![Lifschitz Realizability for Intuitionistic Zermelo ...rathjen/Lifschitz.pdf · set theories). Rathjen [22] adapted realizability to the context of constructive Zermelo-Fraenkel set](https://static.fdocuments.us/doc/165x107/5f5538ed98402f3a506d9d41/lifschitz-realizability-for-intuitionistic-zermelo-rathjen-set-theories.jpg)

No Job Name · 2011-03-16 · years, or a change in the expected realizability of de-ferred tax...

33

FASB Interpretation No. 48 Accounting for Uncertainty in Income Taxes an interpretation of FASB Statement No. 109 Financial Accounting Standards Board ORIGINAL PRONOUNCEMENTS AS AMENDED Copyright © 2010 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be repro- duced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, with- out the prior written permission of the Financial Accounting Foundation.

Transcript of No Job Name · 2011-03-16 · years, or a change in the expected realizability of de-ferred tax...

FASB Interpretation No. 48

Accounting for Uncertainty in Income Taxes

an interpretation of FASB Statement No. 109

Financial Accounting Standards Board

ORIGINAL

PRONOUNCEMENTS

AS AMENDED

Copyright © 2010 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be repro-duced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, with-out the prior written permission of the Financial Accounting Foundation.

FASB Interpretation No. 48Accounting for Uncertainty in Income Taxes

an interpretation of FASB Statement No. 109

STATUS

Issued: June 2006

Effective Date: For fiscal years beginning after December 15, 2006

Affects: Amends FAS 5, paragraphs 2 and 39Replaces FAS 109, paragraph 8(a)Amends FAS 109, paragraphs 10 and 289

Affected by: Paragraphs 8, 10(b), 12, A3, A4, A22, A24 through A26, and A29 amended by FSP FIN 48-1,paragraphs A1(a), A1(b), and A1(d) through A1(k), respectively

Paragraphs 10A through 10C added by FSP FIN 48-1, paragraph A1(c)Paragraph 12A added by FAS 141(R), paragraph E35, and amended by FAS 164,paragraph E19

Paragraph 12B added by FAS 141(R), paragraph 35Paragraphs 13 and A30 amended by Accounting Standards Update 2010-08, paragraphs A14(a)and A14(b), respectively

Paragraph 22 amended by FSP FIN 48-2, paragraph 6(a)Paragraph 22A added by FSP FIN 48-2, paragraph 6(b)Paragraph 22A amended by FSP FIN 48-3, paragraph 12Paragraph A31 amended by FAS 165, paragraph B16Paragraph C1 amended by FAS 162, paragraph B13Footnote 3 deleted by FAS 162, paragraph B13

Other Interpretive Releases: FASB Staff Position FAS 13-2FASB Staff Positions FIN 48-1 through FIN 48-3 (FSP FIN 48-2 effectivelysuperseded by FSP FIN 48-3)

Issues Discussed by FASB Emerging Issues Task Force (EITF)

Affects: No EITF Issues

Interpreted by: No EITF Issues

Related Issue: EITF Issue No. 93-7

FIN48

FIN48–1

SUMMARY

This Interpretation clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s fi-nancial statements in accordance with FASB Statement No. 109, Accounting for Income Taxes. This Interpre-tation prescribes a recognition threshold and measurement attribute for the financial statement recognition andmeasurement of a tax position taken or expected to be taken in a tax return. This Interpretation also providesguidance on derecognition, classification, interest and penalties, accounting in interim periods, disclosure, andtransition.

The evaluation of a tax position in accordance with this Interpretation is a two-step process. The first step isrecognition: The enterprise determines whether it is more likely than not that a tax position will be sustainedupon examination, including resolution of any related appeals or litigation processes, based on the technicalmerits of the position. In evaluating whether a tax position has met the more-likely-than-not recognition thresh-old, the enterprise should presume that the position will be examined by the appropriate taxing authority thathas full knowledge of all relevant information. The second step is measurement: A tax position that meets themore-likely-than-not recognition threshold is measured to determine the amount of benefit to recognize in thefinancial statements. The tax position is measured at the largest amount of benefit that is greater than 50 percentlikely of being realized upon settlement.

Differences between tax positions taken in a tax return and amounts recognized in the financial statementswill generally result in one of the following:

a. An increase in a liability for income taxes payable or a reduction of an income tax refund receivableb. A reduction in a deferred tax asset or an increase in a deferred tax liabilityc. Both (a) and (b).

An enterprise that presents a classified statement of financial position should classify a liability for unrecog-nized tax benefits as current to the extent that the enterprise anticipates making a payment within one year orthe operating cycle, if longer. An income tax liability should not be classified as a deferred tax liability unless itresults from a taxable temporary difference (that is, a difference between the tax basis of an asset or a liabilityas calculated using this Interpretation and its reported amount in the statement of financial position). This Inter-pretation does not change the classification requirements for deferred taxes.

Tax positions that previously failed to meet the more-likely-than-not recognition threshold should be recog-nized in the first subsequent financial reporting period in which that threshold is met. Previously recognized taxpositions that no longer meet the more-likely-than-not recognition threshold should be derecognized in the firstsubsequent financial reporting period in which that threshold is no longer met. Use of a valuation allowance asdescribed in Statement 109 is not an appropriate substitute for the derecognition of a tax position. The require-ment to assess the need for a valuation allowance for deferred tax assets based on the sufficiency of future tax-able income is unchanged by this Interpretation.

Reason for Issuing This Interpretation

In principle, the validity of a tax position is a matter of tax law. It is not controversial to recognize the benefitof a tax position in an enterprise’s financial statements when the degree of confidence is high that that tax posi-tion will be sustained upon examination by a taxing authority. However, in some cases, the law is subject tovaried interpretation, and whether a tax position will ultimately be sustained may be uncertain. Statement 109contains no specific guidance on how to address uncertainty in accounting for income tax assets and liabilities.As a result, diverse accounting practices have developed resulting in inconsistency in the criteria used to recog-nize, derecognize, and measure benefits related to income taxes. This diversity in practice has resulted in non-comparability in reporting income tax assets and liabilities.

FIN48 FASB Interpretations

FIN48–2

How This Interpretation Will Improve Financial Reporting

This Interpretation will result in increased relevance and comparability in financial reporting of incometaxes because all tax positions accounted for in accordance with Statement 109 will be evaluated for recogni-tion, derecognition, and measurement using consistent criteria. Finally, the disclosure provisions of this Inter-pretation will provide more information about the uncertainty in income tax assets and liabilities.

How the Conclusions in This Interpretation Relate to the Conceptual Framework

In developing the recognition and measurement guidance of this Interpretation, the Board considered thequalitative characteristics discussed in FASB Concepts Statement No. 2, Qualitative Characteristics of Ac-counting Information. Those characteristics emphasize that comparable information enables users to identifysimilarities in and differences between two sets of economic events. This Interpretation establishes a consistentthreshold for recognizing current and deferred taxes.

When a position is taken in a tax return that reduces the amount of income taxes paid to a taxing authority,the enterprise realizes an immediate economic benefit. However, considerable time can elapse before the ac-ceptability of that tax position is determined. This Interpretation requires the affirmative evaluation that it ismore likely than not, based on the technical merits of a tax position, that an enterprise is entitled to economicbenefits resulting from positions taken in income tax returns. If a tax position does not meet the more-likely-than-not recognition threshold, the benefit of that position is not recognized in the financial statements.

The Effective Date of This Interpretation

This Interpretation is effective for fiscal years beginning after December 15, 2006. Earlier application of theprovisions of this Interpretation is encouraged if the enterprise has not yet issued financial statements, includ-ing interim financial statements, in the period this Interpretation is adopted.

FIN48Accounting for Uncertainty in Income Taxes

FIN48–3

FASB Interpretation No. 48Accounting for Uncertainty in Income Taxes

an interpretation of FASB Statement No. 109

CONTENTSParagraphNumbers

Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1−2Interpretation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3−21

Scope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3−4Recognition. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5−7Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Tax-Planning Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Subsequent Recognition, Derecognition, and Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10−12Change in Judgment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13−14Interest and Penalties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15−16Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17−19Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20−21

Effective Date and Transition. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22−24Appendix A: Illustrative Guidance for Applying This Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A1−A33Appendix B: Background Information and Basis for Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B1−B74Appendix C: Impact on Related Authoritative Literature. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . C1−C5

INTRODUCTION

1. This Interpretation clarifies the accounting for un-certainty in income taxes recognized in an enter-prise’s financial statements in accordance with FASBStatement No. 109, Accounting for Income Taxes.Statement 109 does not prescribe a recognitionthreshold or measurement attribute for the financialstatement recognition and measurement of a tax posi-tion taken in a tax return. Consistent with State-ment 109, the term enterprise is used throughout thisInterpretation because accounting for income taxes isprimarily an issue for business enterprises. However,the requirements of this Interpretation apply to not-for-profit organizations. This Interpretation also ap-plies to pass-through entities and entities whose taxliability is subject to 100 percent credit for dividendspaid (for example, real estate investment trusts andregistered investment companies) that are potentiallysubject to income taxes.

2. Diversity in practice exists in the accounting forincome taxes. To address that diversity, this Interpre-tation clarifies the application of Statement 109 bydefining a criterion that an individual tax position

must meet for any part of the benefit of that positionto be recognized in an enterprise’s financial state-ments. Additionally, this Interpretation providesguidance on measurement, derecognition, classifica-tion, interest and penalties, accounting in interim pe-riods, disclosure, and transition.

INTERPRETATION

Scope

3. This Interpretation applies to all tax positions ac-counted for in accordance with Statement 109.

4. The term tax position as used in this Interpretationrefers to a position in a previously filed tax return or aposition expected to be taken in a future tax returnthat is reflected in measuring current or deferred in-come tax assets and liabilities for interim or annualperiods. A tax position can result in a permanent re-duction of income taxes payable, a deferral of in-come taxes otherwise currently payable to future

FIN48 FASB Interpretations

FIN48–4

years, or a change in the expected realizability of de-ferred tax assets. The term tax position also encom-passes, but is not limited to:

a. A decision not to file a tax returnb. An allocation or a shift of income between

jurisdictionsc. The characterization of income or a decision to

exclude reporting taxable income in a tax returnd. A decision to classify a transaction, entity, or

other position in a tax return as tax exempt.

Recognition

5. The appropriate unit of account for determiningwhat constitutes an individual tax position, andwhether the more-likely-than-not recognition thresh-old is met for a tax position, is a matter of judgmentbased on the individual facts and circumstances ofthat position evaluated in light of all available evi-dence. The determination of the unit of account to beused in applying the provisions of this Interpretationshall consider the manner in which the enterprise pre-pares and supports its income tax return and the ap-proach the enterprise anticipates the taxing authoritywill take during an examination.

6. An enterprise shall initially recognize the financialstatement effects of a tax position when it is morelikely than not, based on the technical merits, that theposition will be sustained upon examination. As usedin this Interpretation, the term more likely than notmeans a likelihood of more than 50 percent; theterms examined and upon examination also includeresolution of the related appeals or litigation proc-esses, if any. The more-likely-than-not recognitionthreshold is a positive assertion that an enterprise be-lieves it is entitled to the economic benefits associ-ated with a tax position. The determination ofwhether or not a tax position has met the more-likely-than-not recognition threshold shall consider thefacts, circumstances, and information available at thereporting date.

7. In assessing the more-likely-than-not criterion asrequired by paragraph 6 of this Interpretation:

a. It shall be presumed that the tax position will beexamined by the relevant taxing authority thathas full knowledge of all relevant information.

b. Technical merits of a tax position derive fromsources of authorities in the tax law (legislationand statutes, legislative intent, regulations, rul-ings, and case law) and their applicability to thefacts and circumstances of the tax position. Whenthe past administrative practices and precedentsof the taxing authority in its dealings with the en-terprise or similar enterprises are widely under-stood, those practices and precedents shall betaken into account.

c. Each tax position must be evaluated without con-sideration of the possibility of offset or aggrega-tion with other positions.

Measurement

8. A tax position that meets the more-likely-than-notrecognition threshold shall initially and subsequentlybe measured as the largest amount of tax benefit thatis greater than 50 percent likely of being realizedupon settlement with a taxing authority that has fullknowledge of all relevant information. Measurementof a tax position that meets the more-likely-than-notrecognition threshold shall consider the amounts andprobabilities of the outcomes that could be realizedupon settlement1 using the facts, circumstances, andinformation available at the reporting date.As used inthis Interpretation, the term reporting date refers todate of the enterprise’s most recent statement of fi-nancial position.

Tax-Planning Strategies

9. When a tax-planning strategy is contemplated as asource of future taxable income to support the realiz-ability of a deferred tax asset under paragraph 21(d)of Statement 109, paragraphs 5–8 of this Interpreta-tion shall be applied in determining the amount ofavailable future taxable income.

Subsequent Recognition, Derecogniton, andMeasurement

10. If the more-likely-than-not recognition thresholdis not met in the period for which a tax position istaken or expected to be taken, an enterprise shall rec-ognize the benefit of the tax position in the first in-terim period that meets any one of the followingthree conditions:

a. The more-likely-than-not recognition threshold ismet by the reporting date.

1For further explanation and illustration, see the illustrative examples in paragraphs A19–A30.

FIN48Accounting for Uncertainty in Income Taxes

FIN48–5

b. The tax position is effectively settled through ex-amination, negotiation, or litigation.

c. The statute of limitations for the relevant taxingauthority to examine and challenge the tax posi-tion has expired.

10A. In accordance with paragraph 10(b) of Inter-pretation 48, an enterprise shall recognize the benefitof a tax position when it is effectively settled. An en-terprise shall evaluate all of the following conditionswhen determining effective settlement:

a. The taxing authority has completed its examina-tion procedures including all appeals and admin-istrative reviews that the taxing authority is re-quired and expected to perform for the taxposition.

b. The enterprise does not intend to appeal or liti-gate any aspect of the tax position included in thecompleted examination.

c. It is remote that the taxing authority would exam-ine or reexamine any aspect of the tax position. Inmaking this assessment management shall con-sider the taxing authority’s policy on reopeningclosed examinations and the specific facts andcircumstances of the tax position. Managementshall presume the relevant taxing authority hasfull knowledge of all relevant information inmaking the assessment on whether the taxingauthority would reopen a previously closedexamination.

In the tax years under examination, a tax positiondoes not need to be specifically reviewed or exam-ined by the taxing authority to be considered effec-tively settled through examination. Effective settle-ment of a position subject to an examination does notresult in effective settlement of similar or identicaltax positions in periods that have not been examined.

10B. If an enterprise that had previously considereda tax position effectively settled becomes aware thatthe taxing authority may examine or reexamine thetax position or intends to appeal or litigate any aspectof the tax position, the tax position is no longer con-sidered effectively settled and the enterprise shall re-evaluate the tax position in accordance with Interpre-tation 48.

10C. An enterprise may obtain information duringthe examination process that enables that enterpriseto change its assessment of the technical merits of a

tax position or of similar tax positions taken in otherperiods. However, the effectively settled conditionsin paragraph 10A do not provide any basis for the en-terprise to change its assessment of the technical mer-its of any tax position in other periods.

11. An enterprise shall derecognize a previously rec-ognized tax position in the first period in which it isno longer more likely than not that the tax positionwould be sustained upon examination. Use of a valu-ation allowance2 is not a permitted substitute forderecognizing the benefit of a tax position when themore-likely-than-not recognition threshold is nolonger met.

12. Subsequent recognition, derecognition, andmeasurement shall be based on management’s bestjudgment given the facts, circumstances, and infor-mation available at the reporting date. A tax positionneed not be legally extinguished and its resolutionneed not be certain to subsequently recognize, derec-ognize, or measure the position. Subsequent changesin judgment that lead to changes in recognition,derecognition, and measurement should result fromthe evaluation of new information and not from anew evaluation or new interpretation by managementof information that was available in a previous finan-cial reporting period.

[Note:After the adoption of FASB Statement No. 141(revised 2007), Business Combinations (effectivefor business combinations with an acquisitiondate on or after the beginning of the first annualreporting period beginning on or after 12/15/08),paragraph 12Aand the related heading are addedas follows:]

Income Tax Uncertainties Acquired in aBusiness Combination

12A. The tax bases used in the calculation of de-ferred tax assets and liabilities as well as amountsdue to or receivable from taxing authorities relatedto prior tax positions at the date of a business com-bination shall be calculated in accordance with thisInterpretation.

[Note: After the adoption of FASB StatementNo. 164, Not-for-Profit Entities: Mergers and Ac-quisitions (effective prospectively in the first set ofinitial or annual financial statements for a report-ing period beginning on or after December 15,

2The term valuation allowance in this Interpretation has the same meaning as in Statement 109.

FIN48 FASB Interpretations

FIN48–6

2009) by not-for-profit entities, paragraph 12Ashould read as follows:]

12A. The tax bases used in the calculation of de-ferred tax assets and liabilities as well as amounts dueto or receivable from taxing authorities related toprior tax positions at the date of a business combina-tion or combination of not-for-profit entities—that is,an acquisition of a business or nonprofit activity by anot-for-profit entity or a combination of not-for-profitactivities—shall be calculated in accordance withthis Interpretation.

[Note: After the adoption of Statement 141(R)(effective for business combinations with anacquisition date on or after the beginning of thefirst annual reporting period beginning on or af-ter 12/15/08), paragraph 12B is added as follows:]

12B. The effect of a change to an acquired tax posi-tion, or those that arise as a result of the acquisition,shall be recognized as follows:

a. Changes within the measurement period that re-sult from new information about facts and cir-cumstances that existed as of the acquisition dateshall be recognized through a corresponding ad-justment to goodwill. However, once goodwillis reduced to zero, the remaining portion of thatadjustment shall be recognized as a gain on abargain purchase in accordance with para-graphs 36–38 of FASB Statement No. 141 (re-vised 2007), Business Combinations.

b. All other changes in acquired income tax posi-tions shall be accounted for in accordance withthis Interpretation.

Change in Judgment

13. A change in judgment that results in subsequentrecognition, derecognition, or change in measure-ment of a tax position taken in a prior annual period(including any related interest and penalties) shall berecognized as a discrete item in the period in whichthe change occurs. The provisions of paragraphs35−38 in Statement 109 that pertain to intraperiod taxallocation are not changed by this Interpretation.

14. A change in judgment that results in subsequentrecognition, derecognition, or change in measure-ment of a tax position taken in a prior interim periodwithin the same fiscal year is an integral part of anannual period and, consequently, shall be reflectedpursuant to the provisions of paragraph 19 of APB

Opinion No. 28, Interim Financial Reporting, andFASB Interpretation No. 18, Accounting for IncomeTaxes in Interim Periods.

Interest and Penalties

15. When the tax law requires interest to be paid onan underpayment of income taxes, an enterprise shallbegin recognizing interest expense in the first periodthe interest would begin accruing according to theprovisions of the relevant tax law. The amount of in-terest expense to be recognized shall be computed byapplying the applicable statutory rate of interest to thedifference between the tax position recognized in ac-cordance with this Interpretation and the amount pre-viously taken or expected to be taken in a tax return.

16. If a tax position does not meet the minimumstatutory threshold to avoid payment of penalties(considering the factors in paragraph 7 of this Inter-pretation), an enterprise shall recognize an expensefor the amount of the statutory penalty in the periodin which the enterprise claims or expects to claim theposition in the tax return. If penalties were not recog-nized when the position was initially taken, the ex-pense shall be recognized in the period in which theenterprise’s judgment about meeting the minimumstatutory threshold changes. Previously recognizedinterest and penalties associated with tax positionsthat subsequently meet one of the conditions in para-graph 10 of this Interpretation shall be derecognizedin the period that condition is met.

Classification

17. As a result of applying this Interpretation, theamount of benefit recognized in the statement of fi-nancial position may differ from the amount taken orexpected to be taken in a tax return for the currentyear. These differences represent unrecognized taxbenefits, which are the differences between a tax po-sition taken or expected to be taken in a tax returnand the benefit recognized and measured pursuant tothis Interpretation. A liability is created (or theamount of a net operating loss carryforward oramount refundable is reduced) for an unrecognizedtax benefit because it represents an enterprise’s po-tential future obligation to the taxing authority for atax position that was not recognized pursuant to thisInterpretation. An enterprise that presents a classifiedstatement of financial position shall classify a liabilityassociated with an unrecognized tax benefit as a cur-rent liability (or the amount of a net operating loss

FIN48Accounting for Uncertainty in Income Taxes

FIN48–7

carryforward or amount refundable is reduced) to theextent the enterprise anticipates payment (or receipt)of cash within one year or the operating cycle, iflonger. The liability for unrecognized tax benefits (orreduction in amounts refundable) shall not be com-bined with deferred tax liabilities or assets.

18. A tax position recognized in the financial state-ments as a result of applying this Interpretation mayalso affect the tax bases of assets or liabilities andthereby change or create temporary differences. Ataxable and deductible temporary difference is a dif-ference between the reported amount of an item inthe financial statements and the tax basis of an itemas determined by applying the recognition thresholdand measurement provisions of this Interpretation.A liability recognized as a result of applying thisInterpretation shall not be classified as a deferred taxliability unless it arises from a taxable temporarydifference.

19. Interest recognized in accordance with para-graph 15 of this Interpretation may be classified inthe financial statements as either income taxes or in-terest expense, based on the accounting policy elec-tion of the enterprise. Penalties recognized in accord-ance with paragraph 16 of this Interpretation may beclassified in the financial statements as either incometaxes or another expense classification, based on theaccounting policy election of the enterprise. Thoseelections shall be consistently applied.

Disclosures

20. An enterprise shall disclose its policy on classifi-cation of interest and penalties in accordance withparagraph 19 of this Interpretation in the footnotes tothe financial statements.

21. An enterprise shall disclose the following at theend of each annual reporting period presented:

a. A tabular reconciliation of the total amounts ofunrecognized tax benefits at the beginning andend of the period, which shall include at aminimum:(1) The gross amounts of the increases and

decreases in unrecognized tax benefits as aresult of tax positions taken during a priorperiod

(2) The gross amounts of increases and de-creases in unrecognized tax benefits as a re-sult of tax positions taken during the currentperiod

(3) The amounts of decreases in the unrecog-nized tax benefits relating to settlementswith taxing authorities

(4) Reductions to unrecognized tax benefits as aresult of a lapse of the applicable statute oflimitations

b. The total amount of unrecognized tax benefitsthat, if recognized, would affect the effective taxrate

c. The total amounts of interest and penalties recog-nized in the statement of operations and the totalamounts of interest and penalties recognized inthe statement of financial position

d. For positions for which it is reasonably possiblethat the total amounts of unrecognized tax ben-efits will significantly increase or decrease within12 months of the reporting date:(1) The nature of the uncertainty(2) The nature of the event that could occur in

the next 12 months that would cause thechange

(3) An estimate of the range of the reasonablypossible change or a statement that an esti-mate of the range cannot be made

e. A description of tax years that remain subject toexamination by major tax jurisdictions.

EFFECTIVE DATE AND TRANSITION

22. For public enterprises (as defined in para-graph 289, as amended, of Statement 109) and non-public consolidated entities of public enterprises thatapply U.S. generally accepted accounting principles(GAAP), this Interpretation shall be effective for fis-cal years beginning after December 15, 2006. Earlieradoption is permitted as of the beginning of an enter-prise’s fiscal year, provided the enterprise has not yetissued financial statements, including financial state-ments for any interim period, for that fiscal year.

22A. For nonpublic enterprises (as defined in para-graph 289, as amended, of Statement 109), except fornonpublic consolidated entities of public enterprisesthat apply U.S. GAAP, this Interpretation shall be ef-fective for annual financial statements for fiscal yearsbeginning after December 15, 2008 (applied as of thebeginning of the enterprise’s fiscal year) unless thenonpublic enterprises issued a full set of annual fi-nancial statements using the recognition, measure-ment, and disclosure provisions of this Interpretationbefore the issuance of FSP FIN 48-3, Effective Dateof Interpretation No. 48 for Certain Nonpublic Enter-prises. Nonpublic enterprises that issued a full set ofannual financial statements using the recognition,

FIN48 FASB Interpretations

FIN48–8

measurement, and disclosure provisions of this Inter-pretation prior to the issuance of FSP FIN 48-3 mustcontinue to apply the provisions of this Interpretation.Earlier adoption is permitted as of the beginning ofan enterprise’s fiscal year.

23. The provisions of this Interpretation shall be ap-plied to all tax positions upon initial adoption of thisInterpretation. Only tax positions that meet the more-likely-than-not recognition threshold at the effectivedate may be recognized or continue to be recognizedupon adoption of this Interpretation. The cumulativeeffect of applying the provisions of this Interpretationshall be reported as an adjustment to the opening bal-ance of retained earnings (or other appropriate com-ponents of equity or net assets in the statement of fi-nancial position) for that fiscal year, presented

separately. The cumulative-effect adjustment doesnot include items that would not be recognized inearnings, such as the effect of adopting this Interpre-tation on tax positions related to business combina-tions. The amount of that cumulative-effect adjust-ment is the difference between the net amount ofassets and liabilities recognized in the statement of fi-nancial position prior to the application of this Inter-pretation and the net amount of assets and liabilitiesrecognized as a result of applying the provisions ofthis Interpretation.

24. An enterprise shall disclose the cumulative effectof the change on retained earnings in the statement offinancial position as of the date of adoption. This dis-closure is required only in the year of adoption.

The provisions of this Interpretation neednot be applied to immaterial items.

This Interpretation was adopted by the unanimous vote of the seven members of the Financial AccountingStandards Board:

Robert H. Herz,Chairman

George J. Batavick

G. Michael CroochKatherine SchipperLeslie F. Seidman

Edward W. TrottDonald M. Young

Appendix A

ILLUSTRATIVE GUIDANCE FOR APPYLING THIS INTERPRETATION

CONTENTSParagraphNumbers

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A1Recognition Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A2–A18

Two-Step Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A2–A4Recognition Determinations Are Made for Each Unit of Account. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A5–A7Change in the Unit of Account. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A8–A9Recognition of a Liability upon Adoption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A10–A11Administrative Practices—Asset Capitalization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A12–A13Administrative Practices—Nexus. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A14–A15Valuation Allowance and Tax-Planning Strategies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A16–A18

Measurement Examples. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A19–A30Highly Certain Tax Positions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A19–A20Measurement with Information about the Approach to Settlement (Scenario 1) . . . . . . . . . . . . . . . A21–A22Measurement with Information about the Approach to Settlement (Scenario 2) . . . . . . . . . . . . . . . A23–A24Measurement of a Tax Position after Settlement of a Similar Position. . . . . . . . . . . . . . . . . . . . . . . . . . A25–A30

Differences Related to Timing of Deductibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A26–A27Change in Timing of Deductibility. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A28–A30

Subsequent Events . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A31–A32Illustrative Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A33

FIN48Accounting for Uncertainty in Income Taxes

FIN48–9

Appendix A

ILLUSTRATIVE GUIDANCE FORAPPLYING THIS INTERPRETATION

Introduction

A1. This appendix, which is an integral part of therequirements of this Interpretation, provides illustra-tive guidance for applying the provisions of this In-terpretation. The examples and related assumptionsin this appendix are illustrative only; the examplesare not all-inclusive and they may not represent ac-tual situations. The tables in paragraphsA21 andA23are intended to assist in understanding the provisionsof this Interpretation. The Board does not intend toimply a documentation requirement by includingthese examples in this Interpretation.

Recognition Examples

Two-Step Process

A2. The application of this Interpretation requires atwo-step process that separates recognition frommeasurement. The first step is determining whether atax position has met the recognition threshold; thesecond step is measuring a tax position that meets therecognition threshold. The recognition threshold ismet when the taxpayer (the reporting enterprise) con-cludes that, consistent with paragraphs 5–7 of this In-terpretation, it is more likely than not that the tax-payer will sustain the benefit taken or expected to betaken in the tax return in a dispute with taxing au-thorities if the taxpayer takes the dispute to the courtof last resort.

A3. Relatively few disputes are resolved throughlitigation, and very few are taken to the court of lastresort. Generally, the taxpayer and the taxing author-ity negotiate a settlement to avoid the costs and haz-ards of litigation. As a result, the measurement of thetax position is based on management’s best judgmentof the amount the taxpayer would ultimately acceptin a settlement with taxing authorities.

A4. This Interpretation requires that the enter-prise recognize the largest amount of benefit that isgreater than 50 percent likely of being realized uponsettlement.

Recognition Determinations Are Made for EachUnit of Account

A5. An enterprise anticipates claiming a $1 millionresearch and experimentation credit on its tax returnfor the current fiscal year. The credit comprises equalspending on 4 separate projects (that is, $250,000 oftax credit per project). The enterprise expects to havesufficient taxable income in the current year to fullyutilize the $1 million credit. Upon review of the sup-porting documentation, management believes it ismore likely than not that the enterprise will ulti-mately sustain a benefit of approximately $650,000.The anticipated benefit consists of approximately$200,000 per project for the first 3 projects and$50,000 for the fourth project.

A6. In its evaluation of the appropriate amount torecognize, management first determines the appro-priate unit of account for the tax position. Because ofthe magnitude of expenditures in each project, man-agement concludes that the appropriate unit of ac-count is each individual research project. In reachingthis conclusion, management considers both the levelat which it accumulates information to support thetax return and the level at which it anticipates ad-dressing the issue with taxing authorities. In this ex-ample, upon review of the four projects including themagnitude of expenditures, management determinesthat it accumulates information at the project level.Management also anticipates the taxing authoritywill address the issues during an examination at thelevel of individual projects.

A7. In evaluating the projects for recognition, man-agement determines that three projects meet themore-likely-than-not recognition threshold. How-ever, due to the nature of the activities that constitutethe fourth project, it is uncertain that the tax benefitrelated to this project will be allowed. Because thetax benefit related to that fourth project does not meetthe more-likely-than-not recognition threshold, itshould not be recognized in the financial statements,even though tax positions associated with that projectwill be included in the tax return. The enterprisewould recognize a $600,000 financial statement ben-efit related to the first 3 projects but would not recog-nize a financial statement benefit related to the fourthproject.

FIN48 FASB Interpretations

FIN48–10

Change in the Unit of Account

A8. Presume the facts in the preceding example foryear 1. In year 2, the enterprise increases its spendingon research and experimentation projects and antici-pates claiming significantly larger research credits inits year 2 tax return. In light of the significant increasein expenditures, management reconsiders the appro-priateness of the unit of account and concludes thatthe project level is no longer the appropriate unit ofaccount for research credits. This conclusion is basedon the magnitude of spending and anticipatedclaimed credits and on previous experience and isconsistent with the advice of external tax advisors.Management anticipates the taxing authority will fo-cus the examination on functional expenditures whenexamining the year 2 return and thus needs to evalu-ate whether it can change the unit of account in sub-sequent years’ tax returns.

A9. Determining the unit of account requires evalu-ation of the enterprise’s facts and circumstances. Inmaking that determination, management evaluatesthe manner in which it prepares and supports its in-come tax return and the manner in which it antici-pates addressing issues with taxing authorities duringan examination. The unit of account should be con-sistently applied to similar positions from period toperiod unless a change in facts and circumstances in-dicates that a different unit of account is more appro-priate. Because of the significant change in the taxposition in year 2, management’s conclusion that thetaxing authority will likely examine tax credits in theyear 2 tax return at a more detailed level than the in-dividual project is reasonable and appropriate. Ac-cordingly, the enterprise should reevaluate the unit ofaccount for the year 2 financial statements based onthe new facts and circumstances.

Recognition of a Liability upon Adoption

A10. On December 31, 2005, an enterprise accruedbut did not pay $1 million in environmental remedia-tion costs. The enterprise did not expect to take a de-duction for those costs in its income tax return. Theenterprise has a statutory effective tax rate of 40 per-cent and recognized a $1 million expense, reduced bya $400,000 deferred tax benefit which it recognizedas a deferred tax asset. The enterprise had sufficientfuture taxable income of an appropriate character anddid not recognize a valuation allowance on the de-ferred tax asset. Also on December 31, 2005, the en-terprise entered into a transaction that accelerated thedeductibility of the environmental remediation costs

into the current year. As a result, the enterprise took acurrent tax benefit of $400,000, with a correspondingdecrease to the deferred tax asset. The enterprise tookthis position in its 2005 income tax return. Uponadopting the provisions of this Interpretation on Janu-ary 1, 2007, the enterprise evaluates the accelerateddeduction of the environmental remediation costsand determines that the position does not meet themore-likely-than-not recognition threshold. The en-terprise does not believe that previously recognizingthose costs was an error (as defined in FASB State-ment No. 154, Accounting Changes and Error Cor-rections) based on its historical accounting policy forconsidering tax law uncertainties.

A11. The enterprise does not expect that it will makeany payments to the taxing authority related to thededuction of those accelerated costs within the next12 months, which is the company’s operating cycle.Accordingly, the enterprise would derecognize thetax benefit related to those accelerated costs by rec-ognizing a $400,000 increase in the noncurrent tax li-ability, with a corresponding increase in the deferredtax asset. The enterprise determines that it has suffi-cient future taxable income of the appropriate charac-ter, and thus a valuation allowance is not necessary.Based on the provisions of the tax law, the enterprisewould evaluate the tax position for accrual of interestand penalties.

Administrative Practices—Asset Capitalization

A12. An enterprise has established a capitalizationthreshold of $2,000 for its tax return for routine prop-erty and equipment purchases. Assets purchased forless than $2,000 are claimed as expenses on the taxreturn in the period they are purchased. The tax lawdoes not prescribe a capitalization threshold for indi-vidual assets, and there is no materiality provision inthe tax law. The enterprise has not been previouslyexamined. Management believes that based on previ-ous experience at a similar enterprise and current dis-cussions with its external tax advisors, the taxing au-thority will not disallow tax positions based on thatcapitalization policy and the taxing authority’s his-torical administrative practices and precedents.

A13. Some might deem the enterprise’s capitaliza-tion policy a technical violation of the tax law, sincethat law does not prescribe capitalization thresholds.However, in this situation the enterprise has con-cluded that the capitalization policy is consistent withthe demonstrated administrative practices and prece-dents of the taxing authority and the practices of

FIN48Accounting for Uncertainty in Income Taxes

FIN48–11

other enterprises that are regularly examined by thetaxing authority. Based on its previous experiencewith other enterprises and consultation with its exter-nal tax advisors, management believes the adminis-trative practice is widely understood. Accordingly,because management expects the taxing authority toallow this position when and if examined, the more-likely-than-not recognition threshold has been met.

Administrative Practices—Nexus

A14. An enterprise has been incorporated in Juris-dictionAfor 50 years; it has filed a tax return in Juris-diction A in each of those 50 years. The enterprisehas been doing business in Jurisdiction B for ap-proximately 20 years and has filed a tax return in Ju-risdiction B for each of those 20 years. However, theenterprise is not certain of the exact date it began do-ing business, or the date it first had nexus, in Jurisdic-tion B. Upon adoption of this Interpretation, the en-terprise commences a review of all open tax years inall jurisdictions.

A15. If a tax return is not filed, the statute of limita-tions never begins to run; accordingly, failure to file atax return effectively means there is no statute oflimitations. The enterprise has become familiar withthe administrative practices and precedents of Juris-diction B and understands that Jurisdiction B willlook back only six years in determining if there is atax return due and a deficiency owed. Because of theadministrative practices of the taxing authority andthe facts and circumstances, the enterprise believes itis more likely than not that a tax return is not requiredto be filed in Jurisdiction B at an earlier date and thata liability for tax exposures for those periods is notrequired upon adoption of this Interpretation.

Valuation Allowance and Tax-Planning Strategies

A16. An enterprise has a wholly owned subsidiarywith certain deferred tax assets as a result of severalyears of losses from operations. Management has de-

termined that it is more likely than not that sufficientfuture taxable income will not be available to realizethose deferred tax assets. Therefore, managementrecognizes a full valuation allowance for those de-ferred tax assets both in the separate financial state-ments of the subsidiary and in the consolidated finan-cial statements of the enterprise.

A17. Management has identified certain tax-planning strategies that might enable the realizationof those deferred tax assets. Management has deter-mined that the strategies will meet the minimumstatutory threshold to avoid penalties and that it is notmore likely than not that the strategies would besustained upon examination based on the technicalmerits.

A18. Accordingly, those strategies may not be usedto reduce the valuation allowance on the deferred taxassets. Only a tax-planning strategy that meets themore-likely-than-not recognition threshold would beconsidered in evaluating the sufficiency of future tax-able income for realization of deferred tax assets.

Measurement Examples

Highly Certain Tax Positions

A19. An enterprise has taken a tax position that itbelieves is based on clear and unambiguous tax lawfor the payment of salaries and benefits to employ-ees. The class of salaries being evaluated in this taxposition is not subject to any limitations on deduct-ibility (for example, executive salaries are not in-cluded), and none of the expenditures are required tobe capitalized (for example, the expenditures do notpertain to the production of inventories); all amountsaccrued at year-end were paid within the statutorilyrequired time frame subsequent to the reportingdate. Management concludes that the salaries arefully deductible.

FIN48 FASB Interpretations

FIN48–12

A20. Because of the difficulty of defining an uncer-tain tax position, the Board decided that all tax posi-tions are subject to the provisions of this Interpreta-tion. However, because the deduction is based onclear and unambiguous tax law, management has ahigh confidence level in the technical merits of thisposition. Accordingly, the tax position clearly meetsthe recognition criterion and should be evaluated formeasurement. In determining the amount to measure,management is highly confident that the full amountof the deduction will be allowed and it is clear that itis greater than 50 percent likely that the full amountof the tax position will be ultimately realized. Ac-

cordingly, the enterprise would recognize the fullamount of the tax position in the financial statements.

Measurement with Information about theApproach to Settlement (Scenario 1)

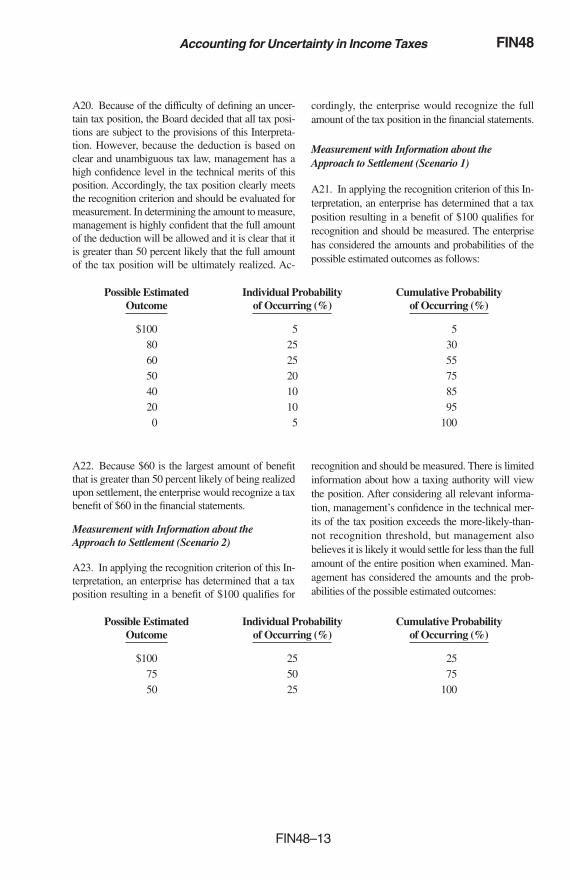

A21. In applying the recognition criterion of this In-terpretation, an enterprise has determined that a taxposition resulting in a benefit of $100 qualifies forrecognition and should be measured. The enterprisehas considered the amounts and probabilities of thepossible estimated outcomes as follows:

Possible EstimatedOutcome

Individual Probabilityof Occurring (%)

Cumulative Probabilityof Occurring (%)

$100 5 580 25 3060 25 5550 20 7540 10 8520 10 950 5 100

A22. Because $60 is the largest amount of benefitthat is greater than 50 percent likely of being realizedupon settlement, the enterprise would recognize a taxbenefit of $60 in the financial statements.

Measurement with Information about theApproach to Settlement (Scenario 2)

A23. In applying the recognition criterion of this In-terpretation, an enterprise has determined that a taxposition resulting in a benefit of $100 qualifies for

recognition and should be measured. There is limitedinformation about how a taxing authority will viewthe position. After considering all relevant informa-tion, management’s confidence in the technical mer-its of the tax position exceeds the more-likely-than-not recognition threshold, but management alsobelieves it is likely it would settle for less than the fullamount of the entire position when examined. Man-agement has considered the amounts and the prob-abilities of the possible estimated outcomes:

Possible EstimatedOutcome

Individual Probabilityof Occurring (%)

Cumulative Probabilityof Occurring (%)

$100 25 2575 50 7550 25 100

FIN48Accounting for Uncertainty in Income Taxes

FIN48–13

A24. Because $75 is the largest amount of benefitthat is greater than 50 percent likely of being realizedupon settlement, the enterprise would recognize a taxbenefit of $75 in the financial statements.

Measurement of a Tax Position after Settlement ofa Similar Position

A25. In applying the recognition criterion of this In-terpretation, an enterprise has determined that a taxposition resulting in a benefit of $100 qualifies forrecognition and should be measured. In a recentsettlement with the taxing authority, the enterprisehas agreed to the treatment for that position for cur-rent and future years. There are no recently issuedrelevant sources of tax law that would affect the en-terprise’s assessment. The enterprise has not changedany assumptions or computations, and the current taxposition is consistent with the position that was re-cently settled. In this case, the enterprise would havea very high confidence level about the amount thatwill be ultimately realized and little informationabout other possible outcomes. Management will notneed to evaluate other possible outcomes because itcan be confident of the largest amount of benefit thatis greater than 50 percent likely of being realizedupon settlement without that evaluation.

Differences related to timing of deductibility

A26. In year 1, an enterprise acquired a separatelyidentifiable intangible asset for $15 million that hasan indefinite life for financial statement purposes andis, therefore, not subject to amortization. Based onsome uncertainty in the tax code, the enterprise de-cides for tax purposes to deduct the entire cost of theasset in year 1. While the enterprise is certain that thefull amount of the intangible is ultimately deductiblefor tax purposes, the timing of deductibility is uncer-tain under the tax code. In applying the recognitioncriterion of this Interpretation, the enterprise has de-termined that the tax position qualifies for recogni-tion and should be measured. The enterprise believesit is 25 percent likely it would be able to realize im-mediate deduction upon settlement, and it is certain itcould sustain a 15-year amortization for tax purposes.Thus, the largest year 1 benefit that is greater than50 percent likely of being realized upon settlement isthe tax effect of $1 million (the year 1 deduction fromstraight-line amortization of the asset over 15 years).

A27. At the end of year 1, the enterprise should re-flect a deferred tax liability for the tax effect of the

temporary difference created by the difference be-tween the financial statement basis of the asset ($15million) and the tax basis of the asset computed in ac-cordance with this Interpretation ($14 million, thecost of the asset reduced by $1 million of amortiza-tion). The enterprise also should reflect a tax liabilityfor the tax-effected difference between the as-filedtax position ($15 million deduction) and the amountof the deduction that is considered more likely thannot of being sustained ($1 million). The enterpriseshould evaluate the tax position for accrual of statu-tory penalties as well as interest expense on the dif-ference between the amounts reported in the financialstatements and the tax position taken in the tax return.

Change in timing of deductibility

A28. Prior to the issuance of this Interpretation, anenterprise took a tax position in which it amortizedthe cost of an acquired asset on a straight-line basisover three years, while the amortization period for fi-nancial reporting purposes is seven years. At the datethe enterprise adopts this Interpretation, it has de-ducted one-third of the cost of the asset in its incometax return and one-seventh of the cost in the financialstatements and, consequently, has a deferred tax li-ability for the difference between the financial report-ing and tax bases of the asset.

A29. Upon adoption, the enterprise evaluates the taxposition in accordance with the provisions of this In-terpretation. The enterprise determines that it is cer-tain that the entire cost of the acquired asset is fullydeductible, so the more-likely-than-not recognitionthreshold has been met. However, the enterprise be-lieves that the largest benefit that is greater than50 percent likely of being realized upon settlement isstraight-line amortization over 7 years.

A30. Upon adoption of this Interpretation, the enter-prise should eliminate the deferred tax liability andrecognize a liability for unrecognized tax benefitsbased on the difference between the three- and seven-year amortization. Additionally, the enterprise shouldrecognize any additional liability required for interestand penalties, if applicable under the tax law with theoffsetting amount reflected as part of the cumulative-effect adjustment to the opening balance of retainedearnings (or other appropriate components of equityor net assets in the statement of financial position) forthat fiscal year.

FIN48 FASB Interpretations

FIN48–14

Subsequent Events

A31. Enterprise A has evaluated a tax position at itsmost recent reporting date and has concluded that theposition meets the more-likely-than-not recognitionthreshold. In evaluating the tax position for recogni-tion, Enterprise A considered all relevant sources oftax law, including a court case in which the taxing au-thority has fully disallowed a similar tax positionwith an unrelated enterprise (Enterprise B). The tax-ing authority and Enterprise B are aggressively liti-gating the matter. Although Enterprise A was awareof that court case at the recent reporting date, man-agement determined that the more-likely-than-notrecognition threshold had been met. Subsequent tothe reporting date, but prior to the financial state-ments being issued or being available to be issued(appropriate date determined in accordance withFASB Statement No. 165, Subsequent Events), thetaxing authority prevailed in its litigation with Enter-prise B, and Enterprise A concludes that it is nolonger more likely than not that it will sustain theposition.

A32. Paragraph 11 of this Interpretation notes that“an enterprise shall derecognize a previously recog-nized tax position in the first period in which it is nolonger more likely than not that the tax positionwould be sustained upon examination,” and para-graph 12 indicates that “subsequent recognition,derecognition, and measurement shall be based onmanagement’s best judgment given the facts, circum-stances, and information available at the reportingdate.” Because the resolution of Enterprise B’s litiga-tion with the taxing authority is the information thatcaused Enterprise A to change its judgment about thesustainability of the position and that informationwas not available at the reporting date, the change injudgment would be recognized in the first quarter ofthe current fiscal year.

Illustrative Disclosure

A33. The following example illustrates disclosuresabout uncertainty in income taxes. In this illustrativeexample, the reporting entity has adopted the provi-sions of this Interpretation for the year ended Decem-ber 31, 2007:

The Company or one of its subsidiaries files in-come tax returns in the U.S. federal jurisdiction,and various states and foreign jurisdictions. Withfew exceptions, the Company is no longer sub-ject to U.S. federal, state and local, or non-U.S.income tax examinations by tax authorities foryears before 2001. The Internal Revenue Service(IRS) commenced an examination of the Compa-ny’s U.S. income tax returns for 2002 through2004 in the first quarter of 2007 that is anticipatedto be completed by the end of 2008. As of De-cember 31, 2007, the IRS has proposed certainsignificant adjustments to the Company’s transferpricing and research credits tax positions. Man-agement is currently evaluating those proposedadjustments to determine if it agrees, but if ac-cepted, the Company does not anticipate the ad-justments would result in a material change to itsfinancial position. However, the Company antici-pates that it is reasonably possible that an addi-tional payment in the range of $80 to $100 mil-lion will be made by the end of 2008.

The Company adopted the provisions of FASBInterpretation No. 48, Accounting for Uncer-tainty in Income Taxes, on January 1, 2007. As aresult of the implementation of Interpretation 48,the Company recognized approximately a$200 million increase in the liability for unrecog-nized tax benefits, which was accounted for as areduction to the January 1, 2007, balance of re-tained earnings. A reconciliation of the beginningand ending amount of unrecognized tax benefitsis as follows:

(in thousands)

Balance at January 1, 2007 $370,000Additions based on tax positions related to the current year 10,000Additions for tax positions of prior years 30,000Reductions for tax positions of prior years (60,000)Settlements (40,000)

Balance at December 31, 2007 $310,000

FIN48Accounting for Uncertainty in Income Taxes

FIN48–15

Included in the balance at December 31, 2007,are $60 million of tax positions for which the ulti-mate deductibility is highly certain but for whichthere is uncertainty about the timing of such de-ductibility. Because of the impact of deferred taxaccounting, other than interest and penalties, thedisallowance of the shorter deductibility periodwould not affect the annual effective tax rate butwould accelerate the payment of cash to the tax-ing authority to an earlier period.

The Company recognizes interest accrued relatedto unrecognized tax benefits in interest expenseand penalties in operating expenses. During theyears ended December 31, 2007, 2006, and 2005,the Company recognized approximately $10,$11, and $12 million in interest and penalties.The Company had approximately $60 and$50 million for the payment of interest and penal-ties accrued at December 31, 2007, and 2006,respectively.

Appendix B

BACKGROUND INFORMATION AND BASIS FOR CONCLUSIONS

CONTENTSParagraphNumbers

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B1Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B2–B8Objective of This Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B9Scope of This Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B10–B12Unit of Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B13–B14Benefit Recognition Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B15–B16Examination Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B17–B22Approaches That Combine Recognition and Measurement. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B23–B26

Fair Value Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B23–B24Measurement Attributes That Use Fair Value Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B25–B26

Approaches That Discretely Consider Recognition and Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . B27–B34Two-Step Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B27–B28Alternative Recognition Thresholds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B29–B34

Minimum Statutory Threshold . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B29Probable Recognition Threshold . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B30–B32More Likely Than Not . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B33Tax Opinions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B34

Administrative Practices and Precedents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B35–B37Subsequent Events . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B38–B40Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B41–B44Subsequent Recognition, Derecognition, and Measurement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B45–B47Change in Judgment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B48–B49Interest and Penalties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B50–B53Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B54–B59Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B60–B64Impact on Convergence with International Financial Reporting Standards . . . . . . . . . . . . . . . . . . . . . . . . B65–B67Nonpublic Enterprises. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B68–B69Effective Date and Transition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B70–B72Benefits and Costs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B73–B74

FIN48 FASB Interpretations

FIN48–16

Appendix B

BACKGROUND INFORMATION AND BASISFOR CONCLUSIONS

Introduction

B1. This appendix summarizes considerations thatBoard members deemed significant in reaching theconclusions in this Interpretation. It includes reasonsfor accepting certain approaches and rejecting others.Individual Board members gave greater weight tosome factors than to others.

Background

B2. Diverse accounting practices had developedwith respect to the recognition and measurement ofcurrent and deferred tax assets and liabilities in finan-cial statements. That diversity resulted from inconsis-tency in the criteria used to recognize, derecognize,and measure the economic benefits associated withtax positions.

B3. On July 12, 2005, the Board issued an ExposureDraft, Uncertain Tax Positions, that proposed guid-ance for the recognition, derecognition, and measure-ment of tax positions, as well as certain disclosure re-quirements. The Board received 118 comment letterson the Exposure Draft. On October 10, 2005, theBoard held a public roundtable discussion on issuesaddressed in the Exposure Draft and comments re-ceived in the comment letters. The Board consideredcomments and concerns raised by respondents andconstituents in its redeliberations of the issues ad-dressed by the Exposure Draft in public meetingsfrom December 2005 through May 2006. This Inter-pretation reflects the results of those deliberations.

B4. Prior to the issuance of this Interpretation, taxpositions were sometimes recognized in the financialstatements on an as-filed or to-be-filed tax basis, suchthat current or deferred tax assets and liabilities wereimmediately recognized when the related tax posi-tion was taken (or expected to be taken). In somecases, the ultimate realizability of any current or de-ferred tax benefit was evaluated and a valuation al-lowance was recorded.

B5. Tax positions were also sometimes categorizedas uncertain, but not aggressive, and recognized on abest estimate basis or when the benefit met the defini-tion of an asset in FASB Concepts Statement No. 6,Elements of Financial Statements. They were also

sometimes deemed aggressive based on an enter-prise’s preestablished criteria and accounted for inaccordance with the guidance on accounting for gaincontingencies in paragraph 17 of FASB StatementNo. 5, Accounting for Contingencies.

B6. Finally, tax positions were sometimes recog-nized based on a predetermined threshold of whetherthe positions would be sustained on examination andreduced by a liability for a contingent loss that wasrecorded either when the threshold was no longermet or when it became probable that a paymentwould be made to the taxing authority.

B7. In developing this Interpretation, the Board con-sidered the following issues:

a. Whether the financial statement recognition of atax position should presume a review of an indi-vidual tax position during an examination by ataxing authority

b. How the nature of evidence supporting a tax po-sition should be used to establish recognition andmeasurement guidance.

B8. The Board considered the approaches currentlyused in practice to recognize and measure the finan-cial statement consequences of tax positions and de-veloped two kinds of alternative approaches: thosethat combine recognition and measurement into asingle methodology and those that treat recognitionand measurement separately. The Board considered:

a. Measuring tax assets and liabilities at fair valueor using fair-value-type measurement techniques,which combine recognition and measurement

b. Three recognition approaches that require sepa-rate consideration of measurement:(1) Recognition when a tax position has met a

minimum statutory threshold and additionalamounts are not anticipated to be paid tosettle underpayment controversies

(2) Recognition and derecognition based on asingle threshold

(3) Recognition when a tax position has met aspecified confidence level and derecognitionwhen the position falls below a specifiedconfidence level.

Objective of This Interpretation

B9. This Interpretation provides guidance for recog-nizing and measuring tax positions taken or expectedto be taken in a tax return that directly or indirectly

FIN48Accounting for Uncertainty in Income Taxes

FIN48–17

affect amounts reported in financial statements. ThisInterpretation also provides accounting guidance forthe related income tax effects of tax positions that donot meet the recognition threshold specified in thisInterpretation.

Scope of This Interpretation

B10. The Board considered whether to apply theprovisions of this Interpretation to all taxes (incometaxes and other taxes), to all tax positions subject toStatement 109, or to some subset of tax positionsdeemed to be uncertain based on their attributes. TheExposure Draft stated that the “proposed Interpreta-tion would broadly apply to all tax positions ac-counted for in accordance with Statement 109, in-cluding tax positions that pertain to assets andliabilities acquired in business combinations. Itwould apply to tax positions taken in tax returns pre-viously filed as well as positions anticipated to betaken in future tax returns.”

B11. Respondents to the Exposure Draft suggestedthat normal business transactions be excluded fromthe scope of the final Interpretation and that the finalInterpretation apply only to tax positions character-ized by (a) substantial uncertainty (such as tax shel-ters, tax motivated positions, and listed transactions)or (b) nontaxable or nondeductible differences be-tween financial statements and tax returns (some-times referred to as permanent differences).

B12. In its redeliberations, the Board consideredwhether to apply the provisions of this Interpretationto all income tax positions or some subset of incometax positions, specifically, uncertain tax positions.The Board concluded that limiting the application toonly uncertain tax positions, or tax positions withspecified attributes, would create a rules-based stand-ard that would result in inconsistent application andwould add complexity to the accounting guidance forincome taxes. The Board does not anticipate that thisInterpretation will have a significant effect on howenterprises account for tax positions that are routinebusiness transactions that are clearly more likely thannot of being sustained at their full amounts upon ex-amination (see the example in paragraphs A19 andA20). Accordingly, the Board decided that this Inter-pretation should broadly apply to all tax positions.

Unit of Account

B13. The Exposure Draft indicated that the appro-priate unit of account would be a matter of individualfacts and circumstances evaluated in light of all avail-

able evidence. Respondents to the Exposure Draft re-quested that the Board provide additional guidanceon the unit of account in the final Interpretation. TheBoard believes that it is not possible to provide de-finitive guidance that would address every circum-stance on how to determine the unit of account. Be-cause the individual facts and circumstances of a taxposition and of an enterprise taking that position willdetermine the appropriate unit of account, the Boarddoes not believe a single defined unit of accountwould be applicable to all situations.

B14. The Board decided to describe two factors thatshould affect the determination of the unit of account:the manner in which the enterprise prepares and sup-ports its income tax returns and the approach the en-terprise anticipates the taxing authority will take dur-ing an examination. Both factors would be expectedto vary with the facts and circumstances of a tax posi-tion and of the enterprise taking that position. In addi-tion, consistent with other presumptions in this Inter-pretation, the Board believes that the determinationof the unit of account should presume that taxing au-thorities will evaluate the position and have fullknowledge of all relevant information.

Benefit Recognition Approach

B15. A tax position could result in or affect themeasurement of a current or deferred tax asset or li-ability in the statement of financial position. Accord-ingly, the Board considered both a benefit recogni-tion approach, under which only a tax position thatmeets a stated confidence level would be recognizedin the financial statements, and an impairment ap-proach, which would require a determination of theamount of incremental income taxes that an enter-prise might have to pay. Under an impairment ap-proach, the as-filed tax position would be recognizedin the financial statements and a liability would berecognized when, at a stated confidence level, an in-cremental payment would be made to the taxingauthority.

B16. The Board decided that there is conceptualsupport for both a benefit recognition approach andan impairment approach. However, the Board de-cided that an impairment approach, which presumesthe existence of a benefit, would not be appropriatewhen an enterprise cannot conclude, to a specifiedconfidence level, that it is entitled to the economicbenefits of a tax position. Therefore, the Board de-cided to use the notion of a specified confidence levelas a precondition for recognition in a benefit recogni-tion approach.

FIN48 FASB Interpretations

FIN48–18

Examination Risk

B17. The Board considered whether uncertaintyabout the examination of a tax position by taxing au-thorities (examination risk) should be a factor in thedecision to recognize the effect of a tax position.

B18. Liabilities are required to be recognized whenthe obligating event has occurred. For current incometax liabilities, the obligating event is the generation oftaxable income. Generally, income tax systems arefounded on the principles of compliance, self-assessment, and self-reporting. That is, a taxpayercomputes its taxable income and related tax liabilityand reports that information to taxing authorities asrequired by law. The enforcement powers of the tax-ing authority are secondary to the self-assessmentand self-reporting requirements.

B19. Some Board members believe that basing theaccounting for tax positions on examination risk—the risk that a taxing authority would examine a par-ticular tax position—is analogous to reporting ac-counts payable based not on the amount owed but,rather, on the amount that would be ultimately paid ifthe creditor filed suit to collect the liability.

B20. The Board considered the guidance on unas-serted claims in paragraph 38 of Statement 5. TheBoard does not believe that guidance is applicable totax positions because a tax return is generally re-quired to be filed based on the provisions of tax law.Accordingly, the Board concluded that this Interpre-tation should presume that a tax position will beevaluated by taxing authorities.