Next generation CHP in competitive heat and power markets by Jouni Haikarainen, VP Finland and...

11

Next generation CHP in competitive heat and power markets COGEN Europe Annual Conference, Brussels, May 19 th 2015 Jouni Haikarainen, Vice President, Finland and Baltic countries Heat, Electricity Sales and Solutions Division

-

Upload

fortum -

Category

Presentations & Public Speaking

-

view

235 -

download

0

Transcript of Next generation CHP in competitive heat and power markets by Jouni Haikarainen, VP Finland and...

Next generation CHP in competitive heat and power marketsCOGEN Europe Annual Conference, Brussels, May 19th 2015

Jouni Haikarainen, Vice President, Finland and Baltic countries

Heat, Electricity Sales and Solutions Division

2

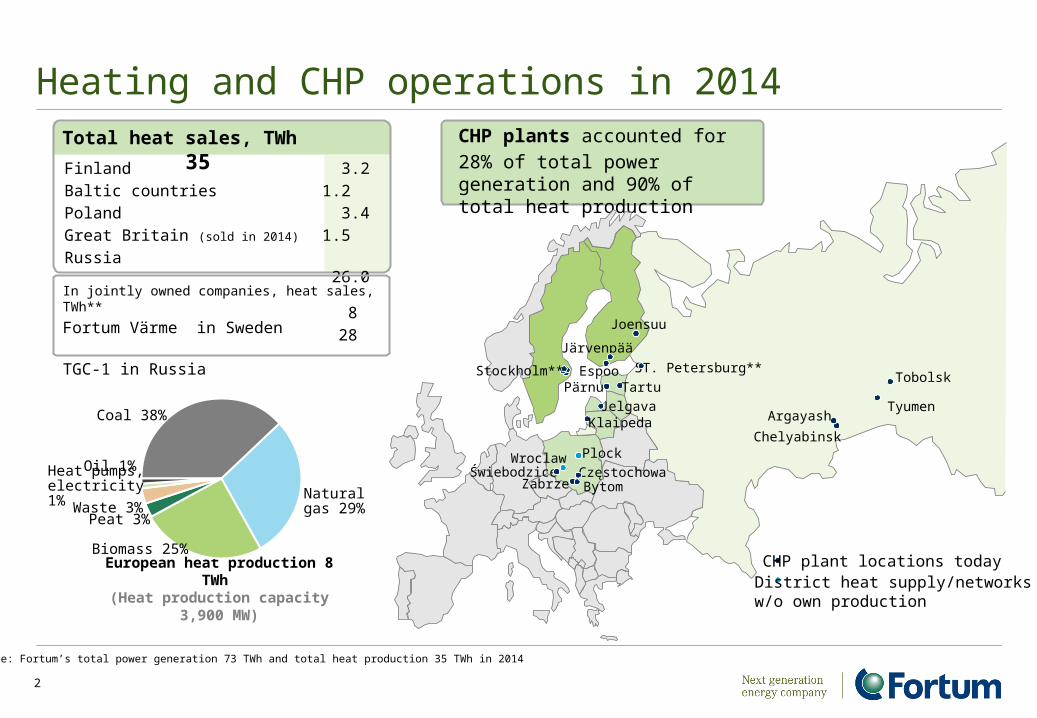

Heating and CHP operations in 2014

Note: Fortum’s total power generation 73 TWh and total heat production 35 TWh in 2014

European heat production 8 TWh (Heat production capacity 3,900 MW)

Peat 3%

Oil 1%

Waste 3%Natural gas 29%

Biomass 25%

Heat pumps, electricity 1%

Coal 38%

CHP plants accounted for

28% of total power generation and 90% of total heat production

Chelyabinsk

Tobolsk

Tyumen

Stockholm**Tartu

JelgavaKlaipeda

Pärnu

Joensuu

Järvenpää

Bytom Częstochowa Świebodzice

Zabrze

PlockWroclaw

Argayash

CHP plant locations todayDistrict heat supply/networksw/o own production

ST. Petersburg**Espoo

Total heat sales, TWh 35 Finland

Baltic countries

Poland

Great Britain (sold in 2014)

Russia

3.2

1.2

3.4

1.5

26.0In jointly owned companies, heat sales, TWh**

Fortum Värme in Sweden

TGC-1 in Russia 8

28

Heat markets for district heating and CHP in Baltic Rim

3

Heat solutions of residential customers(data 2013)

DH production mix by source (data 2013)

Sources: Euroheat & Power, 2015

• DH market share 40%...65%

• RES and heat pumps share to increase

• Renewables mainly wood sources

• Resource-efficient DH production sources• Sweden over ~80%• Finland and Baltics ~30%• Poland ~15%

• Industrial surplus heat utilized in Nordics and Poland

• Fossil fuels 85% in Poland

4

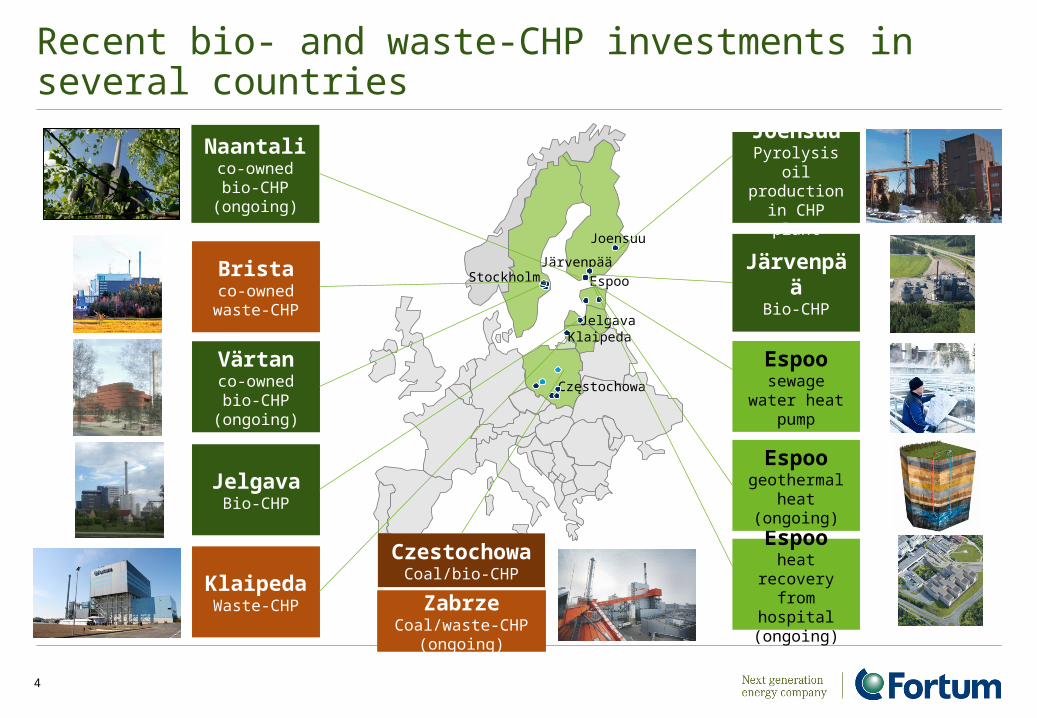

Recent bio- and waste-CHP investments in several countries

Stockholm

JelgavaKlaipeda

Joensuu

Järvenpää

Espoo

Częstochowa

JärvenpääBio-CHP

Bristaco-owned

waste-CHP

Värtanco-owned bio-CHP (ongoing)

JelgavaBio-CHP

KlaipedaWaste-CHP

CzestochowaCoal/bio-CHP

Espoosewage water

heat pump

Espooheat recovery from hospital

(ongoing)

Joensuu Pyrolysis oil production in

CHP plant

Naantalico-owned bio-CHP (ongoing)

Espoogeothermal

heat (ongoing)

ZabrzeCoal/waste-CHP

(ongoing)

5

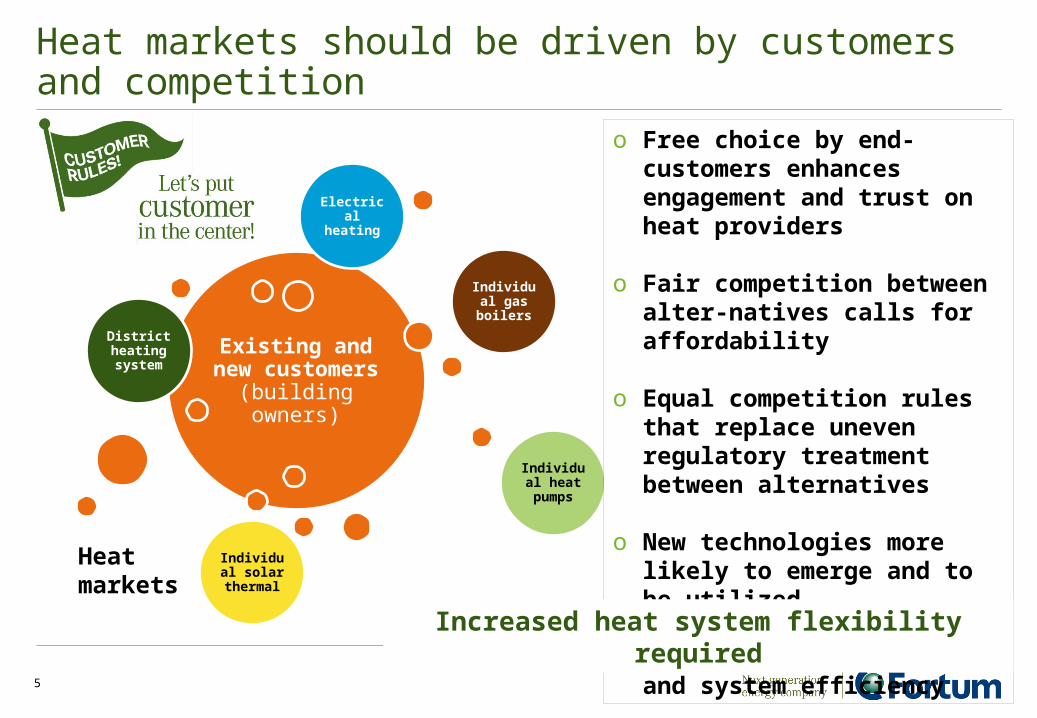

Heat markets should be driven by customers and competition

Existing and new customers (building owners)

District heating system

Individual gas

boilers

Individual heat

pumps

Individual solar

thermal

Electrical heating

o Free choice by end-customers enhances engagement and trust on heat providers

o Fair competition between alter-natives calls for affordability

o Equal competition rules that replace uneven regulatory treatment between alternatives

o New technologies more likely to emerge and to be utilized

o Drives for best resource and system efficiency

Heat markets

Increased heat system flexibility required

DH price competitiveness with main alternatives

6

Espoo Joensuu Keski-Uusimaa Stockholm0

10

20

30

40

50

60

70

80

90

100

DH 2015 Ground heat pump 2015

€/MWh

• Low electricity prices and interest rates are driving ground heat pump competitiveness.

• Ground heat pumps are competitive with DH with current low power price in the Nordics.

• Gas boilers are serious competitors to DH i.e. in the Baltic countries.

• Air heat pumps have also become more efficient and less expensive and might reduce substantially the base load heat demand.

• Total heating cost (CAPEX, variable and fixed OPEX)

• High fossil fuel taxation of DH production in Finland and Sweden

• Challenging for gas based CHP but biomass CHP remains competitive

Finland: Large city(gas/coal/other)

Finland: Mid-sized city(biofuels)

Finland: Mid-sized city(biofuels/gas)

Sweden: Large city(bio/waste/coal/

geothermal)

7

CHP competing with other heat sources

The single DH system operator to set up voluntary economic and technical conditions to promote lowest cost and sustainable heat sources for the benefit of end-customers, system and society.

Competitive high-efficient renewable CHP in heat markets

8

How to secure competitive heat

from CHP?

Competitive heat from CHP against

alternative heat sources

Economic and optimized base load

capacity in heat production mix

Energy recovery from non-recyclable

waste

CHP+ (cooling, pyrolysis) ETS as steering

mechanism, no additional emission

tax burden

Using sustainable biomass and other

renewable fuels

Maximize electricity to save primary

energy

Competitive DH against

alternatives to end-customers

Heat price competitiveness

Fuel flexibility

Energy efficiency

Equal taxationTechnology

Electricity market developments to encourage CHP

9

Towards internal markets

• Larger markets enforce competition, more stable and competitive prices and a better service level for customers

• Investment in transmission infrastructure to improve market efficiency and security of supply

• Positive regional developments as a stepping stone towards a common European markets

• Full integration of the retail and wholesale electricity markets

Energy-only market development

• Energy-only markets as preferred market model• Remove regulated energy prices both from heat and electricity• Clarification of EU level principles and criteria for the use of capacity

mechanisms, including rules for cross-border participation• Proper integration of renewable energy

Key takeaways

10

• Heat markets are driven by customers and competition

• Free choice of heating alternatives for end-customers

• CHP needs to be competitive source in heat supply to DH networks

• Renewable, next generation CHP to enhance competitiveness

• Integrated and energy-only electricity markets to encourage high-efficient CHP as relatively small scale, renewable electricity production

11

Thank you!