No Time to be Complacent: What Post-2008 U.S., Europe and China Can Learn from Japan 1990-2005...

29

No Time to be Complacent: What Post-2008 U.S., Europe and China Can Learn from Japan 1990- 2005 Richard C. Koo Chief Economist Nomura Research Institute Tokyo February 2011

-

Upload

dale-strickland -

Category

Documents

-

view

213 -

download

0

Transcript of No Time to be Complacent: What Post-2008 U.S., Europe and China Can Learn from Japan 1990-2005...

No Time to be Complacent:What Post-2008 U.S., Europe and China Can Learn from Japan 1990-2005

Richard C. Koo

Chief Economist

Nomura Research Institute

Tokyo

February 2011

2

Exhibit 1. US Housing Prices Are Moving along the Japanese Experience

40

60

80

100

120

140

160

180

200

220

240

260

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

US: 10 Cities Composite Home Price Index

(US: Jan. 2000=100, Japan: Dec. 1985=100)

Note: per m2, 5-month moving averageSources: Bloomberg, Real Estate Economic Institute, Japan, S&P, S&P/Case-Shiller® Home Price Indices, as of Feb. 1, 2011

Composite Index Futures

Japan: Tokyo Area Condo Price1

77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99

Japan: Osaka Area Condo Price1

Futures

US

Japan

Exhibit 2. Drastic Rate Cuts Have Done Little to Revive Employment or House Prices

3

0

1

2

3

4

5

6

7

8

2003 2004 2005 2006 2007 2008 2009 2010 2011

(%)

Sources: BOJ, FRB, ECB, BOE and RMB Australia. As of Feb. 1, 2011.

Australia

EU

US

UK

Japan

4

Exhibit 3. US Economy Is still a Long Way from Previous Peak

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.083

85

87

89

91

93

95

97

99

101

103

98 99 00 01 02 03 04 05 06 07 08 09 10

(%, Seasonally adjusted, inverted)

Unemployment Rate(right scale)

Sources: US Department of Labor, FRB

(2007=100, Seasonally adjusted)

Last seen in 2005

Unemployment rate:Last seen in 1983

Industrial Production:Last seen in 1998

Industrial Production(left scale)

5

Exhibit 4. Euro-Zone Economy Is still a Long Way from Previous Peak

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.585

90

95

100

105

110

115

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Sources: Eurostat

(%, Seasonally adjusted, inverted)(Seasonally adjusted, 2005=100)

Industrial Production(left scale)

Unemployment Rate(right scale)

Last seen in 1998

Last seenin 2005

Exhibit 5. Except in Germany, Industrial Production in EuropeIs still Weak

6

70

75

80

85

90

95

100

105

110

115

120

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Spain

France

Italy

Germany

(2005 = 100, Seasonally Adjusted)

Source: Eurostat

Level Last Seen in

2006: Germany

1997: France

1994: Italy

1997: Spain

Exhibit 6. Japan’s Economy Is still a Long Way from Previous Peak

7

65

70

75

80

85

90

95

100

105

110

115

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Note: Forecasts are calculated f rom METI's survey on planned production.Sources: Ministry of Economy, Trade and Industry (METI), and Ministry of Health, Labour and Welfare

Job offers to applicants ratio(left scale)

(Seasonally adjusted, 2005=100)(Seasonally adjusted)

Industrial production (right scale) forecast

Last seen in 2003

Lowest on record

Last seen in 1983

Last seen in 2002

Exhibit 7. US Demand for Funds Has Finally Stopped Falling

8

-50

-40

-30

-20

-10

0

10

20

30

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

(D.I.)

small firms

housing bubble

collapse

IT bubblecollapse

Source: Nomura Research Institute, based on FRB, Senior Loan Officer Opinion Survey on Bank Lending Practices .Note: D.I. are calculated f rom the answers to the question, "Apart f rom normal seasonal variation, how has demand for C&I loans changed over the past three months?" D.I. = ("Substantially stronger" + "Moderately stronger"× 0.5) - ("Moderately weaker"× 0.5 + "Substantially weaker")

businesses increasing demand for funds compared to 3 months ago

businesses decreasing demand for funds compared to 3 months ago

0

large and middle-market firms

Exhibit 8. Euro Zone Demand for Funds Has Finally Stopped Falling

9

-25

-20

-15

-10

-5

0

5

10

15

2003 2004 2005 2006 2007 2008 2009 2010 2011

(D.I.)

small and mediumsized firms

Source: Nomura Research Institute, based on ECB, The Euro Area Bank Lending Survey.Note: D.I. are calculated f rom the answers to the question, "Over the past three months, how has the demand for loans or credit lines to enterprises changed at your bank, apart f rom normal seasonal f luctuations?" D.I. = ("Increased considerably" + "Increased somewhat"×0.5) - ("Decreased somewhat"×0.5 + "Decreased considerably")

business increasing demand for funds compared to 3 months ago

business decreasing demand for funds compared to 3 months ago

0

large sized firms

Exhibit 9. Japan’s De-leveraging with Zero Interest Rates Lasted for 10 Years

10

-6

-4

-2

0

2

4

6

8

10

-15

-10

-5

0

5

10

15

20

25

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Borrowings from Financial Institutions (left scale)

Funds raised in Securities Markets (left scale)

CD 3M rate (right scale)

(% Nominal GDP, 4Q Moving Average) (%)

Sources: Bank of Japan, Cabinet Of f ice, Japan

Debt-financedbubble

(4 years)

Balance sheetrecession(16 years)

Funds Raised by Non-Financial Corporate Sector

Exhibit 10. Japan’s GDP Grew in spite of Massive Loss of Wealth and Private Sector De-leveraging

11

down87%

0

100

200

300

400

500

600

700

800

200

250

300

350

400

450

500

550

600

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

(Tril.yen, Seasonally Adjusted)

Real GDP(Left Scale)

Land Price Index in Six Major Cities(Commercial, Right Scale)

(Mar. 2000=100)

Sources: Cabinet Of f ice, Japan Real Estate Institute

Nominal GDP(Left Scale)

Likely GDP Path w/o Government Action

Last seen in 1973

Cumulative 90-05 GDP

Supported by Government

Action: ~ ¥2000 trillion

Cumulative Loss of

Wealth on Shares and Real Estate

~ ¥1500 trillion

Exhibit 11. Japanese Government Borrowed and Spent the Excess Savings of the Private Sector to Sustain GDP

12

overall deficit ¥460

trillion

20

30

40

50

60

70

80

90

100

110

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Source: Ministry of Finance, JapanNote: FY 2010 includes supplementary budget. FY2011 are initial budget.

Government spending

Tax revenueBubble Collapse

(Tril. yen)

cumulativecyclical deficit 90-05

¥315 trillion

Exhibit 12. Premature Fiscal Reforms in 1997 and 2001 Weakened Economy, Reduced Tax Revenue and Increased Deficit

13

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Tax RevenueBudget Deficit

Hashimotofiscal

reform

Koizumifiscal

reform

(Yen tril.) (Yen tril.)

(FY)

Global Financial

Crisis

*

Obuchi-Morifiscal

stimulus

Source: Ministry of Finance, Japan*: estimated by MOF

unnecessaryincrease in

deficit:¥103.3 tril.

Exhibit 13. Spanish Private Sector Financial Surpluses Increased more than Government Deficit

14

-12

-8

-4

0

4

8

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Financial Surplus or Deficit by Sector

(Financial Surplus)

(Financial Deficit)

General Government

Corporate Sector(Non-Financial Sector +

Financial Sector)

Rest of the WorldHouseholds

(as a ratio to nominal GDP, %)

Shift from 2007 in private sector:16.93% of GDPCorporate: 11.45%Households: 5.48%

Shift from 2007 in public sector:11.32% of GDP

Sources: Banco de España and National Statistics Institute (INE),Spain, and EurostatNote: For 2010' figures, 4 quarter averages ending with 3Q/10' are used.

Exhibit 14. Irish Private Sector Financial Surpluses Increased more than Government Deficit

15

-15

-10

-5

0

5

10

15

2002 2003 2004 2005 2006 2007 2008 2009

Sources: Eurostat, Central Statistics Of f ice, Ireland

(as a ratio to nominal GDP, %)

Financial Surplus or Deficit by Sector

Corporate Sector(Non-Financial Sector + Financial Sector)

(Financial Surplus)

Rest of the World

Households

General Government

(Financial Deficit)

Shift from 2006 in private sector:21.55% of GDPCorporate: 7.29%

Households: 14.26%

Shift from 2006 in public sector:16.78% of GDP

Exhibit 15. Portuguese Private Sector Financial Surpluses Increased more than Government Deficit

16

-12

-9

-6

-3

0

3

6

9

12

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Sources: Banco de Portugal, Instituto Nacional de Estatística, Portugal, and EurostatNote: For 2010' f igures, 4 quarter averages ending with 3Q/10' are used.

(Financial Surplus)

(Financial Deficit)

Financial Surplus or Deficit by Sector

(as a ratio to nominal GDP, %)

Corporate Sector(Non-Financial Sector +

Financial Sector)

Rest of the World

General Government

Households

Shift from 2008 in private sector:

8.60% of GDPCorporate: 6.45%

Households: 2.15%

Shift from 2008 in public sector:

6.38% of GDP

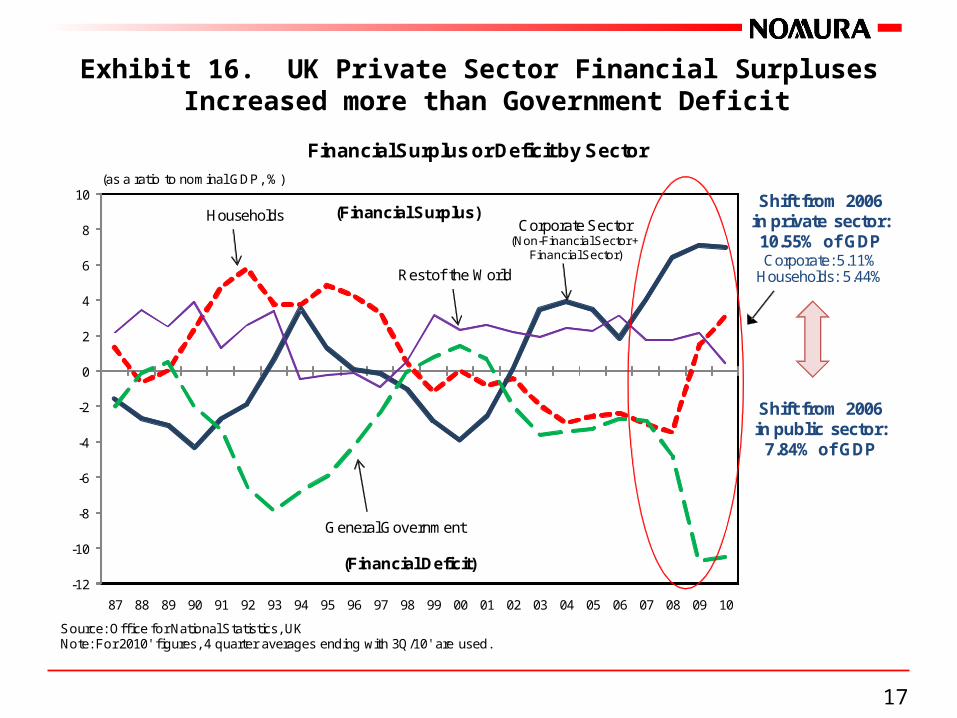

Exhibit 16. UK Private Sector Financial Surpluses Increased more than Government Deficit

17

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Financial Surplus or Deficit by Sector(as a ratio to nominal GDP, %)

(Financial Deficit)

Corporate Sector(Non-Financial Sector +

Financial Sector)

(Financial Surplus)

General Government

Rest of the World

Households

Source: Of f ice for National Statistics, UKNote: For 2010' f igures, 4 quarter averages ending with 3Q/10' are used.

Shift from 2006in private sector:10.55% of GDPCorporate: 5.11%

Households: 5.44%

Shift from 2006 in public sector:

7.84% of GDP

Exhibit 17. In Italy, Increase in Private Savings Is Not Enough to Cover Deterioration in Government Deficit

18

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Sources: Banca d'Italia, EurostatNote: For 2010' f igures, 4 quarter averages ending with 3Q/10' are used.

(Financial Surplus)

(Financial Deficit)

Corporate Sector(Non-Financial Sector +

Financial Sector)General

Government

Rest of the World

(as a ratio to nominal GDP, %)

Financial Surplus or Deficit by Sector

Households

Shift from 2008 in private sector:

0.87% of GDPCorporate: 4.35%

Households: -3.48%

Shift from 2008 in public sector:

1.68% of GDP

Exhibit 18. In Greece, Increase in Private Savings Is Not Enough to Cover Deterioration in Government Deficit

19

-16

-12

-8

-4

0

4

8

12

16

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Sources: Bank of Greece, EurostatNote: For 2010' figures, 4 quarter averages ending with 2Q/10' are used.

Financial Surplus or Deficit by Sector

(Financial Surplus)

(Financial Deficit)

Corporate Sector(Non-Financial Sector +

Financial Sector)

General Government

Households

Rest of the World

(as a ratio to nominal GDP, %)

Shift from 2008 in private sector:

2.34% of GDPCorporate: -2.94%

Households: 5.28%

Shift from 2008 in public sector:

4.82% of GDP

Exhibit 19. US Flow of Funds Data after 2008 Are Useless…

20

-12

-10

-8

-6

-4

-2

0

2

4

6

8

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Households

General Government

Rest of the World

(as a ratio to nominal GDP, %)

Sources: FRB, US Department of CommerceNote: 2010's f igures are for f rom the 1st to 3rd quarters only.

(Financial Surplus)

(Financial Deficit)

Financial Surplus or Deficit by Sector

IT Bubble

Housing BubbleCorporate Sector

(Non-Financial Sector +Financial Sector)

Numbers do not add up

at all

Shift from 2006in public sector:

8.50% of GDP

Exhibit 20. … Because of Massive Discrepancy Between Two Definitions of “Private Sector”

21

8.28% of GDP

13.29% of GDP

-8

-6

-4

-2

0

2

4

6

8

10

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

(as a ratio to nominal GDP, %)

"Private Sector" as a residual after Government and Foreign Sectors

"Private Sector" as obtained by adding Corporate, Households and

Financial Sectors

Sources: FRB, US Department of CommerceNote: 2010's f igures are for f rom the 1st to 3rd quarters only.

Exhibit 21. Japanese Corporate Financial Surplus Is Growing Again

22

-18

-15

-12

-9

-6

-3

0

3

6

9

12

15

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

(Financial Deficit)

(Financial Surplus)

(FY)

(as a ratio to nominal GDP, %)

Households

Rest of the World

Corporate Sector(Non-Financial Sector +

Financial Sector)

General Government

Financial Surplus or Deficit by Sector

Sources: Bank of Japan, Flow of Funds Accounts, and Government of Japan, Cabinet Of f ice, National AccountsNote: For 2010' f igures, 4 quarter averages ending with 3Q/10' are used.

Balance Sheet RecessionGlobal

FinancialCrisis

Shift from 2008 in public sector:

6.37% of GDP

Shift from 2008in private sector:

7.49% of GDPCorporate: 7.80%

Households: -0.31%

Exhibit 22. Summary of Private Savings and Government Deficits

23

0

5

10

15

20

25

Spain Ireland Portugal UK US Japan Italy Greece

Increases in Private Savings

Increases in Government Deficits

(indicated as % of GDP)

3

Notes: 1. Measured f rom the recent trough in private sector savings: Spain (2007), Ireland (2006), Portugal (2008), Italy (2008), UK (2007), Japan (2008), US (2006), Greece (2008).2. Changes in private savings include debt repayments.3. A range of 13% to 8% exists for the US private savings data because of problems with its Flow of Funds statistics since 2008. Economic and market indicators suggest that the 13% f igure (shown) is closer to the truth than the 8% f igure.4. Greece is NOT in balance sheet recession. Included for comparison purposes only.Source: Nomura Resarch Institute, f rom respective countries' f low of funds data

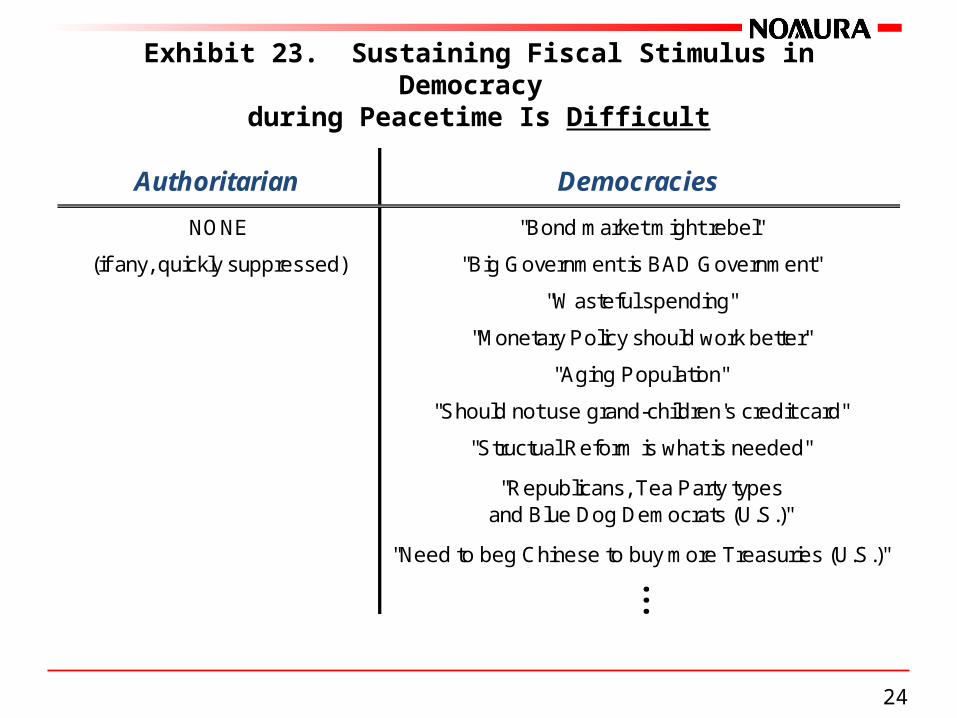

Exhibit 23. Sustaining Fiscal Stimulus in Democracy during Peacetime Is Difficult

24

Authoritarian Democracies

NONE "Bond market might rebel"

(if any, quickly suppressed) "Big Government is BAD Government"

"Wasteful spending"

"Monetary Policy should work better"

"Aging Population"

"Should not use grand-children's credit card"

"Structual Reform is what is needed"

"Republicans, Tea Party typesand Blue Dog Democrats (U.S.)"

"Need to beg Chinese to buy more Treasuries (U.S.)"...

Exhibit 24. Recovery from Lehman Shock Is NOT Recovery from Balance Sheet Recession

25

Source: Nomura Research Institute

?

Lehman Shock

Actual PathCurrent Location

Likely GDP Pathwithout Lehman Shock

Weaker Demand from Private Sector

De-leveraging

Stronger Demand from Government's

Fiscal Stimulus

(A)

(B)

Economic weakness from private-sector

de-leveraging

Economic weakness from policy mistake

on Lehman

BubbleBurst

Exhibit 25. The Exit Problem: Debt Rejection Syndrome It Took U.S. 30 Years to Normalize Interest Rate after 1929

0

1

2

3

4

5

6

7

8

9

1920 21 2223 24 2526 27 2829 30 3132 33 3435 36 3738 39 4041 42 4344 45 4647 48 4950 51 5253 54 5556 57 5859 60

US government bond yieldsPrime BA, 90daysUS government bond yields 1920-29 average (4.09%, June 1959)Prime BA, 90days 1920-29 average (4.13%, September 1959)

Oct '29 NY StockMarket Crash

Jun '50 Korean War

Dec '41 PearlHarbor Attack

(%)

'33~New Deal

Source: FRB, Banking and Monetary Statistics 1914-1970 Vol.1, pp.450-451 and 468-471, Vol.2, pp.674-676 and 720-727

26

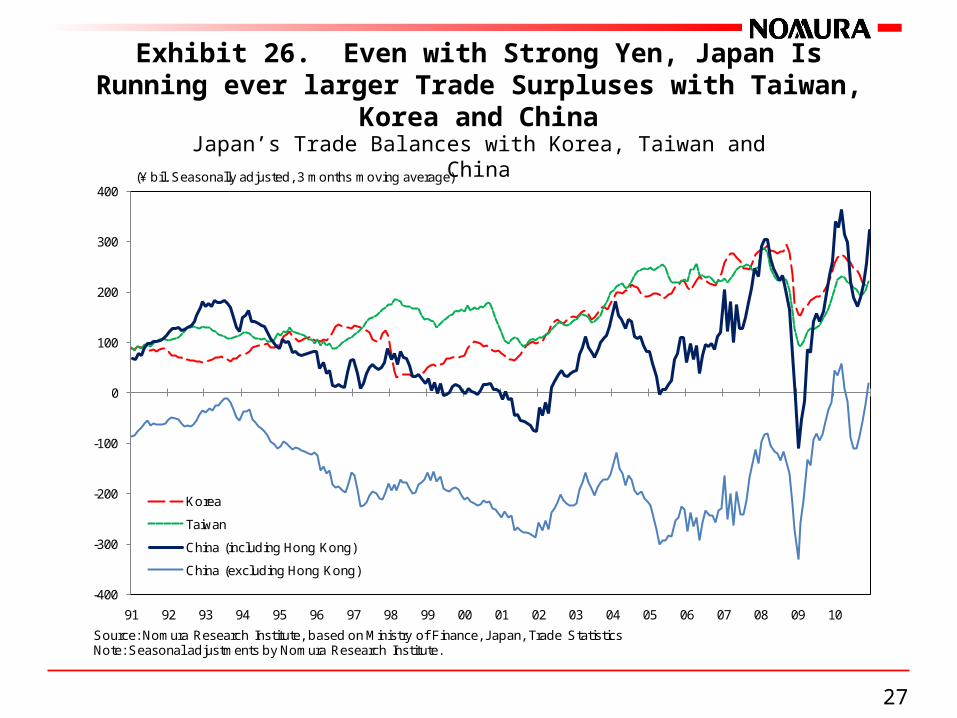

Exhibit 26. Even with Strong Yen, Japan Is Running ever larger Trade Surpluses with Taiwan, Korea and China

27

Japan’s Trade Balances with Korea, Taiwan and China

-400

-300

-200

-100

0

100

200

300

400

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Korea

Taiwan

China (including Hong Kong)

China (excluding Hong Kong)

(¥ bil. Seasonally adjusted, 3 months moving average)

Source: Nomura Research Institute, based on Ministry of Finance, Japan, Trade StatisticsNote: Seasonal adjustments by Nomura Research Institute.

28

Disclaimer

This publication has been approved for distribution in Australia by Nomura Australia Limited, which is authorised and regulated in Australia by the Australian Securities and Investment Commission ('ASIC'). This material is confidential and for your private information only. It is subject to the copyright of Nomura and no part of it may be reproduced or distributed without Nomura’s consent. This material is for discussion purposes only and is not an offer or solicitation to sell or purchase any investment or investment advice. Although it may contain indicative information which is reflective of the terms under which Nomura believes a transaction or a financial product might be arranged or agreed as of the date of this material, no assurance is given that such a transaction or product could in fact be executed, or executed on the specific terms indicated.This material does not contain all of the information that is material to any investor and may not be relied upon by you in evaluating the merits of entering into any transaction or investing in any financial products. While information other than indicative terms presented herein has been obtained from sources which we consider to be reliable, Nomura does not represent or warrant that this material is accurate or complete and, to the extent permitted by applicable law, does not accept any liability whatsoever for any loss arising from any action taken in reliance on the content of this material. Opinions and information contained herein are current as of the date of this material and are subject to change without notice. All data are historical and some or all of them may have changed since the issuance of this material. Any projections, estimates, valuations, statistical or back testing analyses are provided solely for illustrative purposes. They may be based on subjective assumptions, assessments, interpretation or interpolation of historical data and should not be relied upon as a prediction of future performance or a suggestion that any outcome is more likely than another.This material is not intended for retail clients or private customers. It is provided on the basis that you have the capability to make your own independent evaluation of the financial, market, legal, regulatory, credit, tax and accounting risks and consequences involved in the transaction or product and its suitability for your purposes and, to the extent permitted by applicable law, Nomura accepts no responsibility or liability in this regard. The transactions or products described herein may contain complex financial characteristics, risks and exposure. You may get back less than the amount you invested or in certain circumstances, none at all. Accordingly, the transaction or product is only suitable for investors who can afford to risk losing all or part of their original investment. Nomura is not your designated investment adviser. Nomura and its directors and employees may from time to time perform investment banking or other services, or may have positions or act as market maker, for or in connection with the entities or investments mentioned herein and these services and positions may be financially detrimental to you and/or this transaction or product. If you are in doubt as to any aspect of this material, you should consider obtaining independent professional advice.The information presented herein is deemed to be superseded by any subsequent versions of this material and is subject to the information later appearing in any related prospectus, offer document or final transaction documentation, which will prevail. Any decision to enter into any transaction or invest in any product must be made solely on the basis of such final transaction documentation. Nomura Australia Ltd. Tel: +61 2 8062 8000 Level 25, Governor Phillip Tower, 1 Farrer Place, NSW 2000, Australia Fax: +61 2 8062 8360 Australian Financial Services Licence No: 246412

29