New Jersey State Investment Council Annual Meeting … · New Jersey State Investment Council...

49

New Jersey State Investment Council Annual Meeting FY 2009 Investment Environment and Results William G. Clark, Director New Jersey Division of Investment November 19, 2009

Transcript of New Jersey State Investment Council Annual Meeting … · New Jersey State Investment Council...

New Jersey State Investment CouncilAnnual Meeting

FY 2009 Investment Environment and Results

William G. Clark, DirectorNew Jersey Division of Investment

November 19, 2009

Outline

Summary of Market Environment

Portfolio Actions During FY09

FY09 Performance

Performance by Asset Class

FY 2010 So Far

Concluding Thoughts

Market Returns for FY 2009Ending June 30, 2009

1 Year 3 Years 5 Years

US Equities

S&P 1500 Index -26.34 -8.23 -1.97

International Equities

MSCI EAFE ex-prohibited -31.17 -8.14 2.20

Emerging Markets Equities

MSCI Emerging Markets Index -25.23 3.56 14.88

Investment-Grade Bonds

Barclays US Treasuries Index 6.47 7.41 5.46

Barclays Corporate Index 3.84 4.49 3.82

Barclays Mortgage Backed Index 9.38 7.86 5.98

High Yield Bonds

Barclays High Yield Index -2.43 2.09 4.33

Market Returns for FY 2009Ending June 30, 2009

1 Year 3 Years 5 Years

Commodities

DJUBS TR Index -47.09 -8.30 -0.23

Private Equity* -22.00 3.00 12.17

Real Estate

NCREIF Property Index -19.57 0.98 7.66

Hedge Funds

HFRI Funds of Funds Index -15.24 -1.13 2.62

Cash

90 Day US T-Bill Index 0.80 3.04 3.02

These returns do not fully capture the impact of the “shock” to the financial markets and the economy.

The return on US stocks for FY09 was the lowest since 1932

-

20

40

60

80

100

120

S&P 500 Index June 2007 – June 2009

More importantly, the ten year annualized return on stocks was negative for the first time since the 1930’s

-10%

-5%

0%

5%

10%

15%

20%

25%

Rolling 10 yr return

S&P 500 Index Rolling Ten Year Return

Emerging market equity returns were slightly better than global equities because of the weakening U.S. dollar and the superior financial position of

many emerging markets countries

0

20

40

60

80

100

120

140

MSCI EAFE MSCI EM

MSCI EAFE and Emerging Markets Return June 2007 – June 2009

The credit markets were hit even harder by the “seizing up” of the global financial system

Option Adjusted Spread (bps)

Source: Barclays Capital; History Through August 31, 2009, monthly data

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Aug-99 Aug-00 Aug-01 Aug-02 Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09

0

200

400

600

800

1000

1200

U.S. Corporate Investment Grade

U.S. Corporate High Yield

High Yield: +849 bps

Investment Grade: +232 bps

Incremental Yields on U.S. Corporate Bonds vs. U.S. Treasuries 1999 - 2009

The market was reacting to the economy falling off a cliff

(3-Month Percent Change Annualized, September to December)

(79%)

(47%) (46%)

(37%)

(29%)

(9%)

Housing Starts Durable Goods

Orders

New Home Sales Exports Retail Sales Industrial

Production

Source: U.S. Census, Bureau of Economic Analysis, Gluskin Sheff

Warren Buffett, October 1, 2008, PBS “The Charlie Rose Show”

“The long-feared

capitulation of

American consumers

has arrived”

— October 31, 2008

How did the consumer respond?

―Something is definitely going on.

We’re back to eating dog food.‖

How did the consumer respond?

What Brought the Global Financial MarketsBack From the Brink

Monetary Stimulus

Fiscal Stimulus

Other Government Intervention

The Federal Reserve and other Central Banks cut short-term interest rates to unprecedented levels

01

234

5678

9101112

13141516

FED BOE ECB BOJ

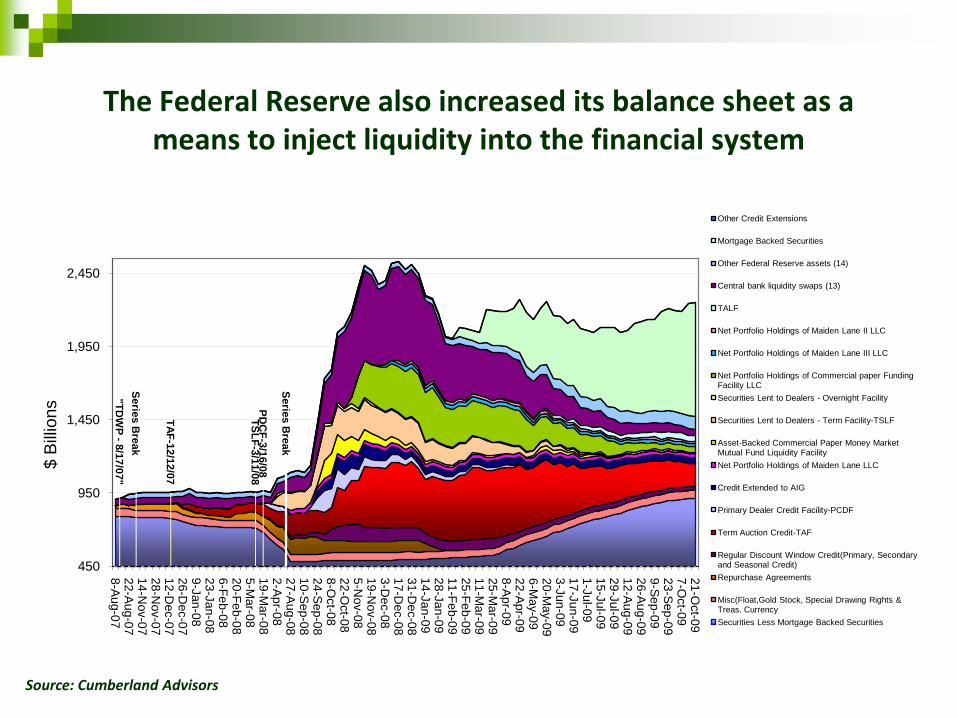

The Federal Reserve also increased its balance sheet as a means to inject liquidity into the financial system

"T

DW

P -

8/1

7/0

7"

TS

LF

-3/1

1/0

8P

DC

F-3

/16/0

8

Serie

s B

reak

TA

F-1

2/1

2/0

7

Serie

s B

reak

450

950

1,450

1,950

2,450

8-A

ug

-07

22

-Au

g-0

71

4-N

ov-0

72

8-N

ov-0

71

2-D

ec-0

72

6-D

ec-0

79

-Ja

n-0

82

3-J

an

-08

6-F

eb

-08

20

-Fe

b-0

85

-Ma

r-08

19

-Mar-0

82

-Ap

r-08

27

-Aug

-08

10

-Se

p-0

82

4-S

ep

-08

8-O

ct-0

82

2-O

ct-0

85

-No

v-0

81

9-N

ov-0

83

-De

c-0

81

7-D

ec-0

83

1-D

ec-0

81

4-J

an

-09

28

-Ja

n-0

91

1-F

eb

-09

25

-Fe

b-0

91

1-M

ar-0

92

5-M

ar-0

98

-Ap

r-09

22

-Ap

r-09

6-M

ay-0

92

0-M

ay-0

93

-Jun

-09

17

-Ju

n-0

91

-Ju

l-09

15

-Ju

l-09

29

-Ju

l-09

12

-Au

g-0

92

6-A

ug

-09

9-S

ep

-09

23

-Se

p-0

97

-Oct-0

92

1-O

ct-0

9

$ B

illio

ns

Other Credit Extensions

Mortgage Backed Securities

Other Federal Reserve assets (14)

Central bank liquidity swaps (13)

TALF

Net Portfolio Holdings of Maiden Lane II LLC

Net Portfolio Holdings of Maiden Lane III LLC

Net Portfolio Holdings of Commercial paper Funding Facility LLC

Securities Lent to Dealers - Overnight Facility

Securities Lent to Dealers - Term Facility-TSLF

Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility

Net Portfolio Holdings of Maiden Lane LLC

Credit Extended to AIG

Primary Dealer Credit Facility-PCDF

Term Auction Credit-TAF

Regular Discount Window Credit(Primary, Secondary and Seasonal Credit)

Repurchase Agreements

Misc(Float,Gold Stock, Special Drawing Rights & Treas. Currency

Securities Less Mortgage Backed Securities

Source: Cumberland Advisors

Both developed and emerging countries injected massive amounts of fiscal stimulus into their economies

3.4%

0.0%

0.3%

0.5%

1.0%

1.3%

1.3%

1.5%

1.7%

1.7%

2.2%

2.4%

2.6%

2.8%

2.8%

3.5%

4.4%

4.5%

5.0%

5.9%

9.2%

0% 2% 4% 6% 8% 10%

G-20

Turkey

Italy

Brazil

Mexico

France

Argentina

U.K.

Russia

India

Japan

Indonesia

South Africa

Korea

Canada

Germany

China

Australia

Spain

U.S.

Saudi Arabia

Fiscal Stimulus as a % of GDP

Various other steps taken by the government also helped to unfreeze the financial market

TARP related capital infusions into systemically important financial institutions

Increase in FDIC deposit insurance limits

Extension of FDIC guarantees to inter-bank loans and to certain public debt issuances

The “Alphabet Soup” of Government Responses

TAF TALF

TSLF TARP

PDCF CAP

AMLF MMIFF

CPFF PPIF

TLGP PPIP

TMMGP SCAP

Concern #1: Is the U.S. Economy becoming too dependent on monetary stimulus?

Long-Term Interest Rates: Choke Points Have Been Progressively Lower

Double

dip

14

12

10

8

6

4

80 85 90 95 2000 05 10

14

12

10

8

6

4

U.S. 10-Year Government Bond Yield

% %

S&L

crisisMid-cycle

slowdown

Mexican

peso crisis Burst tech

bubble Burst

real estate

bubble

© BCA Research 2009

Concern #2: After the fiscal stimulus wears off, then what?

Impact of ARRA 2009 on the Growth of GDP

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2009.1 2010.1 2011.1 2012.1 2013.1 2014.1 2015.1 2016.1 2017.1

Source: Macroeconomic Advisers, LLC

Ann

ualiz

ed P

erce

nt C

hang

e

1-Quarter

4-Quarter

From ―Fiscal Stimulus to the Rescue – Final Answer‖

(MA’s MACRO FOCUS, February 19, 2009)

Concern # 3: The level of fiscal stimulus is unprecedented and unsustainable

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09 12

USA Federal Budget Deficit %PGDP 1yr moving avg BW Forw ard-Looking Estimate

How much more debt can the Government issue?

Concern # 4: The debt levels of both U.S. consumers and businesses remain at all-time high

1.1

1.12

1.14

1.16

1.18

1.2

1.22

1.24

1.26

1.28

1.3

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08

Household Leverage

Leverage levels at highs

Source: Bridgewater

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08

Non-Financial Business Leverage

Leverage levels at highs

Concern # 4: Growth in consumer spending is likely to remain low as the savings rate rises

0

2

4

6

8

10

12

14

16US Savings Rate %

Concern # 5: Growth in capital spending will be impacted by the spare production capacity already in the system

50

55

60

65

70

75

80

85

90

95

100

Policy objective is to replace private sector debt with public sector borrowing to maintain an “acceptable” level of growth while U.S.

consumers and businesses continue to “delever”

15

10

5

0

70 75 80 85 90 95 2000 05 10

15

10

5

0

U.S. Net Issuance*: Non-Government Debt Gov ernment Debt

% of GDP

% of GDP

* Source: Flow of Funds data.Note: Shaded areas represent NBER-designated periods of recession.

© BCA Research 2009

Change in New Jersey’s Portfolio During FY 2009

Asset Class June 08 June 09 Difference

US Equities 30.8% 25.9% -4.9%

International Equities 17.4% 17.4% 0.0%

Emerging Markets Equities 1.4% 1.9% 0.5%

US Fixed Income 24.1% 29.3% 5.2%

US High Yield 0.9% 2.4% 1.5%

International Fixed Income 2.7% 0.1% -2.6%

Commodities/Real Assets 1.2% 1.0% -0.2%

TIPS 4.5% 5.2% 0.7%

Private Equity 3.4% 4.6% 1.2%

Real Estate 2.4% 2.8% 0.4%

Absolute Return 4.2% 4.3% 0.1%

Cash 7.0% 5.1% -1.9%

Actual $ Millions $78,201 $63,179

FY 2009 Net Purchases/Sales by Quarter

(1,500,000)

(1,000,000)

(500,000)

-

500,000

1,000,000

1,500,000

2,000,000

9/08 12/08 3/09 6/09 9/09

Tho

usa

nd

s

Domestic Equities Domestic Fixed Income Int'l Equities

Notable portfolio moves during FY 2009

Purchase of $2.5 billion of investment grade corporate bonds in August 08 –March 09. Result: Up 21% from November 08 – June 09

Made additional investments of $243 million in several bank loans funds in October 08 in response to margin calls to prevent forced liquidation of nearly $750 million in positions. Result: Up 19% from October 08 – June 09

Bought $2.6 billion in Japanese equities as a means to capitalize on a likely global economic recovery. Result: Too early to tell

In January 2009 cancelled five commitments totaling $365 million to private equity and real estate funds and redeemed $200 million from two hedge fund investments. Result: Preserved liquidity to take advantage of better opportunities in other asset classes

Estimated FY 2009 Performance

Asset Class Actual Benchmark Difference

US Equities -22.84 -26.34 3.5

International Equities -31.17 -31.17 0

Emerging Markets Equities -28.37 -25.40 -2.97

US Fixed Income 6.64 7.38 -0.74

US High Yield 10.38 -2.40 12.78

Mortgages 12.35 9.38 2.97

International Fixed Income 19.73 8.54 11.19

Commodities -43.03 -47.09 4.06

TIPS -3.99 -1.12 -2.87

Private Equity* -25.89 -25.20 -0.69

Absolute Return -17.70 -13.02 -4.68

Real Estate* -32.38 -15.16 -17.22

Cash 1.58 0.80 0.78

Overall Portfolio -14.20 -16.47 2.27

* Returns are through 3/31/09

The Division also exceeded its respective benchmarks in each of its internally managed portfolios over the previous 3 and 5 year periods as well

1-Year 3-Years 5-Years

US Equities -22.84 -5.80 -0.15

Benchmark -26.34 -8.18 -1.94

International Equities -23.98 -3.89 4.71

Benchmark -31.17 -8.14 2.20

US Investment Grade Fixed Income 6.64 7.02 5.52

Benchmark 7.38 6.19 4.85

Annualized Returns

For FY 2009, New Jersey was the top performing fundin the country

State FundFY 09 Estimated

Performance

New Jersey DOI -14.2%

CalSTRS -25.0%

Florida -19.0%

Illinois Teachers -22.3%

North Carolina -14.2%

Ohio Teachers -21.7%

Pennsylvania School Employees -26.5%

Texas Teachers -21.9%

Wisconsin SIB -17.7%

Average of 44 State Funds that have reported FY09 results -19.6%

Over the longer term, New Jersey has consistentlyout-performed its peer group

1 Year 3 Years 5 Years

New Jersey -14.20% -0.73% 3.16%

Wilshire TUCS Category

All Master Trusts -17.00% -2.51% 2.06%

Public Funds -17.06% -2.69% 2.19%

All Master Trusts with Assets > $1 billion -18.13% -2.60% 2.45%

Public Funds with Assets > $1 billion -18.76% -2.69% 2.36%

All Master Trusts with Assets > $5 billion -18.76% -2.47% 2.64%

Public Funds with Assets > $5 billion -18.76% -2.77% 2.41%

Note: Outperformance of 1% for one year equates to $700 million inportfolio value

Putting the Year in PerspectiveThe Division had minimal or no exposure to…..

Debt

Subprime Mortgage Securities

Non-agency Mortgage Backed Securities

CDOs

Asset Back Commercial Paper/SIVs

Student Loan Paper

Equities

Mortgage Brokers

Monoline Insurers

Student Loan Issuers

Thrifts/S&L’s

Auto Makers (GM/Ford)

Freddie Mac/Fannie Mae Common Stock

Rating Agency Stocks (Moody’s & McGraw Hill)

Bear Stearns

S&P 500FY 2009 Returns by Sector

SectorS&P 500

FY09 Returns

Consumer Discretionary -16.60

Consumer Staples -10.20

Energy -41.34

Financials -37.33

Health Care -11.49

Industrials -34.47

Information Technology -18.03

Materials -38.79

Telecommunication Services -19.24

Utilities -28.23

Total -25.82

Energy, Materials and Financials were the biggest drag on the market. We were significantly underexposed to financials for the entire fiscal year.

For FY 2009 “Success” was defined by “Dodging Bullets”

# of Stocks inDOI Universe % Examples

Down >50% 420 20.7% LehmanWashington Mutual

FNMA/FHLMCCitigroup

GMLiz Claiborne

AlcoaCBS

Down 25% - 50% 545 26.8% ChevronBank of America

MonsantoMedtronic

Down 0% - 25% 605 29.8% Exxon MobilProcter & Gamble

MicrosoftJohnson & Johnson

UP 463 22.7% JP Morgan ChaseWells Fargo

OracleMcDonald’s

MSCI EAFE ex-ProhibitedFY 2009 Returns by Sector

SectorMSCI EAFE ex-Prohibited

FY09 Returns

Consumer Discretionary -22.54

Consumer Staples -18.15

Energy -32.72

Financials -36.25

Health Care -19.34

Industrials -32.71

Information Technology -29.84

Materials -44.62

Telecommunication Services -21.99

Utilities -29.98

Total -30.85

Energy, Materials and Financials were also the worst-performing sectors in the international markets. We were significantly

under-exposed to Financials in this portfolio as well.

Emerging market equities rebounded the most in 2009. We are evaluating whether it makes sense to increase our very small

exposure to this asset class.

0

20

40

60

80

100

120

140

S&P 500 MSCI EAFE MSCI EM

Domestic Fixed Income: Participating in the significant turn in High Grade and High Yield Credit was the key to strong performance

FY 2009 Performance by Quarter

BarclaysLong Govt/Credit

BarclaysLong Treasuries

BarclaysLong Credit

BarclaysHigh Yield

July - Sept -3.40 2.82 -8.78 -8.89

Oct - Dec 13.06 18.66 8.16 -17.88

Jan – March -6.16 -5.23 -6.94 5.98

April - June 2.78 -7.14 12.93 12.07

While inflation does not seem to be an imminent threat, both Commodities and TIPS have rebound nicely from their lows in the Fall of 2009

0.00

0.50

1.00

1.50

2.00

2.50

3.00

TIPS Breakeven Inflation SpreadCommodities

-40

-30

-20

-10

0

10

20

30

S&P GSCI TR (%Total Return)

New commitments to Private Equity have slowed in 2009

New Commitments

Source: Thomson Venture EconomicsTM as of June 2009

(US$ in billions)

$93$63

$39 $47 $65

$163$215

$259 $240

$38

$213

$124

$59 $49

$82

$143

$187

$245$242

$52

$0

$100

$200

$300

$400

$500

$600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 YTD

Global buyouts Global private equity ex buyouts

While total 2008 fundraising remained strong, there were significantly fewer commitments in 1H 2009 as the broader market went through a downturn

Private Equity: While recent performance has been disappointing, our portfolio is significantly under exposed to the mega-buyout funds, which

were the worst-performing sector of the market

25%

37%

12%

14%

6%

4% 2% 0%

NJDOI PE allocation

LBO

MMBO /SMBO

Distressed

International Buyouts

Mezzanine

Secondaries

Venture Capital

Other

48%

10%

10%

19%

2%

1%

9% 5%

Avg of 4 largest US Pension plans

LBO

MMBO /SMBO

Distressed

International Buyouts

Mezzanine

Secondaries

Venture Capital

Other

Real Estate: The pace of the current correction is unprecedented

65

70

75

80

85

90

95

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

Cap

ital

Val

ue

fro

m P

eak

Quarters from Peak

Peak to Trough Write-downs for US Real Estate (NFI-ODCE)Previous Major Correction vs Current through 2nd Qtr Prelim

1990-1994 Correction

Cumulative write-downs over the last three quarters equals five years of the 1990’s downturn

Source: The Townsend Group

Long-Term Real Estate Indices

All sectors show a material correction The premium for taking risk has evaporated (traditional core now outperforming)

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Real Estate Indices - Rolling Five Year ReturnsAs of June 30, 2009

NCREIF Property Index NCREIF-Townsend High Return Fund Index EPRA/NAREIT Global REIT Index

Source: The Townsend Group

Hedge Funds have rebounded in 2009 as liquidity and market conditions improved

Hedge Fund Performance %

Hedge Fund Style July – December 08 January – June 09

Fund of Funds -19.36 4.27

Credit - Other -33.13 7.95

Credit - Loan Funds -47.11 50.38

Distressed -16.75 14.12

Event Driven -21.09 9.06

Equity Long/Short -21.69 14.48

Multi-Strategy -26.42 12.74

Over The Long Run, Hedge Funds Have Experienced Lower Volatility Than Public Equities

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

S&P 500 Index

HFRI (Hedge Fund) Fund Weighted Index

Rolling 12 Month Returns: 1994 – July 2009

FY 2010 So Far

Asset Class June 09 ($mm) September 09 ($mm)

US Equities 16.4 17.6

International Equities 11.0 12.8

Emerging Markets Equities 1.2 1.2

US Fixed Income 18.5 19.2

US High Yield 1.5 1.7

International Fixed Income 0.0 0.0

Commodities/Real Assets 0.6 0.7

TIPS 3.3 3.7

Private Equity 2.9 3.1

Real Estate 1.8 1.6

Absolute Return 2.7 2.8

Cash 3.2 3.6

Total 63.2 68.2

FY 2010 Investment Performance ThroughSeptember 30, 2009

Asset Class Performance % Benchmark %

US Equities 15.19 16.06

International Equities 19.30 20.03

Emerging Markets Equities 22.57 21.96

US Fixed Income 9.34 8.53

US High Yield 15.52 14.22

International Fixed Income 6.07 2.03

Commodities/Real Assets 4.95 4.24

TIPS 2.79 3.08

Private Equity NA NA

Real Estate NA NA

Absolute Return 6.91 4.11

Cash 0.14 0.04

Total 11.62 11.99

Current Division staff dedicated to internal management

6/30/2009 InvestmentAmount ($mm)

InvestmentProfessional FTEs*

Asset Per InvestmentProfessional ($mm)

Cash Management 14,563 2.5 5,825

Domestic Fixed Income 21,832 1.5 14,555

Subtotal – Fixed Income 36,395 4.0 9,099

Domestic Equity 16,351 8 2,044

Int’l Equity 11,022 4 2,756

Subtotal – Public Equity 27,373 12 2,281

Total 63,768 16 3,986

•Excludes Director and Deputy DirectorFigures are unaudited and are subject to change