NEW Actian PowerPoint Template and Guide - PIDX · Upsetting the Status Quo ... does not warrant...

35

“How increased visibility into e-Invoicing & other P2P KPI Metrics speeds up Invoice Payment while also improving Operator / Supplier Relations” Daryl Fullerton Oil & Gas Industry Principal PIDX EU Conference – April 30 th 2013

Transcript of NEW Actian PowerPoint Template and Guide - PIDX · Upsetting the Status Quo ... does not warrant...

“How increased visibility into e-Invoicing & other P2P KPI Metrics speeds up Invoice Payment while also improving Operator / Supplier Relations”

Daryl Fullerton

Oil & Gas Industry Principal

PIDX EU Conference – April 30th 2013

Presentation Agenda / Discussion Points P2P Invoice Status Visibility within the Oil & Gas Industry at present.

Key Drivers for increased visibility on P2P metrics.

• Operator Drivers

• Supplier Drivers

Examples of KPI Metrics used in P2P/ e-invoice Initiatives

Visibility Dashboards in Action @ Marathon Oil

Challenges / Complexities faced in implementing.

• Remittance Data, Workflow Status, PIDX Invoice response.

Impact of Dashboards on Faster Invoice Payment.

Other Wins – Lower Costs, Effect of Operator / Supplier Relations

Key Takeaways

Questions & Answers

Confidential © 2012 Actian Corporation 2

Invoice Status Visibility – O&G Industry (Present) Many Operators have e-invoice Initiatives in operation or

underway.

On average 35% Electronic / EDI V 65% Paper

Very few provide Visibility on the necessary KPIs to fully leverage the process efficiencies and cost reductions.

Many do not provide Workflow Status / Remittance Data, under 8% provide full visibility on Invoice Status.

Cost per 1 Page Invoice processing ranges from $1.30 to $67.30 all inclusive.

Right First Time needs improved- Rework is high, approx 3 - 7%

Automated Validation extremely low

Many SME’s and “Mom & Pops” type organizations are struggling with DSO, some even going to the wall through lack of Finance to fund DSO.

Confidential © 2012 Actian Corporation 4

Examples of P2P KPIs used in e-Invoice Initiatives

Confidential © 2012 Actian Corporation 5

Financial Metrics Days Payables Outstanding (DPO) Figure % Payables Compliance with Net Terms Impact of Errors on Average DPO Alignment

Quality / Compliance Metrics Right First Time Purchase Orders Right first Time Invoices Three Way Match – PO, Invoice , Remittance

Process Efficiencies Average Time to Process Invoice AP Team Size to Total Invoice Ratio

Environmental Efficiencies Percentage Paper V Electronic Ratio Quarter on Quarter Paper Reduction %

Operator Drivers for KPI Visibility

Improve Days Payables Outstanding (DPO)

Reduce Accounts Payable (AP) Costs

Meet Supplier Charter of Net 30 Days

Higher 3 Way Match Ratio

Improve Supplier Relations

Confidential © 2012 Actian Corporation 6

Supplier / Service Co Drivers for KPI Visibility

Reduction in Days Sales Outstanding (DSO)

Reduce costs & time spent on Invoice Chasing

Improved Forecasting on Accounts Receivable

More Accurate Cashflows

Ability to use Dashboard Reports on Invoice Status to provide assurance when raising finance for short to medium term.

Confidential © 2012 Actian Corporation 7

Finance for Days Sales Outstanding (DSO)

Factoring (Cost in region or 1.25-4% )

Invoice Discounting / Dynamic Discounting (.25 to 7%)

Bank Finance (Overdraft)

New Investment

Confidential © 2012 Actian Corporation 8

Systems Vendors- Drivers for KPI Visibility

9

Visibility Dashboards in Action @

Marathon Oil - Key P2P Initiative Objectives

10

Increase Efficiencies within P2P Process Invoices Submission / Approval / Payment

Drive Better relations with Suppliers Invoice Error Reduction Faster Payment DPO Alignment to Net Terms Better Supplier relations

Reduce Costs Automate & Reduce Manual Entry Supplier Costs – Time o/s Chasing Invoices

Improve P2P Reporting Capabilities Management Information Visibility Reporting to Suppliers

Learning and Continuous Improvement Marathon Side Improvements Supplier Side Improvements Drive Success to other Areas of Marathon Oil Corp

Challenges faced on Marathon’s “Journey to Success”

11

Upsetting the Status Quo Benefits of moving to Electronic Business Case Managing the Risks of Switchover

Suppliers e-Commerce Capability Technology / Systems Integration Experience

Change in Process

On-boarding / Handholding Error Resolution Ticket Management

Fear of the Dark Hole

Giving Suppliers Visibility on Status Demonstrating Improvements on DSO

A Joint approach to Invoice Errors & DPO Alignment

12

Education: - Establish and educate that the problem was from both sides (a shared problem) - Needed a way of sharing with Supplier the Impact of Errors on their Days Sales Outstanding - Show trending of better Right First Time Invoices on the reduction in DSO figure.

Provide Visibility on Problem: -Visibility needed to be shared:

- DSO Trends - Right First Time Invoices - Invoices in Error

Improve: - Show the improvements to the Supplier

- Faster Invoice Processing - DSO Reduction

- Share the Success – Net Terms Alignment

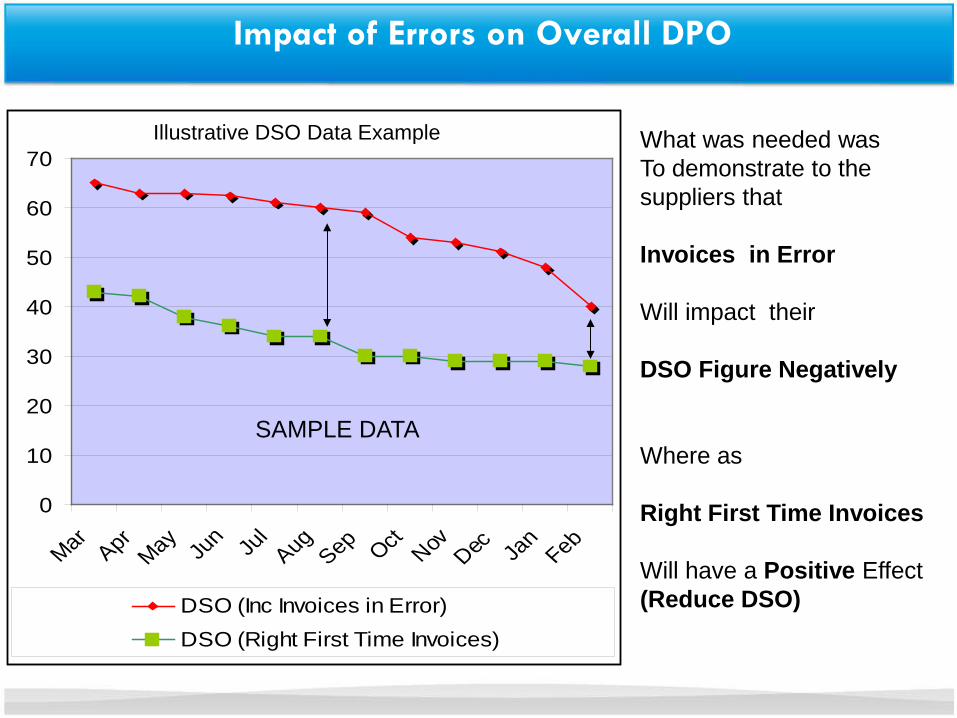

Impact of Errors on Overall DPO

0

10

20

30

40

50

60

70

MarApr

MayJu

n Jul

AugSep Oct Nov Dec Ja

nFeb

DSO (Inc Invoices in Error)DSO (Right First Time Invoices)

What was needed was To demonstrate to the suppliers that Invoices in Error Will impact their DSO Figure Negatively Where as Right First Time Invoices Will have a Positive Effect (Reduce DSO)

Illustrative DSO Data Example

SAMPLE DATA

Impact of Right First Time Invoices on DPO / DSO

Five Step Approach 1. Visibility on current DPO against Net Terms (DSO Dashboards)

2. Visibility on Invoice Errors and Exceptions

3. Collaborative Approach with Suppliers on Fixing Errors

4. Live Reporting on Invoice Error Reduction 5. Show Supplier improvement on Suppliers Days Sales Outstanding (ongoing access)

Visibility

Giving Marathon Suppliers Visibility was Key

Marathon Oil Provided Dashboard Visibility to Suppliers

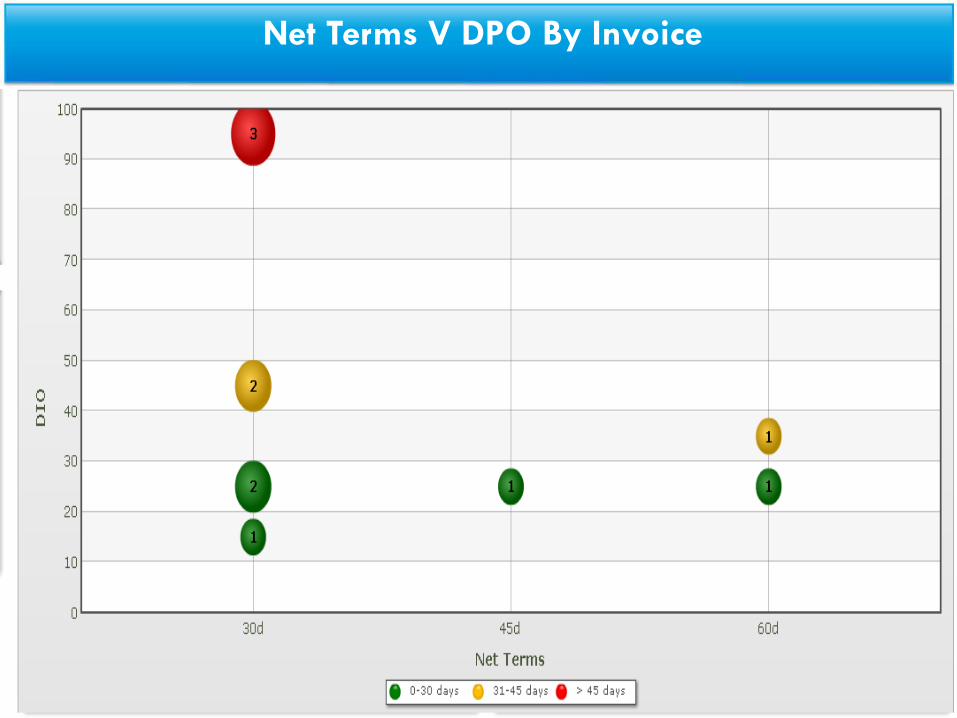

DPO Report - Drill Down to Invoice Level

DPO Percentage by Month

Net Terms V DPO By Invoice

Dashboard Visibility Provided to Suppliers

Visibility

Likewise for Invoices in Error

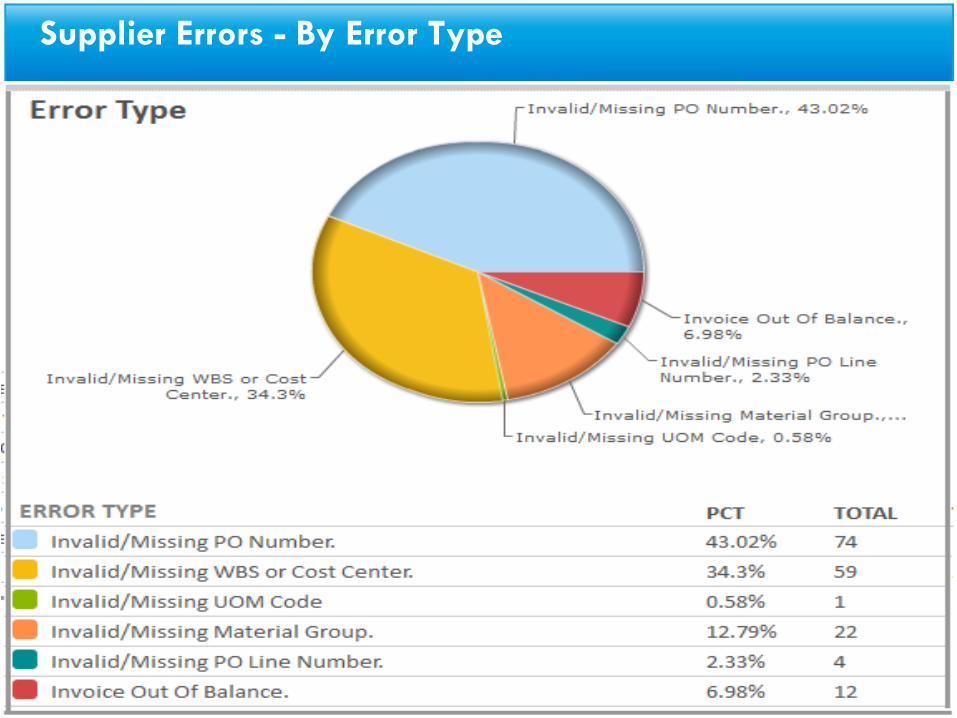

Marathon Oil Errors Management - Visibility to Suppliers

SUPPLIER 1

SUPPLIER 2SUPPLIER 3

SUPPLIER 4

SUPPLIER 5

SUPPLIER 6

SUPPLIER 7

Supplier Errors - By Error Type

0

510

1520

25

3035

4045

50

Mar AprMay Ju

n Jul

Aug Sep Oct Nov Dec Jan

Feb

DSO (Inc Invoices in Error)DSO (Right First Time Invoices)

2014 Desired State - Minimal Error impact DPO

Desired State is that there are so few errors that the impact on Days Sales Outstanding is as Close to Zero as possible Or that there are ZERO Errors And 100% Right First Time Invoices

2014 Illustrative DSO Data Example

Marathon Oil “Success” – What does it Look Like ?

25

Marathon Success : Compliance with Supplier Charter on Net Terms Full Visibility on status of all Invoices

Drill down ability to Invoice Level. Workflow approval status.

MOC Cost per Invoice Processed Less than $1 Better Invoice Errors and Exceptions Mgt Reduced time on Supplier Calls

Supplier Success: All Invoices Paid within Net Terms Rework Eliminated – Right First Time Invoice Reduced AR Costs Eliminate the need for invoice Chasing. Better Operator / Supplier Relations

Challenges / Complexities faced in implementing.

Reporting Time-lag - Electronic / EDI V Paper

Not All Operators systems provide Invoice Response

Only a few Operators Provide Remittance Data

Work Flow Status not always provided.

AP to document and Log Invoice Error Reasons Properly.

Confidential © 2012 Actian Corporation 26

Challenges / Complexities faced in implementing.

Reporting Time-lag - Electronic / EDI V Paper

Not All Operators systems provide Invoice Response

Only a few Operators Provide Remittance Data

Work Flow Status not always provided.

AP to document and Log Invoice Error Reasons Properly.

Ways to Overcome

Extract of Workflow Status on Paper Invoices.

Invoice Payment Extract from ERP – Feeds Remittance Data

Confidential © 2012 Actian Corporation 27

Impact of Dashboards on Faster Invoice Payment. Supplier has ongoing access to visibility

on Invoice Status thereby providing a focus for timely and accurate invoicing.

Reduces the gap between Invoice Date and Receipt Date

Visibility on Impact or Invoices in Error on DSO helps drive better Right First Time Invoice Ratio.

AP team have more time for approval processing invoices rather than fielding telephone calls on invoice status.

AP team can focus on ways of driving further efficiencies

Confidential © 2012 Actian Corporation 28

Bank Finance (what do they want ?) Always require:

Detailed Cashflow Forecasts

Detailed Status on Current Debtors Listing

Proof of Net Terms Agreed

Confidential © 2012 Actian Corporation 29

Bank Finance (what do they want ?) Banks always require:

Detailed Cashflow

Detailed Status on Debtors Listing

Proof of Net Terms Agreed

Improving the chance of securing Bank Finance:

Assurance to Bank on past DSO to Net Terms Alignment, ie 28.8 days

Assurance on Right First Time Invoice track record 100% Right First Time Invoices – Detailed Report

Confidential © 2012 Actian Corporation 30

100%

Right First Time

Other Wins from increased Supplier Visibility

Lower costs for Operator & Supplier • Making Calls, Fielding Calls, Invoice Rework

Better Operator Supplier Relations

Less Drain on other Resources • Supply Chain Managers, Account executives

Improved Cashflows for Suppliers

Higher degree of Assurance on Invoice payment for Finance Commitments

Less Suppliers going to Wall

Confidential © 2012 Actian Corporation 31

Key Takeaways

Sharing Visibility on Invoice Status / P2P Metrics with Suppliers reduces AP / AR team costs.

Show Right First Time Invoices KPIs to further reduce costs

Share the Success – Others will follow.

Confidential © 2012 Actian Corporation 32

Confidential © 2012 Actian Corporation 33

Questions

?

? ?

www.actian.com facebook.com/actiancorp @actiancorp

Thank You

Confidential © 2012 Actian Corporation 34

Disclaimer

This document is for informational purposes only and is subject to change at any time without notice. The information in this document is proprietary to Actian and no part of this document may be reproduced, copied, or transmitted in any form or for any purpose without the express prior written permission of Actian. This document is not intended to be binding upon Actian to any particular course of business, pricing, product strategy, and/or development. Actian assumes no responsibility for errors or omissions in this document. Actian shall have no liability for damages of any kind including without limitation direct, special, indirect, or consequential damages that may result from the use of these materials. Actian does not warrant the accuracy or completeness of the information, text, graphics, links, or other items contained within this material. This document is provided without a warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability, fitness for a particular purpose, or non-infringement.

35 Confidential © 2012 Actian Corporation