Net Energy MeteringNet Energy Metering (NEM) enables a customer with distributed renewable...

21

Net Energy Metering & Rate Changes – Implications for Distributed Generation Jay Paidipati & Andrea Romano, Navigant Consulting April 25, 2017

Transcript of Net Energy MeteringNet Energy Metering (NEM) enables a customer with distributed renewable...

Net Energy Metering & Rate Changes –Implications for Distributed GenerationJay Paidipati & Andrea Romano, Navigant ConsultingApril 25, 2017

Click to edit Master title styleAgenda

2

Team Update Today’s Discussion

What is Net Energy Metering (NEM)? What’s Changing? State NEM Policies 2016 NEM Policy Changes & Rate Reform State NEM Case Studies Implications for Solar PV Role of Energy Storage BBA Member Recommendations

Click to edit Master title styleTeam Update

3

New Resource The Energy Storage Decision Guide is now available! You can get it in the Better Buildings Solution Center at

https://betterbuildingssolutioncenter.energy.gov/resources/site-energy-storage-decision-guide

Thank you to those of you who provided peer review. Better Buildings Summit Activities

Wednesday morning session on PV and Storage entitled Saving the Sun for Later: Opportunities and Barriers for Solar PV + Energy Storage. Boston Properties, the City of San Francisco, and Stem will talk about their PV+storageexperiences to date.

Two Ask an Expert Sessions on renewable energy on Wednesday RE 100 roundtable lunch on Wednesday. Come meet companies pursuing 100%

renewables and hear about drivers and barriers.

Click to edit Master title styleWhat is Net Energy Metering?

4

Net Energy Metering (NEM) enables a customer with distributed renewable generation to sell excess electricity back to the utility at the same rate at which the customer purchases electricity from the grid when the solar PV system is not producing enough electricity to meet demand.

Source: “Learn About Net Metering.” Pacific Gas & Electric Company.

Net Metering Electricity Flows

Click to edit Master title styleNEM – What’s Changing?

5

NEM policies have contributed to the rapid growth of the distributed solar industry in the US, however, with higher levels of market penetration, debates are taking place in many states regarding “fair” compensation.

Utilities

Raised concerns about cost shifting to non-solar customers and utility shareholder profitability.

Solar Advocates

Point to studies showing at low penetrations and under certain assumptions, the marginal value of solar can be calculated as exceeding the retail rate in some areas.

Other Stakeholders

Describe NEM as an instrument that sends inaccurate price signals to the demand side of the market.

Click to edit Master title styleNet Energy Metering State Policies

6

Note: Revising Net Metering rules are being actively discussed in many state public service & utility commissions across the country.

(Source: www.dsireusa.org, July 2016)

Most states have some form of NEM policy.

State-developed mandatory rules for certain utilities (41 states + DC+ 3 territories)

No statewide mandatory rules, but some utilities allow net metering (2 states)

KEY

U.S. Territories:

41 States + DC,AS, USVI, & PR have mandatory net metering rules.

DC

Statewide distributed generation compensation rules other than net metering (4 states + 1 territory)

GU

AS PR

VI

Click to edit Master title styleTop NEM and Rate Reform Trends

7

Nearly every US state took some type of policy action related to distributed energy in 2016, aligning with the following trends.

Reconsider net energy metering rates, in many cases reducing or proposing to reduce NEM rates

Consider the development of a Value of Solar (VOS) and Community Solar Credit Rate

Request to increase fixed charges and/or increase C&I demand charges

NC Clean Energy Technology Center, 50 States of Solar, January 2017, https://nccleantech.ncsu.edu/wp-content/uploads/Q42016_ExecSummary_v.3.pdf

1

3

2

Click to edit Master title styleNEM Policy Changes & Rate Reform

8

Of the 212 actions taken in 2016, the most common were related to net metering (73), followed by residential fixed charge and minimum bill increases (71).

NC Clean Energy Technology Center, 50 States of Solar, January 2017, https://nccleantech.ncsu.edu/wp-content/uploads/Q42016_ExecSummary_v.3.pdf

Click to edit Master title style

Active states

States to watch

Both

NEM Policy – States to Watch

*Additional information about these states is provided in the appendix.

Click to edit Master title styleCase Study - Arizona

10

• Under previous NEM policy, customers were credited full retail rate ($0.13-$0.14/kWh).

• Utilities and other rate payers argued that a full NEM retail rate resulted in a cost shift.

• In March 2017, Arizona Public Service Co. and a group of solar interests filed a settlement on rate design and rooftop solar compensation with the Arizona Corporation Commission, following years of contentious debate.

Initial NEM Policy

Current NEM Policy

• This deal being passed has given distributed generators, especially the solar industry, economic clarity when building new projects.

• After years of disagreement, Arizona utilities and solar backers seem to agree on this settlement.

Future

• Under the new agreement, the rooftop solar customer will be paid $0.129/kWh for excess energy exported to the grid.* Export rate will fall 10% annually, but customers will lock in rates for 10 years at sign up.

• Solar energy consumed by end users valued at ~$0.105/kWh, with a lower rate for demand charge rate options, likely in the $0.096-$0.078/kWh range.

• New settlement includes a 20-year grandfathering period for customers who file for interconnection before rate case decision.

*Rooftop solar customers can choose from four rate design options that include a time-of-use rate plan with a grid access charge or a demand-based rate plan without a grid access charge. The settlement does not include a mandatory demand charge.

Presenter

Presentation Notes

Arizona recently (3/1/2017) filed a settlement on the rate design and rooftop solar compensation. Under the new agreement, the rooftop solar customer will be paid $0.129/kWh for exporting any energy back into the grid. This export rate will fall 10% annually, but customers have the ability lock in their rates for 10 years when they sign up for the new program. The offset rate* would be $0.105/kWh, but these rates will differ by usage and rate patterns. The price of energy from the $0.105/kWh price would be changed by demand charge rate to between $0.096 and $0.078/kWh. Under this new agreement a 20-year grandfathering period for customers who file an interconnection application before a decision is issued in the rate case. Under the current program in Arizona, solar customers are paid under retail NEM at $0.13kWh and $0.014kWh. Another notable detail about the settlement is that APS can not build any new generation before 2022 unless given approval by the ACC. This deal being passed has given solar activists some sort of policy to look at when they decide to build new solar investments. Arizona utilities and solar backers seem to be in current state of peacefulness after this new settlement. That is until a new rate change is brought up again. *The offset rate is the rate solar customer will be credited on their utility bills.

Click to edit Master title styleCase Study - Hawaii

11

• Hawaii NEM has been very popular with 60,000 utility customers installing solar PV systems under the NEM program since 2001.

• NEM commercial customers received full retail rates for export ($0.28/kWh – 0.34/kWh).

• Due to penetration rates, Hawaii forced to adapt to a new system for solar customers.

• Customers with an installed solar system or complete application by 10/2015 – grandfathered into the old program and will benefit from full retail rate export credit in perpetuity.

Initial NEM Policy

Current NEM Policy

• Revised NEM policy has had a negative impact on solar companies due to less desirable economics.

• Uptick in solar company growth in Hawaii is expected as energy storage prices decline.

• Energy storage price decline is expected to shift customer preference between CSS and CGS.

Future

• End of retail NEM led to two new tariffs.

• Customer Self-Supply –Intended for customers that do not export to the grid as no compensation provided for energy export. Customers pay a minimum monthly bill of $25 (residential) or $50 (commercial).

• Customer Grid-Supply –Customers export electricity to the grid on a fixed rate ranging from $0.15/kWh - $0.28/kWh.

• CGS used by nearly all consumers due to CSS requiring consumer energy storage.

• CGS reached 35 MW cap in August 2016, current discussion underway to raise cap limits.

Presenter

Presentation Notes

Hawaii is currently in a position that perhaps no other state is in. Hawaii was so successful in NEM that they counterintuitively decided to end NEM in 2015 and have now adopted a new system that currently has two options for customers to choose from. These two options are CSS or CGS. CSS is a flat rate of $25 for residential vs $50 for commercial customer. The idea of CSS is to put minimum stress on grids, which are already overloaded. CGS allows customers to export electricity to the grid on a fixed ranging from $0.15kWh - $0.28kWh. The latter of the two is used by nearly all consumers. The reason for the second option (CGS) being adopted more by consumers is due to the first option (CSS) requiring storage from the consumer. Until the price of storage comes down, there will continue to be more participants in CGS than CSS. When storage prices do come down there will likely be a shift from the current selection of CGS to CSS. Since the end of NEM in Hawaii we’ve seen solar companies becoming smaller and smaller due to a shrinking market. However, we can expect an uptick in solar company growth when there is a growth in storage accessibility with customers. Going forward Hawaii will hopefully see an increase in battery storage production resulting in a more affordable batteries. Until then Hawaii solar customers will continue to use CGS. Source to be added to source slide: https://www.hawaiianelectric.com/clean-energy-hawaii/producing-clean-energy/customer-self-supply-and-grid-supply-programs

Click to edit Master title styleCase Study – New York

12

• Enacted in 1997, NEM originally only applied to PV systems but later expanded to other distributed generation technologies.

• NEM provided on a first come first serve basis, crediting customers the full retail rate.

• In December 2016, New York Dept. of Public Service released a report on the value of distributed energy, indicating existing solar projects interconnected by March 2017 should receive the full retail rate NEM credit for 20 years.

Initial NEM Policy

Current NEM Policy

• In May 2017, the Public Service Commission will commence the discussion on the next phase of the transition process.

• Topics of phase two will be value stacks(e.g. energy, capacity, environmental, demand, social).

• Debates are ongoing regarding the value stacks that should be considered.

Future

• Through January 1, 2020, all the mass market DER projects interconnected to the grid will be compensated through full NEM tariff, gradually dropping the credit until it aligns with the states LMP + D value.*

• LMP is based on Day Ahead hourly zonal locational-based marginal price (LBMP)

• LMP + D value is noted to be lower than retail electricity prices.

*LMP (locational marginal price) represents wholesale market value and D represents all other values, including distribution system benefits and environmental externalities.

Presenter

Presentation Notes

In December of 2016 New York Department of Public Service released it’s report on the value of distributed energy. In the recommendations of the report it says existing solar projects should receive the full retail rate NEM credit for 20 years. The allotment of 20 years provided for current NEM customers stated in the report is there to protect their solar investments. It also states that solar customers should preserve new resident and small commercial projects through 2020 then dropping the credit until it aligns with LMP + D value. This value is noted to be lower than the retail electricity prices. The thing is nice about this is that it’s not an overnight switch like there has been in other NEM states but instead it is being phased in. The phasing strategy has shown to be something of a common ground for utilities and solar companies as shown in the rate settlement in Arizona. Just last week, March 8th 2017, regulators finalized the order approving the first phase of new compensation structure for DER. This can be considered the first step in moving away from retail NEM. While it seems this may be a bad thing if you’re a NEM customer, it may be quite the contrary. It proves that New York is moving to address the problem while not completely ignoring the investments hat have been made. The transparency in this process has proven to be beneficial for all parties. LMP is the locational marginal price of electricity. D is the value of the resource to the distribution system

Click to edit Master title styleCase Study – California

13

• Original NEM applied to customers who installed distributed solar, wind, biogas, and fuel cell generating assets.

• Customers received the full retail rate.

• With California NEM popularity, the discussion around fair compensation arose.

• In January 2016, the California Public Utilities Commission issued the NEM 2.0 decision.

• Investor owned utilities required to offer NEM until utility reaches NEM cap (exceeds 5% of its aggregate customer peak demand) or July 1, 2017, whichever is first.

Initial NEM Policy

Current NEM Policy

• NEM 2.0 will extend through 2019.

• In 2019, the CPUC will implement a new NEM program, referred to by some as NEM 3.0.

• This new program is intended to incorporate the locational and temporal benefits of solar.

Future

• NEM 2.0 upheld retail rate bill credits through 2019 but requires solar owners to switch to TOU rates, pay a system interconnection fee, and pay a non-bypassablecharge ($0.02-0.03/kWh) for utility delivered electricity.

• NEM 2.0 impacts investor owned utilities (SCE, PG&E, and SDG&E).

• NEM 2.0 grandfathers customers under NEM or NEM 2.0 for 20 years from interconnection date.

• Once this grandfathering period is over, customers are placed into NEM 2.0 or the subsequent program.

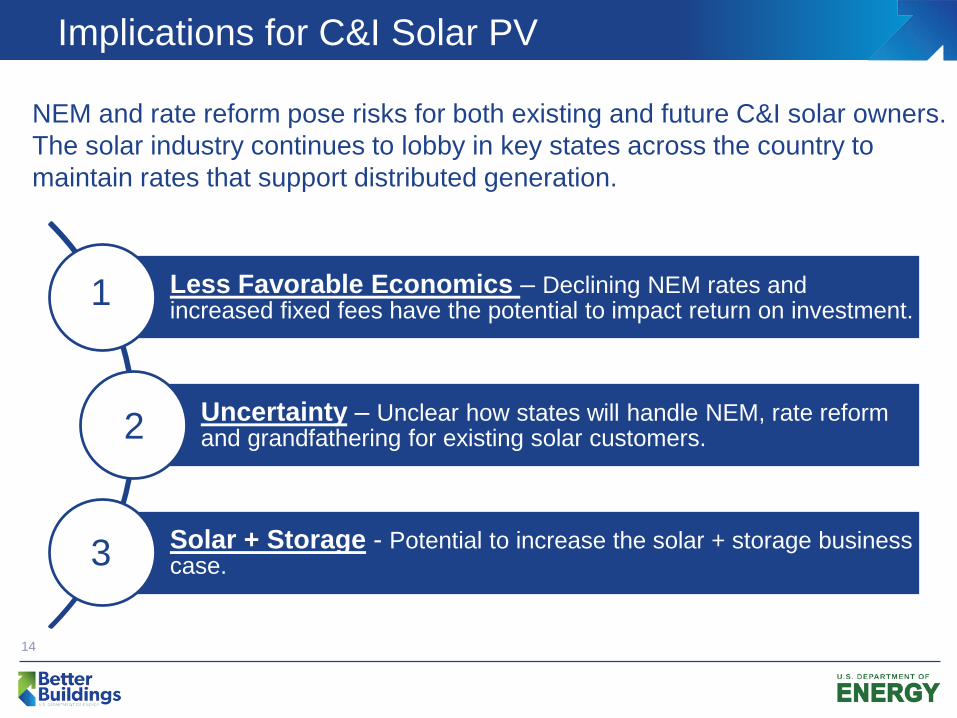

Click to edit Master title styleImplications for C&I Solar PV

14

Less Favorable Economics – Declining NEM rates and increased fixed fees have the potential to impact return on investment.

Uncertainty – Unclear how states will handle NEM, rate reform and grandfathering for existing solar customers.

Solar + Storage - Potential to increase the solar + storage business case.

NEM and rate reform pose risks for both existing and future C&I solar owners. The solar industry continues to lobby in key states across the country to maintain rates that support distributed generation.

1

3

2

Click to edit Master title styleRole of Energy Storage

15

Emerging trends in rate structures and regulation favor solar + storage over stand-alone PV systems.

NEM Rollback Demand Charges TOU Rates

• ES can increase the amount of solar generated electricity self-consumption, either reducing or eliminating the need to export electricity to the grid.

• ES can reduce demand charges by reducing peak demand.

• A much smaller storage system required when coupled with solar.

• ES can shift generation and consumption from one time of day to another time, to minimize energy costs for time-of-use (TOU) rates.

Click to edit Master title styleRecommendations for BBA Members

16

#1. Understand state policy and the risks of proposed NEM or rate reform.

#2. Determine whether existing utility customers with solar PV will be grandfathered.

#3. Ask solar provider to evaluate economics of solar PV under existing and reforming structures.

Click to edit Master title styleProject Partners

17

Navigant Consulting Jay Paidipati, Director (project lead), [email protected], 303-728-2489 Andrea Romano, Managing Consultant, [email protected], 415-399-2125 Nick Hernandez, Consultant, [email protected], 303-248-4031

DOE BBA Technical Team Oversight Jordan Hibbs, [email protected], 202-287-1381 Amy Jiron, [email protected], 720-339-7475

Appendix

Click to edit Master title styleNEM Policy Changes & Rate Reform - 2016

19

• Arizona – Value of DG proceeding took center stage and the state’s three IOUs proposed major changes to net metering, residential demand charges, and increased fixed charges.

• California – Net metering successor tariff adopted early in the year.• Colorado – Xcel Energy’s proposed Grid Use Charge was dropped in a settlement

agreement in favor of time-of-use rates.• Florida – Contentious ballot initiative that would have prohibited cross-subsidization due

to net metering didn’t pass.• Hawaii – State’s utilities hit their caps on the new Grid-Supply option, leaving Customer

Self-Supply as the remaining option.• Maine – Net metering successor bill was vetoed and the work toward a new policy has

continued at the Public Utilities Commission.• Massachusetts – Compromise bill increased the state’s aggregate cap on net metering

and made other changes to the state’s solar policy.• Nevada – Resolved debate over grandfathering existing net metering customers.• New Hampshire – Public Utilities Commission initiated the development of a net metering

successor tariff following legislation enacted earlier in the year.• New York – State’s Reforming the Energy Vision proceeding continued and led to the

noteworthy “LMP + D” valuation methodology for distributed energy resources.

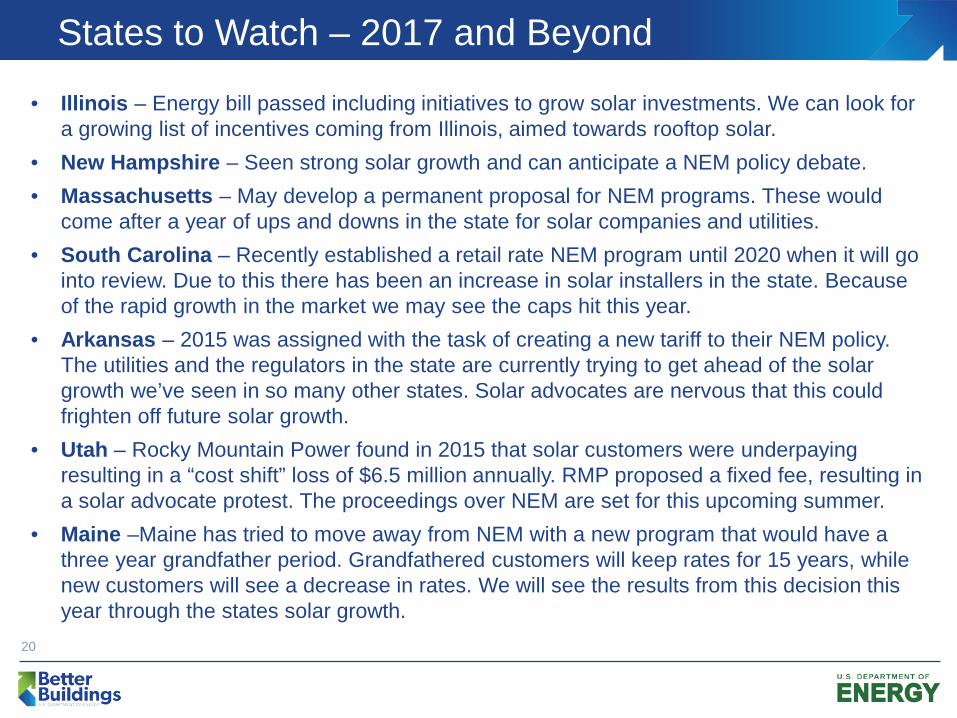

Click to edit Master title styleStates to Watch – 2017 and Beyond

20

• Illinois – Energy bill passed including initiatives to grow solar investments. We can look for a growing list of incentives coming from Illinois, aimed towards rooftop solar.

• New Hampshire – Seen strong solar growth and can anticipate a NEM policy debate. • Massachusetts – May develop a permanent proposal for NEM programs. These would

come after a year of ups and downs in the state for solar companies and utilities. • South Carolina – Recently established a retail rate NEM program until 2020 when it will go

into review. Due to this there has been an increase in solar installers in the state. Because of the rapid growth in the market we may see the caps hit this year.

• Arkansas – 2015 was assigned with the task of creating a new tariff to their NEM policy. The utilities and the regulators in the state are currently trying to get ahead of the solar growth we’ve seen in so many other states. Solar advocates are nervous that this could frighten off future solar growth.

• Utah – Rocky Mountain Power found in 2015 that solar customers were underpaying resulting in a “cost shift” loss of $6.5 million annually. RMP proposed a fixed fee, resulting in a solar advocate protest. The proceedings over NEM are set for this upcoming summer.

• Maine –Maine has tried to move away from NEM with a new program that would have a three year grandfather period. Grandfathered customers will keep rates for 15 years, while new customers will see a decrease in rates. We will see the results from this decision this year through the states solar growth.

Click to edit Master title styleCase Study Sources

21

General Policy• DSIRE, http://www.dsireusa.org/

Arizona• Krysti Shallenberger, Arizona Public Service, solar industry reach critical rate case settlement, March 2017,

http://www.utilitydive.com/news/arizona-public-service-solar-industry-reach-critical-rate-case-settlement/437186/

Hawaii• Customer Self-Supply and Grid-Supply Programs, https://www.hawaiianelectric.com/clean-energy-hawaii/producing-clean-energy/customer-self-

supply-and-grid-supply-programs• Krsyti Shallenberger, Hawaii regulators nix bid to raise caps on grid-supply rooftop solar incentive, http://www.utilitydive.com/news/hawaii-

regulators-nix-bid-to-raise-caps-on-grid-supply-rooftop-solar-incent/432464/• Mark Dyson, Hawaii just ended net metering for solar. Now what? October 2015,

http://blog.rmi.org/blog_2015_10_16_hawaii_just_ended_net_metering_for_solar_now_what

Nevada• Julia Pyper, Nevada Regulators Restore Retail-Rate Net Metering in Sierra Pacific Territory Dec 2016,

https://www.greentechmedia.com/articles/read/nevada-regulators-retore-retail-rate-net-metering-in-sierra-pacific-territo• Pieter Gagnon, Ben Sigrin and Mike Gleason, January 2017, The Impacts of Changes to Nevada’s Net Metering Policy on the Financial

Performance and Adoption of Distributed Photovoltaics, http://www.nrel.gov/docs/fy17osti/66765.pdf

New York• Shayle Kann, How to Find Compromise on Net Metering, April 2016, https://www.greentechmedia.com/articles/read/how-to-find-compromise-on-

net-metering• Katherine Tweed, New York Resets Distributed Energy rates, maintains Residental Net Metering, October 2016,

https://www.greentechmedia.com/articles/read/new-york-resets-distributed-energy-rates-maintains-residential-net-metering• Energy and Environmental Economic, Inc., Nevada Net Energy Metering Impacts Evaluation, July2014,

http://puc.nv.gov/uploadedFiles/pucnvgov/Content/About/Media_Outreach/Announcements/Announcements/E3%20PUCN%20NEM%20Report%202014.pdf

California• Breaking: California’s NEM 2.0 Decision Keeps Retail Rate for Rooftop Solar, add Time-of-Use

https://www.greentechmedia.com/articles/read/Californias-Net-Metering-2.0-Decision-Rooftop-Solar-to-Keep-Retail-Payme• Net Metering 2.0 in California: Everything You Need to Know, http://news.energysage.com/net-metering-2-0-in-california-everything-you-need-to-

know/• California Public Utilities Commission, Net Energy Metering, http://www.cpuc.ca.gov/General.aspx?id=3800