Neither sec. 194C nor sec. 195 attracted if sums paid to ... · Neither sec. 194C nor sec. 195...

16

Neither sec. 194C nor sec. 195 attracted if sums paid to NR outside India for services rendered outside India IT/ILT : Where assessee paid freight charges to foreign parties outside India for rendering services abroad, income did not accrue or arise in India and, thus, assessee was not liable to deduct tax at source while making said payments ■■■ [2013] 40 taxmann.com 310 (Delhi - Trib.) IN THE ITAT DELHI BENCH 'B' Deputy Commissioner of Income-tax - Circle-3(1), New Delhi v. Chandabh Impex (P.) Ltd. *

Transcript of Neither sec. 194C nor sec. 195 attracted if sums paid to ... · Neither sec. 194C nor sec. 195...

Neither sec. 194C nor sec. 195 attracted if sums paid to NR outside India for services

rendered outside India

IT/ILT : Where assessee paid freight charges to foreign parties outside

India for rendering services abroad, income did not accrue or arise in Indiaand, thus, assessee was not liable to deduct tax at source while making

said payments

■■■

[2013] 40 taxmann.com 310 (Delhi - Trib.)

IN THE ITAT DELHI BENCH 'B'

Deputy Commissioner of Income-tax - Circle-3(1), New Delhi

v.

Chandabh Impex (P.) Ltd.*

DIVA SINGH, JUDICIAL MEMBER AND T.S. KAPOOR, ACCOUNTANT MEMBER

IT APPEAL NO.773 & 230 (DELHI) OF 2013[ASSESSMENT YEAR 2009-10]

OCTOBER 18, 2013

I. Section 9, read with sections 194C and 195, of the Income-tax Act, 1961 - Income -Deemed to accrue or arise in India [Business operations - Payments made abroad

for services rendered abroad] - Assessment year 2009-10 - During relevant year

assessee made payments of freight, inspection and testing charges to foreignparties without deducting tax at source - Assessee's case was that since services

were rendered outside India, no TDS was required to be deducted - Assessing

Officer, however, held that assessee exported about 40 per cent goods from India

and freight was paid for those services as such section 194C was attracted -Commissioner (Appeals) noted that neither freight nor inspection charges were

paid by assessee company for any services rendered in India nor payments were

made to foreign parties in India and, therefore, provisions of section 194C orsection 195 were not applicable - Accordingly, disallowance made by Assessing

Officer was deleted - Whether since finding of fact recorded by Commissioner(Appeals) was not assailed by bringing any cogent evidence on record, same was

to be upheld - Held, yes [Para 9] [In favour of assessee]

CASES REFERRED TO

ITO v. Diza Holdings (P.) Ltd. [2002] 255 ITR 573/120 Taxman 539 (Ker.) (para 2.5), Sassoon J.

David & Co. (P.) Ltd. v. CIT [1979] 118 ITR 261/1 Taxman 485 (SC) (para 3.7), L.H. Sugar

Factory & Oil Mills (P.) Ltd. v. CIT [1980] 125 ITR 293/4 Taxman 5 (para 3.7), CIT v. Imperial

Chemical Industries (India) (P.) Ltd. [1969] 74 ITR 17 (SC) (para 3.7).

Ashwani Taneja and Somil Agarwal for the Appellant. Vivek Kumar for the Respondent.

ORDER

Diva Singh, Judicial Member - These are two cross-appeals filed by the assessee and the Revenue

against the order dated 05.11.2012 of CIT(A)-VI, New Delhi pertaining to 2009-10 assessment years.

Both these appeals are being decided by a common order as issues raised therein are interlinked. The

grounds raised by the revenue read as under :—

"1. Whether the Ld. CIT(A) has erred on facts and in law in deleting the addition of

Rs.11,120,775/- (typographical error, the amount should read Rs.11,12,775/-) made on account

of disallowance of commission expenses ignoring the facts:—

(a) The assessee company is claiming expenses merely on the basis of amount deleted in bankaccount but there is nothing on record to prove services rendered expenses are genuine for

the business purposes.

(b) The assessee company failed to provide the documentary evidences during the assessment

proceedings.

2. Whether the Ld. CIT(A) has erred on facts and in law in deleting the addition made u/s 40(a)(ia)amounting to Rs.50,95,012/- ignoring the facts that assessee company has not deducted TDS on

making the payment of freight & cartage.

3. The appellant craves leave for reserving the right to amend, modify, alter, add or forego any

ground(s) of appeal at any time before or during the hearing of this appeal."

1.1 The assessee is in appeal before the Tribunal on the following grounds:—

"1. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law

and on facts in not deleting the disallowance of Rs.1,04,86,640/- made by Ld. AO on

account of commission expenses paid by the assessee and has erred in sustaining the

disallowance being commission paid to Sh. Rakesh Talwar and M/s R.T. Associates and hasfurther erred in not considering and appreciating the evidence placed on record by the

assessee.

2. That in any case and in any view of the matter, action of Ld. CIT(A) in not deleting the

disallowance fully as made by Ld. AO on account of commission expenses paid by the

assessee is contrary to law and facts, void ab initio, and without giving adequate opportunity

of hearing, by recording incorrect facts and findings and the same is not sustainable on

various legal and factual grounds.

3. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law

and on facts in not reversing the action of Ld. AO in charging interest u/s 234B of the Income

Tax Act, 1961.

4. That the appellant craves the leave to add, modify, amend or delete any of the grounds of

appeal at the time of hearing and all the above grounds are without prejudice to each other."

2. The relevant facts of the case are that the assessee in the year under consideration who was engaged

in the business of export sale of chemicals particularly for mining and quarry industry declared an incomeof Rs.4,77,95,762/-by way of filing a return. The return was processed u/s 143(1) and subsequently by

issuance of notice u/s 143(2) and 142(1) accompanied by questionnaire etc. it was selected for scrutiny

assessment. The AO in the course of the assessment proceedings considering the fact that the assessee

had claimed commission expenses amounting to Rs.1,15,99,415/- required the assessee to provide the

necessary details.

2.1. In response thereto the assessee as per the assessment order claimed commission expenses in the

name of the following parties:-

"1. M/s R.T. Associates, Dubai Rs.3904560/-

2. Shri Rakesh Talwar, Dubai Rs.3631968/-

3. M/s R.T. Associates, Dubai Rs.2950112/-

4. M/s Alem Dasta & Co. Rs.1076285/-

5. Shri Zhou Chunyu Rs.136490/-

Rs.11599415/-

2.2 The AO required the assessee to justify its claim by providing the following details in order to

establish the genuineness of the expenses claimed:—

- Proof of services rendered by the party concerned

- Confirmation of the concerned parties

- Copies of communication, e-mains, advisory etc. between the assessee and person to whom

commission has been paid."

2.3 In response thereto the assessee filed written submissions dated 15.11.20111, the same areextracted in the assessment order and reproduced hereunder for ready-reference:—

"The assessee has tried to contact them over phone and via e-mail to with reminder sent to RT

Associates/Rakesh talwar UAE as also Mr. Zhou of Chunyu Consultants, China but unfortunately

there is no response from any of them till date. As regards, Alem Desta & Co., Ethipia, there is no

e-main contact address, but the owner Mr. Alem Desta was contacted over phone once and

requested to provide the required information for the tax purpose. He has neither sent any

information nor is responding to out telephone calls."

2.4 Considering the submissions advanced the AO was of the view that the assessee does not having

any documentary evidence to prove services rendered by the concerned parties and taking into

consideration the fact that no communication is available from the parties and even confirmation of the

recipient is not filed and the only plea taken is that the amount is paid through banking channel held the

explanation as not acceptable. He was of the view that the genuineness of the expenses for businesscannot be accepted merely on the basis of the fact that the amount was credited through banking

channels.

2.5 Reliance was placed upon ITO v. Diza Holdings (P) Ltd. [2002] 255 ITR 573/120 Taxman 539

(Ker.) for the proposition that the burden was on the assessee to offer a satisfactory explanation about

the nature and source of the amount found credited in the books of the assessee. Mere furnishing of

particulars was not enough and the mere fact that the payment was by way of account payee cheque

was also not conclusive. Reliance was also placed on the following judgements:—

"(i) Sassoon J. David & Co. (P) Ltd. v. CIT [1979] 118 ITR 261/1 Taxman 485 (SC);

(ii) L.H.Sugar Factory & Oil Mills (P.) Ltd. v. CIT [1980] 125 ITR 293/4 Taxman 5 (SC);

(iii) CIT v. Imperial Chemical Industries (India) (P) Ltd. [1969] 74 ITR 17 (SC);

(iv) Jaswant Trading Co. v. CIT [1995] 212 ITR 24/[1996] 85 Taxman 639 (Raj.);

(v) Annamma Alexander v.CIT[1989] 176 ITR 229/[1990] 48 Taxman 329 (Ker.)."

2.6 Accordingly the claim of the assessee was disallowed with the following observations :—

"In view of the above noted facts it is proved that the assessee company is claiming expenses

merely on the basis of amount debited in bank account but there is nothing on record to prove

services rendered & expenses are genuine for business purposes. The assessee company failed to

provide the documentary evidences as called for by the AO during the assessment proceedings.

Thereby assessee failed to substantiate its claim of expenses by not submitting documentary

evidence. Hence amount of Rs.11599415/- is hereby disallowed and added back to the income of

the assessee company."

3. In appeal before the First Appellate Authority the assessee moved a petition under Rule 46A of the

ITAT Rules 1962 requesting for admission of additional documents/evidences. The CIT(A) forwarded

the same to the AO seeking a report on the additional evidence. As per para 3 of the impugned order

the AO submitted his report dated 09.07.2012 and the assessee in response thereto filed its rejoinder

thereto (the copy of the Remand Report was provided by the assessee in the course of the hearing).

3.1 Considering the arguments of the assessee, the fresh evidences were admitted by the CIT(A) on the

following reasoning :—

"5.3. I have carefully considered the submissions made by the Ld. AR and have gone through the

assessment order. I have also considered the remand report submitted by the AO, written

submissions of the appellant company, and the rejoinder on the above ground.

5.3.1 As regards to admissions of additional evidences are concerned, I find that assessment order

in the present case was passed by the AO on 16.12.2011, and the appellant submitted a letter

dated 15.12.2011 with which copies of the relevant agreements towards payment of commission

were filed before the OA, which were not considered by the AO while passing the impugned

order. Similarly copies of email message from Mr. Zhou of Chunyu Consultants confirming the

commission paid to them by the assessee and further confirming that they had seen the mail of the

appellant late, could not be filed by the appellant due to genuine reasons explained, and therefore,

in the interest of justice, when such evidences prove the genuineness of the transactions, and go to

the root of the matter, cannot be ignored just because, for the reasons explained by the appellant,

could not be filed during the course of assessment proceedings. All these evidences were

forwarded to the AO for examination, but no comments are given by the AO on any of these

evidences. As a find that these evidences filed are necessary to adjudicate the grounds of theappeal, the additional evidences filed by the appellant company are admitted."

3.2 The CIT(A) further took into consideration the arguments that the assessee had no control over the

commission agents for ensuring timely reply and the commissions/facilitation fees are essential for

fructification of the trading business and that the agents were necessary as the assessee does not have

any permanent/exclusive agents. The assessee had canvassed that in the year under consideration on

account of the ban of exports of Ammonium Nitrate by China due to Beijing Olympics an acute shortage

and steep rise in prices in the international market resulted and the window of opportunity so created

was utilized by the assessee which had resulted in huge margins which could be earned only with the help

of these foreign agents/parties who sourced the material according to the requirements of the assessee.

The profit has resulted it was argued only with the help of these foreign parties/agents. It was stated the

assessee faced difficulty in providing the required information to the AO as these parties were based

overseas and the assessee had no control over them so as to force through phone etc. to confirm the

transactions to the satisfaction of the AO as having no control over the parties the assessee was not in aposition to insist for their co-operation as such could initially only rely on the fact that the payments have

been made through the banking channels.

3.3 It was submitted that these parties namely R.T. Associates and Rakesh Talwar, UAE who facilitated

in making available most of the company's requirements of Ammonium Nitrate by sourcing from Egypt,

Iran and Europe whereas Alem Desta Co. and Zhou Chunyu Consultants facilitated sales with Chinese

Company engaged in quarry operations in Ethiopia was in itself adequate evidence for having rendered

the requisites service for which commission was paid. It was also submitted that the commissions had

been remitted only when the company realized full payments from its overseas clients/buyers. In support

of the claim it was stated that before the AO confirmation of the swift advice from the ICICI Bank were

available for R.T. Associates; whereas for Alem Desta & Co. and Zhou Chunyu Consultants they were

not readily available because these were relating to old records. However it was argued the bank had

separately confirmed the payments made and the confirmations were filed before the AO. It was further

submitted that it was specifically brought to the notice of the AO that payment to Rakesh Talwartowards commission for product sourcing from Iran was made through SBI, South Extension Branch,

New Delhi as no other bank was willing to transact business with Iran at that point of time due to

uncertainty in the geographical location etc. In these circumstances the insistence of the AO to provide

copy of PAN Card, I.D. proof, Indian address of these parties and their other business connections inIndia was assailed as these documents could not be provided as none of the parties resided in India. Itwas also argued that the AO was informed that the assessee has had no dealings with these parties in

any subsequent year. It was also submitted that the AO was also informed that Mr. Talwar was settled

in Dubai for over 30 years and had no interest in India.

3.4 The record shows that on behalf of the assessee it was also argued that the AO was informed that

the assessee had no permanent/exclusive agent outside India and in order to obtain the facilities and in

the interests of the business the assessee had to obtain the services of these parties for facilitating in

procuring the material to ship the same to the respective destinations where the sales are made. It was

stated that in order to ensure the timely payment from the parties and related activities and for

satisfactorily completion of the business transaction the parties had provided services to the assessee and

for the rendering of these services the commission had been paid. It was emphasized that it had been

brought to the notice of the AO that at the relevant point of time there was an acute shortage of

Ammonium Nitrate due to restrictions imposed on exports of Ammonium Nitrate by China due to

Beijing Olympics and the assessee made efforts to exploit this opportunity by engaging R.T. Associates/Rakesh Talwar who could facilitate in the procurement and shipment of Ammonium Nitrate as the

assessee on its own was not able to secure the required quantity in the prevailing scarcity of the product

from its regular source namely Deepak Fertilizers & Petrochemical Corporation Ltd, Pune who was able

to provide only limited quantities and since it had received a much larger order from its client in

Indonesia, it was imperative to source quality Ammonium Nitrate from overseas suppliers so as to

supplement the ordered quantity to the extent possible. It was submitted that only on account of the

efforts of and services provided by R.T. Associates/Rakesh Talwar that the assessee company earned a

five fold profit as compared to what is generally made on this product during this period of scarcity of

Ammonium Nitrate. It was submitted that substantial profits were generated for sale of product to

Ethiopia through Alem Desta Co./Chunya Consultants. The total commission paid to these parties it was

submitted works out to about 5.5% of the total turn over of the assessee company and the assessee

generated a profit of 25% (Rs.4,79,02,567/-) as reflected in the P&L A/c of the assessee company. It

was emphasized that it had been explained to the AO that in the last 2 years the assessee had no

dealings with any of these parties and as such it is difficult to prevail upon them to provide the required

information. It was submitted that the assessee had tried to contact the parties over phone and e-mail

and also sent reminder to R.T. Associates and Rakesh Talwar, UAE and also Mr.Zhou of Chunyu

Consultant, China but unfortunately there was no response of any of them. As regards Alem Desta &

Co., Ethiopia it was stated there was no e-mail, contact address but the owner Mr. Alem Desta was

contacted over phone and requested to provide information for tax purposes.

3.5 It was reiterated that the commissions were paid in pursuance to services rendered not only for

procuring the material but also to send the same to the destination i.e customers of the assessee requiring

the making of arrangement for transportation of the same and ensuring the payments from customers and

ensuring payments to the assessee. Apart from these bare and simple activities the parties performed

various activities outside India as goods were sourced from outside India and sold and delivered outside

India which was possible for these parties only as the assessee could not handle these from India and

had it attempted to do so itself the sheer cost and lack of local awareness would have been an obstacle.

3.6 The action of the AO was also assailed on the ground that the AO has ignored the ground realities

which prevail in a business scenario where services are procured from outside agents the filling of

agreements, invoices, copies of swift advices issued by the bank confirmations that the payments were

remitted from the bank cannot be ignored merely because the assessee who is not in contact with these

parties as it has no business dealings as such is unable to give confirmations. It was argued that the AO

has ignored that the assessee has tried to contact them on phone and e-mail and has no control over

them. It was submitted that it is not the case of the AO that the parties to whom commission has beenpaid are known to the assessee or are relatives or family member or are related to the director either in

the company or sister concerns if any. The commission paid it was submitted is not very high when

compared to the profits earned the commission it was argued has not even been held to be bogus or

genuine by the AO.

3.7 The reliance placed by the AO on Sassoon J. David & Co.(P) Ltd. v. CIT [1979] 118 ITR 261/1

Taxman 485 (SC) was wrongly applied as that was a case where disallowance of the commission wasthe nature of the salary and the facts are entirely distinguishable. Similarly reliance on L.H.Sugar

Factory & Oil Mills (P) Ltd. v. CIT [1980] 125 ITR 293/4 Taxman 5 (SC) and CIT v. Imperial

Chemical Industries (India) (P.) Ltd. [1969] 74 ITR 17 (SC) also it was stated did not applied as the

assessee has submitted voluminous evidences to justify the expenditure incurred on commission paid. It

was submitted that it is not even the case of the AO that the commission was not remitted by these

parties, he has only disallowed the same as the assessee could not submit the confirmations of the

parties. Had the parties been situated in India, it was stated the assessee could have produced them but

since they are situated outside India it was not possible to produce them. Reference was made to the

various documents in the paper book filed namely copies of e-mail reminders, copies of e-mail received

from Mr. Zhou of Chunyu confirming the payment certificate from the ICICI Bank, telephone no. and e-

mail of Rakesh Talwar, Alem Desta. It was submitted that these are substantial evidences to prove that

the commission was paid. Nothing contrary to the said fact it was argued has been brought on record by

the AO. It was reiterated that it was a legitimate business expenditure of the assessee which has not

been doubted and it has resulted in high profit because of the services rendered by these persons which

profit the assessee could not have earned without the help of these persons as all the activities performed

by them in the absence of the parties abroad could not have been possibly performed by the assessee. It

was argued that had the assessee not taken the services of these persons than the assessee would have

had to open some office/offices in those countries and employ persons to look after its business affairs

who would then seek services from the local persons and as such it was a prudent business decision to

pay commission which was a cheaper course of action by way of which the assessee has maximized its

profit by exploiting the scarcity of the Ammonium Nitrate at the relevant point of time instead of

establishing a business office abroad. Addressing the additional evidences filed it was stated that the AO

has not commented negatively thereon which leads to the conclusion that the AO has nothing before it to

disregard the same. Reliance was placed upon following judgments:—

"(i) ITO v. Shyam Sunder Jajodia [2008] 26 SOT 541;

(ii) CIT v. Konkan Marine Agencies [2009] 313 ITR 308 (Kar.);

(iii) Asstt. CIT v. Shree Sajjan Mills Ltd. [2008] 112 ITD 135 (Indore) (TM)

(iv) CIT v. Printers House (P) Ltd. [2008] 112 Taxman 70 (Delhi)."

3.8 A perusal of the impugned order shows that the fresh evidences which the assessee could obtain by

the time of the appellate proceedings were admitted by the CIT(A) accepting the reasoning that the

evidences filed on 16.12.2011 before the AO could not be considered as the assessment order was

passed on the said date itself. The relevant agreement in support of the commission paid alongwith copy

of e-mail, message from M/s Zhou Chunyu Consultants etc. since went to the root of the matter the

CIT(A) was held could not be ignored as such they were taken into consideration and since these

evidences were not considered by the AO the same were confronted to him. The CIT(A) it is seen

taking note of the fact that these were not controverted by the AO as he offered no comments despite

opportunity accepted the same.

3.9. Addressing the evidence filed in support of the commission paid to Mr. Alem Desta it is seen that

the CIT(A) took into consideration the fact that the assessee submitted a Copy of the Agreement with

the said party for soliciting business particularly from Chinese company working in Ethiopia for Bitumen

and Explosives/Accessories sourced from various countries including India alongwith copy of invoices

for commission payable; confirmation from ICICI Bank dated 08.02.2012 confirming the payment

remitted to the bank of M/s Alem Desta & Co., Ethiopia. These evidences were considered to be

sufficient to prove that commission was paid by the assessee to M/s Alem Desta company of Ethiopia.

3.10 Considering the evidence for Chunyu Consultants the CIT(A) took note of the fact that

confirmations received through e-mail dated 25.02.2012 from M/s Mr. Zhou of Chunyu Consultants

confirming commission paid substantially proved that the expenses incurred by the assessee for

commission was paid to the said party wherein the said party confirmed the receipt of USD 3150 in

2008 from the assessee company towards commission for facilitating sale of explosives in Ethiopia.

3.11 However considering the claim of commission paid to M/s R.T. Associates wherein the assessee

did not provide documentary evidence and merely stated that the assessee was unable to contact the

said party, the CIT(A) was of the view that in the present day and times where there are so many means

of communication available namely e-mail, telephone no etc and confirmations from Alem Desta,

Ethiopia and Mr. Zhou Chunyu of China could be filed despite that the assessee has not been able toeven contact Sh.Rakesh Talwar was considered to be not credible. In this background the mere fact of

payment of commission through banking channels was considered to be not sufficient evidence of

rendering the services. Addressing the evidences filed, the CIT(A) noticed that the passports of Mr.

Rakesh Talwar, first passport was issued on 21.03.2007 and was valid upto 20.03.2017 and despite

that copy of another passport issued on 11.01.2011 was available which was valid upto 10.01.2021.

Both the passports showed that the said person was an Indian National and the passports were issued

by Consulate General of India, Dubai, UAE. According to the CIT(A), there was a doubt on the identity

of Sh. Rakesh Talwar itself. Accordingly rendering of services by M/s. R.T. Associates was not

accepted by the CIT(A). 4.3.1.

3.12 The Reliance placed upon ITO v. Shyam Sunder Jajodia [2008] 26 SOT 541 (Delhi) by the

assessee was considered to be not relevant as in the facts of that case the commission agents had

responded to the query of the AO and some of them had even supplied information regarding rendering

of services. Apart from that fact the commission payment was allowed to these agents in the earlier yearsand in subsequent years on similar lines. Thus the facts were considered to be distinguishable.

3.13 Similarly in Asstt. CIT v. Sh. Sajan Mills Ltd [2008] 112 ITD 135 (Indore) (TM) the CIT(A)

was of the view that the assessee had fully discharged the burden placed upon it to prove the payment of

commission as similar commission was paid to the assessee in earlier years. In the facts of present case

he was of the view that there is no regular dealing with M/s R.T. Associates either in the past or in

subsequent years accordingly the claim qua the said party was held to be disallowed. Consequently only

the payment of commission made to Alem Desta and M/s Zhou of Chunyu Consultants were allowed

and the payment of commission to M/s Rakesh Talwar was held to be not genuine and disallowed.

4. Aggrieved by this both the assessee and the department is in appeal before the Tribunal. The assessee

has moved Ground No-1 & 2 and the departmental ground qua the relief granted by the CIT(A) has

agitated Ground No-1 which have been reproduced in the earlier part of this order.

4.1 The Ld. Sr. DR addressing the departmental ground invited attention to the assessment order so as

to contend that the said order was passed on 16.12.2011 as such the assessee has filed the evidencesought by the AO only on 15.12.2011 and why the same evidence could not be filed in the course of the

assessee proceedings was questioned. The evidences it was argued were filed only at the fag end of the

assessment proceedings which lead to the need for filing petition for admission of fresh evidence beforethe CIT(A). The said fact it was requested needs to be addressed by the assessee. It was his stand that

merely stating that the commission has been paid through the banking channels cannot be said to

discharging the onus placed to prove that services have been rendered by the commission agent. The

said onus it was submitted was upon the assessee which should have been discharged by the assessee

during the assessment proceedings. As such relying upon the departmental ground it was his submission

that the assessee has failed to provide documentary evidence in the course of the assessment

proceedings. Accordingly it was his submission that the assessment order be upheld and the impugned

order be set aside.

4.2 Ld. AR addressing the departmental grounds submitted that the CIT(A) has arrived at a finding that

sufficient opportunity was not given by the AO in the course of the assessment proceedings as such the

evidence could be filed at the fag end of the assessment proceedings. It was also his submission that the

AO has failed to appreciate the fact that the transaction took place in 2008 and the assessee had neither

any prior dealing with these parties and nor subsequent dealing with these parties. It was his submission

that there is not even a whisper of suspicion cast by the Revenue on the fact that these were related

parties or associated concern or sister concerns etc. It was stated that parties were contacted when due

to the prevalence of peculiar shortage occurring due to the restriction imposed by China before the

Beijing Olympics for acquiring the specific product as a result of which the assessee exploited the

situation for commercial considerations and made attempts in the international market to source and

provide the chemicals by utilizing the services of these different parties who not only made the specific

chemicals available to the assessee but also ensured transportation of the same from the sourcing

countries to the customers and ensure the payment from the customers to the assessee and only after

these services were performed commissions were paid. It was submitted that before the CIT(A) it had

been argued that had the assessee not utilized the services of these parties then the assessee would have

had to open an office in these countries, engage manpower, to further engage the local parties to ensure

transportation, delivery and payment from the parties and since the assessee does not have any dealing

with these parties, the occasion to control and ensure co-operation to give confirmations in support ofthe transaction cannot be held against the assessee as it had no control over the parties. It was his

submission that the record would show that the assessee in-compliance with the requirements of the AO

tried his level best to contact these three parties and from two of the parties the assessee could get

confirmations/agreement etc and the said evidence could be made available at the fag end of the

assessment proceedings despite the best efforts of the assessee. The said evidences it was submitted has

been rightly considered by the CIT(A) to be crucial and relevant evidence and the record would show

was made available to the AO who has not led any evidence to discredit the same. Addressing the

arguments moved on behalf of the Revenue it was his submission that the Ld. Sr. DR has also not

discredited the evidence and has merely argued that why the same could not be made available in the

assessment proceedings. It was argued that the assessee has led sufficient arguments addressing this

aspect and as soon as the evidences were available the assessee placed them on record and if the AO

could not go through the same on account of paucity of time, the evidences have been admitted by the

CIT(A) and confronted to the AO. The arguments that the assessee neither had any control over the

said parties and nor had any prior or subsequent dealings is a matter of record as such the mere

arguments that why it could not be made available during the assessment proceedings does not detract

from that fact that nothing adverse to the evidences has been argued as such it was his submission that

the departmental appeal deserves to be dismissed.

4.3 Addressing the ground raised by the assessee it was his submission that the assessee has filed

petition for admission of additional evidences before the ITAT. Referring to the same it was submitted

the petition was filed for admission of additional evidence under Rule 29 of the I.T. Rules on 08.08.2013

and the appeal was adjourned to 14.08.2013 in order to afford department to go through the same.

Addressing the said petition which is in continuation of the paper book filed on 01.07.2013 running into

195 pages, it was stated that the additional evidence sought to be admitted are placed in a separate

paper book on additional evidence running from 196 to 246 of the paper book. The Ld. AR submitted

that page 139 to page 164 of the original paper book contains the written submissions filed dated

12.03.2012., specific attention was invited to page 144 of the same in support of the arguments that the

bank confirmations confirming the fact that the payments have been remitted to the specific persons were

available on record of the AO and the assessee had explained that for the last few years there has been

no occasion to stay in contact with the said persons and the efforts made over phone and e-mail and

reminders have not resulted in any confirmations and copies of e-mail reminders as per page 145 of the

paper book were filed before the CIT(A) and copies of details of invoices and purchases for payment of

commission paid to M/s R.T. Associates alongwith invoices of M/s R.T. Associates, Dubai were alsofiled before the CIT(A). Copy of the invoice dated 18.03.2009 of R.T. Associates, Dubai, UAE was

also filed showing charging of the commission of USD 57800 towards sale of Ammonium Nitrate from

Egypt, France, Sweden to Indonesia before the CIT(A). Similarly copy of invoice dated 09.03.2009 of

M/s R.T. Associates, Dubai to the assessee company for charging of commission of USD 76500

towards sale of Ammonium Nitrate Egypt to Indonesia has been filed before the CIT(A). Copy of

agreement dated 20.05.2005 made between the assessee company and R.T. Associates for payment of

commission for facilitating supply of Porous Prilled Ammonium Nitrate as per agreed specifications from

Egypt/Europe/South Africa for a minimum quantity of 3000 M.T. of Ammonium Nitrate to be shipped

latest by 31.03.2009 wherein the commission payable agreed @ USD 55/MT upon full realization of the

payment from the assessee overseas customers had also been filed before the CIT(A) as would be

evident from page 146 of the paper book. Copy of the swift advise of the ICICI Bank of the specific

amount were also filed. Similarly copy of the agreement dated 20.05.2008 between assessee and

Rakesh Talwar of UAE and validity of agreement upto 31.03.2009 for shipment of 1000 MT of

Ammonium Nitrate with commission payable @ USD 70/MT payable upon full realization of the

payment from the assessee's overseas customers was also filed before the CIT(A). Copy of the bank

statement of the assessee company from State Bank of India showing that payment of USD 69200 to

Mr. Rakesh Talwar along with copy of relevant bills on which commission has been paid were filed by

the CIT(A) as would be evident from page 147. As such it was his argument that all these evidences

were similar to the evidences filed before the CIT(A) for the other two parties which the CIT(A)

accepted as sufficient evidence for rendering services. The only reason for discarding these relevant and

similar evidences in the case of M/s R.T. Associates was that unlike the other two parties herein the

assessee could not file a confirmation in response to its e-mails or telephones etc. and the CIT(A) for the

said specific reason has rejected the cogent evidence as in insufficient evidence. In these circumstances,

it was his submissions that the assessee needs to file additional evidence which has now come in

possession of the assessee. The fact that it goes to the root of the matter cannot be disputed. The saidevidence it was submitted is the copy of the Death certificate of Mr. Rakesh Talwar which shows his

permanent address as A1/302, Diera, Dubai (copy placed on page 196 of the paper book). Addressing

page 196A of paper book it was submitted that the said death certificate has been attested by the

Embassy of UAE. It was his submission that copies of the old passport and new passport of erstwhile of

Rakesh Talwar are placed at page 197-224 which on account of the frequent travel of the said person

had to be issued again as per the requirements of the passport office. Addressing the fact as to why Sh.

Rakesh Talwar did not respond to the e-mail and the telephones, it was his submission that Sh. Rakesh

Talwar expired on 24.12.2012 after a prolonged illness which required his diagnosis, hospitalization and

investigation and on account of being pre-occupied with his medical condition, the said person did not

respond to the e-mails and telephones of the assessee for reasons which can now be understood with

hindsight. The medical papers showing continuous ill health of the Sh. Rakesh Talwar, it was submitted

are placed at pages 225-245 of the paper book. Addressing in this background the evidence sought to

be filed, attention was invited to page 52 of the paper book which would show that all necessary

evidence was available before the CIT(A) i.e the Agreement for sourcing Ammonium Nitrate dated

20.05.2008 between the assessee and Mr. Rakesh Talwar signed by the erstwhile Sh. Rakesh Talwar

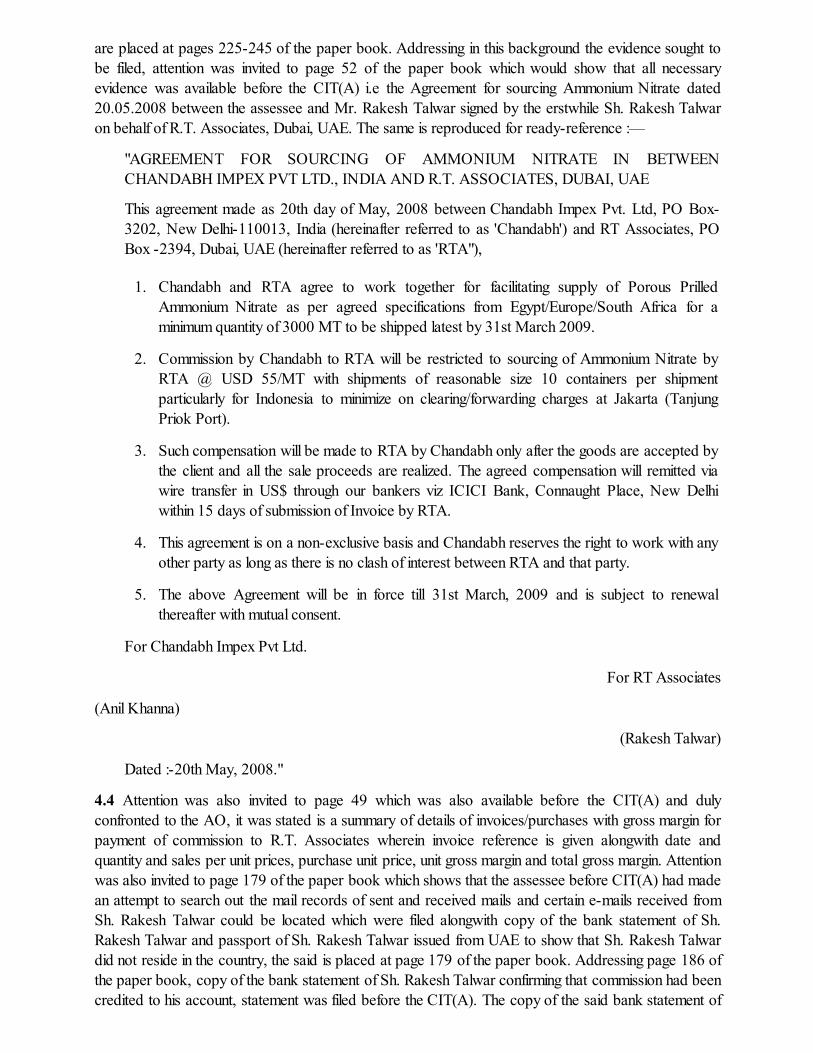

on behalf of R.T. Associates, Dubai, UAE. The same is reproduced for ready-reference :—

"AGREEMENT FOR SOURCING OF AMMONIUM NITRATE IN BETWEEN

CHANDABH IMPEX PVT LTD., INDIA AND R.T. ASSOCIATES, DUBAI, UAE

This agreement made as 20th day of May, 2008 between Chandabh Impex Pvt. Ltd, PO Box-

3202, New Delhi-110013, India (hereinafter referred to as 'Chandabh') and RT Associates, PO

Box -2394, Dubai, UAE (hereinafter referred to as 'RTA"),

1. Chandabh and RTA agree to work together for facilitating supply of Porous Prilled

Ammonium Nitrate as per agreed specifications from Egypt/Europe/South Africa for a

minimum quantity of 3000 MT to be shipped latest by 31st March 2009.

2. Commission by Chandabh to RTA will be restricted to sourcing of Ammonium Nitrate by

RTA @ USD 55/MT with shipments of reasonable size 10 containers per shipment

particularly for Indonesia to minimize on clearing/forwarding charges at Jakarta (Tanjung

Priok Port).

3. Such compensation will be made to RTA by Chandabh only after the goods are accepted by

the client and all the sale proceeds are realized. The agreed compensation will remitted via

wire transfer in US$ through our bankers viz ICICI Bank, Connaught Place, New Delhi

within 15 days of submission of Invoice by RTA.

4. This agreement is on a non-exclusive basis and Chandabh reserves the right to work with any

other party as long as there is no clash of interest between RTA and that party.

5. The above Agreement will be in force till 31st March, 2009 and is subject to renewal

thereafter with mutual consent.

For Chandabh Impex Pvt Ltd.

For RT Associates

(Anil Khanna)

(Rakesh Talwar)

Dated :-20th May, 2008."

4.4 Attention was also invited to page 49 which was also available before the CIT(A) and duly

confronted to the AO, it was stated is a summary of details of invoices/purchases with gross margin for

payment of commission to R.T. Associates wherein invoice reference is given alongwith date and

quantity and sales per unit prices, purchase unit price, unit gross margin and total gross margin. Attention

was also invited to page 179 of the paper book which shows that the assessee before CIT(A) had made

an attempt to search out the mail records of sent and received mails and certain e-mails received from

Sh. Rakesh Talwar could be located which were filed alongwith copy of the bank statement of Sh.

Rakesh Talwar and passport of Sh. Rakesh Talwar issued from UAE to show that Sh. Rakesh Talwar

did not reside in the country, the said is placed at page 179 of the paper book. Addressing page 186 of

the paper book, copy of the bank statement of Sh. Rakesh Talwar confirming that commission had been

credited to his account, statement was filed before the CIT(A). The copy of the said bank statement of

Sh. Rakesh Talwar it was stated is placed at page 190 of the paper book. Addressing the background itwas submitted that the AO had started his inquiry from December 2011 and Sh. Rakesh Talwar has

been ill from January 2011 as such there was sufficient and credible evidence to show why Sh. Rakesh

Talwar could not and did not respond but the evidence on record show that services have been

rendered by the Sh. Rakesh Talwar on account of which substantial profits have been earned and

payments have been made to Sh. Rakesh Talwar and there is no shred of evidence or doubt for that

matter that the payment has come back to the assessee. Accordingly in these circumstances it was his

submission that the fresh evidence deserves to be accepted and considering the same the additionsustained deserves to be deleted.

4.5 The Ld. Sr. DR qua the assessee's appeal opposed the admission of additional evidence it was hissubmission that the record shows that the concerned persons traveled a lot as would be evident from the

stamping from page 217 and page 221 of the paper book which is the fresh evidence sought to beadmitted. Referring to the same it was pointed out that Sh. Rakesh Talwar was granted a visa and he

traveled to USA in December 2011. Similarly page 223 of the paper book it was submitted would showthat on 10.06.2012 Sh. Rakesh Talwar traveled to Delhi. Accordingly it was his submission that when

the said person was fit to travel to different countries, he most definitely could have responded to the e-mails and telephones of the assessee as such the fresh evidence sought to be admitted itself does not

support the case of the assessee.

4.6 Ld. AR addressing the objections of the Sr. DR invited attention to page 196 of the paper book soas to emphasize that it would show that Sh. Rakesh Talwar who traveled to India on 10.06.2012 passed

away in India on 28.06.2012 at Max Devki Heart & VA at 2 Press Enclave Road, Saket, New Delhi.Inviting attention to page 242 of the paper book it was his submission that the travel to the US wasundertaken on account of getting medical help/investigation in order to diagnose the medical condition

and the Report of the department of Neurological Surgery, Surgery Directors of California Center forsome rare medical condition available on record at page 242 would show that Associate Professor,

Sandeep Kunwar, MD examined him and his Report is on record. As such it was his submission that thesuspicion of the department that the travel was vacation/travel is misplaced as the same were frantic

efforts made to diagnose the medical condition and ultimately Sh. Rakesh Talwar succumbed to thedisease as such it was submitted that the reasons for non-reply of Sh. Rakesh Talwar the only reason

which prevailed upon the CIT(A) to discard the cogent evidences which were similar to the other twoparties is crucial and goes to the root of the matter and deserves to be admitted.

5. We have heard the rival submissions and perused the material available on record. On a consideration

of the same, we are of the view that the additional evidence sought to be admitted by the Ld. AR onbehalf of the assessee deserves to be admitted as the reasoning taken by the CIT(A) for not acceptingthe assessee's claim namely the fact that Sh. Rakesh talwar of R.T. Associates has not responded to the

e-mails/telephones of the assessee confirming the rendering of services can be addressed by theseevidences. The suspicion so addressed for discarding the evidences relied upon can be addressed only

by these evidences as such they go to the root of the matter and deserves to be admitted. Theseevidences directly throw light on the suspicion of the department as they address why Sh. Rakesh

Talwar did not respond to the telephone and e-mails, the fresh evidence sought to be admitted towardsthis fact as such are relevant and cogent material as the transaction has been held to be not genuine,

solely on account of the fact that the said party did not respond. It is seen that the evidence and materialavailable on record before the CIT(A) which is confronted to the AO has not been discredited by the

AO for all the three parties and whereas for the two parties the CIT(A) has found the evidence sufficientand cogent namely for Chunyu and Alem Desta and for Rakesh Talwar of R.T. Associates he has

decided the issue against the assessee as the concerned party did not confirm the rendering of services.Addressing the departmental ground as discussed in the earlier part of this order where the detailed

arguments before the CIT (A) have been discussed in detail as found advanced before the CIT (A)which was reiterated before we find no good reason to interfere with the finding of the CIT (A) qua

Chunyu Consultants and M/s Alem Desta as the evidence relied upon has not been assailed by theRevenue nor any argument has been advanced on merit as to why the relief granted should be withdrawn

apart from the argument that the evidences ought have been filed in the assessment proceedings beforethe AO which has already been addressed as on facts we confirm the finding of the CIT(A) that the

assessee having no control over the said parties cannot be held accountable for the delay in bringing onrecord the material at the fag end of the proceedings which had arisen due to paucity of time during the

assessment proceedings. On considering the arguments advanced before the CIT(A) which wererepeated before us, we concur with the finding of the CIT(A) that for reason beyond the control of the

assessee the evidences could not be filed in the course of the assessment proceedings due to paucity oftime granted by the AO specially as the assessee had no interaction with the said parties and was not in

a position to control the parties to direct immediate compliance by confirming. Accordingly we upholdthe action of the CIT(A) in accepting the assessee's claim qua the two parties. As such the departmental

ground is dismissed.

5.1 Addressing the assessee's ground we have already recorded a finding that the evidences sought to

be filed addressing the demise after travel for obtaining medical opinion diagnose the medical conditionof Sh. Rakesh Talwar erstwhile resident of Dubai who ultimately passes away on 28.06.2012 in Max

Hospital, Saket, New Delhi, within a month of his arrival in India, as such the assessee had adequatelyled sufficient and cogent evidence to demonstrate that Sh. Rakesh Talwar during the period the assessee

was attempting to get a reply to its e-mails / phones etc. Sh. Rakesh Talwar was pre-occupied with hismedical treatment due to which confirmation reply could not be obtained. The various pages in the

passport referred to by the Sr. DR showed that he traveled to USA, India on specific dates andevidences at pages 225 to 246 which contains copies of medical papers of Sh. Rakesh Talwar from

19.01.2011 in Sharjah, UAE, Dubai, UAE, India, California, USA etc. as such qua M/s R.T.Associates support the plea of the assessee accordingly we set aside the finding of the CIT(A) wherein

he has not cared to address the evidences relied upon qua the rendering of services by the said partyand restore the issue back to the AO to consider the evidence and pass a speaking order in accordance

with law after giving the assessee a reasonable opportunity of being heard. Accordingly assessee'sground is allowed for statistical purposes.

6. Qua the second issue addressed by the department the facts as per the assessment order are that theAO has observed that the assessee has not deducted TDS on the following payments:-

"Freight & Cartage (Contractual in nature)

9.6.2008 AL Ansr Co. for coke & Chem Rs.326721/-

7.7.2008 APM Global Logistics Egypt Limited Rs.864731/-

12.10.2008 APM Global Logistics Egypt Limited Rs.909972/-

28.10.2008 APM Global Logistics Egypt Limited Rs.592706/-

3.11.2008 APM Global Logistics Egypt Limited Rs.1088450/-

1.12.2008 APM Global Logistics Egypt Limited Rs.461519/-

31.01.2009 APM Global Logistics Egypt Limited Rs.575460/-

Rs. 4819559/-"

6.1 Accordingly he required the assessee to explain the same by way of issuance of show cause notice.

In response thereto the assessee pleaded that the services were rendered outside India and accordinglyno TDS was required to be deducted. Support was derived from circular No.786 dated 07.02.2000.However the AO was not convinced with the explanation offered and held that the assessee exported

about 40% goods from India & freight & cartage was paid for these services as such section 194C wasattracted. He was also of the view that testing charges were also paid for the testing of goods sent from

India and the circular relied upon had been withdrawn as such he held TDS should have been deductedfor the said payments as such on account of failure on the part of the assessee to do so, disallowance u/s

40(a)(ia) of the Income Tax Act, 1961 amounting to Rs.50,95,012/- was made u/s 40(a)(ia) read withsection 100 of the Income Tax Act.

7. In appeal before the First Appellate Authority the factual finding on the legal principles relied upon bythe AO was assailed on behalf of the assessee. These arguments are found recorded at para 6.2 at

pages 17-20 of the impugned order. A perusal of the same shows that attention was invited to the factthat the details of payments of freight and cartage claimed in the P&L Account were made to APM

Global Logistics Egypt and M/s Al Ansr Co. supported by copies of invoices filed before the AO wererelied upon. The inspection charges it was stated were paid to M/s Egyptian Chemical industries and the

copies of invoices in support of the said claim available before the AO were relied upon. It wasreiterated that TDS was not required to be deducted as the payment towards the said expenses were

made to non-resident parties for services rendered outside India which were exempt from tax u/s 9 ofthe Income Tax Act, 1961 as well as under the relevant DTAA with the respective countries. Regarding

freight and cartage on purchases it was submitted that the purchase was generally made on CFR basiswhich include cost and transportation freight which is paid directly by the supplier except from supplier

from Egypt who only supply on FOB basis, requiring the freight to be paid by the buyer. It wassubmitted that the price which the assessee charges from its customers includes freight (CFR basis) but

this is not separately shown in the bills raised for sales made to the foreign buyers. It was also submittedthat all transactions under review are based on shipments on high seas that is from country of origin (not

India) to the overseas customer. As such no freight was paid to any shipping agent in India. Accordinglysince the assessee had purchased goods outside India which were sent directly which too were outside

India as would be evident from the sale and purchase invoices the details of which were also filed beforethe AO while explaining the commission paid to the foreign parties. The reliance placed upon circular

no-7 dated 22.10.2009 by the AO, it was submitted was not relevant as the circular no-786 was reliedupon by the assessee. It was also submitted that the payments of freight and inspection charges had notbeen doubted by the AO and even considering the Board's Circulation No-7 dated 22.10.2009 which

came into force from 22.10.2009 was not even relevant on account of the specific facts of the presentcase. Reliance was placed upon the following judgements :—

"(i) ACIT v. M/s P.P. Overseas IT Appeal No.-733 (Mum) of 2010 dated 18.02.2011;

(ii) Chandrakant Thackar v. Asstt. CIT [2011] 45 SOT 13;

(iii) R.R. Caryying Cor. v. Asstt. CIT [2009] 126 TTJ 240 (Ctk);

(iv) ITO v Freight Systems (India) (P.) Ltd [2006] 6 SOT 473 (Delhi);

(v) Dy. CIT v. Divi's Laboratories Ltd .[2011] 12 taxmann.com 103/131 ITD 271 (Hyd.)."

8. Considering these submissions the CIT(A) deleted the addition made as a result of a disallowance

holding as under :—

"6.3 I have carefully considered the submissions made by the Ld. AR and have gone through the

assessment order. I have also considered the remand report submitted by the AO, writtensubmissions of the appellant company, and the rejoinder on the above ground. No comments are

given by the AO in the remand report on these issues. It is observed from the Assessment orderpassed that the expenses incurred and paid are not disputed by the AO. The only reason to make

disallowance is non deduction of tax by the appellant company on these payments made asaccording to the AO is that he found that the services in this case were rendered in India and the

assessee exported about 40% goods from India & freight and cartage was paid for these services.Whereas, appellant claims that no goods were exported from India, and no freight or inspection

charges were paid for any services rendered in India by the above companies to whom appellantcompany has made the payment. Thus, the only issue to be examined is as to whether any expense

is claimed by the appellant under the head freight and cartage to these persons for the servicesrendered in India or the services were rendered by these companies outside India, on which

provisions of section 194C are not applicable.

The Appellant company has furnished details of Freight charges paid to M/s. APM Global

Logistics Egypt Ltd., and M/s. Al Nasr Co. for Coke & Chem. The Inspection charges amountingto Rs.28,500/- are paid to M/s. Egyptian Chemical Industries. As per Circular No. 786 dated

7.2.2000, no tax was to be deducted where the non-resident agent operates outside the country,and no part of his income arises in India. Further, since the payment is usually remitted directly

abroad it cannot be held to have been received by or on behalf of the agent in India. Suchpayments were therefore, held to be not taxable in India. In the present appeal, appellant company

has submitted copies of all the invoices of the freight paid which is in respect of ocean freight paidto M/s. APM Global Logistics Egypt Ltd., for Alexandria to Jakarta, and none of the payment is

made for any freight which can be said to have incurred for freight paid in India. Appellant has alsoplaced on record the evidences that it has wrongly debited Inspection charges by Freight amount.

In any case neither the freight nor the inspection charges are paid by the appellant company for anyservices rendered by these company in India, and nor the payments are made to these parties in

India, and therefore, by no imagination either the provisions of section 194 C or section 195 areapplicable on any of these payments made to these parties by the appellant company. Furthermore,

neither the AO has brought on record as to which freight amount or inspection charges were paidby the appellant company to any Indian party, which is subject to deduction of tax u/s 40(a)(ia). Inview of these observations, the addition made on these findings when no amount of freight is paid in

India, the addition made of Rs.50,95,012/-on account of freight and inspection charges is deleted."

9. Aggrieved by this the Revenue is in appeal before the Tribunal. The Ld. Sr. DR placed reliance uponthe assessment order. However the findings on facts were not assailed by leading any cogent evidence

nor the evidence taken into consideration by the CIT(A) and the judgements relied upon were assailed.The Ld. AR on the other hand in the absence of any serious arguments on behalf of the Revenue placed

reliance upon the impugned order however it was his submission that in case the Sr. DR wants toseriously contest the issue then he is ready to argue at length addressing the evidence which have been

considered as admittedly the facts are undisputed that the purchase and sale due to the services of thespecific parties were made at high seas as such no agent in India was paid consequently for the

payments made to companies/parties situated in different countries having no presence in India, theoccasion to deduct TDS does not arise.

10. We have heard the rival submissions the perused the material available on record. On aconsideration of the facts and circumstances and position of law which we have referred to at length in

the earlier part of this order, we find no infirmity in the impugned order. Being satisfied with the reasoningand finding arrived at therein, the departmental ground is dismissed.

11. In the result the appeal of the department is dismissed and the appeal of the assessee is allowed forstatistical purposes.

SUNIL

*In favour of assessee.