Negotiations on Non-Agriculture Market Access (NAMA ... · •Special and Differential Treatment...

32

Negotiations on Non-Agriculture Market Access (NAMA) before and after Nairobi: Opportunities and Challenges for Indonesia Jully P. Tambunan Directorate of Multilateral Cooperation Directorate General of International Trade Cooperation

Transcript of Negotiations on Non-Agriculture Market Access (NAMA ... · •Special and Differential Treatment...

Negotiations on Non-Agriculture Market Access (NAMA) before and

after Nairobi: Opportunities and Challenges for Indonesia

Jully P. TambunanDirectorate of Multilateral Cooperation

Directorate General of International Trade Cooperation

Key Presentation Points

• Introduction to NAMA in the WTO

• NAMA negotiations in DDA: key Issues

• Progress made in NAMA negotiations prior to Nairobi

• Key Positions and Differences on NAMA of major WTO members/groups

• What happened in Nairobi on NAMA

• Opportunities and Challenges for Indonesia

(1) Introduction to NAMA in the WTO

4

INTERNATIONAL TRADE AND GROWTH

• Trade becomes an engine of economic

growth for any countries

• For Indonesia, trade is also very important

as an engine of economic growth.

• In the 1980’s, Indonesia issued its export

development policies (Tambunan 2005).

• International trade supports countries to

focus on special production that has

comparative advantages

History of the WTO

• During the multilateral trade negotiations of the Uruguay Round, It wasagreed to set up the World Trade Organization (WTO) on 1 January 1995.

• Since 1 January 1995, multilateral trade negotiations were organized bythe WTO. The scope of the negotiations cover goods, services and IPR.

• Indonesia was an original member of the WTO (now total 164

members); Indonesia has ratified the agreement of WTO in the

Law number (UU) No. 7/1994 (2 November 1994) re Ratification ofthe WTO.

• Main task of WTO is to support free trade, to eliminate and erase thetrade barrier (tariff and non tariff); provide international negotiationforum; solve trade disputes and conduct trade policy reviews amongmember countries.

Three Pillar of the world economy

Based on the three pillars of the “Bretton Woods” system:

• IMF (International Monetary Fund) the year 1946;

• IBRD (International Bank for Reconstruction andDevelopment)/World Bank the year 1945;

• ITO (International Trade Organization) failed due to therejection of the US Congress but GATT survived.– GATT (General Agreement on Tariff and Trade) in 1947 World

Trade Organization/ WTO in 1995.

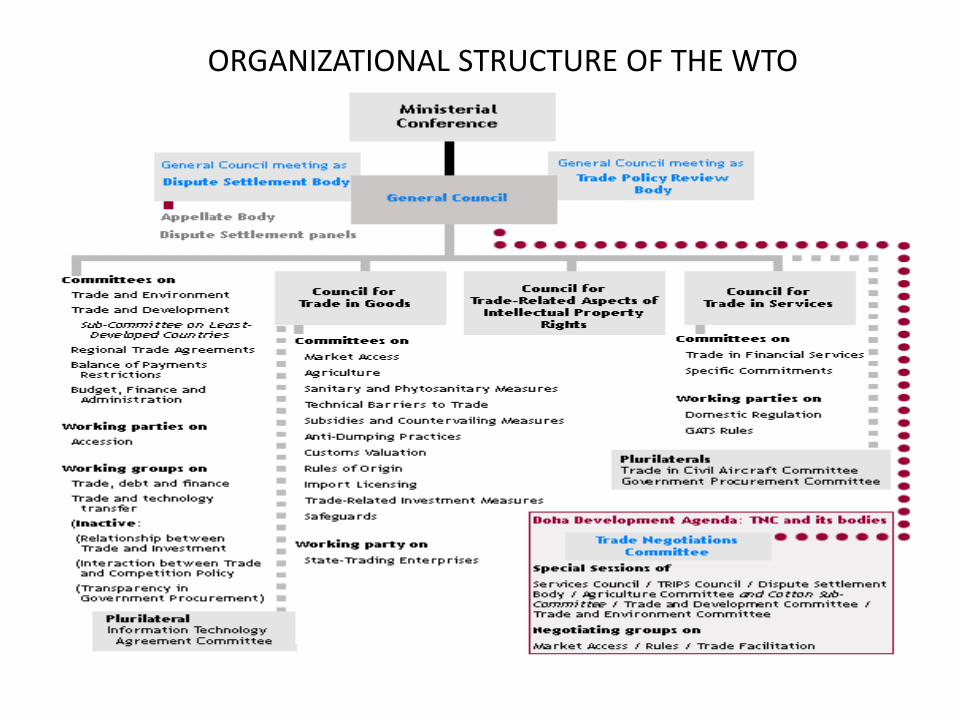

ORGANIZATIONAL STRUCTURE OF THE WTO

8

Base Principal of the MULTILATERAL

TRADING SYSTIM

• Non-discrimination MFN Most Favoured Nation : non discrimantion

among WTO member countries

National Treatment: non discrimination among

imported products and domestic product.

• Transparency:

TPRM: Review on trade policies of the WTO

member coutries on a regular basis

Notifications: submit rules and policies of the

trade of WTO member countries.

9

The basic principles of multilateral trading

system

• Reduce trade barriers (tariff and non-tariff)

To create trade with more open and predictable

• Special and Differential Treatment

Allowing the members of developing countries to

adjust, the flexibility and other treatments

• Tariff Protection to protect with tariffmechanism only;

• ReciprocityApart from the above, trade policy issues that are

developed can create more competitive because it

eliminates unfair trade practices. Furthermore, trade

systems which are developed by WTO can be more

competitive becaus it reduces tariffs.

More competitive because it reduces unfair trade practices

such as dumping and subsidy

NAMA negotiations in DDA: key Issues

11

Doha Mandate on NAMA:

“…reduce or as appropriate eliminate tariffs, including reduction or elimination of tariff peaks, high tariffs & tariff escalation, as well as NTBs, in particular on products of export interest to developing countries”

“… take fully into account the special needs & interests of developing & least-developed country participants, including through less than full reciprocity in reduction commitments”

the overarching principle remains: development

Progress Made in NAMA Negotiations prior to Nairobi

13

Selected Members

Binding Coverage

Average Applied

Tariff

Average Bound Tariff

Swiss Ave. Bound Tariff

Coe 8 Coe 20 Coe 22 Coe 25

US 100 3.1 3.3 2.34

EU 100 4.2 3.9 2.62

Brazil 100 14.1 30.8 12.13 12.83 13.80

China 100 9.1 9.0 6.21 6.39 6.62

Costa Rica 100 4.6 43.1 13.66 14.57 15.82

Egypt 99.2 9.3 27.5 11.58 12.22 13.10

India 70.5 10.2 34.6 12.67 13.45 14.51

Malaysia 81.9 5.5 14.9 8.54 8.88 9.34

Nigeria 7.0 11.1 49.2 14.22 15.20 16.58

Thailand 71.3 8.3 25.4 11.19 11.79 12.60

Indonesia 96.1 6.7 35.6 12.81 13.60 14.69

Source: unknown

• Instrumen Modalitas NAMA

a) Tariff ReductionSimple Swiss Formula

b) Special and Differencial Treatment (S&D)Azas perlakuan khusus yang berbeda bagi Negara Berkembang (NB) dibandingkan NegaraMaju (NM) dalam implementasi modalitas NAMA.

Draft Text NAMA Modalitas – Fourth Revision, Dec 6th, 2008

MODALITAS NAMA WTO

• Swiss Simple Formula : (untuk Negara Berkembang)

koefisien (b) x t0 (tarif awal)t1 (tarif akhir) = ---------------------------------

koefisien (b) + t0 (tarif awal)

where,t1 = Final bound rate of dutyt0 = Base rate of duty x = 20, y = 22, z = 25 (to be chosen) = Coefficients for Developing Members.

8 =Coefficient for Develop Members

Koefisien Formula Untuk

NB

Fleksibilitas: Opsi 1(Pemotongan Tarif separuh dari

pemotongan tarif dengan formula)

Fleksibilitas: Opsi 2(Tidak dikenakan formula

atau “post tarif unbound”)

Jumlah Post Tarif (%)

Nilai Impor Maks (%)

Jumlah Post Tarif (%)

Nilai Impor Maks (%)

Opsi X: 20 14% 16% 6,5% 7,5%

Opsi Y: 22 10% 10% 5% 5%

Opsi Z: 25 0 0 0 0

MODALITAS NAMA WTO

• Coefficient and Flexibilities for Developing Members

(1) Current position:• Average bound tariff : 36.79%• Number of Post Tariff Unbound : 443 • Number of total tariff line (2003) : 6446

(2) Application of Swiss formula:

No DescriptionCoefficient:

Flex. for Un-Bound:

Coefficient opt.; Flexibility

X Y Z

20 22 25

6,5% 5% 0

abcdef

New average bound tariff (%)Average discounted per bound tariff (%)Average Applied Tariff (2003) (%)New average Applied Tariff (2003) (%)Average discounted per Applied Tariff (%)Post Tariff which are discounted to get avg new bound tariff:- Number of (%) post Tarif (2003)- Number of Post Tarif

12,8665,067,036,606,19

15,45997

13,6662,877,036,724,44

15,45997

14,7759,857,036,872,32

9,83634

g -Number Unbound Tariff which have to be bounded-Number of tariff which are remain unbound (443-419)=

24419

120323

4430

Source: Tariff Schedule Indonesia (HS 2002); WTO Sekretariat (Tariff Simulation)Note : 1. Simulation is not including Unbound tariff; 2.Total of Tariff Unbound : 6,87%; 3. Aplied Tariff average of 2010 : 6,7%

MODALITAS NAMA WTO

2. Simulasi Pengurangan Tarif NAMA (Simple Swiss Formula)

17

0

5

10

15

20

25

30

35

40

Can

ada

EC-1

5

Jap

an

USA

Ch

ina,

PR

Ho

ng

Kon

g…

Ind

one

sia

Kor

ea

Mal

aysi

a (*

)

Phi

lippi

nes

Sin

gap

ore

Thai

land

Arg

ent

ina

Bra

zil

Ch

ile

Ind

ia

Me

xico

Sou

th A

fric

a

AV

G (%

)

AVG Final Bound

AVG MFN Applied

(*) Binding coverage could be overestimated due to partial bindings; Courtesy of South Center

Results of Uruguay Round: Bound vs Applied Rates

18

What on the table? 2008 Draft Modality Rev.3. Some consider it toocomplex & needs simplification (Argentina’s non-paper)

HK Declaration: “ We adopt a Swiss Formula with coefficients….” appliedon a line-by-line basis:

{a or (x or y or z)} x t0

t1 = ___________________________ where{a or (x or y or z)} + t0

t1 = Final bound rate of dutyt0 = Base rate of duty a = 8 = Coefficient for developed Membersx = 20, y = 22, z = 25 Coefficients for developing Members.

Other issues to address: anti-concentration, preference erosion, tariff peaks, high tariffs, tariff escalation, NTBs, sectoral initiatives (14), DFQF,remanufactured goods, environmental goods, different tariff structures

The Ministry of Trade of the Republic of Indonesia

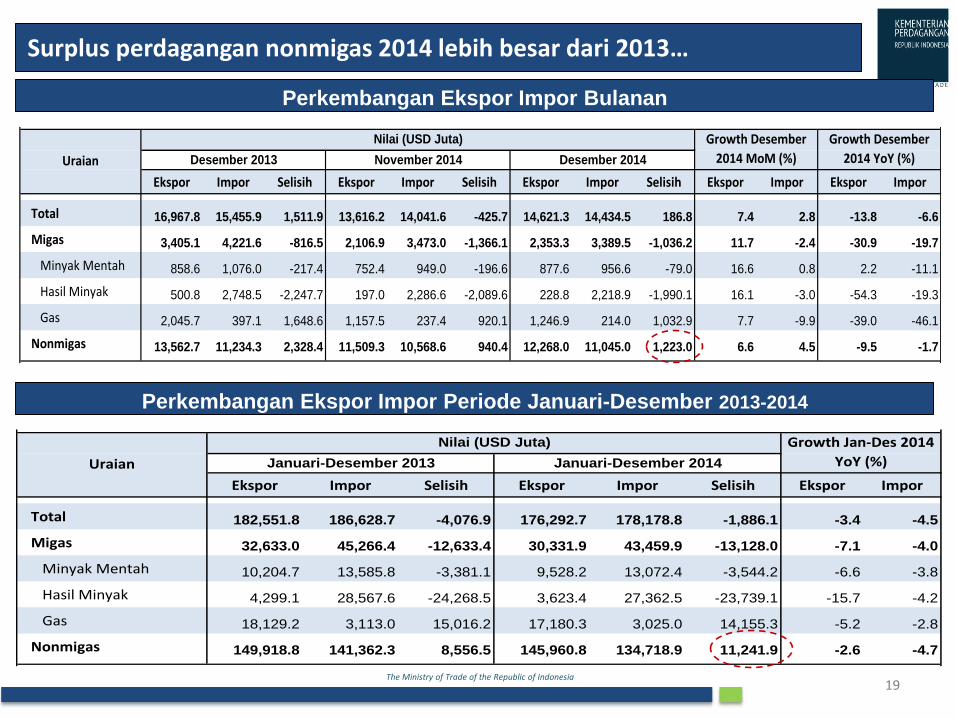

Ekspor Impor Selisih Ekspor Impor Selisih Ekspor Impor

Total 182,551.8 186,628.7 -4,076.9 176,292.7 178,178.8 -1,886.1 -3.4 -4.5

Migas 32,633.0 45,266.4 -12,633.4 30,331.9 43,459.9 -13,128.0 -7.1 -4.0

Minyak Mentah 10,204.7 13,585.8 -3,381.1 9,528.2 13,072.4 -3,544.2 -6.6 -3.8

Hasil Minyak 4,299.1 28,567.6 -24,268.5 3,623.4 27,362.5 -23,739.1 -15.7 -4.2

Gas 18,129.2 3,113.0 15,016.2 17,180.3 3,025.0 14,155.3 -5.2 -2.8

Nonmigas 149,918.8 141,362.3 8,556.5 145,960.8 134,718.9 11,241.9 -2.6 -4.7

Uraian

Growth Jan-Des 2014

YoY (%)Januari-Desember 2014Januari-Desember 2013

Nilai (USD Juta)

Ekspor Impor Selisih Ekspor Impor Selisih Ekspor Impor Selisih Ekspor Impor Ekspor Impor

Total 16,967.8 15,455.9 1,511.9 13,616.2 14,041.6 -425.7 14,621.3 14,434.5 186.8 7.4 2.8 -13.8 -6.6

Migas 3,405.1 4,221.6 -816.5 2,106.9 3,473.0 -1,366.1 2,353.3 3,389.5 -1,036.2 11.7 -2.4 -30.9 -19.7

Minyak Mentah 858.6 1,076.0 -217.4 752.4 949.0 -196.6 877.6 956.6 -79.0 16.6 0.8 2.2 -11.1

Hasil Minyak 500.8 2,748.5 -2,247.7 197.0 2,286.6 -2,089.6 228.8 2,218.9 -1,990.1 16.1 -3.0 -54.3 -19.3

Gas 2,045.7 397.1 1,648.6 1,157.5 237.4 920.1 1,246.9 214.0 1,032.9 7.7 -9.9 -39.0 -46.1

Nonmigas 13,562.7 11,234.3 2,328.4 11,509.3 10,568.6 940.4 12,268.0 11,045.0 1,223.0 6.6 4.5 -9.5 -1.713732.36 11210.40 13732.36 11210.40

Uraian

Growth Desember

2014 YoY (%)November 2014 Desember 2014

Growth Desember

2014 MoM (%)Desember 2013

Nilai (USD Juta)

Surplus perdagangan nonmigas 2014 lebih besar dari 2013…

19

Perkembangan Ekspor Impor Bulanan

Perkembangan Ekspor Impor Periode Januari-Desember 2013-2014

Key Positions and Differences on NAMA of major WTO members/groups

21

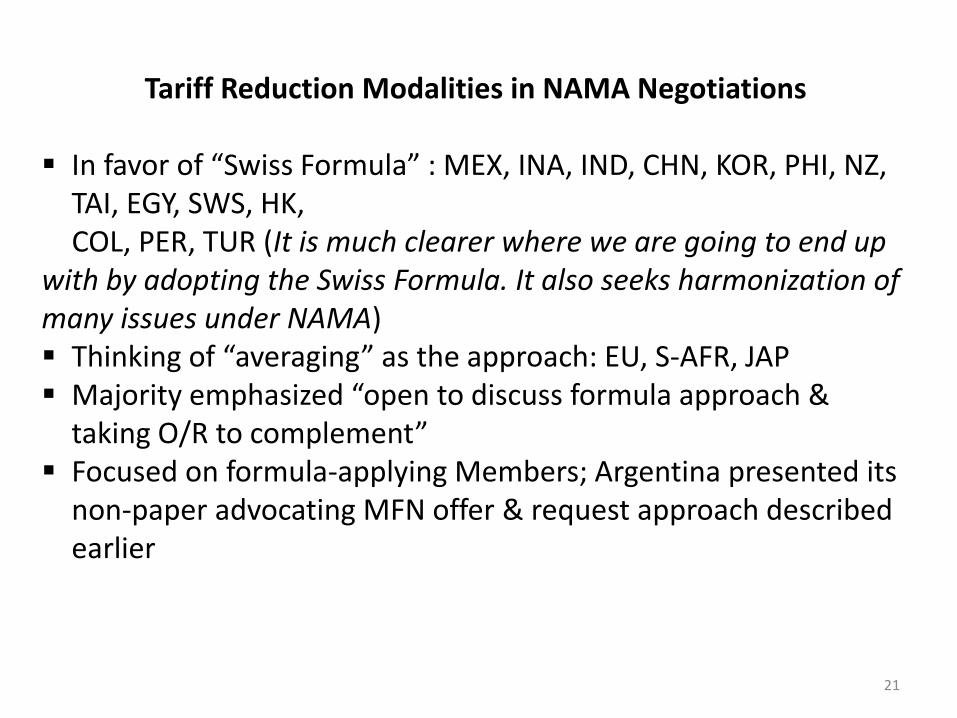

Tariff Reduction Modalities in NAMA Negotiations

In favor of “Swiss Formula” : MEX, INA, IND, CHN, KOR, PHI, NZ, TAI, EGY, SWS, HK, COL, PER, TUR (It is much clearer where we are going to end up

with by adopting the Swiss Formula. It also seeks harmonization of many issues under NAMA) Thinking of “averaging” as the approach: EU, S-AFR, JAP Majority emphasized “open to discuss formula approach &

taking O/R to complement” Focused on formula-applying Members; Argentina presented its

non-paper advocating MFN offer & request approach described earlier

22

Argentina Non-Paper (3 February 2015) referred to Bali Declaration on Post-Bali Work Program: “… including the need to look at ways that may allow Members to overcome the most critical and fundamental stumbling blocks”

“MFN Treatment Requests & Offers Negotiating Procedures to help building and keeping an ongoing balance country by country negotiation with demand driven results. In such approach no specific defensive tools will be needed”

“Members shall submit bilaterally at their own initiative requests and offers to other members and engage in negotiations with those members in a limited timeframe to be agreed upon”

“There would be the following types of requests: (i) removal of tariffs, charges & other duties on products concerned; (ii) reduction of tariffs, charges & other duties on products concerned; (iii) the binding of unbound products (if applicable); (iv) creation of a TRQ of volume expansion of an existing TRQ”

23

Cautions & recommendations from the South Center:

“Swiss Formula” leads to deeper cuts for developing countries Bind only the average tariff, not line-by-line Stop protecting declining industries & cut tariff unilaterally Consider time-bound agreements

RI might also:

Focus on increasing the binding coverage of as other countries: HK, Korea, Malaysia, Philippines, Singapore, Thailand,India levelling the playing field for RI with major competitors

What happened in Nairobi on NAMA

Information Technology Agreement

• The Information Technology Agreement (ITA) is a plurilateral tradeagreement that requires participants to eliminate their tariffs on aspecific list of information technology (IT) and telecommunicationsproducts. The agreement covers approximately 97 percent of worldtrade in defined IT products, which is currently estimated to exceed $1trillion.

• The ITA is a tariff-cutting agreement focused on trade in informationtechnology goods, and does not include services or software; the agreementdoes contain a commitment to address non-tariff barriers, but withoutspecifics.

• It is subject to a "free rider" problem since all WTO members would benefitwhen the expanded agreement is concluded. Under WTO most-favored nationprinciples, the non-participating WTO members are able to benefit from theconcessions made by other countries while maintaining their own tariffs.

• In order to minimize the free rider problem, the ITA requires a threshold 90% ofglobal trade coverage to come into force. There are currently 81 participants inthe original ITA, including the United States, the 28 members of the EuropeanUnion (EU), and key East Asian trading partners Japan, South Korea, China andTaiwan

ITA countinue ...

• Products covered under the ITA include computer hardware andperipherals, telecommunications equipment, computer software,semiconductor manufacturing equipment, analytical instruments,and semiconductors and other electronic components. The chartbelow gives examples of the products in the ITA.

• The Ministerial Declaration on Trade in Information TechnologyProducts (ITA) was concluded by 29 participants at the SingaporeMinisterial Conference in December 1996.

• The number of participants has grown to 81, representing about 97per cent of world trade in information technology products. The ITAprovides for participants to completely eliminate duties on ITproducts covered by the Agreement. Indonesia is a member of ITA.

• After 17 rounds of negotiations, at a meeting on 24 July 2015, nearlyall the participants agreed to expand the products covered by theAgreement and eliminate tariffs on an additional list of 201 products– Information Technology Agreement 2 – ITA2

ITA2 Negotiations In Nairobi

• Negotiations on the expanded ITA were conducted by 53WTO members, including both developed and developingcountries, which account for approximately 90 per cent ofworld trade in these products.

• All WTO members will benefit from the agreement, asthey will all enjoy duty-free market access to the marketsof the members eliminating tariffs on these products.

• For every product on the list, ITA2 participants havenegotiated the level of reductions and over how manyyears it will fully eliminate the tariffs. As a result of thesenegotiations, approximately 65% of tariff lines will be fullyeliminated by 1 July 2016. Most of the remaining tarifflines will be completely phased out in four stages overthree years. This means that by 2019, almost all importsof the relevant products will be duty free.

• Indonesia has not yet decided to join the ITA2.

Opportunities and Challenges for Indonesia

Indonesia, 597.912

AS, 11.301.656

Korea, 614.776

India, 1.202.762

Cina, 3.127.233

EU, 11.791.878

Brasil, 121.238

Jepang, 5.376.9150%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-10,000 0 10,000 20,000 30,000 40,000 50,000 60,000

Ra

ta-r

ata

Ta

rif

Be

a M

asu

k

PDB per Kapita

Tariff MFN Product Non-Agriculture (2010)

Sumber : WTO, 2010, diolah Kemenperin

NON-AGRICULTURE

Country GDP/capAverage Tariff

Line

GDP (billion) /

2010

1 EU 32.700,00 4,00% 11.791.878

2 AS 46.860,24 3,30% 11.301.656

3 Japan 42.782,52 2,50% 5.376.915

4 China 4.382,13 8,70% 3.127.233

5 Brazil 10.816,48 14,20% 1.530.110

6 India 1.371 10,10% 1.202.762

7 Korea 20.756,24 6,60% 614.776

8 Indonesia 2.974,02 6,60% 597.912

29

Challenges for Indonesian Manufactures

Daya Saing Global

A. TANTANGAN GLOBALISASI BAGI INDUSTRI MANUFAKTUR

The Global Competitiveness index 2014-2015 rankings and 2013-2014 comparisons

Ranking tertinggi diduduki oleh negara barat yang maju dan tiga macan asia.

Posisi Indonesia lebih rendah dari Singapura, Jepang, N.Zealand, Malaysia, Korea dan China. Namun posisi Indonesia lebih baik dari Brazil, Turkey, Mexico, India dan Russia. Ranking Idonesia meningkat 4 point dibandingkan dengan tahun sebelumnya.

Source: Global Competitiveness Report 2014-2015,World Economic Forum

Competitiveness Industrial Performance Index

----- ASEAN FTA Dialog Partners -----

----- ASEAN -----

Source: Competitiveness Industrial Performance Report, 2012/2013,UNIDO

Daya Saing Industri Manufaktur

A. TANTANGAN GLOBALISASI BAGI INDUSTRI MANUFAKTUR

CONCLUSIONS