Nick Downing, Sales Director, iGD March 6th -...

61

Transcript of Nick Downing, Sales Director, iGD March 6th -...

© IGD 2012

IGD – Consumer Goods Experts

• Insight and training, with a total supply chain perspective– Retail, supply chain, shoppers, category management, in‐store excellence

– Focus on food and grocery retailing

– Online services, customised projects, training

• Focus on primary research, local store visits– Unique relationships with leading retailers and suppliers

• Internationally connected– Central role in ECR Europe, a member of the Consumer Goods Forum

• A team of 100+ with practical industry experience

“IGD gave us the confidence that we had the best insights on food retailing in Europe. Retail Analysis proved to be a very valuable tool, saving us time and money and helped us in developing the best store concept for the customer.”

Nico Meyer, Format Director, Albert Heijn

© IGD 2012

Some of our 700+ members

© IGD 2012

Sources of this presentation

• ShopperVista www.shoppervista.igd.com

• Retail Analysis www.retailanalysis.igd.com

• IGD conferences www.igd.com/conferences

© IGD 2012

Agenda

• The online grocery shopper

• Case studies – Tesco and others

• Online grocery in context

• Opportunities for suppliers

• The future

© IGD 2012

© IGD 2012Images: Waitrose.com, Supermercadoelcorteingles.es, Genghisgrill.com, Mydish.co.uk, Asda.com/symtv

How are retailers engaging with shoppers digitally?

© IGD 2012Source: IGD Research

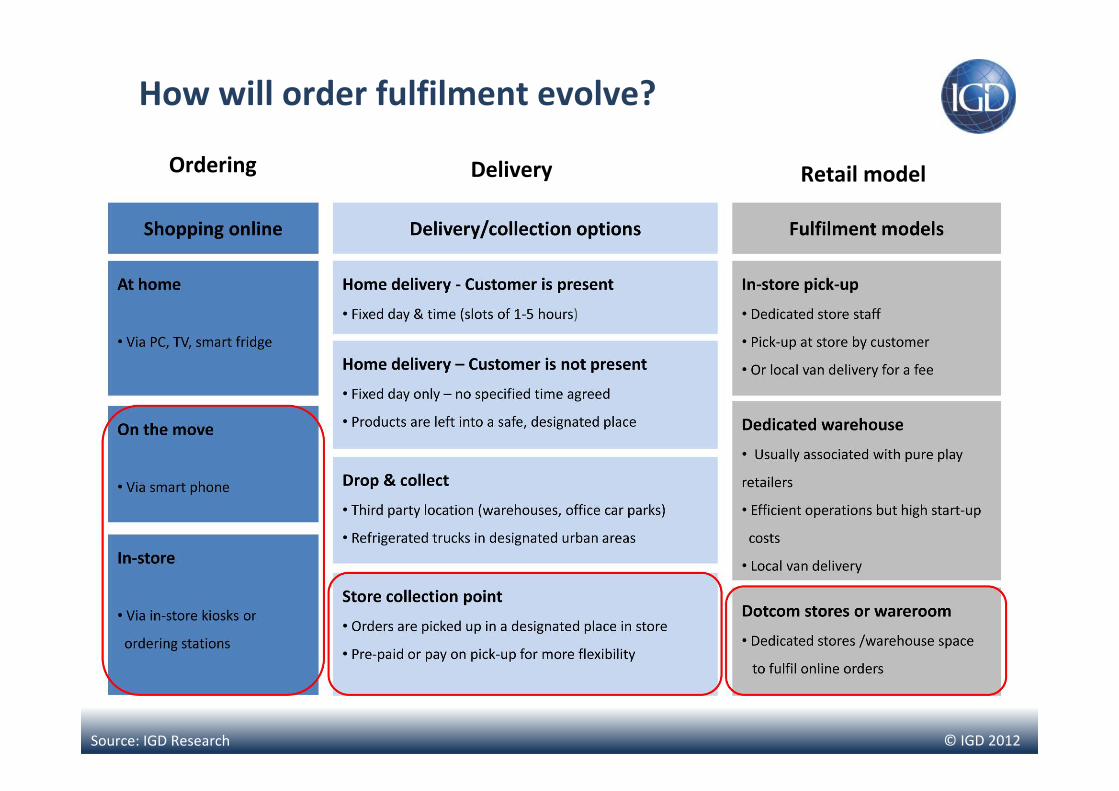

How will order fulfilment evolve?

Ordering Delivery Retail model

© IGD 2012

The development of apps in grocery retailing

Images: Ah.nl, Coopathome.ch, Supermercadoelcorteingles.es, Ocado.com

© IGD 2012Source: Office for National Statistics, 2011 base: All UK adults accessing the internet in last three months

Frequency of using internet

Boxes denote significant differences between years

Method of internet access away from home/work

Frequency and method of online access is changing

© IGD 2012

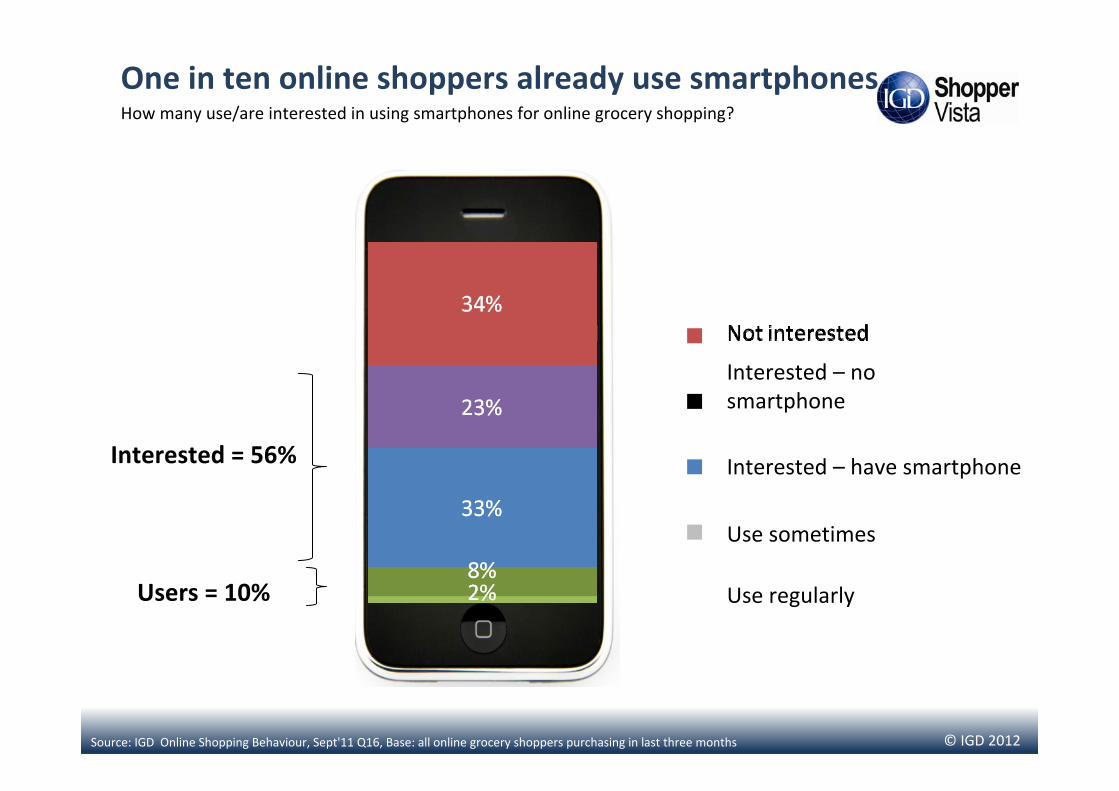

One in ten online shoppers already use smartphones

Source: IGD Online Shopping Behaviour, Sept'11 Q16, Base: all online grocery shoppers purchasing in last three months

Users = 10%

Interested = 56%

Interested – no smartphone

Interested – have smartphone

Use sometimes

Use regularly

How many use/are interested in using smartphones for online grocery shopping?

© IGD 2012

Ocado : 18% of orders placed by mobile in 2011

Source: Ocado

18%

“Mobile first”

© IGD 2012Source: IGD ShopperTrack, March‐May 2011.

Arrows denote significant differences between groups

Online grocery shopping appeals to young families

© IGD 2012

Variations by category

Other toiletries

Ambient slimming products

Bathroom toiletries

Haircare

Frozen poultry and game

Take home soft drinks

Household and cleaning products

Savoury carbohydrates and snacks

Packet breakfast

Savoury home cooking

Top 10 online Bottom 10 online

*Index = Share of total online sales/ share of total in‐store sales Source: TNS, 52 week ending 4th October 2009

Take home confectionery

Chilled bakery products

Ambient bakery products

Alcohol

Fresh fish

Fresh meat

Chilled convenience

Fruit, vegetables and salad

Hot beverages

Dairy products

© IGD 2012

Category insight from Sainsbury’s

Source : cat growth FYTD P1‐10 proportion of sales week 44, Sainsbury’s trade briefing

Online is a big proportion of some categories overall sales

Baby9.9%

FrozenMeat8.4%

Inspire to Cook7.2%

Still Drinks8.2%

Detergents8.3%

© IGD 2012

Online shoppers are quite promiscuous

• Two in three (64%) use multiple online retailers

• Furthermore, 47% of online shoppers say they intend to, or would like to, try another online retailer

Source: IGD Online Shopping Behaviour Sept’11

More promiscuous than anticipated?

© IGD 2012Source: IGD Online Shopping Behaviour, Sept'11 Q14, Base: all online grocery shoppers purchasing in last three months

More in‐store = 57%More online = 17%

Do online shoppers impulse purchase more online or in‐store?

Online shoppers are less impulsive when online

© IGD 2012

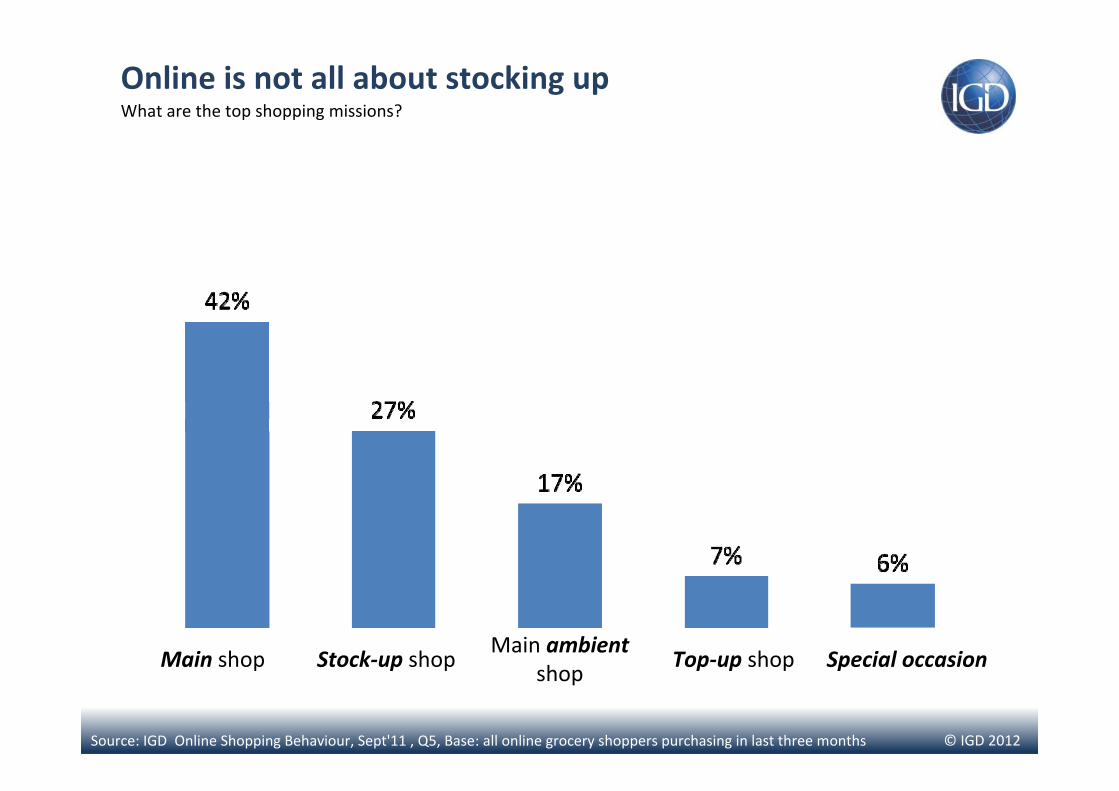

Online is not all about stocking up

Source: IGD Online Shopping Behaviour, Sept'11 , Q5, Base: all online grocery shoppers purchasing in last three months

What are the top shopping missions?

Main shop Stock‐up shopMain ambient

shopTop‐up shop Special occasion

© IGD 2012

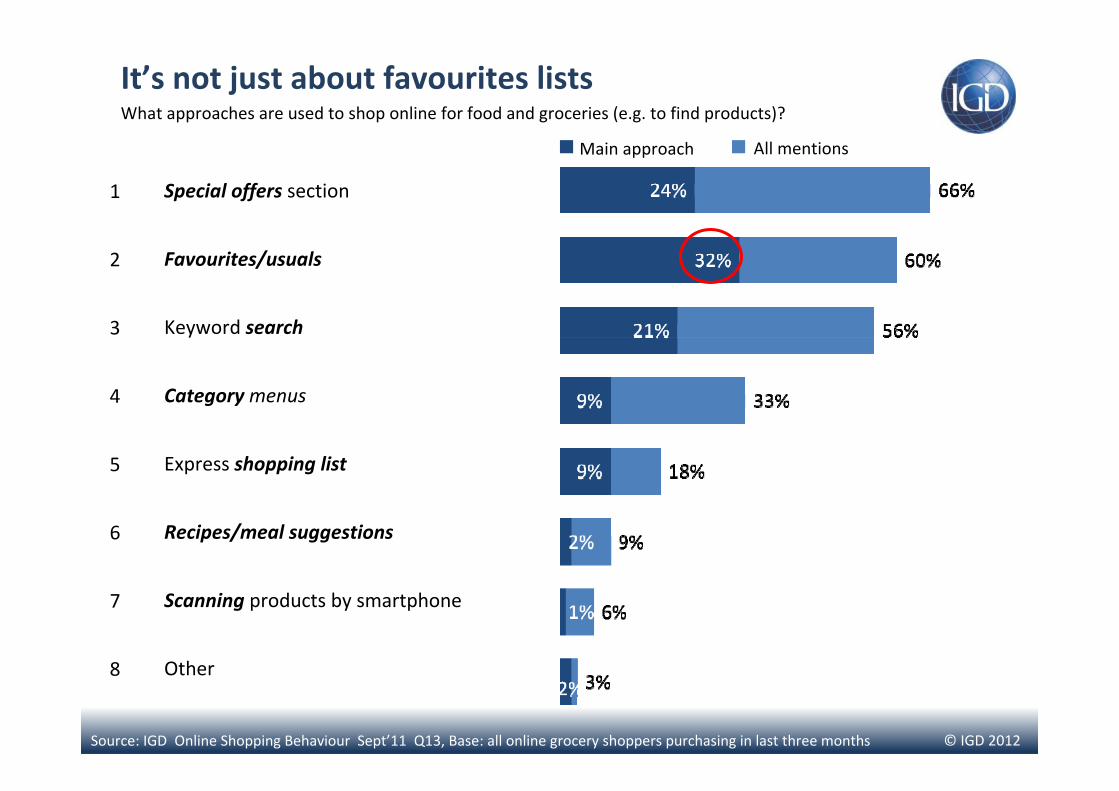

It’s not just about favourites lists

All mentions

Source: IGD Online Shopping Behaviour Sept’11 Q13, Base: all online grocery shoppers purchasing in last three months

1 Special offers section

2 Favourites/usuals

3 Keyword search

4 Categorymenus

5 Express shopping list

6 Recipes/meal suggestions

7 Scanning products by smartphone

8 Other

Main approach

What approaches are used to shop online for food and groceries (e.g. to find products)?

© IGD 2012

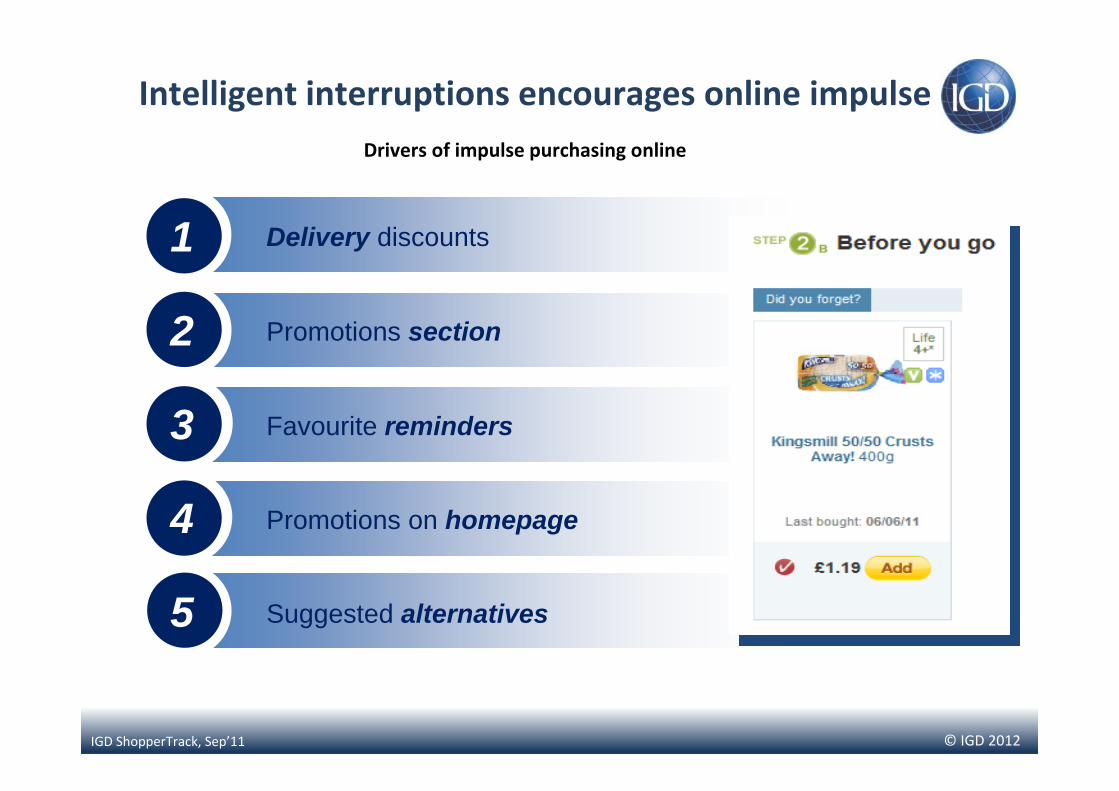

Delivery discounts

Promotions section

Favourite reminders

Promotions on homepage

Suggested alternatives

IGD ShopperTrack, Sep’11

1

2

3

4

5

Drivers of impulse purchasing online

Intelligent interruptions encourages online impulse

© IGD 2012

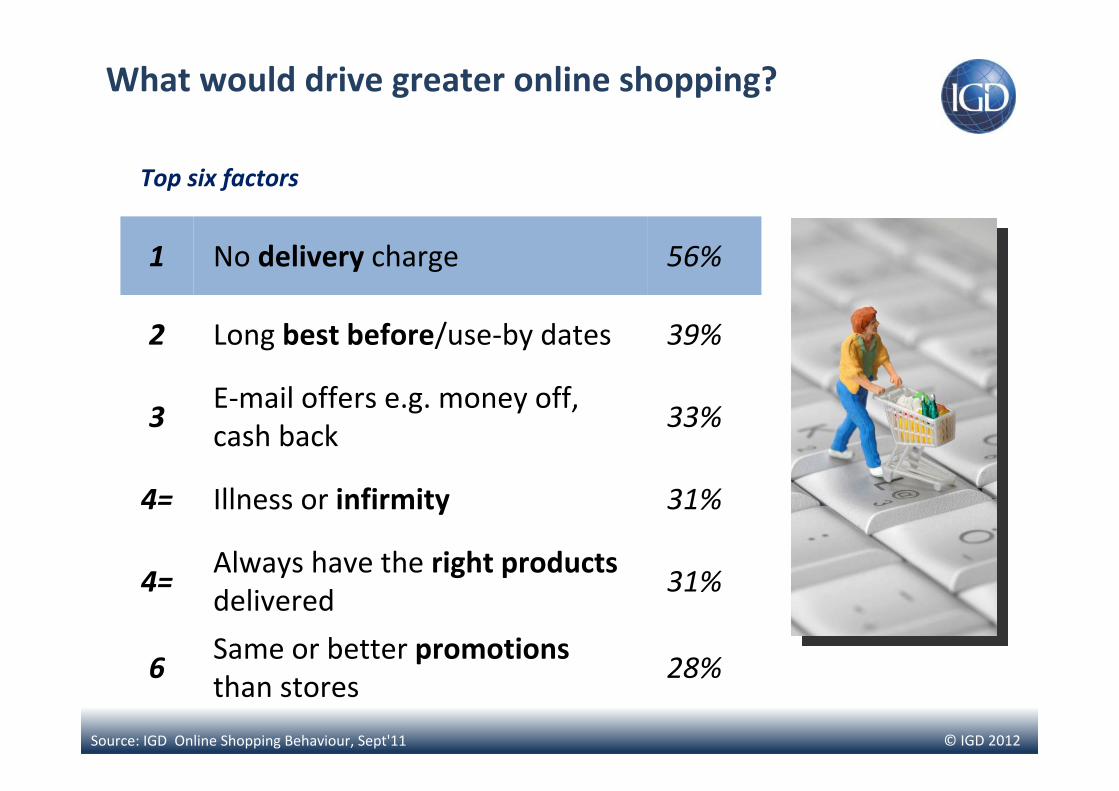

What would drive greater online shopping?

Source: IGD Online Shopping Behaviour, Sept'11

Top six factors

1 No delivery charge 56%

2 Long best before/use‐by dates 39%

3E‐mail offers e.g. money off, cash back

33%

4= Illness or infirmity 31%

4=Always have the right products delivered

31%

6Same or better promotionsthan stores

28%

© IGD 2012

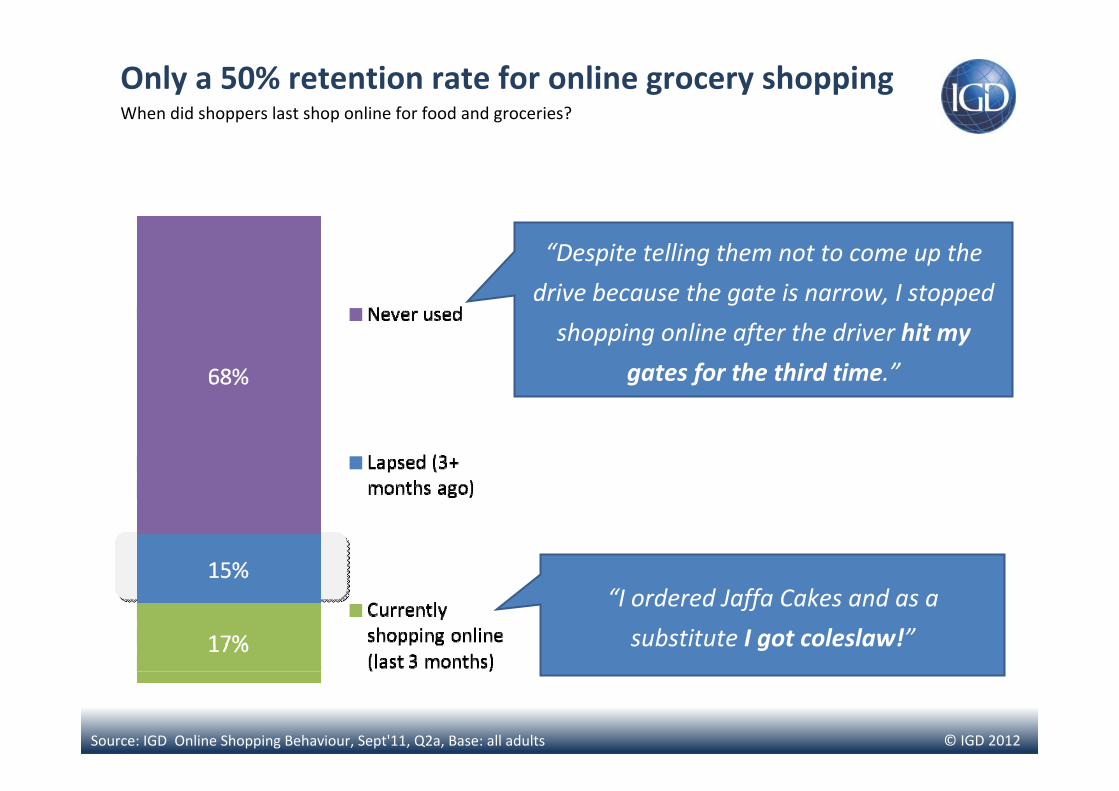

Only a 50% retention rate for online grocery shopping

Source: IGD Online Shopping Behaviour, Sept'11, Q2a, Base: all adults

When did shoppers last shop online for food and groceries?

“Despite telling them not to come up the

drive because the gate is narrow, I stopped

shopping online after the driver hit my

gates for the third time.”

“I ordered Jaffa Cakes and as a

substitute I got coleslaw!”

© IGD 2012

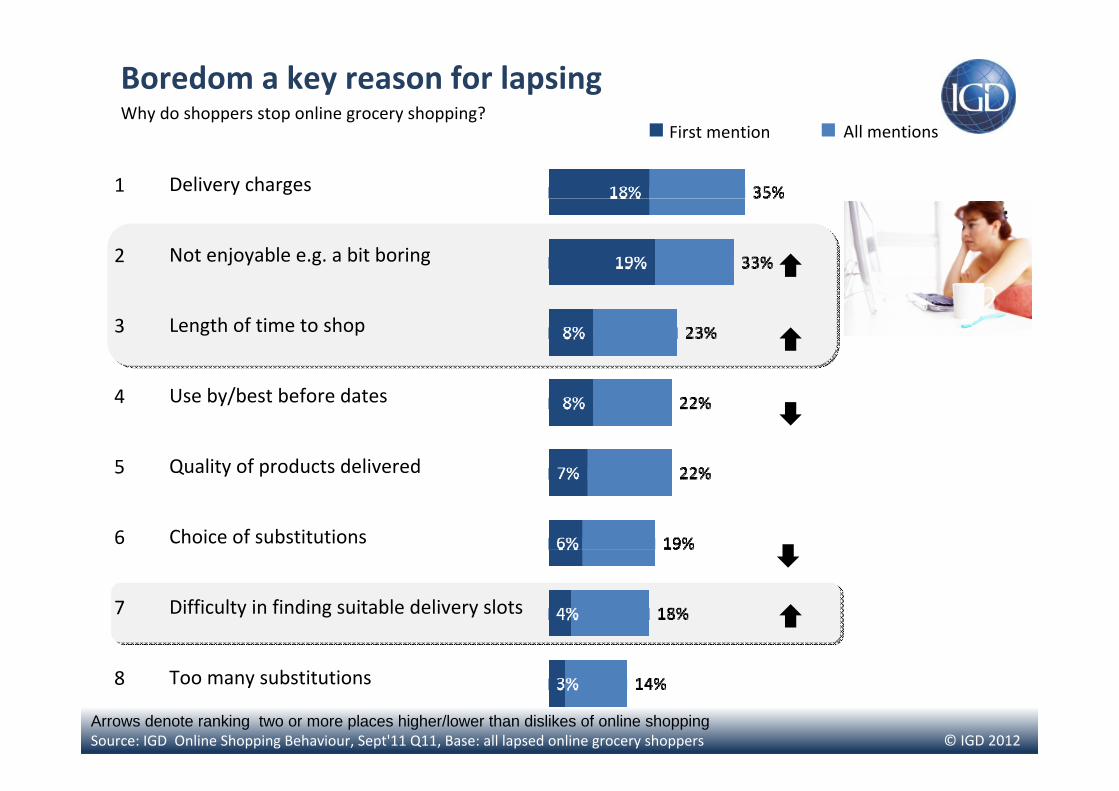

Boredom a key reason for lapsingAll mentions

Source: IGD Online Shopping Behaviour, Sept'11 Q11, Base: all lapsed online grocery shoppers

1 Delivery charges

2 Not enjoyable e.g. a bit boring

3 Length of time to shop

4 Use by/best before dates

5 Quality of products delivered

6 Choice of substitutions

7 Difficulty in finding suitable delivery slots

8 Too many substitutions

First mention

Arrows denote ranking two or more places higher/lower than dislikes of online shopping

Why do shoppers stop online grocery shopping?

© IGD 2012

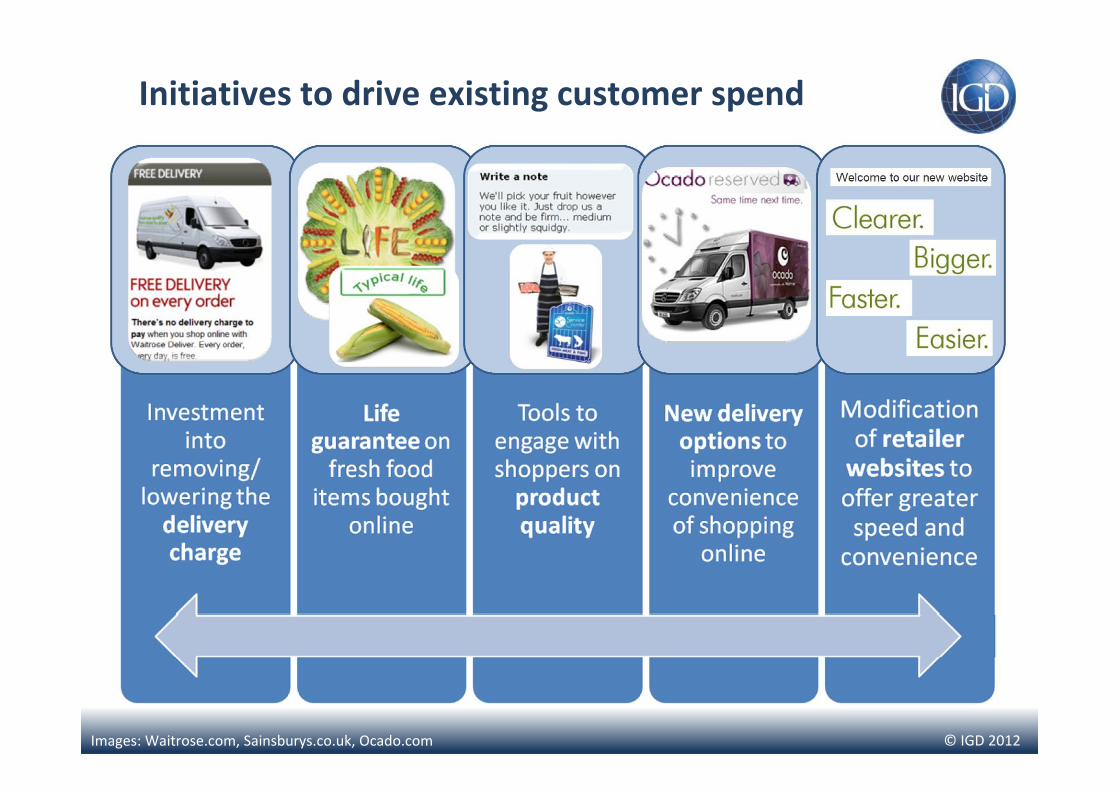

Initiatives to drive existing customer spend

Images: Waitrose.com, Sainsburys.co.uk, Ocado.com

© IGD 2012

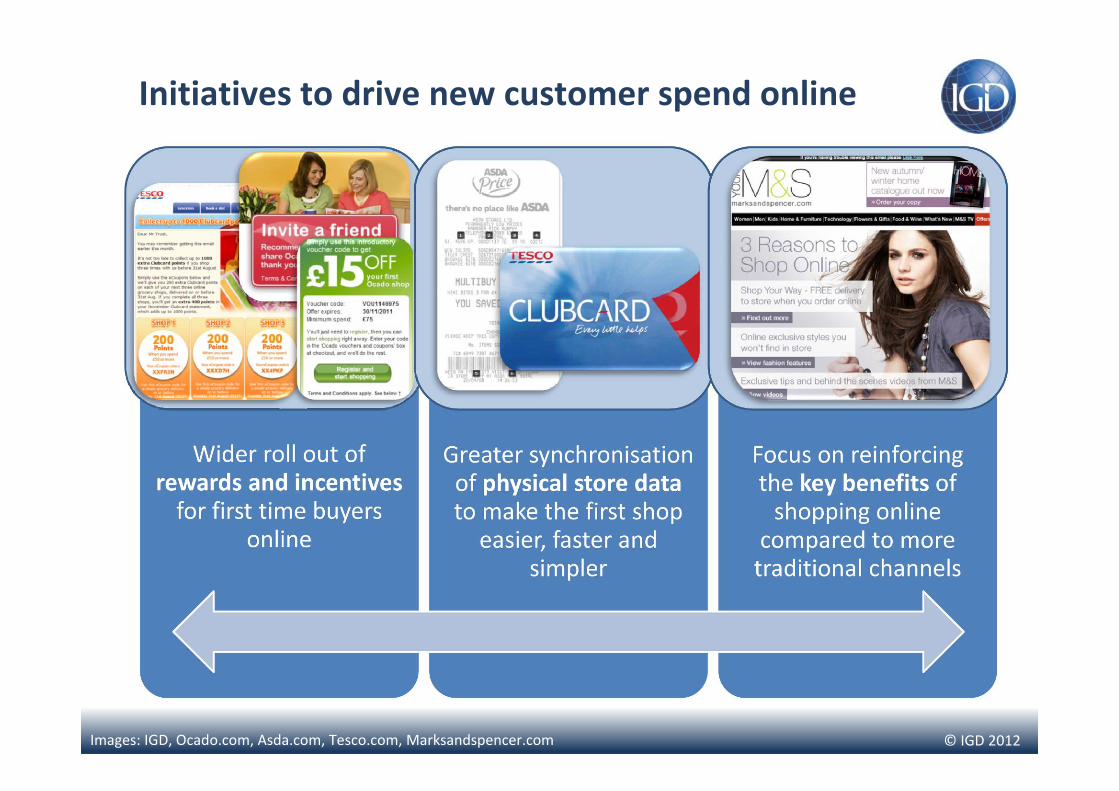

Initiatives to drive new customer spend online

Images: IGD, Ocado.com, Asda.com, Tesco.com, Marksandspencer.com

© IGD 2012

© IGD 2012

Tesco’s strategy is to extend the brand into new channels and new areas

Growth of online sales in 2011, taking into account both grocery and Tesco Direct, in all markets

Contribution of iPhone grocery app to customer traffic to the tesco.com website

Growth of Tesco direct sales including clothing in the UK

15%

12%

30%

Source: IGD Research, Tesco, 2012

© IGD 2012

Online strategy development – time line

Source: IGD Research, Tesco, 2012

© IGD 2012

Online store in the Czech republic

• Tesco recently launched its online store in Prague to extend its consumer reach, marking the retailer's first online presence in Central Europe and the only retailer to offer such a service in the market.

• The online store allows Czech customers to browse and purchase more than 20,000 lines of food and groceries, as well as non‐food items such as toys and accessories.

• Tesco is working towards becoming a dominant multi‐channel retailer in the international market through an online platform that can be used in multiple countries.

• Three of the supermarket's Prague stores ‐ Zličínský, Letňany and Rock, will service online orders initially, though an expansion of the service is planned.

Source: IGD Research, Tesco

© IGD 2012

Developments in Asia showing the way.......

Source: IGD Research, Cheil Worldwide, cnngo

•Tesco opened a virtual store in the subway in Seoul, South Korea

•The concept featured over 500 popular products, complete with QR codes which can be scanned using the Homeplus app

•Products range from daily essentials such as milk and fresh produce, to pet foods

•Orders placed before 13:00 will be delivered to home the same day•A three month trial store

© IGD 2012

Appealing to the multi‐channel shopper

Apply a joined‐up approach across offline and online ranging and merchandising to support retailers as they promote access to an online catalogue of products in‐store.

Customers at Tesco Extra Dudley, UK, can use interactive kiosks to browse 40,000 non‐food lines and order for next day delivery.

The area is staffed at all times and additional pods are positioned around the store.

© IGD 2012

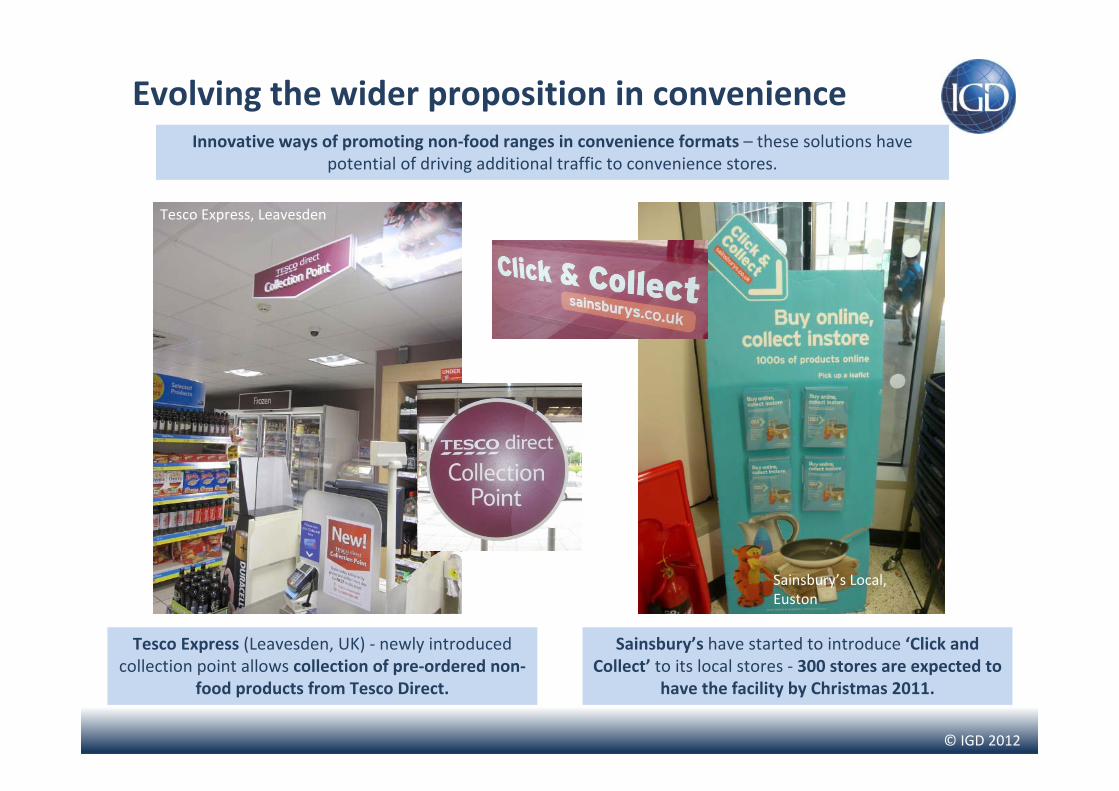

Evolving the wider proposition in convenienceInnovative ways of promoting non‐food ranges in convenience formats – these solutions have

potential of driving additional traffic to convenience stores.

Tesco Express (Leavesden, UK) ‐ newly introduced collection point allows collection of pre‐ordered non‐

food products from Tesco Direct.

Sainsbury’s have started to introduce ‘Click and Collect’ to its local stores ‐ 300 stores are expected to

have the facility by Christmas 2011.

Sainsbury’s Local, Euston

Tesco Express, Leavesden

© IGD 2012

Order processing for the online channel

• Initial strategy: – To pick orders from stores, not the distribution network

• This strategy has evolved, and now:– In UK, Tesco operates dedicated “dark stores” in areas of high demand

– These are laid out and replenished as stores with products on shelves, but only service on‐line orders.

– There are currently three such dark stores operating, with one more nearing completion and another one planned

Source: IGD Research, 2012

© IGD 2012

Dark stores: anticipated to contribute to 15% of online turnover by 2014

Source: IGD Research, 2012; www.maps.google.com

Dark store 1 Croydon

Dark store 2 Aylesford

Dark store 3 Greenford

Dark store 5 Crawley

Dark store 4 Enfield

© IGD 2012

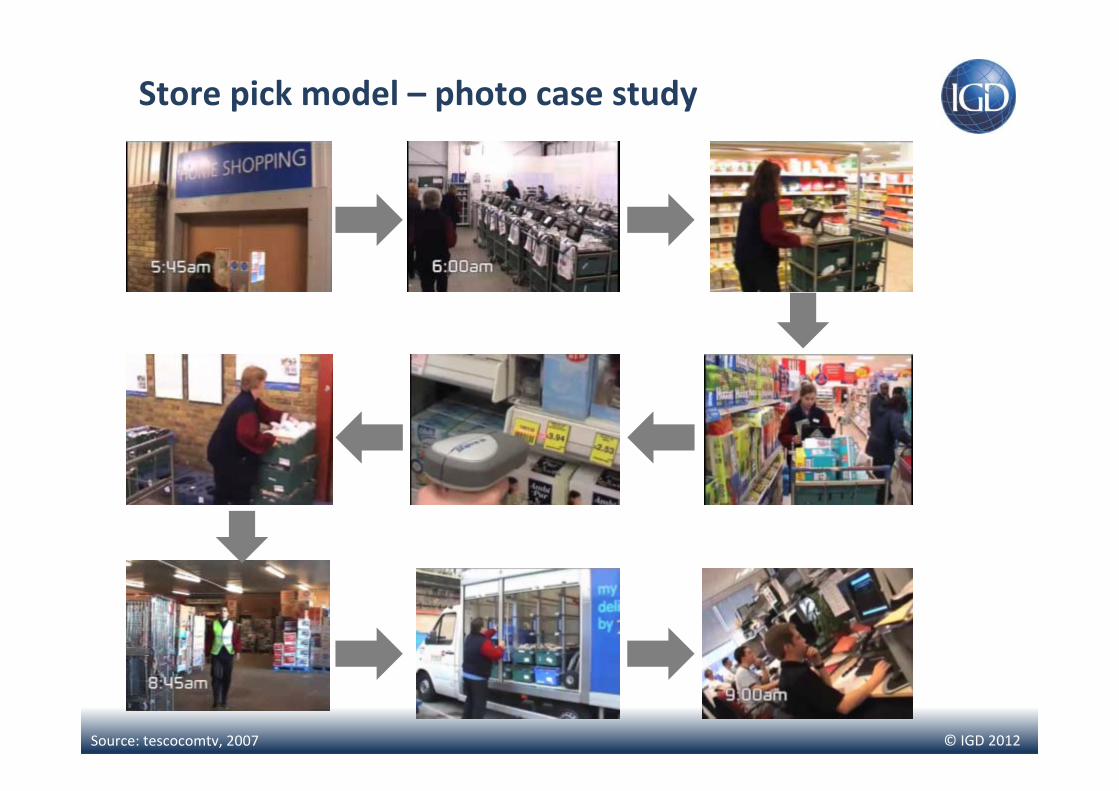

Store pick model – photo case study

Source: tescocomtv, 2007

© IGD 2012

How do “dark stores” operate?

Products stocked in the same way as a regular store, except that 'customers' are replaced by order picking staff. Staff pick from shelving into order crates; up to six customers orders can be picked simultaneously, spread across van routes.

Source: IGD Research, Vanderlande Industries, 2012

Orders are brought to a manually loaded line, which takes the crates to a consolidation buffer mounted on a platform. This buffer consists of a three‐aisle Quickstore Highly Dynamic System (HDS) Automated Storage and Retrieval System.

Order crates are spread throughout the consolidation buffer and held until a predefined release time of complete delivery van loads.

When empty vans are assigned and directed to a loading bay, the driver will indicate the van's presence to the to initiate release of all ambient orders destined for that van. On exit from the DCOS site, the van is scanned and that load is deleted from the system.

© IGD 2012

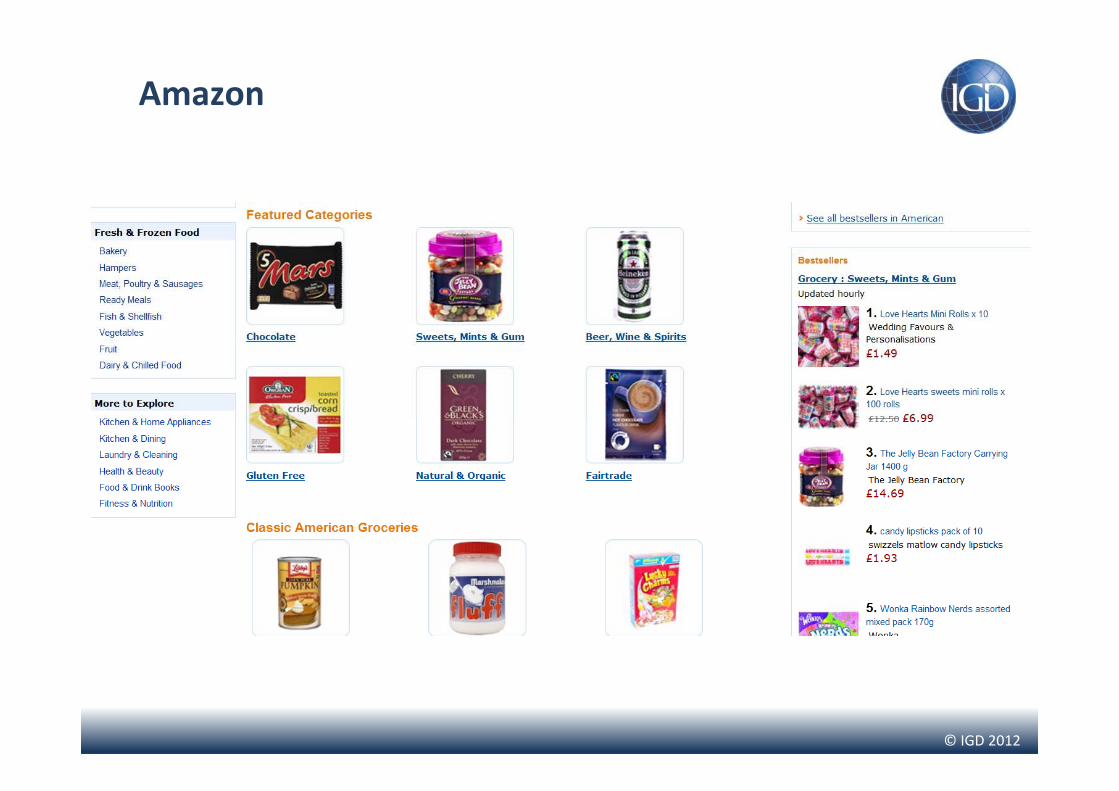

Amazon

© IGD 2012

Amazon’s online grocery business

Source: IGD Research Images: Amazon.co.uk

Global sales of $34.2bn in 2010, up 40% on the previous year

4 = Number of countries where Amazon has built a consumables business to date

22,000 = Number of grocery SKUs sold at launch in the UK

One of the fastest growing online food retailers in the USA

Key developments

Focus on dry grocery, but experimenting with fresh / chilled

Strong coverage of specialist and niche products

Branded lines sold in bulk packs

Focus on brands, not private label

© IGD 2012

‘Click & Collect’ – France driving the model

Source: IGD Research

Saves timeFill basket when chooseLess tempting

Who’s leading the way?

Systeme U = 334 sitesCasino = Over 100 sitesLeclerc = 100 sites

Auchan/ChronoDrive = 80 sites ITM = 25 sites

Carrefour = 20 sites Cora = 4 sites

© IGD 2012

Other ‘innovators’ internationally

E‐grocer Based Why ‘Ten to watch’

NL Award winning smartphone app and a first for the Dutch market. Functionality also in place to build a basket which includes items from Albert Heijn’s three separate web portals

FR Continues to adapt and develop its drive‐through concept in France and beyond. Also one of the few retailers which has a dedicated online marketing strategy in place

FR Leading e‐commerce operator in France, with learnings for many on how to integrate a non‐food and food online service. Also offers online pick‐up across certain Petit Casino c‐stores

SP Focus on engaging and building a dialogue with shoppers around food. Functionality also in place to build your own food menu which is based on your personal food preferences

US Example of how fresh food can work in an online environment. Pure play grocer which operates out of a state‐of‐the‐art site facility which includes onsite production

JP Concept born out of Japan’s rapidly growing and diversifying e‐commerce market. Specialises in out of season grocery products at discounted prices. Part of the Nissen Group

SZ Another pure play operator which pioneered online retailing in the Swiss market. Strategic sourcing agreement in place with Migros, leading supermarket operator in Switzerland

US Leading online grocer which operates out of a series of specially designed spaces in existing supermarkets (known internally as ‘warerooms’)

JP Portal which provides selling space to small, medium and large size food and non‐food merchants, trading in Japan, Taiwan, Thailand and now China

US One of the fastest growing businesses in US e‐tailing at the current time, with ambitious growth plans for its international operations going forward. Now selling groceries in the US

Source: IGD Research

© IGD 2012

© IGD 2012

Online grocery retailing in the UK, 2010‐2016

6%

% of total grocery market by 2016

© IGD 2012

UK grocery, sales by format (€bn), 2011‐2016

€188bn €221bn

© IGD 2012

UK retailers, sales by format, 2012 (f)

£46bn £24bn £19bn£23bn Total UK sales

© IGD 2012

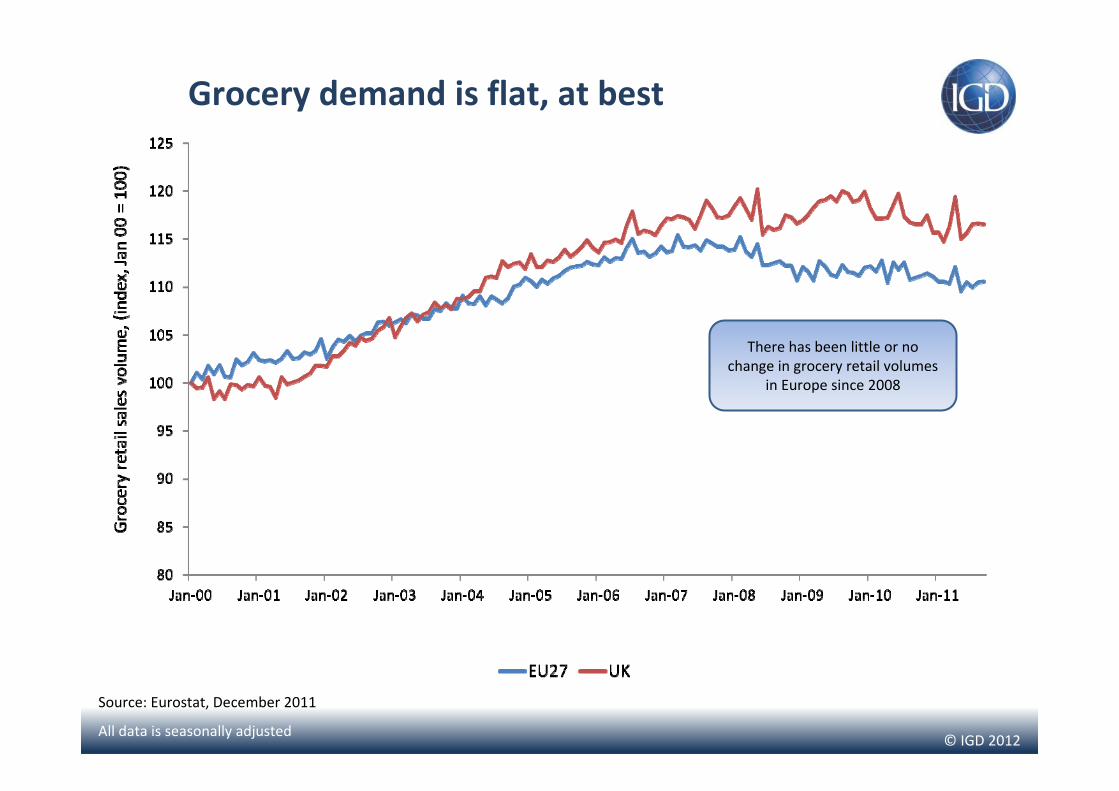

Grocery demand is flat, at best

Source: Eurostat, December 2011

All data is seasonally adjusted

There has been little or no change in grocery retail volumes

in Europe since 2008

© IGD 2012

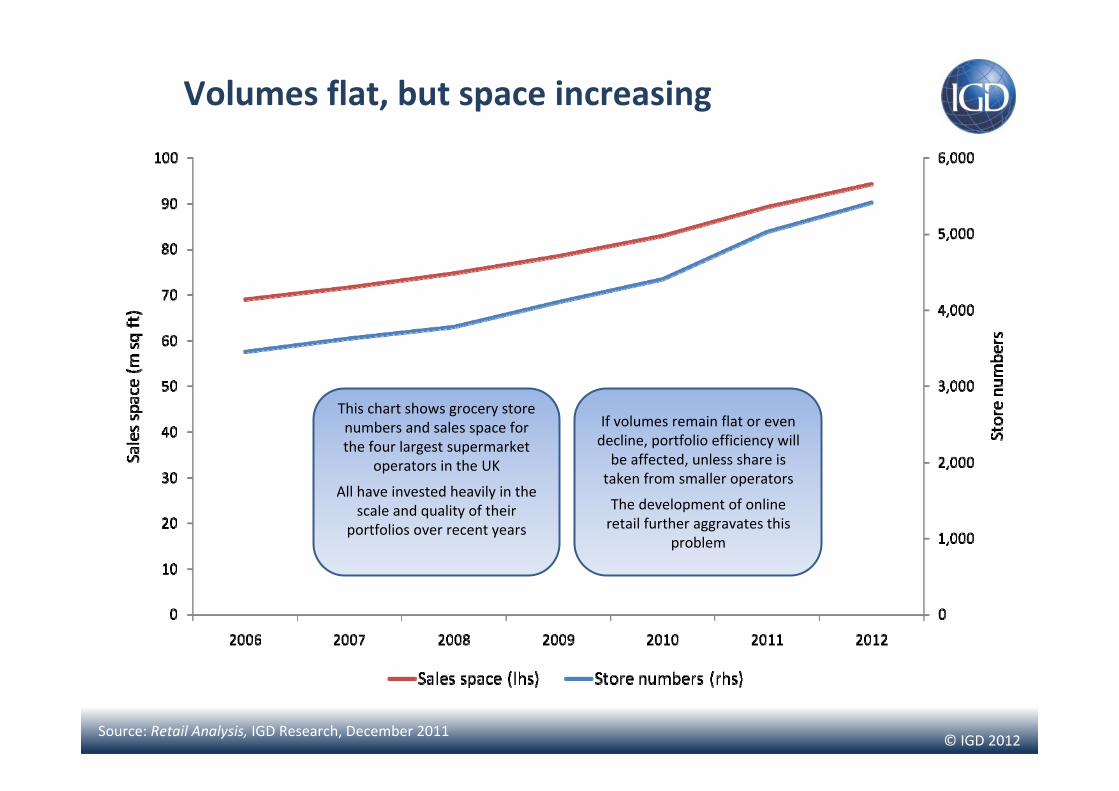

Volumes flat, but space increasing

Source: Retail Analysis, IGD Research, December 2011

This chart shows grocery store numbers and sales space for the four largest supermarket

operators in the UK

All have invested heavily in the scale and quality of their

portfolios over recent years

If volumes remain flat or even decline, portfolio efficiency will be affected, unless share is taken from smaller operators

The development of online retail further aggravates this

problem

© IGD 2011

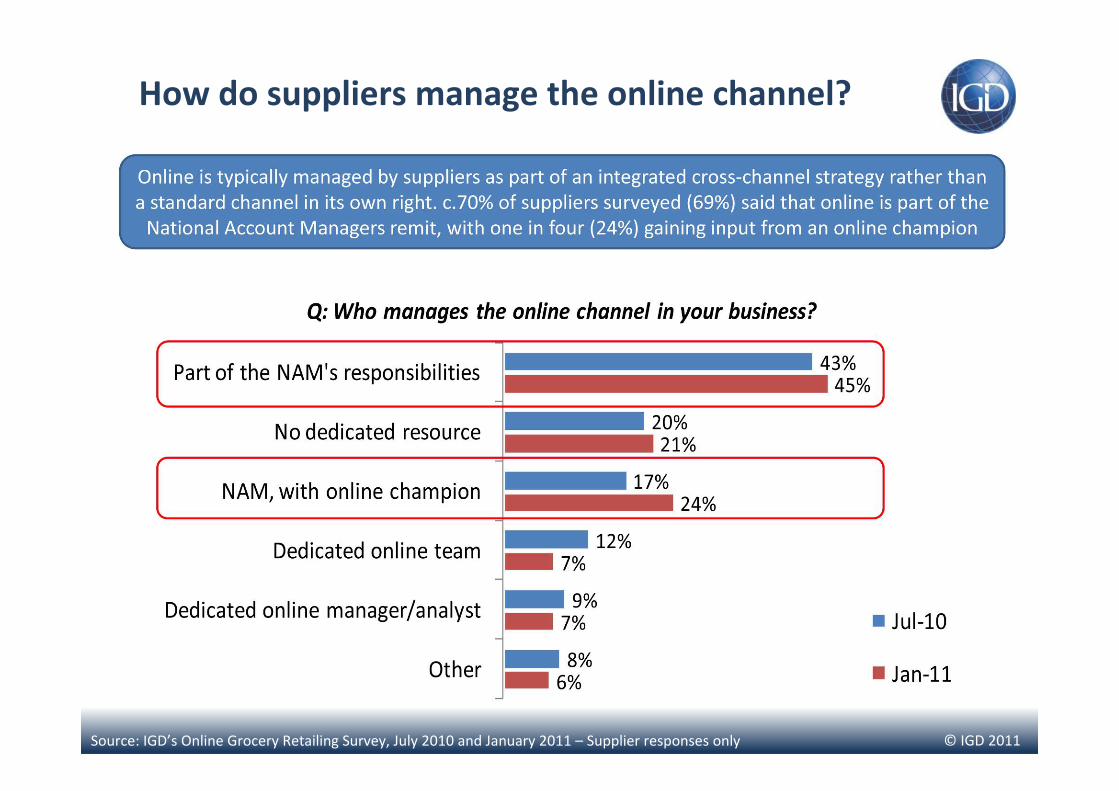

© IGD 2011Source: IGD’s Online Grocery Retailing Survey, July 2010 and January 2011 – Supplier responses only

How do suppliers manage the online channel?

© IGD 2011

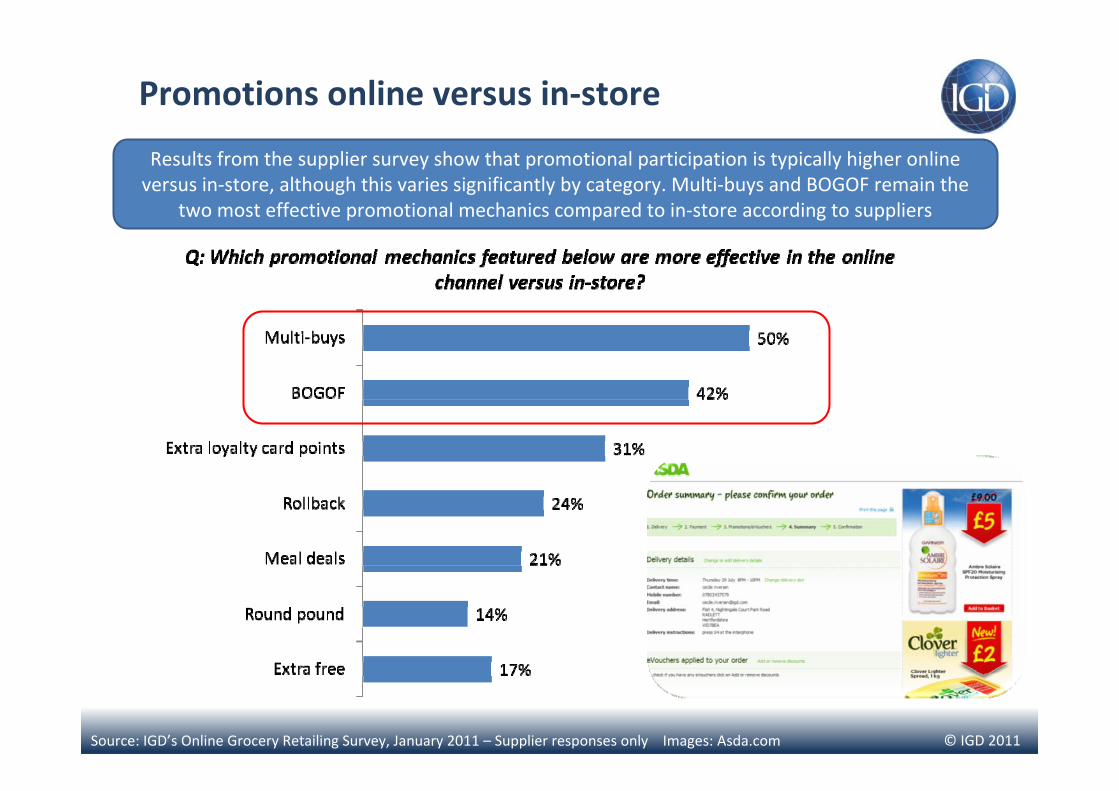

Promotions online versus in‐store

Results from the supplier survey show that promotional participation is typically higher online versus in‐store, although this varies significantly by category. Multi‐buys and BOGOF remain the

two most effective promotional mechanics compared to in‐store according to suppliers

Source: IGD’s Online Grocery Retailing Survey, January 2011 – Supplier responses only Images: Asda.com

© IGD 2011

Ways to promote your brand online

Source: IGD’s Online Grocery Retailing Survey, January 2011 – Supplier responses only Images: Tesco.com

© IGD 2011

Pack sizes and packaging

Images: Walmart.com, Amazon.com

© IGD 2012

Digital revolution removing the ‘middle man’

"The digital revolution that has turbo‐charged globalisation is transforming how consumers and companies behave. This revolution is boosting competition, lowering prices, creating

new virtual companies, allowing people to sell goods to each other without a middle man.”

Philip Clarke, CEO, Tesco

© IGD 2011

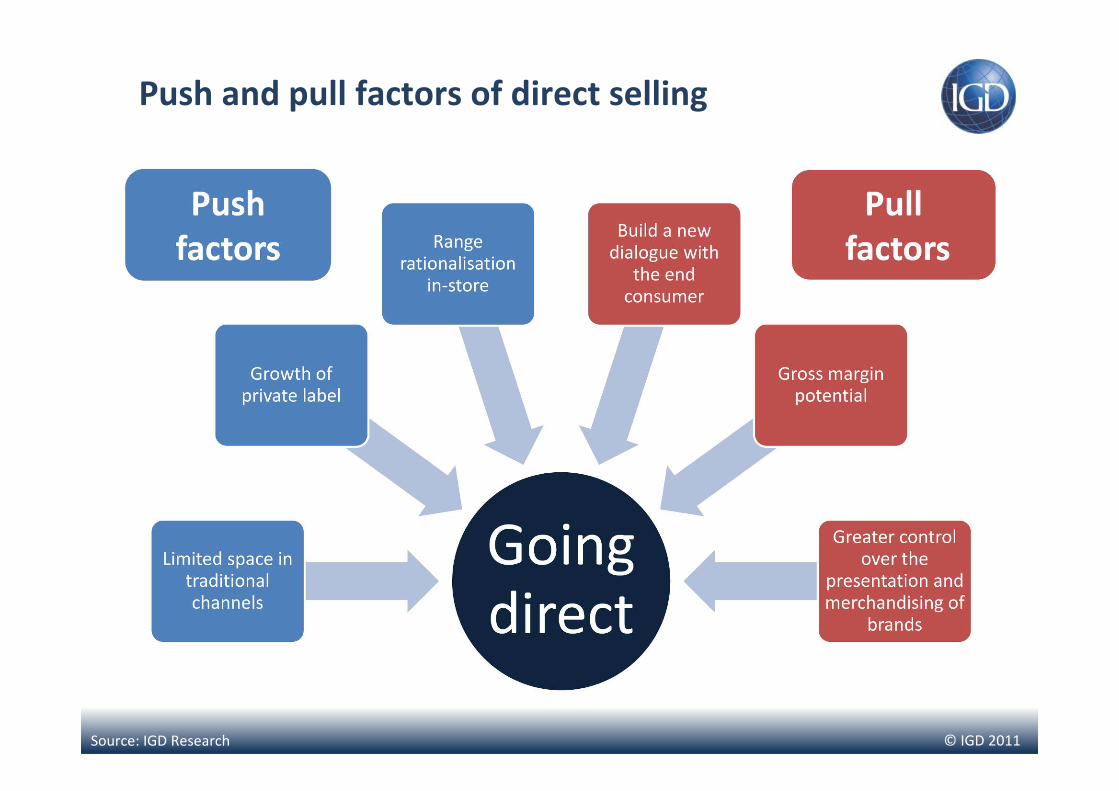

Push and pull factors of direct selling

Source: IGD Research

© IGD 2011

Challenges of trading online

Although suppliers highlighted a number of different challenges associated with trading online, responses to the survey were heavily skewed towards issues relating to data availability and the

level of internal focus within their business

Source: IGD’s Online Grocery Retailing Survey, January 2011 – Supplier responses only

Data considerations

Internal focus

© IGD 2011

Direct selling: The P&G eStore

Images: Pgestore.com

© IGD 2012

© IGD 2012

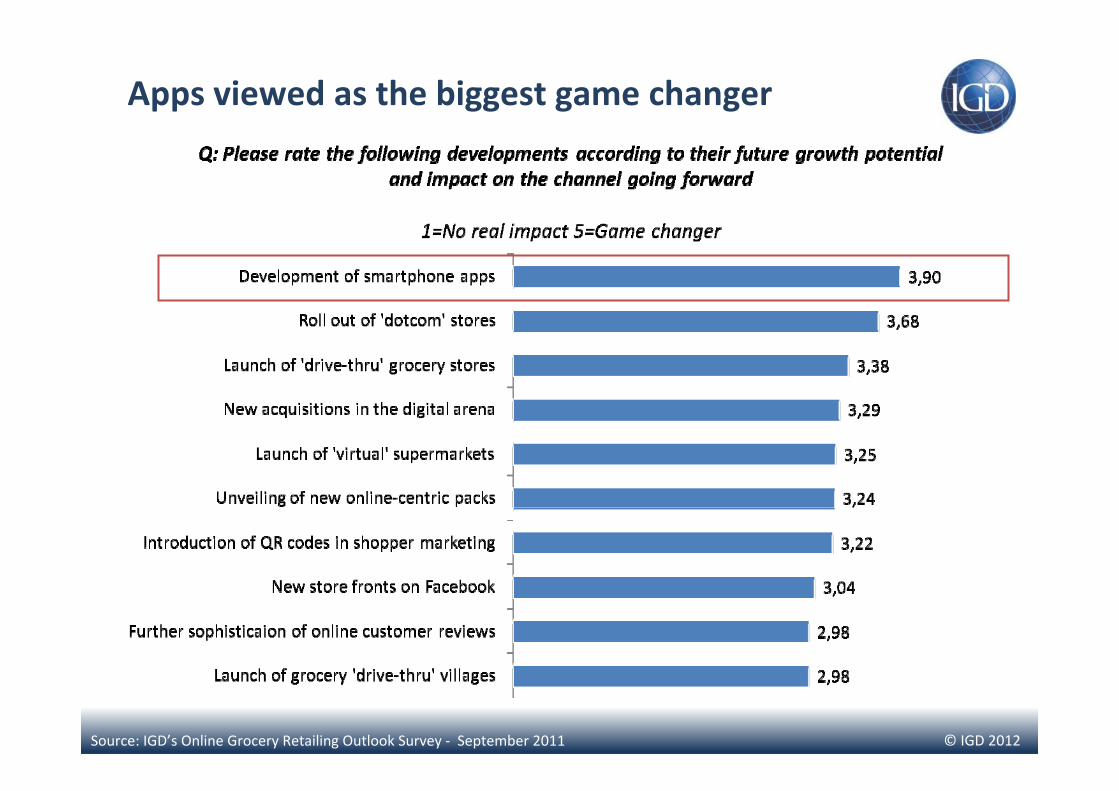

Apps viewed as the biggest game changer

Source: IGD’s Online Grocery Retailing Outlook Survey ‐ September 2011

© IGD 2012

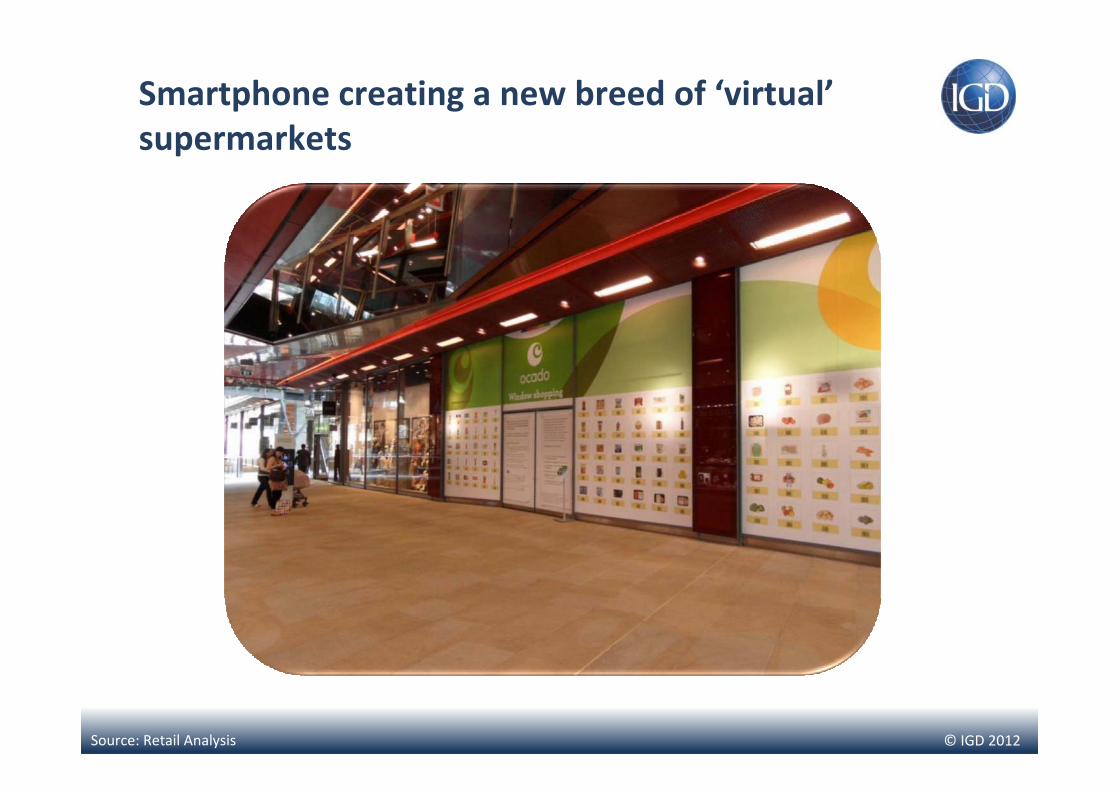

Smartphone creating a new breed of ‘virtual’supermarkets

Source: Retail Analysis

© IGD 2012

Smart phone a “remote control” for consumption

QR barcodes promotions

Product traceability information

Shopping list and product rating capability

Link between loyalty cards, online promotions and the storeIn‐store scanning device and

payment tool (contactless payment)

Source: IGD Research

© IGD 2012

Final thoughts

• Image recognition

• Voice activation – E.g. Locating stores, shopping lists

• Search engines becoming eCommerce sites– Product availability and price data

© IGD 2012

For a free copy of our new report on online retailing, please email me at