Nonprofit Organizations Spring 2004 Class Six: Overview of Federal Tax Considerations/Income Tax...

24

Nonprofit Nonprofit Organizations Organizations Spring Spring 2004 2004 Class Six: Overview of Class Six: Overview of Federal Tax Federal Tax Considerations/Income Tax Considerations/Income Tax Rules Relating to Tax-Exempt Rules Relating to Tax-Exempt Organizations Organizations Michelle Coleman-Johnson Bourland, Wall & Wenzel, P.C. 817-877-1088 [email protected]

-

Upload

amberly-greer -

Category

Documents

-

view

215 -

download

1

Transcript of Nonprofit Organizations Spring 2004 Class Six: Overview of Federal Tax Considerations/Income Tax...

Nonprofit Nonprofit OrganizationsOrganizations Spring Spring 20042004

Class Six: Overview of Federal Tax Class Six: Overview of Federal Tax Considerations/Income Tax Rules Considerations/Income Tax Rules Relating to Tax-Exempt Relating to Tax-Exempt OrganizationsOrganizations

Michelle Coleman-Johnson

Bourland, Wall & Wenzel, P.C.

817-877-1088

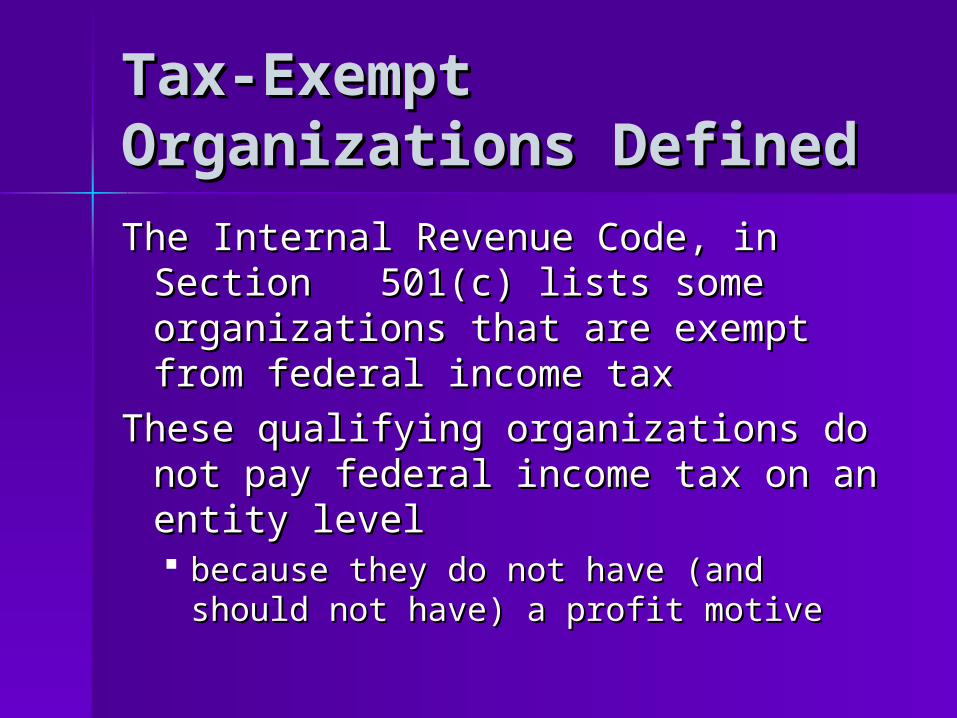

Tax-Exempt Tax-Exempt Organizations DefinedOrganizations Defined

The Internal Revenue Code, in Section The Internal Revenue Code, in Section 501(c) lists some organizations 501(c) lists some organizations that are exempt from federal that are exempt from federal income taxincome tax

These qualifying organizations do not These qualifying organizations do not pay federal income tax on an entity pay federal income tax on an entity levellevel because they do not have (and should because they do not have (and should

not have) a profit motivenot have) a profit motive

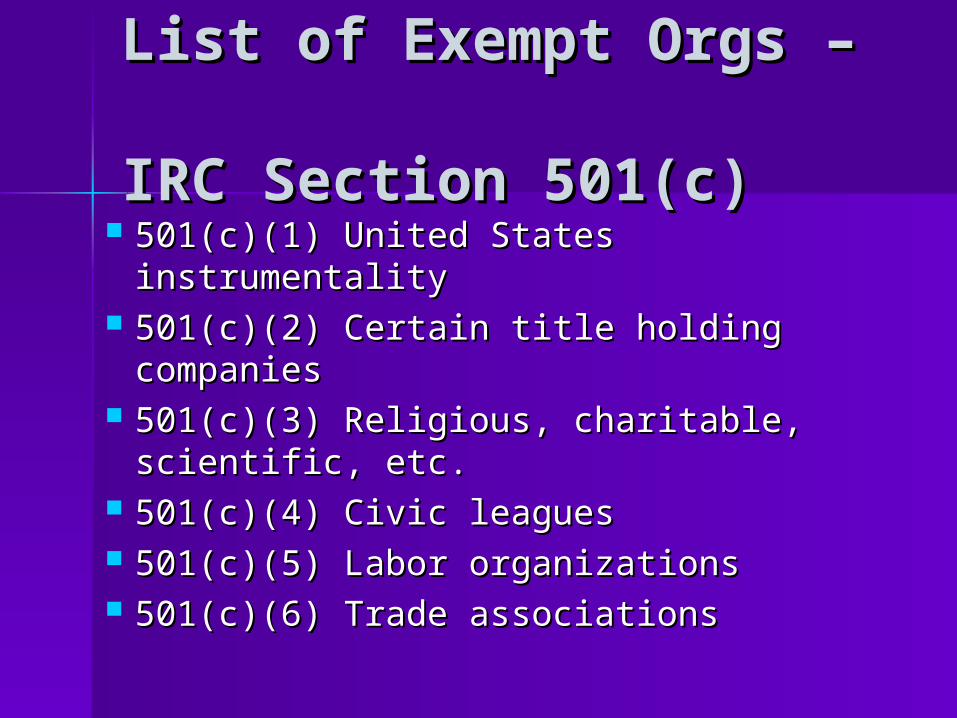

List of Exempt Orgs – List of Exempt Orgs – IRC Section 501(c)IRC Section 501(c)

501(c)(1) United States instrumentality501(c)(1) United States instrumentality 501(c)(2) Certain title holding 501(c)(2) Certain title holding

companiescompanies 501(c)(3) Religious, charitable, 501(c)(3) Religious, charitable,

scientific, etc.scientific, etc. 501(c)(4) Civic leagues501(c)(4) Civic leagues 501(c)(5) Labor organizations501(c)(5) Labor organizations 501(c)(6) Trade associations501(c)(6) Trade associations

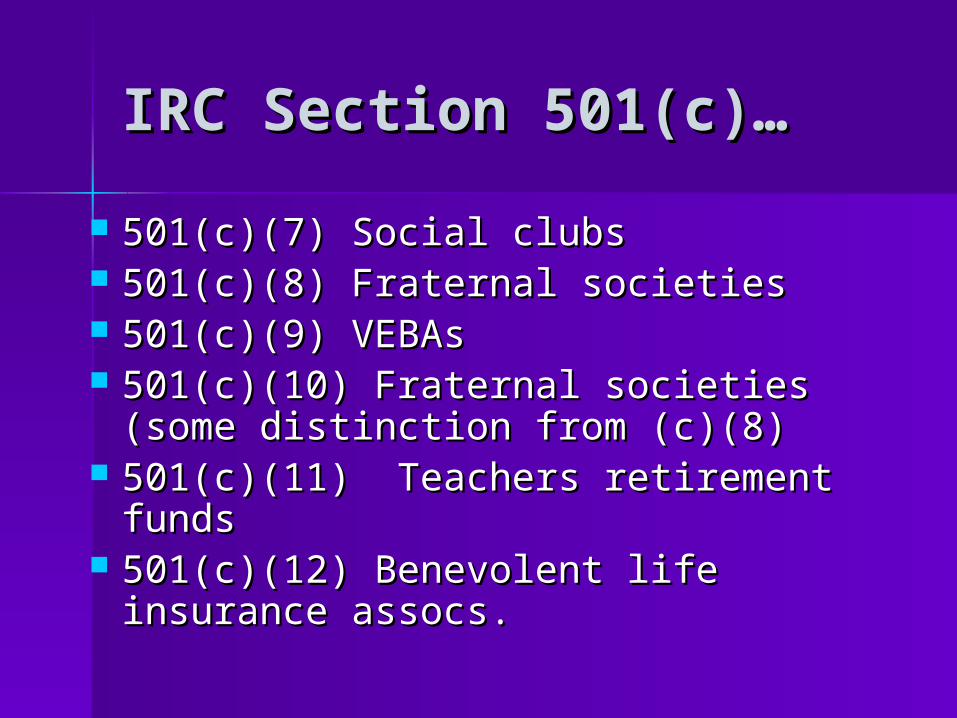

IRC Section 501(c)…IRC Section 501(c)…

501(c)(7) Social clubs501(c)(7) Social clubs 501(c)(8) Fraternal societies 501(c)(8) Fraternal societies 501(c)(9) VEBAs501(c)(9) VEBAs 501(c)(10) Fraternal societies (some 501(c)(10) Fraternal societies (some

distinction from (c)(8)distinction from (c)(8) 501(c)(11) Teachers retirement funds501(c)(11) Teachers retirement funds 501(c)(12) Benevolent life insurance 501(c)(12) Benevolent life insurance

assocs.assocs.

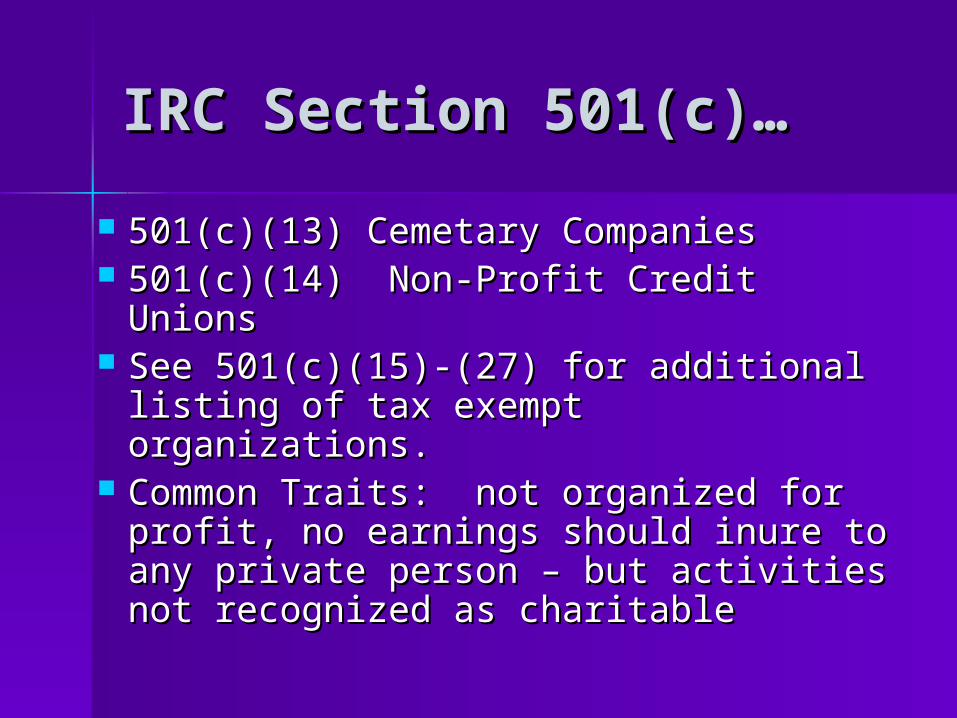

IRC Section 501(c)…IRC Section 501(c)…

501(c)(13) Cemetary Companies501(c)(13) Cemetary Companies 501(c)(14) Non-Profit Credit Unions 501(c)(14) Non-Profit Credit Unions See 501(c)(15)-(27) for additional See 501(c)(15)-(27) for additional

listing of tax exempt organizations.listing of tax exempt organizations. Common Traits: not organized for Common Traits: not organized for

profit, no earnings should inure to profit, no earnings should inure to any private person – but activities any private person – but activities not recognized as charitable not recognized as charitable

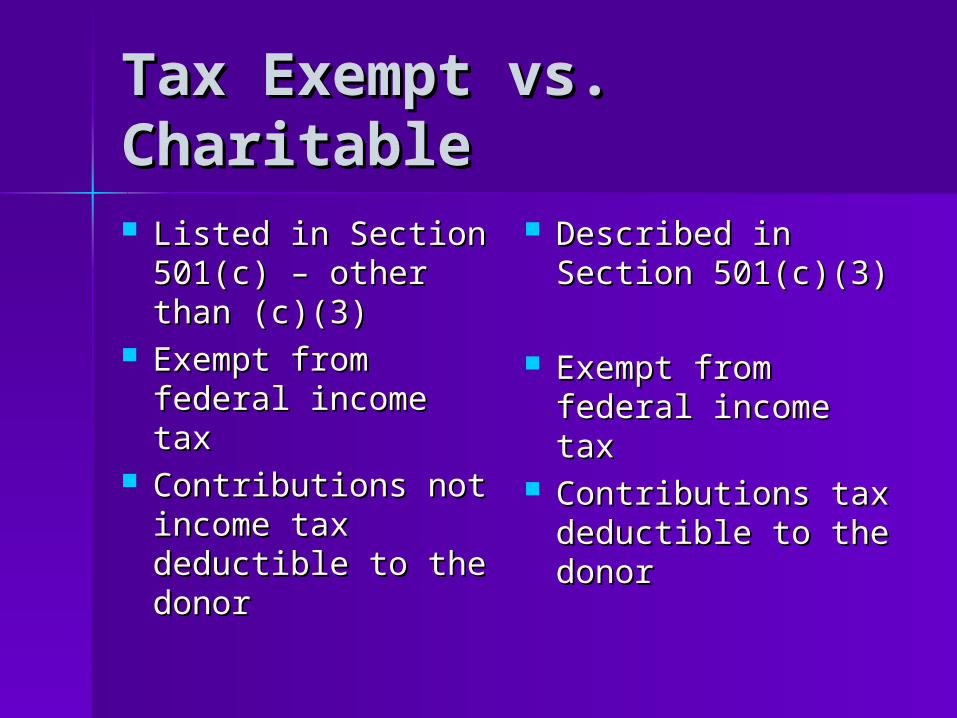

Tax Exempt vs. Tax Exempt vs. CharitableCharitable Listed in Section Listed in Section

501(c) – other 501(c) – other than (c)(3)than (c)(3)

Exempt from Exempt from federal income taxfederal income tax

Contributions not Contributions not income tax income tax deductible to the deductible to the donordonor

Described in Described in Section 501(c)(3)Section 501(c)(3)

Exempt from Exempt from federal income federal income taxtax

Contributions tax Contributions tax deductible to the deductible to the donordonor

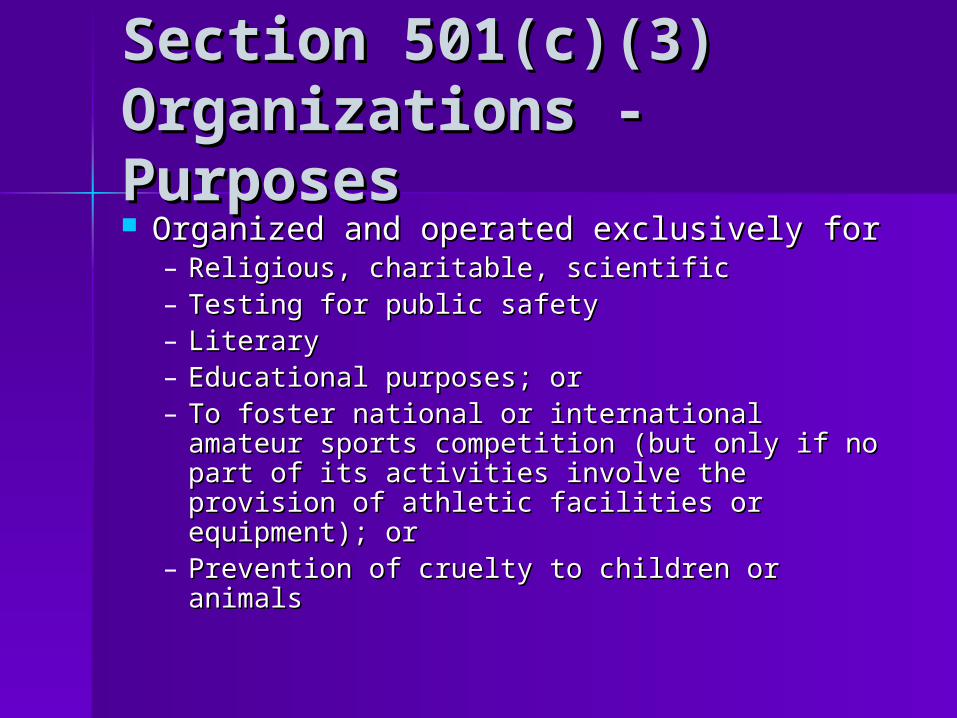

Section 501(c)(3) Section 501(c)(3) Organizations - Organizations - PurposesPurposes Organized and operated exclusively for Organized and operated exclusively for

– Religious, charitable, scientificReligious, charitable, scientific– Testing for public safetyTesting for public safety– LiteraryLiterary– Educational purposes; orEducational purposes; or– To foster national or international amateur To foster national or international amateur

sports competition (but only if no part of sports competition (but only if no part of its activities involve the provision of its activities involve the provision of athletic facilities or equipment); orathletic facilities or equipment); or

– Prevention of cruelty to children or animalsPrevention of cruelty to children or animals

501(c)(3) Orgs – 501(c)(3) Orgs – Prohibited ActivitiesProhibited Activities No part of net earnings may inure No part of net earnings may inure

to the benefit of any private to the benefit of any private shareholder or individualshareholder or individual– Private benefit/inurement doctrinePrivate benefit/inurement doctrine

No substantial part of activities No substantial part of activities may be carrying on propaganda, may be carrying on propaganda, or otherwise attempting, to or otherwise attempting, to influence legislationinfluence legislation– Except as provided in (c)(h)Except as provided in (c)(h)

501(c)(3) 501(c)(3) Organizations – Organizations – Prohibited ActivitiesProhibited Activities May not participate in, or May not participate in, or

intervene in (including the intervene in (including the publishing or distributing of publishing or distributing of statements) any political statements) any political campaign on behalf of (or in campaign on behalf of (or in opposition to) any candidate for opposition to) any candidate for public office.public office.

Charitable Charitable ContributionsContributions Donors are allowed an income tax Donors are allowed an income tax

charitable deduction for charitable deduction for contributions to 501(c)(3) contributions to 501(c)(3) organizationsorganizations– See sections 170(a)(1) and 170(b)(1)See sections 170(a)(1) and 170(b)(1)

(A)(A)– Some organizations are “charitable” Some organizations are “charitable”

by definition or by the activities by definition or by the activities carried oncarried on

Private Foundation – under section Private Foundation – under section 509(a), an organization is presumed 509(a), an organization is presumed to be a private foundation unless it to be a private foundation unless it is demonstrated that it fits an is demonstrated that it fits an exception, and thus is a public exception, and thus is a public charitycharity

Further Classification - Further Classification - Private FoundationPrivate Foundation

Types of Public Types of Public CharitiesCharities

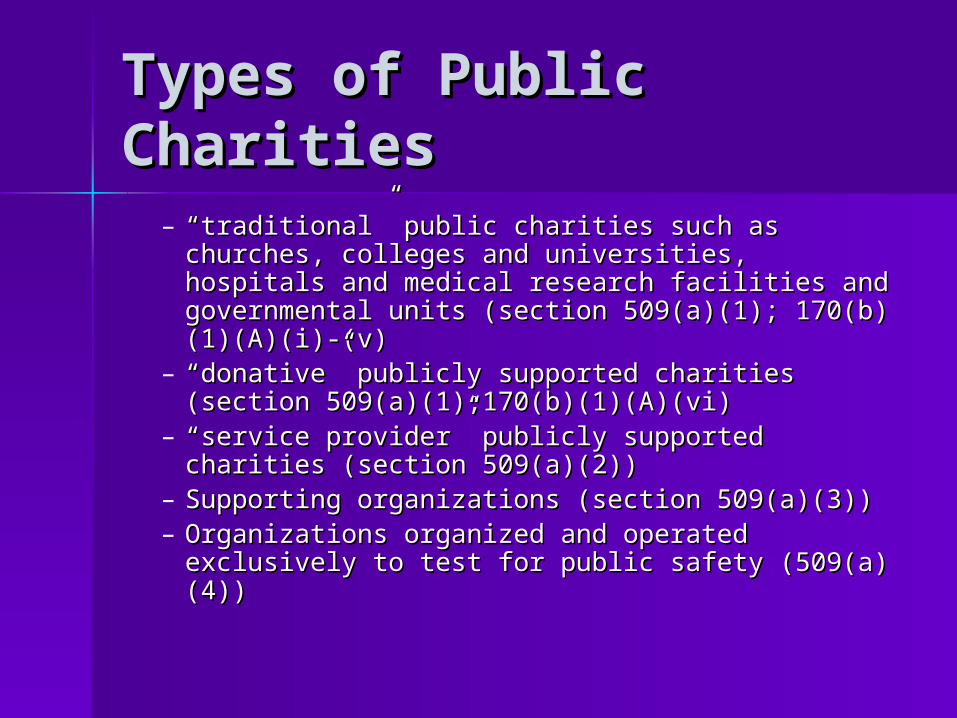

– ““traditional” public charities such as churches, traditional” public charities such as churches, colleges and universities, hospitals and colleges and universities, hospitals and medical research facilities and governmental medical research facilities and governmental units (section 509(a)(1); 170(b)(1)(A)(i)-(v)units (section 509(a)(1); 170(b)(1)(A)(i)-(v)

– ““donative” publicly supported charities donative” publicly supported charities (section 509(a)(1);170(b)(1)(A)(vi)(section 509(a)(1);170(b)(1)(A)(vi)

– ““service provider” publicly supported charities service provider” publicly supported charities (section 509(a)(2))(section 509(a)(2))

– Supporting organizations (section 509(a)(3))Supporting organizations (section 509(a)(3))– Organizations organized and operated Organizations organized and operated

exclusively to test for public safety (509(a)(4))exclusively to test for public safety (509(a)(4))

Examples of Public Examples of Public CharitiesCharities Community Foundation (donative Community Foundation (donative

public charity)public charity) Boy Scouts/Girl Scouts (typically a Boy Scouts/Girl Scouts (typically a

service provider public charity)service provider public charity) Baylor University (educational Baylor University (educational

institution – not required to meet institution – not required to meet support test)support test)

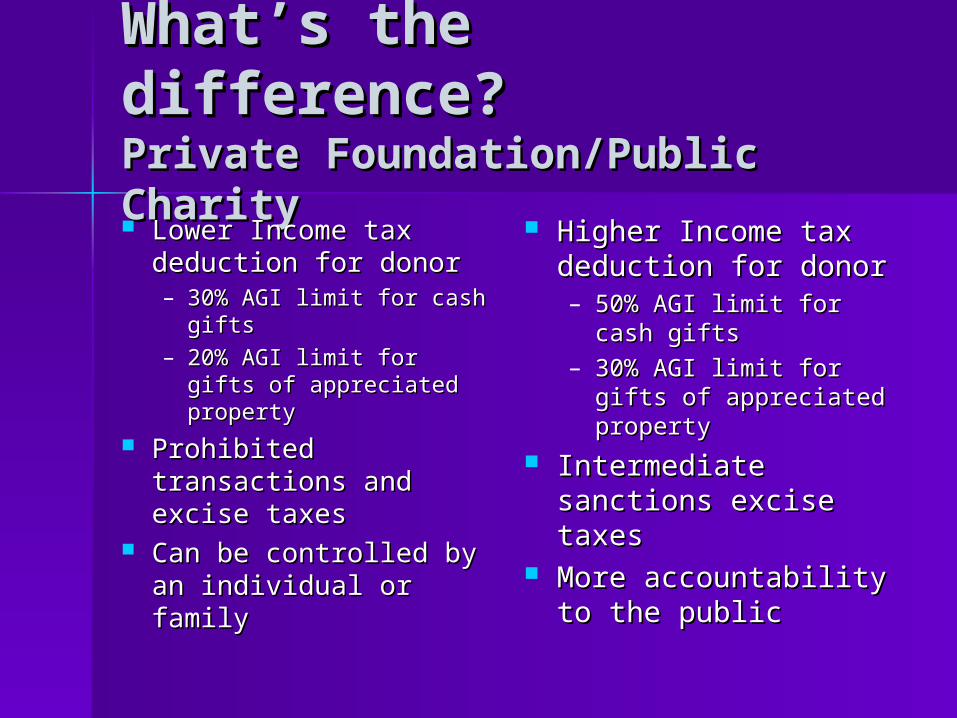

What’s the difference? What’s the difference? Private Foundation/Public Private Foundation/Public CharityCharity Lower Income tax Lower Income tax

deduction for donordeduction for donor– 30% AGI limit for cash 30% AGI limit for cash

giftsgifts– 20% AGI limit for gifts 20% AGI limit for gifts

of appreciated propertyof appreciated property Prohibited Prohibited

transactions and transactions and excise taxesexcise taxes

Can be controlled by Can be controlled by an individual or familyan individual or family

Higher Income tax Higher Income tax deduction for donordeduction for donor– 50% AGI limit for cash 50% AGI limit for cash

giftsgifts– 30% AGI limit for gifts 30% AGI limit for gifts

of appreciated of appreciated propertyproperty

Intermediate Intermediate sanctions excise sanctions excise taxestaxes

More accountability More accountability to the publicto the public

Recognition of Tax Recognition of Tax Exempt StatusExempt Status

1.1. Organize for state law purposes Organize for state law purposes • in Texas, can be unincorporated in Texas, can be unincorporated

association, trust or non-profit association, trust or non-profit corporationcorporation

2.2. File IRS Form 1023, Application File IRS Form 1023, Application for Recognition of Exemption for Recognition of Exemption Under Section 501(c)(3) of the Under Section 501(c)(3) of the Internal Revenue CodeInternal Revenue Code

• If seeking exemption under another If seeking exemption under another section, file Form 1024section, file Form 1024

Form 1023Form 1023

Filed within 15 months from the Filed within 15 months from the end of the month of organization end of the month of organization (date of formation or (date of formation or incorporation)incorporation)– Automatic 12 month extension – to Automatic 12 month extension – to

27 months from formation27 months from formation– Additional extension may be granted Additional extension may be granted

for good causefor good cause

Effect of Timely and Effect of Timely and Complete Filing of Complete Filing of 10231023 Once approved, IRS will issue either a Once approved, IRS will issue either a

determination letter or an advance determination letter or an advance ruling, depending on the type of ruling, depending on the type of organizationorganization– Determination letter – evidence of an Determination letter – evidence of an

organization’s exempt statusorganization’s exempt status– Advance ruling – for public charities Advance ruling – for public charities

subject to a support test, a preliminary subject to a support test, a preliminary ruling that will be again examined after an ruling that will be again examined after an initial five year periodinitial five year period

Substantiation RulesSubstantiation Rules

Substantiation documentation for Substantiation documentation for donationsdonations– A charitable organization must issue A charitable organization must issue

substantiation letters to its donors where the substantiation letters to its donors where the donation has a value of $250 or moredonation has a value of $250 or more

– Must be in writing and state whether goods or Must be in writing and state whether goods or services were provided in returnservices were provided in return

– If gift of appreciated property is received and If gift of appreciated property is received and sold within 2 years of acquisition, the charity sold within 2 years of acquisition, the charity must prepare and file Form 8282must prepare and file Form 8282

– See Publication 1771 for further guidanceSee Publication 1771 for further guidance

Common Issues:Common Issues:Unrelated Business Taxable Unrelated Business Taxable Income (UBTI)Income (UBTI) Income from an unrelated trade Income from an unrelated trade

or businessor business– Taxed at highest corporate rateTaxed at highest corporate rate– Could result in loss of exemption if Could result in loss of exemption if

substantialsubstantial– Theory: tax exempt organizations Theory: tax exempt organizations

should not be in competition with should not be in competition with for-profit businessesfor-profit businesses

UBTI DefinedUBTI Defined

Income from any regularly Income from any regularly conducted trade or business conducted trade or business which is not substantially related which is not substantially related to the performance of the to the performance of the organization’s exempt functionorganization’s exempt function

UBTI ExclusionsUBTI Exclusions

Passive income such as dividends Passive income such as dividends and interest, rents, royalties, and interest, rents, royalties, certain gains or losses from sale, certain gains or losses from sale, exchange or other disposition of exchange or other disposition of propertyproperty

Income from some research Income from some research (Section 512(b))(Section 512(b))

UBTI ExceptionsUBTI Exceptions

Volunteer exceptionVolunteer exception– Where substanitally all the work in carrying Where substanitally all the work in carrying

on the trade or business is performed for the on the trade or business is performed for the exempt organization without compensationexempt organization without compensation

Convenience exceptionConvenience exception– Governmental college or university, Governmental college or university,

primarily for the convenience of its primarily for the convenience of its members, students, patients, officers or members, students, patients, officers or employees (dining hall)employees (dining hall)

Selling of donated merchandise (ex: Selling of donated merchandise (ex: thrift store)thrift store)

UBTI – Debt Financed UBTI – Debt Financed PropertyProperty Income incurred with respect to debt-Income incurred with respect to debt-

financed propertyfinanced property– Any property held to produce income and Any property held to produce income and

with respect to which there is acquisition with respect to which there is acquisition indebtednessindebtedness

– Acquisition indebtedness – debt incurred in Acquisition indebtedness – debt incurred in connection with acquisition or connection with acquisition or improvement of propertyimprovement of property

Exclusions: See Section 514 – beyond scope of Exclusions: See Section 514 – beyond scope of classclass

Future ClassesFuture Classes

Private FoundationsPrivate Foundations

- prohibited transactions- prohibited transactions

- excise taxes- excise taxes Public CharitiesPublic Charities

- intermediate sanctions- intermediate sanctions

- support tests- support tests