An Analysis of Health Insurance Premiums Under the Patient ...

1

Navigating Health Care Reform Leading Age Delta Region Meeting

Presented by Erika James Oct. 9, 2013 Erika James Vice President, Employee Benefits Phone: 925-407-0416 Email: [email protected]

2

Table of Contents

▲ State of the Union: Healthcare Trends

▲ Understanding the Affordable Care Act (ACA)

▲ Timeline and Compliance Checklists

▲ Plan Design Requirements / Provisions

▲ Employer Obligations

▲ Premium Tax Credits and Cost Sharing Subsidies

▲ Health Insurance Exchanges

▲ Emerging Healthcare Models for Employers and Employees

▲ Additional Resources

____ __ ____ _____ ____ ______ _______

3

State of the Union: Healthcare Trends

4

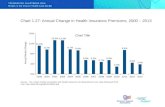

$508

$999

$2,875

$4,885

2003 2013

ER Contribution EE Contribution

$3,383

$5,884 74% Total Premium Increase

97% EE Contribution Increase

Average Annual Health Insurance Premiums and Worker Contributions

for Single Coverage

5

$2,411

$4,565

$6,657

$11,786

2003 2013

ER Contribution EE Contribution

$9,068

$16,351

80% Total Premium Increase

89% EE Contribution Increase

Average Annual Health Insurance Premiums and Worker Contributions

for Family* Coverage

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2013 * Family coverage is defined as health coverage for a family of four.

6

▲ Since 2002, premiums in California rose by 169.7%, more than five times the 31.5% increase in the state's overall inflation rate

▲ Average 2012 annual premiums for single and family coverage in California were 16% and 6% higher than national respectively

▲ Proportion of CA employers offering coverage has declined significantly over the last decade, from 71% in 2002 to 60% in 2012

— Higher offering rates are associated with larger firms, firms with higher wages, and firms with fewer part-time workers

$6,540

$16,632

$5,616

$15,744

Single Coverage Family Coverage

CA US

Source: California HealthCare Foundation/NORC California Employer Health Benefits Survey, 2012

____ __ ____ _____ ____ ______ _______

7

Understanding the Affordable Care Act (ACA)

8

Understanding ACA… Easy as 1, 2, 3!

1. Comply Implement all ACA

health coverage and associated requirements

2. Understand How is ACA/HCR

supposed to work?

How will it change coverage marketplaces (Individual, Group, Public Programs)?

Where could it fail?

What does it mean for your organization?

3. Strategize A compliance

strategy is not a HCR/health care management strategy

Don’t take your eye off the cost

Where does your organization want to be: reactive vs. proactive?

9

Understanding ACA New Industry Taxes and Fees

▲ Comparative Effectiveness Research Fee (PCORI) — $1 PMPY (due July 2013) for plans ending on or after

10/1/12

▲ Health Insurance Industry Fee — $8 billion in 2014 — +$100 billion over 10 years — Expected to increase premiums 2%-2.5% in 2014, 3%-4%

in later years

▲ Reinsurance Assessment Fee — Program to stabilize carriers in individual market from

“guarantee issue” risk — 2014―fully insured & self-insured plans — Approx. $60 PMPY

▲ Employer Excise (“Cadillac”) Tax — 2018―Employer Plan Sponsors with coverage costs

exceeding threshold are responsible for a 40% excise tax on the difference

$10,200 single/$27,500 family — Estimates are that many employer plans will exceed the

threshold based on current health care costs and industry norm trends

10

Understanding ACA Implications by Financing Options

FULLY INSURED PLANS SELF-INSURED PLANS

• Carriers in defensive position due to plethora of ACA-related requirements & changes

• Guarantee Issue & No Pre-Ex for Ind./Small Group markets

• Weak Individual Mandate

• Modified Community Rating for Ind./Small Group markets

• Required Coverage of Essential Health Benefits for Ind./Small Group Plans

• Essential Health Benefits cannot have dollar limits and are defined by State’s BM Plan

• MLR Requirements

• Insurance Industry Fee = +2%-2.5% (2014), +3%-4% (later yrs.)

• Plan sponsors are not subject to community rating rule s and other carrier requirements

• Elimination of taxes and carrier pass through fees

• Essential Health Benefits not required, but if covered cannot have dollar limits

• Plan sponsor defines EHB

• Plan sponsors are able to customize plans to meet specific needs – Value -based plan design – Custom provider networks – Direct return on successful population health

management strategies / claims impact

• Employers of various sizes embracing self-insured strategies

11

Understanding the ACA How is it supposed to work?

PROVIDE ACCESS FOR 48 MILLION UNINSURED /

IMPROVE ACCESS FOR OTHERS STRENGTHEN COVERAGE STABILIZE COVERAGE COSTS

• All individual coverage is guarantee issue/no pre-ex, no medical UW

• Establishes Health Insurance Exchanges for individuals/ small businesses

• Employer mandate & child eligibility to age 26

• Insurance Affordability Programs

Medicaid expansion, federal premium tax credits & subsidies

• “Minimum Essential Coverage” Plan Requirements

• Individual / Small Group Coverage Reforms

Essential Health Benefits requirement with no annual/ lifetime dollar limits

100% preventive care requirement

Deductible limits

Out-of-pocket limits

Actuarial value 60%

• Large Group / Employer Coverage Reforms

No annual / lifetime limits on Essential Health Benefits

100% preventive care

Out-of-pocket limits

Minimum value 60%

• Phase out of most Limited Medical Plans

• “Individual Coverage Requirement” (Individual Mandate)

• New Individual/ Small Group Market Rating Reform

“Modified Community Rating” & “Single risk pool” requirements

• Reinsurance, Risk Corridors & Risk Adjustment Programs to Stabilize Individual/Small Group Markets

• New Medical Loss Ratio Requirements for Carriers

• Some provisions allowing individual coverage costs to be tied to health/ wellness factors

12

Understanding the ACA Will it work?

PROVIDE ACCESS: STRENGTHEN COVERAGE: STABILIZE COVERAGE COSTS:

• Will guarantee issue/no pre-ex requirement cause huge carrier losses? Who will buy?

• Will health insurance exchanges be ready, much less work?

• Will employers exit?

• Will the U.S./ state fiscal situation lead to a scaling back of Insurance Affordability Programs?

• Will new coverage requirements lead to spiraling costs?

• Individual/Small Group coverage requirements are staggering for carriers

Essential Health Benefits

60% Minimum Actuarial Value

Exchange Requirements―Qualified Health Plans

• Will the Individual Mandate be sufficient enough to motivate younger uninsured individuals to buy and maintain coverage?

$95 (2014)

$695 (2016)

• Will new Individual/ Small Group Market Rating Reform work or throw insured market into turmoil?

GI / No pre-ex ― carriers must take all comers

Modified community rating ― changes the playing field

Reinsurance, Risk Corridors & Risk Adjustment Programs ― unsubstantiated

13

Understanding the ACA Implications by Financing Options?

FULLY INSURED PLANS SELF-INSURED PLANS

• Carriers in defensive position due to plethora of ACA-related requirements & changes

• Guarantee Issue & No Pre-Ex for Ind./Small Group markets

• Weak Individual Mandate

• Modified Community Rating for Ind./Small Group markets

• Required Coverage of Essential Health Benefits for Ind./Small Group Plans

• Essential Health Benefits cannot have dollar limits and are defined by State’s BM Plan

• MLR Requirements

• Insurance Industry Fee = +2%-2.5% (2014), +3%-4% (later yrs.)

• Employers of various sizes embracing self-insured strategies

• Elimination of taxes and carrier pass through fees

• Essential Health Benefits not required but if covered cannot have dollar limits

• Plan sponsor defines EHB

• Plan sponsors are able to customize plans to meet specific needs – Value -based plan design – Custom provider networks – Direct return on successful population health

management strategies / claims impact

• Stop-loss markets are responsive and competitive (down market)

____ __ ____ _____ ____ ______ _______

14

Timeline & Compliance Checklists

15

Affordable Care Act Implementation Timeline

2010 2011 2012 2013 2014 2015 2018 Small Business Tax

Credits Funding for Small Business Wellness

Programs

Summaries of Benefits and

Coverage

FSA Limits 90-Day Max Waiting Period

60-Day Max Waiting Period CA

Small Group

Employer Mandate-Play or Pay

Cadillac Tax

Adult Dependent Coverage

Medical Loss Ratio Rebates

Medicare Tax Increase

Individual Mandate Automatic Enrollment

No Lifetime Dollar Limits

No Part D Deduction Health Insurance Exchanges

New Nondiscrimination

Rules

Restrictions on Annual Dollar Limits

PCORI Fee Community Rating-Small Group &

Individual

Employer Reporting Requirements*

No Rescissions Except Fraud

Health Insurance Exchange

Notifications

Guaranteed Issue / No Pre-Ex

No Pre-existing Conditions for

Children

No Annual Dollar Limits

No OTC Reimbursement from FSA, HSA

Enhanced Wellness Incentive/ Penalty

External Review Procedures

Cost Sharing & Ded. Limits

Full Coverage of Preventive Services

*2016 requirement for 2015 plan year

16

Employer Compliance Checklist Notices and Disclosures

Notice/Disclosure Plans Impacted Effective Date GF/non-GF

Notice of Exchange* Small/ Large Employer Oct. 1, 2013 Both

Summary of Benefits and Coverage Small/ Large Employer

First OE and plan years beginning on or after

9/23/12 Both

60-Day Notice of Plan Changes Small/ Large Employer SBC plan year effective

date Both

Notice of Rescission Small/ Large Employer Plan years beginning on

or after 9/23/10 Both

Statement of Grandfathered Plan Status Small/ Large Employer Plan years beginning on

or after 9/23/10 GF

Notice of Patient Protections and Selection of Providers

Small/ Large Employer Plan years beginning on

or after 9/23/10 Non-GF

* No penalty for non-compliance

17

Employer Compliance Checklist Plan Design & Coverage Requirements ― in Effect

Requirements Effective Now Plans Impacted Effective Date plan years beginning

on or after:

GF/ non-GF

Dependent Coverage to Age 26 Small/ Large Employer 9/23/10 Both

No Lifetime Dollar Limits/Dollar Limit Restrictions on Annual Limits

Small/ Large Employer 9/23/10 Both

No Rescissions (except for fraud and material misrepresentations)

Small/ Large Employer 9/23/10 Both

No Pre-Existing Condition Exclusions for Children Small/ Large Employer 9/23/10 Both

No reimbursement for OTC Medicine and Drugs (w/o a prescription)

Small/ Large Employer 1/1/11 Both

No Cost-sharing for Preventive Care Services Small/ Large Employer 9/23/10 Non-GF

Additional Preventive Care Services for Women Small/ Large Employer 8/1/12 Non-GF

Requirements for Internal Claims and Appeals and External Review

Small/ Large Employer 9/23/10 Non-GF

Patient Protections and Selection of Providers (PCP, OB/GYN, ER)

Small/ Large Employer 9/23/10 Non-GF

$2,500 Employee Contribution Limit to Health FSAs Small/ Large Employer 1/1/13 Both

18

Employer Compliance Checklist Plan Design & Coverage Requirements ― 2014

2014 Requirements Plans Impacted Effective Date plan years beginning

on or after:

GF/ non-GF

No Pre-Existing Condition Limitation Small/ Large Employer 1/1/14 Both

No Annual Dollar Limits on Essential Health Benefits

Small/ Large Employer 1/1/14 Both

90-day Waiting Period Limit 60-Day Waiting Period Limit for CA Small Groups

Small/ Large Employer 1/1/14 Both

Deductible Limits for Health Plans Small Employer 1/1/14 Non-GF

Out-of-Pocket Max Limits for Health Plans Small/ Large Employer 1/1/14 Non-GF

Required Coverage of Clinical Trials Small/ Large Employer 1/1/14 Non-GF

Non-discrimination for Fully Insured Plans* Small/Large Employer Delayed Non-GF

Required Coverage of Essential Health Benefits Small Employer 1/1/14 Non-GF

* Regulations pending or not final

19

Employer Compliance Checklist Employer Obligations

Provision Plans Impacted Effective Date

W-2 reporting Large Employer** 2013 for 2012 pay year

Comparative Effectiveness Research Fee Small/ Large Employer 2013

Transitional Reinsurance Fees Small/ Large Employer 2014

Additional Medicare Tax N/A 2013 pay year

Employer Penalties for Not Offering Coverage- Section 4980H “Play or Pay”*

Large Employer Delayed until 1/1/15

Automatic Enrollment* Large Employer unknown

Employer Health Plan Reporting* Large Employer Delayed until 1/1/15

* Regulations pending or not final **Required if ≥ 250 EE W-2’s issued

20

Employer Compliance Checklist Miscellaneous

Provision Plans Impacted Effective Date plan years beginning

on or after:

GF/ non-GF

Non-discriminatory Health-contingent Wellness Programs

Small/Large Employer 1/1/14 Both

MLR Rebate Participant Distributions (if any)

Small/Large Employer Fully Insured

8/1/12, 8/1/13, 9/1/14 Part. Distributions w/in

90 days Both

New Notice of HIPAA Privacy Practices Self-Insured Plans 9/23/13 Both

21

“Play or Pay” Section 4980H Basics

Large employers are required to offer coverage to full-time employees (and dependents*) or pay a penalty/excise tax

Defines who is a full-time employee and when they must be offered coverage

• Eligibility Definition

• Eligibility Determination

• Waiting Period

Defines acceptable Employer Coverage as that which has “Minimum Value” and is “Affordable”

*Employers are required to offer coverage to dependent children; however, employers are not required to contribute to coverage for dependent children

22

“Play or Pay” Section 4980H Large ER Full-Time EE Determination

▲ Full-time = 30 hours/week average (130 hours/month)

— Hours of service include PTO, vacation, sick time, leave etc.

— Hours of service must be “reasonably” calculated for certain positions

▲ If EE is expected to be full-time at the time of hire, they are

full-time for the purposes of 4980H

▲ What about variable hour and seasonal EEs?

— IRS acknowledges practical challenges in determining full-time status

on a monthly basis and is providing a more flexible approach

▲ IRS Safe Harbor allows for ERs to use a look back approach

(“Measurement Period”) to determine full-time status for

subsequent predetermined “Stability Period”

23

4980H Full-Time EE Determination Ongoing Employees

▲ ERs define Standard Measurement Period (SMP) to determine if ongoing EEs were FT (30 hrs. per service week/130 hrs. per mo.)

— SMP can range from 3 to 12 months

▲ If ongoing EE was FT during the SMP, they must be considered FT for the entire Stability Period (SP)

— Formula used is total hours worked in SMP divided by months in the MP ≥ 130 hours

— If ≥ 130 hours, ER must offer EE coverage for entire SP or face penalty

— SP must be at least 6 months, but not shorter than the SMP

▲ If ongoing EE was not FT during the SMP, they would not be considered FT for the entire SP

— SP cannot be longer than SMP

▲ Administrative Period (AP) allowed (up to 90 days) to calculate FT status; however, AP cannot create a “gap if covered”

▲ Allows different MPs & SPs to be used for different EE classifications (hourly vs. salary, CBA/non-CBA, different states)

24

4980H Full-Time EE Determination New Variable Hour/Seasonal EEs

▲ ERs may use same look-back (Measurement Period)/ Stability Period approach with a few differences

▲ “Initial Measurement Period” (IMP) allowed for any new Variable Hour EE if ER cannot reasonably determine if they are expected to work more than 30 hours per week

— After Date of Hire, IMP can range from 3 to 12 months

▲ If Variable Hour EE was FT during the IMP, the EE must be considered FT for the entire Stability Period (SP)

— ISP must be at least 6 months, but not shorter than the IMP

▲ If Variable Hour EE was not FT during the IMP, they would not be considered FT for the entire SP

— SP cannot be longer than the IMP + 1 month and cannot exceed the end of the SMP + AP (90 days)

▲ Administrative Period (AP) allowed (up to 90 days) on both front end and/or back end of IMP to calculate FT status

— However, the IMP and AP together cannot extend beyond last day of the first month beginning on or after the anniversary of the EE’s start date

▲ Once Variable Hour EE has been employed for one full SMP, they must be retested as a ongoing EE

25

4980H Full-Time EE Determination Example

26

ACA Employer Penalties

▲ In general, failure to comply can result in excise tax under the Internal Revenue Code or penalties under PHSA or ERISA, depending on which of these statutes is applicable to the employer – $100/day “with respect to each individual

to whom such failure relates”

– Maximum for unintentional failure is the lesser of: • 10% of the total spent of the group health

plan for preceding year; or

• $500,000

27

DOL Plan Audits

▲ DOL Plan Audit Program is underway

▲ Because there is no history of audits, health and welfare plan compliance is often lacking

▲ Auditors looking at historic areas of non-compliance in plan documentation

▲ Review also encompasses ACA-required provisions

____ __ ____ _____ ____ ______ _______

28

Plan Design Requirements and Select Provisions

29

Cost-sharing Limitations

Deductible Limits

• $2,000/$4,000

• Non-GF Small Group Plans

Cost Sharing

Limits

• Pegged to IRS CDHP OOP Limits ($6,250/$12,500 for 2013)

• Non-GF Individual, Small Group Large Group, and Self-insured Plans

30

Essential Health Benefits (EHB) Basics

▲ Fully insured, non-GF small group and individual plans must cover all EHB w/o an annual or lifetime dollar caps on EHB

▲ Fully insured large group and self-insured plans are not required to cover EHB, but if they do so are prohibited from imposing any annual or lifetime dollar caps on EHB

▲ ACA-defined 10 EHB Categories:

1 Ambulatory patient

services

2 Emergency services

3 Hospitalization

4 Mental health and substance abuse

disorders/behavioral health treatment

5 Maternity and newborn care

6 Prescription drugs

7 Rehabilitative

services/devices

8 Laboratory services

9 Preventive and

wellness services and chronic disease

management

10 Pediatric services,

incl. oral and vision care

31

Essential Health Benefits Defining Covered Items & Services

▲ DHHS authorized states to define EHB through establishment of a benchmark plan

▲ States may choose from four existing health plan options for benchmark plan to establish the covered items/services within each EHB category : • Largest plan by enrollment in any of the three largest small group products • Any of the largest three state employee health benefit plans by enrollment • Any of the largest three federal employee health plan options by

enrollment • Largest insured commercial non-Medicaid HMO operating in the state

▲ State mandates associated with the selected benchmark plan will be included in the EHB package

▲ If State does not select a benchmark plan, default option will be largest small group product in the state

32

Essential Health Benefits Plans Effected ▲ Effective for plans beginning on or after 1/1/14

* Large group = 51+ in all states currently (will be 101+ in all states as of 1/1/16)

Plan/Funding Type

Grandfather Status

Must Cover EHBs?

Defines EHB Annual Lifetime Limits on EHB

Permitted?

Individual and Fully Insured Small Group

Non-GF Yes State No

GF No State No

Fully Insured Large Group

Non-GF No Employer No

GF No Employer No

ASO Small Group and Large Group

Non-GF No Employer No

GF No Employer No

33

Other Plan Design & Coverage Requirements ▲ Contraceptive Services Requirements

• Exemptions for Religious Employers

• Accommodations for Religious Affiliated Organizations

▲ 90-day Waiting Period Limit

▲ Required Coverage for Participants in Clinical Trials • Cannot deny a qualified individual the right to participate in an approved

clinical trial

• Cannot limit or impose additional conditions on coverage of routine patient costs for items and services furnished in connection with the approved clinical trial

• Cannot discriminate against a qualified individual based on participation in an approved clinical trial

▲ Non-discrimination Rules for Fully Insured Health Plans • Expected to closely follow IRS Section 105H Rules for self-insured plans

34

Non-discriminatory Wellness Programs Proposed Regulations

▲ Explains differences in types of incentive based wellness programs (participatory vs. health factor)

▲ Increases permissible incentive (penalty) for health factor contingent wellness programs

▲ 2014―permissible incentive increased to 30% of cost of coverage (up to 50% for tobacco cessation standards)

▲ Health factor contingent wellness programs must meet revised non-discrimination requirements

— Reasonably designed — Include annual opportunity to comply — Provide “reasonable alternative” standard for participants

• Not clear if “reasonable alternative” is medically driven

▲ Aggressive programs must comply with ADA, HIPAA & GINA

▲ Wellness programs that are not contingent on a health factor have more flexibility w/ incentives

____ __ ____ _____ ____ ______ _______

35

Employer Obligations

36

“Play or Pay” Section 4980H Basics

Large employers are required to offer coverage to full-time employees (and dependents*) or pay a penalty/excise tax

Defines who is a full-time employee and when they must be offered coverage

• Eligibility Definition

• Eligibility Determination

• Waiting Period

Defines acceptable Employer Coverage as that which has “Minimum Value” and is “Affordable”

*Employers are required to offer coverage to dependent children; however, employers are not required to contribute to coverage for dependent children

37

“Play or Pay” Section 4980H Large Employer Determination ▲ Large Employer

• Defined as employer that averaged at least 50 full-time employees during prior calendar year Transition rule 2014―employers may

use any consecutive 6 mo. period from 2013

• To calculate full-time employees: Add number of full‐time employees

(30 or more hours a week) and number of full‐time equivalent employees (FTEs)

Divide total monthly part time hours by 120

▲ Must include all full‐time employees and FTEs in “controlled group” to determine if Large Employer (but penalty applies on member‐by-member [separate tax ID] basis)

38

“Play or Pay” Section 4980H Large ER Full-Time EE Determination

▲ Full-time = 30 hours/week average (130 hours/month) • Hours of service include PTO, vacation, sick time, leave etc.

• Hours of service must be “reasonably” calculated for certain positions

▲ If employee is expected to be full-time at the time of hire then they are full-time for the purposes of 4980H

▲ What about variable hour and seasonal employees? • IRS acknowledges practical challenges in determining full-time status

on a monthly basis and is providing a more flexible approach

▲ IRS Safe Harbor allows for employers to use a look back approach (“Measurement Period”) to determine full-time status for subsequent predetermined “Stability Period”

39

“Play or Pay” 4980H Large Employer Requirements

▲ Must offer Minimum Essential Coverage to all full-time employees

– Employer subject to a penalty for failure to do so if any single full time employee receives federal premium tax credit (“assistance”) to purchase coverage through a qualified exchange

– $2,000 penalty for each full-time employee (minus first 30 EEs)

▲ Minimum Essential Coverage must provide “Minimum Value” and be “Affordable”

— Employer is subject to a penalty of the lesser of the $2,000 coverage penalty OR $3,000 for each full-time employee receiving a federal premium tax credit (assistance) to purchase coverage through a qualified exchange

▲ Employer penalties are triggered if employee(s) receive federal premium tax credit (assistance) for coverage through a qualified exchange ▲ Only apply to full time employees (defined as those working

30 hours per week or more)

40

“Play or Pay” Section 4980H Employer Requirements

Potential Annual Penalties Beginning in 2015 for Large Employers Applies to For-profit and Nonprofit Organizations

Not a large employer (Fewer than 50 full-time equivalent employees)

Large employer: 50 or more full-time equivalent employees

Does not offer coverage Does not offer coverage Offers coverage

A No full-time

employees receive credits for

exchange coverage

B 1 or more full-time employees receive

credits for exchange coverage

C No full-time

employees receive credits for

exchange coverage

D 1 or more full-time employees receive

credits for exchange coverage

No penalty No penalty Number of full-time employees minus 30 multiplied by $2,000

No penalty Lesser of: • Number of full-time

employees minus 30, multiplied by $2,000.

• Number of full-time employees who receive credits for exchange coverage, multiplied by $3,000.

41

4980H Full-Time EE Determination Ongoing Employees ▲ Employers define Standard Measurement Period (SMP)

to determine if ongoing employees were full-time status (30 hrs. per service week/130 hrs. per mo.) • SMP can range from 3 to 12 months

▲ If ongoing employee was full-time status during the SMP, then they must be considered full-time status for the entire Stability Period (SP) • Formula used is total hours worked in SMP divided by months

in the MP ≥ 130 hours • If ≥ 130 hours, employer must offer EE coverage for entire SP

or face penalty • SP must be at least 6 months but not shorter than the SMP

▲ If ongoing employee was not full-time status during the SMP, then they would not be considered full-time status for the entire SP • SP cannot be longer than SMP

▲ Administrative Period (AP) allowed (up to 90 days) to calculate FT status; however, AP cannot create a “gap if covered”

▲ Allows different MPs & SPs to be used for different employee classifications (hourly vs. salary, CBA/non-CBA, different states)

42

4980H Full-Time EE Determination New Variable Hour/Seasonal EEs

▲ Employers may use same look-back (Measurement Period)/ Stability Period approach with a few differences

▲ “Initial Measurement Period” (IMP) allowed for any new Variable Hour Employee if employer cannot reasonable determine if they are expected to work more than 30 hrs. per week • After Date of Hire, IMP can range from 3 to 12 months

▲ If Variable Hour Employee was full-time status during the IMP, then the EE must be considered full-time for the entire Stability Period (SP) • ISP must be at least 6 months but not shorter than the IMP

▲ If Variable Hour Employee was not full-time status during the IMP, then they would not be considered full-time status for the entire SP • SP cannot be longer than the IMP + 1 month and cannot

exceed the end of the SMP + AP (90 days) ▲ Administrative Period (AP) allowed (up to 90 days) on both front

end and/or back end of IMP to calculate the full-time status • However, the IMP and AP together cannot extend beyond

last day of the first month beginning on or after the anniversary of the EEs start date

▲ Once Variable Hour Employee has been employed for one full SMP they must be retested as a ongoing employee

43

Large ER Requirements 4980H Minimum Value Determination ▲ Minimum Value―Plan’s share of the total allowed costs of benefits

provided under the plan ≥ 60%

▲ Employers may select from three methodologies for determining Minimum Value of Plan • Minimum Value Calculator

• Plan Design Checklist Safe Harbor

• Certification by certified actuary

▲ Employer HSA contributions & HRA contributions newly made available count toward Plan’s Minimum Value

▲ 60% Minimum Value requirement based only on Essential Health Benefits*

* Note: Large group and self-insured employer plan sponsors are not required to cover specific EHB and it appears MV

calculation is based all covered benefits

44

Large ER Requirements 4980H Affordable ER Coverage Determination

▲ ACA and Subsequent Federal Regulations/Guidance define “affordable” employer coverage as: • Single (Self-only) coverage costing employee no more than 9.5% of

income

• IRS Safe Harbor allows employers to base affordability on employee W-2 income. For example:

FT Employee earning $20,000 year;

Employer could not charge EE more than $1,900 year ($158 mo.) for Single (Self-only) coverage

▲ Employees w/o access to affordable ER coverage may be eligible for federal Premium Tax Credits & Subsidies (Households @ 100%-400% FPL)

45

“Play or Pay” Section 4980H Miscellaneous

▲ Under the proposed regulations’ transition relief, solely for purposes of stability periods beginning in 2014, employers may adopt a transition measurement period that: • Is shorter than 12 months, but not less than 6 months long; and

• Begins no later than July 1, 2013, and ends no earlier than 90 days before the first day of the first plan year beginning on or after Jan. 1, 2014.

▲ Proposed regulations provide allowances to use standard payroll periods for the purposes of Measurement Period calculations with exception

46

“Play or Pay” Section 4980H Miscellaneous

▲ Authorized Safe Harbor / “95% Rule”: • Employer complies with 4980H if it

offers Minimum Essential Coverage to at least 95% of full-time employees (and dependents)

▲ Dependent coverage requirement: Must provide coverage to children of full-time employees under age 26 • No penalty in 2014 if employer takes

steps toward compliance

▲ Fiscal year plans: Employers will not be subject to 4980H penalties until the first day of the 2015 plan year.

▲ Common Law Employer standard used to determine employer -employee relationship

____ __ ____ _____ ____ ______ _______

47

Premium Tax Credits and Cost Sharing Subsidies

48

Premium Tax Credits & Subsidies Why They Matter to Employers

▲ Premium Tax Credits and Cost-Sharing Subsides are available to households with low to moderate incomes (100%-400% FPL) if they meet eligibility requirements

▲ Low- to middle-income employees (households) may have more affordable coverage options through a Public Exchange due to these Insurance Affordability Programs

▲ Premiums Tax Credits

– Households w/ incomes b/t 100%-400% FPL eligible for advanceable tax-credits capping premiums for a 70% “Silver Plan” at 2% to 9.5% of modified adjusted gross household income

• 133%-400% threshold in states that enact Medicaid expansion

▲ Cost Sharing Subsides

– Households w/ incomes b/t 100% to 250% FPL are eligible for additional cost sharing subsides

• Increase the actuarial value of the Silver Plans to greater than 70%

49

Premium Tax Credits/Subsidies Why They Matter to Large Employers ▲ If employee is offered affordable

coverage by employer, they are not eligible for Premium Tax Credits/ Subsidies through Public Exchange for both self/dependents

▲ If employer does not offer affordable coverage, EEs may be eligible for Premium Tax Credits/ Subsidies for self/dependents

▲ The eligibility requirements for Premium Tax Credit/Subsidy appear to create an incentive for employers to make coverage less affordable for certain lower-wage employees so they can qualify

50

Premium Tax Credit Cost Analysis EE w/ Family Example

ER EE

EE 395.69$ 336.34$ 59.35$

EE+Sp 791.39$ 474.83$ 316.55$

EE+Ch 791.39$ 474.83$ 316.55$

Fam 1,187.08$ 712.25$ 474.83$

ER EE

EE 395.69$ 218.62$ 54.84$

EE+Sp 791.39$ 308.64$ 292.50$

EE+Ch 791.39$ 308.64$ 292.50$

Fam 1,187.08$ 462.96$ 438.74$

Family Income FPL % of income Cap

35,137 150% 4%

46,850 200% 6.3%

70,275 300% 9.5%

93,700 399% 9.5%

Cost w/o affordable ESI ER EE EE Savings 192.78$

250.00$ 245.96$ ER Savings 212.96$

EE Unaffordable Threshold (9.5%)

278.17$

370.90$

556.34$

741.79$

Cost ESI (80/20 Plan)

Tax Adjusted Cost ESI

Premium Cap (Mo.)

117.12$

EE+Child

245.96$

556.34$

741.79$

51

Tax Credits/Subsidies Why They Matter to Individuals PPACA Premium and Cost-Sharing Subsidy

PREMIUM SUBSIDY COST-SHARING SUBSIDY³

INCOME (%PPL)

ANNUAL INCOME (BASED ON TRENDED

2014 FPL¹)

PREMIUM PERCENT OF INCOME CAP²

MONTHLY MAXIMUM PREMIUM

REDUCTION IN MAXIMUM OOP LIMIT

REDUCED MAXIMUM ANNUAL LIMITATION OF COST SHARING (2014)

REQUIRED ACTUARIAL VALUE OF

BENEFIT PLAN

<133% $15,455 2.00% $26 66.70% $2,250 94%

150% $17,430 4.00% $58 66.70% $2,250 87%

200% $23,240 6.30% $122 20.00% $5,200 73%

250% $29,050 8.05% $195 N/A $6,400⁴ 70%

300% $38,860 9.50% $276 N/A $6,400* 70%

400% $46,480 9.50% $386 N/A $6,400* 70%

1. Based on 2012 100% FPL of $11,170 for a single individual, trended two years at 2% annual trend (rounded). 2. Premium tax credit percentages are for 2014 and will be indexed in the future. 3. Excluding cost-sharing reductions for Indians with household income not more than 300% FPL of proposed rule for cost-sharing reductions 4. HHS estimated 2014 maximum annual limitation on cost sharing. For future years, will be based on IRS dollar limit on cost sharing for high-deductible plans..

52

Tax Credits/Subsidies Considerations ▲ Most employers offer affordable self-only coverage, would they

adjust contributions to allow certain workers eligibility for premium tax credits and subsidies?

▲ Is it appropriate for an employer to drive lower wage workers to the exchanges to qualify for these programs? • Sustainability • Public relations aspect • Will increased pay be required for those who don’t qualify for these

programs be required to offset higher employee premium contributions

▲ Many questions and uncertainties exist about these insurance affordability programs

▲ Will the premium tax credits/subsidies be scaled back in 2014 and beyond?

▲ Legal challenges to premium tax credits/subsidies through federal exchanges?

____ __ ____ _____ ____ ______ _______

53

Health Insurance Exchanges

54

Qualified Health Insurance Exchanges

Medicaid & CHIP Insurance Affordability Programs: Subsidized

Coverage - Premium Tax Credits & Cost Sharing

Subsidies

Unsubsidized Coverage SHOP/Small Group ER Coverage

< 100%/133% FPL (state option) including adults

100%/133% - 400% FPL w/out affordable ESI

> 400% FPL ERs < 50/100 (state option)

Carriers Products Plan Types Actuarial Value

Cigna Aetna Kaiser BC/BS

Etc.

HMO PPO POS

Co-Op Plans State Basic Health Plan

Platinum Gold Silver

Bronze Catastrophic Plan (≤30)

90% 80% 70% 60% N/A

Product Choices

Programs

Exchanges

Federal State Partnership (Federal + State)

55

Health Insurance Exchange State Progress & Federal Defaults

____ __ ____ _____ ____ ______ _______

56

Emerging Healthcare Models for Employers and Employees

57

Emerging Models Employer/Employee Health Coverage

POPULATION HEALTH & RISK MANAGEMENT

MARKETPLACE APPROACH

• Self-insured models

• Wellness programs that actually achieve behavior change

• Incentives and penalties (ACA increases wellness allowance to 30%)

• Value-based benefit design

• Multi-purchasing Coalitions, Value-Based Networks, Patient-Centered Medical Home Models

– Direct contracting for larger self-insured employers

• Market alternatives exist

– GI & No Pre-Ex

– Exchanges (Public & Private)

• Defined Contribution Model

• Reallocation of compensation & benefits spend based on best available options

– Leverage Premium Tax Credits & Subsides

• Stability of non-large group market in question!

58

Guess What? It’s Still About Rising Health Care Costs

59

Health Care Strategy Fundamentals

Employee Education/ Communication Campaign on Health Care Costs & Quality!

Population Health Management

Delivery System Strategies

• Total Rewards Conversation

• Value-Based Benefit Design

• Keep healthy members healthy!

• Keep those with costly health issues compliant and from getting worse!

• Incentives/ Penalties

• Carrier programs are very limited/ that’s not enough

• Population Health Management within your organization is up to you!

• Centers of Excellence

• Focus/ Narrow Networks

• Pay for Performance Initiatives

• Patient-Centered Medical Home/ ACO’s

• On-site Clinics

• Tele-Medicine

60

Defined Contribution Approach Through Public/Private Exchange DEFINED CONTRIBUTION

SUBSIDY INSURED PLAN OFFERINGS FOR PARTICIPANTS

THROUGH EXCHANGE (Public or Private)

1 2 3

Health Care Credit Standardized Plans Competing Carriers

Employer makes a defined contribution per month

Bronze -60% Silver-70% Gold-80%

Platinum-90%

Aetna Cigna

United Kaiser

▲ Many questions remain about this model ▲ Group or Individual products ▲ Employer tax deduction/employee tax

deduction status in question ▲ What does it do to impact underlying health

care costs?

61

Modeling Coverage Scenarios Impact on Employer & Employee Costs Potential Employer Scenarios Employer Costs Employee

Expenses

Status Quo • Maintain current ER plan • Continue to treat all benefit-eligible EEs the same • Employer costs are plan costs less EE contributions

Employer Plan

Cost-sharing

EE contributions

Encourage Exchanges for Certain EEs • Maintain current ER Plan for certain EEs • Steer EE’s to most cost-effective coverage source • Employer costs are combination of plan costs less EE

contributions, 4980H taxes/fees, possible increased EE compensation for higher-income EEs (+400% FPL)

Employer Plan Cost-sharing

EE contributions

PPACA Fees Subsidies

Exit Completely • Terminate current ER plan • Increase EE compensation or use “Defined Contribution”

strategy & allow EEs to purchase individual coverage through Public Exchange, Private Exchange, or off exchange

• Employer costs are combination of 4980H taxes/fees & defined contribution/increased EE compensation

Increased Compensation

Cost-sharing

PPACA Fees Subsidies

____ __ ____ _____ ____ ______ _______

62

Additional Resources

63

Additional Resources

▲ Kaiser Family Foundation www.kff.org

▲ Federal Government HCR Website www.healthcare.gov

▲ Health Insurance Tax Credit Calculator http://healthreform.kff.org/subsidycalculator.aspx

▲ California Health Insurance Exchange Website www.CoveredCa.com Contact: Erika James, Vice President, Employee Benefits Ascension Benefits & Insurance Solutions 925-407-0416 [email protected]

64

We appreciate the work you do …

Thank You!