NFI:TSX Investor Update - New Flyer...Source: FactSet, Company filings * Total Shareholder Return...

22

0 NFI:TSX Investor Update Q2-17 as at August 10, 2017

Transcript of NFI:TSX Investor Update - New Flyer...Source: FactSet, Company filings * Total Shareholder Return...

0

NFI:TSX Investor Update

Q2-17 as at August 10, 2017

1

Q2-17 Company Highlights

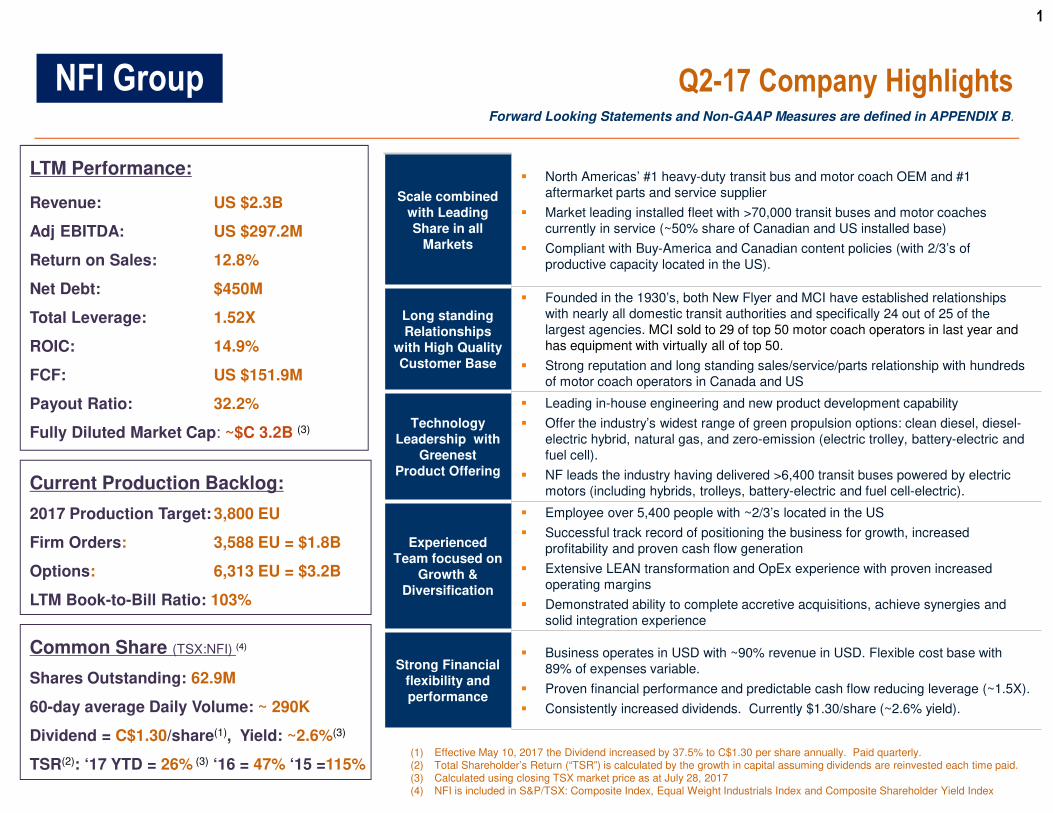

LTM Performance:

Revenue: US $2.3B

Adj EBITDA: US $297.2M

Return on Sales: 12.8%

Net Debt: $450M

Total Leverage: 1.52X

ROIC: 14.9%

FCF: US $151.9M

Payout Ratio: 32.2%

Fully Diluted Market Cap: ~$C 3.2B (3)

Common Share (TSX:NFI) (4)

Shares Outstanding: 62.9M

60-day average Daily Volume: ~ 290K

Dividend = C$1.30/share(1), Yield: ~2.6%(3)

TSR(2): ‘17 YTD = 26% (3) ‘16 = 47% ‘15 =115%(1) Effective May 10, 2017 the Dividend increased by 37.5% to C$1.30 per share annually. Paid quarterly.(2) Total Shareholder’s Return (“TSR”) is calculated by the growth in capital assuming dividends are reinvested each time paid.(3) Calculated using closing TSX market price as at July 28, 2017(4) NFI is included in S&P/TSX: Composite Index, Equal Weight Industrials Index and Composite Shareholder Yield Index

Current Production Backlog:

2017 Production Target: 3,800 EU

Firm Orders: 3,588 EU = $1.8B

Options: 6,313 EU = $3.2B

LTM Book-to-Bill Ratio: 103%

Forward Looking Statements and Non-GAAP Measures are defined in APPENDIX B.

Scale combined with Leading Share in all

Markets

� North Americas’ #1 heavy-duty transit bus and motor coach OEM and #1 aftermarket parts and service supplier

� Market leading installed fleet with >70,000 transit buses and motor coaches currently in service (~50% share of Canadian and US installed base)

� Compliant with Buy-America and Canadian content policies (with 2/3’s of productive capacity located in the US).

Long standing Relationships

with High Quality Customer Base

� Founded in the 1930’s, both New Flyer and MCI have established relationships with nearly all domestic transit authorities and specifically 24 out of 25 of the largest agencies. MCI sold to 29 of top 50 motor coach operators in last year and has equipment with virtually all of top 50.

� Strong reputation and long standing sales/service/parts relationship with hundreds of motor coach operators in Canada and US

Technology Leadership with

GreenestProduct Offering

� Leading in-house engineering and new product development capability

� Offer the industry’s widest range of green propulsion options: clean diesel, diesel-electric hybrid, natural gas, and zero-emission (electric trolley, battery-electric and fuel cell).

� NF leads the industry having delivered >6,400 transit buses powered by electric motors (including hybrids, trolleys, battery-electric and fuel cell-electric).

Experienced Team focused on

Growth & Diversification

� Employee over 5,400 people with ~2/3’s located in the US

� Successful track record of positioning the business for growth, increased profitability and proven cash flow generation

� Extensive LEAN transformation and OpEx experience with proven increased operating margins

� Demonstrated ability to complete accretive acquisitions, achieve synergies and solid integration experience

Strong Financial flexibility and performance

� Business operates in USD with ~90% revenue in USD. Flexible cost base with 89% of expenses variable.

� Proven financial performance and predictable cash flow reducing leverage (~1.5X).

� Consistently increased dividends. Currently $1.30/share (~2.6% yield).

NFI Group

2

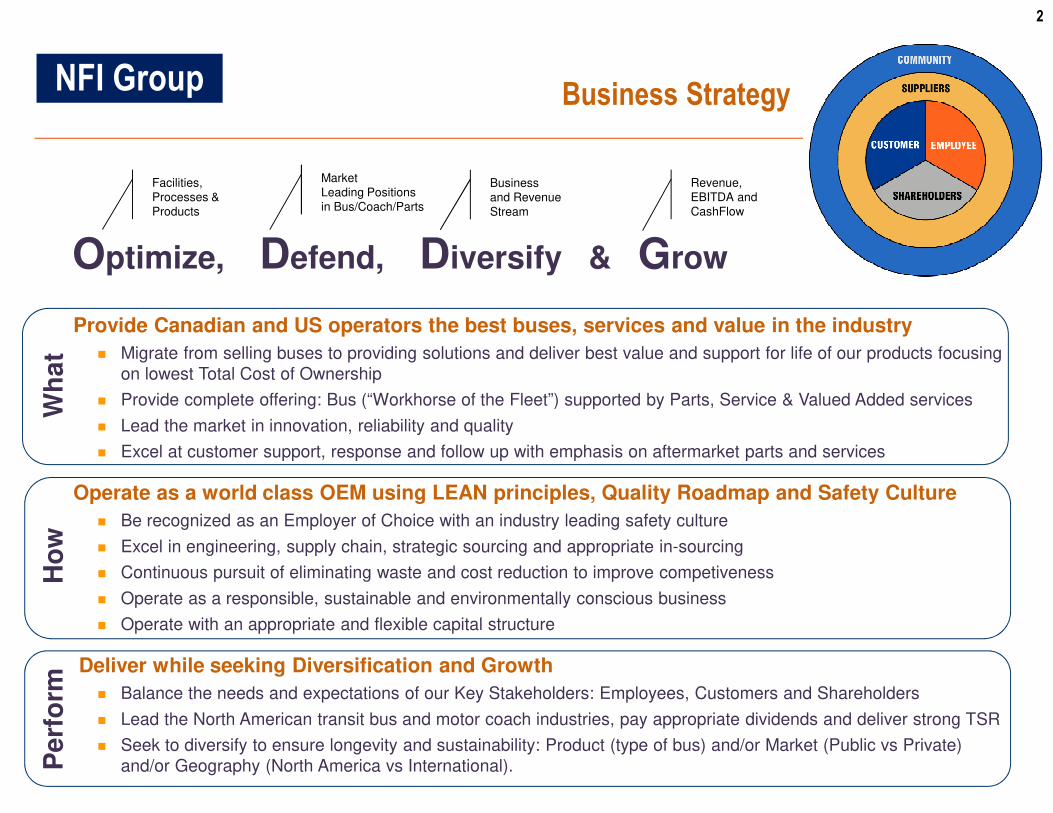

Provide Canadian and US operators the best buses, services and value in the industry

� Migrate from selling buses to providing solutions and deliver best value and support for life of our products focusing on lowest Total Cost of Ownership

� Provide complete offering: Bus (“Workhorse of the Fleet”) supported by Parts, Service & Valued Added services

� Lead the market in innovation, reliability and quality

� Excel at customer support, response and follow up with emphasis on aftermarket parts and services

Operate as a world class OEM using LEAN principles, Quality Roadmap and Safety Culture

� Be recognized as an Employer of Choice with an industry leading safety culture

� Excel in engineering, supply chain, strategic sourcing and appropriate in-sourcing

� Continuous pursuit of eliminating waste and cost reduction to improve competiveness

� Operate as a responsible, sustainable and environmentally conscious business

� Operate with an appropriate and flexible capital structure

Deliver while seeking Diversification and Growth

� Balance the needs and expectations of our Key Stakeholders: Employees, Customers and Shareholders

� Lead the North American transit bus and motor coach industries, pay appropriate dividends and deliver strong TSR

� Seek to diversify to ensure longevity and sustainability: Product (type of bus) and/or Market (Public vs Private) and/or Geography (North America vs International).

+

Facilities, Processes & Products

Market Leading Positions in Bus/Coach/Parts

Business and Revenue Stream

Revenue, EBITDA and CashFlow

Optimize, Defend, Diversify & Grow

Business StrategyNFI GroupW

ha

tH

ow

Pe

rfo

rm

3

846.8

149.3

--

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Total

Retu

rnTotal Shareholder Return*

S&P/TSX Composite

Source: FactSet, Company filings

* Total Shareholder Return includes capital appreciation and dividends paid. Calculated using closing TSX market price as at July 28, 2017

Acquired North America’s leading manufacturer of motor coach & parts/service

Acquired US manufacturer of HD transit buses & parts distributor

Acquired Orion’s transit bus parts business from Daimler

Equity investment in NFI by a global bus and coach body manufacturer

Acquired Can/US Composite Supplier

--Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Acquired US part fabrication supplier

Conversion from IDS to Common Share (NFI)

NFI Group

820.5

145.9

4

Proven Leadership with extensive Industry Experience

Wayne Joseph President, Transit Bus

Joined New Flyer in 2008 as VP Operations and then assumed responsibility as EVP Transit Bus. Prior held executive positions in bus manufacturing for over forty years with NABI, Blue Bird and Flxible, and then at BAE Systems.

Holds a Bachelor of Science in Business Administration and an Accounting Degree and is Certified in Production and Inventory Management (CPIM).

Ian SmartPresident, Motor Coach

Joined New Flyer in 2011 as EVP Aftermarket and prior held various executive positions at Standard Aero for 15 years - one of the world’s largest independent aviation service companies.

Lead the project to privatize and conduct LEAN implementation at a United States Air Force Base.

Holds a Bachelor of Science in Industrial Engineering.

Brian Dewsnup President, Aftermarket Parts

Forrmely NABI’s CFO since 2006 (which NFI acquired in 2013), and then VP Business Development of New Flyer. Led the acquisition of MCI and became VP & GM Aftermarket. Prior served as Controller of Johns Manville's-Waterville operations, and held various capacities at Ford Motor and Visteon.

Holds a Bachelor's in Mechanical Engineering, Masters in Mechanical Engineering, and an MBA in Finance.

Paul SoubryPresident & CEO, NFI Group

Joined New Flyer in 2009 as President and CEO after 24 years with Standard Aero. Holds a Bachelor of Commerce, attended Exec Ed at Harvard Business School and the Institute of Corporate Directors.

In 2003, was named a recipient of ‘Canada’s Top 40 under 40’ award, inducted into the CME Manufacturing Hall of Fame in 2014, and recognized as Canada’s 2016 CEO of the Year by the Financial Post.

David WhiteEVP Supply, NFI Group

Joined New Flyer in 1998 as Corporate Controller, and became Vice President Supply Management in 2002. Prior worked for Deloitte as a Chartered Accountant. Holds a Bachelor of Commerce in Finance and obtained Chartered Accountant designation.

Glenn AshamCFO, NFI Group

Joined New Flyer in 1992. Obtained chartered accountant designation and holds a Bachelor of Commerce. Prior worked with Deloitte providing client services in the areas of accounting, auditing, taxation and management consulting

Colin Pewarchuk, General Counsel, NFI Group

Joined New Flyer in 2006. Prior practiced law with Aikins, Macauley and Thorvaldson and was a Banking Officer with Royal Bank of Canada. Holds a Bachelor of Commerce in Finance and a Bachelor of Laws.

Janice HarperEVP HR, NFI Group

Joined New Flyer in 1998. Holds a Diploma in Creative Communications, a Certificate in Human Resources, is a Charterer Professional in Human Resources (CPHR), a HR Compensation Committee management designation and BA in Communications.

NFI Group

5

#1 Market Share in Transit Bus

Heavy-Duty: Xcelsior®

� Launch in 2009 based on >20 years experience with low floor transit buses. Primary targets is metropolitan & urban fleets

� Offered in 35’, 40’, and 60’ lengths and with the industry’s widest range of propulsion options: clean diesel, diesel-electric hybrid, natural gas, and zero-emission (electric trolley, battery-electric and fuel cell).

Active Canada/US HD Transit Bus Coach Fleet ~85,000

Source: New Flyer Database & Management Estimates

Average Age of the HD Transit Fleet: US = 7.8 years, Canada = 7.3 yearsSource: APTA Public Transportation Factbook 2016

Orion Parts and NABI acquired by NFI in 2013

19%

45%

30%

5%

1%

HD Transit Bus Share (2016 market is ~5,800 units)

Montreal and New YorkOwned by Volvo Truck & Bus

CaliforniaOwned by REV Group

CaliforniaPrivately Owned by

Henry Crown and Company

6

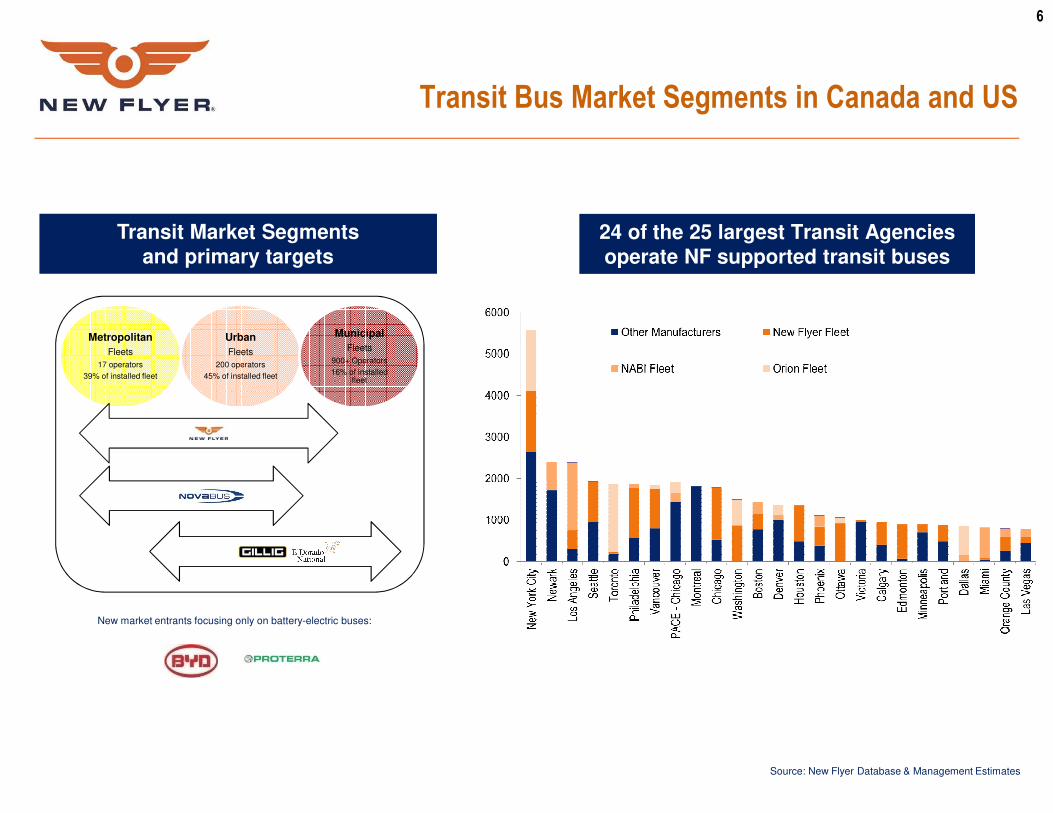

Metropolitan

Fleets

17 operators

39% of installed fleet

Urban

Fleets

200 operators

45% of installed fleet

Municipal

Fleets

900+ Operators

16% of installed fleet

Transit Bus Market Segments in Canada and US

Source: New Flyer Database & Management Estimates

Transit Market Segments and primary targets

24 of the 25 largest Transit Agencies operate NF supported transit buses

New market entrants focusing only on battery-electric buses:

7

28%

39%

26%

7%

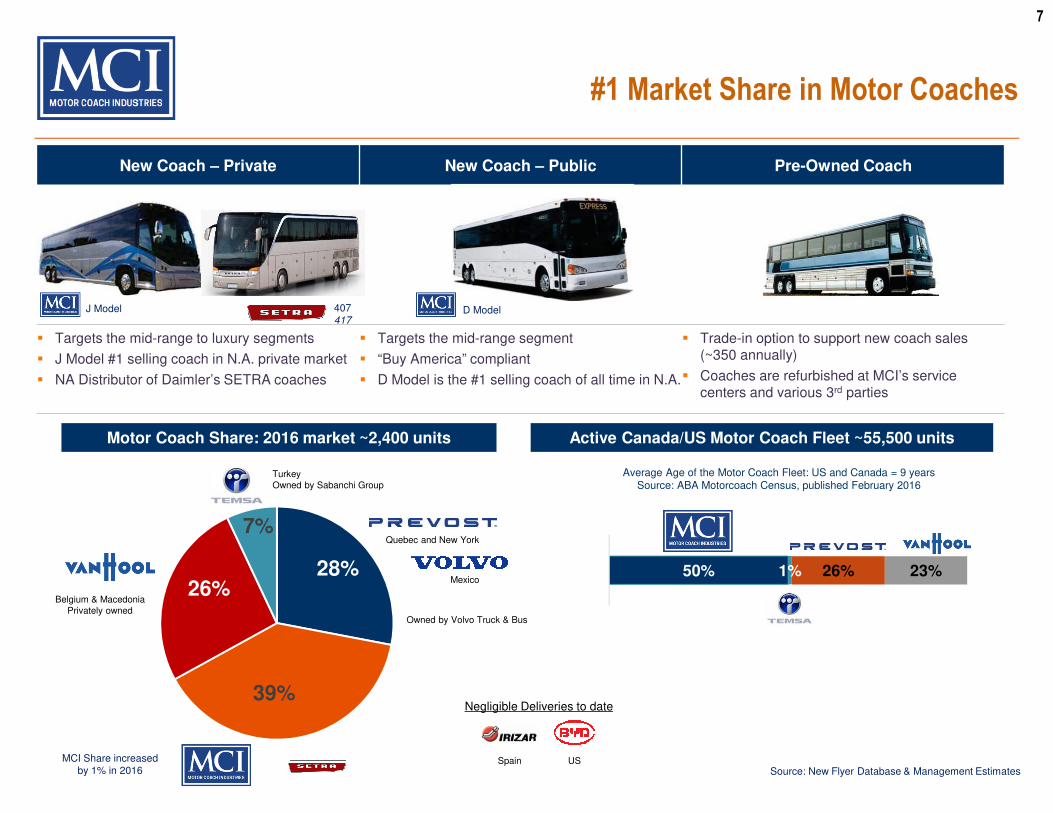

#1 Market Share in Motor Coaches

50% 1% 26% 23%

New Coach – Private New Coach – Public Pre-Owned Coach

� Targets the mid-range to luxury segments

� J Model #1 selling coach in N.A. private market

� NA Distributor of Daimler’s SETRA coaches

� Targets the mid-range segment

� “Buy America” compliant

� D Model is the #1 selling coach of all time in N.A.

� Trade-in option to support new coach sales (~350 annually)

� Coaches are refurbished at MCI’s service centers and various 3rd parties

Active Canada/US Motor Coach Fleet ~55,500 units

Average Age of the Motor Coach Fleet: US and Canada = 9 yearsSource: ABA Motorcoach Census, published February 2016

MCI Share increased by 1% in 2016

J Model D Model407417

Motor Coach Share: 2016 market ~2,400 units

Belgium & MacedoniaPrivately owned

Quebec and New York

TurkeyOwned by Sabanchi Group

Spain US

Mexico

Owned by Volvo Truck & Bus

Negligible Deliveries to date

Source: New Flyer Database & Management Estimates

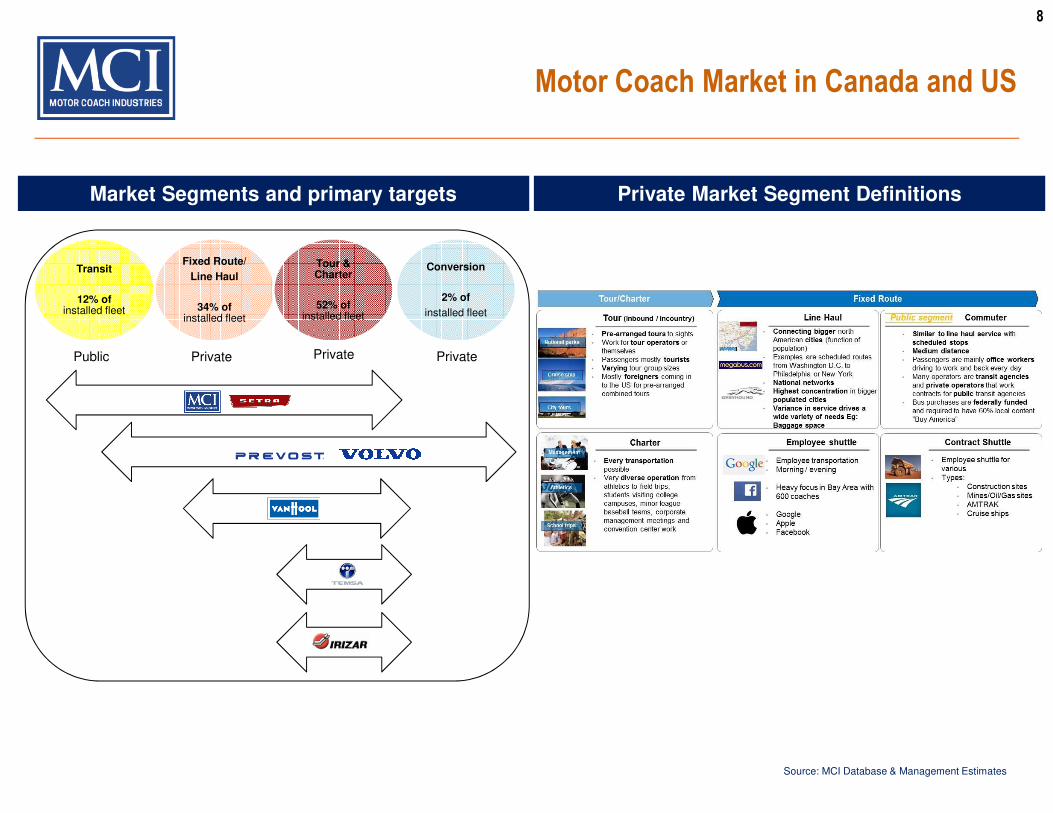

8

Motor Coach Market in Canada and US

Market Segments and primary targets

Transit

12% of installed fleet

Fixed Route/

Line Haul

34% of installed fleet

Tour & Charter

52% of installed fleet

Conversion

2% of

installed fleet

Public Private Private Private

Source: MCI Database & Management Estimates

Private Market Segment Definitions

9

-

5,000

10,000

15,000

20,000

25,00012

-Jan

-09

12-J

an-1

0

12-J

an-1

1

12-J

an-1

2

12-J

an-1

3

12-J

an-1

4

12-J

an-1

5

12-J

an-1

6

12-J

an-1

7

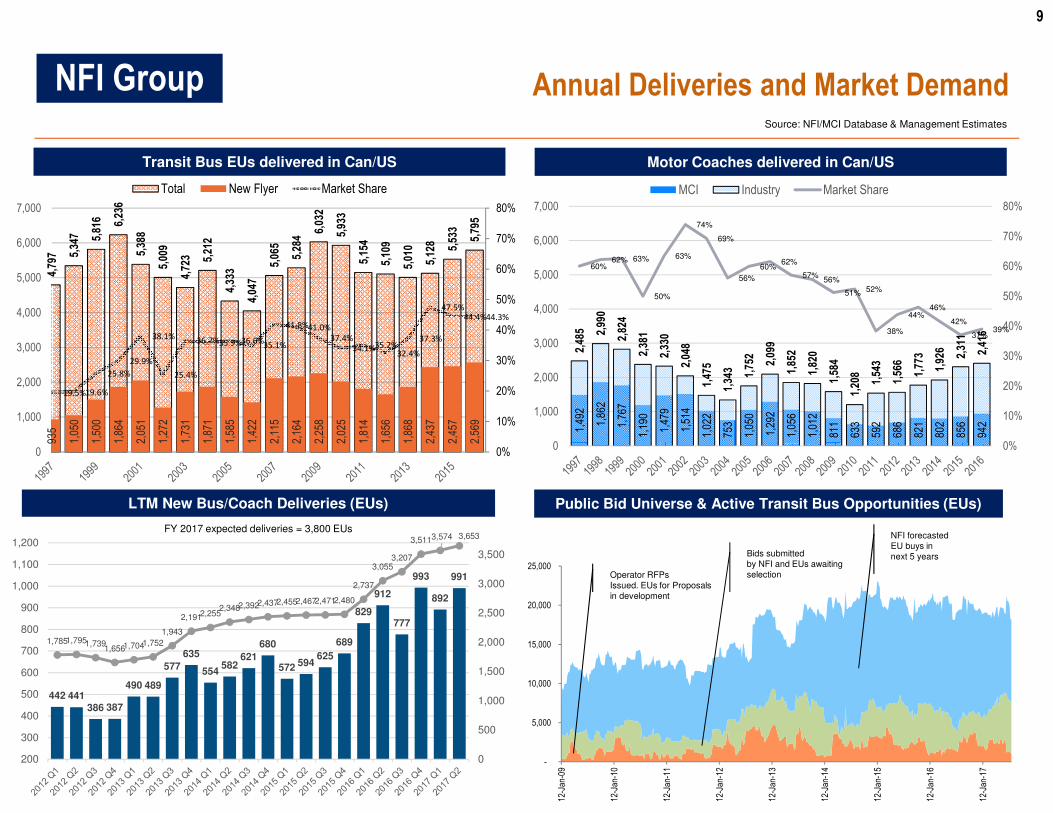

Annual Deliveries and Market Demand

Transit Bus EUs delivered in Can/US Motor Coaches delivered in Can/US

Public Bid Universe & Active Transit Bus Opportunities (EUs)

NFI forecasted EU buys in next 5 yearsBids submitted

by NFI and EUs awaiting selectionOperator RFPs

Issued. EUs for Proposals in development

Source: NFI/MCI Database & Management Estimates

1,49

2

1,86

2

1,76

7

1,19

0

1,47

9

1,51

4

1,02

2

753

1,05

0

1,29

2

1,05

6

1,01

2

811

633

592

686

821

802

856

942

2,48

5 2,99

0

2,82

4

2,38

1

2,33

0

2,04

8

1,47

5

1,34

3 1,75

2

2,09

9

1,85

2

1,82

0

1,58

4

1,20

8

1,54

3

1,56

6

1,77

3

1,92

6

2,31

1

2,41

6

60%62% 63%

50%

63%

74%

69%

56%

60%62%

57%56%

51% 52%

38%

44%46%

42%

37%39%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

MCI Industry Market Share

4,79

7 5,34

7 5,81

6 6,23

6

5,38

8

5,00

9

4,72

3 5,21

2

4,33

3

4,04

7

5,06

5

5,28

4

6,03

2

5,93

3

5,15

4

5,10

9

5,01

0

5,12

8 5,53

3

5,79

5

935

1,05

0

1,50

0

1,86

4

2,05

1

1,27

2

1,73

1

1,87

1

1,58

5

1,42

2

2,11

5

2,16

4

2,25

8

2,02

5

1,81

4

1,65

6

1,86

8

2,43

7

2,45

7

2,56

9

19.5%19.6%

25.8%

29.9%

38.1%

25.4%

36.7%35.9%36.6%35.1%

41.8%41.0%

37.4%

34.1%35.2%

32.4%

37.3%

47.5%

44.4%44.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Total New Flyer Market Share

LTM New Bus/Coach Deliveries (EUs)

442 441386 387

490 489

577

635

554582

621

680

572 594625

689

829

912

777

993

892

991

1,7851,7951,7391,6561,7041,752

1,943

2,1912,2552,3482,3922,4372,4552,4672,4712,480

2,737

3,0553,207

3,5113,574 3,653

0

500

1,000

1,500

2,000

2,500

3,000

3,500

200

300

400

500

600

700

800

900

1,000

1,100

1,200

NFI Group

FY 2017 expected deliveries = 3,800 EUs

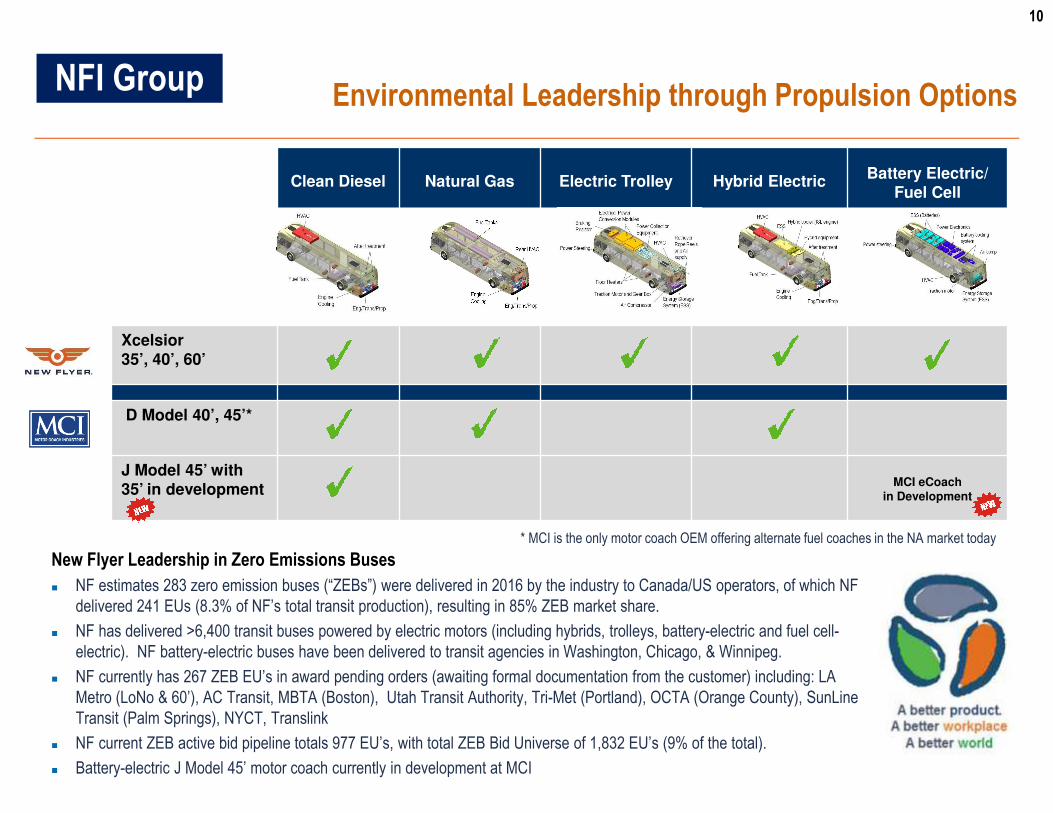

10

Clean Diesel Natural Gas Electric Trolley Hybrid ElectricBattery Electric/

Fuel Cell

Xcelsior35’, 40’, 60’

D Model 40’, 45’*

J Model 45’ with 35’ in development

MCI eCoachin Development

Environmental Leadership through Propulsion OptionsNFI Group

New Flyer Leadership in Zero Emissions Buses

� NF estimates 283 zero emission buses (“ZEBs”) were delivered in 2016 by the industry to Canada/US operators, of which NF

delivered 241 EUs (8.3% of NF’s total transit production), resulting in 85% ZEB market share.

� NF has delivered >6,400 transit buses powered by electric motors (including hybrids, trolleys, battery-electric and fuel cell-

electric). NF battery-electric buses have been delivered to transit agencies in Washington, Chicago, & Winnipeg.

� NF currently has 267 ZEB EU’s in award pending orders (awaiting formal documentation from the customer) including: LA

Metro (LoNo & 60’), AC Transit, MBTA (Boston), Utah Transit Authority, Tri-Met (Portland), OCTA (Orange County), SunLine

Transit (Palm Springs), NYCT, Translink

� NF current ZEB active bid pipeline totals 977 EU’s, with total ZEB Bid Universe of 1,832 EU’s (9% of the total).

� Battery-electric J Model 45’ motor coach currently in development at MCI

* MCI is the only motor coach OEM offering alternate fuel coaches in the NA market today

11

Manufacturing, Fabrication and Service Footprint

`

FL

AL

TX

CA

NDMN

IL IN OH

KY

WV

PA

NY

NJ

SK MB

ON

QC

AB

Renton, WANFI Service Center

Ontario, CANFI Completion & Service Center

Crookston, MNNFI Bus Completion

St Cloud, MNNFI Bus Manufacture

Fiberglass FabricationAnniston, AL

NFI Bus ManufactureParts Fabrication

Fiberglass Fabrication

Elkhart, INTCB Part Fabrication

Arnprior, ONNFI Service Center

NFI - Winnipeg, MBParts Fabrication

Fiberglass FabricationBus Shell Assembly

New Product Development

MCI - Winnipeg, MBParts Fabrication, MCI D Model Shell Assembly

Complete J Model manufactureNew Product Development

Fiberglass FabricationMontreal, PQ

MCI Service Center

Blackwood, NJMCI Service Center

Winter Garden, FLMCI Service Center

Dallas, TXMCI Service Center

Los Alamitos, CAMCI Service Center

Pembina, NDMCI D Shell Completion

Des Plaines, ILMCI Service Center

Jamestown, NYPart Fabrication/Assembly

+

Hayward, CAMCI Service Center

Opening Q3-17

NFI Group

WA

12

The Industry’s most comprehensive Parts offering+

� Widest bus and motor coach product inventory, industry leading distribution network with shortest delivery times.

� Added value through unique offerings (Kits, Mid-life upgrade programs, Vendor Managed Inventory, KanBan, etc).

� New MCI website offering state of the art on-line sales and distribution features.

13

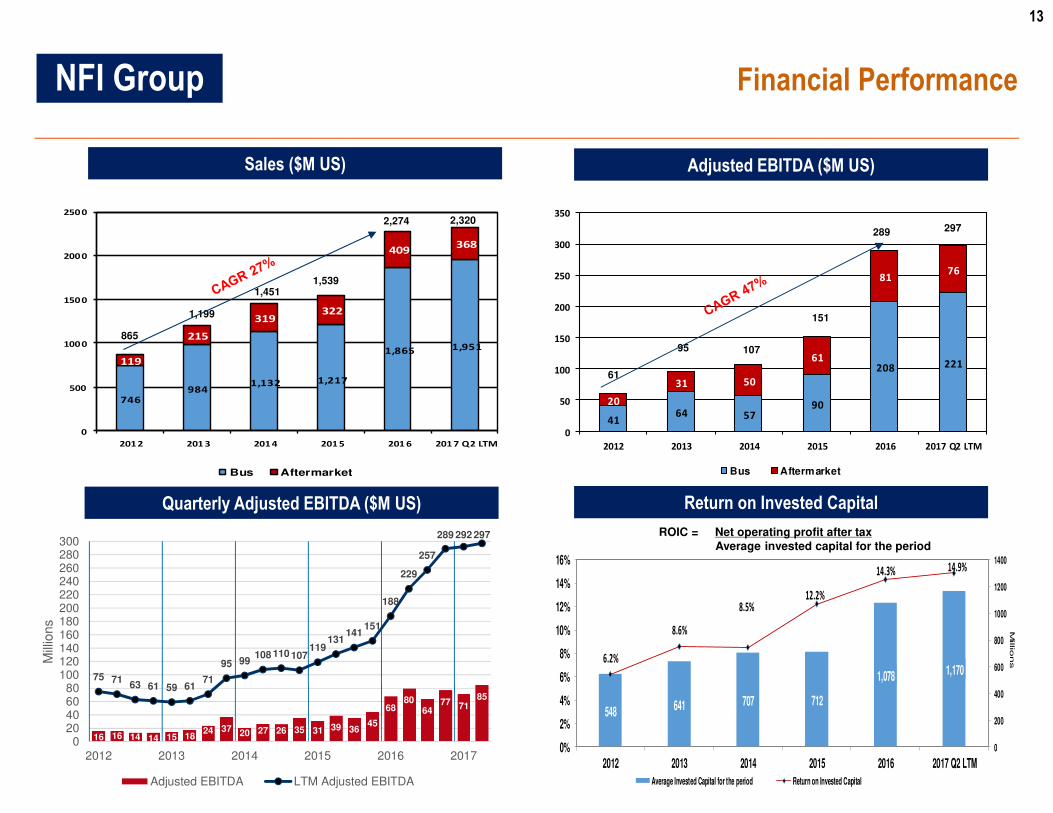

548 641 707 712

1,078 1,1706.2%

8.6%

8.5%12.2%

14.3% 14.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

200

400

600

800

1000

1200

1400

2012 2013 2014 2015 2016 2017 Q2 LTM

Millio

ns

Average Invested Capital for the period Return on Invested Capital

746

9841,132 1,217

1,865 1,951

119

215

319322

409368

0

500

1000

1500

2000

2500

2012 201 3 2014 2015 201 6 2017 Q2 LTM

Bus Aftermarket

4164 57

90

208 221

20

31 50

61

8176

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016 2017 Q2 LTM

Bus Aftermarket

ROIC = Net operating profit after taxAverage invested capital for the period

Financial Performance

Sales ($M US) Adjusted EBITDA ($M US)

Return on Invested Capital

+

61

95 107

151

289

1,199

1,4511,539

2,274

Quarterly Adjusted EBITDA ($M US)

2972,320

865

16 16 14 14 15 1824 37 20 27 26 35 31 39 36

45

6880

6477 71

85

75 7163 61 59 61

71

95 99108 110 107

119131

141151

188

229

257

289 292 297

020406080

100120140160180200220240260280300

2012 2013 2014 2015 2016 2017

Mill

ions

Adjusted EBITDA LTM Adjusted EBITDA

NFI Group

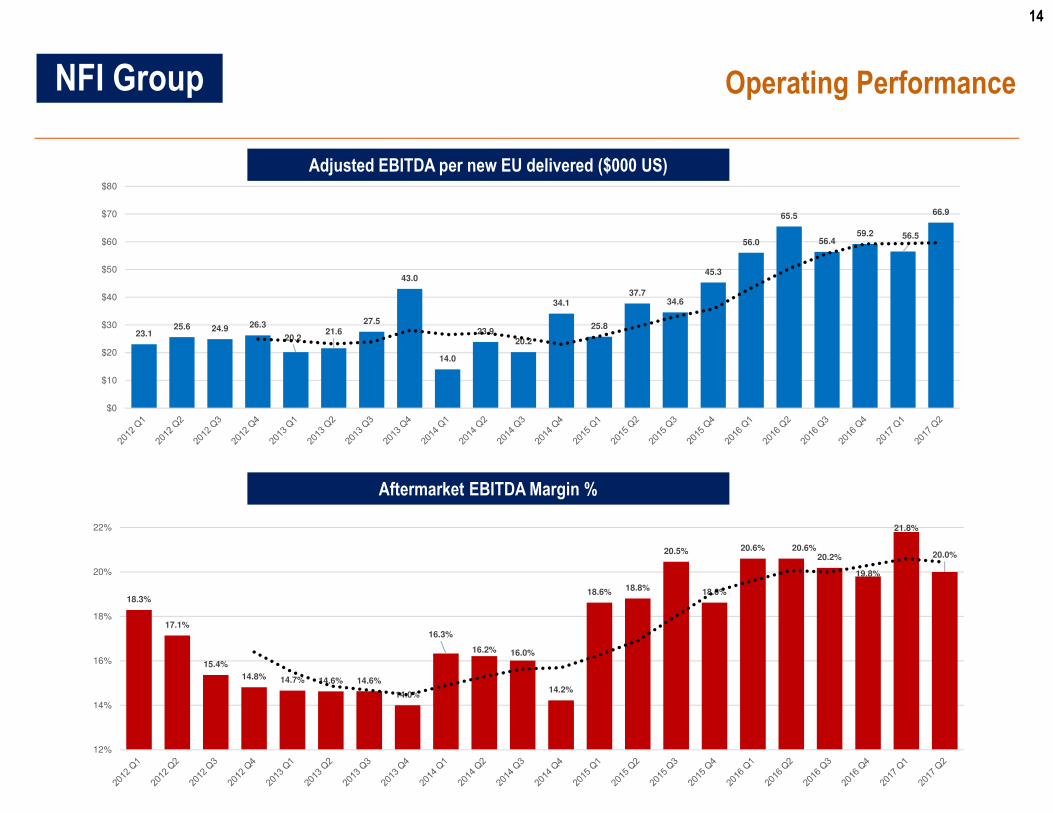

14

Operating Performance

Adjusted EBITDA per new EU delivered ($000 US)

Aftermarket EBITDA Margin %

23.125.6 24.9 26.3

20.221.6

27.5

43.0

14.0

23.920.2

34.1

25.8

37.734.6

45.3

56.0

65.5

56.459.2 56.5

66.9

$0

$10

$20

$30

$40

$50

$60

$70

$80

18.3%

17.1%

15.4%

14.8% 14.7% 14.6% 14.6%

14.0%

16.3%

16.2% 16.0%

14.2%

18.6% 18.8%

20.5%

18.6%

20.6% 20.6%20.2%

19.8%

21.8%

20.0%

12%

14%

16%

18%

20%

22%

NFI Group

15

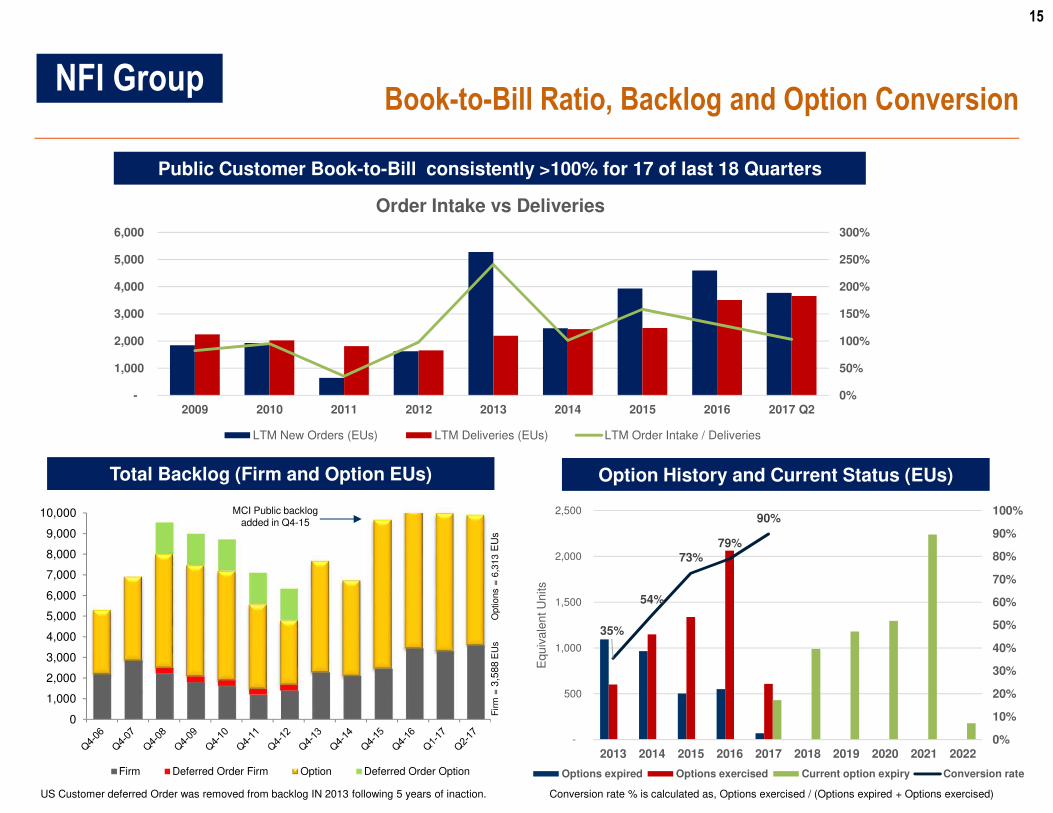

Book-to-Bill Ratio, Backlog and Option Conversion

Public Customer Book-to-Bill consistently >100% for 17 of last 18 Quarters

Total Backlog (Firm and Option EUs)

US Customer deferred Order was removed from backlog IN 2013 following 5 years of inaction.

Firm

= 3

,588

EU

sO

ptions =

6,3

13 E

Us

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Firm Deferred Order Firm Option Deferred Order Option

Option History and Current Status (EUs)

Conversion rate % is calculated as, Options exercised / (Options expired + Options exercised)

35%

54%

73%79%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

500

1,000

1,500

2,000

2,500

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Eq

uiv

ale

nt U

nits

Options expired Options exercised Current option expiry Conversion rate

MCI Public backlog added in Q4-15

0%

50%

100%

150%

200%

250%

300%

-

1,000

2,000

3,000

4,000

5,000

6,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 Q2

Order Intake vs Deliveries

LTM New Orders (EUs) LTM Deliveries (EUs) LTM Order Intake / Deliveries

NFI Group

16

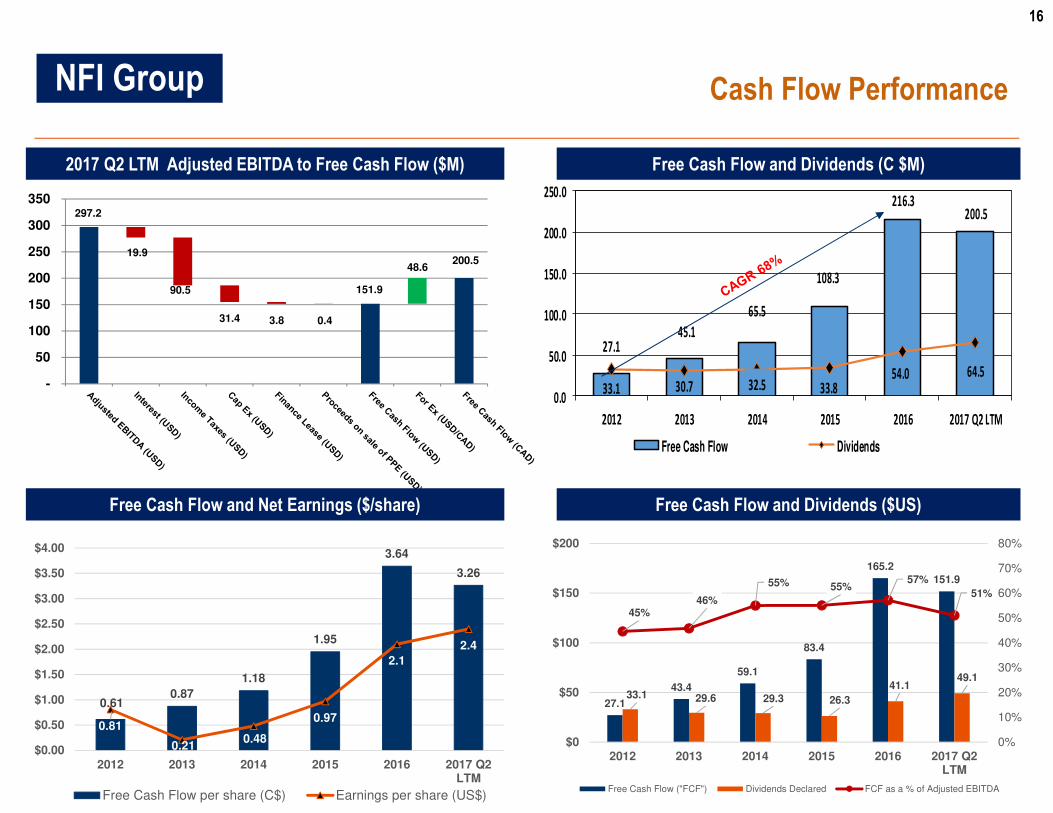

Cash Flow Performance

Free Cash Flow and Dividends (C $M)2017 Q2 LTM Adjusted EBITDA to Free Cash Flow ($M)

297.2

19.9

90.5

31.4 3.8 0.4

151.9

48.6 200.5

-

50

100

150

200

250

300

350

+

Free Cash Flow and Dividends ($US)

0.610.87

1.18

1.95

3.64

3.26

0.81

0.210.48

0.97

2.1

2.4

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

2012 2013 2014 2015 2016 2017 Q2LTM

Free Cash Flow per share (C$) Earnings per share (US$)

Free Cash Flow and Net Earnings ($/share)

27.145.1

65.5

108.3

216.3200.5

33.1 30.7 32.5 33.854.0 64.5

0.0

50.0

100.0

150.0

200.0

250.0

2012 2013 2014 2015 2016 2017 Q2 LTM

Free Cash Flow Dividends

27.1

43.4

59.1

83.4

165.2151.9

33.1 29.6 29.3 26.3

41.149.1

45%46%

55% 55%57%

51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

$0

$50

$100

$150

$200

2012 2013 2014 2015 2016 2017 Q2LTM

Free Cash Flow ("FCF") Dividends Declared FCF as a % of Adjusted EBITDA

NFI Group

17

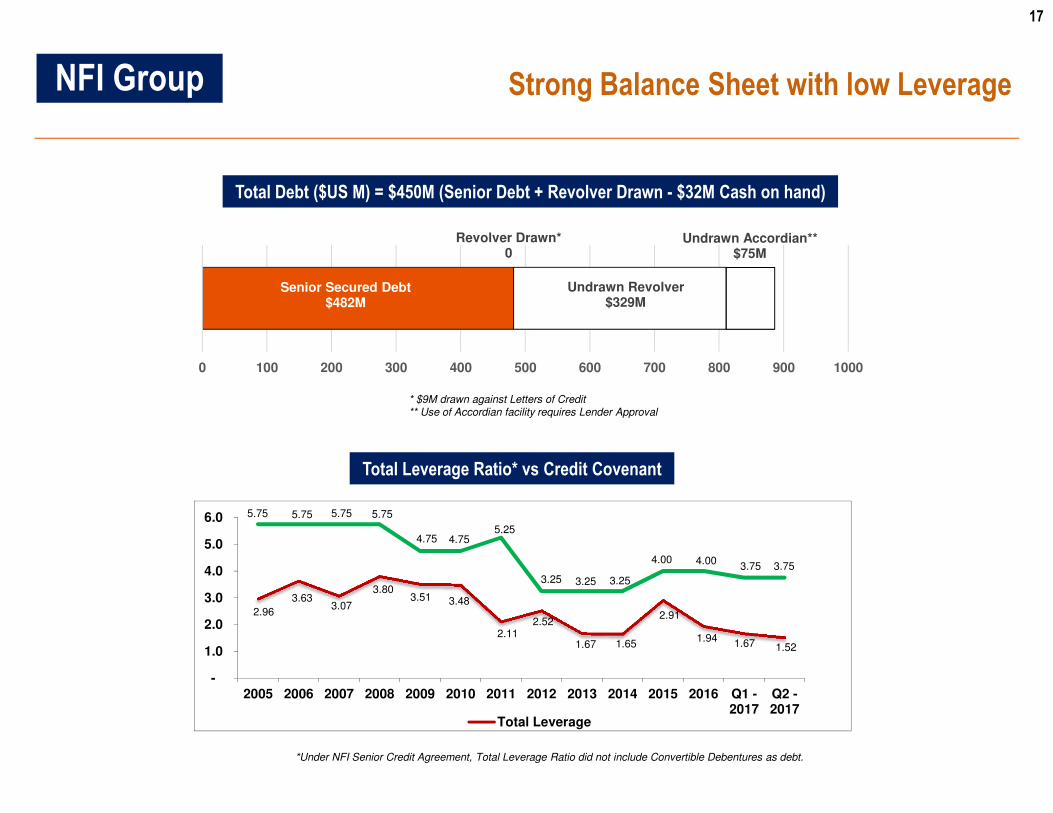

Strong Balance Sheet with low Leverage

*Under NFI Senior Credit Agreement, Total Leverage Ratio did not include Convertible Debentures as debt.

Total Debt ($US M) = $450M (Senior Debt + Revolver Drawn - $32M Cash on hand)

Total Leverage Ratio* vs Credit Covenant

+NFI Group

Senior Secured Debt$482M

Revolver Drawn*0

Undrawn Revolver$329M

Undrawn Accordian**$75M

0 100 200 300 400 500 600 700 800 900 1000

2.96

3.633.07

3.80 3.51 3.48

2.11 2.52

1.67 1.65

2.91

1.94 1.67 1.52

5.75 5.75 5.75 5.75

4.75 4.75 5.25

3.25 3.25 3.25

4.00 4.00 3.75 3.75

-

1.0

2.0

3.0

4.0

5.0

6.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 -2017

Q2 -2017

Total Leverage

* $9M drawn against Letters of Credit ** Use of Accordian facility requires Lender Approval

18

� New US Administration focus on Infrastructure spending, US economic health and tax

reform could assist with further rejuvenation of the aging transit bus/motor coach fleet

� New Canadian government commitment to federal spending on transit infrastructure

� Proven LEAN manufacturing and OpEx expertise deployment continues company-wide

which has cost reduction and working capital benefits, plus improved competitiveness

� Significant progress made with additional investments planned for critical parts fabrication

� New product offerings in development (35’ coach, battery-electric transit buses and motor

coaches announced). Ground breaking innovation soon to launch for accessible

community segment in motor coach. Vehicle Innovation Centre to launched in Q4-17.

� Potential for synergies resulting from common IT platform across NFI and MCI (in process)

� Potential to grow market share in both core bus (NF) and coach (MCI) OEM segments

� Potential for additional aftermarket share with added cost reduction and working capital

benefits from combining NFI and MCI parts businesses into one (in process)

� Continue M&A opportunities being investigated: Vertical (part fabrication, supply chain and

aftermarket) and Horizontal (other bus types or other bus markets)

Opportunities for Growth and Margin Enhancement+NFI Group

19

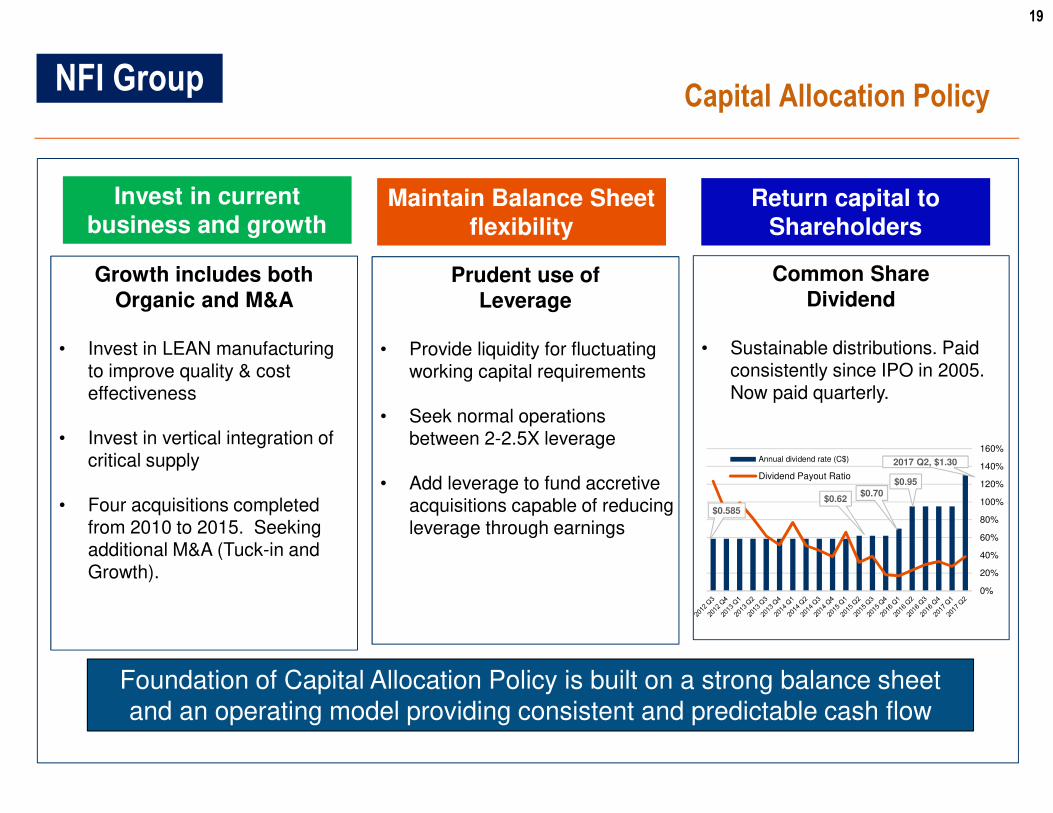

Capital Allocation Policy+

Invest in current business and growth

Maintain Balance Sheet flexibility

Return capital to Shareholders

Growth includes both Organic and M&A

• Invest in LEAN manufacturing to improve quality & cost effectiveness

• Invest in vertical integration of critical supply

• Four acquisitions completed from 2010 to 2015. Seeking additional M&A (Tuck-in and Growth).

Prudent use of Leverage

• Provide liquidity for fluctuating working capital requirements

• Seek normal operations between 2-2.5X leverage

• Add leverage to fund accretive acquisitions capable of reducing leverage through earnings

Common Share Dividend

• Sustainable distributions. Paid consistently since IPO in 2005. Now paid quarterly.

Foundation of Capital Allocation Policy is built on a strong balance sheet and an operating model providing consistent and predictable cash flow

$0.585

$0.62$0.70

$0.95

2017 Q2, $1.30

0%

20%

40%

60%

80%

100%

120%

140%

160%Annual dividend rate (C$)

Dividend Payout Ratio

NFI Group

20

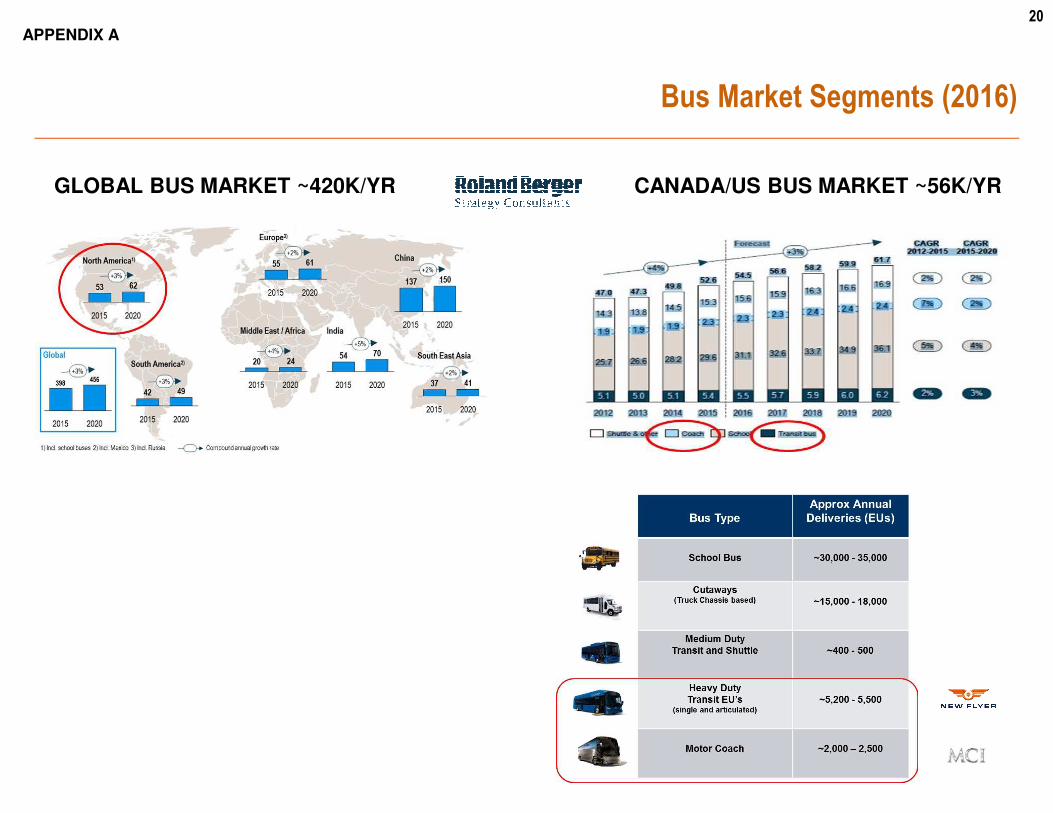

GLOBAL BUS MARKET ~420K/YR CANADA/US BUS MARKET ~56K/YR

Bus Market Segments (2016)

APPENDIX A

21

FORWARD LOOKING STATEMENTS

This investor presentation contains forward-looking statements relating to expected future events, including the integration of the acquired business into New Flyer’s existing business and expected synergies, the

diversification and growth of the combined bus, motor coach and aftermarket parts businesses. Although the forward-looking statements contained in this investor presentation are based upon what management

believes to be reasonable assumptions, investors cannot be assured that actual results will be consistent with these forward-looking statements, and the differences may be material. Actual results may differ

materially from management expectations as reflected in such forward-looking statements for a variety of reasons, including risks related the ability to implement the operational changes necessary to achieve the

intended synergies, acquisitions, joint ventures and other strategic relationships with third parties (including liabilities relating thereto), the covenants contained in the Company’s new senior credit facilities could

impact the ability of the Company to fund dividends, market and general economic conditions and economic conditions of and funding availability for customers to purchase buses and to purchase parts or services,

customers may not exercise options to purchase additional buses, the ability of customers to suspend or terminate contracts for convenience and the other risks and uncertainties discussed in the materials filed with

the Canadian securities regulatory authorities and available on SEDAR at www.sedar.com. Due to the potential impact of these factors, the Company disclaims any intention or obligation to update or revise any

forward-looking statements, whether as a result of new information, future events or otherwise, unless required by applicable law.

FINANCIAL TERMS, DEFINITIONS AND CONDITIONS

References to “EBITDA” are to earnings before interest, income taxes, depreciation and amortization, gains or losses on disposal of property, plant and equipment and unrealized foreign exchange losses or gains

on non-current monetary items. References to “Adjusted EBITDA” are to EBITDA after adjusting for: the effects of certain non-recurring and/or non-operations related items that have impacted the business and are

not expected to recur, including non-recurring costs relating to business acquisitions, product rationalization costs, impairment loss on equipment and intangible assets, equity settled stock-based compensation, fair

value adjustment to MCI’s inventory and deferred revenue, proportion of the total return swap realized, loss on derecognition of long-term debt and costs associated with assessing strategic and corporate initiatives.

Return on Invested Capital “ROIC” is calculated by dividing Net Operating Profit After Tax by Average Invested Capital for the period. References to “Net Operating Profit After Tax” are to Adjusted EBITDA less

depreciation of plant and equipment and income taxes. References to “Invested Capital” are to shareholders’ equity plus long-term debt, obligations under finance leases, other long-term liabilities, convertible

debentures and derivative financial instrument liabilities less cash.

Management believes EBITDA, Adjusted EBITDA, ROIC and Free Cash Flow (as defined below) are useful measures in evaluating the performance of the Company. “Free Cash Flow” means net cash generated by

operating activities adjusted for changes in non-cash working capital items, interest paid, interest expense, income taxes paid, current income tax expense, effect of foreign currency rate on cash, defined benefit

funding, non-recurring transitional costs relating to business acquisitions, costs associated with assessing strategic and corporate initiatives, product rationalization costs, defined benefit expense, cash capital

expenditures, fair value adjustment to MCI’s inventory and deferred revenue, proceeds from disposition of property, plant and equipment, gain received on total return swap settlement, proportion of the total return

swap realized and principal payments on capital leases. However, EBITDA, Adjusted EBITDA, ROIC and Free Cash Flow are not recognized earnings measures and do not have standardized meanings prescribed

by IFRS. Readers of this presentation are cautioned that EBITDA, Adjusted EBITDA and ROIC should not be construed as an alternative to net earnings or loss determined in accordance with IFRS as an indicator of

New Flyer's performance, and Free Cash Flow should not be construed as an alternative to cash flows from operating, investing and financing activities determined in accordance with IFRS as a measure of liquidity

and cash flows. A reconciliation of net earnings and cash flow to EBITDA and Adjusted EBITDA, based on the Financial Statements, has been presented In Management’s Discussion and Analysis of Financial

Condition under the heading “Reconciliation of Net Earnings to EBITDA and Adjusted EBITDA” and “Reconciliation of Cash Flow to EBITDA and Adjusted EBITDA”, respectively. A reconciliation of Free Cash Flow to

cash flows from operations is provided under the heading “Summary of Free Cash Flow”.

New Flyer’s method of calculating EBITDA, Adjusted EBITDA, ROIC and Free Cash Flow may differ materially from the methods used by other issuers and, accordingly, may not be comparable to similarly titled

measures used by other issuers. Dividends paid from Free Cash Flow are not assured, and the actual amount of dividends received by holders of Shares will depend on, among other things, the Company's financial

performance, debt covenants and obligations, working capital requirements and future capital requirements, all of which are susceptible to a number of risks, as described in New Flyer’s public filings available on

SEDAR at www.sedar.com.

All figures are in U.S. dollars unless otherwise noted.

FORWARD LOOKING STATEMENTS, FINANCIAL TERMS, DEFINITIONS AND CONDITIONS

+

APPENDIX B