New Feature for Deutsche Bank Financial Information Systempeople.duke.edu/~lde2/Posters/DBPoster7...

1

New Feature for Deutsche Bank Financial Information System Chao Chen, Jay Choi, Ruoyan Qin, Gowri Rao Krishnamurthy, Lin Gui, Amrit Anand Vanchinathan Pratt School of Engineering, Duke University Duke University Center for Quantitative Modeling 1 Background & Introduction The “dbRadar” provides alerts on important market trends to Deutsche Bank’s Sales and Trading desks. It is used on a daily basis by more than 1800 professionals worldwide. In the fall of 2010, Deutsche Bank challenged a student team at Duke’s Master of Engineering Management Program to develop a new form of alert for dbRadar. This new alert will signal maximum opportunities for excess returns through active management – “alpha” – in emerging market (EM) equities. Building on the cross-sectional correlation measure proposed in Solnik (2000), we tested a variety of related measures. The measure described here reliably identifies both maximum market dispersion, or active investment opportunity (low mean Solnik Correlation) and maximum market herding or concentration, or minimum active investment opportunity (high mean Solnik Correlation) among the 21 EM country indices evaluated. Chart 1. Weekly Difference of Country Returns Against EMF Index 3 Statistical Method We decided to use Solnik’s Model describing the cross-sectional correlation. The cross-sectional method of estimating global correlation was dynamic, and gives instantaneous information about change in the level of global correlations. Note that Solnik (2000) recommends, but does not demonstrate, using a rolling calculation for the Beta of each country index against the world index, and for the standard deviation of world returns and tracking error and world volatility of returns. After evaluating a number of alternatives, we settled on a rolling 24 weeks data for each. Solnik (2000) estimates the “world” return benchmark as the equal-weighted mean of all country returns, which may overweight small markets; we chose to substitute the market-capitalization weighted EMF index. , 2 2 2 1 1 iw e i w ρ σ βσ = + ρ i,w : Correlaon between certain market and world index σ w : Standard deviaon of world index σ e : Standard deviaon of tracking error 2 Data Analyzed Deutsche Bank provided daily country index data, in local currencies, for 21 EM countries, covering the time period from November 2006 to July 2010. (The included countries are listed in Chart 1). Data were converted, using Wednesday closing prices, to a time series of one-hundred eighty-six (186) weekly returns. Weekly local currency returns were then normalized to dollar-denominated returns using the US Dollar exchange rate against each local currency each week. We calculated excess returns for each country as the difference between that country’s dollar-denominated index return, and a benchmark representing the worldwide total Emerging Market return. Chart 1 shows absolute returns for all 21 countries, and Charts 2-4 show the weekly differences between the 21 countries’ index returns and the return of the MSCI Emerging and Frontier Markets (EMF) Index. In our data-set of 186 weeks, the maximum weekly cross-sectional standard deviation of country returns was 11.2% (Chart 2) the median was 2.6% (Chart 3), and the minimum was 1.1% (Chart 4). 6 References 1. Bruno Solnik, Jacques Roulet. 2000. Dispersion as Cross-Sectional Correlation. Financial Analysts Journal, Vol. 56, No. 1 pp. 54-61 (Jan. - Feb., 2000) 2. Daniel Egger, Jai Jacob. 2010. Emerging Markets: Return Dispersion and Portfolio Concentration. LazardNet.com 03/10 HB00226. Table 2. Threshold Values 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 1.1 0 5 10 15 20 25 30 35 Frequency Upper Threshold: 0.84 Lower Threshold: 0.57 Total weeks: 163 Chart 5. Histogram of 163 Weeks of Mean Solnik Correlations 0.00 30.00 60.00 90.00 120.00 150.00 180.00 Hungary (Budapest) Brazil Czech Republic Indonesia Malaysia Mexico Phillipines Oct-06 May-07 Aug-08 Jan-08 Jul-10 Dec-09 Apr-09 Chile China (Shanghai) South Korea Taiwan Colombia Egypt India Morocco Peru Poland Russia (Moscow) South Africa Thailand Turkey 5 Acknowledgments This Project would not have been possible without the sponsorship of Deutsche Bank. Thanks to Daniel Egger, Director of Duke's Center for Quantitative Modeling, for mentoring this project. Special thanks to William Calhoun, John Eagleson, Brett Josloff, Brianne Sullivan, and Nithin Varam at the DBGT in Cary, NC. Chart 2. Weekly Cross-Sectional Dispersion of Returns (Maximum) 20.0% Russia (Moscow) = 10.6% 0 0% 10.0% -10.0% 0.0% -20.0% -30.0% China (Shanghai) = 47 0% -40.0% China (Shanghai) = -47.0% -50.0% 07-Oct- 4 1 9 0 -Oct-09 Chart 3. Weekly Cross-Sectional Dispersion of Returns (Median) 20.0% South Africa = 9 3% 0 0% 10.0% South Africa = 9.3% -10.0% 0.0% Chile = -1.1% -20.0% -30.0% -40.0% -50.0% 24-Feb- 3 0 0 1 -Mar-10 Chart 4. Weekly Cross-Sectional Dispersion of Returns (Minumum) 20.0% 0 0% 10.0% Morocco = 3.4% -10.0% 0.0% Budapest = -0.8% -20.0% -30.0% -40.0% -50.0% 24-Mar- 1 3 0 1 -Mar-10 S D U p p e r T h r e s h o l d L o w e r T h r e s h o l d A n n u a l E x p e c t e d A l e r t s +/- 2σ 0.97 0.44 3 +/- 1.5σ 0.91 0.51 7 +/- σ 0.84 0.57 16 +/- 0.5σ 0.77 0.64 30 4 Conclusion The mean Solnik Correlation were near normally distributed around the average of 0.71, ranged from a low of 0.25 to a high of 0.97, with a standard deviation of 0.13. Alerts +/-σ would occur about 16 times a year.

Transcript of New Feature for Deutsche Bank Financial Information Systempeople.duke.edu/~lde2/Posters/DBPoster7...

New Feature for Deutsche Bank Financial Information SystemChao Chen, Jay Choi, Ruoyan Qin, Gowri Rao Krishnamurthy, Lin Gui, Amrit Anand Vanchinathan

Pratt School of Engineering, Duke University

Duke University Center for Quantitative Modeling

1 Background & IntroductionThe “dbRadar” provides alerts on important market trends to Deutsche Bank’s Sales and Trading desks. It is used on a daily basis by more than 1800 professionals worldwide.

In the fall of 2010, Deutsche Bank challenged a student team at Duke’s Master of Engineering Management Program to develop a new form of alert for dbRadar. This new alert will signal maximum opportunities for excess returns through active management – “alpha” – in emerging market (EM) equities. Building on the cross-sectional correlation measure proposed in Solnik (2000), we tested a variety of related measures.

The measure described here reliably identifies both maximum market dispersion, or active investment opportunity (low mean Solnik Correlation) and maximum market herding or concentration, or minimum active investment opportunity (high mean Solnik Correlation) among the 21 EM country indices evaluated.

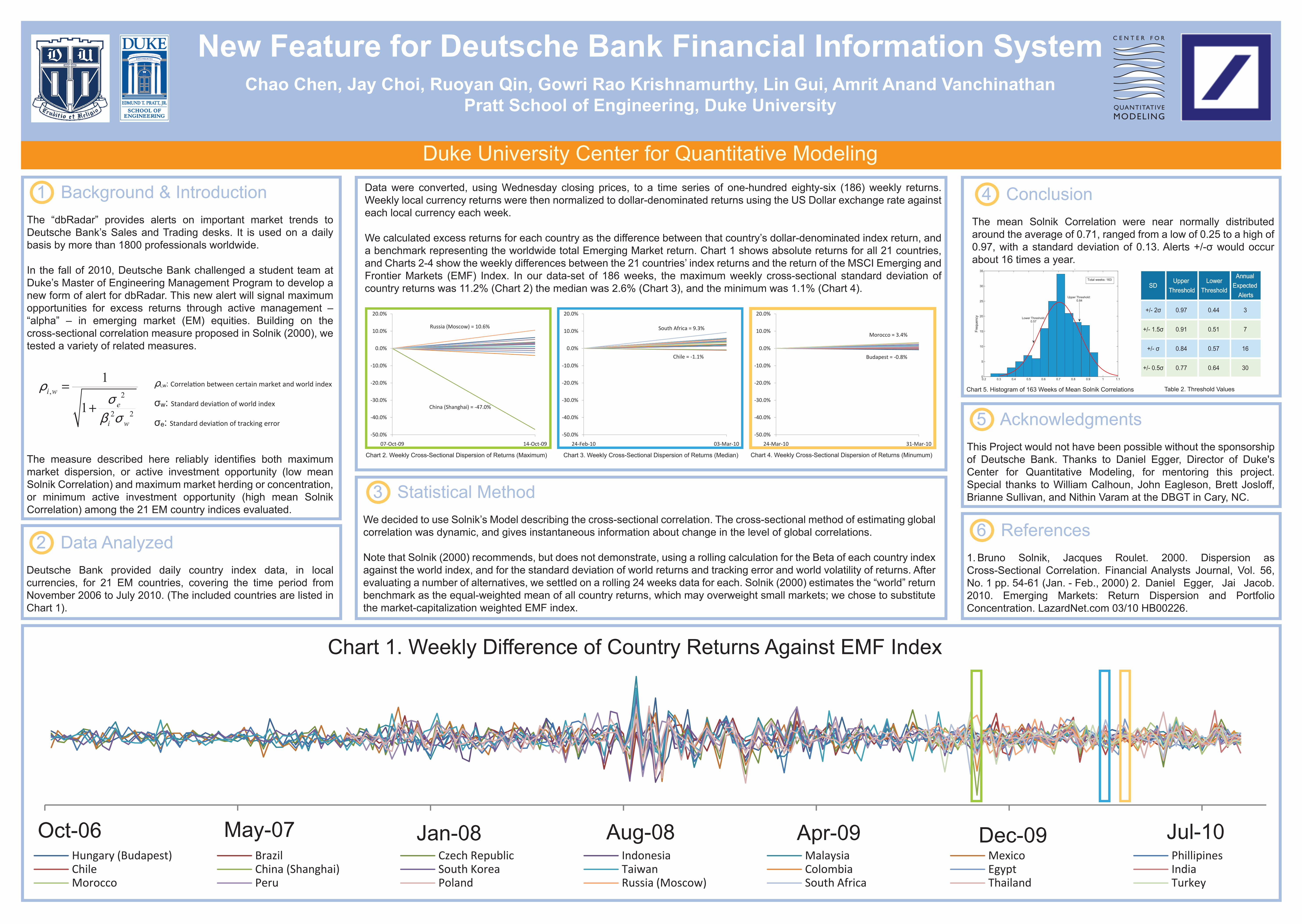

Chart 1. Weekly Difference of Country Returns Against EMF Index

3 Statistical MethodWe decided to use Solnik’s Model describing the cross-sectional correlation. The cross-sectional method of estimating global correlation was dynamic, and gives instantaneous information about change in the level of global correlations.

Note that Solnik (2000) recommends, but does not demonstrate, using a rolling calculation for the Beta of each country index against the world index, and for the standard deviation of world returns and tracking error and world volatility of returns. After evaluating a number of alternatives, we settled on a rolling 24 weeks data for each. Solnik (2000) estimates the “world” return benchmark as the equal-weighted mean of all country returns, which may overweight small markets; we chose to substitute the market-capitalization weighted EMF index.

, 2

2 2

1

1i w

e

i w

ρσ

β σ

=

+

ρi,w: Correlation between certain market and world index

σw: Standard deviation of world index

σe: Standard deviation of tracking error

2 Data AnalyzedDeutsche Bank provided daily country index data, in local currencies, for 21 EM countries, covering the time period from November 2006 to July 2010. (The included countries are listed in Chart 1).

Data were converted, using Wednesday closing prices, to a time series of one-hundred eighty-six (186) weekly returns. Weekly local currency returns were then normalized to dollar-denominated returns using the US Dollar exchange rate against each local currency each week.

We calculated excess returns for each country as the difference between that country’s dollar-denominated index return, and a benchmark representing the worldwide total Emerging Market return. Chart 1 shows absolute returns for all 21 countries, and Charts 2-4 show the weekly differences between the 21 countries’ index returns and the return of the MSCI Emerging and Frontier Markets (EMF) Index. In our data-set of 186 weeks, the maximum weekly cross-sectional standard deviation of country returns was 11.2% (Chart 2) the median was 2.6% (Chart 3), and the minimum was 1.1% (Chart 4).

6 References1. Bruno Solnik, Jacques Roulet. 2000. Dispersion as Cross-Sectional Correlation. Financial Analysts Journal, Vol. 56, No. 1 pp. 54-61 (Jan. - Feb., 2000) 2. Daniel Egger, Jai Jacob. 2010. Emerging Markets: Return Dispersion and Portfolio Concentration. LazardNet.com 03/10 HB00226.

Table 2. Threshold Values

0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 1.10

5

10

15

20

25

30

35Mean Correlation of EM Weekly Returns against EMF Index

Freq

uenc

y

Upper Threshold: 0.84

Lower Threshold:0.57

Total weeks: 163

Chart 5. Histogram of 163 Weeks of Mean Solnik Correlations

0.00 30.00 60.00 90.00 120.00 150.00 180.00Hungary (Budapest) Brazil Czech Republic Indonesia Malaysia Mexico Phillipines

Oct-06 May-07 Aug-08Jan-08 Jul-10Dec-09Apr-09Chile China (Shanghai) South Korea Taiwan Colombia Egypt IndiaMorocco Peru Poland Russia (Moscow) South Africa Thailand Turkey

5 AcknowledgmentsThis Project would not have been possible without the sponsorship of Deutsche Bank. Thanks to Daniel Egger, Director of Duke's Center for Quantitative Modeling, for mentoring this project. Special thanks to William Calhoun, John Eagleson, Brett Josloff, Brianne Sullivan, and Nithin Varam at the DBGT in Cary, NC.

Chart 2. Weekly Cross-Sectional Dispersion of Returns (Maximum)

20.0%

Russia (Moscow) = 10.6%

0 0%

10.0%( )

-10.0%

0.0%

-20.0%

-30.0%China (Shanghai) = 47 0%

-40.0%

China (Shanghai) = -47.0%

-50.0%

07-Oct- 4190 -Oct-09

Chart 3. Weekly Cross-Sectional Dispersion of Returns (Median)

20.0%

South Africa = 9 3%

0 0%

10.0% South Africa = 9.3%

-10.0%

0.0%

Chile = -1.1%

-20.0%

-30.0%

-40.0%

-50.0%

24-Feb- 3001 -Mar-10

Chart 4. Weekly Cross-Sectional Dispersion of Returns (Minumum)

20.0%

0 0%

10.0%Morocco = 3.4%

-10.0%

0.0%

Budapest = -0.8%

-20.0%

-30.0%

-40.0%

-50.0%

24-Mar- 1301 -Mar-10

SDUpper

ThresholdLower

Threshold

Annual Expected

Alerts

+/- 2σ 0.97 0.44 3

+/- 1.5σ 0.91 0.51 7

+/- σ 0.84 0.57 16

+/- 0.5σ 0.77 0.64 30

4 ConclusionThe mean Solnik Correlation were near normally distributed around the average of 0.71, ranged from a low of 0.25 to a high of 0.97, with a standard deviation of 0.13. Alerts +/-σ would occur about 16 times a year.