New decade, new crisis - Kearney

23

New decade, new crisis European Retail Banking Radar Photo by Karen King Kearney, Chicago

Transcript of New decade, new crisis - Kearney

New decade, new crisisEuropean Retail Banking Radar

Phot

o by

Kar

en K

ing

Kear

ney,

Chi

cago

Foreword 1

The 2020 retail banking outlook: minimizing loss and maximizing customer trust 2Revenue will drop at least 20 percent 2Meanwhile, costs will by and large remain the same 3One in eight banks will face losses this financial year 3

New decade, new crisis: lessons learned from the Global Financial Crisis and why this time it’s different 4Lessons learned from the Global Financial Crisis 5In some ways, it’s similar. But in others, it is very, very different 5Banking for good 5Regardless of the current cost position, the task at hand is the same for all: dramatically change the operating model 6European banks will need to reduce their cost base by more than EUR 35 billion in order to survive 62021 and beyond 6

A new normal: fortifying your distribution channels in a world post-COVID-19 7Customers won’t go back to how things were, so neither should banks 8The lockdown has accelerated the trend toward a cashless society 9End-to-end online banking services have become more important than ever 9Contact centers will go digital—and replace branches as the #1 point of contact for customers 10Branch closures will continue… 10…but we will see a new role for bank branches 11Customers will expect a frictionless experience across channels 11If it can’t be done in-house, banks will look to acquire a business that can do it 11A new age for banking 11

Be bold, act now: the operating models of the future 12Universal banks: using mass scale to deliver both standardized and specialized products 12Specialist banks: a quality over quantity approach 13Direct banks: a quicker, more convenient form of banking 13Lifestyle platforms: a new lifestyle companion 13Banks need to commit to a new operating model 14Doing more with less 14The knowledge and skills that have helped banks get where they are won’t be enough to get them where they need to be 15Time to make a decision 15

Life after COVID-19: building a new banking landscape through M&A 16Post-crisis M&A shows promising results 16For some players, M&A may be the only option 17The need for efficiency—based on scale and focus—will lead to divestment of non-core businesses and acquisitions to strengthen the core 17The rise of strategic partnerships 17It’s not just about strategic mergers, acquisitions, and divestments—it’s also about what follows 17A mixed outlook for fintechs 18Why the only constant will be change 18

Contents

Foreword

Through identifying these key challenges we hope to help retail banking leaders across the region identify the emerging opportunities we are seeing to support mid- to long-term growth for their organizations.

I hope you will find these articles insightful and if you would like to discuss any of the themes covered in more detail please do contact any member of the Kearney team.

Simon Kent Partner and Global Lead, Financial Services, Kearney Connect via Linkedin

I am delighted to share with you a compilation of five short articles we recently published under the banner title New decade, new crisis.

The series stems from our successful European Retail Banking Radar which is now in its 11th year. Our recent 2020 headline analysis concluded that revenue for retail banks across the region will fall by an average of 20% by year end, with one in eight retail banks facing losses this year, and profitability per customer projected to reduce by approximately 60%. Retail banks are therefore having to weather enormous and unprecedented changes, intensified by the recent COVID-19 crisis.

In this series, we examine key opportunities and risks across retail banking over the next few years in light of the pandemic. After months of lockdown, customers’ banking habits—and indeed expectations—have shifted irreversibly toward digital banking. Retail banks have come under strain as revenues drop while operating costs have not, leading to a critical review of existing infrastructure, specifically bank branches, employee skill sets, and even employee workplaces. Cost reduction is paramount, but it won’t be enough—banks need to consider a complete transformation of their operating model and articulate a new minimum viable operating model for the future of the bank. For many banks, M&A will be a viable way to make quick and impactful changes to their operating model and the resulting surge in M&A activity will present a multitude of opportunities. While the COVID crisis in Europe is subsiding, it is far from over. Only those who embrace the urgency for change, make bold deci-sions, and take quick action will survive.

1European Retail Banking Radar

The 2020 retail banking outlook: minimizing loss and maximizing customer trust

Our modelling shows that this combination of payment holidays, low base interest rates, reduced economic activity, and reduced revenue from management fees of financial assets under manage-ment will result in an average 20 percent decline in retail banking revenues. This is a base scenario, relying on a partial recovery toward the end of the year. However, it’s very likely that revenues could drop by 35 to 40 percent, depending on the starting point and revenues mix between different European banks.

Travel, leisure, and entertainment spend has ground to a halt and customers are adopting a wait-and-see approach, especially on the lending side.

Over the past few months, nationwide restrictions on travel, work, and leisure across most European countries have led to a dramatic drop in consumer spend.Meanwhile, repayment holidays on credit cards and loans and offers of interest-free overdrafts abound while base rates have been cut across most countries, leaving banks in a precarious position as their income levels drop while operating costs remain largely unchanged. It is an unprecedented situation and our research predicts that despite best efforts, one in eight banks will suffer losses this financial year. Our modelling has identified three predictions for how COVID-19 will impact retail banking profits in 2020:

Revenue will drop at least 20 percentBanks are taking dramatic measures to make life easier for their customers. With government support, European banks are granting mortgage repayment holidays, cancelling overdraft fees, and increasing credit card limits. Many countries have also cut their interest base rates in a bid to keep the economy afloat, leading to an additional pressure on revenue for banks. While there are a few notable consumer areas where business is thriving—food shopping, streaming services, and online retail—customers have dramatically scaled back their spending habits. Travel, leisure, and entertainment spend has ground to a halt and customers are adopting a wait-and-see approach, especially on the lending side, where applications for new loans and mortgages have declined.

2European Retail Banking Radar

Our research suggests that the average cost-to-income ratio will increase to ~80 percent, with some banks seeing costs exceeding revenues.This is not only the right thing to do, it’s also a shrewd move. Those banks will be remembered for the active participation they took in helping their customers through a challenging time. The trust they gain from customers will not only be rewarded through increased loyalty and new business but will also prepare the bank’s customer services for a world post-COVID-19. After all, it is unlikely that customers will fully return to their pre-COVID-19 habits and the crisis is likely to become a catalyst for a permanent shift toward more digital banking habits.

One in eight banks will face losses this financial yearEven with modest impairments, it will be a tough year for banks—along with most other sectors. Our estimates suggest that up to 12 percent of banks could see losses in the current financial year, with profitability per customer being reduced by as much as 60 percent compared to 2019.

The crisis presents unprecedented challenges, and its long-term impact is yet unknown. However, by looking after employees, proving value to customers, preparing for the worst economic scenario, and fortifying core business activities, businesses stand the best chance of emerging from the crisis stronger. Read more on our six steps to weathering the COVID-19 outbreak.

Many banks will be looking back to the last decade and revisiting how they weathered the Global Financial Crisis and navigated the recovery. There are some obvious similarities—and differences—between the COVID-19 crisis and the Global Financial Crisis that we will examine in more detail in our next installment in the series.

Meanwhile, costs will by and large remain the sameAlong with most other sectors, banks are entering a holding pattern where basic operations need to be kept afloat as they consider what they reopen and what they agree to restart following the introduction of a crisis operating model. Many banks are commit-ted to keeping their headcount—a move that plays favorably with both the media and public opinion, as well as being a sensible long-term investment. But while the attention is on management salaries and bonuses, news is also emerging of pay cuts, reduced working hours, and voluntary unpaid leave across regular staff.

Most branches have ether closed or reduced their operating hours, and some governments have issued rent deferrals, which may alleviate some of the short-term operational costs. However, for the most part operations costs remain the same for banks, leading to a tight squeeze on profit margins. Our research suggests that this will push the average cost-to-income ratio up to ~80 percent with some banks seeing costs exceeding revenues. All of this will need to be weathered before banks see an uptick in revenue.

Some banks have also taken on the additional expense of launching new and improved digital services for customers, such as Lloyds Bank providing free digital training and issuing free tablets to elderly customers, Intesa Sanpaolo launching preapproved credit lines to small businesses and families in need, and TSB setting up dedicated customer care chatbots among other online features to channel customers toward specific services designed to help those in need due to the outbreak. Such examples demonstrate how banks are taking the opportunity to deliver high-value services at a relatively small cost, allowing them to actively support customers during the outbreak.

3European Retail Banking Radar

Lessons learned from the Global Financial Crisis mean that this time banks are better prepared. However, it will take a radical change in operating models to survive. Banks will need to invest in the digitalization of customer interactions and employee value propositions to ready themselves for a new banking era that addresses the needs of changed behaviors and habits. Unlike previously, it will not be a case of doing “more of this and less of that” but about doing things differently, by tackling bold operational decisions and significantly upgrading digital capabilities.

It is becoming increasingly clear that a rapid and full recovery in 2021 is unlikely. The resulting recession from the crisis, dubbed the “Great Lockdown,” could lead to a global GDP contraction of at least 3 percent in 2020, according to the IMF, making this the worst recession since the Great Depression, and certainly much worse than the Global Financial Crisis. This throws everything we know about a recession into harsh relief—we are facing a much slower recovery, a higher rate of unemployment, and a long journey back to the levels of consumer confidence seen just a few months ago.

New decade, new crisis: lessons learned from the Global Financial Crisis and why this time it’s different

Banks will need to invest in the digitalization of customer interactions and employee value propositions to ready themselves for a new banking era.

4European Retail Banking Radar

In some ways, it’s similar. But in others, it is very, very differentIn some ways, the two crises are similar—for the banking industry at least. Both crises started in other markets—the Global Financial Crisis started as a real estate crisis, which spilled over to the economy, and we are currently in a health crisis, which will do the same.

The industry has been in a period of long-term low interest rates since the Global Financial Crisis and this is likely to continue in the years ahead in order to stimulate the economy post-COVID-19, much in the same way that low interest rates were introduced post-Global Financial Crisis. In this respect, not much will change. Banks will continue to operate in a similar environment as before and it will weigh heavily on their performance.

However, in most ways, this crisis will be different. It has happened quickly, hit very hard, and will remain with us for some time. GDP forecasts for 2020 are already predicting a contraction of 3 percent, compared with the post-Global Financial Crisis contraction of 1.9 percent in 2009. In some countries, it’s worse. This crisis is already showing signs that it will last longer and cut deeper. It looks like the economy is in for a recession followed by a prolonged period of slow recovery, which could result in an unprecedented shakeup in many industries and a battle for survival for small entrepreneurs and private individuals.

Banking for goodIn one significant way, this crisis will be different for a good reason. During the Global Financial Crisis, many banks had insufficient liquidity and inadequate capital. And they suffered for it. Now, due to lessons learned from the crisis, banks are well capitalized and have the capacity to support the economy—at least from today’s perspective. As the motor of economic recovery, banks will be expected to provide credit where it is needed most, to open “doors” and operate even if the rest of the economy is in a lockdown. This time, they won’t be standing in line for government aid and may instead be able to actively support the recovery, providing credit where it’s needed most. There is a compelling need to use the lessons learned from the past crisis to curb risks and ensure business continuity, while addressing the new challenges of social distancing and remote operations, which the lockdown necessitated.

Lessons learned from the Global Financial CrisisBanks emerged from the Global Financial Crisis stronger, thanks to increased regulation and the tough decisions each bank had to make to survive, be it restructuring, streamlining operations, reducing headcount, increasing capital buffers— or all of the above.

The regulations were designed not only to strengthen the industry, but to provide protection against future crises. Banks are significantly better positioned as a result. The Global Financial Crisis highlighted the need for banks to strengthen their capital adequacy and to maintain solid liquidity buffers, as the crisis showed that a short-term lack of liquidity can bring down a profitable bank in a matter of weeks—both hard lessons learned that have made the industry signifi-cantly more resilient to future economic disruption.

Banks are also now acutely aware that the hit from impairments is not immediate but can have a long tail. This time, banks know to prepare and account for impairments extending far beyond the immediate crisis. We predict that up to 80 percent of crisis-re-lated impairments will come after 2020 and while most impairments will hit in 2021, some local econo-mies will continue to feel the effects into 2022.

Since the crisis, the industry has also seen a huge shift toward digitalization, leading to significant cost efficiencies as branches have closed and operations have been further streamlined. Some would argue that the banking industry is as strong as it has ever been. This time, they’re ready.

5European Retail Banking Radar

European banks will need to reduce their cost base by more than EUR 35 billion in order to surviveWhile recent measures—branch closures, reduced headcount, improved operating efficiencies—may have contributed between 15 and 20 percent cost reduction in the past decade, the effects are not visible in the cost-to-income ratios of banks.

Across Europe, banks will need to reduce their costs by EUR 35–45 billion over the next few years. This will require a reduction of at least an additional 20 percent of the cost base. This is by no means an easy undertaking. During the peak of the Global Financial Crisis, banks managed to reduce cost per client on average by EUR 20. In order to keep the 2019 cost-to-income ratio of 62 percent, savings of EUR 80 per client will be needed from the current 305€ per client. While this is a massive effort, the banks who manage to move in this direction, diversify with more digital services, and deliver a minimum viable operating model while at the same time staying close to clients at this pivotal moment in their lifetime will have an opportunity to build upon existing client loyalty and increase their market share significantly.

2021 and beyondTo achieve such a sizable—and sustainable—cost reduction, there is no alternative but to fundamentally transform the operating model with a new way to serve clients and new way of working. For those who treat this crisis not as a hiatus to operations but as a catalyst for a new era of retail banking, they can expect to see a good chance of a strong recovery.

For the remainder of the series, we will explore ways to fortify distribution channels, the operating model of the future, and how to build a new banking land-scape through M&A. In our next article, we will examine the broader, bolder steps banks can take to prepare for the channel shift in retail banking and position themselves as a next-generation retail bank.

Regardless of the current cost position, the task at hand is the same for all: dramatically change the operating modelBanks have been on an efficiency drive over the last decade. Since 2007, about 61,000 branches have closed across Europe, representing around 36 percent of all branches, and approximately 600,000 employees lost their jobs, amounting to 22 percent of total employment in the banking sector. Banks are all too familiar with cost reductions.

And yet cost discipline is something they will need to explore further to fight the effects of the crisis. The picture is uneven across Europe, as each country has a different starting point and subsequent challenge ahead. While retail banks in Scandinavia and Poland have already created efficient cost structures and reduced their cost-to-income ratio below 50 percent, two of the largest European markets—Germany and France—struggle with fragmented markets and costs accounting for 70 percent+ of the revenue.

The easy cuts have already been made, leaving little room for further traditional cost reduction. But further cost reductions are imperative. Banks will need to look at bolder, broader transformations. This means not simply cutting costs but rethinking existing operating models, digital transformation in both back-end operations and front-end customer services, and reviewing their core positioning to ensure they are meeting the needs of a new era of retail banking.

6European Retail Banking Radar

A new normal: fortifying your distribution channels in a world post-COVID-19

From a payments perspective, the banking industry is holding up well. While the total number of payments has declined, online spend has increased amidst the COVID-19 lockdown, with Visa and Mastercard reporting a 20 percent uplift in “card not present” transactions and a notable rise in customers trying online payments for the first time. Online and mobile banking are helping customers to easily service their accounts remotely. For some individuals and busi-nesses, online services have helped them to cope with financial difficulties and banks have risen to the challenge to offer more online help than ever before as a broadening range of customers visit their site in lieu of a local bank branch.

As our collective familiarity with online banking increases, it’s likely that a lot of these habits will stick beyond the pandemic. So, what does this mean for banks?

The lockdown has led to a massive shift to online activity, as people take to the web for everyday tasks and entertainment. What once served as a convenient alternative to the real thing has now become the sole link to the outside world. Shopping, socializing, and entertainment are now done online, and thanks to delivery apps, even our eating habits have gone digital.None of this is new, of course. The trend toward digital has been around for years as technologies improve and businesses expand their services to include better online capabilities. But this pandemic has accelerated that trend, regardless of industry or demographic group. Businesses that weren’t previ-ously offering online services are now frantically upgrading their capabilities and any Internet-averse individuals are receiving quick and basic tutorials by their relatives over Zoom.

Shopping, socializing, and entertainment are now done online, and thanks to delivery apps, even our eating habits have gone digital.

7European Retail Banking Radar

https://seekingalpha.com/article/4345056-visa-and-mastercard-covidminus-19-and-q1-results-assessment

https://seekingalpha.com/article/4345056-visa-and-mastercard-covidminus-19-and-q1-results-assessment

Source: Kearney analysis

Austria, Spain, and Portugal are the most traditional markets, where >65% of customers perform their operations only in branches and through advisors

Norway, UK, and Sweden are the most innovative markets, where 70% of customers rely on remote channels to research and purchase products

Customers choosing physical vs. remote channel(%, all countries and product types combined)

Figure 1Although significant di�erences exist between countries, at European level more than half of customers do not use physical sales channels to research and buy new products

47%

100%

53%

2020 2025F

65%

35%

100%

Physical channels

— Bank branch

— Independent advisor

Remote channels

— Online

— Mobile

— Call center

Our study reveals that 53 percent of European banking customers do not use physical channels at all when researching and buying products (see figure 1). As customers become more familiar with online banking, due to the lockdown, we predict that this is set to increase to 65 percent in 2025, requiring European banks with branch-heavy operating models to focus on developing their digital channels further.

Digital banking should now be considered the preferred way for customers to engage with their bank. If banks continue to improve their processes at the same speed and agility demonstrated at the beginning of the pandemic, they could be in a significantly stronger position by the end of the year.

Those that don’t will miss the opportunity to continue the momentum created by customers’ new digital habits, structurally change their cost base, and dramatically improve customer experience. Whatever happens, don’t expect to turn everything back on and go back to the old world.

Customers won’t go back to how things were, so neither should banksCustomers have shown that they can and will interact with banks digitally. The key is to do it in the right order, and at pace. This is a great opportunity for banks to audit their customer processes—particularly offline processes and their connectivity to digital processes—and prioritize these areas for further investment and improvement. For those customer processes that have been rapidly digitized in the early days of the pandemic, these now need to be stress-tested and improved as required to ensure long-term operational resilience. The same goes for any digital processes that were already in place, which also need to be stress-tested for a more integrated and digital banking era. It’s a win-win situation—digital banking is not only better for the customer, but cheaper for the bank.

8European Retail Banking Radar

Source: Kearney analysis

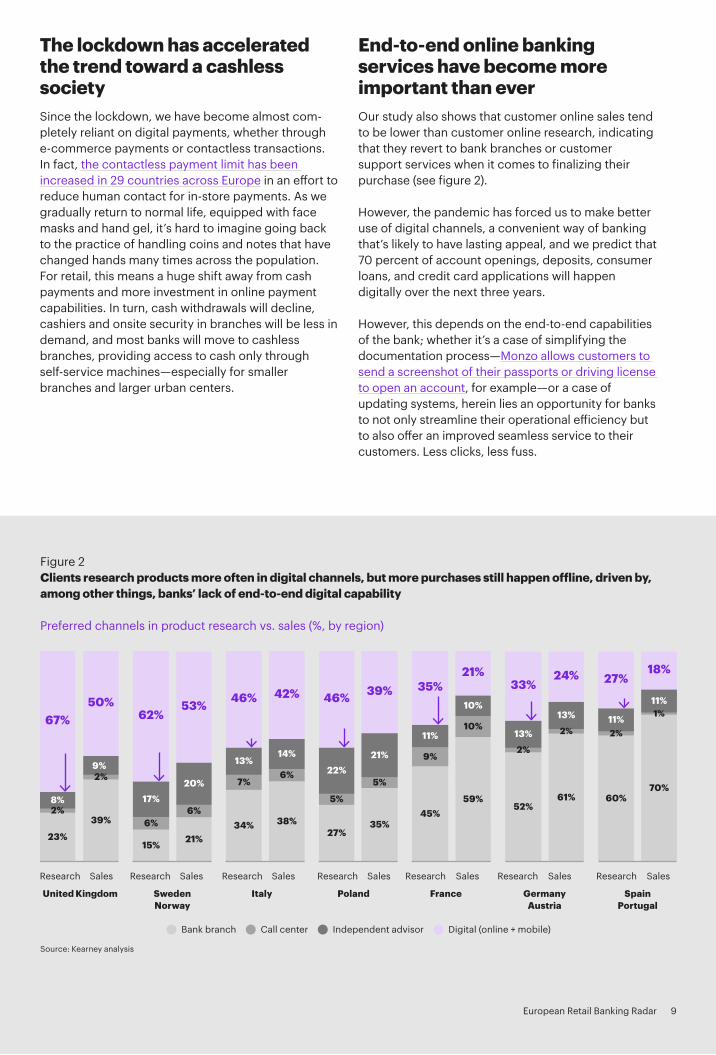

Figure 2Clients research products more often in digital channels, but more purchases still happen offline, driven by, among other things, banks’ lack of end-to-end digital capability

Preferred channels in product research vs. sales (%, by region)

United Kingdom SwedenNorway

Italy Poland France GermanyAustria

SpainPortugal

Research Sales Research Sales Research Sales Research Sales Research Sales Research Sales Research Sales

Bank branch Call center Independent advisor Digital (online + mobile)

23%

2%8%

67%

39%

2%9%

50%

45%

9%

11%

35%

59%

10%

10%

21%

34%

7%

13%

46%

38%

6%

14%

42%

5%

27%

5%

22%

46%

35%

21%

39%

15%

6%

17%

62%

21%

6%

20%

53%

52%

2%13%

33%

61%

2%

13%

24%

60%

2%11%

27%

70%

1%11%

18%

End-to-end online banking services have become more important than everOur study also shows that customer online sales tend to be lower than customer online research, indicating that they revert to bank branches or customer support services when it comes to finalizing their purchase (see figure 2).

However, the pandemic has forced us to make better use of digital channels, a convenient way of banking that’s likely to have lasting appeal, and we predict that 70 percent of account openings, deposits, consumer loans, and credit card applications will happen digitally over the next three years.

However, this depends on the end-to-end capabilities of the bank; whether it’s a case of simplifying the documentation process—Monzo allows customers to send a screenshot of their passports or driving license to open an account, for example—or a case of updating systems, herein lies an opportunity for banks to not only streamline their operational efficiency but to also offer an improved seamless service to their customers. Less clicks, less fuss.

The lockdown has accelerated the trend toward a cashless societySince the lockdown, we have become almost com-pletely reliant on digital payments, whether through e-commerce payments or contactless transactions. In fact, the contactless payment limit has been increased in 29 countries across Europe in an effort to reduce human contact for in-store payments. As we gradually return to normal life, equipped with face masks and hand gel, it’s hard to imagine going back to the practice of handling coins and notes that have changed hands many times across the population. For retail, this means a huge shift away from cash payments and more investment in online payment capabilities. In turn, cash withdrawals will decline, cashiers and onsite security in branches will be less in demand, and most banks will move to cashless branches, providing access to cash only through self-service machines—especially for smaller branches and larger urban centers.

9European Retail Banking Radar

1 Nordics and Switzerland includes Denmark, Finland, Norway, Sweden, Switzerland; Western Europe includes Austria, Benelux, Germany, France, United Kingdom; Southern Europe includes Spain, Italy, Portugal; Eastern Europe includes Czech Republic, Croatia, Hungary, Poland, Romania, Slovenia, Slovakia

2 2008–2015 data for Serbia and 2008–2012 data for Croatia are estimates obtained by considering the percentage amount of branches included in RBR tool for 2019

Sources: ECB number of branches, domestic – home or reference area (UK data since 2015 from ONS via NOMIS database, Norway data from Finansnorge, Switzerland data from SNB); Kearney analysis

Figure 3Since 2008, Southern Europe has seen a 49% decrease in branches, while Eastern Europe has reduced its branch network by just 33%

Regional branch network evolution1 (annual percentage change)

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

-10.9

1.3

-3.2

-7.7

-2.3

-3.0

-2.7

-2.8

-4.7

-5.6

53.4

100%

-5.1

-4.6

-3.4

-3.4

-1.8

-2.3

-1.3

-2.1

-0.8

-0.9

-2.6

75.4

100%

1.3

100%

-6.8

-5.2

-5.4

-2.7

-3.9

-7.5

-3.6

-3.9

-1.9

-1.9

50.9

-6.2

0.8

0.8

2.4

76.7

100%

-6.5

-2.0

-3.9

-1.7

-5.9

-0.6

-1.9

-4.8

Nordics and Switzerland2 Western Europe Southern Europe Eastern Europe2

Branch closures will continue…Thanks to the increasing adoption of online banking, which has become even more popular since the pandemic, the role of the bank is becoming less relevant for customers in its current format and branch numbers will continue to decrease, perhaps at an even faster rate than before the pandemic. Our study indicates that we are likely to see as many as 40,000 branches (25 percent of all branches in Europe today) close across Europe in the next three years. The rate and extent of branch reduction will differ by market, as some have already made dramatic reductions with European branches numbering around 165,000 in 2019, down from 209,000 in 2014 and 240,000 in 2009 (see figure 3).

While the starting points will be different, the trend is the same across all European countries: banks will operate with less branches in the future.

Contact centers will go digital—and replace branches as the #1 point of contact for customersCall centers are also feeling the effects of shifting trends to online browsing as customers increasingly go online to research and buy banking products and services. However, those who still wish to speak to someone in-person are more likely to use customer services, either through webchat, video calls, chatbots, or by phone, than visit a branch. This provides contact centers with a continued role in the omnichannel mix as they take on more complex customer enquiries and provide support for online research and sales, providing the personal human contact of a branch visit without the inconvenience of visiting one.

10European Retail Banking Radar

Customers will expect a frictionless experience across channelsEven though online banking is becoming increasingly popular, it will always be part of a broader, omnichan-nel offering due to the variety of products and services offered, particularly when it comes to more complex products. Banks will need to invest in an omnichannel concept with simple and smooth handover between channels. This isn’t a new idea—banks have been trying to get this right for years and while many banks have made significant improve-ments, many still lag behind. If there was ever a time to invest in providing a seamless customer journey across digital and offline channels, it’s now. Customers will expect a frictionless experience. If they start an application online or a conversation on the phone, they will expect to be able to resume their enquiries at a later date using any channel. Seamless connectivity will be expected as standard.

If it can’t be done in-house, banks will look to acquire a business that can do itIn the race to become a frictionless and optimized omnichannel offering, some banks may not be in a position, either financially or strategically, to develop the necessary capabilities in-house quickly enough. In fact, our first article in this series predicted that European banks would need to reduce their costs by EUR 35 billion over the next few years.

We therefore predict a rise in bolt-on M&A acquisi-tions or strategic partnerships as banks build out their digital proficiency—something we will focus on in more detail in our next article in the European Banking Radar Series.

A new age for bankingThe pandemic has proven to be a catalyst for many changes already underway in the banking industry. The shift to digital banking, the reduction of branches, and the need for more connectivity between channels are not new trends, but the pandemic has significantly accelerated demand for these changes to happen, and quickly. By necessity, the industry has found new ways of doing things that wouldn’t have previously happened, resulting in a new way of doing things that may even prove to be for the better in the long run for customers and banks alike.

…but we will see a new role for bank branchesThe relevance of bank branches continues to spark debate, especially when it comes to financial inclusion for those living in rural areas or those who prefer to bank in-branch, notably older generations. It’s therefore unlikely that bank branches will disappear, although they will need to be adapted to better suit this new age of retail banking. As customer adoption of online banking increases, bank branches will be primarily staffed by higher-qualified advisors to focus on more complex products, such as mort-gages, life insurance, pensions, and investments advice. In some countries, such as the UK, there are regulations requiring advised sale for certain products, further adding to the longevity of advisory services for retail banking.

This isn’t the only change that we will see in local branches.

Remote working, forced by the pandemic, has led to companies and employees alike adjusting to a new way of working that has in the main proven to be considerably cheaper for businesses and more convenient for staff. Suddenly, those big city-based headquarters seem to make less sense than they did a few months ago. The CEO of Barclays recently spoke about reducing its head office space and even repurposing local bank branches as sites for employees holding centralized roles. If others follow suit, we may well see a mass repurposing of local bank branches into hybrid space for both custom-er-facing staff and head office staff. The pandemic has also proven that remote working can work under the right circumstances, so it’s likely that we will not see a return to the five-day commute but instead may see desk-based employees, such as contact center and head office staff, splitting their time between office and remote working. Indeed, banks are already starting to set up investment programs to support the new way of working.

11European Retail Banking Radar

The starting point is different across Europe. Some banks have already embarked on their chosen model which will need to pivot for a post-COVID-19 market. Some banks will have more limited options, as not all four models described below will be viable. However, for the majority of European banks, they need to act now, challenge their current trajectory, and make a strategic choice: what model will work best for us?

Universal banks: using mass scale to deliver both standardized and specialized productsBy taking advantage of their enormous infrastructure of branches, employees, and mass operations, many bigger banks will be ideally suited to deliver a broad range of good value and standardized services at a lower cost. Scale brings market power, pricing advantages, and high share of customer wallet. However, standardization by no means implies a limited offering or basic products. By virtue of scale, these banks will also have the capability to pick and choose a selection of specialized products and business to suit different customer segments, all delivered through highly disciplined, automated processes and back-end operations. This model might eventually evolve into a utility service that may also be used for smaller banks as a back-end function—as a bolt-on to their own banking customer interface.

With a history of both reduced revenues and rising costs per customer, coupled with the macroeconomic headwinds, decisive strategic change is needed in retail banking. The most efficient and intuitive way to achieve this is by deploying the appropriate “minimum viable operating model” for your organization and market. The pre-crisis model needs to adapt to the post-crisis world. Operating models will look very different, very quickly, and not every bank will have the same setup. In fact, we will see a move away from the “generalist” operating model as banks have to make choices to deliver improved efficiency and to deliver a compelling customer proposition.

Be bold, act now: the operating models of the future

12European Retail Banking Radar

Lifestyle platforms: a new lifestyle companionSome banks will move away from the traditional concept of banking to fully integrate into a customer’s everyday life. Using data gleaned from everyday customer spending habits and retailer and leisure preferences, such platforms will have the insights needed to anticipate and recommend offers and services across all businesses—retail, entertainment, household bills, travel, and so on. A one-stop solution to the customer’s daily needs, they will no longer be just a bank. They will become a lifestyle platform. This model is also an option for entrants from other industries—especially large e-commerce and social networking platforms that have a loyal client base and from where banking, especially everyday banking, provides an opportunity to broaden the services to their clients and solidify existing relationships.

Specialist banks: a quality over quantity approachSome banks may choose to specialize and focus on the client interface in a niche segment of banking. As more banking products become digitized, especially everyday banking, banks may choose to reallocate resources to more customized and complex products, such as mortgages, insurance, and investments, where returns are higher and can be protected from universal banks. By focusing on specific “verticals,” these banks will become specialists in a subset of services and products. While they may continue to offer everyday banking, they will be best known as the gold standard for offering highly personalized propositions. Such specialist banks will deploy technology, offer excellent end-to-end service, collect data and analytics to get to know each client individu-ally, better understand patterns of banking product use, and offer products with more relevant context and purpose. For this specialism and insight, the bank can develop a mutually better outcome for both the customer and the bank.

Direct banks: a quicker, more convenient form of bankingNot surprisingly, the number of direct banks is set to increase, with challenger banks leading the way. These banks will focus on setting the new standards for digital capabilities and embrace strategic acquisi-tions and partnerships to grow or fill product gaps. The target audiences for these banks will be digitally savvy customers who are comfortable with online banking and familiar with digital processes and interactions, much preferring the convenience of apps and chatbots over in-branch banking services. They benefit from lower-cost operations, modern flexible architectures, and a customer-first mindset. Their challenge is growing the returns for the business in line with the growth in customer numbers.

Most European banks need to act now, challenge their current trajectory, and make a strategic choice: what model will work best for us?

13European Retail Banking Radar

Doing more with lessAs with many industries, digitization will significantly improve operational efficiencies and will inevitably lead to a lower headcount and a different mix of skill sets. Operations will be the most-affected depart-ment as it becomes largely automated with straight through processing (STP). Banking models will evolve with certain banks opting to share processing infrastructure with others to reduce overall costs. This will be particularly true where combining undifferenti-ated activities helps gain scale efficiencies, for example in cash handling or basic KYC processing. Advanced analytics will also increase as it integrates into almost every aspect of retail banking from predictive sales and gauging client price sensitivity to fueling more robust risk models and better managing internal capacities.

Banks need to commit to a new operating model It’s been a long time coming, but the effects of COVID-19 have accelerated the need for banks to make a choice about the type of bank they want to be in the future and to make those changes now, harnessing the transformative potential of minimum viable operating models and adjusting accordingly. Up to now, most banks have strived for size and scale, trying to be everything to everyone. This has led to inefficient cost structures and a generic customer offer that are unsustainable in the longer term.

Irrespective of size or geography, most institutions manage their cost base in line with the expectation about the development of revenues. Bold changes in the operating models—either toward significantly leaner cost structure or stronger focus on client and top-line opportunities—are rare. The case for change is clear in both the high operating costs and reduced income per customer shown below (see figure 4).

While the choice of the operating model is crucial, bringing it to life will be even more challenging. The changes will touch on almost every aspect of business and most employees in retail banks.

1 Europe includes Germany, Austria, Spain, France, Benelux, Italy, UK, Portugal, Switzerland, Nordics, Czech Republic, Hungary, Slovenia, Slovakia, Poland, Croatia, Romania, and Serbia.2 Relative marketing position is computed on the basis of the percentage of business volume (client deposits and loans) of each bank vs. its country; in some cases, an adjustment was required.

3 2019 data is partially based on actual annual figures, partially on forecasts based on Q3 2019 results.

4 When analyzing changes of indicators denominated in Euros, we applied 2019 constant exchange rates to present growth in real terms.

Source: Kearney 2020 Retail Banking Radar

Leader Follower End tail

% business volume in their country

Evol

utio

n of

ope

rati

ng c

osts

per

cus

tom

er

Evolution of income per customer

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

-70% -60% -50% -40% -30% -20% -10% 0% 10% 20% 30% 40% 50% 60% 70%

Evolution of income per customer vs. operating costs per customer—Europe, di�erent relative market position1,2

(2015–2019f, %3,4)

Figure 4Banks have historically clustered in the same operating model, with no real breakout performance from the norm, and then scaled up or down accordingly

14European Retail Banking Radar

The knowledge and skills that have helped banks get where they are won’t be enough to get them where they need to beThese changes will mean a significant transformation of employee skill sets, requiring a balance between reskilling existing staff for business continuity and a selective onboarding of new talent. Millennials and Gen Z now make up 59 percent of the global work-force and they are driving a more flexible, progres-sive, and purpose-led working culture and a trend for shorter employment tenures. Like many industries, financial services will also need to move away from hierarchical and matrix structures and adopt flatter, more flexible structures.

In financial services, the people agenda has become a crucial challenge for the boardroom—not just for attracting the best talent, but attracting talent to the financial services industry as a whole. As roles become more technical, banks will not just be competing among themselves but also with technol-ogy companies and will need to offer a compelling employee proposition—not just financially but in terms of career progression, learning opportunities, and purpose—to acquire and retain the best talent.

Time to make a decisionRetail banking is always evolving, but we are now witnessing an acceleration of trends—across all industries—forced by the COVID-19 pandemic. It’s no longer just about cost reduction, but a fundamental transformation of the operating model. It’s time for banks to critically evaluate their operating model in order to best position themselves for a more digi-tized, customer-centric world.

Rather than being everything to every customer, now is the time to choose scale, specialism, becoming fully digitized, or making the transcendent step out of financial services and becoming a lifestyle platform.

The people agenda is a top priority as the business adapts to a new operating model. While headcount reduction is both cost-effective and easy to measure, the biggest focus should be on reskilling existing staff and becoming an attractive employer for both technology specialists and younger generations.

Finally, banks should consider developing their partnership ecosystems—starting in the technology area—to accelerate their shift to a new operating model, something we will explore in our fifth and final article in this year’s European Retail Banking Radar series.

As the number of bank branches decreases, staff numbers will also decrease with remaining roles expanding beyond semi-skilled cashiers to skilled advisors. Technical support departments, ironically, will decline by 25 to 30 percent as banks increasingly outsource to technological specialist players. It will be crucial to change the resource mix in order to orchestrate and control the IT platform design and its evolution. Generally, many departments will reduce headcount as automation and predictive analytics lead to greater transparency and data availability (for example, risk management could decline by 10 to 15 percent). While overall headcount will decline, there will be some notable growth areas. Remote advisory, for example, is likely to gain popularity once again as customers increasingly shift to digital channels, leading to banks finally breaking through the long-standing threshold of 10 to 15 percent of customers using this channel.

It’s also important to rethink the IT governance and operating model, consolidating and focusing only on those partners that help the bank reach their operat-ing and business objectives, as significant cost reductions will unlock resources that can then be invested in business model transformation programs. This includes reviewing the vendor base to minimize supply chain risks related to a changing business landscape and improving service levels to meet the new customers’ needs. Meanwhile, it’s important to evaluate existing stratified and stand-alone solutions for new business efficiency, looking for new services and solutions (such as end-to-end investment platforms and powerful advisory tools).

15European Retail Banking Radar

Post-crisis M&A shows promising resultsFollowing the financial crisis of 2008–2009, the number of mergers and acquisitions briefly surged, followed by a slump during the eurozone crisis of 2010–2012 when pan-European M&A activity stalled. Since then, cross-border acquisitions have decreased and remain at a two-decade low, with most transac-tions occurring in-market ever since. While the pandemic lockdowns have stalled international activities and might not be conducive to cross-border M&A, we anticipate that the number of domestic transactions will significantly increase.

Our Retail Banking Radar database shows that eight out of 10 domestic mergers and acquisitions follow-ing the financial crisis of 2008–2009 outperformed their local retail markets—in terms of profit growth per customer—in the three years after completing their integration. This indicates that crisis-driven M&A can and does improve performance. Many banks will need to consider M&A as the most efficient means to radically reshape their business portfolio—for both buyers and sellers—to achieve the required scale of cost reduction and transformation before it is too late.

While the banking industry has been in a state of transformation for years, the COVID-19 pandemic—both through changing customer habits and a radically shifted economic landscape—has put immense pressure on retail banking performance, accelerating the need to reinvent the operating model. This will require new capabilities—and fast. As a result, we expect to see a rise in mergers and acquisitions but also divestitures over the next couple of years as banks seek to reduce costs in the short term, refocus the core business for the long term, and ultimately transform their operating models.Our study shows that one in four banks will see their cost-to-income ratio surge above 80 percent as revenues fall but operating costs prove stickier. There will be some winners, but some notable losers also as our study shows that one in seven banks will have a cost-to-income ratio that might exceed 90 percent. For those banks, M&A may be their only option to survive by delivering cost synergies, strengthening their focus on selected client segments or products, and improving their ability to innovate or to engage clients. Those who are shrewd and quick to act with strategic acquisitions and divestments will succeed, whereas those who lag will suffer. The resulting shakeout might even see some big names disappear, as based on our analysis more than half of the banks with exceptionally high cost-to-income ratios are national champions and well-known brands.

Life after COVID-19: building a new banking landscape through M&A

16European Retail Banking Radar

The rise of strategic partnershipsIn addition to a rise in M&A, we also predict a rise in strategic partnerships, particularly across smaller banks, as they seek to gain reach quickly and effi-ciently. We have previously explored four new business models—universal, direct bank specialist, digital, and lifestyle platforms—as possible strategies for retail banks to reshape their cost base, but conversely, as banks differentiate themselves in a new retail banking landscape, we may actually see an increase in partnerships and collaborations as banks leverage capabilities off others through back-end operations, technology platforms, or shared supplier networks. This need for efficiencies will drive a culture of retail banking partnerships.

It’s not just about strategic mergers, acquisitions, and divestments—it’s also about what followsLet’s not forget that M&A is just a facilitator for a much broader plan. As already discussed, making an acquisition just after a crisis—when valuations are low and targets plentiful—is not enough. Every M&A is a massive change. How companies create value from the acquisition and how they manage the integration is key. The process requires:

— Strong due diligence and realistic synergy expectations

— A practical and realistic plan for integrating both entities, including multiple dependencies

— Consistent care and communication to all stakeholders, such as clients, employees, and investors

— Paying close attention to external market conditions and not being consumed with internal integration operations

— High rates of employee retention and strong employee motivation

— A conscious commitment to fuse and align the unique cultural working practices of the two organizations

A realistic and actionable post-merger plan will be the difference between a successful and canny strategic investment versus an expensive and potentially irreversible mistake.

For some players, M&A may be the only optionDuring the previous global economic crisis, financial distress was a key driver of M&A. This time, banks are better capitalized in general, but a prolonged recession and resulting rise in impairments could lead to some banks facing capital shortfalls. As a result, the potential balance sheet stress driven by a sharp increase in impairments, together with a decline in revenues, could lead to some lenders being forced into M&A. Our database analysis indicates that domestic mergers and acquisitions are often driven by the need for scale and cost reduction. In 80 percent of cases, the acquired entity had substantially higher cost-to-income ratio than the acquirer and well beyond the European average of 60 percent. Organizations with either of these issues should take heed.

The need for efficiency—based on scale and focus—will lead to divestment of non-core businesses and acquisitions to strengthen the coreAs retail banks revise their future operating models and refocus their core business offering, some might seek to divest assets where they are unable to maintain competitive edge in the mid-term, such as asset management subsidiaries given the rapidly consolidating industry brought about by lower costs and better performance of the global asset manage-ment giants. Some retail banks will need help in bolstering and scaling up their core business (for example, profitable segments or products) or strengthening their franchise in certain geographies. Some might opt to “source” new capabilities, such as analytics or AI. One way to achieve this—quickly—is through acquiring businesses that help improve scale and deliver cost synergies.

Meanwhile, the fintech landscape has seen an emerging dichotomy with the valuations of estab-lished players with a track record of profitability at all-time highs, while those that are still unprofitable may become a distressed acquisition for opportunis-tic buyers looking to acquire new technologies or a new customer base.

17European Retail Banking Radar

Why the only constant will be changeRecent socioeconomic disruption has radically changed the economic outlook. Never has there been a better opportunity—or more dire need—for retail banks to reshape their cost base and revise their long-term future operating model. Quick to appear and slow to recede, this crisis is unprecedented in magnitude and the economic relief we are seeing across Europe will only be temporary; banks will continue to feel the effects of the crisis for the next two to three years. Banks cannot carry on as before. Change is needed for the vast majority of European retail banks, requiring bold decisions and quick action.

In this series, we have examined and summarized key opportunities and risks across retail banking over the next few years in light of the COVID-19 crisis. After months of lockdown, customers’ banking habits—and indeed expectations—have shifted irreversibly toward digital banking. Retail banks have come under strain as revenues drop while operating costs have not, leading to a critical review of existing infrastructure, specifically bank branches, employee skill sets, and even employee workplaces. Cost reduction is paramount, but it won’t be enough—banks need to consider a complete transformation of their operating model, incrementally implemented through minimum viable operating models to shape the future of the bank. For many banks, M&A will be a viable way to make quick and impactful changes to their operating model and the resulting surge in M&A activity will present a multitude of opportunities. While the COVID crisis in Europe is subsiding, it is far from over. Only those who embrace the urgency for change, make bold decisions, and take quick action will survive.

A mixed outlook for fintechsWhile the fintech industry covers a broad spectrum of business models, one issue remains the same for all: capital raising for fintechs has been declining in 2020, putting pressure on the industry. While some business models will be more resilient than others, many fintech start-ups have struggled during the lockdown, with several not qualifying for government subsidies.

Those who offer loan products need to be sensitive to changed client behaviors—decreased demand for lending and increased risk of default could be a potent combination creating a difficult future and potentially failure. Challenger banks less reliant on lending may be in a better position based on strong brand positioning and their ability to scale up their digital operations to meet the needs of a more digitized banking landscape. However, these banks will also face challenges to their top line due to reduced consumer spend and cross-border travel.

Technology fintechs, such as payment providers, might find new partnership opportunities with banks and retailers.

We believe that many mid-sized and small fintechs will come under funding pressure, which will divide the industry into winners and losers. For some, the only option will be to sell. For others, this could provide opportunities to augment their capabilities at a good price and expand their partnership ecosystem to include, for example, established banks.

18European Retail Banking Radar

Roberto FreddiPrincipal, Milan [email protected]

Sameer PethePrincipal, London [email protected]

Ettore Pastore Partner, Milan [email protected]

Simon KentPartner, London [email protected]

Daniela ChikovaPartner, Vienna [email protected]

Authors

Krystian KamykPartner, Warsaw [email protected]

19European Retail Banking Radar

For more information, permission to reprint or translate this work, and all other correspondence, please email [email protected]. A.T. Kearney Korea LLC is a separate and independent legal entity operating under the Kearney name in Korea. A.T. Kearney operates in India as A.T. Kearney Limited (Branch Office), a branch office of A.T. Kearney Limited, a company organized under the laws of England and Wales. © 2020, A.T. Kearney, Inc. All rights reserved.

As a global consulting partnership in more than 40 countries, our people make us who we are. We’re individuals who take as much joy from those we work with as the work itself. Driven to be the difference between a big idea and making it happen, we help our clients break through.

kearney.com

kearney.com