Netherlands: Exchange of information versus tax … report... · 2015-06-10 · Netherlands:...

13

1 Netherlands: Exchange of information versus tax solutions of equivalent effect Prof. Dr. Sjoerd Douma 1 1. Introduction The topic of exchange of information is very much on the political agenda in the Netherlands. In the context of the domestic and international debate on the taxation of multinationals, the Dutch government actively supports EU and OECD initiatives on exchange of information and country-by-country reporting. 2 The Dutch government aims at the international implementation of automatic exchange of information. It wants to use the momentum created by the US Foreign Account Tax Compliance Act (FATCA) and by the initiative of the so- called G5-countries (France, Germany, Italy, Spain and the United Kingdom) involving a pilot for automatic exchange of information based on the FATCA-standard. 3 The Netherlands has joined this pilot as one of the first other EU Member States. 4 Apart from the expressed strong support for transparency and exchange of information, the Dutch government is taking a number of other measures to combat tax fraud and evasion and to enhance tax compliance. Currently, the Dutch tax authorities are doing a pilot project with their German counterparts involving a bilateral joint audit in a direct taxation case. 5 In respect of national and legal persons engaged in tax evasion, the Dutch State Secretary for Finance has recently published a form of tax amnesty. No penalties will be imposed on taxpayers who come clean with all their tax affairs before 1 July 2014. After that date, the rules will become stricter in comparison with the rules as they were before the tax amnesty. These developments certainly justify a report from the Netherlands on the just-discussed topics. Firstly, the legal and practical aspects of exchange of information based on bilateral or multilateral agreements will be discussed. Secondly, the same exercise will be done for exchange of information based on domestic legislation which implements relevant EU directives. Thirdly, the effects of FATCA in the Netherlands will be described. Fourthly, the report discusses other measures targeted at combatting tax fraud and evasion and at enhancing tax compliance. The report will conclude with an outlook to future developments. 2. Exchange of information: bilateral and multilateral measures The Netherlands is a founding member of the OECD. As such, it has been involved in the development of the OECD Model Tax Convention, including Art. 26 thereof. In 2005, two important additions were made to this provision: i) a State cannot refuse to exchange information on the ground that it has no domestic interest, and ii) a bank secrecy is not a sufficient reason to refuse to exchange information. It is Dutch tax treaty policy to follow the OECD Model with respect to exchange of information. 6 This means that tax treaties concluded after 2005 will normally contain the new Art. 26 of the OECD. In addition, the Netherlands negotiates protocols to amend existing tax treaties to bring the exchange of information provision in line with current standards. 7 The Netherlands provides information on request if the request is sufficiently individualized. Fishing expeditions are not allowed. 8 This does not mean, however, that the Dutch authorities are of the view that Art. 26 of the OECD Model prohibits requests of information concerning a group of customers of, for instance, a bank. The Dutch tax authorities are in fact of the view that such requests are possible and they have indicated that they 1 International Tax Center Leiden, Leiden University, and PwC. The author would like to thank Mr. Rob de Vries, policy advisor at the Netherlands Ministry of Finance, for providing valuable background information for the present report. Comments are welcome at [email protected]. 2 Letter of the State Secretary for Finance of 10 December 2013 to the First Chamber of Parliament, No. AFP/2013/847 U, p. 2-3. 3 Kamerstukken 2012/13, 25087, nr. 60, p. 18. 4 Letter of the State Secretary for Finance of 10 December 2013 to the First Chamber of Parliament, No. AFP/2013/847 U, p. 2. 5 Kamerstukken 2012/13, 22112, nr. 1145, p. 5. 6 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 63-64. 7 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 92-93. 8 General Instruction Mutual Administrative Assistance Direct Taxes (Decision of 6 April 2006, CPP2006/546/M), para. 5.1.

Transcript of Netherlands: Exchange of information versus tax … report... · 2015-06-10 · Netherlands:...

1

Netherlands: Exchange of information versus tax solutions of equivalent effect

Prof. Dr. Sjoerd Douma1

1. Introduction

The topic of exchange of information is very much on the political agenda in the Netherlands. In the context ofthe domestic and international debate on the taxation of multinationals, the Dutch government activelysupports EU and OECD initiatives on exchange of information and country-by-country reporting.2 The Dutchgovernment aims at the international implementation of automatic exchange of information. It wants to use themomentum created by the US Foreign Account Tax Compliance Act (FATCA) and by the initiative of the so-called G5-countries (France, Germany, Italy, Spain and the United Kingdom) involving a pilot for automaticexchange of information based on the FATCA-standard.3 The Netherlands has joined this pilot as one of thefirst other EU Member States.4

Apart from the expressed strong support for transparency and exchange of information, the Dutch governmentis taking a number of other measures to combat tax fraud and evasion and to enhance tax compliance.Currently, the Dutch tax authorities are doing a pilot project with their German counterparts involving abilateral joint audit in a direct taxation case.5 In respect of national and legal persons engaged in tax evasion,the Dutch State Secretary for Finance has recently published a form of tax amnesty. No penalties will beimposed on taxpayers who come clean with all their tax affairs before 1 July 2014. After that date, the rules willbecome stricter in comparison with the rules as they were before the tax amnesty.

These developments certainly justify a report from the Netherlands on the just-discussed topics. Firstly, thelegal and practical aspects of exchange of information based on bilateral or multilateral agreements will bediscussed. Secondly, the same exercise will be done for exchange of information based on domestic legislationwhich implements relevant EU directives. Thirdly, the effects of FATCA in the Netherlands will be described.Fourthly, the report discusses other measures targeted at combatting tax fraud and evasion and at enhancingtax compliance. The report will conclude with an outlook to future developments.

2. Exchange of information: bilateral and multilateral measures

The Netherlands is a founding member of the OECD. As such, it has been involved in the development of theOECD Model Tax Convention, including Art. 26 thereof. In 2005, two important additions were made to thisprovision: i) a State cannot refuse to exchange information on the ground that it has no domestic interest, andii) a bank secrecy is not a sufficient reason to refuse to exchange information. It is Dutch tax treaty policy tofollow the OECD Model with respect to exchange of information.6 This means that tax treaties concluded after2005 will normally contain the new Art. 26 of the OECD. In addition, the Netherlands negotiates protocols toamend existing tax treaties to bring the exchange of information provision in line with current standards.7 TheNetherlands provides information on request if the request is sufficiently individualized. Fishing expeditionsare not allowed.8 This does not mean, however, that the Dutch authorities are of the view that Art. 26 of theOECD Model prohibits requests of information concerning a group of customers of, for instance, a bank. TheDutch tax authorities are in fact of the view that such requests are possible and they have indicated that they

1 International Tax Center Leiden, Leiden University, and PwC. The author would like to thank Mr. Rob deVries, policy advisor at the Netherlands Ministry of Finance, for providing valuable background information forthe present report. Comments are welcome at [email protected] Letter of the State Secretary for Finance of 10 December 2013 to the First Chamber of Parliament, No.AFP/2013/847 U, p. 2-3.3 Kamerstukken 2012/13, 25087, nr. 60, p. 18.4 Letter of the State Secretary for Finance of 10 December 2013 to the First Chamber of Parliament, No.AFP/2013/847 U, p. 2.5 Kamerstukken 2012/13, 22112, nr. 1145, p. 5.6 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 63-64.7 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 92-93.8 General Instruction Mutual Administrative Assistance Direct Taxes (Decision of 6 April 2006,CPP2006/546/M), para. 5.1.

2

have not encountered any difficulties with such requests vis-à-vis other tax administrations.9 Moreover, theDutch authorities are of the view that the Commentary on the OECD Model should be applied dynamically tothe extent it has clarified the meaning of an existing bilateral tax treaty provision after the conclusion of thattreaty. If the Commentary amounts to an interpretation which deviates from the one prevailing at the timewhen the treaty was concluded, a case by case approach is necessary to determine whether a dynamicinterpretation approach is reasonable.10 The 2012 update to the Commentary to Art. 26 of the OECD Modelwith regard to the interpretation of the standard of “foreseeable relevance” and the term “fishing expeditions”,including with respect to a group of taxpayers not individually identified, in my view reflects an interpretationof an existing bilateral tax treaty provision which does not conflict with previous interpretations in theNetherlands. Therefore, in my view, the Dutch tax authorities will apply this new Commentary and in particularparagraph 8 thereof, including the limits to group requests mentions in paragraph 8.1.

Next to the new Art. 26 of the OECD Model, the OECD has published a Model Agreement on Exchange ifInformation on Tax Matters 2002. Starting from this model, the Netherlands signed its first Tax InformationExchange Agreement (TIEA), with the Isle of Man in 2005. Just like the 2005 version of the OECD Model, aState cannot refuse to exchange information on the ground that it has no domestic interest nor on the groundthat it has bank secrecy. Currently, the Netherlands has concluded 29 TIEA’s. These are depicted in thefollowing table.

Dutch TIEAs per 1 October 2013

TIEA Signed Entry into forceAndorra 6-11-2009 1-1-2011Anguilla 22-7-2009 1-5-2011Antigua and Barbuda 2-9-2009 1-3-2010Bahama's 4-12-2009 1-12-2010Belize 4-2-2010 1-1-2011Bermuda 8-6-2009 1-2-2010BVI 11-9-2009 1-7-2013Cayman Islands 8-7-2009 29-12-2009Cook Islands 23-10-2009 7-9-2011Costa Rica 29-3-2011 1-7-2012Dominica 11-5-2010 1-3-2012Gibraltar 23-4-2010 1-12-2011Grenada 18-2-2010 20-1-2012Guernsey 25-4-2008 11-4-2009Isle of Man 12-10-2005 24-7-2006Jersey 20-6-2007 1-3-2008Liberia 27-5-2010 1-6-2012Liechtenstein 10-11-2009 1-12-2010Marshall Islands 14-5-2010 8-11-2011Monaco 11-1-2010 1-12-2010Montserrat 10-12-2009 1-12-2011Saint Kitts and Nevis 2-9-2009 29-11-2010Saint Lucia 2-12-2009 31-3-2011Saint Vincent and theGrenadines

1-9-2009 21-3-2011

Samoa 14-9-2009 2-3-2012San Marino 27-1-2010 1-1-2011Seychelles 4-8-2010 1-9-2012Turks and CaicosIslands

22-7-2009 1-5-2011

Uruguay 24-10-2012 1-1-2014

Apart from the just-mentioned bilateral treaties, the Netherlands has also ratified the OECD Convention onMutual Administrative Assistance in Tax Matters in 1996. In 2010, it signed the Protocol amending thisConvention (ratification took place in 2013).

9 Global Forum on Transparency and Exchange of Information for Tax Purposes Peer Reviews: TheNetherlands 2011, Combined: Phase 1 + Phase 2 (the Netherlands), p. 73-74.10 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 24.

3

The Netherlands regards the current international standard on exchange of information as a minimum. TheNetherlands will continue to seek for enhancing the instruments for ex-change of information both on a multi-lateral and a bi-lateral level, for instance by spontaneous and automatic exchanges.11 The Netherlands is not infavor of replacing automatic exchange of information with other measures such as the imposition ofwithholding taxes by a source State (e.g. the so called Rubik agreements signed by Switzerland and othercountries). At present, the Netherlands automatically exchanges information with respect to certain items ofincome on a bilateral basis with 15 countries.12 Negotiations with other territories are ongoing.13 Recently, theNetherlands has agreed with Curacao on the content of a new ‘bilateral’ agreement which includes, inter alia,automatic exchange of information.14

In 2006 the OECD published the “Manual on the implementation of exchange of information provisions for taxpurposes”. As De Goede, Hemels and Schenk have described in their 2009 EATLP report, “the Netherlands donot follow the manual as such. However, the international obligation is in accordance with the spirit of themanual implemented in domestic legislation, by rules of application, and by instructions (manuals) for differentmethods of exchanging information (e.g. the presence of foreign tax officials at tax investigations, simultaneousaudits etc.). They are widely available for the tax officials who have to work with them.”15

In October 2011 (reflecting the legal and regulatory framework as at July 2011), the OECD Global Forum onTransparency and Exchange of Information for Tax Purposes published its peer review of the Netherlands.Generally, the peers were of the view that the Netherlands is a very important and valued partner exchanging asignificant amount of information in tax matters.16 Only a few minor recommendations were made, e.g. withrespect to identity information concerning the limited partners in Dutch limited partnerships (which are fiscallytransparent in the Netherlands).17

3. Administrative cooperation in tax matters: domestic law and implementation of EUdirectives

As of 1 January 2013, the ‘Wet op de internationale bijstandsverlening bij de heffing van belastingen’ (Law onthe international assistance in the levying of taxes; hereafter: WIB) implements Directive 2011/16/EU onadministrative cooperation in the field of taxation and repealing Directive 77/799/EEC, which the WIBimplemented before that date.18 The WIB also implements, inter alia, Directive 2003/48/EC on the taxation ofsavings income in the form of interest payments. Finally, the WIB serves as a domestic legal basis for otherinternational obligations which the Netherlands has entered into, such as bilateral and multilateral agreementson exchange of information. In short, the WIB enables the Dutch tax authorities to deal with the internationalobligations of the Netherlands.

Chapter I of the WIB contains introductory provisions such as definitions of terms.

Chapter 1A contains detailed rules for Netherlands resident paying agents and certain other market participantsand other entities concerning savings income in the form of interest payments. These detailed rules prescribeprecisely the extent of the obligations which these persons have to exchange information in the context ofDirective 2003/48/EC.

11 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 64.12 Memoranda of Understanding to this effect have for instance been signed with Australia, Belgium, Canada,Germany, Estonia, France, Japan, Poland, Spain, Lithuania, Slovenia, Denmark, Sweden, Hungary and theCzech Republic.13 Kamerstukken 2013/14, 22112, nr. 1545, p. 4.14 Internationale fiscale mededeling of 12 December 2013, IFZ 2013/863.15 Jan J.P. de Goede, Sigrid J.C. Hemels and Tonny C.M. Schenk, ‘The Netherlands’, in: Mutual Assistance andInformation Exchange, EATLP International Tax Series, Vol. 8, distributed by IBFD (2010), p. 421.16 Global Forum on Transparency and Exchange of Information for Tax Purposes Peer Reviews: TheNetherlands 2011, Combined: Phase 1 + Phase 2 (the Netherlands), p. 8.17 Global Forum on Transparency and Exchange of Information for Tax Purposes Peer Reviews: TheNetherlands 2011, Combined: Phase 1 + Phase 2 (the Netherlands), p. 119.18 The WIB has been worked out in two Decrees (the ‘Uitvoeringsbesluit internationale bijstandsverlening bij deheffing van belastingen’ and the ‘Uitvoeringsregeling internationale bijstandsverlening bij de heffing vanbelastingen’).

4

Chapter II of the WIB contains rules with respect to certain types of exchange of information by theNetherlands.

Section 1 concerns exchange of information on request. Art. 5 states that the Dutch authorities will provide thecompetent authority of a requesting State with all information which is relevant for the process of taxation inthat other State. If the Dutch authorities already have the requested information available, the information willbe provided within two months. In other cases, the information will be provided within six months (Art. 5A). Asof 1 January 2014, the provider of the information will not be notified anymore of any exchange ofinformation.19 The provider of the information has also lost his right to oppose a decision on exchange ofinformation.20 The reason for this change in the law can be found in the criticism which the OECD GlobalForum on Transparency and Exchange of Information for Tax Purposes expressed in its peer review report ofthe Netherlands.21 This criticism mainly concerns the, sometimes considerable, delays caused by thenotification procedure, for instance if the provider of the information starts legal proceedings against thedecision on exchange of information.22 The Dutch legislature has responded to this criticism by taking thenotification procedure out. This would foster an effective means of exchange of information and wouldcontribute to the fight against tax avoidance.23

Section 2 concerns the automatic exchange of information. Art. 6 provides the Dutch Minister of Finance withthe authority to introduce – in consultation with a competent authority of another State – automatic exchangeof information in certain cases of groups of cases. Art. 6b, which will be effective as from 1 January 2015, statesthat information concerning residents of other EU Member States will be exchanged automatically with respectto: income from employment, director’s fees, life insurance products not covered by other Union legalinstruments on exchange of information and other similar measures, pensions, and ownership of and incomefrom immovable property. Information will be exchanged at least once a year, within six months after thetaxable year in which the information has become available. The Netherlands will not exchange informationautomatically with a Member State which has informed the Netherlands that it does appreciate the receipt ofsuch information. The Netherlands will also not exchange information with a Member State which has notinformed the European Commission about the information which is available there.

Section 3 concerns the spontaneous exchange of information. Artt. 7(1) and 7A state that the Netherlands willspontaneously exchange information with the competent authority of another EU Member State within onemonth after the information has become available, in the following situations:

(a) there are grounds for supposing that there may be a loss of tax in the other Member State if the informationwould not be exchanged;(b) a person liable to tax obtains a reduction in, or an exemption from, tax in the Netherlands which could berelevant for the levying of tax in the other Member State;(c) legal acts of other acts have been performed in the Netherlands with the purpose of making the impositionof tax the other Member States wholly or partially impossible;(d) if the Minister of Finance decides that information should be exchanged spontaneously.

Art. 7(2) states that the Minister of Finance may spontaneously exchange information in the above-mentionedsituations with the competent authority of another State (not being an EU Member State).

Section 4 provides for rules for investigations conducted in the context of mutual assistance. Art. 8(1) statesthat investigations may be performed to obtain the information mentioned in Artt. 5, 6 or 7 (see above). Art.8(2) provides for the possibility to perform investigations with respect to other information at the request of thecompetent authority of another State. If the Netherlands is of the view that such an investigation is not

19 Law of 18 December 2013, Stb. 566.20 See K.R.C.M. Jonas and J.A.R. van Eijsden, ‘De kennisgeving vooraf bij internationale uitwisseling vaninformatie verdwijnt. En daarmee de rechtsbescherming ook!’, WFR 2013/1180.21 Global Forum on Transparency and Exchange of Information for Tax Purposes Peer Reviews: TheNetherlands 2011, Combined: Phase 1 + Phase 2 (the Netherlands), p. 84-85.22 The Global Forum Report (p. 112-113) shows that for the three year period 2008 to 2010, the Netherlandsresponded to 35% of requests within 90 days, to 18% of requests within 90-180 days, to 24% of requests within180-360 days and 23% of requests took more than 360 days.23 Kamerstukken 2013/14, 33753, nr. 7, p. 13.

5

necessary, the grounds for such a decision will be made know to that competent authority at its request. Art.8(3) states that, in principle, investigations in the context of mutual assistance are performed under the samelegal framework which is used in ‘domestic’ tax investigations; the tax administration has the same powers. Art.8(6) states that no appeal is possible against the investigation or against the announcement thereof. On thebasis of Art. 8(5) the Government may issue a Decree obliging certain taxpayers to provide informationautomatically to the tax authorities in the context of international agreements on exchange of information. As of1 January 2014, Art. 3a of this Decree contains detailed rules for resident corporate income taxpayers theactivities of which mainly consist of the direct or indirect receipt or payment of interest, royalties, rent or leaseterms, in any form whatsoever, from or to non-resident entities which belong to the same group as thetaxpayer.24 The taxpayer will have to declare to the Dutch tax authorities annually that it meets the substancerequirements mentioned in Art. 3a(7):

a. At least half of the board members of the taxpayer is resident in the Netherlands;b. The board members resident in the Netherlands have sufficient professional knowledge to take responsibilityfor the transactions entered into by the taxpayer;c. The employees of the taxpayer have sufficient professional knowledge to carry out and administer thetransactions entered into by the taxpayer;d. Management decisions are taken in the Netherlands;e. The most important bank accounts of the taxpayer are held in the Netherlands;f. The books are kept in the Netherlands;g. The address of the taxpayer is in the Netherlands;h. To be best of its knowledge, no other country regards the taxpayer as a resident;i. The taxpayer runs sufficient risk with regard to its activities and maintains a sufficient level of equity inaccordance with its functions.

If the taxpayer does not meet these requirements, it will have to disclose to the tax authorities to what extent ithas invoked in another State a bilateral tax treaty with the Netherlands, Directive 2003/49/EC (the Interest &Royalty Directive) or a domestic measure implementing that directive. This information will be exchangedspontaneously with the competent authority of the State concerned. Non-compliance by the taxpayer with anyof these information requirements is an offence in respect of which penalties apply (Art. 11 of the WIB).

Section 5 states that lower levels of administration – e.g. provinces or municipalities – shall cooperate with thetax authorities in the context of international mutual assistance for tax purposes.

Section 6 contains general provisions. Art. 14(2)(b) stipulates that the tax authorities are not obliged toexchange information if such information could legally not have been obtained in a domestic case. Art. 14(2)(c)states that the tax authorities are not obliged to exchange information if it is likely that the competent authorityof the other State has not exhausted its own possibilities to obtain the information. Art. 14(2)(d) states that thetax authorities are not obliged to exchange information if the other State does not the respect the principle ofreciprocity. Art. 14(3) determines that exchange of information will never be denied on the ground that theinformation is held by a financial institution or on the ground that the information concerns ownershipinterests in a person (this can be a natural or legal person but also any legal construction which manages assetsor income).25 Art. 16 states that the Netherlands will not provide information to a competent authority ofanother State if the civil servants in that other State have no obligation of professional secrecy in respect of theinformation they receive in the context of their work at the tax administration. Art. 18 contains the most favorednation principle: if the Netherlands reaches agreement with the competent authority of another State whichgoes beyond what Directive 2011/16/EU requires, the Netherlands will grant this treatment also to every EUMember State which so requests. Art. 19 states that any communication with the competent authority ofanother State will as far as possible take place electronically and through the use of standard forms which arecompliant with Directive 2011/16/EU.

Appendix 1 to this report contains information (numbers) with respect to information received and exchanged

24 Decree of 18 December 2013, Stb. 569.25 This is an implementation of Art. 18(2) of Directive 2011/16/EU. See Kamerstukken 2011/12, 33246, nr. 3, p.14. It also addresses the criticism of the Global Forum on Transparency and Exchange of Information for TaxPurposes Peer Reviews: The Netherlands 2011, Combined: Phase 1 + Phase 2 (the Netherlands), p. 119; seeparagraph 3 above.

6

in 2009-2012.26 Appendix 2 contains specific references for the year 2012.

4. FATCA

On 18 December 2013, the Netherlands - United States FATCA Agreement (2013) was signed, in The Hague. Inaddition, a memorandum of understanding regarding the interpretations of the agreement and anaccompanying exchange of letters were signed concurrently. The US-Netherlands Agreement is substantiallysimilar to the Model 1A Agreement as of 4 November 2013 that includes a reciprocal approach for the sharing ofinformation between the two governments. The Netherlands plans to present the Agreement to its parliamentfor its approval in 2014 and to propose implementing legislation with the goal of having the Agreement enterinto force by 30 September 2015.27 The implementation of FATCA into local legislation avoids a conflictbetween the two. The exchange of letters further states the following:

“The United States notes that both the United States and the Netherlands provide high levels of data protectionwith information they receive in the exchange of information in tax matters, as confirmed in the Peer Reviewsin the context of the Global Forum on Transparency and Exchange of Information for Tax Purposes. Pursuantto paragraph 7 of Article 3 of the Agreement, the information exchanged under the Agreement is subject to theconfidentiality and other protections provided for in the Convention between the United States of America andthe Kingdom of the Netherlands for the Avoidance of Double Taxation and the Prevention of Fiscal Evasionwith Respect to Taxes on Income, done at Washington on 18 December 1992, as amended on 13 October 1993and 8 March 2004 (“Double Tax Convention”) and the Convention on Mutual Administrative Assistance in TaxMatters, done at Strasbourg on 25 January 1988 (“the Mutual Assistance Convention”). Those protectionsinclude those set out in paragraph 1 sentences 3 through 7 of Article 30 of the Double Tax Convention andArticle 22 of the Mutual Assistance Convention. In the context of the implementation of the Agreement, thecompetent authorities are expected by mutual arrangement to establish procedures on data protection specificto the exchange of information under the Agreement.”

This, in my view, avoids a conflict with other rules or principles of international law. Or, in other words, if thereis a conflict, it already existed before the FATCA Agreement.

5. Other instruments

Collection of taxes

It is Dutch tax treaty policy to include in bilateral tax treaties a provision on the assistance in the collection oftaxes in conformity with Art. 27 OECD MTC.28 In addition to this, the Netherlands aims at the adoption of thefollowing elements:

(i) A material and practical threshold for assistance requests. The Dutch government aims at threshold which issimilar to the one in Directive 2010/24/EU, e.g. Article 18 thereof (Limits to the requested authority’sobligations).29 In addition, the Dutch government aims at coming to an agreement on practical aspects withrespect to, inter alia, time limits, the use of standard forms and digital technology.

(ii) Safeguards for legal remedies. It is likely that a non-resident person is less aware of the legal remediesagainst a tax assessment in the other State than a resident person. Therefore, assistance in the collection oftaxes will only be provided if the tax is finally determined and fully recoverable, i.e. if all legal remedies havebeen exhausted or if the tax inspector shows that the tax is materially due. In addition, assistance in the

26 Numbers with respect to 2011 can be found in the Management Report of the tax authorities (in English)(http://download.belastingdienst.nl/belastingdienst/docs/dutch_tax_custom_adm_manag_report_2010_bjv0021z11fdeng.pdf), p. 85-86, and in G.J.M.E. de Bont and E.C.J.M. van der Hel-Van Dijk, ‘Netherlands’, in:Exchange of information and cross-border cooperation between tax authorities, IFA Cahiers, Vol. 98b, theNetherlands: Sdu 2013, p. 552-553.27 See the exchange of letters between the United States and the Netherlands of 18 December 2013.28 Ministry of Finance, Notitie Fiscaal Verdragsbeleid 2011 (Notice on Dutch Tax Treaty Policy), p. 64.29 Directive 2010/24/EU has been implemented in the Dutch legal order through the Law of 8 December 2011,Stb. 632 (effective 1 January 2012).

7

collection of taxes will only be provided if the material tax debt does not conflict with the bilateral tax treaty orother international agreement to which the States are a party.

Joint audits

In a letter to the Dutch parliament of 11 January 2013, the Dutch Minister of Foreign Affairs explained that theNetherlands has advocated to experiment with joint audits. At present, the Dutch tax authorities are engaged ina pilot with the German tax authorities in this regard. It is the idea that other countries are invited to participatein such a pilot.30 Artt. 8a et seq. and 27 et seq. of the ‘Wet op de internationale bijstandsverlening bij de heffingvan belastingen’ (Law on the international assistance in the levying of taxes) provides a domestic legal basis forthis.31

Asset Recovery Office

The ‘Bureau Ontnemingswetgeving Openbaar Ministerie’ (often referred to as BOOM or, in English, theCriminal Assets Deprivation Bureau of the Prosecution Service) serves as the national Asset Recovery Officementioned in Council Decision 2007/845/JHA of 6 December 2007 concerning cooperation between AssetRecovery Offices of the Member States in the field of tracing and identification of proceeds from, or otherproperty related to, crime.32 The Evaluation Report on the fifth round of Mutual Evaluations "Financial Crimeand Financial Investigations" - Report on the Netherlands, 19 October 2010, 11989/1/10 REV 1, provides fordetailed information on the Dutch implementation of this decision.33 One of the recommendations of thisreport reads as follows:

“Mutual access to databases, especially between law enforcement agencies such as police and tax authorities,should be enhanced. Should it not be possible at national level, tailor-made agreements on data exchange (…)should be promoted. Investigators should be provided with quicker access to data relating to bank accounts.”

A standard financial information database accessible by all law enforcement agencies does not exist in theNetherlands, according to the Report. This does not mean that the tax authorities and other law enforcementbodies do not work well together in the event of concrete suspicions.

Measures against money laundering

Directive 2005/60/EC, as amended by Directive 2008/20/EC), on the prevention of the use of the financialsystem for the purpose of money laundering and terrorist financing and Directive 2006/70/EC laying downimplementing measures for Directive 2005/60/EC have been implemented by the following laws:

1) the Law of 15 July 2008, Stb. 2008/302 (‘Wet houdende wijziging van de Wet identificatie bijdienstverlening en de Wet melding ongebruikelijke transacties’) and

2) the Law of 15 July 2008, Stb. 2008/303 (‘Wet houdende samenvoeging van de Wet identificatie bijdienstverlening en de Wet melding ongebruikelijke transacties (Wet ter voorkoming van witwassen enfinancieren van terrorisme)’).

These laws entered into force on 1 August 2008 (Stb. 2008, 304). The ‘Wet ter voorkoming van witwassen enfinancieren van terrorisme’ (hereafter: Wwft) has been explained by the Ministry of Finance in a policy rule

30 Kamerstukken 2012/13, 22112, nr. 1545, p. 5.31 See for more information the detailed description in G.J.M.E. de Bont and E.C.J.M. van der Hel-Van Dijk,‘Netherlands’, in: Exchange of information and cross-border cooperation between tax authorities, IFA Cahiers,Vol. 98b, the Netherlands: Sdu 2013, p. 554 -559.32 See the Report from the Commission to the European Parliament and to the Council of 12 April 2011,COM(2011) 176 final.33 For the text of this report go to:http://register.consilium.europa.eu/doc/srv?l=EN&t=PDF&gc=true&sc=false&f=ST%2011989%202010%20REV%201&r=http%3A%2F%2Fregister.consilium.europa.eu%2Fpd%2Fen%2F10%2Fst11%2Fst11989-re01.en10.pdf.

8

(‘Algemene leidraad Wet ter voorkoming van witwassen en financieren van terrorisme (WWFT) en Sanctiewet(SW)’, updated in January 2014). The Wwft contains four obligations for the financial sector:34

1) client identification and acceptance procedures;2) notification of unusual transactions;3) supervision and enforcement; and4) keeping an administration.

The following institutions play a role in the supervision of the Wwft:

1) The Dutch Central Bank (bank, insurance companies, casino’s);2) The Financial Supervision Office, in Dutch: Bureau Financieel Toezicht (legal profession: lawyers, notaries,tax advisors, etc.);3) A division of the tax authorities, in Dutch: Belastingdienst Hollands-Midden (brokers and the trading ingoods such as cars, art and antiques, jewelry); and4) The Netherlands Authority For the Financial Markets, in Dutch: Autoriteit Financiële Markten (investmentfunds).

In addition, the Financial Intelligence Unit – Netherlands plays a role (see www.fiu-nederland.nl for a detailedEnglish description of its activities). Unusual transactions must be reported in detail to the Dutch FiscalIntelligence Unit. The Dutch Fiscal Intelligence Unit wishes to cooperate closely with FIUs from other MemberStates.35 In 2012, FIU Netherlands has sent 270 information requests to other FIUs. In turn, it received 747information requests from other FIUs.36 In the Netherlands, such information can be used in principle inproceedings concerning administrative or penal sanctions, unless the use of such information would becontrary to what one should expect from a fair government to such an extent that such use is impermissibleunder any circumstance.37 This is for instance the case if government officials have willingly broken the law toobtain information (e.g. if they would have paid for information which was clearly obtained illegally in anothercountry).

Policy for whistleblowers (‘tipgeversregeling’)

The Dutch policy for reward money for whistle blowers dates back to a resolution in 1985.38 In 2010 and 2014the State Secretary for Finance reiterated that his policy is still based on the resolution of 1985.39 A decision topay for information will not be taken lightly and the tax authorities apply a very strict policy in this respect. Thisshould be expected from a government which is integer, diligent and reliable. The following conditions shouldbe met before any reward money can be paid:

• A considerable financial interest should be at stake;• The tax authorities are satisfied that the information is reliable;• An assessment should be made with respect to the risks associated with the information for the involved civilservants as well as for the person providing the information;• Reward money will only be paid after the ‘extra’ tax revenue has been paid to the treasury;• No concessions will be made in the area of penalties, or the imposition or collection of taxes;• Under no circumstance immunity from criminal prosecution will be granted.

Rules on voluntary disclosure

On 2 September 2013, the State Secretary for Finance has decided that the rules voluntary disclosure will berelaxed temporarily.40 The reason for this is the government’s submission to parliament of new rules on the

34 See http://www.rijksoverheid.nl/onderwerpen/integriteit-financiele-markten/aanpak-witwassen-en-financieren-van-terrorisme.35 FIU Netherlands Annual Report 2012, p. 42.36 FIU Netherlands Annual Report 2012, p. 43.37 HR 9 September 1992, nr. 27.399, BNB 1992/366.38 Resolution State Secretary for Finance of 24 October 1985, nr. 585–24843, VN 1985, p. 2168.39 Kamerstukken 2009/10, 31 066, nr. 85, p. 2-3; Kamerstukken 2013/14, 31 066, nr. 188, p. 28.40 Policy rule of 2 September 2013, nr. BLKB2013/509M, Stcrt. 25169.

9

imposition of additional tax assessments.41 If the taxpayer has acted in bad faith – for instance in case of a falsetax return – the statutory time limit for the imposition of an additional tax assessment will be extended fromfive to twelve years. As a transitional measure, taxpayers are provided with the opportunity to ‘come clean’before 1 July 2014. This means that no penalties will be imposed if a taxpayer voluntarily discloses previouslynon-disclosed facts which are relevant for a correct tax assessment process (the tax itself will, of course, belevied).42 Between 1 July 2014 and 1 July 2015 the current voluntary disclosure rules will apply again. Thismeans that a taxpayer will not be fined if he voluntarily discloses previously non-disclosed facts within twoyears starting from the date on which the false tax return was submitted but before the taxpayer knows orreasonable should have known that the tax inspector is aware – or will be aware – of the incorrect statements(Art. 67n of the ‘Algemene wet inzake rijksbelastingen’, in English: General Tax Act). If the taxpayer disclosesvoluntary after two years, the penalty will be moderated to 10-30% of the maximum penalty which can legallybe imposed. After 1 January 2015, a voluntary disclosure within two years starting from the date on which thefalse tax return was submitted will lead to a moderation of the maximum penalty which can legally be imposedto 20-60%.

There are no legal restrictions for the international exchange of information which has become known to theDutch tax authorities after a voluntary disclosure.

Nemo tenetur principle

As De Bont and Van der Hel-van Dijk have stated, the principle of self-incrimination – Art. 6 of the ECHR – isonly applicable if investigative powers are used towards a suspect (a taxpayer who may reasonably expect thatthe authorities are considering to impose an administrative penalty or to start a criminal procedure).Information requests normally concern information which a third party (not being the taxpayer) has in itspossession. This third party does not have a right to invoke the principle of self-incrimination.43

In case the information is to be obtained from the taxpayer himself, the Dutch Supreme Court has formulated anumber of rules.44 First, a taxpayer can be forced to provide all information which may be relevant for a correcttax assessment process, irrespective of whether this information is dependent on his will. If, however, theinformation depends on his will it can only be used for the tax assessment process and not for the imposition ofadministrative sanctions or in a criminal procedure. If – contrary to this rule – the will-dependent informationis used in such a situation, the criminal court (in case of a criminal procedure) of the tax court (in case of anadministrative sanction) will have to decide which consequences such a violation will have. Secondly, if thetaxpayer fails to provide the required information, penalties may be imposed. In a procedure against theimposition of the penalty, the State has to prove that the taxpayer is actually capable to produce theinformation.

6. Future developments

As stated above, the Dutch government aims at achieving more international automatic exchange ofinformation. This is a cornerstone of international tax policy and no doubt we will see more internationalagreements in this area. At the same time, one may expect that enforcement of information requirements inrespect of taxpayers will be enhanced (compare the above-described stricter rules on voluntary disclosure in thefuture, combined with a favorable short period to ‘come clean’), both domestically and in internationalsituations. The ongoing pilot on joint audits and the abolition of the notification of providers of information incase of an international exchange of information are good examples of this.

41 Kamerstukken 2012/13, 33 714, nr. 2 (Wet vereenvoudiging formeel verkeer Belastingdienst).42 A ‘voluntary’ disclosure is possible only before the taxpayer knows or reasonable should have known that thetax inspector is aware – or will be aware – of the incorrect statements43 J.M.E. de Bont and E.C.J.M. van der Hel-Van Dijk, ‘Netherlands’, in: Exchange of information and cross-border cooperation between tax authorities, IFA Cahiers, Vol. 98b, the Netherlands: Sdu 2013, p. 565-566.44 HR 12 July 2013, nr. 12/01880, ECLI:NL:HR:2013:BZ3640.

10

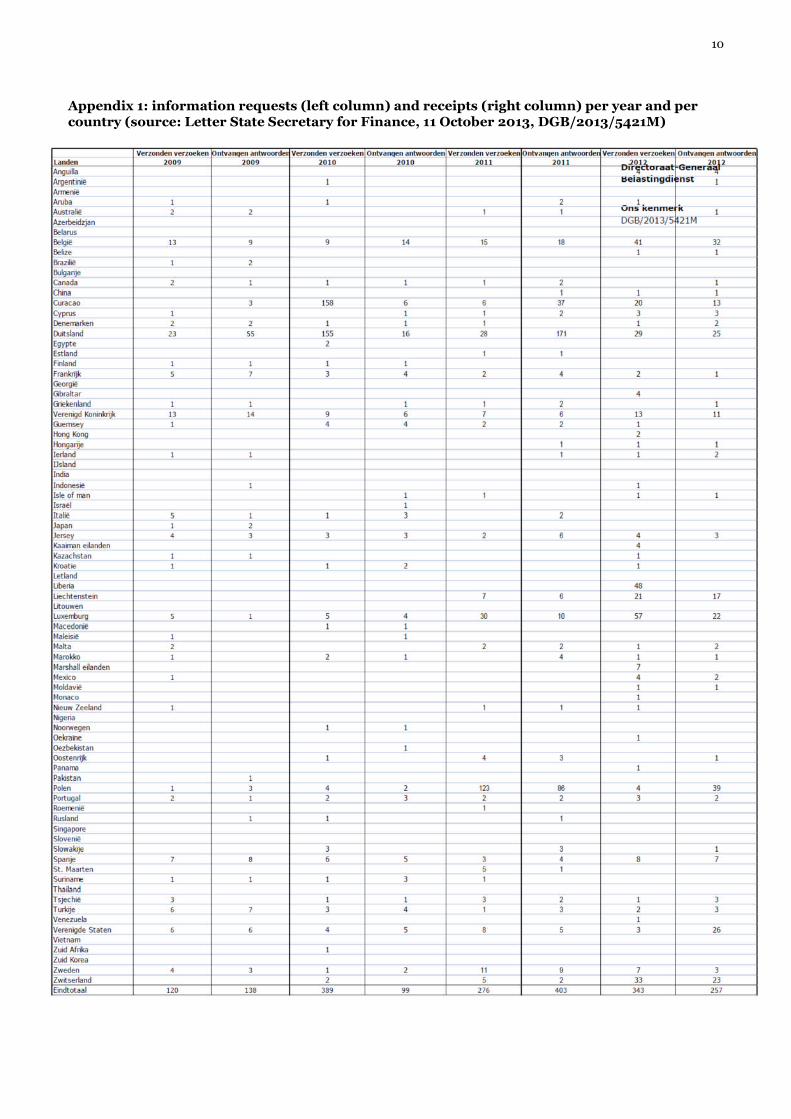

Appendix 1: information requests (left column) and receipts (right column) per year and percountry (source: Letter State Secretary for Finance, 11 October 2013, DGB/2013/5421M)

11

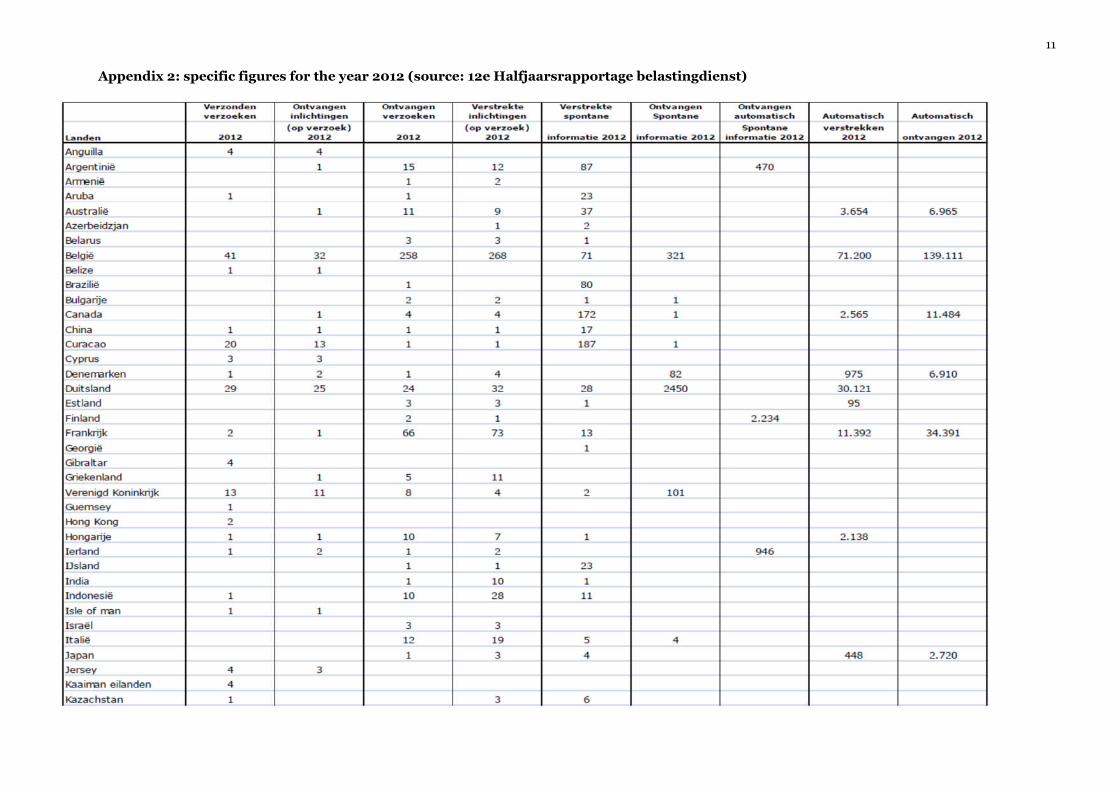

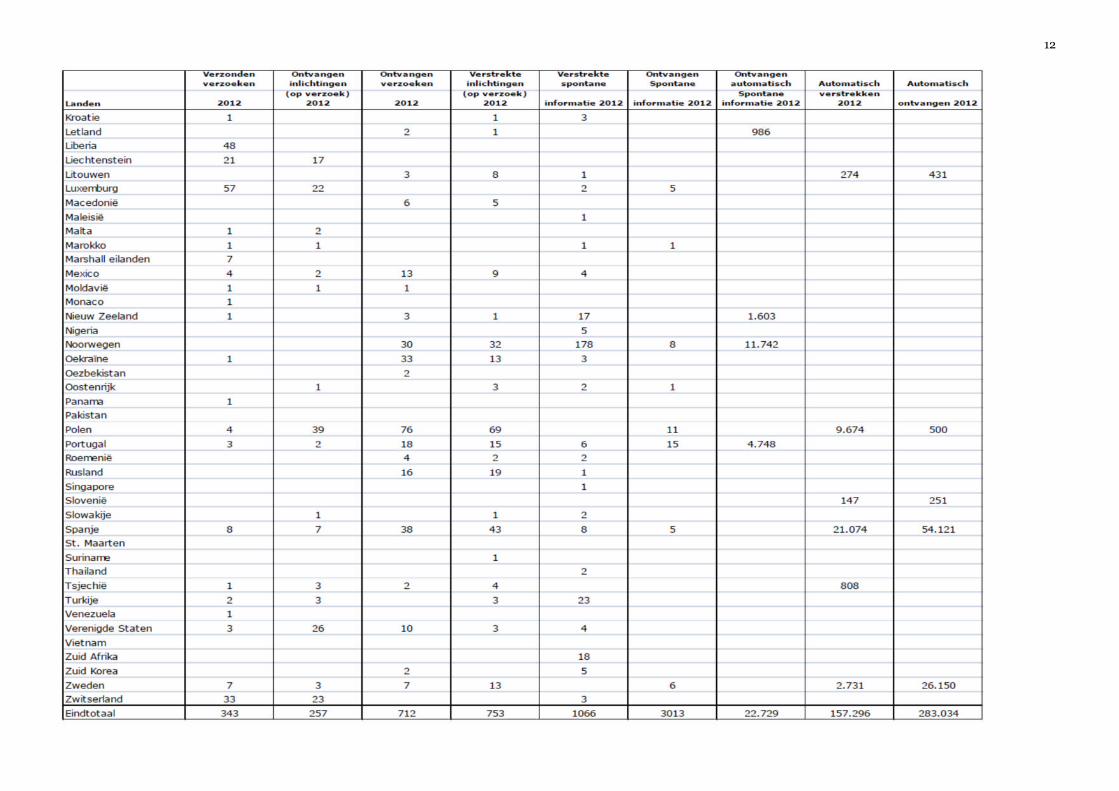

Appendix 2: specific figures for the year 2012 (source: 12e Halfjaarsrapportage belastingdienst)

12

13

Explanation to appendix 2:

Column 1: the country concernedColumn 2: requests sent by the NetherlandsColumn 3: information received on request by the NetherlandsColumn 4: requests received by the NetherlandsColumn 5: information exchanged by the Netherlands on requestColumn 6: information exchanged by the Netherlands spontaneouslyColumn 7: information received by the Netherlands spontaneouslyColumn 8: automatic spontaneous information received by the NetherlandsColumn 9: information exchanged by the Netherlands automaticallyColumn 10: information received by the Netherlands automatically