NAYARA ENERGY LIMITED€¦ · Essar Oil Trading Mauritius Ltd Nayara Energy Ltd Vadinar Oil...

32

NAYARA ENERGY LIMITED Corporate Presentation September 2018 1

Transcript of NAYARA ENERGY LIMITED€¦ · Essar Oil Trading Mauritius Ltd Nayara Energy Ltd Vadinar Oil...

NAYARA ENERGY LIMITED

Corporate Presentation

September 2018

1

2

Legal Disclaimer

NOT FOR PUBLICATION OR DISTRIBUTION, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES

This presentation and the information contained herein are not an offer of the securities for sale in the United States and are not for publication or distribution to persons in the United States. The presentation is being made to you on the

basis that you have confirmed you are not located or resident in the United States. No securities have been, nor will they be, registered under the US Securities Act of 1933 (the “US Securities Act”) or the securities laws of any state or

other jurisdiction of the United States. No securities may be offered or sold in the United States unless those securities have been registered under the US Securities Act or are offered or sold pursuant to an exemption from, or in a

transaction not subject to, the registration requirements of the US Securities Act and applicable state securities laws. There will be no public offer of securities in the United States.

THIS PRESENTATION DOES NOT CONSTITUTE OR FORM PART OF AN OFFER OR SOLICITATION OF AN OFFER TO PURCHASE OR SUBSCRIBE FOR ANY SECURITIES AND SHALL NOT FORM THE BASIS OF OR BE

RELIED ON IN CONNECTION WITH ANY CONTRACT OR BINDING COMMITMENT WHATSOEVER.

This presentation is confidential and has been prepared by Nayara Energy Limited (the “Company”) solely for information purposes.

This presentation is the sole responsibility of the Company and has been prepared by the Company based on information and data which the Company considers reliable. The Company does not make any representation or warranty,

express or implied, whatsoever, and no reliance shall be placed on, the truth, accuracy, completeness, fairness and reasonableness of the contents of this presentation, which have not been independently verified. This presentation may

not be all-inclusive and may not contain all of the information that you may consider material. The Company expressly excludes any liability in respect of the contents of, or any omission from, this presentation. Opinions and estimates

constitute the sole judgment of the Company as of the date of this presentation and are subject to change without notice.

This presentation contains statements about future events and expectations that constitute “forward-looking statements.” These forward-looking statements include words or phrases such as the Company or its management “believes”,

“expects”, “anticipates”, “intends”, “plans”, “foresees”, “targets”, “aims”, “may”, “would”, “could” or other words or phrases of similar import. Similarly, statements that describe the Company's objectives, plans or goals are also forward-

looking statements. All such forward-looking statements are subject to known and unknown risks and uncertainties that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement.

Such forward looking statements are made based on management’s current expectations or beliefs as well as assumptions made by, and information currently available to, management. These forward-looking statements speak only as

at the date of this presentation and nothing contained in this presentation is or should be relied upon as a promise or representation as to the future. There is no obligation to update or revise any forward-looking statements, whether as a

result of new information, future events or otherwise. You should not place undue reliance on forward-looking statements, which speak only as of the date of this presentation.

The historical financial information in this presentation was prepared and presented in accordance with International Financial Reporting Standards (“IFRS”) and have not been audited or reviewed by an independent auditor.

Consequently, such financial statements should not be relied upon to provide the same type or quality of information associated with information that has been subject to an audit or review by an independent auditor. None of the

Company nor any of its affiliates, directors or advisors make any representation or warranty, expressed or implied, regarding the accuracy of such consolidated financial statements or their sufficiency for an assessment of the Company.

Caution must be exercised when using such data to evaluate the Company’s financial condition and results of operations.

The historical financial information in this presentation also includes financial information that is not presented in accordance with IFRS. These non-IFRS financial measures are not measures of financial performance in accordance with

IFRS and may exclude items that are significant in understanding and assessing the Company’s financial results. Accordingly, these non-IFRS financial measures may be considered in addition to IFRS financial information, but should not

be considered in isolation or used as substitutes for the corresponding IFRS measures. Non-IFRS measures in this presentation may be calculated in a way that is not comparable to similarly titled measures reported by other companies.

This presentation is being furnished to you solely for your information and may not be reproduced or redistributed to any other person. In particular, this presentation may not be taken or transmitted into the United States, Canada or

Japan or any other jurisdiction where to do so would be illegal or distributed, directly or indirectly, in the United States, Canada or Japan or any other such jurisdiction.

The information contained in this presentation is not to be taken as any recommendation made by the Company or any other person to enter into any agreement with regard to any investment.

By accepting to access any copy of the information presented, you agree to be bound by the foregoing limitations.

Strong parentage and governance framework

Integrated business value chain

Consistent track record of operational excellence

High complexity refinery

Crude sourcing and procurement advantage

Predictable product offtake through downstream presence and strong distribution

Attractive industry dynamics

Experienced management team with proven track record

3

Introduction

Key Highlights

Financial Overview

A

B

D

Near Term Strategic PlansC

Table of Contents

Introduction

4

Evolution and Key Milestones

5

2003 2004 2006 2008 2012 2013 2016 2017 2018

2004

Enters into Corporate

Debt Restructuring

(“CDR”); construction of

refinery recommences

along with captive

power plant and port

2012

EOL completes expansion and

optimisation projects; capacity

increased to 20 MMTPA

Commissioned 510 MWe coal

fired captive power plant

2016

EOL delisted

2006

Vadinar refinery

commences

operations on a

trial basis

2008

Vadinar refinery

commences

commercial

operations with

nameplate

capacity of 10.5

MMTPA

2013

EOL exits CDR loan

facility in March 2013;

improvement in local

credit rating1 by two

notches from BBB- to

BBB+

2018

Name changed to

Nayara Energy Limited

(“Nayara”)

Local credit rating1

upgraded by three

notches to “AA”

2017

Acquisition of VOTL and VPCL

and divestment of E&P assets

Acquisition of 98.26% stake by

Rosneft and Kesani, a

consortium led by Trafigura and

UCP, at an enterprise value of

US$ 12.9bn in August 2017

2003

Essar Oil Limited

(“EOL”) commences

building its network of

franchised retail

petrol stations

Pre-Nayara regime Nayara regime

1 Refers to CARE long term rating

2018

Refinancing of INR

Debt for optimization of

capital structure

Raised INR 2,400cr (c.

US$ 355mn) through its

placement of non-

convertible debentures

2015

2015

Major turnaround

completed;

commissioning of

VGO MHC

Ownership Structure

6

PJSC Rosneft Oil Company

Rosneft Singapore Pte Ltd Minority ShareholdersKesani Enterprises Company

Ltd (Cyprus)

Trafigura Holdings Pte Ltd

UCP PE Investment Ltd

Oil Holdings Ltd1

Vadinar Power Company Ltd2

Nayara Energy Properties Ltd2

Essar Oil Trading Mauritius Ltd

Nayara Energy Ltd

Vadinar Oil Terminal Ltd3

Coviva Energy Terminals Ltd

Enneagon Ltd

1 Previously known as Essar Power Holdings Ltd2 Vadinar Power Company Limited and Nayara Energy Properties Limited are being merged with Nayara Energy Limited; merger application filed 3 Merger of Vadinar Oil Terminal Limited with Nayara Energy Limited being evaluated

49.13%1.74%49.13%

98.00%

75.00%

100.00%

100.00%

100.00%

100.00%

100.00%

25.00%

49.00%

49.00%

2.00%

Company Overview

7

Integrated refinery with dedicated infrastructure and proven track record – well positioned to cater to domestic and international demand

Highly complex

refinery

Captive power

plant

Captive port

with single

point mooring

Strong retail

business chain

• Co-generation power plants with a capacity of

1,010 MWe owned and operated through Vadinar

Power Company Ltd (wholly owned subsidiary)

• Meets captive requirements of steam and power

for the refinery

• 4,473 operational retail stations and 2,688 retail

stations under implementation across India

• Domestic sales account for 57% while exports

account for 43% of FY18 sales

• India's second largest single location refinery –constitutes c. 8% of Indian refinery capacity1

• High complexity index of 11.8, capable of processingultra-heavy, heavy and light crudes across globalmarket

• Strategically located on Indian west coast, proximityto Middle East and high consumption domestic aswell as export markets

• Fully captive port with Single Point Mooring

(Vadinar Oil Terminal Ltd)

• End-to-end infrastructure including storage

facilities, water intake facilities, product jetty and

dispatch facilities by rail, road, port and pipelines

1Source: Ministry of Petroleum and Natural Gas, Government of India - annual report 2017-18

Key Highlights

8

Key Highlights

9

Crude sourcing and procurement advantage

5

High complexity refinery4

Consistent track record of operational excellence3

Predictable product offtake through downstream presence and strong distribution6

Attractive industry dynamics7

Strong parentage and governance framework

1

Experienced management team with proven track record8

Integrated business value chain

2

10

Shareholders

Effective ownership

in Nayara Energy Summary description

49.13%

• World’s largest publicly traded petroleum company - c. 6% of world oil production and a market capitalization of US$69.6bn1

• Ownership structure2: Russian Government - ~50%, BP - 19.75%, QH Oil Investments – 18.93%, Public / others – ~11.32%

• Credit rating: S&P - BB+ (Positive outlook), Moody’s - Baa3 (Stable outlook)

• FY2017 key figures (as at 31 December 2017) 3: Revenue - US$104.3bn, Total Assets - US$212.0bn

24.07%

• One of the leading commodity traders in the world and the largest independent LNG trader4

• Two main lines of business: physical trading and industrial assets portfolio

• FY2017 key figures (as at 30 September 2017): Revenue - US$136.4bn, Total Assets - US$48.6bn4

24.07%

• Independent, private investment group established in 2006

• Focused on investing in high-growth private companies or mature enterprises with proven business model and stable cash-flow

• Total assets under management exceed US$3bn

1. Source: Rosneft website; market cap as of September 19, 2018

2. As of September 18, 2018

3. FX – 1 US$ = 57.68 RUB, as of 31 Dec 2017

4. Source: Trafigura website

1 High Quality and Experienced Shareholders

FY 2017 key figures (as at 31 December 2017)Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

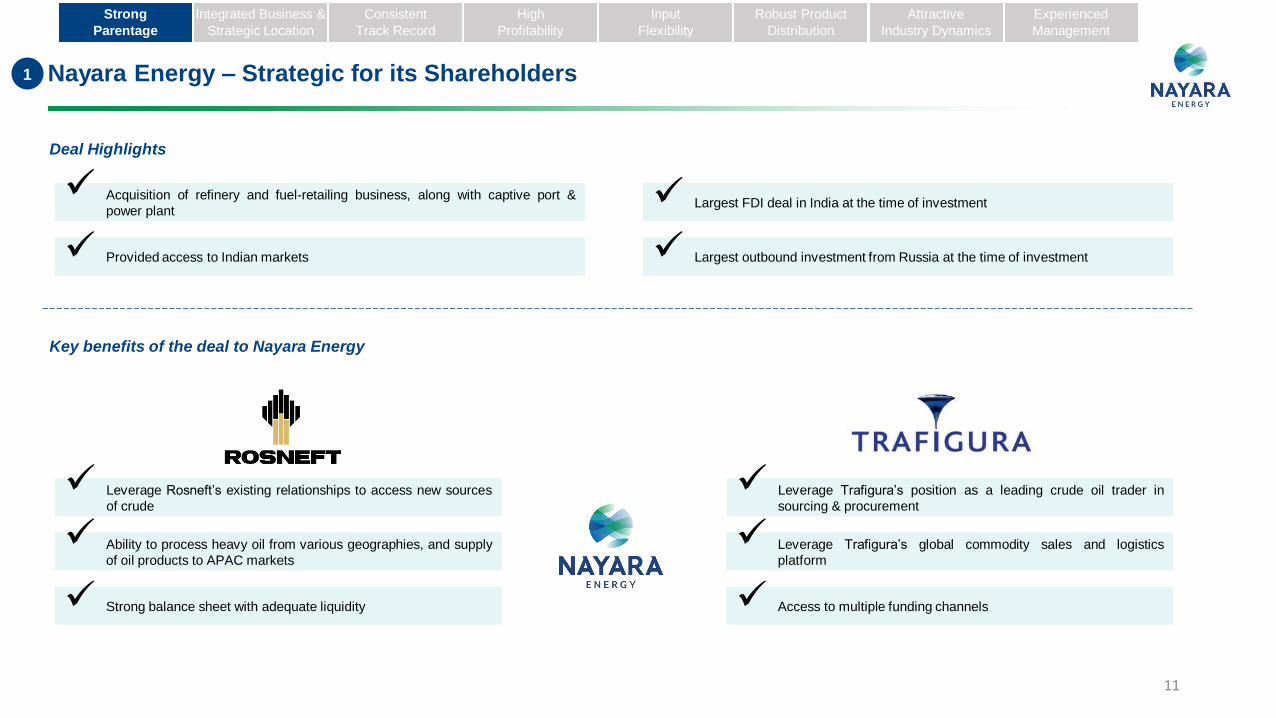

1 Nayara Energy – Strategic for its Shareholders

Leverage Rosneft’s existing relationships to access new sources

of crude

Acquisition of refinery and fuel-retailing business, along with captive port &

power plant

Ability to process heavy oil from various geographies, and supply

of oil products to APAC markets

Provided access to Indian markets

Largest FDI deal in India at the time of investment

Strong balance sheet with adequate liquidity

Leverage Trafigura’s position as a leading crude oil trader in

sourcing & procurement

Leverage Trafigura’s global commodity sales and logistics

platform

Access to multiple funding channels

Key benefits of the deal to Nayara Energy

Deal Highlights

Largest outbound investment from Russia at the time of investment

11

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

12

BoD to have at least 2 independent directors1 No control of any single shareholder4 4 2 2

12

Krzysztof

Zielicki Antoni

Non Executive Director

• Over 37 years of experience in oil and gas

industries; worked with BP

• BSc and MSc, Mathematics

A Balgarnie

Non Executive Director

• Advisor to the CEO of Rosneft Oil Company

• Over 30 years of experience in finance and

natural resources industry

• BA Hons. and Morehead–Cain scholar -

University of North Carolina, Chapel Hill, USA

Didier Casimiro

Non Executive Director

• Held top management position at BP since

1996 and thereafter at TNK-BP since 2005

• Over 25 years of experience

• Rosneft board member since June 2012

• Graduated - Ghent University, Belgium

Alexander Romanov

Non Executive Director

• Vice President for Refining & Petrochemicals in

Rosneft Oil Company

• Over 21 years of experience in oil and gas

companies in refining and petrochemical

• Degree in Chemical Engineering, Economics

Chin Hwee Tan

Non Executive Director

• Director and Head of Asia Pacific in Trafigura

• Over 23 years of experience

• CFA, CA (Australia and Singapore) with

Masters’ degree - Yale University, Post

Graduate - Harvard University

Jonathan Kollek

Non Executive Director

• President of Trafigura Eurasia LLC

• Over 35 years of experience in oil industry

• B.Sc., Economics and International Relations

E Sapozhnikova

Non Executive Director

• Partner at United Capital Partners

• Over 18 years of experience

• LLM - New York University, Law degree -

Moscow State University

Charles A. Fountain

Executive Chairman

• Non-Executive Director in ATCO Group

• Over 34 years of experience

• BSc, Economics & International Studies -

Warwick University, MPhil, Economics - Oxford

Rosneft RepresentativesKesani Representatives

1 Representation of all Major Shareholders on the Board…

Rosneft Kesani IndependentExecutive /

Nominee

Board of Directors (BoD) Composition

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

1 As per Companies Act

1313

C Manoharan

Director & Head of Refinery

• Over 40 years of refining industry

experience with key assignments across

operations, maintenance and tech

• Was Executive Director with IOCL at

Panipat Refinery

• Chemical Engineer

R Sudarsan

Nominee of LIC

• Executive Director (Inspection) of LIC

• Served in various offices of LIC across

regions

• Masters Degree in Economics

Naina Lal Kidwai

Independent Director

• Worked with organizations like PWC,

ANZ Grindlays Bank PLC, Morgan

Stanley and HSBC

• Chartered Accountant, MBA - Harvard

Business School

Deepak Kapoor

Independent Director

• Fellow Member of ICAI, Fellow Member of

ICSI and member of Institute of Certified

Fraud Examiners, USA

• Commerce graduate - Delhi University

(ranked 3rd)

1 …With Eminent Industry Professionals as Independent and Executive Directors

Audit Committee Banking & Finance CommitteeTrading and Risk Management

CommitteeOther Committees

Management Committee of

Executives

Governance structure

2 Independent + 1 Nominee 1 Independent + 2 NomineeChairman of the Board + 2

Nominee

CSR, Safety & Sustainability

Committee Meeting; Nomination

& Remuneration Committee;

Stakeholders’ Relationship

Committee

CEO + CFO + CCO + CMO +

CDO + Director & Head of

Refinery

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

14

2

Retail

sales

Single Point Mooring

(SPM) System

Pipeline network connecting port

terminal to refinery

World-class

refinery

Offtake via water,

road and rail

• Ability to handle VLCCs 8 kms

in the sea

• Natural deep draft available

throughout the year

• Extensive network of pipelines

helps transport crude to refinery

• High complexity resulting in

sustainable profitability

• Strategic location provides

advantage in sourcing and offtake

• Captive coal based power plants

with back-up of liquid/gas based

gas turbines/boilers boosts refinery

profits by providing substantial

savings

• 2 jetties, loading facilities and

gantry allow for product offtake

through multiple channels

• Strong network of 4,473

operational retail stations

Fully captive

power plant

Integrated facilities provide operational efficiency at reduced cost

Port availability through the year – no disruption

Reduces dependence on third-party service providers

Flexibility to maximize value across the entire value chain

Integrated Business Value Chain with Dedicated End-to-End Infrastructure

Strong

Parentage

Integrated Business

& Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

15

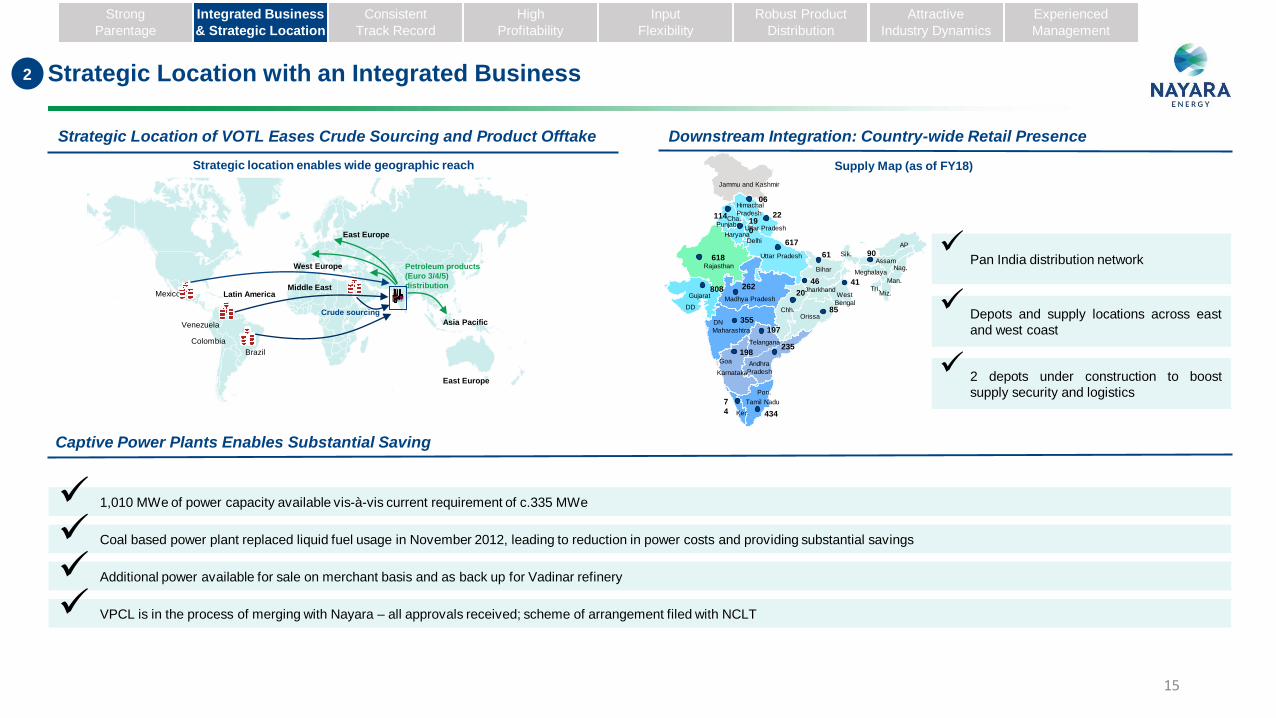

Strategic Location of VOTL Eases Crude Sourcing and Product Offtake Downstream Integration: Country-wide Retail Presence

Captive Power Plants Enables Substantial Saving

Mexico

Venezuela

Colombia

Asia Pacific

Latin AmericaMiddle East

East Europe

West Europe Petroleum products

(Euro 3/4/5)

distribution

Brazil

East Europe

Crude sourcing

617

355

262808

618

19

0

22 114

197

198235

434

7

4

46

61 90

41

20

85

06

Jammu and Kashmir

Himachal

Pradesh

Uttar Pradesh

Cha.Punjab

HaryanaDelhi

Uttar Pradesh Sik.

BiharRajasthan

Madhya Pradesh

JharkhandWest

Bengal

Tri.Miz.

Man.

Nag.Assam

Meghalaya

AP

Chh.Orissa

Telangana

Gujarat

DD

DN

Maharashtra

Goa Andhra

PradeshKarnataka

Pon.

Tamil Nadu

Ker.

Pan India distribution network

Depots and supply locations across east

and west coast

2 depots under construction to boost

supply security and logistics

Strategic location enables wide geographic reach Supply Map (as of FY18)

2 Strategic Location with an Integrated Business

1,010 MWe of power capacity available vis-à-vis current requirement of c.335 MWe

Coal based power plant replaced liquid fuel usage in November 2012, leading to reduction in power costs and providing substantial savings

Additional power available for sale on merchant basis and as back up for Vadinar refinery

VPCL is in the process of merging with Nayara – all approvals received; scheme of arrangement filed with NCLT

Strong

Parentage

Integrated Business

& Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

Confederation of Indian Industry: First Prize in CII Safety, Health and

Environment Excellence & Innovation Award, 2017

16

• Refinery started in May 2008 with 10.5 MMTPA of nameplate capacity & complexity of 6.1

• Capacity presently stands at 20 MMTPA with a complexity of 11.8

• Two Crude Distillation Units (CDUs): CDU-I and CDU-II with a capacity of 18 MMTPA and

2 MMTPA respectively, with both operating at over 99% reliability since commercial

operation in 2008

• CDU refining units had less than 5 days of unplanned shutdowns each year since inception

12.013.5

14.813.5

19.8 20.2 20.519.11

20.9 20.7

114%

129%

141%

129%

101% 101% 102%96%

105% 104%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Throughput (MMTPA) Capacity utilization

3 High Capacity Utilization Maintained Consistently since Inception

Consistently operating above 100% of capacity since commencement Key highlights

1 Throughput was low due to refinery shutdown

Skoch BSE Award: Merit of Certificate for Petroleum Refining in the category of

Occupational Health and Safety, 2017

Government of India: National Safety Award for Performance Year 2015 based

on Accident-free Year, 2017

British Safety Council: International Safety Award in the category of Health and

Safety Management, 2016

Key safety awards won over the past 2 years

Major Fire-

free Days:

3,327(1st July 2018)

Lost-Time

Injury-free

Days:

3,742(1st July 2018)

Standard

Operating

Procedures:

3,412(1st July 2018)

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

17

19%

61% 62%

53%

33% 31%

28%

6% 7%

FY12 FY15 FY18

Ultra Heavy Heavy Light

31%

15% 15%

42%61% 58%

27% 24% 27%

FY12 FY15 FY18

Heavy Middle Light

Crude mix geared towards ultra heavy crudes… …while the product mix is geared towards light and middle distillates

69% 85%

4

85%

• High complexity allows the

crude mix to be geared

towards ultra heavy crude,

enabling superior Gross

Refining Margin (GRMs)

• Tech allows production of

light and middle distillates

from the heavy and ultra

heavy crudes, which

boosts profitability

12.7 12.6 12.2 11.8

9.8 9.7 9.1 8.8 8.6

6.6 6.4

Reliance HMEL IOCLParadip

Nayara Thai Oil SK Corp BPCL Bina Sinopec IRPC Esso StarPetroleum

Complexity index for refineries

Profitable Crude and Product Mix Achieved due to High Complexity Index

• Superior complexity enables processing crude ranging

from 15-60 API with an average API of 24

• Capable of producing high quality of Euro 4 and 5

specifications of petroleum products

• Refinery expected to be Euro 6 compliant post

shutdown1 in FY19

1 A major shutdown of 25-30 days is conducted at the refinery once every 3 years

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

Source: Publically available sources on the respective companies’ websites

In FY 2018, high value-added products, MS and HSD, accounted for c. 70% of total

production

18

Nayara has consistently outperformed the Singapore benchmark GRM

4 Industry Leading GRMs with Focus on High Value-added Products

3.9

6.1 6.0 5.56.7

5.7 5.77.0

9.410.0

8.69.7

8.9 8.6

Q2 FY17 Q3 FY17 Q4 FY17 Q1 FY18 Q2 FY18 Q3 FY18 Q4 FY18

Singapore GRM Nayara CP GRMGross Refining Margin

(GRM) ($/bbl)

3.1

Delta of Nayara CP GRM

over Singapore GRM

3.3 4.0 3.1 3.0 3.2 2.9

x.x

Diversified product slate (FY18)

5.0

1.5 2.2

1.0 0.4 0.3

5.4

1.8 0.1

-1.0 0.8

0.1 -

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

HSD MS Petcoke LPG Naphtha SKO/ATF Bitumen Sulphur VGO

MM

T

Domestic Export

13.8 MMT

Domestic Sales accounted for more than 50% of total sales

High complexity enables Nayara to optimize product mix as per market

requirements

Ability to produce Euro 6 compliant product with nominal investment

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

19

5

Strategic location• Located in the Gulf of Kutch region in Gujarat, with natural deep draft availability (SPM - 32m & Jetties – 20m, 16m)

• Proximity to Middle East countries helps reduces freight cost and lead time

Current

long-term supply

contracts

• Long-term contracts exist with reputable suppliers

• Special arrangements for procurement and processing of indigenous Mangala crude

Regionally diversified

crude sourcing

• Nayara has a geographically diversified crude sourcing strategy, which helps in minimizing risk of disruption in supply

• Rosneft and Trafigura provide additional optionality for crude sourcing which can be leveraged by Nayara in the future

Engagement in spot

and long-term

arrangements

• Crude oil secured through both long term and spot arrangements to maintain balance between security of supply and optimization based on market conditions

Middle East50%

Latam33%

India8%

Other regions

9%

34% 26% 16% 30%

66% 74% 84% 70%

FY15 FY16 FY17 FY18

Term (%)

Spot (%)

FY18 crude sourcing mix

Crude Sourcing & Procurement Advantage for Nayara Energy

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

Robust Product Distribution / Offtake Network Along with an Asset-light Retail Model

20

Export sales• Export of gas oil, jet fuel and Naphtha to over 15 countries

• Contracts are generally for six months or less with variable pricing terms

Domestic sales to

oil marketing

companies

• Current contracted oil offtake of 5.9 MMTPA with domestic OMCs

• LPG offtake by PSU OMC is around 1 MMTPA

Domestic retail

sales• Current network of 4,473 operational retail fuel stations

Domestic bulk

sales

• Include both spot and term sales for primarily HSD, fuel oil, sulphur and bitumen

• Customers typically have a tenor of 1 year and include direct commercial users,

railways & defence segments and petroleum product traders

6

7% 6% 15%

12% 18%

17%

36% 22%

26%

45% 55%

43%

FY16 FY17 FY18

Bulk Retail PSUs Export

19.0 21.421.1

x.x Total Sales in MT

Marquee Customers in India and Globally

PSUs Global Oil Majors International Petroleum Traders National Oil Companies1

Sales Mix Trend (FY16-18)

1Supply to the National Oil Companies of countries such as UAE and Saudi Arabia

Nayara has achieved rapid expansion through an asset-light model with small format ROs located at secondary highways and tier 2/3 towns

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

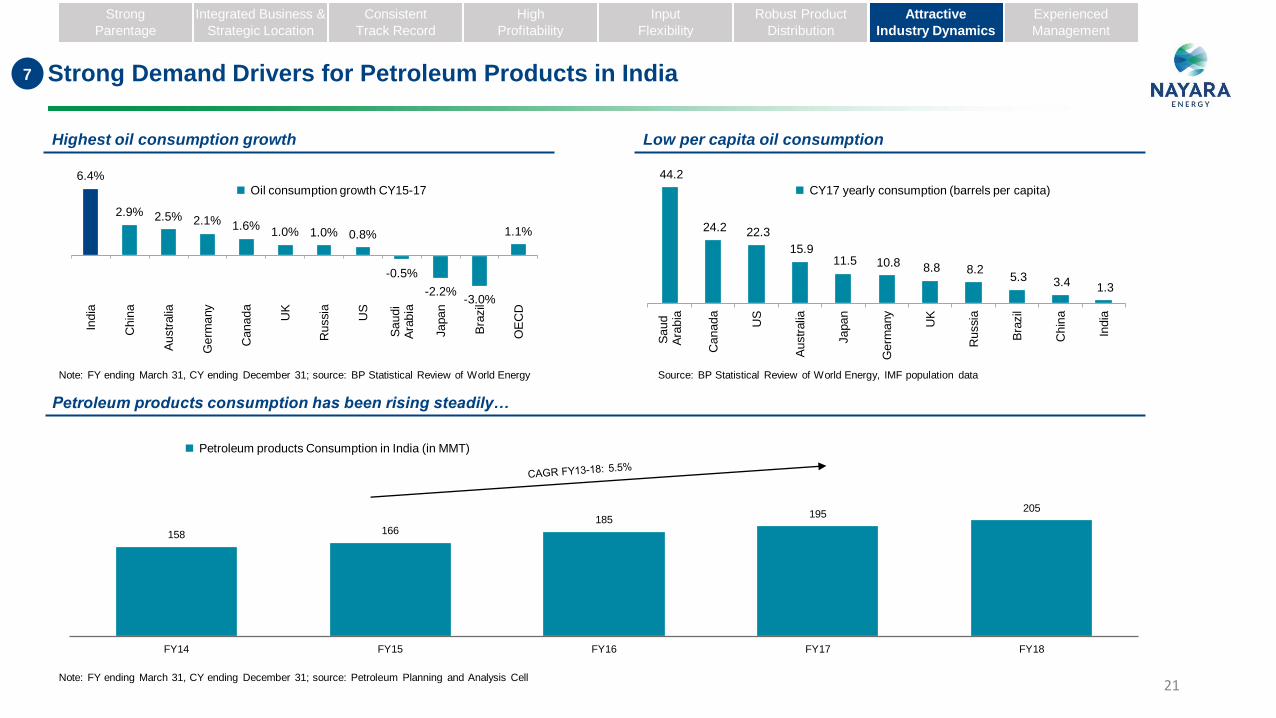

Petroleum products consumption has been rising steadily…

21

Oil consumption growth CY15-17 CY17 yearly consumption (barrels per capita)

158 166185

195205

FY14 FY15 FY16 FY17 FY18

Petroleum products Consumption in India (in MMT)

7 Strong Demand Drivers for Petroleum Products in India

Low per capita oil consumptionHighest oil consumption growth

Note: FY ending March 31, CY ending December 31; source: Petroleum Planning and Analysis Cell

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

Note: FY ending March 31, CY ending December 31; source: BP Statistical Review of World Energy

44.2

24.2 22.3

15.9 11.5 10.8 8.8 8.2

5.3 3.4 1.3

Saud

Ara

bia

Canada

US

Austr

alia

Japan

Germ

any

UK

Russia

Bra

zil

Chin

a

India

Source: BP Statistical Review of World Energy, IMF population data

6.4%

2.9% 2.5% 2.1% 1.6%1.0% 1.0% 0.8%

-0.5%

-2.2%-3.0%

1.1%

India

Chin

a

Austr

alia

Germ

any

Canada

UK

Russia

US

Saudi

Ara

bia

Japan

Bra

zil

OE

CD

22

Indian Refining Capacity & Product Specifications

• Out of an installed capacity of c.248 MMTPA in India, 63 MMTPA capacity refineries

are more than 20 years old

• Domestic consumption of petroleum products is c.205 MMTPA with a 5-year CAGR

of 5.5%

• Nayara is well placed to capitalise on growing domestic market for cleaner fuels as

mandated by the government

Euro Norms 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

European Union Euro 4 Euro 5 Euro 6

India (NCR+ 13 Cities) Euro 3 (BS III) Euro 4 (BS IV)

India (Nationwide) Euro 2 (BSII) Euro 3 (BSIII) BSIV

Hong Kong3 Euro 4 Euro 5 Euro 6

South Korea Euro 4 Euro 5 Euro 6

China (Beijing)4 Euro 2 Euro 3 Euro 4 Euro 5

Singapore5 Euro 4 Euro 5 Euro 6

Malaysia Euro 2 Euro 4

Thailand Euro 3 Euro 4

Philippines Euro 2 Euro 4

Bangladesh (gasoline) Euro 2 Euro 3

Bangladesh (Diesel) Euro 1 Euro 2

7

BSVI - 2020

Industry refining capacity split and outlook1

As India moves towards BS-VI, Nayara is capable of producing high quality petroleum products meeting fuel standards2

BSVI - 2019

Strong retail annual volume growth achieved by Nayara post deregulation of diesel prices in October 2014

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

1,644 2,797

4,500

7683

93

40

60

80

100

-

1,000

2,000

3,000

4,000

5,000

FY16 FY17 FY18

Volume (TKL) - LHS TPO - RHS

65% CAGR since FY16

• On 18th October, 2014, the Union Cabinet Committee of Economic Affairs, formally

announced deregulation of diesel prices

• The biggest benefit could be through higher marketing margins

• Deregulation to lead to market-linked pricing and encourage private oil refiners to

foray into domestic oil marketing space

Note:

1. Source: Petroleum Planning and Analysis Cell

2. Compiled from various sources including Delphi Worldwide Emission Standards, The Air Pollution Control (Vehicle Design Standards) (Emission)(Amendment) Regulation 2017, National Environment Agency report Singapore, CIMB equity research

3. Hong Kong commenced Euro 6 for private car and taxi from 2017. For light bus and goods vehicle, Euro 6 commenced from 2018

4. In Beijing, Euro 5 was implemented in 2013 for PI without IUPR and CI / for PI with IUPR, it was implemented in 2015

5. For diesel-run vehicles

23

B Anand

Chief Executive Officer

C Manoharan

Director & Head of Refinery

Anup Vikal

Chief Financial Officer

Alan McGown

Chief Marketing Officer

Evgeny Storozhuk

Chief Commercial Officer

Sergey Denisov

Chief Development Officer

23

Vastly Experienced Management with Substantial Execution Experience in the Petroleum Sector

• Experience in corporate finance, strategy, investment banking and commodity trading

• Previously was the CFO of Trafigura India Private Limited; prior to Trafigura, was Group Director of Finance for Future Group and held

senior positions with Vedanta Resources Group

• Handled variety of assignments in key positions in Refining Operations, Maintenance and Technical Services at Gujarat Refinery, Panipat

Refinery as well as Head Office (Refinery Division)

• Prior to Nayara Energy, he was Executive Director with IOCL at the Panipat Refinery

• Rich experience in Banking and Finance industry

• Prior to Nayara Energy, he was the CFO of Snapdeal and has held senior positions with Aircel, Interglobe Aviation, COLT Telecom & Bharti

Airtel

• Holds Mechanical Engineering and MBA degree

• Experience in the Oil Marketing sector; he holds a degree in Business Studies Finance and Post Graduate Diploma in Marketing

• Prior to Nayara Energy, he worked with Rosneft, BP &TNK BP in various key positions in Poland, US, China and Russia

• Vast Experience in Oil and Gas industry

• Prior to Nayara Energy, he worked with Rosneft and TNK-BP in Russia and Ukraine

• Holds degree in Economics and Management, MBA and has completed his post-graduation in Accounting

• Experience in the area of Upstream Field Development, Project Management, Refining Commercial and Downstream Strategy

• Prior to Nayara Energy, he has worked with BP, TNK BP and Sidanco in Russia, Ukraine, Netherlands, UK and Germany

• Holds a degree in Mechanical Engineering

8

30+

40+

26+

25+

20+

20+

xx Years of experience

Strong

Parentage

Integrated Business &

Strategic Location

Consistent

Track Record

High

Profitability

Experienced

Management

Input

Flexibility

Robust Product

Distribution

Attractive

Industry Dynamics

Near Term Strategic Plans

24

Near Term Strategic PlansSecuring the Base

Optimization of capital

structure

• Plans implemented

o Achieved refinancing of INR term loans at favourable terms with lower spreads

o INR Bond of INR 2,400cr (c. US$ 355mn) availed and in process of availing long term prepayments for converting short term liabilities into

long term debt

o Aiming at further reduction in interest cost by availing synthetic full currency swaps

o Entered into a US$750mn long term export advance facility to reduce reliance on short term debt

Margin Improvement

Projects

• CCR Unit Revamp (Increase in capacity from 3.2 KTPD to 3.7 KTPD)

o Improves GRM by upgrading Hydro-Treated Heavy Naphtha from NHT to high value octane rich Reformate

• New SRU (Sulphur Recovery Unit) and SWS (Sour Water Stripper) Units

o Expected to lead to enhancement of crude blend window with respect to Sulphur and Nitrogen, and optimizing Crude basket on a

sustained basis

• NHT and ISOM Revamp

o NHT revamp improves the margins by upgrading sour Naphtha to Gasoline and Diesel; NHT can supply incremental Hydro-Treated

conditioned feed to match revamps of ISOM unit and CCR unit which is expected to eventually produce more of high value Octane barrels

o Higher incremental Isomerate volumes are expected to improve flexibility to upgrade incremental naphtha into Gasoline, and produce

Incremental high octane and low Sulphur Gasoline grades

• Retail Expansion

o Leverage existing ready retail platform for further expansion to capitalize on deregulation of gasoline prices

o 4,473 operational retail stations and 2,688 retail stations under implementation across India

o Plan to setup 5 depots across strategic locations in the country to improve supply security and reduce dependency on PSUs

o Automation of all retail stations under implementation in phased manner

Retail expansion and

automation

Low cost

projects with low

payback period

Asset light model

for value

creation

Saving in

interest cost and

extension of

maturity

25

Restoration of Sanctions on Iran by US Administration

Alternate Plans of Nayara Energy

• In May 2018, US announced discontinuation of its participation in the Joint Comprehensive Plan of Action (JCPoA)

• 180 days wind-down period until 4th Nov 2018 given to demonstrate the reduction of trade with Iran and Iranian counterparties

• Nayara’ s position:

• Shall always remain complaint with the US Sanctions imposed on Iran

• If the Govt. of India negotiates a waiver / exemptions with Govt. of USA, Nayara shall remain in compliance with Sanctions and such exemptions read together

Restoration of Sanctions on Iran : Nayara Energy’s Plans Going Forward

26

Compliance with Sanctions Laws

Secure suitable replacement crudes from Middle East and Latin America through combination of spot and term volumes

Leverage on established relationships with all major suppliers

Nayara plans to have replacement contracts to minimize the economic hit

Financial Overview

27

28

Nayara’s Financial Performance (Provisional unaudited IFRS financials)

Particulars FY16 FY17 FY18 3mFY18 3mFY19

(in US$mn1, unless stated otherwise)

(12 months ended

Mar 2016)

(12 months ended

Mar 2017)

(12 months ended

Mar 2018)

(3 months ended

Jun 2017)

(3 months ended

Jun 2018)

Throughput - Million Tons 19.11 20.95 20.70 5.13 5.24

Throughput - Million Barrels 133 145 144 36 37

INCOME

Revenue from Operations 9,405 11,117 13,148 3,241 4,024

Other Income 345 519 110 133 12

Total Income 9,750 11,637 13,258 3,374 4,036

EXPENDITURE

Cost of Goods Sold (COGS)2 6,395 7,497 9,145 2,106 2,937

Excise Duty 1,475 1,730 2,260 730 632

Other Expenditure3 611 574 634 182 155

Total Expenditure 8,481 9,800 12,039 3,017 3,724

EBITDA4 924 1,317 1,108 224 300

Interest & Finance Charges 415 583 508 101 83

Depreciation 236 258 260 56 64

Exceptional Items Gain / (Loss) (107) (801) (155) (144) (4)

Share of Gain / (Loss) of associates - (8) - - -

Net Exchange Rate differences (138) - (64) 1 (107)

Profit before Tax (PBT) 373 187 231 57 54

(Loss) from Discontinued Operations (38) (341) (14) (14) -

Tax Expense 198 227 139 70 20

Profit after Tax (PAT) 137 (381) 78 (27) 34

Note:

1. USDINR rates used: FY16 – 66.33; FY17 – 64.84; FY18 – 65.04; 3mFY18 – 64.74; 3mFY19 – 68.58

2. COGS = Cost of raw materials consumed + Purchases of stock-in-trade (petroleum products) + Changes in inventory of finished goods, stock-in-trade and work-in-progress

3. Other Expenditure = Employee benefits expense + Other expenses (does not include net exchange rate differences)

4. EBITDA = Revenue from operations – COGS – Excise duty – Other Expenditure

0.63x

0.60x 0.60x

0.64x

FY16 FY17 FY18 Jun-18

29

Revenue from Operations (US$mn) EBITDA (US$mn)

Leverage Profile

Key Financial Metrics (Provisional unaudited IFRS financials)

Note:

1. USDINR rates used: FY16 – 66.33; FY17 – 64.84; FY18 – 65.04; 3mFY18 – 64.74; 3mFY19 – 68.58

2. Gross Debt (Debt) = Non-current Interest-bearing loans and borrowings + Current Interest-bearing loans and borrowings + Interest accrued but not due to borrowing

3. Gross Debt for June-18 includes additional debt of c. US$ 1,105mn which Nayara has undertaken after 30 June 2018 i.e. Export advance facility of US$ 750mn and INR Bond of INR 2,400cr (c. US$ 355mn)

4. Net Debt = Gross Debt – (Cash and short term deposits + Investments in mutual funds)

5. Gross Debt / EBITDA and Net Debt / EBITDA for Jun-18 have been calculated using LTM Jun 2018 EBITDA = FY18 EBITDA + 3mFY19 EBITDA – 3mFY18 EBITDA

9,405

11,117

13,148

FY16 FY17 FY18

3,241

4,024

3mFY18 3mFY19

224

300

3mFY18 3mFY19

924

1,317

1,108

FY16 FY17 FY18

5.06x

3.14x

3.79x4.08x

4.80x

2.75x3.13x

3.58x

FY16 FY17 FY18 Jun-18

Gross Debt / EBITDA Net Debt / EBITDA

33

01/01/10 09/16/11 05/31/13 02/14/15 10/29/16 07/15/18

BBB

BBB+

A-

A

A+

AA-

BBB-

AA

Acquisition

(Aug-2017)

Continuous Improvement in Local Credit Rating

30

Improvement by three notches (“A” to “AA”) post acquisition

Strong market position of consortium promoters

Strong operational profile with one of the highest complexities across refineries in India

Relatively higher Gross Refining Margins (GRMs) than peers in the industry

Crude throughput more than rated capacity of 20 MMTPA

Strategic location of refinery along with captive port terminal and power plant

Adequate debt coverage metrics

CARE Long

term rating

Source: CARE rating rationale, as of 25 May 2018

31

List of Abbreviations

Abbreviation Nomenclature

API American Petroleum Institute gravity

ATF Aviation Turbine Fuel

BBL Barrel (unit)

Bn Billion

BP British Petroleum

BPCL Bharat Petroleum Corporation Limited

CAGR Compounded Annual Growth Rate

CCR Continuous Catalytic Regeneration Unit

CCO Chief Commercial Officer

CDO Chief Development Officer

CDR Corporate Debt Restructuring

CDU Crude Distillation Unit

CI Compression Ignition Engine

CII Confederation of Indian Industry

CMO Chief Marketing Officer

E&P Exploration and Production

GRM Gross Refining Margin

HMEL HPCL-Mittal Energy Limited

HPCL Hindustan Petroleum Corporation Limited

HSD High Speed Diesel

IOCL Indian Oil Corporation Ltd.

ISOM Isomerization Unit

IUPR In Use Performance Ratio

Abbreviation Nomenclature

KTPD Kilo Tonnes per Day

LIC Life Insurance Corporation of India

LNG Liquefied Natural Gas

LPG Liquefied Petroleum Gas

MHC Mild Hydrocracker Project

MMT Million Metric Tonnes

MMTPA Million Metric Tonnes Per Annum

MS Motor Spirit (Petrol) or Gasoline

MWe Megawatt Electric

NCLT National Company Law Tribunal

NHT Naphtha Hydro-Treater unit

OMC Oil Marketing Companies

PPAC Petroleum Planning & Analysis Cell

PSU Public Sector Undertaking

SRU Sulphur Recovery Unit

SWS Sour Water Stripper

TNK Tyumenskaya Neftyanaya Kompaniya, Tyumen Oil Company

TKL Total Kilo Litres

TPO Throughput per Outlet

VGO Vacuum Gas Oil

VLCC Very Large Crude Carriers

VOTL Vadinar Oil Terminal Limited

VPCL Vadinar Power Company Limited

Thank You

32