NOMINAL RIGIDITIES IN A DSGE M BASIC CALVO-YUN MODEL · tit t tttt t t tst ss ttsst pPP x py E y E...

26

1 NOMINAL RIGIDITIES IN A DSGE MODEL: BASIC CALVO-YUN MODEL OCTOBER 9, 2008 October 9, 2008 2 DIFFERENTIATED-GOODS FIRMS DSGE Calvo-Yun Model Optimal-pricing condition With sticky prices, optimal P i balances current and future marginal revenues against current and future marginal costs until the next (expected) price re-optimization Differentiated firm i’s (and hence the aggregate) markup will be time-varying As “initial marginal revenues” > “initial marginal costs” to balance against “later marginal revenues” < “later marginal costs” See King and Wolman (1999) Conduct full non-linear analysis (around distorted steady state) Later: typical New Keynesian analysis (around efficient steady state) | 1 0 s t i i t s t st s s s s s t t t P P E P y mc P P ε ε α ε − ∞ − + = ⎧ ⎫ ⎛ ⎞ ⎡ ⎤ − ⎪ ⎪ − = ⎨ ⎬ ⎜ ⎟ ⎢ ⎥ ⎝ ⎠ ⎣ ⎦ ⎪ Ξ ⎪ ⎩ ⎭ ∑ Real marginal revenue As inflation erodes the relative price of firm i

Transcript of NOMINAL RIGIDITIES IN A DSGE M BASIC CALVO-YUN MODEL · tit t tttt t t tst ss ttsst pPP x py E y E...

1

NOMINAL RIGIDITIES IN A DSGEMODEL: BASIC CALVO-YUN MODEL

OCTOBER 9, 2008

October 9, 2008 2

DIFFERENTIATED-GOODS FIRMS

DSGE Calvo-Yun Model

Optimal-pricing condition

With sticky prices, optimal Pi balances current and future marginal revenues against current and future marginal costs until the next (expected) price re-optimization

Differentiated firm i’s (and hence the aggregate) markup will be time-varying

As “initial marginal revenues” > “initial marginal costs” to balance against “later marginal revenues” < “later marginal costs”See King and Wolman (1999)

Conduct full non-linear analysis (around distorted steady state)Later: typical New Keynesian analysis (around efficient steady state)

|1 0s t i i

ts

t s t s s ss s

t t

t

P PE P y mcP P

ε

εα ε

−∞

−+

=

⎧ ⎫⎛ ⎞ ⎡ ⎤−⎪ ⎪− =⎨ ⎬⎜ ⎟ ⎢ ⎥⎝ ⎠ ⎣ ⎦⎪

Ξ⎪⎩ ⎭

∑

Real marginal revenue

As inflation erodes the relative price of firm i

2

October 9, 2008 3

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Optimal-pricing condition

Define

Optimal-pricing condition:Emphasizes that optimal Pi balances current and future mr against current and future mc

Write recursively (following SGU (2005 NBER Macro Annual))

|1 0s t it it

t t s t s s ss t s s

P PE P y mcP P

εεαε

−∞

−+

=

⎧ ⎫⎛ ⎞ ⎡ ⎤−⎪ ⎪Ξ − =⎨ ⎬⎜ ⎟ ⎢ ⎥⎝ ⎠ ⎣ ⎦⎪ ⎪⎩ ⎭

∑

1|

1s t it itt t t t s t s s

s t s s

P PPx E P yP P

εεαε

−∞

−+

=

⎧ ⎫⎛ ⎞ −⎪ ⎪= Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

∑

1 2t tx x=

2|

s t itt t t t s t s s s

s t s

PPx E P y mcP

ε

α−

∞−

+=

⎧ ⎫⎛ ⎞⎪ ⎪= Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

∑

PDV of nominal marginal revenues until next price change

PDV of nominal marginal costs until next price change

1 2,t tx x

October 9, 2008 4

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Some notation and definitions

itit

t

PpP

≡

itP

1it itP P+ =

Relative price of good i in period t

Evolution of nominal price if no price change

Nominal price of good i in period t

3

October 9, 2008 5

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Some notation and definitions

1

1

1

1

1

1

it iit

it

t

t t

it t

t

t

t

P PP PPP

p

P

pP

π

+

+ +

+

+

+

=

= =

=

Relative price of good i in period t

Evolution of nominal price if no price change

As long as no nominal price change, a firm’s relative price erodes at the rate of inflation

(πt+1 = Pt+1/Pt)

Nominal price of good i in period t

itit

t

PpP

≡

itP

1it itP P+ =

October 9, 2008 6

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively

1|

1s t it itt t t t s t s s

s t s s

P PPx E P yP P

εεαε

−∞

−+

=

⎧ ⎫⎛ ⎞ −⎪ ⎪= Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

∑

1tx

1 11 1

1| 1 |21

1 1 s tt it t it s itt t t t t t t t s t s s

s tt t t t t s

P P P P P Px y E y E y mcP P P P P P

ε ε εε εα αε ε

− − −∞

−++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

Divide by Pt; write out first two terms

4

October 9, 2008 7

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively

1|

1s t it itt t t t s t s s

s t s s

P PPx E P yP P

εεαε

−∞

−+

=

⎧ ⎫⎛ ⎞ −⎪ ⎪= Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

∑

1tx

1 11 1

1| 1 |21

1 1 s tt it t it s itt t t t t t t t s t s s

s tt t t t t s

P P P P P Px y E y E y mcP P P P P P

ε ε εε εα αε ε

− − −∞

−++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

Divide by Pt; write out first two terms

Pit+1 = Pit while no price change opportunity

1 11 1 1

1| 1 |21

1 1 s tit t it s itt t t t t t t t s t s s

s tt t t t s

P P P P Px y E y E y mcP P P P P

ε ε εε εα αε ε

− − −∞

−+ ++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

October 9, 2008 8

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively

1|

1s t it itt t t t s t s s

s t s s

P PPx E P yP P

εεαε

−∞

−+

=

⎧ ⎫⎛ ⎞ −⎪ ⎪= Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

∑

1tx

1 11 1

1| 1 |21

1 1 s tt it t it s itt t t t t t t t s t s s

s tt t t t t s

P P P P P Px y E y E y mcP P P P P P

ε ε εε εα αε ε

− − −∞

−++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

Divide by Pt; write out first two terms

Pit+1 = Pit while no price change opportunity

1 11 1 1

1| 1 |21

1 1 s tit t it s itt t t t t t t t s t s s

s tt t t t s

P P P P Px y E y E y mcP P P P P

ε ε εε εα αε ε

− − −∞

−+ ++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑Use definitions

11 11| 1 1 1 |

2

1 1 s t s itt it t t t t t it t t t s t s s

s t t s

P Px p y E p y E y mcP P

εε εε εα π α

ε ε

−∞

− − −+ + + + +

= +

⎧ ⎫⎛ ⎞− − ⎪ ⎪⎧ ⎫= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟⎩ ⎭ ⎝ ⎠⎪ ⎪⎩ ⎭

∑

5

October 9, 2008 9

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively

1|

1s t it itt t t t s t s s

s t s s

P PPx E P yP P

εεαε

−∞

−+

=

⎧ ⎫⎛ ⎞ −⎪ ⎪= Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

∑

1tx

1 11 1

1| 1 |21

1 1 s tt it t it s itt t t t t t t t s t s s

s tt t t t t s

P P P P P Px y E y E y mcP P P P P P

ε ε εε εα αε ε

− − −∞

−++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

Divide by Pt; write out first two terms

Pit+1 = Pit while no price change opportunity

1 11 1 1

1| 1 |21

1 1 s tit t it s itt t t t t t t t s t s s

s tt t t t s

P P P P Px y E y E y mcP P P P P

ε ε εε εα αε ε

− − −∞

−+ ++ + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑Use definitions

11 11| 1 1 1 |

2

1 1 s t s itt it t t t t t it t t t s t s s

s t t s

P Px p y E p y E y mcP P

εε εε εα π α

ε ε

−∞

− − −+ + + + +

= +

⎧ ⎫⎛ ⎞− − ⎪ ⎪⎧ ⎫= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟⎩ ⎭ ⎝ ⎠⎪ ⎪⎩ ⎭

∑1 1/it it tp p π+ +=Use

October 9, 2008 10

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively 1tx

111

1| 1 1 |21

1 1 s tit s itt it t t t t t t t t s t s s

s tt t s

p P Px p y E y E y mcP P

ε εε ε εα π α

ε π ε

− −∞

− −+ + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

6

October 9, 2008 11

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively 1tx

Rearrange

111

1| 1 1 |21

1 1 s tit s itt it t t t t t t t t s t s s

s tt t s

p P Px p y E y E y mcP P

ε εε ε εα π α

ε π ε

− −∞

− −+ + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

1 111| 1 1 |

2

1 1 s t s itt it t t t t t it t t t s t s s

s t t s

P Px p y E p y E y mcP P

εε εεε εα π α

ε ε

−∞

− − −+ + + +

= +

⎧ ⎫⎛ ⎞− − ⎪ ⎪⎧ ⎫= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟⎩ ⎭ ⎝ ⎠⎪ ⎪⎩ ⎭

∑

October 9, 2008 12

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively 1tx

Rearrange

111

1| 1 1 |21

1 1 s tit s itt it t t t t t t t t s t s s

s tt t s

p P Px p y E y E y mcP P

ε εε ε εα π α

ε π ε

− −∞

− −+ + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

1 111| 1 1 |

2

1 1 s t s itt it t t t t t it t t t s t s s

s t t s

P Px p y E p y E y mcP P

εε εεε εα π α

ε ε

−∞

− − −+ + + +

= +

⎧ ⎫⎛ ⎞− − ⎪ ⎪⎧ ⎫= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟⎩ ⎭ ⎝ ⎠⎪ ⎪⎩ ⎭

∑1

1itp ε−+Multiply and divide by

111 1

1| 1 1 1 |21

1 1 s tit s itt it t t t t t it t t t s t s s

s tit t s

p P Px p y E p y E y mcp P P

ε εε ε εε εα π α

ε ε

− −∞

− − −+ + + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

7

October 9, 2008 13

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively 1tx

Rearrange

111

1| 1 1 |21

1 1 s tit s itt it t t t t t t t t s t s s

s tt t s

p P Px p y E y E y mcP P

ε εε ε εα π α

ε π ε

− −∞

− −+ + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

1 111| 1 1 |

2

1 1 s t s itt it t t t t t it t t t s t s s

s t t s

P Px p y E p y E y mcP P

εε εεε εα π α

ε ε

−∞

− − −+ + + +

= +

⎧ ⎫⎛ ⎞− − ⎪ ⎪⎧ ⎫= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟⎩ ⎭ ⎝ ⎠⎪ ⎪⎩ ⎭

∑1

1itp ε−+Multiply and divide by

111 1

1| 1 1 1 |21

1 1 s tit s itt it t t t t t it t t t s t s s

s tit t s

p P Px p y E p y E y mcp P P

ε εε ε εε εα π α

ε ε

− −∞

− − −+ + + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

Have generated a recursive term

October 9, 2008 14

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Write recursively 1tx

Rearrange

111

1| 1 1 |21

1 1 s tit s itt it t t t t t t t t s t s s

s tt t s

p P Px p y E y E y mcP P

ε εε ε εα π α

ε π ε

− −∞

− −+ + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

1 111| 1 1 |

2

1 1 s t s itt it t t t t t it t t t s t s s

s t t s

P Px p y E p y E y mcP P

εε εεε εα π α

ε ε

−∞

− − −+ + + +

= +

⎧ ⎫⎛ ⎞− − ⎪ ⎪⎧ ⎫= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟⎩ ⎭ ⎝ ⎠⎪ ⎪⎩ ⎭

∑1

1itp ε−+Multiply and divide by

111 1

1| 1 1 1 |21

1 1 s tit s itt it t t t t t it t t t s t s s

s tit t s

p P Px p y E p y E y mcp P P

ε εε ε εε εα π α

ε ε

− −∞

− − −+ + + + +

= ++

⎧ ⎫ ⎧ ⎫⎛ ⎞ ⎛ ⎞− −⎪ ⎪ ⎪ ⎪= + Ξ + Ξ⎨ ⎬ ⎨ ⎬⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠⎪ ⎪ ⎪ ⎪⎩ ⎭ ⎩ ⎭

∑

Express recursively

111 1

1| 1 11

1 itt it t t t t t t

it

px p y E xp

εε εε α π

ε

−−

+ + ++

⎧ ⎫⎛ ⎞− ⎪ ⎪= + Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

x1 expressed recursively

Have generated a recursive term

8

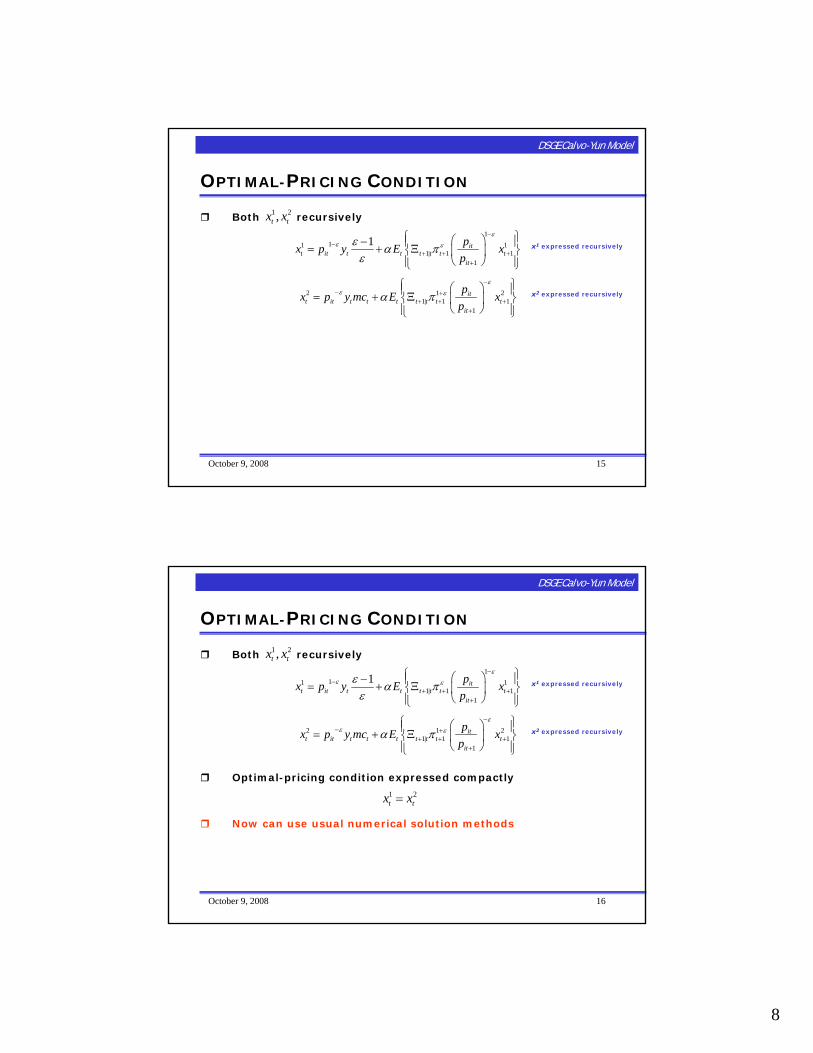

October 9, 2008 15

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Both recursively 1 2,t tx x1

11 11| 1 1

1

1 itt it t t t t t t

it

px p y E xp

εε εε α π

ε

−−

+ + ++

⎧ ⎫⎛ ⎞− ⎪ ⎪= + Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

x1 expressed recursively

2 1 21| 1 1

1

itt it t t t t t t t

it

px p y mc E xp

εε εα π

−− +

+ + ++

⎧ ⎫⎛ ⎞⎪ ⎪= + Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

x2 expressed recursively

October 9, 2008 16

OPTIMAL-PRICING CONDITION

DSGE Calvo-Yun Model

Both recursively

Optimal-pricing condition expressed compactly

Now can use usual numerical solution methods

1 2,t tx x1

11 11| 1 1

1

1 itt it t t t t t t

it

px p y E xp

εε εε α π

ε

−−

+ + ++

⎧ ⎫⎛ ⎞− ⎪ ⎪= + Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

x1 expressed recursively

2 1 21| 1 1

1

itt it t t t t t t t

it

px p y mc E xp

εε εα π

−− +

+ + ++

⎧ ⎫⎛ ⎞⎪ ⎪= + Ξ⎨ ⎬⎜ ⎟⎝ ⎠⎪ ⎪⎩ ⎭

x2 expressed recursively

1 2t tx x=

9

October 9, 2008 17

AGGREGATE PRICE LEVEL

DSGE Calvo-Yun Model

Aggregate price index follows from Dixit-Stiglitz aggregation

1 11 1 1 *1

10 0

t it it itP P di P di P diα

ε ε ε ε

α

− − − −−= = +∫ ∫ ∫

adjustersnon-adjusters

Obtained by substituting demand functions into D-S aggregator

October 9, 2008 18

AGGREGATE PRICE LEVEL

DSGE Calvo-Yun Model

Aggregate price index follows from Dixit-Stiglitz aggregation

1 11 1 1 *1

10 0

t it it itP P di P di P diα

ε ε ε ε

α

− − − −−= = +∫ ∫ ∫

adjustersnon-adjustersEmphasize optimal new price

Obtained by substituting demand functions into D-S aggregator

10

October 9, 2008 19

AGGREGATE PRICE LEVEL

DSGE Calvo-Yun Model

Aggregate price index follows from Dixit-Stiglitz aggregation

1 11 1 1 *1

10 0

t it it itP P di P di P diα

ε ε ε ε

α

− − − −−= = +∫ ∫ ∫

adjustersnon-adjustersEmphasize optimal new price

1 *11 (1 )t tP Pε εα α− −−= + −

KEY: Because adjusters were randomly selected, average (aggregate) price of non-adjusters is same as previous period’s average (aggregate) price

Fraction 1 - α re-set price optimally (and symmetrically)

Obtained by substituting demand functions into D-S aggregator

October 9, 2008 20

AGGREGATE PRICE LEVEL

DSGE Calvo-Yun Model

Aggregate price index follows from Dixit-Stiglitz aggregation

1 11 1 1 *1

10 0

t it it itP P di P di P diα

ε ε ε ε

α

− − − −−= = +∫ ∫ ∫

adjustersnon-adjustersEmphasize optimal new price

1 *11 (1 )t tP Pε εα α− −−= + −

KEY: Because adjusters were randomly selected, average (aggregate) price of non-adjusters is same as previous period’s average (aggregate) price

Obtained by substituting demand functions into D-S aggregatorTRACTABILITY DUE TO THE

CALVO RANDOM-ADJUSTMENT ASSUMPTION

Fraction 1 - α re-set price optimally (and symmetrically)

11

October 9, 2008 21

AGGREGATE PRICE LEVEL

DSGE Calvo-Yun Model

Aggregate price index follows from Dixit-Stiglitz aggregation

1 11 1 1 *1

10 0

t it it itP P di P di P diα

ε ε ε ε

α

− − − −−= = +∫ ∫ ∫

adjustersnon-adjustersEmphasize optimal new price

1 *11 (1 )t tP Pε εα α− −−= + −

1 *11 (1 )t tpε εαπ α− −= + − EQUILIBRIUM EVOLUTION OF AGGREGATE INFLATION –depends on relative price set by firms currently adjusting nominal price

Obtained by substituting demand functions into D-S aggregator

KEY: Because adjusters were randomly selected, average (aggregate) price of non-adjusters is same as previous period’s average (aggregate) price

TRACTABILITY DUE TO THE CALVO RANDOM-ADJUSTMENT ASSUMPTION

Fraction 1 - α re-set price optimally (and symmetrically)

October 9, 2008 22

AGGREGATE PRICE LEVEL

DSGE Calvo-Yun Model

Aggregate price index follows from Dixit-Stiglitz aggregation

1 11 1 1 *1

10 0

t it it itP P di P di P diα

ε ε ε ε

α

− − − −−= = +∫ ∫ ∫

adjustersnon-adjustersEmphasize optimal new price

1 *11 (1 )t tP Pε εα α− −−= + −

1 *11 (1 )t tpε εαπ α− −= + − EQUILIBRIUM EVOLUTION OF AGGREGATE INFLATION –depends on relative price set by firms currently adjusting nominal price

Obtained by substituting demand functions into D-S aggregator

Optimal-pricing condition1 2t tx x=

Together form the “aggregate supply” block of New Keynesian sticky-price model

KEY: Because adjusters were randomly selected, average (aggregate) price of non-adjusters is same as previous period’s average (aggregate) price

TRACTABILITY DUE TO THE CALVO RANDOM-ADJUSTMENT ASSUMPTION

Fraction 1 - α re-set price optimally (and symmetrically)

12

October 9, 2008 23

PRICE DISPERSION

DSGE Calvo-Yun Model

Calvo model implies dispersion of relative pricesAs does Taylor model (see Chari, Kehoe, McGrattan (2000 Econometrica for an example))……but not Rotemberg model (quadratic cost of nominal price adjustment)

October 9, 2008 24

PRICE DISPERSION

DSGE Calvo-Yun Model

Calvo model implies dispersion of relative pricesAs does Taylor model (see Chari, Kehoe, McGrattan (2000 Econometrica for an example))……but not Rotemberg model (quadratic cost of nominal price adjustment)

Dispersion often ignored until recently...…due to linearization around a zero-inflation steady state (typical simple New Keynesian model soon…)With better numerical tools, easier to take account of dispersion

13

October 9, 2008 25

PRICE DISPERSION

DSGE Calvo-Yun Model

Calvo model implies dispersion of relative pricesAs does Taylor model (see Chari, Kehoe, McGrattan (2000 Econometrica for an example))……but not Rotemberg model (quadratic cost of nominal price adjustment)

Dispersion often ignored until recently...…due to linearization around a zero-inflation steady state (typical simple New Keynesian model soon…)With better numerical tools, easier to take account of dispersion

Price dispersion the basic source of welfare losses of non-zero inflation

Because it implies quantity dispersion across intermediate producers……which is inefficient because Dixit-Stiglitz aggregator is symmetric and concave in every good i

October 9, 2008 26

PRICE DISPERSION

DSGE Calvo-Yun Model

Calvo model implies dispersion of relative pricesAs does Taylor model (see Chari, Kehoe, McGrattan (2000 Econometrica for an example))……but not Rotemberg model (quadratic cost of nominal price adjustment)

Dispersion often ignored until recently...…due to linearization around a zero-inflation steady state (typical simple New Keynesian model soon…)With better numerical tools, easier to take account of dispersion

Price dispersion the basic source of welfare losses of non-zero inflation

Because it implies quantity dispersion across intermediate producers……which is inefficient because Dixit-Stiglitz aggregator is symmetric and concave in every good i

The basic driving force of optimal policy in any NK model

14

October 9, 2008 27

PRICE DISPERSION

DSGE Calvo-Yun Model

For firm i, ( , )itit t t it it

t

Py y z f k nP

ε−⎛ ⎞

= =⎜ ⎟⎝ ⎠

October 9, 2008 28

PRICE DISPERSION

DSGE Calvo-Yun Model

For firm i,

Integrating over i

( , )itit t t it it

t

Py y z f k nP

ε−⎛ ⎞

= =⎜ ⎟⎝ ⎠

1 1

0 0

( , )itt t it it

t

Py di z f k n diP

ε−⎛ ⎞

=⎜ ⎟⎝ ⎠∫ ∫

15

October 9, 2008 29

PRICE DISPERSION

DSGE Calvo-Yun Model

For firm i,

Integrating over i

( , )itit t t it it

t

Py y z f k nP

ε−⎛ ⎞

= =⎜ ⎟⎝ ⎠

1 1

0 0

( , )itt t it it

t

Py di z f k n diP

ε−⎛ ⎞

=⎜ ⎟⎝ ⎠∫ ∫

Symmetric choices of k/n ratio across all firms i…

1 1

0 0

,1it tt t it

t t

P ky di z f n diP n

ε−⎛ ⎞ ⎛ ⎞

=⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠∫ ∫

October 9, 2008 30

PRICE DISPERSION

DSGE Calvo-Yun Model

For firm i,

Integrating over i

( , )itit t t it it

t

Py y z f k nP

ε−⎛ ⎞

= =⎜ ⎟⎝ ⎠

1 1

0 0

( , )itt t it it

t

Py di z f k n diP

ε−⎛ ⎞

=⎜ ⎟⎝ ⎠∫ ∫

ts≡

1 1

0 0

,1it tt t it

t t

P ky di z f n diP n

ε−⎛ ⎞ ⎛ ⎞

=⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠∫ ∫

A measure of dispersion: relative price dispersion leads to dispersion of factor usage across differentiated firms, hence dispersion of quantity across differentiated firms

Express st recursively

Symmetric choices of k/n ratio across all firms i…

16

October 9, 2008 31

PRICE DISPERSION

DSGE Calvo-Yun Model

1 1 *

0 0

it it itt

t t t

P P Ps di di diP P P

ε ε εα

α

− − −⎛ ⎞ ⎛ ⎞ ⎛ ⎞

= = +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫ ∫ ∫

Re-setters all choose same price

*

0

(1 ) t it

t t

P P diP P

ε εα

α− −

⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

October 9, 2008 32

PRICE DISPERSION

DSGE Calvo-Yun Model

1 1 *

0 0

it it itt

t t t

P P Ps di di diP P P

ε ε εα

α

− − −⎛ ⎞ ⎛ ⎞ ⎛ ⎞

= = +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫ ∫ ∫

Re-setters all choose same price

*

0

(1 ) t it

t t

P P diP P

ε εα

α− −

⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

Pit = Pit-1 for firms that cannot re-set price

*1

0

(1 ) t it

t t

P P diP P

ε εα

α− −

−⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

17

October 9, 2008 33

PRICE DISPERSION

DSGE Calvo-Yun Model

1 1 *

0 0

it it itt

t t t

P P Ps di di diP P P

ε ε εα

α

− − −⎛ ⎞ ⎛ ⎞ ⎛ ⎞

= = +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫ ∫ ∫

Re-setters all choose same price

*

0

(1 ) t it

t t

P P diP P

ε εα

α− −

⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

*1

0

(1 ) t it

t t

P P diP P

ε εα

α− −

−⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

Multiply by (Pt-1/Pt-1)-ε

*1 1

10

(1 ) t t it

t t t

P P P diP P P

ε ε εα

α− − −

− −

−

⎛ ⎞ ⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫

Pit = Pit-1 for firms that cannot re-set price

October 9, 2008 34

PRICE DISPERSION

DSGE Calvo-Yun Model

1 1 *

0 0

it it itt

t t t

P P Ps di di diP P P

ε ε εα

α

− − −⎛ ⎞ ⎛ ⎞ ⎛ ⎞

= = +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫ ∫ ∫

Re-setters all choose same price

*

0

(1 ) t it

t t

P P diP P

ε εα

α− −

⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

*1

0

(1 ) t it

t t

P P diP P

ε εα

α− −

−⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

Multiply by (Pt-1/Pt-1)-ε

*1 1

10

(1 ) t t it

t t t

P P P diP P P

ε ε εα

α− − −

− −

−

⎛ ⎞ ⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫

1tsα −≡tεπ≡

Pit = Pit-1 for firms that cannot re-set price

18

October 9, 2008 35

PRICE DISPERSION

DSGE Calvo-Yun Model

1 1 *

0 0

it it itt

t t t

P P Ps di di diP P P

ε ε εα

α

− − −⎛ ⎞ ⎛ ⎞ ⎛ ⎞

= = +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫ ∫ ∫

Re-setters all choose same price

*

0

(1 ) t it

t t

P P diP P

ε εα

α− −

⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

*1

0

(1 ) t it

t t

P P diP P

ε εα

α− −

−⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

Multiply by (Pt-1/Pt-1)-ε

*1 1

10

(1 ) t t it

t t t

P P P diP P P

ε ε εα

α− − −

− −

−

⎛ ⎞ ⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫

1tsα −≡tεπ≡

Pit = Pit-1 for firms that cannot re-set price

1

0 0

1it itt

t t

P Ps di diP P

ε εα

α

− −⎛ ⎞ ⎛ ⎞

= =⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠∫ ∫

Because of Calvorandom adjustment and all adjusters choose same price

October 9, 2008 36

PRICE DISPERSION

DSGE Calvo-Yun Model

1 1 *

0 0

it it itt

t t t

P P Ps di di diP P P

ε ε εα

α

− − −⎛ ⎞ ⎛ ⎞ ⎛ ⎞

= = +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫ ∫ ∫

Re-setters all choose same price

*

0

(1 ) t it

t t

P P diP P

ε εα

α− −

⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

*1

0

(1 ) t it

t t

P P diP P

ε εα

α− −

−⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠∫

Multiply by (Pt-1/Pt-1)-ε

*1 1

10

(1 ) t t it

t t t

P P P diP P P

ε ε εα

α− − −

− −

−

⎛ ⎞ ⎛ ⎞ ⎛ ⎞= − +⎜ ⎟ ⎜ ⎟ ⎜ ⎟

⎝ ⎠ ⎝ ⎠ ⎝ ⎠∫

tεπ≡

NOTE:

α= 0: st = 1 (no dispersion)

α > 0: st > 1 (dispersion)

Pit = Pit-1 for firms that cannot re-set price

Because of Calvorandom adjustment and all adjusters choose same price

1tsα −≡

1

0 0

1it itt

t t

P Ps di diP P

ε εα

α

− −⎛ ⎞ ⎛ ⎞

= =⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠∫ ∫

19

October 9, 2008 37

RESOURCE CONSTRAINT

DSGE Calvo-Yun Model

Summarized by three conditions

( , )t t tt

t

z f k nys

=

1 (1 )t t t t ty c k k gδ+= + − − +

*1(1 )t t t ts p sε εα απ−−= − +

“Usual” resource constraint

Some output is a pure deadweight loss

(note st < 1 cannot occur)

Law of motion for deadweight loss

1 1

0 0

,t it t itk k di n n di= =∫ ∫

And using factor market clearing conditions here

October 9, 2008 38

RESOURCE CONSTRAINT

Yun 1996 Model

Summarized by three conditions

Law of motion for st represented using laws of motion for both Pt-1and P*t-1

See equations (25) and (26)

( , )t t tt

t

z f k nys

=

1 (1 )t t t t ty c k k gδ+= + − − +

*1(1 )t t t ts p sε εα απ−−= − +

“Usual” resource constraint

Some output is a pure deadweight loss

(note st < 1 cannot occur)

Law of motion for deadweight loss

= 0 in Yun model

20

October 9, 2008 39

OTHER MODEL DETAILS

Yun 1996 Model

Cash/credit to motivate money demandi.e., Lucas and Stokey (1983), Chari, Christiano, and Kehoe (1991)

(Habit persistence (i.e., time-non-separability) in leisure)As in Kydland and Prescott (1982); unimportant for main results…

Could have been cashless…

October 9, 2008 40

OTHER MODEL DETAILS

Yun 1996 Model

Cash/credit to motivate money demandi.e., Lucas and Stokey (1983), Chari, Christiano, and Kehoe (1991)

(Habit persistence (i.e., time-non-separability) in leisure)As in Kydland and Prescott (1982); unimportant for main results…

Exogenous AR(1) money growth processAlso “endogenous” money supply process, but not as interesting

Exogenous AR(1) TFP process

Could have been cashless…

21

October 9, 2008 41

OTHER MODEL DETAILS

Yun 1996 Model

Cash/credit to motivate money demandi.e., Lucas and Stokey (1983), Chari, Christiano, and Kehoe (1991)

(Habit persistence (i.e., time-non-separability) in leisure)As in Kydland and Prescott (1982); unimportant for main results…

Exogenous AR(1) money growth processAlso “endogenous” money supply process, but not as interesting

Exogenous AR(1) TFP process

Indexation of prices to average (i.e., steady-state) inflationFor firms not re-setting price, (will see again in Christiano, Eichenbaum, and Evans (2005 JPE))

Approximated and simulated using “usual” methodsUsing King, Plosser, Rebelo (1988) linear approximation method

(One…) predecessor to SGU algorithm

1it itP Pπ −=

Could have been cashless…

October 9, 2008 42

NOMINAL EFFECTS OF STICKY PRICES

Yun 1996 Model

Effects on inflation not very different compared to flex-price case

Flexible Prices

Sticky Prices

22

October 9, 2008 43

NOMINAL EFFECTS OF STICKY PRICES

Yun 1996 Model

Effects on inflation not very different compared to flex-price case

Flexible Prices

Sticky Prices

Lack of inflation persistence in basic Calvo-Yun model (now) well-known –see Steinsson (2001 JME)

October 9, 2008 44

REAL EFFECTS OF STICKY PRICES

Yun 1996 Model

Effects on GDP much bigger the stickier are prices

Flexible Prices

Sticky Prices

23

October 9, 2008 45

MARKUP DYNAMICS

Sticky-Price Mechanism

Money (i.e., nontechnology) shock output expands

With zt, kt fixed, output expansion due to increased (equilibrium) hours

October 9, 2008 46

MARKUP DYNAMICS

Sticky-Price Mechanism

Money (i.e., nontechnology) shock output expands

With zt, kt fixed, output expansion due to increased (equilibrium) hours

Downward-sloping product demand curves individual (differentiated) firms must expand their output (partial equilibrium)

Recall aggregate output a shifter of firm i demand function

Can only be achieved in the short-run if a given firm i hires more labor at any real wage

24

October 9, 2008 47

MARKUP DYNAMICS

Sticky-Price Mechanism

Money (i.e., nontechnology) shock output expands

With zt, kt fixed, output expansion due to increased (equilibrium) hours

Downward-sloping product demand curves individual (differentiated) firms must expand their output (partial equilibrium)

Recall aggregate output a shifter of firm i demand function

Can only be achieved in the short-run if a given firm i hires more labor at any real wage

S

Labor

Real wage D

1( , )

t

t n t t t

wz f k n μ

= Sticky-price (or sticky-wage) model delivers endogenously-countercyclical markup

tmc=

October 9, 2008 48

DSGE STICKY-PRICE MODELS

Summary and Roadmap

Nominal rigidities embedded in DSGE modelMonetary shifts quantitatively “big” effects on output(Re-)articulates “old” Keynesian ideasGoodfriend and King (1997 NBER Macroeconomics Annual): the New-Neoclassical Synthesis

25

October 9, 2008 49

DSGE STICKY-PRICE MODELS

Summary and Roadmap

Nominal rigidities embedded in DSGE modelMonetary shifts quantitatively “big” effects on output(Re-)articulates “old” Keynesian ideasGoodfriend and King (1997 NBER Macroeconomics Annual): the New-Neoclassical Synthesis

Output effect not very long-lasting (peak response occurs in period of monetary shock, inconsistent with data)

The “Persistence Puzzle”Examined in Chari, Kehoe, and McGrattan (2000 Econometrica) (next) and Christiano, Eichenbaum, and Evans (2005 JPE)

October 9, 2008 50

DSGE STICKY-PRICE MODELS

Summary and Roadmap

Nominal rigidities embedded in DSGE modelMonetary shifts quantitatively “big” effects on output(Re-)articulates “old” Keynesian ideasGoodfriend and King (1997 NBER Macroeconomics Annual): the New-Neoclassical Synthesis

Output effect not very long-lasting (peak response occurs in period of monetary shock, inconsistent with data)

The “Persistence Puzzle”Examined in Chari, Kehoe, and McGrattan (2000 Econometrica) (next) and Christiano, Eichenbaum, and Evans (2005 JPE)

Inflation not very persistentSteinsson (2001 JME): “backward-looking price-setting”

26

October 9, 2008 51

DSGE STICKY-PRICE MODELS

Summary and Roadmap

Nominal rigidities embedded in DSGE modelMonetary shifts quantitatively “big” effects on output(Re-)articulates “old” Keynesian ideasGoodfriend and King (1997 NBER Macroeconomics Annual): the New-Neoclassical Synthesis

Output effect not very long-lasting (peak response occurs in period of monetary shock, inconsistent with data)

The “Persistence Puzzle”Examined in Chari, Kehoe, and McGrattan (2000 Econometrica) (next) and Christiano, Eichenbaum, and Evans (2005 JPE)

Inflation not very persistentSteinsson (2001 JME): “backward-looking price-setting”

A Phillips Curve?

Optimal policy?