Ninth Annual Domestic Tax Conference - EY - United States · Understanding the difference between...

46

Ninth Annual Domestic Tax Conference 8 May 2014 | Chicago

Transcript of Ninth Annual Domestic Tax Conference - EY - United States · Understanding the difference between...

Ninth AnnualDomestic Tax Conference8 May 2014 | Chicago

Enhancing and integratingtechnology throughout thetax life cycle

Page 3

IRS Circular 230 disclosure

Any US tax advice contained herein was not intended orwritten to be used, and cannot be used, for the purpose ofavoiding penalties that may be imposed under the InternalRevenue Code or applicable state or local tax lawprovisions.

These slides are for educational purposes only and are notintended, and should not be relied upon, as accountingadvice.

Page 4

► EY refers to the global organization, and may refer to one or more, of themember firms of Ernst & Young Global Limited, each of which is aseparate legal entity. Ernst & Young LLP is a client-serving member firmof Ernst & Young Global Limited located in the US.

► This presentation is © 2014 Ernst & Young LLP. All rights reserved. Nopart of this document may be reproduced, transmitted or otherwisedistributed in any form or by any means, electronic or mechanical,including by photocopying, facsimile transmission, recording, rekeying, orusing any information storage and retrieval system, without writtenpermission from Ernst & Young LLP. Any reproduction, transmission ordistribution of this form or any of the material herein is prohibited and is inviolation of US and international law. Ernst & Young LLP expresslydisclaims any liability in connection with use of this presentation or itscontents by any third party.

► Views expressed in this presentation are not necessarily those ofErnst & Young LLP.

Disclaimer

Page 5

Today’s presenters

Gary PaiceJeff York

Daren Campbell

Page 6

Agenda

► Introductions and overview► Enhancing and integrating technology along three

major axes:► Across the globe► Across the tax functions► At the transaction level

► Questions► Wrap-up

Page 7

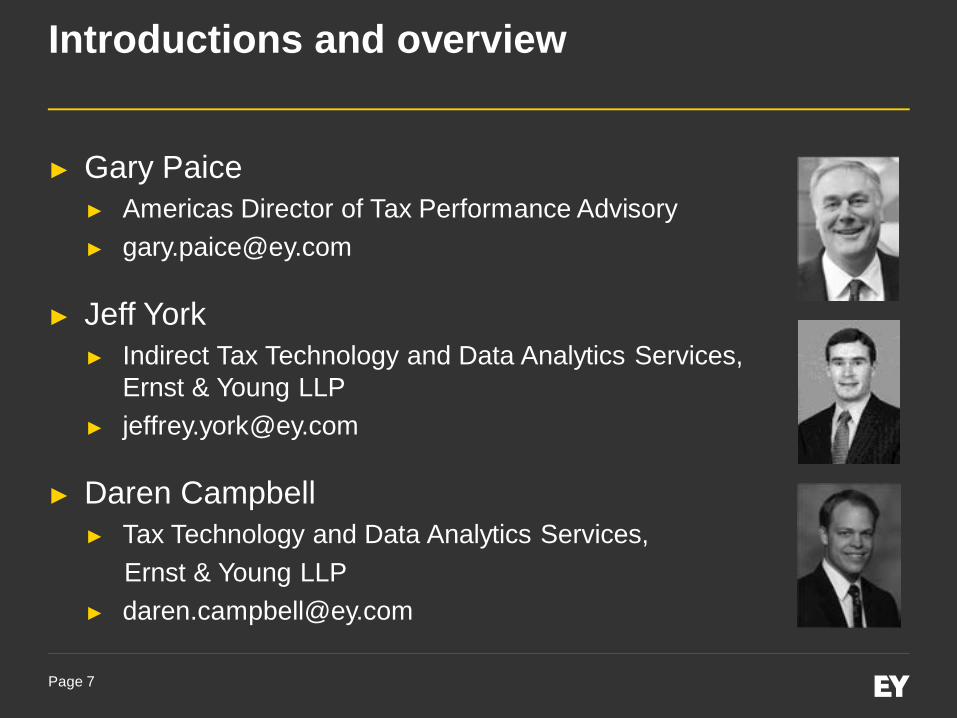

Introductions and overview

► Gary Paice► Americas Director of Tax Performance Advisory► [email protected]

► Jeff York► Indirect Tax Technology and Data Analytics Services,

Ernst & Young LLP► [email protected]

► Daren Campbell► Tax Technology and Data Analytics Services,

Ernst & Young LLP► [email protected]

Page 8

Across the globe

Page 9

Globalization

► Business drivers with globalization► Opportunities► Challenges

Page 10

Greater international exposure

► As the percentage of income and expenses outside of headquartersincreases and more elaborate tax planning is implemented:► The decentralized nature of non-US data becomes more problematic.► Budgeting and forecasting issues with data (not the tools) drive

uncertainty.► Complexity and timing of calculations create risk.

► The solution is to focus on areas that improve international reporting –organization, process and technology.► Why now: the trend is to continue to increase exposure.► The value is reducing risk and providing better planning.

► Example:► A company redesigned process/data so international calculations mostly

were known in the first two months of the close rather than in six months.Also, there was acceleration of statutory filings.

Page 11

Globalization: opportunities

► Improve the data► Continuing trend: further standardization of Enterprise Resource

Planning systems► Growing trend: consolidation tools and forecasting

► Tackle localization (where appropriate)► Indirect tax engines (ONESOURCE, Vertex) more capable► Life cycle moving away from decentralized rules and risk

management

► Prepare for processes independent of location► Begin thinking even more broadly about the life cycle

(e.g., statutory filings influences compliance filings)

Page 12

Improve the data

► Key elements of improving data► Getting to the root cause – determine whether it’s the data, the

process or the people► Building relationships, alliances and business case to improve –

tax doesn’t typically own the more important data► Understanding the difference between technology implementation

and data improvement; we have seen:► Old antiquated technology with very good data quality for Tax► Great, new technology with very poor data quality for Tax

► Recognizing that it is different throughout the life cycle► Reporting – balance level► Compliance – near-transaction► Audit – transaction

Page 13

Improve the data

► Litigation/regulatoryfines

► Financialrestatements

► Loss of efficiency/profitability

► Loss of stakeholderconfidence

Insufficiently definedreporting

requirements

► Ineffective/inefficientbusiness processes

► Poor business insights► Inaccurate financial

reporting► Suboptimal business

decisions► Manual and separate

reporting cycles

These typical issues ...► Poor data capture► Duplicate master

data► Incomplete data► Data

inconsistencies► Inaccurate source

data► Inappropriate data

usage

Insufficiently defined reporting requirements canhave significant and unfavorable businessimplications.

… lead to masterdata challenges …

… with seriousbusiness implications.

Page 14

Five fundamental questions to developreporting requirements

► Direct consumer► User entity► Business partner► Management/Board

of Directors► User service

organization► Regulator► Other

Who willuse the

reporting?

► Controls relevant tofinancial audits

► Profitability analysis► Availability► Processing integrity► Confidentiality► Regulatory/self-

regulatory► Contractual

compliance► Privacy

What is theuser’s

areas ofinterest?

► Meeting audit needs► Governance/risk

management► Vendor

management► Management reports► Regulatory

compliance► Contractual

compliance► Internal report –

managementconfidence

► Financial statementassertions

► Industry standards► Contractually

specified► Regulatory

requirements► Other

What criteriawill the report

measureagainst?

► Balance sheet,income statement

► Statutory andaudit report

► Product and marketanalysis

► Master data► Process validation► Security

What are thereport type

anddistribution

method?

What is theuser’s businesspurpose for the

reporting?

Tools and accelerators required for requirement gathering and mapping► Standard Reporting Matrix► Templates► Industry standards

Tools and accelerators required for requirement gathering and mapping► Standard Reporting Matrix► Templates► Industry standards

► Mapping accelerator► Workshops► Surveys

Page 15

Have you built a proactive strategy aroundimproving each of these areas?

The building blocks of a Tax-optimized SAP – the tax sensitization of ERP involves buildingtax requirements into the company’s business processes and practices.

Optimization of taxprocesses delivers valuesuch as:► Improved visibility into

intercompany transactionsand transfer pricing issuesunlocking and sustainingvalue

► Tax department needscaptured at right level withinsource systems (e.g., legalentity, jurisdiction)

► Improved accuracy andefficiency of tax reportingand planning throughworking closely with financeto "tax-sensitize" forecastingprocesses and systems

► Automated indirect taxdecision-making and end-to-end process through set-upof supplier/customer/productmaster data

Tax technology solutions (e.g., Onesource, Vertex)

Training/guidance for tax users

Tax accounting and reporting controls

Dat

afe

edM

aste

rda

taE

RP

conf

igur

atio

n

Procure to pay

Base ERPsystem Legacy systems

Middlewaresolutions

Third-partylogisticsT&E systems

Material master data

Supplier master data Customer master data

AP tax codes

Jurisdictionalsegregation

AP tax decisions

Transfer pricing AR tax codes

Segregation ofsales and returns

AR taxdetermination

Internationalsourcing

Critical tax sensitive accounts

Foreign jurisdictional indirecttax reports

GL account reports

Fixed assets master data

Order to cash Record to report

Tax depreciation rulesIntercompany and

jurisdictional reports

Tax fixed asset reports

Page 16

Tackle localization

► Indirect tax is becoming more important► Needs more controls and monitoring to avoid penalties

and surprises.► Few good tax engines covering non-US taxes► Common practice of SAP/Oracle customization

► What is different now► Evolution of indirect tax engines► Finance transformations putting past customizations into question

► Example: client made the following changes in technology► Year 1: put in tool and removed custom coding at ERP► Year 2: rolled out to US, Australia, Canada, Japan, Netherlands,

UK and Italy► Year 3: added Brazil, Russia and Mexico; added exemption

certificate manager

Page 17

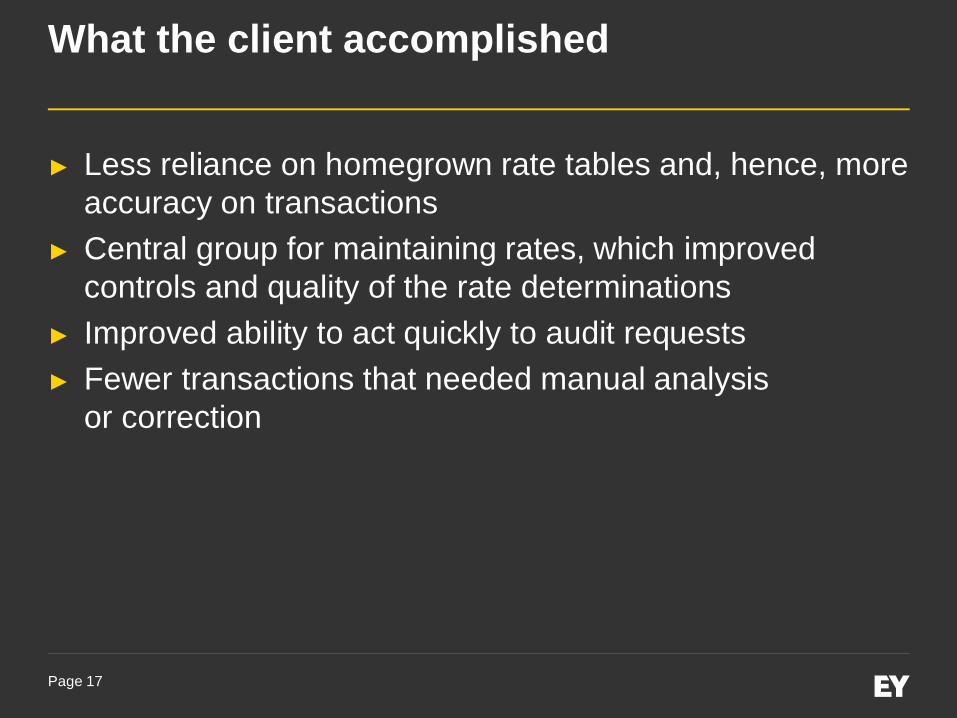

What the client accomplished

► Less reliance on homegrown rate tables and, hence, moreaccuracy on transactions

► Central group for maintaining rates, which improvedcontrols and quality of the rate determinations

► Improved ability to act quickly to audit requests► Fewer transactions that needed manual analysis

or correction

Page 18

Prepare for process independent of location

► Key elements of getting to location independence► Well-designed, well-documented processes and roles► Regular monitoring that establishes and improves quality► Technology that supports standardization

► Example situation: statutory filings► Prior approach: each local country doing its own thing while often

working with an outside third party► Location independent approach: standardize the most common

data preparation process in shared service center/center ofexcellence and third party doing non-standard

► Technology’s role:► Common platform for mapping financials and making adjustments► Online workflow for initiating and substantiating adjustments► Communication with third party

Page 19

Example of moving into different modelsleading to location independence

► Note: We try not to advocate for one approach or another, but thesimple truth is that many companies are employing multiple models allof which impact Tax.

Second generation:Delivering more valueto the business

First generation:Delivering less valueto the business

Global SSC/BPOCountry SSC Operations Regional SSC set-up

BPO

Regional SSC

Country SSC

Global SSC

Key:

Page 20

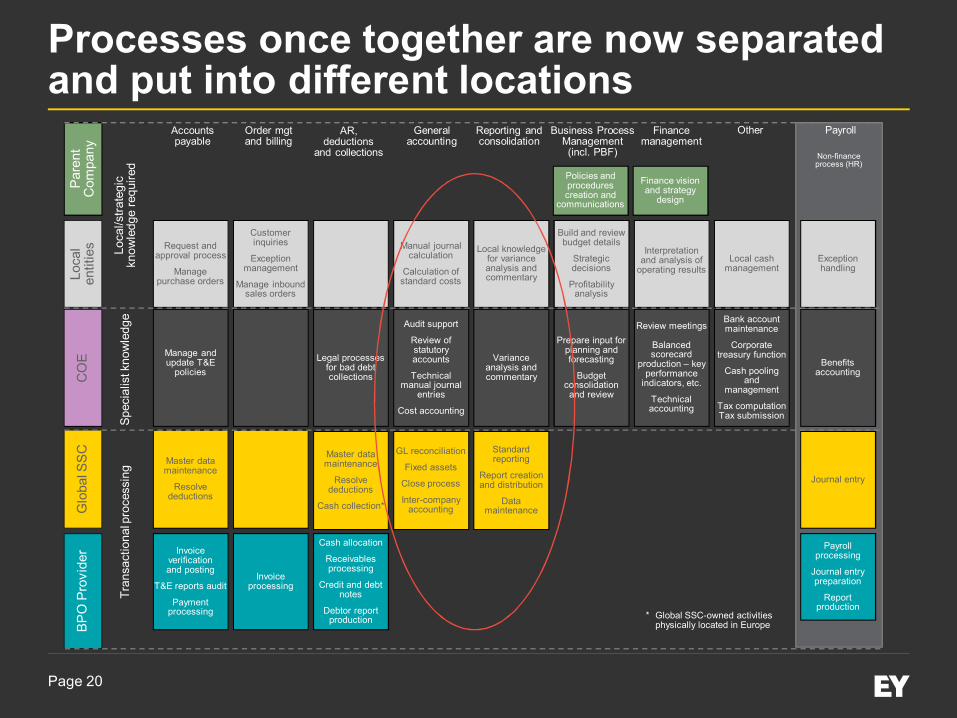

Processes once together are now separatedand put into different locations

Invoiceprocessing

Invoiceverificationand posting

T&E reports audit

Paymentprocessing

Standardreporting

Report creationand distribution

Datamaintenance

Master datamaintenance

Resolvedeductions

Cash collection*

GL reconciliation

Fixed assets

Close process

Inter-companyaccounting

Journal entry

Manage andupdate T&E

policiesLegal processes

for bad debtcollections

Audit support

Review ofstatutoryaccounts

Technicalmanual journal

entries

Cost accounting

Varianceanalysis andcommentary

Benefitsaccounting

Review meetings

Balancedscorecard

production – keyperformance

indicators, etc.

Technicalaccounting

Bank accountmaintenance

Corporatetreasury function

Cash poolingand

management

Tax computationTax submission

Request andapproval process

Managepurchase orders

Manual journalcalculation

Calculation ofstandard costs

Local knowledgefor varianceanalysis andcommentary

Exceptionhandling

Build and reviewbudget details

Strategicdecisions

Profitabilityanalysis

Interpretationand analysis of

operating resultsLocal cash

management

Loca

len

titie

sC

OE

Tran

sact

iona

lpro

cess

ing

Loca

l/stra

tegi

ckn

owle

dge

requ

ired

Spec

ialis

tkno

wle

dge

Glo

balS

SC

Non-financeprocess (HR)

Accountspayable

Generalaccounting

Financemanagement

OtherReporting andconsolidation

PayrollAR,deductions

and collections

Order mgtand billing

Policies andprocedurescreation and

communications

Customerinquiries

Exceptionmanagement

Manage inboundsales orders

BP

OP

rovi

der

Prepare input forplanning andforecasting

Budgetconsolidationand review

Finance visionand strategy

design

Par

ent

Com

pany

Cash allocation

Receivablesprocessing

Credit and debtnotes

Debtor reportproduction

Master datamaintenance

Resolvedeductions

Payrollprocessing

Journal entrypreparation

Reportproduction

* Global SSC-owned activitiesphysically located in Europe

Business ProcessManagement(incl. PBF)

Page 21

Technology combined to create a processacross groups and locations

Loca

len

titie

sC

OE

Glo

balS

SC

BP

OP

rovi

der

Flexible ledger software

Web workflow

Content management

Country A

Country B

Country C

Page 22

Life cycle broader than in the past

► Statutory filing example► Overlaps on related activities – e.g., mapping to chart of accounts,

starting point for local tax return► Implications on timing

► Filing requirements often after other life cycle dates(e.g., US Federal return)

► Companies establishing accelerated internal dates to improveoverall timing

Page 23

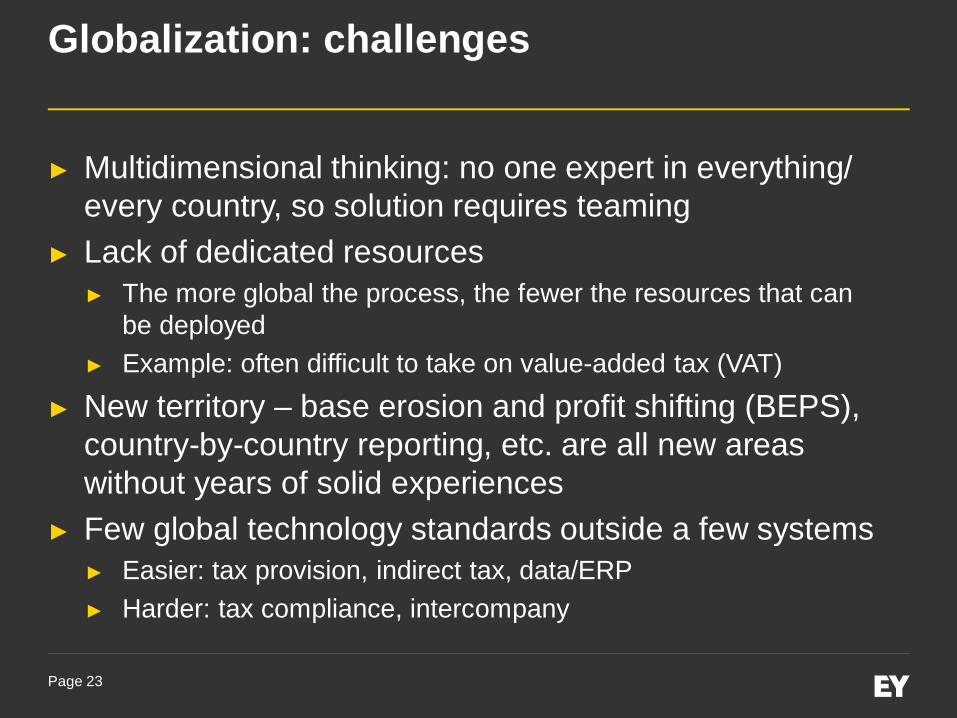

Globalization: challenges

► Multidimensional thinking: no one expert in everything/every country, so solution requires teaming

► Lack of dedicated resources► The more global the process, the fewer the resources that can

be deployed► Example: often difficult to take on value-added tax (VAT)

► New territory – base erosion and profit shifting (BEPS),country-by-country reporting, etc. are all new areaswithout years of solid experiences

► Few global technology standards outside a few systems► Easier: tax provision, indirect tax, data/ERP► Harder: tax compliance, intercompany

Page 24

Bottom line on globalization

► Except for a few leading practice companies, fewclients are proactively thinking about global processesand technology

► Why? Because it requires:► Different thinking and approach► Resources who are willing to think creatively about the process► Applying technology in ways that are not necessarily “out of

the box”

► At the same time, thinking and managing globally will beone of the defining elements of the new tax professional

Page 25

Across the tax functions

Page 26

Co-presenter/panelist

Jeffrey York► National Tax – Indirect Tax Technology

and Data Analytics Services,Ernst & Young LLP

Page 27

Functional teaming

► The need for functional teaming► Challenges► Opportunities

Page 28

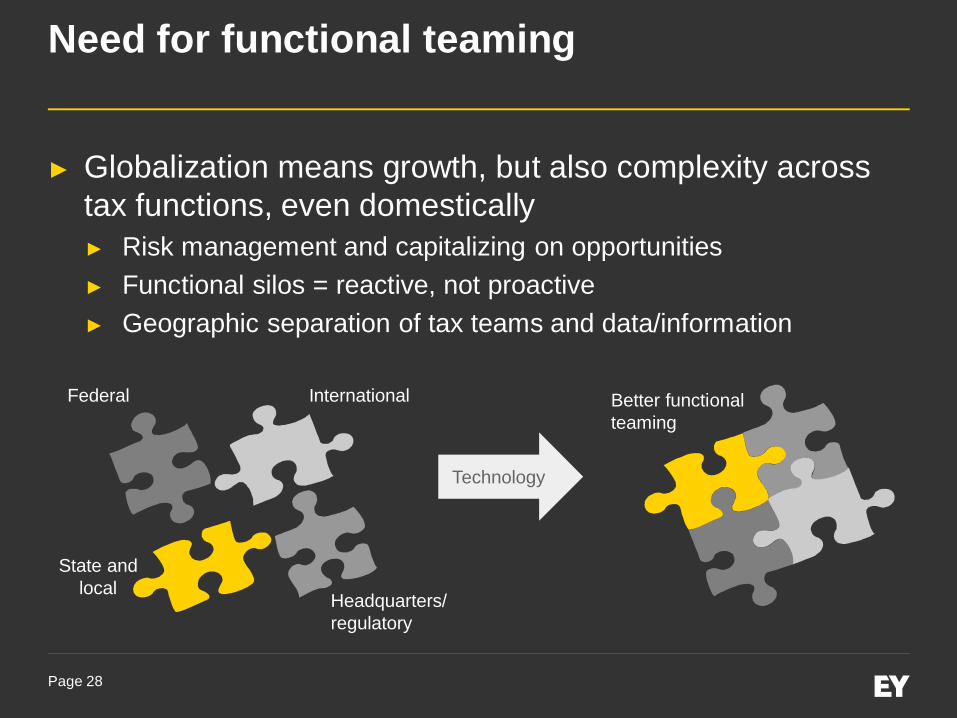

Need for functional teaming

► Globalization means growth, but also complexity acrosstax functions, even domestically► Risk management and capitalizing on opportunities► Functional silos = reactive, not proactive► Geographic separation of tax teams and data/information

Federal

State andlocal

International

Headquarters/regulatory

Technology

Better functionalteaming

Page 29

Need for functional teaming

► Even without globalization, US domestic tax departmentscan be more proactive throughout the tax life cycle► Improved communications and data/information sharing► Multifaceted risks and opportunities► Like global tax teams, domestic tax teams and data/information

spread across domestic geographies

Functional teaming

Page 30

Functional teaming: challenges

► Empowering multidimensional thinking► Breaking down “silos”► Determining whether teaming creates additional work

► Letting technology work for you

► Technology systems not connected or interrelated► Examples: ERP, HR, payroll, fixed assets, real estate► Potential technology solutions

► Data warehousing► Workflow management► Collaboration tools

Page 31

Functional teaming: opportunities

► Improve flow of data and information► Communication► Addressing tax life cycle needs at one time

► Cross-functional awareness► Proactive, cross-functional planning and modeling

► Early identification► Work to avoid surprises

Page 32

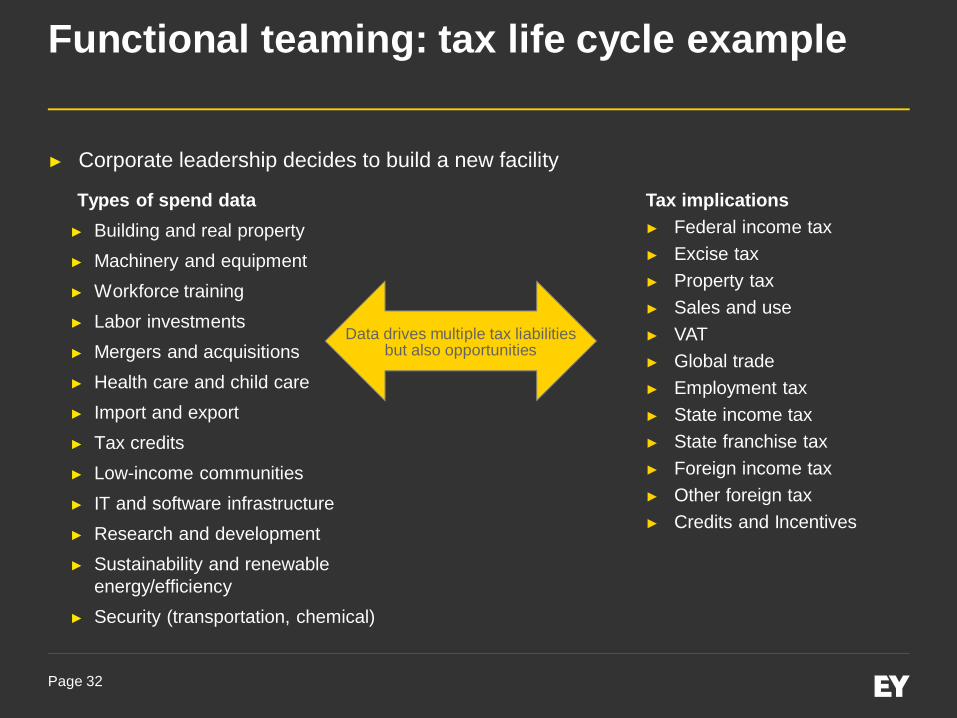

► Corporate leadership decides to build a new facility

Functional teaming: tax life cycle example

Types of spend data► Building and real property► Machinery and equipment► Workforce training► Labor investments► Mergers and acquisitions► Health care and child care► Import and export► Tax credits► Low-income communities► IT and software infrastructure► Research and development► Sustainability and renewable

energy/efficiency► Security (transportation, chemical)

Tax implications► Federal income tax► Excise tax► Property tax► Sales and use► VAT► Global trade► Employment tax► State income tax► State franchise tax► Foreign income tax► Other foreign tax► Credits and Incentives

Data drives multiple tax liabilitiesbut also opportunities

Page 33

Functional teaming: tax life cycle example

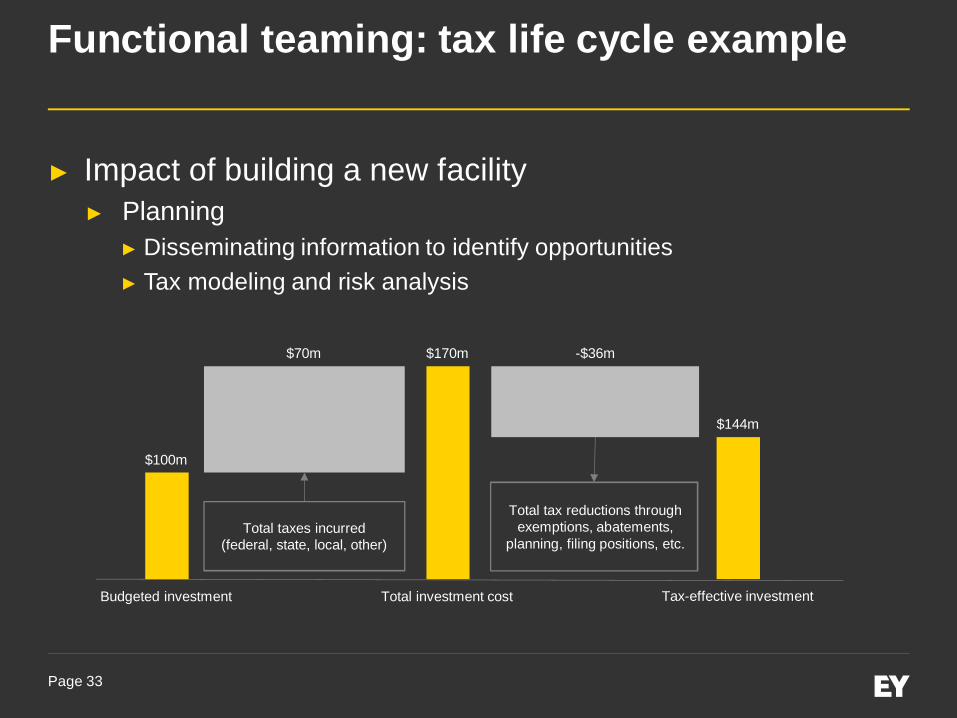

► Impact of building a new facility► Planning

► Disseminating information to identify opportunities► Tax modeling and risk analysis

$100m

$170m

$144m

$70m -$36m

Budgeted investment Total investment cost Tax-effective investment

Total taxes incurred(federal, state, local, other)

Total tax reductions throughexemptions, abatements,

planning, filing positions, etc.

Page 34

Functional teaming: tax life cycle example

► Impact of building a new facility► Accounting

► Tax provision impacts► Compliance

► New filings► Estimated payments► Credits and net operating losses

► Controversy► Create and store required support in advance of audits

Page 35

At the transaction level

Page 36

Co-presenter/panelist

Daren Campbell► Tax Technology and Data

Analytics Services, Ernst & Young LLP

Page 37

Transaction detail

► Business drivers for transactional detail► Challenges► Opportunities

Page 38

Why does tax need to think abouttransactional-level detail?

► Rapidly changing and expanding federal, state and localtax laws and increasing volumes of data have pressuredtax departments like never before. The following fourchanges in the business landscape are driving the need toutilize transactional-level detail:► Globalization of companies► Functional teaming► Tax authority sophistication► Requirements of new regulations

Page 39

Key challenges tax departments face inutilizing transactional data

► Tax has not had access to key processes and systems.► Tax has limited resources and increasing responsibilities.► Tax does not have resources trained in the transactional

systems.

Page 40

Options for utilizing transactional-level detailfor tax determinations

Taxsensitizebusiness

processes

Gatherinformationin a tax datawarehouse

Page 41

Tax sensitizing business process

Benefits► Leveraging non-tax resources► Minimal manipulation required

on received data► Early notification of events

affecting tax

Challenges► Buy-in► Training and education of

non-tax resources

Page 42

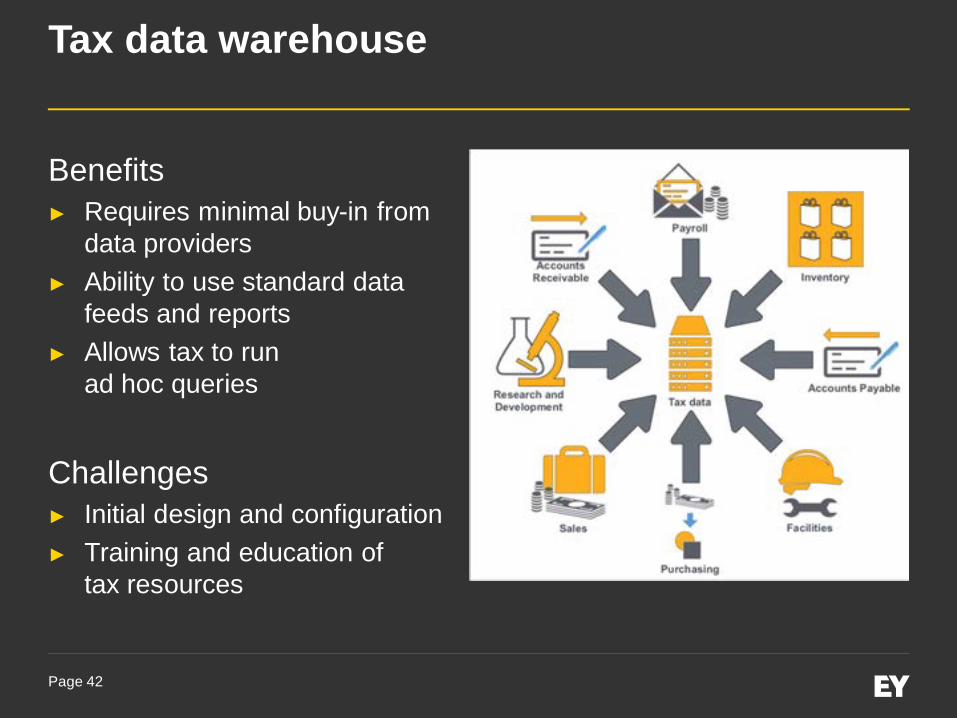

Tax data warehouse

Benefits► Requires minimal buy-in from

data providers► Ability to use standard data

feeds and reports► Allows tax to run

ad hoc queries

Challenges► Initial design and configuration► Training and education of

tax resources

Page 43

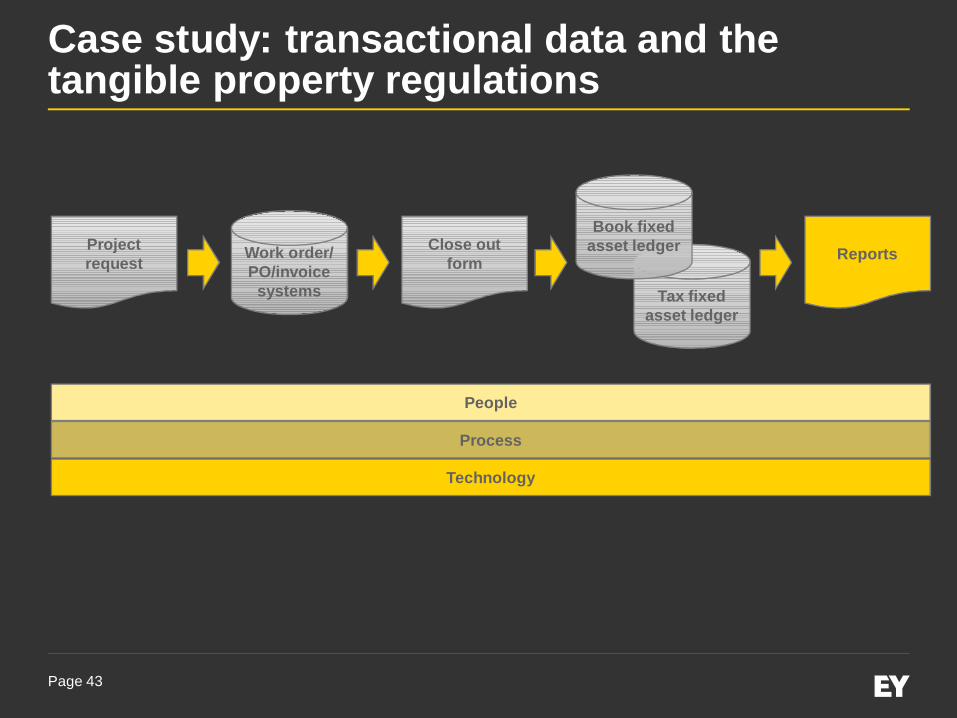

Case study: transactional data and thetangible property regulations

Projectrequest Work order/

PO/invoicesystems Tax fixed

asset ledger

Close outform

Book fixedasset ledger Reports

People

Process

Technology

Page 44

Utilizing transactional-level detail improvesaccuracy and efficiency

► Interpretations are made by people understandingthe transactions.

► Near-time decisions can be made as triggering eventsoccur.

► Tax can readily respond to audit requests with appropriatesupporting detail.

► Tax resources can focus on applying the law instead ofcollecting information.

Enhancing and integrating technology throughout the tax life cyclePage 45

Thankyou!

Ninth AnnualDomestic Tax Conference8 May 2014 | Chicago