NCAC/CSIS Energy Policy Conference US Tight Oil in a Global Context

11

Powerful Thinking for the global energy industry NCAC/CSIS Energy Policy Conference US Tight Oil in a Global Context Presented by Ivan Sandrea President, Energy Intelligence Group April 3rd, 2012

Transcript of NCAC/CSIS Energy Policy Conference US Tight Oil in a Global Context

Powerful Thinking for the global energy industry

NCAC/CSIS Energy Policy Conference

US Tight Oil in a Global Context

Presented by Ivan Sandrea

President, Energy Intelligence Group

April 3rd, 2012

NCAC/CSIS : Tight Oil Conference 2

Strategic Trends: US Light -Tight Oil in a Global Context

Key recent high-impact events; US home to many!

Shale Gas

Light - Tight Oil

Macondo

The Great Recession

OECD/non-OECD Gap

Fukushima

US ME Policy Post Iraq

ME Turmoil

Pre-salt

Global Energy & Policy Reforms

Global R&M Restructuring

Increases in Global YTF

Source: Energy Intelligence

NCAC/CSIS : Tight Oil Conference 3

Global Oil Supply Increases

US major contributor to global expansion, 2008-11

Source: Energy Intelligence – OMI

0 200 400 600 800 1,000 1,200 1,400

Ghana

India

Oman

Kazakhstan

Qatar

Canada

China

Colombia

Nigeria

Brazil

Saudi Arabia

Iraq

Russia

US Light, Tight

US

kbpd

NCAC/CSIS : Tight Oil Conference 4

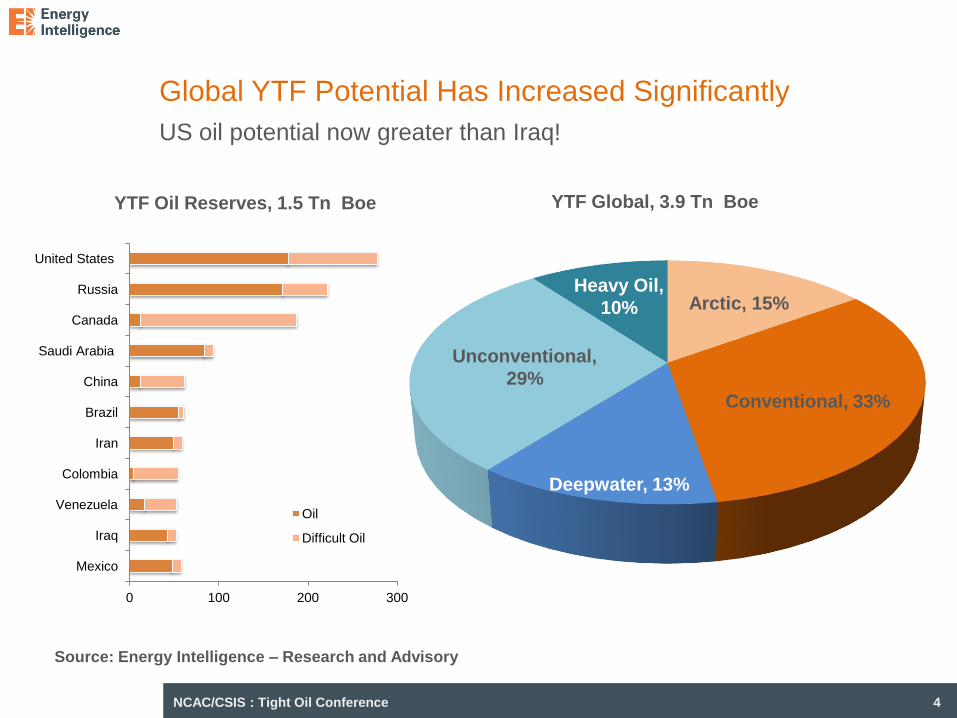

Global YTF Potential Has Increased Significantly

US oil potential now greater than Iraq!

YTF Global, 3.9 Tn Boe

Conventional, 33%

Arctic, 15% Heavy Oil,

10%

Deepwater, 13%

Unconventional,

29%

Source: Energy Intelligence – Research and Advisory

YTF Oil Reserves, 1.5 Tn Boe

0 100 200 300

Mexico

Iraq

Venezuela

Colombia

Iran

Brazil

China

Saudi Arabia

Canada

Russia

United States

Oil

Difficult Oil

NCAC/CSIS : Tight Oil Conference 5

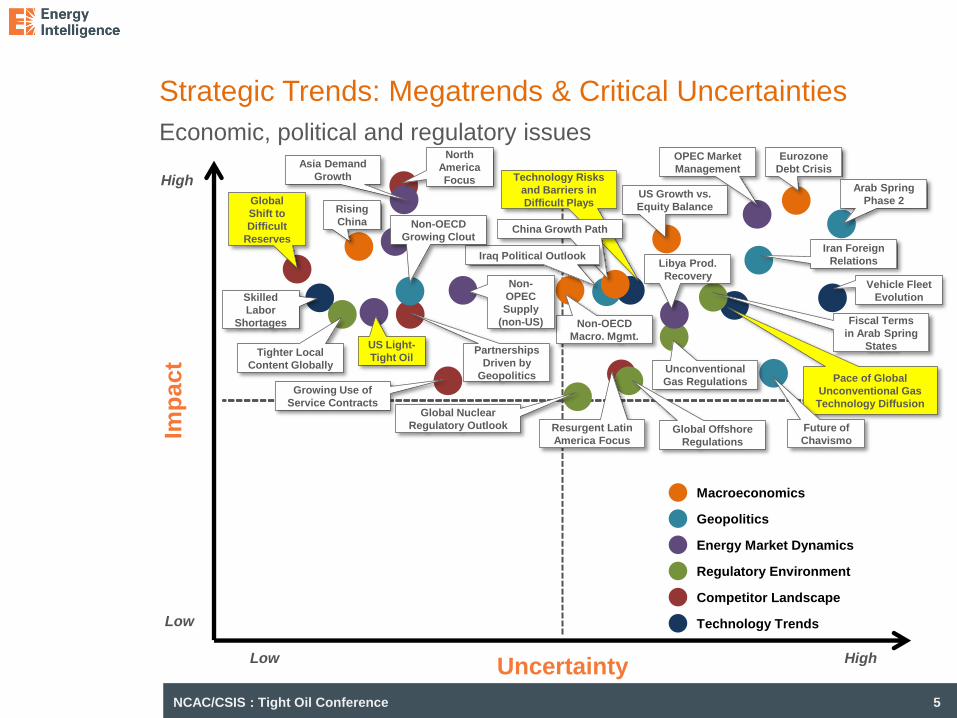

Strategic Trends: Megatrends & Critical Uncertainties

Economic, political and regulatory issues

Imp

act

Low High

High

Low

Uncertainty

Macroeconomics

Geopolitics

Energy Market Dynamics

Regulatory Environment

Technology Trends

Competitor Landscape

Eurozone

Debt Crisis

Arab Spring

Phase 2

OPEC Market

Management

US Growth vs.

Equity Balance

Iran Foreign

Relations

Vehicle Fleet

Evolution

Fiscal Terms

in Arab Spring

States

Libya Prod.

Recovery

Pace of Global

Unconventional Gas

Technology Diffusion

Future of

Chavismo

Resurgent Latin

America Focus

Growing Use of

Service Contracts

Technology Risks

and Barriers in

Difficult Plays

China Growth Path

Iraq Political Outlook

Unconventional

Gas Regulations

Global Offshore

Regulations

North

America

Focus

Rising

China

Asia Demand

Growth

Tighter Local

Content Globally

Global

Shift to

Difficult

Reserves

Non-OECD

Macro. Mgmt.

Non-

OPEC

Supply

(non-US)

Partnerships

Driven by

Geopolitics

US Light-

Tight Oil

Skilled

Labor

Shortages

Global Nuclear

Regulatory Outlook

Non-OECD

Growing Clout

NCAC/CSIS : Tight Oil Conference 6

Extending the New Boom Beyond the US

Key uncertainties remain in other regions with similar potential

Imp

act

Low High

High

Low

Uncertainty

Macroeconomics

Geopolitics

Energy Market Dynamics

Regulatory Environment

Technology Trends

Competitor Landscape

US Unconv.

Gas Boom

Europe UCG

Development

China UCG

Development

Argentina UCG

Development

Unconventional Gas: While the US

gas boom is a Megatrend,

unconventional gas development in

other high potential areas remains a

Critical Uncertainty.

US Light - Tight Oil: Production

boom supported by oil-gas price

gap, improving economics,

technology, lack of opportunities.

How many Bakken are out there?

Argentina

Tight Oil

Development

US Tight Oil

Boom

Poland UCG

NCAC/CSIS : Tight Oil Conference 7

Global Unconventional Oil M&A

Concentrated in North America

‒ Among global M&A transactions in 2011, unconventional oil represented only 8% of deals

‒ The bulk of these deals were concentrated in North America, with a handful of deals in Latin America, Asia and Europe

1086

318

4

8

0

156

278

0 200 400 600 800 1000 1200

Conventional

Deepwater

Pre-Salt

Arctic

EOR

Unconventional Oil

Unconventional Gas

M&A Transactions by Play Type (2011)

Number of

transactions

Unconventional Oil = Oil Sands, Shale Oil, Oil Shale, Heavy Oil

3 2 0 7 2

141

1 0

20

40

60

80

100

120

140

160

ASIA EUR FSU LAC MENA NAM SSA

Unconventional M&A Transactions, by Region (2011) Number of

transactions

Value:

$10,185 mn

Source: Derrick Petroleum, EI

NCAC/CSIS : Tight Oil Conference 8

Major Energy Markets: Current Reforms & Policy Shifts

Primary impact of policies being pursued; US one amongst many

Source: Energy Intelligence – Research and Advisory

KSA

Iran

Russia

USA

Germany

Demand

Argentina

Mexico

Japan

Angola

China

Supply

Iraq

Brazil

Colombia

Canada

Norway

Both

NCAC/CSIS : Tight Oil Conference 9

US Tight Oil - Unconventional Thinking

Distinguishing between hype and reality

• Hype: Game-changing reserve additions in the US …and globally?

• Reality: Complex relationship of resource type and local conditions drive production

Supplies and Technology

• Hype: Boom in US light-tight oil provides windfall for US motorists

• Reality: Market distortions prevail because of mismatch between production and refinery requirements; US petrol prices still exposed to international events!

Market Impact

• Hype: The source of a second American Industrial Revolution

• Reality: While a prop for steel and petrochemicals, longer-term health dependent upon broader trends in the macroeconomy, relative competitive factors

Economic Impact

• Hype: US Energy Independence

• Reality: Does not eliminate interests in Middle East, but will reinforce “pivot” toward Asia; birth of US petro communities

International Political Impact

NCAC/CSIS : Tight Oil Conference 10

What is Happening? What is Next?

EI News Cloud

The Americas

5 East 37th Street, 5th Floor

New York, NY 10016-2807

Tel: 1 212 532 1112

Fax: 1 212 532 4479

1411 K Street, NW, Suite 602

Washington DC 20005-3404

Tel: 1 202 662 0700

Fax: 1 202 783 8230

808 Travis Street, Suite 1014

Houston, TX 77002

Tel: 1 713 222 9700

Fax: 1 713 222 2948

Europe & Africa

Interpark House

7 Down Street, 3rd Floor

London W1J 7AJ, UK

Tel: 44 (0)20 7518 2200

Fax: 44 (0)20 7518 2201

72/4 Leningradsky Pspt, #407

125315, Moscow, Russia

Tel: 7 495 721 1611

Fax: 7 495 721 1614

www.energyintel.com

Middle East & Asia-Pacific

15 A Temple Street, #02-01

Singapore 058562

Tel: 65 6538 0363

Fax: 65 6538 0368

Dubai Media City

Al Thuraya Tower 2 - 1907

P.O Box 71338

Dubai - UAE

Tel: 97 14 364 2607

Fax: 97 14 369 7500

Thank You

www.energyintel.com