Non-Walrasian Labor Markets I: The McCall Search Model · PDF fileOutlineMotivationTwo models...

47

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state Non-Walrasian Labor Markets I: The McCall Search Model Timothy Kam School of Economics & CAMA Australian National University ECON8022, This version May 28, 2008

Transcript of Non-Walrasian Labor Markets I: The McCall Search Model · PDF fileOutlineMotivationTwo models...

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Non-Walrasian Labor Markets I: TheMcCall Search Model

Timothy Kam

School of Economics & CAMAAustralian National University

ECON8022, This version May 28, 2008

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Outline

1 Motivation

2 Two models

3 McCall’s modelGeneral descriptionDecision problemEffect of mean-preserving spreadLayoffs

4 Waiting times

5 Average dynamics

6 Steady state

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Motivation

Statistically, level of unemployment measured as number ofpeople

1 not currently employed, and2 actively seeking work.

Data: non-trivial and quite persistent rates of unemployment.

Deficiency in some theories:1 limitations to Walrasian equilibrium theories of labor market.2 “level of employment” measured at the “intensive margin” – i.e. can vary

the amount of hours work.3 Individuals do fall out of employment altogether – no variations on

aggregate employment on the “extensive margin”.4 earlier unemployment models based on efficiency wages or labor union

theories similar.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

An alternative theory:

Heterogenous goods (labor) with no single marketplace toclear excess demand or supply; and

Parties to a trade must search for someone to trade with.

Double coincidence of wants problem.

i.e. involve transactions costs – it takes time for a person to lookfor a job and it takes time for a vacancy to find a worker.

Search frictions can potentially rationalize significant transit timesbetween unemployment and employment in a equilibrium wheremarkets do not necessarily need to clear.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

We will look at two basic models:

1 one-sided, partial-equilibrium models of job search: McCall(1970) – an optimal stopping time example.

2 Mortensen (1982), Pissarides (2000) and Diamond (1982)search and matching model.

Here we will apply stochastic DP techniques we have learned.

Extensions: see recent survey of the state of the literature, seeRogerson, Shimer, and Wright (2004).

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

McCall one-sided search

Features:

1 Representative unemployed worker’s Markov decision problem.

2 Worker faces given distribution of job offers per period.

3 Binary choice: accept/reject.

4 If accept stay in job forever (or may be laid of in eachsubsequent period with some probability).

5 If reject, take compensation payout, and wait to search nextperiod.

6 Implications for aggregate/average unemployment dynamics.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Let wage offer w be a continuous random variable with cumulativeprobability distribution function F (W ) defined by

Pr (w ≤W ) = F (W ) .

Properties of wage offer distribution:

Wage offers are non-negative; and

It does not make sense to have infinitely positive wage.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

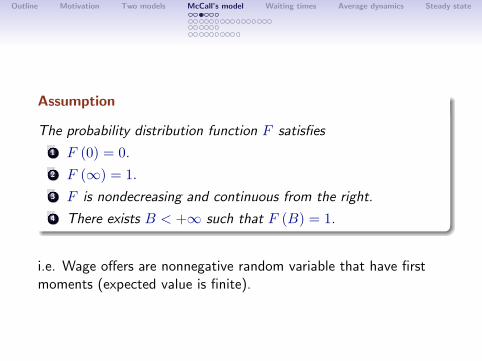

Assumption

The probability distribution function F satisfies

1 F (0) = 0.

2 F (∞) = 1.3 F is nondecreasing and continuous from the right.

4 There exists B < +∞ such that F (B) = 1.

i.e. Wage offers are nonnegative random variable that have firstmoments (expected value is finite).

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

The expected value or mean of w is

E (w) =∫ B

0wdF (w)

Note we can integrate by parts:∫ B

0wdF (w) = wF (w)|B0 −

∫ B

0F (w) dw

= B −∫ B

0F (w) dw

so we can also write

E (w) = B −∫ B

0F (w) dw.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Example

Consider event of independent drawing of w1 and w2 that are lessthan w from distribution F : i.e. the event{(w1 < w) ∩ (w2 < w)} . Then

Pr {(w1 < w) ∩ (w2 < w)} = Pr {max (w1, w2) < w}= F (w)2

The random variable max (w1, w2) has mean

E [max (w1, w2)] = B −∫ B

0F (w)2 dw.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

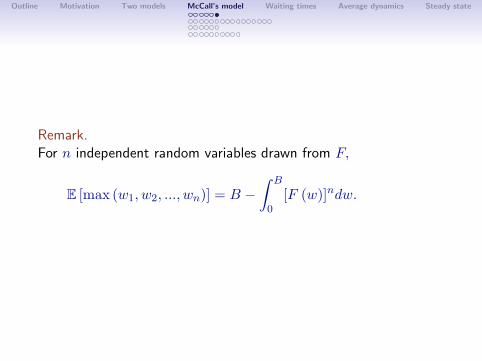

Remark.For n independent random variables drawn from F,

E [max (w1, w2, ..., wn)] = B −∫ B

0[F (w)]ndw.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

The decision problem

Each period worker draws offer w from fixed wage distributionF (W ) = Pr (w ≤W ).

F (W ) satisfies Assumption 1.

Worker’s income per period is yt.

worker can reject w this period and keep searching – i.e. waitfor next period offer w′. Meanwhile receives unemploymentcompensation, yt = c.

or, he can accept w and receives yt = w per period forever(no quits or firing).

worker has no recall.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

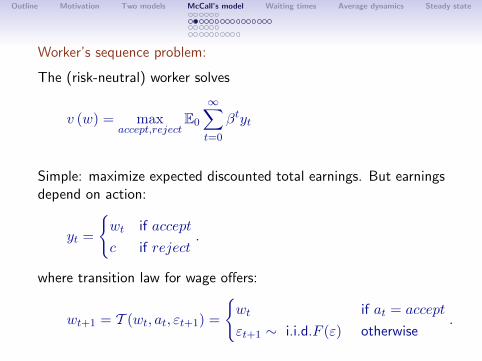

Worker’s sequence problem:

The (risk-neutral) worker solves

v (w) = maxaccept,reject

E0

∞∑t=0

βtyt

Simple: maximize expected discounted total earnings. But earningsdepend on action:

yt =

{wt if accept

c if reject.

where transition law for wage offers:

wt+1 = T (wt, at, εt+1) =

{wt if at = accept

εt+1 ∼ i.i.d.F (ε) otherwise.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

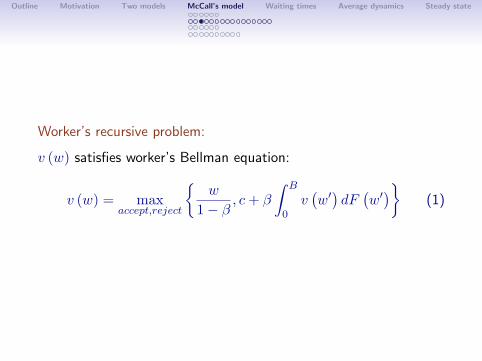

Worker’s recursive problem:

v (w) satisfies worker’s Bellman equation:

v (w) = maxaccept,reject

{w

1− β, c+ β

∫ B

0v(w′)dF(w′)}

(1)

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Worker’s optimal policy function:

The optimal action ∈ {accept, reject} is characterized by:

v (w) =

{c+ β

∫ B0 v (w′) dF (w′) := w

1−β if w < ww

1−β if w ≥ w(2)

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

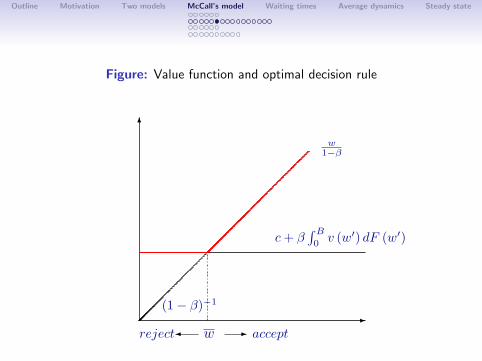

Figure: Value function and optimal decision rule

6

-(1− β)−1

w1−β

c+ β∫ B0v (w′) dF (w′)

w

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Figure: Value function and optimal decision rule

6

-(1− β)−1

w1−β

c+ β∫ B0v (w′) dF (w′)

w accept-reject�

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Note that:

If w < w: reject offer w and get c plus continuation value ofsearching.

A wage offer w s.t. it provides the same present discountedvalue as that from reject and keep searching, is the worker’sreservation wage.

If w ≥ w: Accept w and get w forever.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

At the optimal reservation wage, w,

w

1− β= c+ β

∫ B

0v(w′)dF(w′)

is equivalent to, after some manipulation,

w − c =β

1− β

∫ B

w

(w′ − w

)dF(w′).

LHS ≡ cost of being unemployed at current offer w and searchingagain next period. RHS ≡ expected present value benefit ofsearching one more time in terms of drawing w′ > w.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

w − c =β

1− β

∫ B

w

(w′ − w

)dF(w′).

Jonesy says: “This is just Cost-Benefit Analysis!”

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

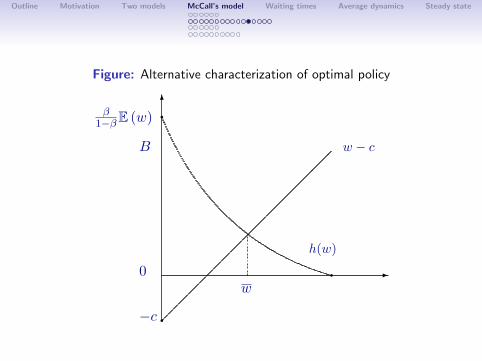

Let the RHS expression for any current offer w be

h (w) ≡ β

1− β

∫ B

w

(w′ − w

)dF(w′).

Note:

h (0) = β1−β

∫ B0 w′dF (w′) = β

1−βE (w) and

h (B) = 0.

h (w) is convex to the origin. Applying Leibniz’s rule:

h′ (w) = − β

1− β[1− F (w)] < 0.

Also

h′′ (w) =β

1− βF ′ (w) > 0.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Exercise

Draw a diagram showing w − c = β1−β

∫ Bw (w′ − w) dF (w′) .

What happens to the solution w if the government increasesunemployment benefits c exogenously?

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Figure: Alternative characterization of optimal policy

6

-

q

q

qw

h(w)

w − c

−c

0

B

β1−βE (w)

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

What is mean preserving spread?

Useful for experimenting with “turbulence in economy”.Interpret as riskiness has increased (in downturns), holdingaverage wage offer constant.

Consider a family of distributions that have the same mean.

We can index distributions in this class by a parameter r ∈ R,where R is some arbitrary index set.

So the rth distribution in our family of distributions withidentical mean is denoted by

Pr (w ≤W ) = F (W, r) .

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

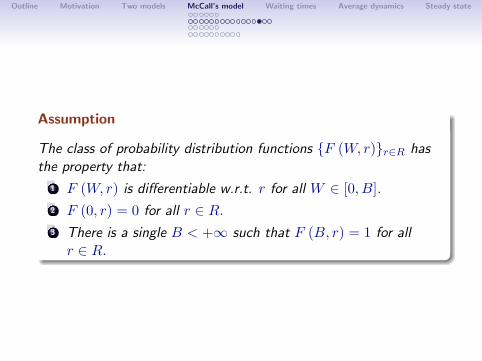

Assumption

The class of probability distribution functions {F (W, r)}r∈R hasthe property that:

1 F (W, r) is differentiable w.r.t. r for all W ∈ [0, B].2 F (0, r) = 0 for all r ∈ R.3 There is a single B < +∞ such that F (B, r) = 1 for allr ∈ R.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Consider R an uncountable set.

Definition

An increase in r represents a mean-preserving increase in risk if∫ B

0

∂F (w, r)∂r

dw = 0 (3)

and ∫ y

0

∂F (w, r)∂r

dw ≥ 0, 0 ≤ y ≤ B. (4)

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

In words, what we want in mean-preserving spread is:

1 Expected value of the r.v. is unchanged as we switch“infinitesimally” from one distribution r to another r + ∂r.

2 But this is done by putting “more mass on the tails” of thedistribution.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Effect of mean-preserving spreadFor another way to see how w is determined we go back to theequation

w − c =β

1− β

∫ B

w

(w′ − w

)dF(w′).

which equates the cost to the benefit of searching.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

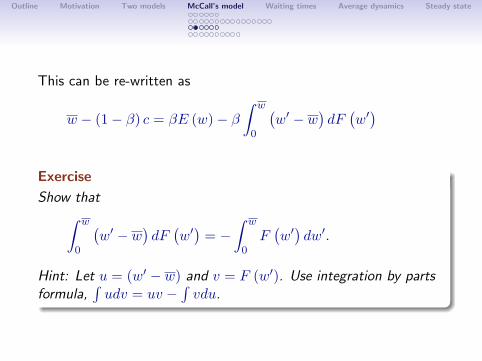

This can be re-written as

w − (1− β) c = βE (w)− β∫ w

0

(w′ − w

)dF(w′)

Exercise

Show that∫ w

0

(w′ − w

)dF(w′)

= −∫ w

0F(w′)dw′.

Hint: Let u = (w′ − w) and v = F (w′). Use integration by partsformula,

∫udv = uv −

∫vdu.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

We use this to show that w can be characterized by:

w − c = β [E (w)− c]− β∫ w

0

(w′ − w

)dF(w′)

= β [E (w)− c] + β

∫ w

0F(w′)dw′.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Let g (w) =∫ w0 F (w′) dw′. Note:

g (0) = 0,g (w) ≥ 0,g′ (w) = F (w) > 0,g′′ (w) = F ′ (w) > 0, for w > 0.

Then we can write

w − c = β [E (w)− c] + β

∫ w

0F(w′)dw′

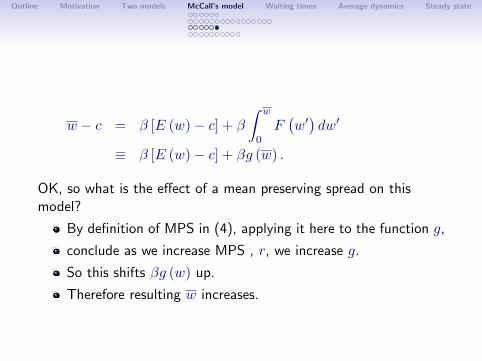

≡ β [E (w)− c] + βg (w) .

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

w − c = β [E (w)− c] + β

∫ w

0F(w′)dw′

≡ β [E (w)− c] + βg (w) .

OK, so what is the effect of a mean preserving spread on thismodel?

By definition of MPS in (4), applying it here to the function g,

conclude as we increase MPS , r, we increase g.

So this shifts βg (w) up.

Therefore resulting w increases.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

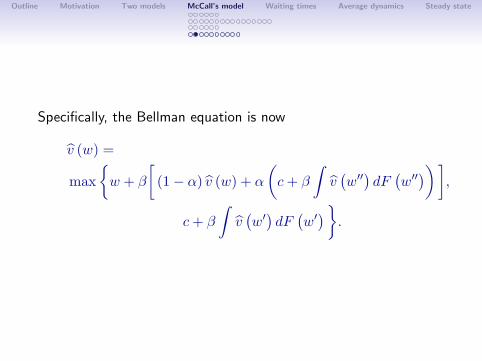

LayoffsConsider the same setup as before.

Now assume after the first period on the job, there is a probabilityα ∈ (0, 1) of being laid off.

For simplicity, assume α independent of tenure. When employed,the worker receives w per period until fired.

Conclude that value function with α > 0 is strictly dominated byvalue function when α = 0.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Specifically, the Bellman equation is now

v̂ (w) =

max{w + β

[(1− α) v̂ (w) + α

(c+ β

∫v̂(w′′)dF(w′′))]

,

c+ β

∫v̂(w′)dF(w′)}

.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Exercise

Show that v̂ (w) defines a unique value function satisfying theBellman equation and it is a nondecreasing function in w.

Hint: Show that the Bellman equation defines an operator T thatmaps a set of bounded and continuous functions into itself; thenshow that T is a contraction map with modulus β on a completemetric space. (What is the metric?) Then show that v is constantif the action is reject, and strictly increasing, since per-periodutility is strictly increasing, if the action is accept.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

So solution of the reservation wage form:

v̂ (w) =

{w+βα(c+β

R bv(w′′)dF (w′′))1−β(1−α) , if w ≥ w

c+ β∫v̂ (w′) dF (w′) , if w < w

where w solves

w + βα(c+ β

∫v̂ (w′′) dF (w′′)

)1− β (1− α)

= c+ β

∫v̂(w′)dF(w′).

Note: E[v̂(w′′)] = E[v̂(w′)]. Why?

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Rearranging,

w

1− β= c+ β

∫v̂(w′)dF(w′)

(*)

Contrast this with the reservation wage in the model previouslywhere there is no risk of layoffs, α = 0:

w

1− β= c+ β

∫ B

0v(w′)dF(w′)

(5)

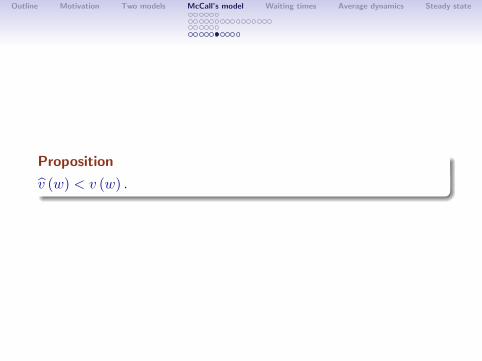

The difference now is that v̂ (w′) 6= v (w′). The two value functionare not the same! In particular, v̂ (w) < v (w) .

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Proposition

v̂ (w) < v (w) .

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Proof.

Consider the more general case where per-period utility isU : [0, B]→ R, and U ′ is everywhere positive.Then

v̂ (w) =

1

1−β(1−α) [U(w) + βαv̂(0)] , if w ≥ w

v̂(0), if w < w

where:

v̂(0) = U(c) + β

∫v̂(w′)dF(w′)

:=U(w)1− β

.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

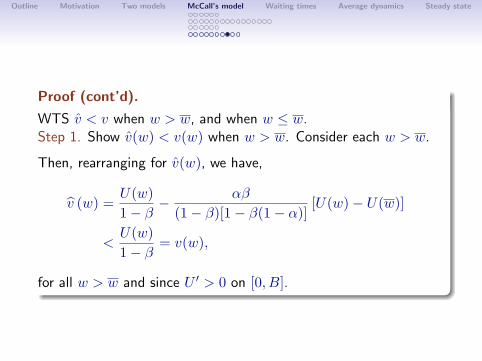

Proof (cont’d).

WTS v̂ < v when w > w, and when w ≤ w.Step 1. Show v̂(w) < v(w) when w > w. Consider each w > w.

Then, rearranging for v̂(w), we have,

v̂ (w) =U(w)1− β

− αβ

(1− β)[1− β(1− α)][U(w)− U(w)]

<U(w)1− β

= v(w),

for all w > w and since U ′ > 0 on [0, B].

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Proof (cont’d).

Step 2. Show w decreases with α and therefore v̂(0) < v(0). Hint:

1 Show that

v̂(0) =U(c) + β

R B

wU(w′)dF (w′)

(1− β)[1 + αβ + βF (w)]

and given that v̂(0) = (1− β)−1U(w), we have two equations for twounknowns v(0) and w.

2 Solving them for w, we have

U(w)[1 + αβ + β] = U(c) + β

Z B

w

[U(w′)− U(w)]dF (w′).

From this conclude that if α↘ 0, then w must increase to some higherlevel, for LHS = RHS. Therefore the reservation wage is lower whenα > 0 than when α = 0.

3 But by definition, v̂(0) = (1− β)−1U(w), so then v̂(0) < v(0).

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

(cont’d).

Step 3. From Steps 1-2, conclude:

1 w decreases with α, and

2 v̂ < v everywhere on the domain [0, B].

Intuition:

The higher the probability of losing your job each period, then theexpected utility (and hence value from accepting a job and henceworking) is lower. [Increasing part of graph(v) shifts down.]

Since v(0) also depends on continuation value that builds in value ofaccepting in later stages, v(0) is lower when α is higher. [Flat piece ofgraph(v) shifts down.]

We showed these two “opposing effects” are s.t. w is lower when α ishigher.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Waiting times

We can also infer the duration of unemployment in the model.Since we assumed independent sequential draws of wage offers thisis easy to calculate. Let N be time until a successful offer isdrawn. Then

Pr (N = 1) = 1−∫ w

0dF(w′)≡ 1− λ.

Pr (N = 2) = (1− λ)λ

and more generally

Pr (N = j) = (1− λ)λj−1

So waiting time is a random variable that is geometricallydistributed. The mean waiting time is then (1− λ)−1.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Average unemployment dynamics

1 Now suppose our economy has a continuum of ex anteidentical workers who face the McCall job-search problempreviously.

2 Each worker may be drawing different w’s so that ex postthey are heterogenous.

3 The agents move recurrently between unemployment andemployment.

4 With mean duration of each employment spell is α−1 andmean duration of unemployment is (1− λ)−1.

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

So the average unemployment rate is governed by the differenceequation

Ut+1 = α (1− Ut) + λUt

where

λ =∫ w0 dF (w′) = F (w) is probability of rejecting an offer.

α is “hazard rate of leaving employment”.

1− F (w) is “hazard rate of leaving unemployment”.

Notes:

Since λ < 1, the difference equation is stable and thus,Ut → U .

Average/aggregate dynamics for U is deterministic. Why?

Outline Motivation Two models McCall’s model Waiting times Average dynamics Steady state

Steady state

A stationary unemployment rate is one where Ut+1 = Ut = U .Solving for this we get

U =[1− F (w)]−1

[1− F (w)]−1 + α−1.

Long-run determinants of U :

Increase in w raises mean duration of unemployment[1− F (w)]−1 and thus steady-state U .

Increase in job separation rate α increases U.