve Bangladesh’s energy deficiency for many decades to come. Some of the resources are at shallow depths and therefore feasible for open pit extraction.

Bangladesh started early to explore its offshore oil resources, but only 90 wells have been dug and neighbouring countries are far ahead in exploration of resources in the Bay of Bengal. In 2008 Petrobangla invited bidders for 30 new blocks. The offshore oil resources are estimated to be limited compared with potential for gas and coal. For many years Bangladesh has been importing crude oil from Saudi Arab and Other Arabian Countries at a reduced rate.

10SurveybyUSGSandNorwegianPetroleumDirectorate

21

3.2.4RenewableEnergyDevelopments in the time to come will for sure consider more environmentally friendly methods of power generating, but with the present deficiency, the government is looking for all kinds of power sources, such as coal, nuclear, gas as well as for solar. The government is in discussion with the Russians on construction of a 1000 MW nuclear power plant. The government is presently preparing a Request for Proposal (REP) to build a windmill park of 50 MW. The company that wins the bidding will build, own and operate the plant and negotiate a purchase agreement with the government.

Renewable energy has so far not taken off, except from schemes of rural electrification, covering individual household and financed mainly through Micro Finance Institutions (MFIS) mostly using solar power and biogas from manure as the source of energy. Taxing on renewable energy (solar) has been fixed in the current fiscal year budget to 5.66%.

The CDM facility is not commonly known in Bangladesh yet, with only 3 projects approved under CDM. However, there is increasing interest in the mechanism and Dhaka Chamber of Commerce and Industry will have a training workshop on the topic in July 2009.

Solar is the most commonly used renewable form of energy and the government has framed a renewable energy policy with specific targets. This is a first step that hopefully later leads to a plan for implementation. At present solar home systems generate 15 MW of electricity across the country. The policy envisions meeting 5 % of the total power demand by 2015 and 10 % in 2020 by developing renewable energy sources such as solar, biogas, biomass, wind and hydropower.11 Grameen Shakti, a leading organisation installing solar home systems in off grid areas, says nearly 80 million people do not have access to electricity and the solar home system helps thousands of rural people to light their homes. Grameen Shakti also provides power to 230,000 households from 7000 biogas plants. GTZ is involved in a program with poultry and dairy farmers where bio-gas is converted into electricity. An estimated 100 MW can be generated through farm based biogas plants. Landfills as a source of biogas have not yet been exploited widely in Bangladesh, but the potential is likely to be high.

Rahimafrooz Renewable Energy Ltd. will start to assemble solar panels to provide the domestic market with solar home systems. Recently the Bangladesh Bank has formed a USD 29 Million revolving fund for banks and financial institutions to extend loans at low interests to renewable energy development. On the time of editing the report (October 2009) the funding is not yet disbursed. In the budget for the fiscal year 2009-2010, the government exempted VAT on solar panel, but custom duty on import was increased to 5.66%, which was earlier 4.07%, though the commitment of the government and proposed budget was to bring down the custom duty on import to 0%.

The government says that it considers possibilities of setting up hydroelectric power plants in high stream rivers, from where 10-15 MW can be produced. Bangladesh has presently only one big hydro power plant with 230 MW installed capacity, but mostly running at lower capacity. The reasons why hydropower has not been developed in a country so rich on water resources are lack of difference in altitude as well as high density population and great controversy of regulating the rivers.

11TheDailyStarBusiness,24thJune2009

22

Bio fuel is presently not considered an interesting venture in Bangladesh in a big scale. The soil is well suited for food crops. The country aims at self-sufficiency of food with a surplus for export.

3.2.5GovernmentPoliciesWhen industries produce their own electricity, the government has been issuing licences for companies’ own power generation at a relatively high price. Also, the companies had to pay a yearly fee to maintain the licence. In the new budget, this licence is lifted and will be a good incentive for companies to invest in power generation. The grid system as well as the present subsidy system in the power sector will hopefully implement purchasing facilities to make better use of surplus electricity produced by companies (captive generation). So far, the government has not explored the possibility of buying excess electricity from captive generation and this might be a reason for low efficiency of the company owned generators.

The government has over the past 9 years only given concessions to 8 relatively small plants. An ongoing bidding process is on for a 450 MW combined cycle (300 MW gas, 150 MW steam) power station, the last project to be gas based. In the future, the government is expected to come out with tenders for energy production on a regular basis. The IPP program worked well in the 1990s, since then many plans have been tendered and awarded but then cancelled due to questions whether rules were followed. The approach of the government to deal with the power situation has been ad hoc and often driven by political considerations. The highly subsidised natural gas for captive generation to offset power supply shortages has failed to attract private investors.

To turn the power sector back on track, the government needs to prioritize and give clear political support. One of the critical issues is to develop an efficient pricing policy with market pricing of gas and power prices to full cost recovery levels and a fair return of investments. The demand for power will never be met until the energy price is market driven. There is no lack of plans as The National Energy Policy (2004) covers all sorts of energy sources, indicates the way forward and invites the private sector to invest in energy. However, the real life situation has proven otherwise and the progress indicated in the plan is not implemented.

3.2.6TheTypicalInvestmentRouteforPowerGenerationPower generation and energy exploration is fully regulated by the government. To operate in the power generation sector, the company must have a purchasing agreement with the government. The Ministry of Power, Energy and Mineral resources is the one inviting bidders to tender in the power sector. Sometimes companies go directly to the BOI to get a licence, but this is not possible in order to invest in the sector. However, interesting concepts that can help Bangladesh solve its power crisis can be presented to the Ministry of Energy and may be later result in an invitation to tender where the initiator becomes pre-qualified based on the company’s technical solution. All tenders must adhere to the public procurement regulations and the bidding process is assumed to be very transparent and following normal procedures. The tender is published on the Ministry’s website. The winner of the bid will negotiate an agreement with the Power Development Board (PDB) or Rural Electrification Board (REB) on selling power to the grid for the next 15 years under Independent Power Policy (IPP). The contract might indicate a variable part taking into consideration the fuel costs and a non-

23

variable part for other costs. This same tender procedure is expected for exploration of oil and gas as well as for rehabilitation of old power plants. Companies with a power purchasing agreement under the IPP have good experience with selling power to the government in terms of timely payment as well as good profit margins.

3.2.7BusinessOpportunitiesinthePowerandEnergySectorThe business opportunities in the Power and Energy Sector may fall under the following categories:

1) Coal-fired or furnace oil power plants.

2) Rehabilitation of old power plants.

3) Exploration of oil and gas.

4) Selling wafers for local assembly in Bangladesh.

5) Selling solar technology to Bangladesh.

6) Selling technology for biogas plants/investments.

7) Preparing projects for CDM facilities.

8) Follow the developments on tenders for wind and hydropower.

9) Construction of terminal for oil and gas. At present smaller vessels have to reload from mother vessels bringing the oil/gas to Colombo or Singapore or outer anchorage (near Kutubdia Islands) as Bangladesh has no deep sea terminal.

3.3ShipbuildingandMaritimeRelatedActivitiesMaersk is the biggest international actor in maritime related business, and has been present in Bangladesh since 1988. As a result of Bangladesh’ successful entry into the market with garments, the demand for container transport has been increasing steadily over the years. In addition to garments, goods as ceramics, pharmaceuticals and frozen shrimps represent huge need for transport. An estimate shows that every year there is a growing demand of containers about 10%.

3.3.1PlansfortheBangladeshishipbuildingsectorThe market for transport services will increase. According to informants, river vessels carry 70% of the domestic transport. There are approximately 2000 domestic transport vessels in the range from 500 DWT to 2500DWT capacity and in addition to this, there are about 1000 passenger ferries (locally known as Launch) for inland transportation. There are 100 oil tankers carrying 3 mill tons of oil per year. 2 mill people are working in the river transport sector. There is a need for renewing the domestic fleet. Accordingly, shipbuilding is likely to become a growth sector. There is huge optimism on behalf of the sector and many new actors express an interest to diversify into shipbuilding directed towards international markets. Due to cheap and accessible labour, many believe that Bangladesh can become a new destination

24

for international shipbuilding. The industry in Bangladesh lacks experience in building bigger ships (from 5000-6000 DWT). Competence in this type of shipbuilding needs to be developed. The local industry needs access to technology and might be ideal projects for business collaboration between international ship builders and local companies. Bangladesh have no ambition of starting to build big ships (above 6000 DWT) in the near future, but would like to use new technology and international experience to build smaller ships for local and international markets and then increase the size of ships as they get the experience. There is need for training in different technical fields, in naval architecture and design, managerial capacity, dealing with international contracts, quality management, health and safety etc. An order from Europe is regarded the best learning experience as the pressure is on to prove the shipyards ability to compete internationally immediately the contract is closed.

3.3.2EnteringtheinternationalmarketThis is exactly the scenario that Western Marine Shipyard in Chittagong is experiencing at the moment. The Danish B2B program brought representatives from the Danish ship building industry to Bangladesh to look for a local shipyard for contracting vessels. The Western Marine Shipyard caught the interest, but the shipyard was too small. As a result, the shipyard has shifted to a new location with 10 ha land. Construction halls are built. The first vessels are contracted and under construction. 5 vessels of 4500 DWT are contracted to Denmark. Another 6 vessels of 5200 DWT are contracted to Germany. The Western Shipyard has achieved a lot within short time, the acid test proving that it can compete internationally is meeting the deadlines of delivery and keeping the quality focus in every step of the building process. Germanischer Lloyd (GL) is classifying the vessels and follows each step taken in the shipyard. To enter into a contract, the buyer and the seller agree on the details of the contract such as who is buying the equipment, what make of equipment to be fitted, which classification shall be used. The contract should further describe the time schedule for the various steps of the construction such as steel cutting, keel laying, launching and delivery date. Negotiating and agreeing on penalties for not respecting delivery time is also an important part of the contract. Equipment bought from abroad to be fitted into vessels can be imported duty free. This has been tested by the contracting of ships for Denmark.

3.3.3WhatcanBangladeshoffer?According to professionals in the shipping sector, a ship can be built for half the price in Bangladesh comparing with China. Good welders are paid 600 USD per month. Due to recession and lay offs in the Middle East, trained welders returned to Bangladesh. They now find interesting jobs in the ship building industry in Bangladesh, which only recently has started to look at international markets. There are a few recognised shipyards as of now operating in Bangladesh, such as Khulna Shipyard, Narayangonj Shipyard, High Speed Shipyard, Ananda Shipyard, Karnaphuli Shipyard and Western Marine Shipyard. The first 2 shipyards are managed by Bangladesh Navy and mainly used for their own ship repair. There are many local shipyards, engaging in making local cargo ships, oil tankers, fishing vessels and passenger launches. Most of them make their own design and do not follow any classification. Ananda Shipyard has started to build ships for export markets, such as Denmark, Mozambique and Germany. Western Marine Shipyard has come up recently. Both those private shipyards have obtained a handful of international contracts.

Many Bangladeshi entrepreneurs would like to enter the ship-building sector. Most of them can offer access to land, some have already shipyards constructed or planned. They are likely to compete to team up with international ship building actors and presumable good deals can be negotiated in the ship-building sector. What local actors expect from the international actor

25

is everything else; contracts (market), experience, technology, competence, design, brand name etc.

80%oftheproductionfromNorwegianshipyardsisfortheoffshoremarket.MosthullsaretodaybuiltoutsideNorway.TheequipmentmightbefittedeitherintheshipyardbuildingthehullorinaNorwegianyard.Someshipownersexperiencethattechnicallycomplicatedvessels,likeoffshorevessels,benefitfrombeingequippedinNorwegianyards,werelongtermexperienceinfittingsuchequipmentexists.

“Fromprosperitytotroubledtimes”12giveanoverviewoftypesofshipsbuiltduring2008andanupdateofthesituationintheNorwegianshipbuildingsector.

3.3.4Businessopportunities• Constructionofsmallercontainervessels(upto6000DWT)fullyequipped

• Constructionofsmallertankers,fullyequipped

• Constructionofhullsfortheoffshoresector

ContractorsmightprefertheequipmentofoffshoreandspecialpurposevesselstobefittedinNorway,duetolongtermexperienceandavailableexpertise.However,thehullsmightbecontractedanywherewherepriceandqualitymeettherequirementsofthecontractors.

• Weldingjobs‐outsourcingofproductionofequipment

TheDaneshaverecentlycarriedoutastudyontheshipbuildingsectorandwillsendadelegationofcompanyrepresentativestoBangladeshespeciallylookingattheshipbuildingindustryinNovember2009.13

3.4MarineactivitiesFish production has increased rapidly over the past 15-20 years, mainly due to farming of fish and shrimps. The capture fishing in rivers and floodplains has stagnated which is creating some concern, as this has been a major source of income for the landless poor. Reasons for the decrease in inland fisheries are due to urbanization, increased pollution and unregulated overfishing.14 Inland aquaculture is the largest source of fish production in the country, with

12www.nmi2008.com/2009/02/19/from‐prosperity‐to‐troubled‐times/

13 http://www.thedailystar.net/newDesign/news-details.php?nid=108927

14Bangladesh:StrategyforSustainedGrowth,2007,p.63

26

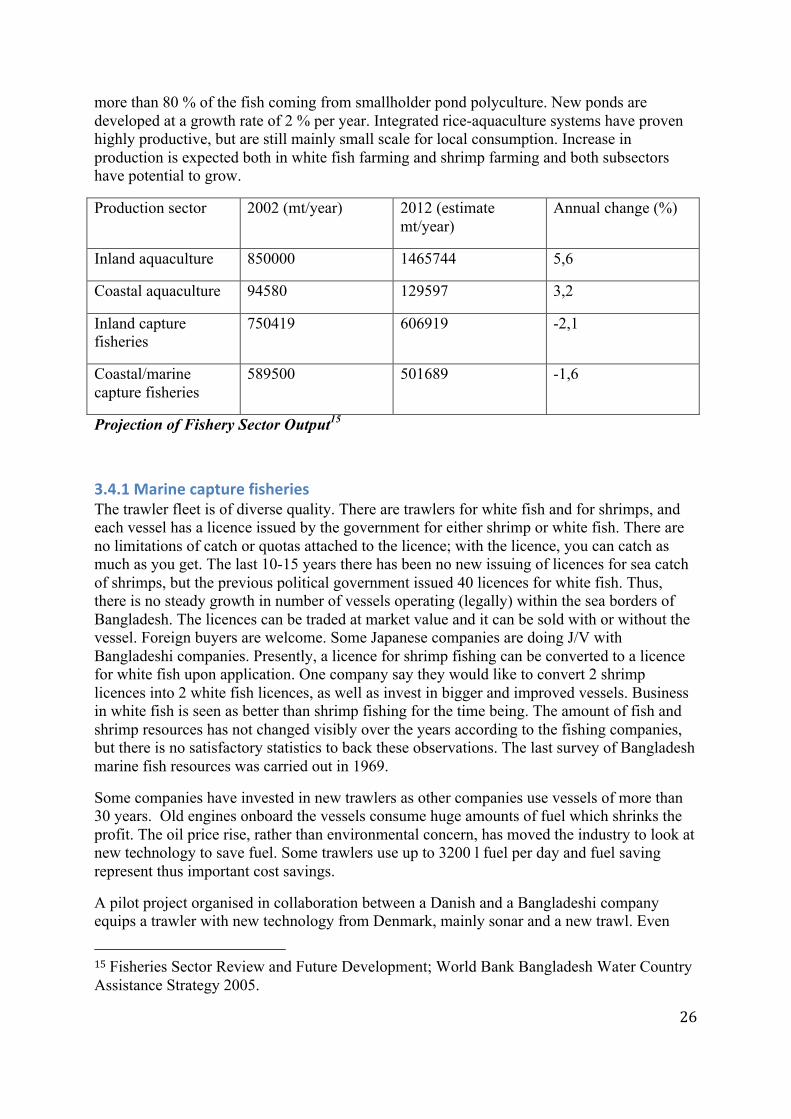

more than 80 % of the fish coming from smallholder pond polyculture. New ponds are developed at a growth rate of 2 % per year. Integrated rice-aquaculture systems have proven highly productive, but are still mainly small scale for local consumption. Increase in production is expected both in white fish farming and shrimp farming and both subsectors have potential to grow.

Production sector 2002 (mt/year) 2012 (estimate mt/year)

Annual change (%)

Inland aquaculture 850000 1465744 5,6

Coastal aquaculture 94580 129597 3,2

Inland capture fisheries

750419 606919 -2,1

Coastal/marine capture fisheries

589500 501689 -1,6

Projection of Fishery Sector Output15

3.4.1MarinecapturefisheriesThe trawler fleet is of diverse quality. There are trawlers for white fish and for shrimps, and each vessel has a licence issued by the government for either shrimp or white fish. There are no limitations of catch or quotas attached to the licence; with the licence, you can catch as much as you get. The last 10-15 years there has been no new issuing of licences for sea catch of shrimps, but the previous political government issued 40 licences for white fish. Thus, there is no steady growth in number of vessels operating (legally) within the sea borders of Bangladesh. The licences can be traded at market value and it can be sold with or without the vessel. Foreign buyers are welcome. Some Japanese companies are doing J/V with Bangladeshi companies. Presently, a licence for shrimp fishing can be converted to a licence for white fish upon application. One company say they would like to convert 2 shrimp licences into 2 white fish licences, as well as invest in bigger and improved vessels. Business in white fish is seen as better than shrimp fishing for the time being. The amount of fish and shrimp resources has not changed visibly over the years according to the fishing companies, but there is no satisfactory statistics to back these observations. The last survey of Bangladesh marine fish resources was carried out in 1969.

Some companies have invested in new trawlers as other companies use vessels of more than 30 years. Old engines onboard the vessels consume huge amounts of fuel which shrinks the profit. The oil price rise, rather than environmental concern, has moved the industry to look at new technology to save fuel. Some trawlers use up to 3200 l fuel per day and fuel saving represent thus important cost savings.

A pilot project organised in collaboration between a Danish and a Bangladeshi company equips a trawler with new technology from Denmark, mainly sonar and a new trawl. Even

15Fisheries Sector Review and Future Development; World Bank Bangladesh Water Country Assistance Strategy 2005.

27

though there has been some start up problems due to different behaviour of the seas (different forces; undercurrent, over current etc.), the pilot testing proves promising, as the pilot vessel has increased the catching capacity with almost 100 %. The project in collaboration with Danish industry aims at starting production of trawl nets in Bangladesh for supply to the market in and adjacent to the Bay of Bengal. An estimate of costs for locally produced equipment is said to be 20 % of the cost of equipment from Denmark.

White fish and wild catch sea prawns are exported. One company visited has 7 trawlers for white fish and 8 for prawns. The vessels are fairly modern and the catch is processed on board. The export is solely block-frozen fish and shrimps and it goes exclusively to the Japanese market. HACCP standards are in place in the processing plants. In the future, the company plans to increase the value addition of the products and fulfil market requirements of the US and EU markets. So far, the Japanese market has been able to pay more than EU and US markets, but the fishery sector is increasingly interested in the EU and US markets.

There are a handful of professional fishing companies in Bangladesh. Typically, these companies are diversified into the sea transport business or even into shipbuilding having their own yard for new construction and maintenance. Forward and backward integration – with companies owned by the same group covering most of the value chain is common in Bangladesh.

3.4.2ShrimpsFarmed shrimps are mainly family businesses and only two out of many companies are listed. It is therefore difficult to get an idea of the profitability. Productivity in Bangladesh is very low, compared with e.g. Thailand, the leading shrimp exporter in the region. Current productivity in Bangladesh is 150 kg/ha, while Thailand has 4-7 tons per ha. Increased productivity is possible through extension services, better construction of ponds, improved hatchery and water management, reduced post larvae mortality as well as improvements in post harvest handling to increase the quality and safety of the final product.16

The sea catch of shrimps has the highest value. The shrimps are processed and packed on board the vessel and export is mainly going to Japan as frozen shrimps. Of the total production of Bangladeshi shrimps, only 10 % is sea catch. 90 % is farmed shrimps.

The second best quality is the farmed shrimps in the brackish water in the coastal belt, the black tiger shrimps. 1/3 of the sea farms are located in Eastern Bangladesh, from Chittagong to Cox’s Bazaar, the rest of the farms are in the West of Bangladesh. Farmed sea prawns in the coastal belt amounts to 60 % of the total shrimp export.

Fresh water prawns are found in ponds in many parts of Bangladesh and comprise 30 % of the total shrimp export (including catch). The shrimp farming amounts to the second largest export sector after RMG. Many of the actors are small holders with a few hundred kilos to sell. Many development programs have been directed towards quality improvements within shrimp farming, still there is a lot of issues to deal with. Government – NGO partnership has proven to be the most effective means for improving smallholder aquaculture. The associations organising the farmers are seen to be weak.

16Bangladesh;StrategyforSustainedGrowth,2007,p.62

28

3.4.3FishfeedandhealthandsafetyissuesBoth local feed and imported feed are available for the shrimp and fish farmers. Chemical additives such as antibiotics are sometimes found in the feed and residues of antibiotics have been detected in exported shrimp. There is no proper public control of the fish and shrimp feed. A container of fresh water shrimp was rejected at the EU border, and this caused a ban on export of fresh water prawns for some time. The processing plants have laboratories to test the levels of bacteria and salmonella before export, and these factors are under control. The Fish Inspection and Quality Control (FIQC), under the Ministry of Fisheries is in charge of testing fish products going to the market. However, the capacity is lacking and they will only test samples to track antibiotics and chemicals. There is no government or private system to monitor the production at farm level and to test chemical residues in the product before going to the market.

There are many processing plants, especially for farmed shrimps. Some are well equipped with HACCP requirements in order for export to the EU. There might be some over capacity of processing plants as companies compete for the raw material to fully utilise their premises.

3.4.4BusinessopportunitiesCage farming as we know from Norway is not seen as very relevant at the moment although Koreans are about to start a pilot project, which should be followed with interest. If successful, this might open opportunities for production and selling of equipment for sea farming. Farming of shrimps is in general unknown to Norwegian fish farmers. Areas of interest for Norwegian expertise might be production of fish and shrimp feed as well as developing farm based programs to improve shrimp health and the environment situation. The latter might be launched as an object for a public private partnership provided the government would like to invest in the shrimp business and secure the sector in the future. As tracking of produce is becoming a necessity for export, there is an urgent need for control with chemical residues as well as farm based quality programs if the shrimp business in Bangladesh shall be able to compete in a market more and more concerned about food safety.

The potential for selling Norwegian salmon in the Dhaka shops is unclear. It is mentioned that people’s taste is traditional. On the other hand, there are 10 million people in Bangladesh with high purchasing power. There is an increase of foreign business people from Korea and China living in Bangladesh demanding most types of seafood. The big hotels serve sushi and sashimi made partly from Norwegian salmon.

The fishing sector needs investors and competence from outside. Marine capture fisheries and the processing industry can benefit from value addition of the catch as well as access to improved equipment and vessels. Norwegian investors can bring farm management and health and safety systems into the inland aquaculture. To reach the EU –market, there is a need to bring in expertise that knows the taste and the demands in the EU market.

• Breeding and production of fresh water and marine species

• Equipment for processing plants and sea based cage farming

• Improved vessels – fuel saving machinery, improved equipment and fishing gear

• Farm health programs – and farm management programs in collaboration with public programs

• Shrimp and fish feed production

29