NEW PowerPoint Template - Standard Chartered

19

Corporate Briefing

Transcript of NEW PowerPoint Template - Standard Chartered

Agenda

Agenda Time

Welcome note and introduction 2:00 PM – 2:05 PM

Recitation of Holy Quran 2:05 PM – 2:10 PM

Company Briefing / Strategy 2:10 PM – 2:30 PM

Financial Performance 2:30 PM – 2:45 PM

Community Investments 2:45 PM – 3:00 PM

Q&A 3:00 PM – 3:15 PM

1

Disclaimer

Important Notice

This document contains or incorporates by reference “forward-looking statements” regarding the belief or current expectations of Standard Chartered Bank

(Pakistan) Limited, the board of the Company (the “Directors”) and other members of its senior management about the strategy, businesses and

performance of the Company and its subsidiaries (the “Group”) and the other matters described in this document. Generally, words such as ‘‘may’’, ‘‘could’’,

‘‘will’’, ‘‘expect’’, ‘‘intend’’, ‘‘estimate’’, ‘‘anticipate’’, ‘‘believe’’, ‘‘plan’’, ‘‘seek’’, ‘‘continue’’ or similar expressions are intended to identify forward-looking

statements.

Forward-looking statements involve inherent risks and uncertainties. They are not guarantees of future performance and actual results could differ materially

from those contained in the forward-looking statements. Recipients should not place reliance on, and are cautioned about relying on, any forward-looking

statements. Forward-looking statements are based on current views, estimates and assumptions and involve known and unknown risks, uncertainties and

other factors, many of which are outside the control of the Group and are difficult to predict. Such risks, factors and uncertainties may cause actual results to

differ materially from any future results or developments expressed or implied from the forward-looking statements. Such risks, factors and uncertainties

include but are not limited to: changes in the credit quality and the recoverability of loans and amounts due from counterparties; changes in the Group’s

financial models incorporating assumptions, judgments and estimates which may change over time; risks relating to capital, capital management and

liquidity; risks associated with implementation of Basel III and uncertainty over the timing and scope of regulatory changes in various jurisdictions in which

the Group operates; risks arising out of legal and regulatory matters, investigations and proceedings; operational risks inherent in the Group’s business; risks

arising out of the Group’s holding company structure; risks associated with the recruitment, retention and development of senior management and other

skilled personnel; risks associated with business expansion and engaging in acquisitions; reputational, compliance, conduct, information and cyber security

and financial crime risks; global macroeconomic and geopolitical risks; risks arising out of the dispersion of the Group’s operations, the locations of its

businesses and the legal, political and economic environment in such jurisdictions; competition; and other similar legislation or regulations; changes in the

credit ratings or outlook for the Group; market, interest rate, commodity prices, equity price and other market risk; foreign exchange risk; financial market

volatility; systemic risk in the banking industry and among other financial institutions or corporate borrowers; country risk; risks arising from operating in

markets with less developed judicial and dispute resolution systems; risks arising out of regional hostilities, terrorist attacks, social unrest or natural disasters;

risks arising out of health crises and pandemics, such as the COVID-19 (coronavirus) outbreak; climate related transition and physical risks; business model

disruption risks; and failure to generate sufficient level of profits and cash flows to pay future dividends.

Any forward-looking statement contained in this document is based on past or current trends and/or activities of the Company and should not be taken as a

representation that such trends or activities will continue in the future. No statement in this document is intended to be a profit forecast or to imply that the

earnings of the Company and/or the Group for the current year or future years will necessarily match or exceed the historical or published earnings of the

Company and/or the Group. Each forward-looking statement speaks only as of the date of the particular statement. Except as required by any applicable law

or regulations, the Company expressly disclaims any obligation or undertaking to release publicly or make any updates or revisions to any forward-looking

statement contained herein whether as a result of new information, future events or otherwise.

Nothing in this document shall constitute, in any jurisdiction, an offer or solicitation to sell or purchase any securities or other financial instruments, nor shall it

constitute a recommendation or advice in respect of any securities or other financial instruments or any other matter.

2

Key messages

We are a global bank with deep local expertise in many of the world’s most dynamic markets

our focus is on to …

Accelerate in areas where we have distinctive competitive advantage

Maintain discipline on costs and improve our productivity

Continue to strengthen our controls environment

Disrupt through digital: we are big enough to be relevant to clients and

partners yet nimble enough to innovate

…which we expect will deliver incremental profitable growth and substantial value for our clients

and shareholders

Leverage the global network and international expertise

3

Deliver our network

Grow our affluent business

Optimize returns

Improve Productivity

Transform and disrupt with digital

Pivot for future growth

Improve Productivity

✓ Re-align ourselves around client journeys to deliver on

#simplefasterbetter agenda

✓ Drive positive JAWS

✓ Continue to maintain strong cost discipline and seek

efficiencies to fund investments

Deliver our network

✓ Leverage the network as a key differentiator

✓ Monetize on opportunities arising out of CPEC (B&R)

✓ Capitalize on Client Eco-system opportunities

✓ Continue to build momentum in Sovereign, GS and FIs

Grow our affluent business

✓ Deepen opportunity and cross-sell in affluent and

emerging affluent segments

✓ Grow the Wealth Management business with superior

propositions

✓ Continue to mobilize low cost CASA and NTB acquisition

across all segments

Transform and disrupt with digital

✓ Invest in technology infrastructure & E2E Digital capabilities

✓ Pursue tailored digitization on existing tech stack

✓ Partnerships with fin-techs and tech-start-ups

✓ Digitize client value chains in collaboration with 3rd party

(B2B Fintech / PSP)

Optimize returns

✓ Invest in areas with high marginal ROI

✓ Continued focus on risk adjusted returns

4

2

3

1

4

• Serving over 1,000 global corporates, financial

institutions, SOEs and Government of Pakistan

• Contributes 30% to bank’s revenue

• YoY income growth of 15%

• Leverages on global footprint to offer unique

products and services to our clients

Corporate and

Institutional Banking

• Serving over 700 local corporates and medium

enterprises

• Contributes 11% to bank’s revenue

• YoY income growth of 27%

• End to end client solutions including cash

management, corporate finance, cross-border

solutions as well as employee banking

Commercial Banking

Retail Banking

• Serving over 700K customers

• Contributes 49% to bank’s revenue

• YoY income growth of 23%

• Efficient and productive network of 60 branches

• Diversified Asset basket with all asset products

• High digital adoption

Central & Other Items

• Comprising non client activities such as Treasury

Markets and some central functions

• Contributes 10% to bank’s revenue

• Treasury Markets income declined by 45% on

account of reduction in interest rates

Largest foreign bank serving all segments

• Serving over 100k customers and cuts across all businesses

• Contributes 13% to bank’s revenue and 24% to bank’s advances

• Bank leverages on Islamic Window model

• Operates under the global SC Islamic brand of “Saadiq”

Anchored on state of

the art and award

wining digital

solutions including:

✓ SC Mobile

✓ Online Banking

✓ Straight2Bank

✓ Straight2Banks FX

✓ CDMs/ CDKs

✓ QR Code Payments

✓ Block-chain based

remittance solutions

✓ Retail workbench

✓ Advanced Data

Analytics

✓ Robotic Process

Automation

✓ Fintech

Collaborations

5

Recent AchievementsAwards & Accolades

17TH Annual Excellence Awards by CFA Society Awards 2020

Best medium sized Bank

Best D&I Bank

Management Association of Pakistan Awards 2020

Best Commercial Bank

Global Diversity and Inclusion Benchmark Awards 2020

Best Practice Award in Vision , Strategy and D&I Learning and Education category

Progressive award in Benefits category

Progressive award in Communications and Integration & Flexibility category

Progressive award in Sustainability category

The Banker Magazine 2020

Best Islamic Bank

Asset Triple A - Islamic Finance Awards 2020

Best Treasury, Trade, SSC and Risk

Global Finance 2020

Best Consumer Digital Bank

Best Sub-Custodian Bank

Management Association of Pakistan Awards 2019

Best Commercial Bank

Asia Money 2019

Best International Bank

Best Bank for Premium Services

Finance Asia 2018/2019

Best Foreign Bank in Pakistan6

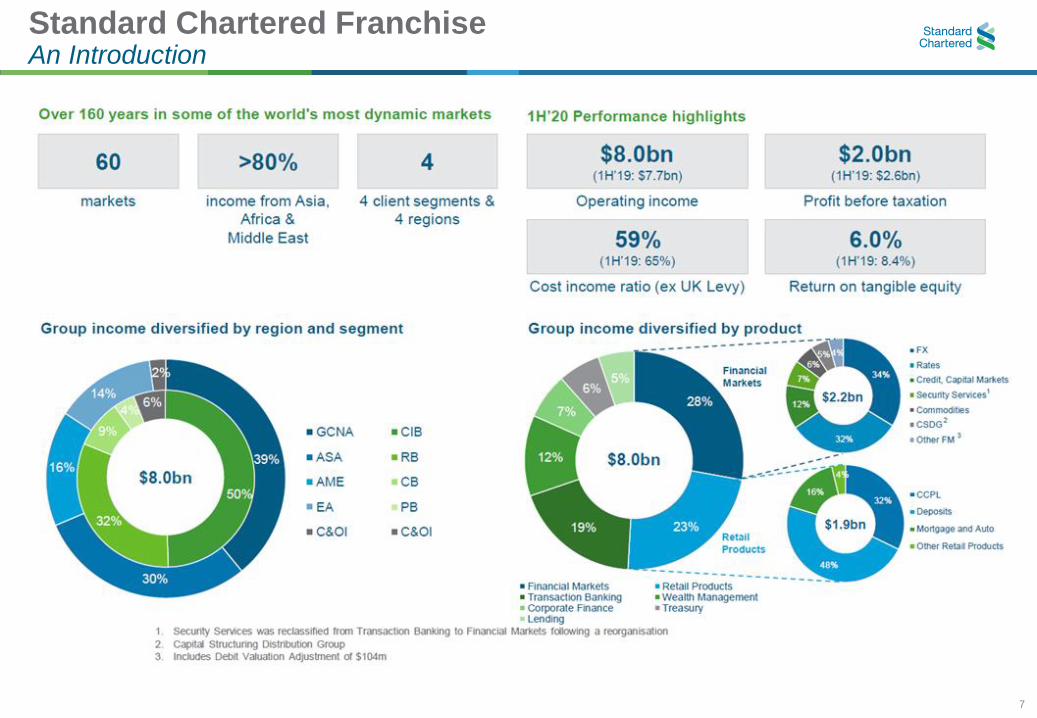

Standard Chartered FranchiseAn Introduction

7

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Dividend PKR - Bn Divdend %

Strong fundamentals

86%14%

2011

2020

220 236267

297304 327 366

378

425466

570

0

10 0

20 0

30 0

40 0

50 0

60 0

25

Segments

* Based on H1’20 peer banks analysis

CIB 30%

CB 11%RB 49%

COI 10%

8

Our Financials

9

YTD Sep 2020 ResultsDriving through challenges

Capital Adequacy

Ratio of 18.99%

Positive jaws of

9% with cost

marginally up by

3%

Resilient

profitability of

PKR 11.9bn (up

4% y/y)

Total income

of PKR 32.1bn (up 12% y/y) and

Client income

of PKR 26.4bn(up 19% y/y)

Total assets

crossed over

PKR 700bn and

Total deposits

crossed over

PKR 550bn

Overall loss

coverage ratio

remains adequate

at 94%

10

PKR Million YTD Sep 2020 YTD Sep 2019 Var %

Net Interest Income 22,170 20,229 10%

Non Interest Income 9,906 8,389 18%

Revenue 32,076 28,618 12%

Operating expenses (excl. SLA) (8,876) (8,595) 3%

SLA & Royalty net - -

Total operating expenses (8,876) (8,595) 3%

Profit before tax and provisions 23,200 20,023 16%

(Provisions)/ Recoveries against loans and advances (3,174) (131) 2331%

Provision for diminution in the value of investments - (52)

Other Provisions (52) (68) -23%

Profit before tax 19,974 19,773 1%

Taxation (8,066) (8,340) -3%

Profit after tax 11,908 11,433 4%

EPS - Rupees 3.08 2.95

ROA 2.4% 2.6%

ROE 20.9% 22.5%

CI Ratio 27.7% 30.0%

Income StatementMaintaining the set bar

▪ Double digit revenue growth; up 12%

y/y to PKR 32.1bn

▪ Revenue growth in all segments; led

by CB (27% y/y) & RB (23% y/y)

▪ Total expenses up marginally by 3%

▪ Additional General Provision of PKR

1.7bn booked to counter COVID

cycle

▪ Resilient PBT of PKR 19.9bn (up 1%)

and PAT of PKR 11.9 (up 4%) y/y

▪ Double digit RoE of 20.9%

▪ Lowest CI ratio in the industry;

reflective of bank’s productivity and

efficient delivery model

11

PKR Million

ASSETS

Cash and balances with banks 70,220 64,775 8%

Lendings to financial institutions 84,051 17,012 394%

Investments – net 337,152 249,164 35%

Advances – net 178,603 218,087 -18%

Intangible assets 26,095 26,095 0%

Other assets 31,842 44,837 -29%

TOTAL ASSETS 727,962 619,971 17%

LIABILITIES

Borrowings from financial institutions 21,324 20,257 5%

Deposits and other accounts 569,698 465,629 22%

Other liabilities 58,116 61,168 -5%

TOTAL LIABILITIES 649,137 547,054 19%

Equity 78,825 72,917 8%

AD Ratio (Country) 31.4% 46.8%

AD Ratio (LCY) 36.9% 56.3%

CAR 18.99% 16.94%

CASA 94.0% 93.1%

Var %Sep-20 Dec-19

Balance SheetWell capitalized and liquid

▪ Growth momentum in underlying balance sheet

continues; Total assets at PKR 728bn, up by PKR

108bn or 17% from Dec 19

▪ Advances (net) reduced by PKR 40bn or 18% at

close of Q3 2020 mainly due to large settlements

and subdued credit demand due to COVID-19

▪ Advances book remains short-term ~ 62% under

one year focusing on trade and working capital

lines at improved returns

▪ Current investment profile balanced with T-Bills

and PIBs/ Sukuks comprising 51% and 49%

respectively

▪ Total loss coverage ratio 93.7% (specific provision

82%)

▪ Deposit growth of PKR 104bn or 22% till Q3’20.

Focus on low cost and sticky CASA

▪ Strong and liquid balance sheet with LCY and Total

AD ratio of 36.9% and 31.4%

▪ Bank remains adequately capitalized with CAR of

18.99%

12

Punching above its weight

2nd

# Rank # Branches # RankMarket

Share# Rank

Market

Share# Rank

Market

Share# Rank

Market

Share# Rank

Market

Share

Branches Loans Deposits IncomeOperating

Profit

Income from

dealing in FX

-2%

-7% -8% -7%

4%1%

-3%

-11%

-3%

11%

-14%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

0

200

400

600

800

1,000

1,200

HBL NBP UBL MCB BAHL BAFL MEBL ABL FABL HMB SCB

Advances analysis

Net Advances Net Advances Growth

10%

6%

8%

11%

5%

15%

12%

3%

-2%

8%

17%

-5%

0%

5%

10%

15%

20%

0

500

1,000

1,500

2,000

2,500

3,000

HBL NBP UBL MCB ABL BAHL MEBL BAFL HMB FABL SCB

Deposits analysis

Deposits Deposits Growth

Based on H1’2020 peer banks analysis

HBL NBP UBL MCB BAHL BAFL MEBL ABL FABL HMB SCB

NPL Ratio 7% 15% 13% 10% 2% 5% 2% 3% 9% 6% 10%

Loss Coverage 97% 95% 87% 94% 143% 92% 129% 107% 84% 104% 87%

13

Potential

headwinds

Potential

tailwinds

▪ Covid-19 second wave likely to impact global economy and different segments that

we cater to

▪ Challenging external environment marred by global trade and territorial tensions, oil

price volatility, currency pressures, FATF placement as well as tough domestic

economic situation

▪ Recent political developments in the country may impact path to recovery

▪ Geopolitical events including US presidential elections

▪ Economic momentum gradually building up with positive sentiments in the market

▪ Focus on financial inclusion and documentation of economy will result in more

bankable clients

▪ Low interest-rate regime supporting financial stability and credit off-take

▪ Increase in exports, continued expansion of CPEC project, Housing and Construction

Finance pick-up and inflows in RDA

14

Community

Investments

Here for Good

15

Embedded in the community

EDUCATION

EMPLOYABILITY

ENTREPRENEURSHIP

We will empower the next generation to learn, earn and grow through

programmes focused on education, employability and entrepreneurship

Empowering adolescent girls with life skills

Employability work readiness and vocational

training schemes for youth

Provide training, capacity building and financing

16

Who will benefit

EDUCATION

EMPLOYABILITY

ENTREPRENEURSHIP

Globally, we will support disadvantaged young people from low-income

households, particularly girls and people with visual impairments

Empowering adolescent girls with life skills

Employability work readiness and vocational training

schemes for youth

Provide training, capacity building and financing

500,000

adolescent girls

100,000

youth for work

50,000

micro & small

businesses

Adolescent girls aged 12 to 19 from low-income backgrounds

Youth aged 16 to 30, prioritising women and people with visual impairments

Micro and small business owners, prioritising women

Reach between 2019 – 2023

17

What are we doing in Pakistan

EDUCATION EMPLOYABILITY

ENTREPRENEURSHIP

SC-KU YOUTH FOOTBALL LEAGUE

18

![[ PowerPoint Template ]](https://static.fdocuments.us/doc/165x107/56814853550346895db565d2/-powerpoint-template--5697ba40150e6.jpg)