Stock market integration: A multivariate GARCH analysis on Poland

Upload

syrto-projectCategory

view

562download

0

Network and risk spillovers: a multivariate GARCH perspective

SYstemic Risk TOmography:

Signals, Measurements, Transmission Channels, and Policy Interventions

M. Billio, M. Caporin, L. Frattarolo, L. Pelizzon Università Ca’ Foscari, Università degli Studi di Padova, SAFE, House of Finance,Goethe University Frankfurt

Final SYRTO Conference - Université Paris1 Panthéon-Sorbonne February 19, 2016

This project has received funding from the European Union’s

Seventh Framework Programme for research, technological

development and demonstration under grant agreement n° 320270

www.syrtoproject.eu

This document reflects only the author’s views.

The European Union is not liable for any use that may be made of the information contained therein.

Spatial Econometrics and Risk Empirical results Concluding Remarks

Motivation

Explaining volatility spillover through information on cross-countryexposure

Use cross-country exposure to identify a dynamic network structure

Introduce them into a variance model to capture spillovers

Generalize a variance model to allow for spillover driven by atime-varying network

Show how to use the model for spillover analysis, varianceforecasting and policy intervention

Spatial Econometrics and Risk Empirical results Concluding Remarks

Spatial proximity and financial closeness

In Spatial Econometrics subjects of the analysis are neighbors in aphysical sense, and distance between subjects is measured by meansof geographical distance

From a financial viewpoint a neighboring relation (closeness,proximity) is a more elusive concept

... that cannot be translated into a physical measure(Fernadez-Aviles et al., 2012)

Possible solutions

subjects (companies) being in the same economic sector (Caporinand Paruolo, 2015)causality relations (Billio et al., 2015)cross-country exposure (this study)

Spatial Econometrics and Risk Empirical results Concluding Remarks

Financial proximity and networks

In spatial econometrics distances are collected into spatial weightmatrices W which are symmetric (before row normalization) andpositive valued

In financial applications W need not to be symmetric (despite weassume it is positive valued)

W matrices are also equivalent to adjacency matrices associatedwith a weighted directed network, therefore, from a financialviewpoint, proximity relations define networks across subjects, and, agiven network existing across subjects allows structuring a spatialweight matrix

Spatial Econometrics and Risk Empirical results Concluding Remarks

Proximity matrices for model construction

Caporin and Paruolo (2015) introduce a more general proximitymatrix

P = ⇢1I + ⇢2W

Motivations: P is a sparse matrix driven by few unknownparameters; P structure depends on economically relevant relations

Easily generalized to allow for heterogenous reaction replacing ⇢jwith a diagonal matrix

This study: allows for dynamic in W ; allows for left and right

multiplication to recover di↵erent interpretations (contributing

to/receiving from a network)

PL = diag (⇢0) I + diag (⇢1,L)Wt

PR = diag (⇢0) I +Wtdiag (⇢1,R)

Spatial Econometrics and Risk Empirical results Concluding Remarks

Proximity matrices for covariance models

Covariance models (GARCH/DCC-type, Stochastic Volatility,Realized Covariance/Correlation) su↵er for the curse ofdimensionality challenging their use with large cross-sectionaldimension for spillover analyses

Intuition: use proximity matrices to structure the model parametersand make parameters number linear in the cross-sectional dimension

Intuition: dynamic proximity matrices induce dynamic in theparameters at limited cost (they are assumed to be known)

We focus on BEKK-type specifications as we focus on covariancedynamic and for the availability of asymptotic theory

Spatial Econometrics and Risk Empirical results Concluding Remarks

BEKK and the curse of dimensionality

BEKK model

Given a vector yt of n cross-sectional observations at time t defineut = yt � y with y being the vector of sample means, we have:

ut = ⌃1/2t ✏t ✏t ⇠ N (0, In) , t = 1, . . . ,T

⌃t = CC

0 + Aut�1u0t�1A

0 + B⌃t�1B0

where A,B and C are n ⇥ n matrices and ⌃1/2t is the Cholesky

decomposition of ⌃t .

Computationally demanding with even moderate cross-sectionaldimension (n > 3) unfeasible for n > 10 (n = 10 ) 255 parameters)

Usually restriction on A and B are imposed; typical example A,B arediagonal (D-BEKK) but we fully loose volatility spillover

Spatial Econometrics and Risk Empirical results Concluding Remarks

Spatial BEKK (S-BEKK)

A and B (BEKK parameter matrices) are proximity matrices and dependon an exogenous sequence of weights matrices Wt

⌃t = CC

0 + A (Wt) ut�1u0t�1A (Wt)

0 + B (Wt)⌃t�1B (Wt)0

Nests the D-BEKK model but allows cross spillovers from di↵erentelements of ⌃t

A and B are time varying due to the time variation of Wt

The total number of parameters is linear in the cross-sectionaldimension

Spatial Econometrics and Risk Empirical results Concluding Remarks

Spatial BEKK (S-BEKK)

Extend proximity matrices with left and right multiplication

A and B proximity matrices with right and left multiplicationspecification

AL (Wt) = diag (a0L) I + diag (a1L)Wt

BL (Wt) = diag (b0L) I + diag (b1L)Wt

AR (Wt) = Idiag (a0R) +Wtdiag (a1R)

BR (Wt) = Idiag (b0R) +Wtdiag (b1R)

Wt is the time dependent foreign claims network

Left and right multiplication models allows focusing on di↵erentaspect of risk propagation

With right multiplication the parameters multiply the source of risk:focus on risk spreaders entities

With left multiplication the parameters multiply the recipient of risk:focus on risk receivers entities

Spatial Econometrics and Risk Empirical results Concluding Remarks

Left and Right Indirect E↵ect

Extend notion of direct and indirect e↵ect of shock di↵usions

LeSage and Pace (2014) SEM

vt = (In + ✓W ) ut = v

0t + v

1t

v

0i,t = [Inut ]i = ui,t Direct E↵ect

v

1i,t = [✓Wut ]i = [W ✓ut ]i = ✓

nX

j=1

!i,juj,t Indirect E↵ect

Di↵erent Left(Risk Receivers), Right (Risk Spreaders),ARCH(ShockResponse)and GARCH (Persistence) Indirect e↵ects due to the noncommutativity of diagonal parameters and network matrices

v

1L,i,t = [A1,LWut ]i = a1,L,i

nX

j=1

!i,juj,t

m

1R,i,t = [WB1,Rut ]i =

nX

j=1

!i,jb1,R,juj,t

Spatial Econometrics and Risk Empirical results Concluding Remarks

Model estimation

Standard BEKK model asymptotic properties

consistency, Jeantheau (1988), under the existence of sixth-ordermomentsasymptotic normality, Comte and Lieberman (2003), under theexistence of eigth-order moments, and Hafner and Preminger (2009)for VECH under the existence of sixth-order moments

In our case we ensure ergodicity and stationarity followingBoussama, Fuchs and Stelzer (2011) and constrain the maximumspectral radius

maxt2[1,T ]

⇢ (AM (Wt)⌦ AM (Wt) + BM (Wt)⌦ BM (Wt)) < 1

...and recover consistency and asymptotic normality assuming theexistence of the sixth-order moments

Spatial Econometrics and Risk Empirical results Concluding Remarks

Inference-based networks

Intuition: merge cross-holding networks and estimated parameters torecover a new network combining observed links (and their size)with statistically relevant spillovers

Filtered (inference-based) network (element i , j with i 6= j)

⇥WA,L

⇤t,i,j

= a1,L,iwt,i,j ⇥ (1� Pval (a1,L,i ))

Four di↵erent inference-based networks obtained from ARCH andGARCH coe�cient matrices for both the Left and Rightmultiplication cases

Spatial Econometrics and Risk Empirical results Concluding Remarks

Inference-based networks

Four di↵erent interpretation to the filtered networks

WA,L: focus on risk receivers entities and response to shocksWB,L: focus on risk receivers entities and persistence of shocksWA,R : focus on risk spreaders entities and response to shocksWB,R : focus on risk spreaders entities and persistence of shocks

Filtered networks allows analyzing entities links from a di↵erentviewpoint

Spatial Econometrics and Risk Empirical results Concluding Remarks

Variance decomposition

shock response (ARCH) persistence (GARCH)

Costant [CC 0]i,j

direct v

0L,i,t�1v

0L,j,t�1

h⌦0,0

L,t�1

i

i,j

indirect v

1L,i,t�1v

1L,j,t�1

h⌦1,1

L,t�1

i

i,j

mixed v

1L,i,t�1v

0L,j,t�1 + v

0L,i,t�1v

1L,j,t�1

h⌦1,0

L,t�1

i

i,j+

h⌦0,1

L,t�1

i

i,j

Where, for example:

h⌦1,1

L,t�1

i

i,j= Cov

�m

1L,i,t�1,m

1L,j,t�1

��It�2,W

�

At the portfolio level (suppressing time-dependence)

V [w0y ] = �2

Constant + �2Direct + �2

Indirect + �2Mixed

Diversification benefits could come from each component

Spatial Econometrics and Risk Empirical results Concluding Remarks

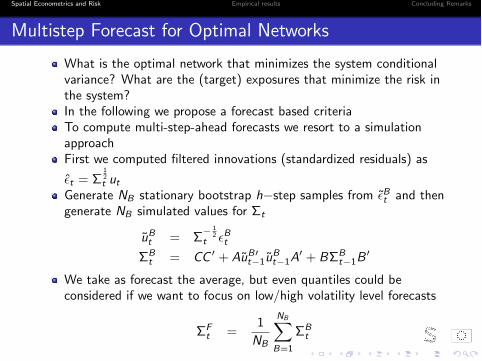

Multistep Forecast for Optimal Networks

What is the optimal network that minimizes the system conditionalvariance? What are the (target) exposures that minimize the risk inthe system?In the following we propose a forecast based criteriaTo compute multi-step-ahead forecasts we resort to a simulationapproachFirst we computed filtered innovations (standardized residuals) as

✏t = ⌃12t ut

Generate NB stationary bootstrap h�step samples from ✏Bt and thengenerate NB simulated values for ⌃t

u

Bt = ⌃

� 12

t ✏Bt⌃B

t = CC

0 + Au

B0t�1u

Bt�1A

0 + B⌃Bt�1B

0

We take as forecast the average, but even quantiles could beconsidered if we want to focus on low/high volatility level forecasts

⌃Ft =

1

NB

NBX

B=1

⌃Bt

Spatial Econometrics and Risk Empirical results Concluding Remarks

Optimal networks and target exposures

Conditional on bootstrapped innovations ✏[b]T+l with b 2 [1, . . . ,NB ]find the optimal network by minimizing the average h-step forecastedvariance path of the EW index with respect to the network

minvecW ?

1

h

hX

l=1

1

n

21

0⌃FT+l (W

?) 1

s.t. 0 [W ?]i,j 1 for i , j = 1 . . . n

Tr (W ?) = 0

We compare the obtained optimal volatility proxy with the realizedvolatility proxy, to have an indication of variance reduction robustagainst model misspecification.

Var✓1

n

1

0y

?T+l

���� IT+l�1

◆'

✓1

n

1

0u

?T+l

◆2

Spatial Econometrics and Risk Empirical results Concluding Remarks

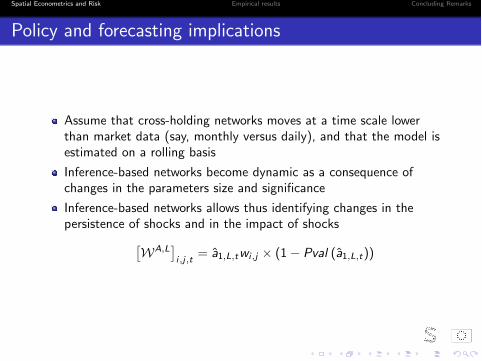

Policy and forecasting implications

Assume that cross-holding networks moves at a time scale lowerthan market data (say, monthly versus daily), and that the model isestimated on a rolling basis

Inference-based networks become dynamic as a consequence ofchanges in the parameters size and significance

Inference-based networks allows thus identifying changes in thepersistence of shocks and in the impact of shocks

⇥WA,L

⇤i,j,t

= a1,L,twi,j ⇥ (1� Pval (a1,L,t))

Spatial Econometrics and Risk Empirical results Concluding Remarks

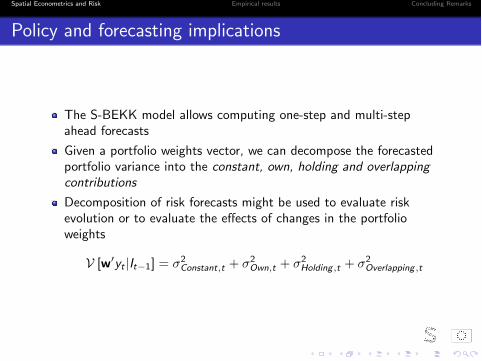

Policy and forecasting implications

The S-BEKK model allows computing one-step and multi-stepahead forecasts

Given a portfolio weights vector, we can decompose the forecastedportfolio variance into the constant, own, holding and overlapping

contributions

Decomposition of risk forecasts might be used to evaluate riskevolution or to evaluate the e↵ects of changes in the portfolioweights

V [w0yt |It�1] = �2

Constant,t + �2Own,t + �2

Holding ,t + �2Overlapping ,t

Spatial Econometrics and Risk Empirical results Concluding Remarks

Policy and forecasting implications

Moreover, as forecasts are function of a given network, assuming thestability of weights and other model parameters, the S-BEKK modelcan be used to determine the impact of network changes

The di↵erential impact of a network change, for instance movingfrom the actual to the target exposure network can be easilycomputed as

� (W ) = V [w0yt |It�1,Wt ]� V [w0

yt |It�1,W?t ]

The computation of e↵ects induced by a network change can becomputed on one-step-ahead as well as multi-step-ahead forecasts

Spatial Econometrics and Risk Empirical results Concluding Remarks

Data description

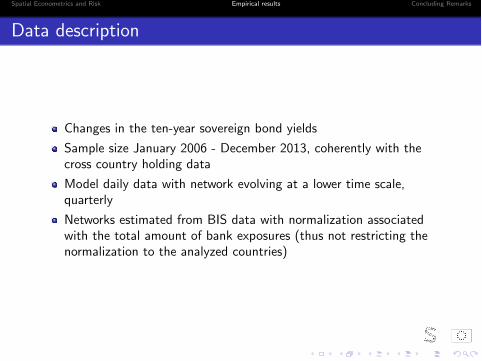

Changes in the ten-year sovereign bond yields

Sample size January 2006 - December 2013, coherently with thecross country holding data

Model daily data with network evolving at a lower time scale,quarterly

Networks estimated from BIS data with normalization associatedwith the total amount of bank exposures (thus not restricting thenormalization to the analyzed countries)

Spatial Econometrics and Risk Empirical results Concluding Remarks

Dependence Network from Foreign Claims

Spatial Econometrics and Risk Empirical results Concluding Remarks

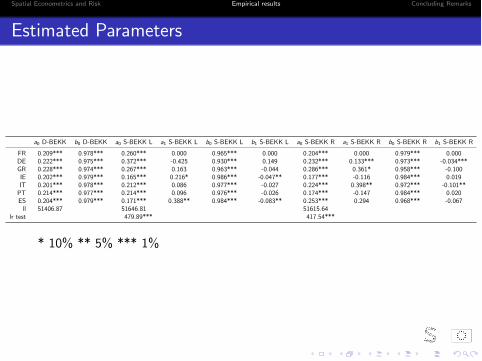

Estimated Parameters

a0 D-BEKK b0 D-BEKK a0 S-BEKK L a1 S-BEKK L b0 S-BEKK L b1 S-BEKK L a0 S-BEKK R a1 S-BEKK R b0 S-BEKK R b1 S-BEKK R

FR 0.209*** 0.978*** 0.260*** 0.000 0.965*** 0.000 0.204*** 0.000 0.979*** 0.000DE 0.222*** 0.975*** 0.372*** -0.425 0.930*** 0.149 0.232*** 0.133*** 0.973*** -0.034***GR 0.228*** 0.974*** 0.267*** 0.163 0.963*** -0.044 0.286*** 0.361* 0.958*** -0.100IE 0.202*** 0.979*** 0.165*** 0.216* 0.986*** -0.047** 0.177*** -0.116 0.984*** 0.019IT 0.201*** 0.978*** 0.212*** 0.086 0.977*** -0.027 0.224*** 0.398** 0.972*** -0.101**PT 0.214*** 0.977*** 0.214*** 0.096 0.976*** -0.026 0.174*** -0.147 0.984*** 0.020ES 0.204*** 0.979*** 0.171*** 0.388** 0.984*** -0.083** 0.253*** 0.294 0.968*** -0.067ll 51406.87 51646.81 51615.64

lr test 479.89*** 417.54***

* 10% ** 5% *** 1%

Spatial Econometrics and Risk Empirical results Concluding Remarks

AL

Networks

edgeweight ) a1,L,iwt,i,j ⇥ (1� Pval (a1,L,i ))

In red positive coe�cents, in blue negative

Spatial Econometrics and Risk Empirical results Concluding Remarks

Inference-based BL

Networks

edgeweight ) b1,L,iwt,i,j ⇥⇣1� Pval

⇣b1,L,i

⌘⌘

In red positive coe�cents, in blue negative

Spatial Econometrics and Risk Empirical results Concluding Remarks

Inference-based AR

Networks

edgeweight ) a1,R,iwt,i,j ⇥ (1� Pval (a1,R,i ))

In red positive coe�cents, in blue negative

Spatial Econometrics and Risk Empirical results Concluding Remarks

Inference-based BR

Networks

edgeweight ) b1,R,iwt,i,j ⇥⇣1� Pval

⇣b1,R,i

⌘⌘

In red positive coe�cents, in blue negative

Spatial Econometrics and Risk Empirical results Concluding Remarks

Variance decomposition Risk Receivers (L)

Most comes from the direct contribution

Negative contributions are possible and lead to diversificationbenefits

2006 2007 2008 2009 2010 2011 2012 2013 2014−0.02

−0.01

0

0.01

0.02

0.03

0.04

0.05

ConstantMixedIndirect

Spatial Econometrics and Risk Empirical results Concluding Remarks

Variance decomposition Risk Spreaders (R)

Most comes from the direct contribution

Negative contributions are possible and lead to diversificationbenefits

2006 2007 2008 2009 2010 2011 2012 2013 2014

0

0.05

0.1

0.15

0.2

0.25

ConstantMixedIndirect

Spatial Econometrics and Risk Empirical results Concluding Remarks

Optimal networks

Forecast one quarter ahead for quarter II of 2010

Recover the optimal target network exposure for both risk receiversand risk spreaders

Constrained optimization implies a redistribution of the claimsamong the considered countries

Unconstrained optimization means that the total amount of claimschanges for each country

Spatial Econometrics and Risk Empirical results Concluding Remarks

Optimal vs. Realized EW variance proxy

01/04/2010 01/05/2010 01/06/2010 01/07/20100

0.01

0.02

0.03

0.04

0.05

Receivers Model Reconstructed Volatility Proxy, Estimation Sample Q1 2006 Q1 2010Receivers Model Constrained Reconstructed Volatility Proxy, Estimation Sample Q1 2006 Q1 2010Realized

01/04/2010 01/05/2010 01/06/2010 01/07/20100

0.005

0.01

0.015

0.02

0.025

Spreaders Model Reconstructed Volatility Proxy, Estimation Sample Q1 2006 Q1 2010Spreaders Model Constrained Reconstructed Volatility Proxy, Estimation Sample Q1 2006 Q1 2010Realized

Spatial Econometrics and Risk Empirical results Concluding Remarks

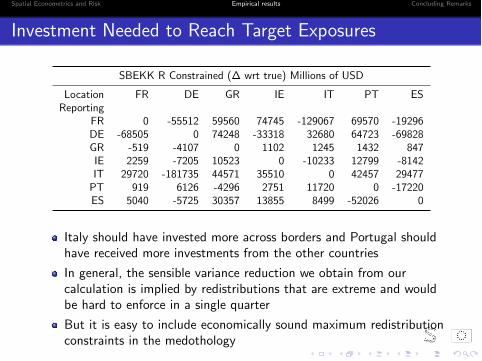

Investment Needed to Reach Target Exposures

SBEKK R Constrained (� wrt true) Millions of USD

Location FR DE GR IE IT PT ESReporting

FR 0 -55512 59560 74745 -129067 69570 -19296DE -68505 0 74248 -33318 32680 64723 -69828GR -519 -4107 0 1102 1245 1432 847IE 2259 -7205 10523 0 -10233 12799 -8142IT 29720 -181735 44571 35510 0 42457 29477PT 919 6126 -4296 2751 11720 0 -17220ES 5040 -5725 30357 13855 8499 -52026 0

Italy should have invested more across borders and Portugal shouldhave received more investments from the other countries

In general, the sensible variance reduction we obtain from ourcalculation is implied by redistributions that are extreme and wouldbe hard to enforce in a single quarter

But it is easy to include economically sound maximum redistributionconstraints in the medothology

Spatial Econometrics and Risk Empirical results Concluding Remarks

Concluding remarks

Concluding remarks

In the European sovereign bond markets part of spillover e↵ects canbe traced back to a physical claim channel: banks’ foreign exposures

Germany, Italy and, to a lesser extent, Greece are playing a centralrole in spreading risk

Ireland and Spain are the most susceptible receivers of spillovere↵ects

Acting on these physical channels before the sovereign crisis, itwould have been possible to have a clear risk mitigation outcome

In progress

Di↵erent Asset Classes (In particular equity )

Inclusion of more countries

Joint Left and Right multiplication model

introduce in the model more networks, jointly, to test and comparethem

Spatial Econometrics and Risk Empirical results Concluding Remarks

Thank You!

![Multivariate DCC-GARCH Model - COnnecting REpositories · introduced the DCC-GARCH model [11], which is an extension of the CCC-GARCH model, for which the conditional correlation](https://static.fdocuments.us/doc/165x107/5e217962f57ff72c8e79583c/multivariate-dcc-garch-model-connecting-repositories-introduced-the-dcc-garch.jpg)