Non-Executive Incentives & Bank Risk-Taking Viral Acharya (NYU Stern, NBER & CEPR) Lubomir P. Litov...

34

Non-Executive Incentives & Bank Risk-Taking Viral Acharya (NYU Stern, NBER & CEPR) Lubomir P. Litov (Univ. of Arizona & WFC, Univ. of Pennsylvania) Simone M. Sepe (Toulouse School of Economics & Univ. of Arizona) May 18 th 2013 American Law & Economics Association Meeting, Vanderbilt University

-

Upload

william-grant -

Category

Documents

-

view

215 -

download

0

Transcript of Non-Executive Incentives & Bank Risk-Taking Viral Acharya (NYU Stern, NBER & CEPR) Lubomir P. Litov...

Non-Executive Incentives &

Bank Risk-Taking

Viral Acharya (NYU Stern, NBER & CEPR)

Lubomir P. Litov (Univ. of Arizona & WFC, Univ. of Pennsylvania)

Simone M. Sepe (Toulouse School of Economics & Univ. of Arizona)

May 18th 2013

American Law & Economics Association Meeting, Vanderbilt University

2

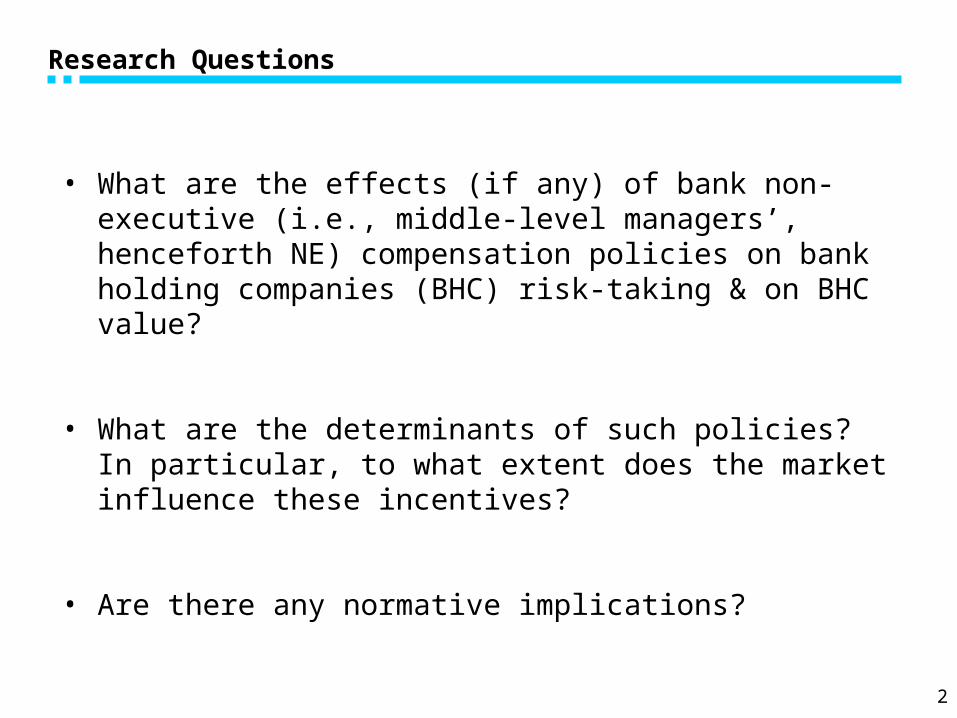

Research Questions

• What are the effects (if any) of bank non-executive (i.e., middle-level managers’, henceforth NE) compensation policies on bank holding companies (BHC) risk-taking & on BHC value?

• What are the determinants of such policies? In particular, to what extent does the market influence these incentives?

• Are there any normative implications?

3

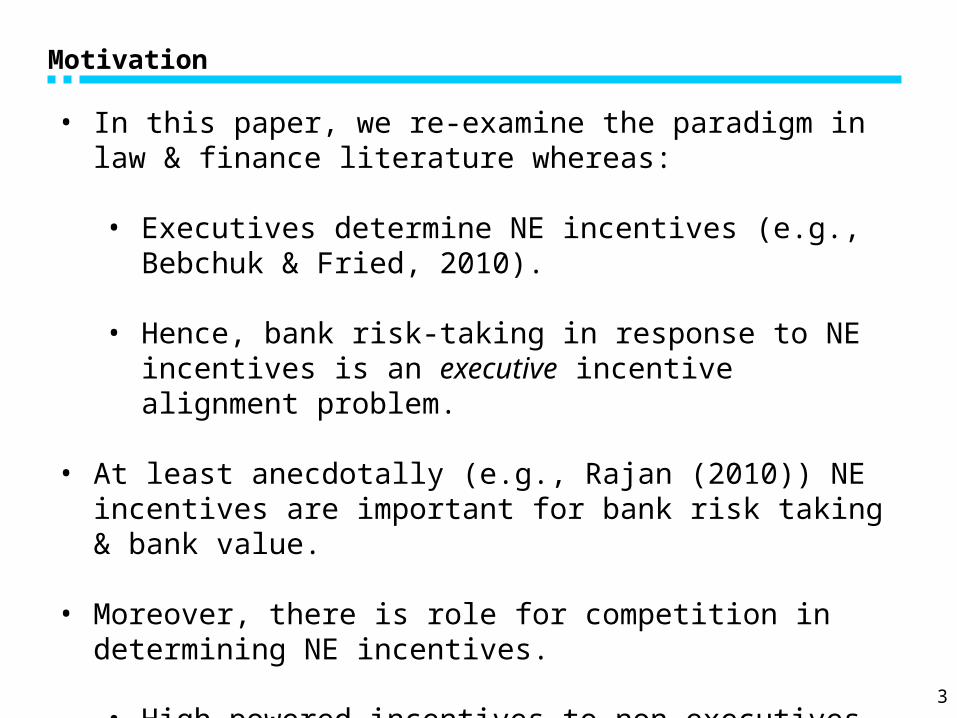

Motivation

• In this paper, we re-examine the paradigm in law & finance literature whereas:

• Executives determine NE incentives (e.g., Bebchuk & Fried, 2010).

• Hence, bank risk-taking in response to NE incentives is an executive incentive alignment problem.

• At least anecdotally (e.g., Rajan (2010)) NE incentives are important for bank risk taking & bank value.

• Moreover, there is role for competition in determining NE incentives.

• High-powered incentives to non-executives may lead to losing them to competitors.

4

Motivation

“As long as the music is playing, you’ve got to get up & dance.”

“We’re still dancing.”

(Charles Prince)

5

Two Empirical Hypotheses

• NE compensation policies in BHC before the crisis were only sensitive to increase revenue which resulted in excessive risk taking and, ultimately, lower bank value.

• The distorted risk incentives underlying BHCs’ NE compensation policies were the product of a negative externality engendered by bank competition for NE services.

6

Executive Compensation

• Mixed evidence of the impact of CEO incentives on bank risk choices:

• Bebchuk & Spamann (2010) and Cheng, Hong, & Sheinkman (2010).

• Fahlenbrach & Stulz (2011).

Non-Executive Compensation

Overall literature scope is limited due to lack of cross-sectional data.

• Experimental Data

• Cole,Kanz & Klapper (2012) and Agarwal & Ben-David (2012).

• Single Lender Data

• Berg, Puri, & Rocholl (2012); Hertzberg, Liberti, & Paravisini (2011); and Gee & Tzioumis (2012).

Bank Risk Taking

Factors to influence bank risk-taking include • Deposit Insurance & Competition → Keeley (1990) among many others.• Ownership & Bank Regulation → Laeven and Levine (2009).• Bank Size → Demsetz and Strahan (1997).• Bank Franchise Value → Demsetz, Saidenberg, & Strahan (1997).• Monetary Policy → Landier, Sraer and Thesmar (2011).• Creditor Rights → Houston et al. (2010).• Risk Management Governance Mechanisms → Ellul and Yerramilli (2012).

.

Prior Literature

7

During the financial crisis of 2007-2009:

1. Pre-crisis Cash & Bonus NE compensation incentives had a significant positive effect on bank risk taking.

2. Pre-crisis Stock NE compensation incentives had a significant negative effect on bank risk taking.

3. Pre-crisis NE compensation incentives affected bank risk-taking primarily trough the part of these incentives specific to peer-group performance.

4. Effects (1) and (3) above were stronger for banks w/ higher pre-crisis employee turnover & were weaker for banks w/ high pre-crisis excess NE compensation.

5. Pre-crisis NE total compensation incentives to above-peer group performance were more important in determining bank risk taking.

6. Pre-crisis NE Cash & Bonus compensation incentives lowered bank value, while NE Stock compensation incentives increased bank value.

Main Findings & Contributions

8

1. We contribute to the bank risk taking literature by testing for a new (to the literature) factor to influence bank risk taking & bank value.

2. As such, we document an inefficiency in bank NE compensation policies, caused by competition among banks to hire NE.

3. Methodologically, we outline a novel cross-sectional proxy for non-executive incentives.

4. Lastly, we contribute to the literature on employee stock-ownership, showing that ESOP plans add value through curbing employee risk taking incentives.

Main Findings & Contributions

9

Data

Collect Data from a Bank Regulatory Database.- Contains information on quarterly bank holding

company accounting data collected by the Federal Reserve Bank of Chicago.

Data available for 77 BHCs:- Only banks w/ available data.- Banks that survived the financial crisis.

Other data:

- CRSP & Compustat (control variables). - ExecuComp (CEO incentives).- Option Metrics (Implied volatility).

10

The Empirical Problem of Incentives

11

The Empirical Problem of Incentives

12

Non-Executive Compensation Elasticity

• Measures of Incentives (2002-2006):

• Elasticity of NE compensation: quarterly variation of total compensation (net of executive pay) w.r.t. quarterly variation of Total Interest Income (TII), or Net Interest Income (incl. Loan & Losses Provisions), Total Income, or Net Income.

• Maximal elasticity w.r.t. TII.

• I.e., banks may reward volume rather than quality of loan products.

𝐥𝐧 ( 𝑪𝒐𝒎𝒑𝒊𝒕

𝑪𝒐𝒎𝒑 𝒊𝒕−𝟏)=𝒂𝒊+𝒃𝒊𝟏 ,𝑻𝑰𝑰

𝑪𝒐𝒎𝒑× 𝒍𝒏( 𝑻𝑰𝑰 𝒊𝒕

𝑻𝑰𝑰 𝒊𝒕 −𝟏)+𝒃𝒊𝟐 ,𝑻𝑰𝑰

𝑪𝒐𝒎𝒑 ×𝒍𝒏( 𝑬𝑴𝑷 𝒊𝒕

𝑬𝑴𝑷 𝒊𝒕−𝟏)+𝒃𝒊𝟑 ,𝑻𝑰𝑰

𝑪𝒐𝒎𝒑× 𝒍𝒏( 𝑴𝑪𝑨𝑷 𝒊𝒕

𝑴𝑪𝑨𝑷 𝒊𝒕−𝟏)+𝜺 𝒊𝒕

13

Key Independent Variables0

510

15

20

Density

.9 .95 1 1.05 1.1Salary_TII_Elasticity

0.5

11.5

2Density

-2 -1 0 1 2 3Stock_TII_Elasticity

05

10

15

Density

.9 .95 1 1.05 1.1TotalComp_TII_Elasticity

14

Non-Executive Elasticity & Bank Risk-Taking

Measures of Risk (2007-2009): (1) Aggregate Risk; (2) Tail Risk; (3) Implied Volatility; (4) Z-Score.

Non-executive cash compensation incentives positively impact bank risk-taking.

In 2007-2009, the effect of NE cash compensation on risk is between 29.5% and 35.9%, instead effect of CEO compensation is, in some instances, 5.7%!

Non-executive stock compensation incentives negatively impact bank risk-taking, but stock incentives are only 2%!

15

Cash & Stock Compensation Effects (Table 7)

Dep. Variable: Tail Risk

Independent Variables: (1) (2) (3) (4)

0.063*** 0.074***

t-stat (2.83) (3.71)

-0.001** -0.001***

t-stat (2.0) (3.80)

0.062**

t-stat (2.16)

CEO Delta (mean 2003-2006) -0.001* -0.001* -0.001** -0.001*

t-stat (1.92) (1.64) (2.03) (1.75)

CEO Vega (mean 2003-2006) -0.011 -0.011 -0.009 -0.010

t-stat (1.13) (1.17) (1.05) (1.10)

(control variables not shown for brevity)

16

Cash & Stock Compensation Effects (Table 7) – Alternative Risk Measures

Dep. Variables: Aggregate Risk Implied Volatility Z-Score

Independent Variables: (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

0.149***

0.182***

1.148**

1.041**

-4.09***

-3.955*

**

t-stat(4.91

) (5.62

) (2.49

) (2.36

) (3.44

) (3.68)

-

0.003

-0.004

* 0.014 0.008

-0.035

** -0.012

t-stat (1.57

) (1.95

) (1.01

) (0.71

) (2.28

) (0.86)

0.119

*** 0.72***

-3.38**

*

t-stat (3.75

) (2.81

) (3.57

) CEO Delta (mean 2003-2006)

0.0001 0.001

0.0001

0.0001 -0.005 -0.016 -0.006 -0.007

0.054*

**

0.0666**

-0.008

0.0592***

t-stat (0.73) (1.20) (0.49) (0.89) (0.82) (1.21) (0.81) (0.80) (2.72) (2.05) (0.20) (3.75)

CEO Vega (mean 2003-2006)

-0.022

-0.023

-0.020

-0.022

0.062*

* 0.054* 0.074*

0.061*

*

-0.085*

**

-0.063*

**

-0.084

***

-0.0838

***

t-stat (1.2) (1.22) (1.12) (1.15) (1.99) (1.79) (1.91) (2.01) (4.76) (3.67) (4.39) (4.82)(control variables not shown for brevity)

17

Employee Turnover (Table 10A)

Panel A. Tail RiskControl Variables (1) (2) (3) (4)

0.06** 0.07***

t-stat (2.23) (3.03)

-0.001 -0.001t-stat (0.79) (1.51)

0.06** t-stat (2.29)

0.046*** 0.18***

t-stat (2.73) (3.36)

-0.008*** -0.011**

t-stat (2.62) (2.25)

.039*** t-stat (2.79)

Employee Turnover (2003-2006) -0.042 0.006* -0.03 -0.13t-stat (0.68) (1.72) (0.54) (1.15)

(control variables not shown for brevity)

18

Excess Cash Compensation (Table 10B)

Panel B. Tail RiskControl Variables (1) (2) (3) (4)

.053** .063***

t-stat (2.18) (2.55)

-.001** -.001***

t-stat (2.26) (4.1)

.051** t-stat (2.21)

-0.13* -0.254*

t-stat (1.93) (1.67)

0.004 -0.005t-stat (1.02) (0.62)

-0.067* t-stat (1.74)

Excess Cash Compensation (estimated 2003-2006) 0.001 -0.009*** -0.002 0.011

t-stat (0.11) (3.91) (0.42) (0.55)(control variables not shown for brevity)

19

Competition Effect

• To verify the relationship b/n competition for NE & their incentives, we consider:

- Sensitivity of NE compensation to BHC-specific performance & to peer-specific performance.

- Impact of turnover (as proxy for competition).

• NE compensation more sensitive to peer-specific performance.

• Turnover positively impacts bank risk-taking.

• Above-peer-group compensation (i.e., excess wage) negatively impacts bank risk-taking.

20

Peer Effects Estimation

where peer-specific performance defined as:

and, where bank-specific performance, i.e., , is defined as the residual of a regression of on

,

ln ( 𝑇𝐼𝐼 𝑡

𝑇𝐼𝐼𝑡 −1)= 1

𝑁 ∑𝑖=1

𝑁 𝑇𝐼𝐼𝑖𝑡

𝑇𝐼𝐼 𝑖𝑡− 1

21

Peer Group Choice

• Empirical challenge is to identify the peer group as it is possible that peer group performance is driven by a common latent factor.

• Potential solution: choose different reference group for different banks. Heterogeneity in peer group choice allows us to use performance of “peer’s peer” as valid instrument to capture peer group’s performance.

• Example. • Bank A1 has peer group, banks (A2, B1). • Bank B1 has a peer group, banks (B2, A1). • B2 performance relevant instrument for A1

performance because:1. Relevant to A1 performance (influences

performance of direct peer B1) &2. Exclusive to A1 performance (i.e., achieves

effect on A1 performance only through peer group).

22

Market Short-Term Performance Effect (Table 8)

Dep. Variables:Tail Risk

AggregateRisk

Implied Volatility

Z-Score

Independent Variables: (1) (2) (3) (4) (5) (6) (7) (8)

0.0853**

0.0858**

0.136**

*

0.132**

*

0.955**

* 0.899** -4.05*** -4.01***

t-stat (2.58) (2.5) (6.31) (5.2) (2.68) (2.25) (8.45) (7.91)

0.0003

-0.002**

*

-0.044**

* -0.054

t-stat (0.27) (3.19) (5.32) (1.41)

CEO Delta (mean 2003-2006) -0.001 -0.001 -0.001 -0.001 0.014 0.010 -0.07*** -0.07***

t-stat (1.31) (1.3) (0.22) (0.32) (1.41) (1.05) (3.1) (3.11)

CEO Vega (mean 2003-2006) 0.0001 0.0001 -0.008 -0.007 0.006 0.043 0.238*** 0.265***

t-stat (0.03) (0.06) (0.59) (0.55) (0.16) (1.03) (2.91) (3.0)

(control variables not shown for brevity)

23

Asymmetric Effects Estimation

We estimate

with denoting an indicator variable that is equal to one if

.

24

Market Asymmetric Performance Effect (Table 9)

Dep. Variables:Tail Risk

Aggregate Risk

ImpliedVolatility

Z-Score

Independent Variables: (1) (2) (3) (4)

-0.0009 0.006* 0.043 0.081*

t-stat (0.11) (1.61) (1.42) (1.11)

0.078*** 0.131*** 0.45*** -1.023***

t-stat (2.75) (2.63) (9.12) (3.19)

CEO Delta (mean 2003-2006) -0.0009* -0.0001 -0.010 -0.063***

t-stat (1.77) (0.55) (1.05) (4.86)

CEO Vega (mean 2003-2006) -0.007 -0.013 0.07** 0.168***

t-stat (0.91) (0.79) (1.98) (4.28)

(control variables not shown for brevity)

25

Bank Value (Table 11)

Dep. Variable: Tobin’s Q

Independent Variables: (1) (2) (3)

-0.2879***

t-stat (3.89)

0.001

t-stat (0.65)

-0.2973***

t-stat (3.78)

0.00066

t-stat (1.48)

CEO Delta (mean 2003-2006) -0.0113*** -0.0093** -0.0142***

t-stat (6.64) (2.43) (24.57)

CEO Vega (mean 2003-2006) 0.0166*** 0.017*** 0.0149**

t-stat (3.27) (3.36) (2.62)

(control variables not shown for brevity)

26

Robustness

• Potential concern w/ empirical design is that both pre-crisis incentives & within-crisis risk exposure may reflect the level of BHC specialization in particular product lines (e.g. subprime loans).

• If such product specialization is not controlled for in our tests, or if it influences dependent and independent variables in these tests in a non-linear way, a correlated-omitted variable bias in our empirical results would arise.

• To address endogeneity concern we use a comprehensive sample that extends from 1994 through 2010 and we use an alternative approach based on a system GMM estimation (Blundell and Bond (1998)).

27

GMM Analysis

Dep. Variable: Tail Risk

Control Variables (1) (2) (3) (4)

0.61*** 0.68***

t-stat (6.30) (3.20)

-.008*** -0.012*

t-stat (3.20) (1.80)

0.41***

t-stat (3.56)

CEO Delta (t-1) -.009*** -.007*** -0.01*** -.008***

t-stat (3.10) (2.80) (3.30) (3.0)

CEO Vega (t-1) .019*** .015*** .018*** .017***

t-stat (4.20) (3.70) (4.0) (3.90)

(control variables not shown for brevity)

28

GMM Analysis

Dep. Variable: Aggregate Risk

Control Variables (1) (2) (3) (4)

0.47** 0.56**

t-stat (1.98) (2.02)

-0.011 -.014*

(1.20) (1.81)

t-stat 0.34*

(1.79)

0.004 0.010 0.007 0.000

t-stat (0.45) (0.61) (0.53) (0.05)

CEO Delta (t-1) .007*** .007*** .006*** .006***

t-stat (3.80) (4.49) (3.60) (3.55)

CEO Vega (t-1) 0.47** 0.56**

t-stat (1.98) (2.02)(control variables not shown for brevity)

29

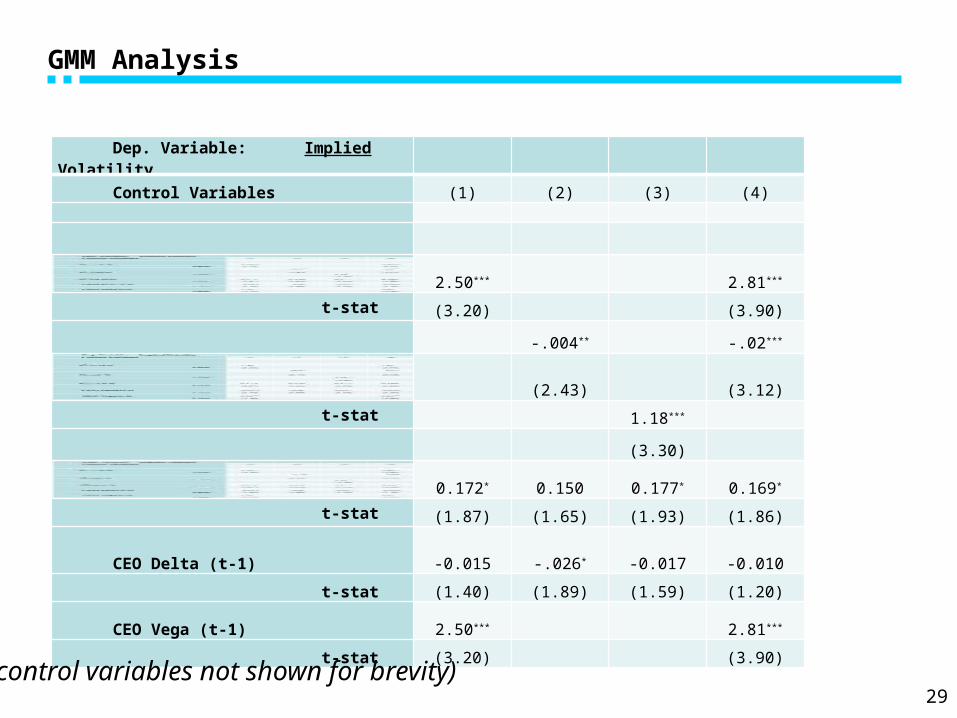

GMM Analysis

Dep. Variable: Implied Volatility

Control Variables (1) (2) (3) (4)

2.50*** 2.81***

t-stat (3.20) (3.90)

-.004** -.02***

(2.43) (3.12)

t-stat 1.18***

(3.30)

0.172* 0.150 0.177* 0.169*

t-stat (1.87) (1.65) (1.93) (1.86)

CEO Delta (t-1) -0.015 -.026* -0.017 -0.010

t-stat (1.40) (1.89) (1.59) (1.20)

CEO Vega (t-1) 2.50*** 2.81***

t-stat (3.20) (3.90)(control variables not shown for brevity)

30

GMM Analysis

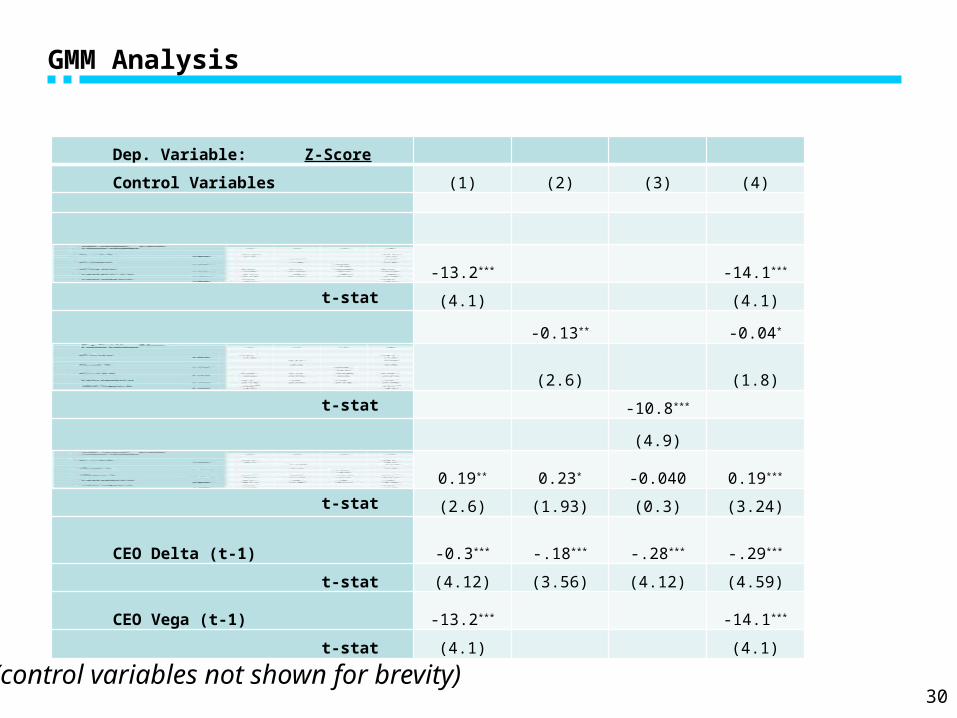

Dep. Variable: Z-Score

Control Variables (1) (2) (3) (4)

-13.2*** -14.1***

t-stat (4.1) (4.1)

-0.13** -0.04*

(2.6) (1.8)

t-stat -10.8***

(4.9)

0.19** 0.23* -0.040 0.19***

t-stat (2.6) (1.93) (0.3) (3.24)

CEO Delta (t-1) -0.3*** -.18*** -.28*** -.29***

t-stat (4.12) (3.56) (4.12) (4.59)

CEO Vega (t-1) -13.2*** -14.1***

t-stat (4.1) (4.1)

(control variables not shown for brevity)

31

Executive Compensation Reform?

• Improving executive compensation practices not enough to solve the problem of excessive bank risk-taking.

• NE risk incentives are independent from executive risk incentives.

• The root of the problem is the negative externality produced by bank competition for non-executives.

32

Limiting Competition for Non-Executives

• Direct: Making employment contracts relational.

• Non-compete provisions for NEs: property rule.

• Pigouvian tax on mobility: liability rule.

• Clawback provisions contingent on mobility.

• Excess compensation (contracts are less subject to renegotiation).

• Pigouvian subsidy: Regressive tax (or tax deduction) on compensation based on tenure.

33

Non-Executive Deferred Stock Compensation

• We find that stock compensation negatively impacts risk-taking, but is only 2% of total compensation.

• Back-loading stock compensation into future periods increases employer specificity.

• Rethink ownership between capital and labor providers when moral hazard is severe and cannot be fully controlled by contract.

• Implementation strategies:- Tough: Mandatory rules.- Soft: Tax deductions.

34

Thank You.