NAVIGATING THE GREAT AMERICAN TRANSITION TO RETIREMENT? · navigating the great american transition...

64

NAVIGATING THE GREAT AMERICAN TRANSITION TO RETIREMENT? Asset Distribution Planning Nasser Ali CFA, CAIA, CFP, AAMS, CMFC, CRPC Director of Financial Advisory Services ©2016 Lincoln National Corporation For education and training purposes. Not for use with the public. CRN-1575502-082216.

Transcript of NAVIGATING THE GREAT AMERICAN TRANSITION TO RETIREMENT? · navigating the great american transition...

NAVIGATING THE GREAT AMERICAN TRANSITION TO RETIREMENT? Asset Distribution Planning

Nasser Ali CFA, CAIA, CFP, AAMS, CMFC, CRPC Director of Financial Advisory Services

©2016 Lincoln National Corporation For education and training purposes. Not for use with the public. CRN-1575502-082216.

Designing an Effective Asset Distribution Plan

9.2

5.0

2.4

0

1

2

3

4

5

6

7

8

9

10

S&P 500 Average EquityInvestor

Inflation CPI-U

Perc

ent

SOURCE: Dalbar Inc. Quantitative Analysis of Investor Behavior 2014. Represents average annually compounded returns of equity indices vs. equity mutual fund investors; based on the length of time shareholders actually remain invested in a fund and the historical performance of the fund’s appropriate index. Returns are from the time period of January 1992 to December 2011. Past Performance is no guarantee of future results. Investors cannot invest directly into in an index.

During the biggest bull market in history (1994 – 2013), equity mutual fund investors significantly lagged the market. Why?

Answer: Investors are repeatedly led astray by past

performance, moods of the market, etc.

Solution: A disciplined investment process.

“Investor Behavior” Penalty

Limbic System

Main structures: Hypothalamus Hippocampus Amygdala

Portfolio Construction Considerations

Client Objectives 1. Objective 2. Risk Tolerance 3. Liquidity 4. Time Horizon 5. Constraints / Taxes 6. Unique Circumstances

Investment Factors 1. Performance 2. Diversification 3. Risk Characteristics 4. Management 5. Expenses 6. Tax Characteristics

Asset Considerations: 1. Cash 2. Bonds 3. Stocks 4. Alternative Investments 5. Vehicles

• ETFs, Mutual Funds, SMAs, Individual Securities, Annuities, Private Placements

Liquidity

SOURCE: LFD

Sequence of Returns

Time Horizon

28%

72%

1 Year Returns

13%

87%

5 Year Returns

100%

15 Year Returns

5%

95%

10 Year Returns

Probabilities of positive/negative returns for given holding periods

SOURCE: Morningstar Direct, LFN Investment Research, data uses calendar returns between 1928-2014.

Risks Characteristics

Source: Standard & Poor’s

Asset Class Short Term

Market Volatility Market Risk Interest Rate

Risk Credit Risk Inflation Risk

Stocks High High Moderate Low Low

REITs Moderate Moderate Moderate Low Low

High Yield Bonds High Moderate High High Moderate

Corporate Bonds Moderate Moderate High Moderate –

High Moderate

U.S. Government

Bonds Low

High

High Low High

Cash Low Low Low – Moderate Low High

Different asset classes are subject to various levels of risk. Below indicates the general risk exposures of various asset classes.

Asset Location

Tax-Deferred Client Dependent Taxable

Client Dependent

Client Dependent Taxable

Either Either Taxable

Tax Efficiency Low High

Low

H

igh

Ret

urn

Pote

ntia

l

Medium

Med

ium

The goal of asset location is to divide their investments

among taxable and retirement accounts in a way that will defer taxes and ultimately provide the best after-tax

returns. The optimal location for an investor's assets can also vary depending on tax bracket, investment holding

periods, and the tax and return characteristics of the

securities.

Order of Distribution

Developing a Distribution Strategy Objective: maximize retirement income and family wealth on an after-tax basis Establish a consolidated cash management account o Deposit all taxable income to this account (Social Security, pensions,

annuities, deferred compensation, required minimum distributions, part-time employment, trust income, rental income, etc.).

o Deposit investment cash flows (dividends, interest, and capital gains from taxable accounts).

o Excess balances may be used to periodically rebalance the portfolio. o Inadequate balances dictate the need for withdrawals from the portfolio.

Determine the order of withdrawal between account types. o Taxable accounts (exclusive of cash management account) - periodic taxable

dividends, interest, and/or capital gains o Tax-deferred accounts - taxable income at distribution only o Tax-free accounts - no taxes periodically or at distribution

ASSET DISTRIBUTION PLANNING 2015

Taxes Absent taxes, any order of withdrawal would yield identical results.*

However, federal ordinary income and capital gains tax rates are a reality and have varied significantly over time.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1913

1919

1925

1931

1937

1943

1949

1955

1961

1967

1973

1979

1985

1991

1997

2003

2009

2015

2021

Tax R

ate

Top Ordinary Income Tax Rate Top Capital Gains Tax Rate

Source: Internal Revenue Service as of 12/31/14.

ASSET DISTRIBUTION PLANNING 2015

* Assuming all accounts earn the same rate of return.

Taxes Qualified (Q) versus Non-Qualified (NQ) Accounts o Qualified accounts are generally funded with pre-tax dollars and grow tax-

deferred. Distributions are fully taxed (exception: after-tax contributions to traditional IRAs and qualified company retirement plans).

o Non-qualified accounts are generally funded with after-tax dollars and do not grow tax-deferred. Distributions are partially taxed (exception: NQ annuities and cash value life insurance).

ASSET DISTRIBUTION PLANNING 2015

Distribution order is highly dependent on your expectations for your future tax liabilities relative to your situation today.

ORDER OF DEPLETION - FINANCIAL INDEPENDENCE

Taxes Decreasing

Taxable ·High basis/loss assets ·Low basis assets

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Taxes Increasing

Taxable ·Low basis assets ·High basis/loss assets

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

*Withdrawals from cash values reduces death benefits and may be subject to surrender charges

Some assets are more attractive than others when passing on wealth to children and/or grandchildren should you predecease them.

*Withdrawals from cash values reduces death benefits and may be subject to surrender charges

ORDER OF DEPLETION - FAMILY

Taxes Decreasing

Taxable ·High basis/loss assets ·Low basis assets

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Taxes Increasing

Taxable ·Low basis assets ·High basis/loss assets

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

·Low basis assets

·Roth IRAs

·Q Retirement Plans/IRAs

·Low basis assets

·Roth IRAs

·Q Retirement Plans/IRAs

The most punitive assets to have in your estate at death are those that are subject to both estate and income tax liability.

*Withdrawals from cash values reduces death benefits and may be subject to surrender charges

ORDER OF DEPLETION - ASSETS IN EXCESS OF THE ESTATE TAX EXEMPTION

Taxes Decreasing

Taxable ·High basis/loss assets ·Low basis assets

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Taxes Increasing

Taxable ·Low basis assets ·High basis/loss assets

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

·Q Retirement Plans/IRAs

·Q Retirement Plans/IRAs

The most beneficial assets to pass to a charity are those that may create significant tax liability to you.

*Withdrawals from cash values reduces death benefits and may be subject to surrender charges

ORDER OF DEPLETION - CHARITY

Taxes Decreasing

Taxable ·High basis/loss assets ·Low basis assets

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Taxes Increasing

Taxable ·Low basis assets ·High basis/loss assets

Tax-Deferred ·NQ Annuities ·Q Retirement Plans/IRAs

Tax-Free ·Cash Value Life Insurance*

·Roth IRAs

·Low basis assets

·Q Retirement Plans/IRAs

·Low basis assets

·Q Retirement Plans/IRAs

Asset Management

Combining assets that are not directly correlated can help reduce risk and potentially increase return.

The EFFICIENT FRONTIER GRAPH identifies a set of asset allocation parameters which may provide an optimal balance between risk and return across a range of risk levels. There can be no assurance that the risk/return characteristics will perform according to the asset allocation strategies chose. Past performance does not guarantee future results.

ASSET ALLOCATION

The placement of assets should not only provide for tax efficiency, but also for withdrawal flexibility to help manage distributions in periods of market volatility.

Some characteristics are more preferable than others within asset classes.

ASSET PLACEMENT

Account Type Taxable Tax-Deferred/Tax-Free

Asset Allocation Same as total portfolio % Same as total portfolio %

Asset Type Municipal bonds Corporate bonds

Low dividend equities High dividend equities

Asset Management Passive, Active (tax-sensitive)

Active

Public Private

General Asset Location Guidelines

Tax-Deferred Client Dependent Taxable

Client Dependent

Client Dependent Taxable

Either Either Taxable

Tax Efficiency Low High

Low

H

igh

Ret

urn

Pote

ntia

l

Medium

Med

ium

Source: FPA Journal – Asset Location: A Generic Framework for maximizing After-Tax Wealth; Journal of Finance: Optimal Asset Location and Allocation with Taxable and Tax-Deferred Investing. See the Main Disclosure for additional information

The goal of asset location is to divide their investments among taxable and retirement accounts in a way that will defer taxes and ultimately provide the best after-tax returns.

The optimal location for an investor's assets

can also vary depending on tax

bracket, investment holding periods, and

the tax and return characteristics of the

securities.

Withdrawal rates can significantly impact the longevity of an investment portfolio

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

Withdrawal Rate Risk: 1973-2014

7% 6% 5% 4.5% 4%

Source: Thompson Financial Investment View 12/31/14

Hypothetical value of $500,000 invested at 12/31/72. Portfolio: 50% large company stocks, 50% intermediate-term bonds. Assumes reinvestment of income, no transaction costs or taxes, annual rebalancing, and no additional deposits. This is for illustrative purposes only and not indicative of any investment. Past performance is no guarantee of future results.

WITHDRAWAL RATES

US Large Company Equity and 10 Year US Treasury Bond Rates 12/31/73-12/31/14

Source: Yahoo Finance

GSPC: Standard & Poor’s 500 Index

TNX: Chicago Board Options Exchange Interest Rate 10 Year Treasury Note

HISTORICAL MARKET PERFORMANCE

6.54% 1.68%

Expectations of future rates of return and inflation may differ from historical averages.

The “4% annual safe withdrawal rate” rule of thumb may be overly aggressive given current market conditions. o Most studies indicate that a withdrawal rate in the range of 2.5% - 3%

may be more appropriate to help ensure longevity of the portfolio.

WITHDRAWAL RATES

Historical

(1973-2014) 10 Year Forward

Assumptions

Intermediate Fixed Income 7.3% 3.9%

US Large Cap Equity 11.9% 7.3%

Portfolio 50%/50% 9.6% 5.6%

Inflation 4.2% 2.7%

Inflation Adjusted Return 5.4% 2.9%

4% WITHDRAWAL RULE

Matching the most appropriate funding sources to specific needs is a key element in designing an effective retirement plan.

Stable Income Sources

Systematic Withdrawals

Specific Distributions

Asset Repositioning

RETIREMENT INCOME PLANNING

Core Expenses Goals

. Legacy

.

Lifestyle Expenses

Portfolio Strategy

PORTFOLIO STRATEGY

Strategy Objective Ideal Situation Distribution

Need

Asset/Liability Matching

Immunize risk by matching a future liability with an asset

1) Portfolio w/ high dist. requirement +5%

Needs / Wants Separation

Fund needs expenses and wants expenses separately and address investor psychology

1) Retirement 2% - 4.5%

Segmented Portfolio

Create risk segments to optimize yield and address investor psychology

1) Retirement, 2) Endowment /

Foundation 2% - 4.5%

Total Return Portfolio

All assets are positioned to achieve the same goals(s)

1) Accumulation, 2) Retirement w/

min. dist. 0% - 2%

ASSET – LIABILITY MATCHING

Description: Strategy to minimize risk to support a required withdrawal strategy beyond the ability of the portfolio.

Best Use: Investor who’s withdrawals are more than a portfolio can sustain Pros:

1. Assure known liabilities are provided for with known asset payoffs 2. Immunize portfolio from duration risk (interest rate rises) 3. Address psychological/behavioral aspects

Cons: 1. Requires futures liabilities to be project with level of certainty 2. Requires monitoring and cash flow budgeting

ASSET/LIABILITY MATCHING

Institutional process to primarily immunize duration risk and seek targeted yields.

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Living Exp. $100k $100k $100k $100k $100k $100k

Travel $20k $20k $20k $20k $20k $20k

Car $50k

Grandson Coll. $25k $27k $30k

TOTAL EXP. $120k $120k $170k $145k $147k $150k

NEEDS / WANTS SEPARATION

Description: Match survival expenses (needs) with known income sources and lifestyle expenses (wants) with variable income sources

Best Use: Investor that has ability to change his/her lifestyle Pros:

1. Apply Asset/Liability matching process 2. Address psychological/behavioral aspects 3. Mitigate panic in down years to allow market recovery 4. Allows for implementation flexibility (use of different products)

Cons: 1. Requires reviewing and cash flow budgeting 2. Discretionary expenses may be tied to market requiring flexibility

NEEDS / WANTS SEPARATION

Expense Category Purpose Examples Funded By…

Basic Needs Pay for expenses to sustain oneself

Food, Shelter, Clothing, Medical, Taxes, etc.

Social Security, Pensions, Annuities, other stable income

Lifestyle Wants Pay for desirable but not necessary lifestyle expenses

Travel, Country Club, Boat Upkeep, Leisure Activities, Restaurants, etc.

Investment portfolio income and/or periodic withdrawals

Specific Goals Pay for non-recurring goals with specific timing

Grand children’s college, Second home, Charitable Gift

Portfolio withdrawals as needed

NEEDS / WANTS SEPARATION

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Mortgage $25k $25k $25k $25k $25k $25k

Food / Utilities $25k $25k $25k $25k $25k $25k

Gas / Transportation $5k $5k $5k $5k $5k $5k

Medical $10k $10k $10k $10k $10k $10k

TOTAL NEEDS $65k $65k $65k $65k $65k $65k

Travel $25k $25k $25k $25k $25k $25k

Country Club / Golf $5k $5k $5k $5k $5k $5k

TOTAL WANTS $30k $30k $30k $30k $30k $30k

Gift $50k

Grandson College $25k $27k $30k

TOTAL GOALS $50k $25k $27K $30K

NEEDS / WANTS SEPARATION

NEEDS / WANTS SEPARATION

SEGMENTED PORTFOLIO (BUCKETED PORTFOLIO)

Description: Establish a series of buckets with more stable and conservative assets in the near term bucket and more aggressive assets in the long term bucket

Best Use: Structure portfolio approach with high unsustainable withdrawal rate Pros:

1. Target assets’ riskiness with appropriate investment horizon 2. Develop a dedicated withdrawal strategy 3. Address psychological/behavioral aspects 4. Mitigate panic in down years to allow market recovery

Cons: 1. Overall portfolio may become more aggressive as strategy matures 2. Need to review and tweak strategy throughout the strategies life span 3. Periodic rebalance to ensure overall portfolio risk

Bucket # 1 Used for short term needs. Primarily comprised of stable assets.

Bucket # 2 Used for intermediate term needs. Primarily comprised of income oriented assets, with some level of fluctuation.

Bucket # 3 Used for long term needs to grow assets and address purchasing power risk. Primarily comprised of growth assets that may high volatility.

SEGMENTED PORTFOLIO

SEGMENTED PORTFOLIO

Cash TIPS Interm. BondsLong Bonds High Yield Bonds REITsLarge Caps Smid Caps Int'l StockEmerg. Mkts Absolute Return

TOTAL RETURN

Single

Joint

IRA

ROTH

Trust

Lifestyle

Car

House

Vacation

College

Platform Considerations

Operational/Administrative Support Materials Proposals Wholesalers Website Reporting Paperwork Procedures

Platform Activities

Investment CMAs Asset allocation Investment selection Trading & rebalancing Security monitoring Due diligence

Advisory Platform Choices

Turnkey? Yes No

Multiple Solutions?

Yes No

Mt. Yale - SMA platform - Availability of Alts

IPC - SMA platform - High Touch Managers

Premier

- Premier Plus is part of the Premier Platform

- Offers funds, ETFs, individual securities and SMAs on a single platform

- Ease of advisor interface - Enhanced Operational Support - Comprehensive platform also

offering turnkey programs

Premier - Turnkey mutual funds, ETF, UMA, &

ActivePassive - SMAs available - Other Strategists available: Symmetry,

Russell, PMC

Brinker - Turnkey mutual funds, UMA programs - SMAs available - Crystal Strategy

Assetmark - Turnkey mutual funds, UMA & ETF

programs - SMAs available - Various strategists available

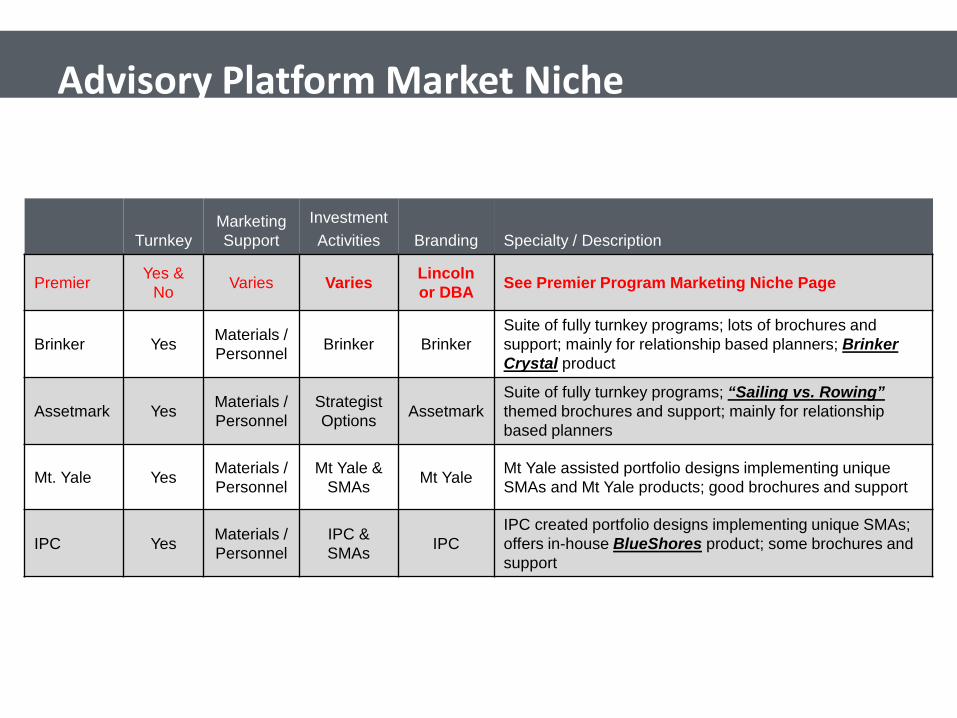

Advisory Platform Market Niche

Turnkey Marketing Support

Investment Activities Branding Specialty / Description

Premier Yes & No Varies Varies Lincoln

or DBA See Premier Program Marketing Niche Page

Brinker Yes Materials / Personnel Brinker Brinker

Suite of fully turnkey programs; lots of brochures and support; mainly for relationship based planners; Brinker Crystal product

Assetmark Yes Materials / Personnel

Strategist Options Assetmark

Suite of fully turnkey programs; “Sailing vs. Rowing” themed brochures and support; mainly for relationship based planners

Mt. Yale Yes Materials / Personnel

Mt Yale & SMAs Mt Yale Mt Yale assisted portfolio designs implementing unique

SMAs and Mt Yale products; good brochures and support

IPC Yes Materials / Personnel

IPC & SMAs IPC

IPC created portfolio designs implementing unique SMAs; offers in-house BlueShores product; some brochures and support

Turnkey or Flexible

Flexible Turnkey

Annuity or Inv. Premier Plus

Annuity

Lincoln Choice Plus American Legacy

Implementation SMA

Prem. SMA

‘40 Act Funds

Combo

Premier UMA

Fund or ETF

Prem. Mgr

Symmetry

Russell

Morningstar Strategic

or Tactical

Fund ETF

Symmetry

Morningstar

Strategic Tactical

PMC: Fixed Income

PMC Dynamic

Combo

Premier Active/Passive

PMC Select

PMC Sect. Rot.

PMC Dynamic Wilshire

S&P

S&P

Vanguard

Premier Platform Choices

Premier Series Market Niche

Turnkey

Marketing Support

Investment Activities Branding Specialty / Description

Premier Plus No LFN team Planner Lincoln or DBA Low cost; limited brochures;

Premier Manager Yes LFN team Envestnet Lincoln or

DBA Low cost turnkey fund program; LFA Allocations; Envestnet fund selection; Allowable planner changes

Premier UMA Yes LFN team Envestnet Lincoln Low cost turnkey program which will incorporate funds, ETFs and stocks; Envestnet selection

Premier Active/Passive Yes LFN team Envestnet Lincoln

Low cost turnkey program which incorporates both active and passive management; Active/Passive ratio varies throughout year.

Premier SMAs Yes LFN team SMAs Lincoln Reasonable cost SMA program; close to 300 SMAs available;

Premier Strategist Market Niche

Turnkey

Marketing Support

Investment Activities Branding Specialty / Description

Morningstar (Premier Strategist)

Yes Materials Morningstar Morningstar Morningstar allocation and fund selection; leverage Morningstar’s name

PMC (Premier Strategist)

Yes Materials PMC PMC PMC provides static and tactical investment selection via ETFs.

Russell (Premier Strategist)

Yes Materials Russell Russell Russell allocation and fund selection; leverage Russell’s institutional processes

Symmetry (Premier Strategist)

Yes Materials / Personnel Symmetry Symmetry

Symmetry executes investment/portfolio decisions based on ACADEMIC research; Symmetry board is comprised of many academics; use of DFA Funds or ETFs; good brochures to support academically based portfolios

S&P Yes Materials / Personnel S&P S&P S&P allocation and fund selection; leverage S&P’s

institutional processes

Vanguard Yes Materials Vanguard Vanguard Vanguard allocation and fund selection; leverage Vanguard’s institutional processes

Wilshire Yes Materials Wilshire Wilshire Wilshire allocation and fund selection; leverage Wilshire’s institutional processes

Holistic Planning for Financial Independence

Even the best finance experts face their share of surprises when they retire, according to a June 2015 article in Forbes. 1) Medicare doesn’t cover everything 2) Travel isn’t cheap 3) Paying off your mortgage pays off 4) Investment risk can lose its allure 5) Taxes can get more complicated when you retire 6) It’s difficult to switch from saving to spending 7) Adjusting to retirement takes time

Top Seven Retirement Surprises

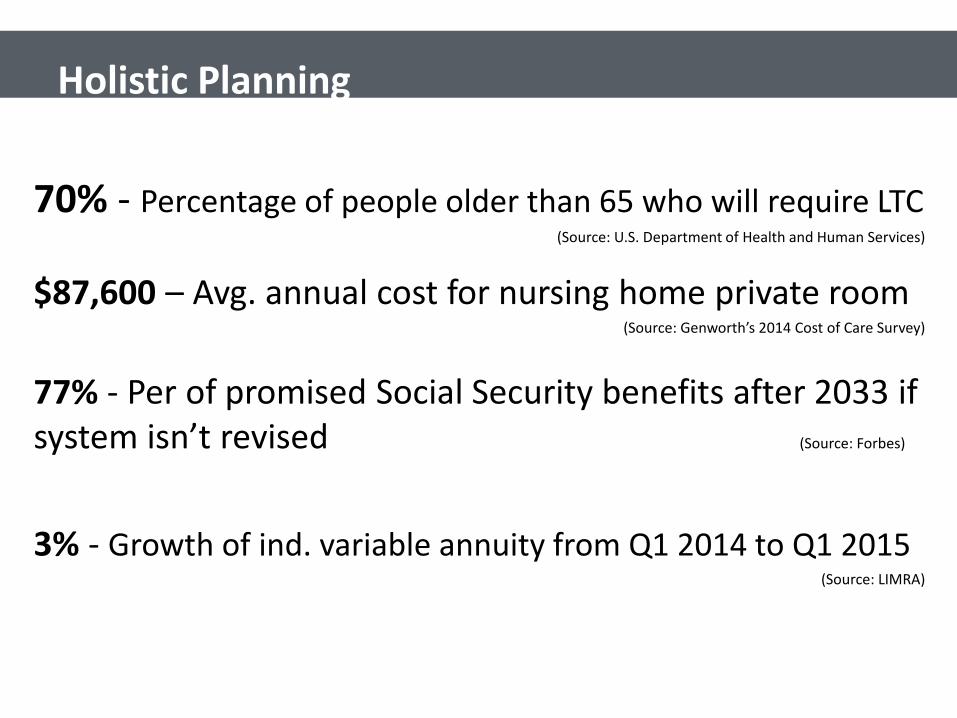

70% - Percentage of people older than 65 who will require LTC (Source: U.S. Department of Health and Human Services)

$87,600 – Avg. annual cost for nursing home private room (Source: Genworth’s 2014 Cost of Care Survey)

77% - Per of promised Social Security benefits after 2033 if system isn’t revised (Source: Forbes)

3% - Growth of ind. variable annuity from Q1 2014 to Q1 2015

(Source: LIMRA)

Holistic Planning

Holistic Planning

The investment portfolio is only a piece of the puzzle!

Investments Annuities

Insurance

LTC

Case Study

Follow the Investment Process

Advice & Planning

Portfolio Modeling Analysis & Design

Development of Investment Policy

Statement

Implementation, Manager Search &

Selection

Ongoing Reviewing and Reporting

Step 1: Gather Information

Step 2: Analyze and Model

Step 2: Analyze and Model

Step 2: Analyze and Model

Step 2: Analyze and Model

Risk Tolerance Questionnaire

Sections:

1) Risk Capacity 2) Risk Attitude

Step 2: Analyze and Model

Step 2: Analyze and Model

Step 2: Analyze and Model

Step 4: Implementation

Step 4: Implementation

Step 5: Monitor

QUESTIONS

64 For agent or broker use only. Not for use with the public.