Natural Hedging Using Multi-population Mortality...

67

Natural Hedging Using Multi-population Mortality Forecasting Models by Shuang Chen B.Sc., Nankai University, 2011 Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of Master of Science in the Department of Statistics and Actuarial Science Faculty of Science © Shuang Chen 2014 SIMON FRASER UNIVERSITY Fall 2014 All rights reserved. However, in accordance with the Copyright Act of Canada, this work may be reproduced without authorization under the conditions for “Fair Dealing.” Therefore, limited reproduction of this work for the purposes of private study, research, criticism, review and news reporting is likely to be in accordance with the law, particularly if cited appropriately.

Transcript of Natural Hedging Using Multi-population Mortality...

Natural Hedging Using

Multi-population Mortality Forecasting Models

by

Shuang Chen

B.Sc., Nankai University, 2011

Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of

Master of Science

in the

Department of Statistics and Actuarial Science

Faculty of Science

© Shuang Chen 2014 SIMON FRASER UNIVERSITY

Fall 2014

All rights reserved.

However, in accordance with the Copyright Act of Canada, this work may be

reproduced without authorization under the conditions for “Fair Dealing.”

Therefore, limited reproduction of this work for the purposes of private study,

research, criticism, review and news reporting is likely to be in accordance

with the law, particularly if cited appropriately.

APPROVAL

Name: Shuang Chen

Degree: Master of Science

Title: Natural Hedging Using Multi-population Mortality Fore-

casting Models

Examining Committee: Chair: Dr. Gary Parker

Associate Professor

Dr. Cary Chi-Liang Tsai

Senior Supervisor

Associate Professor

Simon Fraser University

Dr. Yi Lu

Supervisor

Associate Professor

Simon Fraser University

Dr. David Campbell

Internal Examiner

Associate Professor

Simon Fraser University

Date Approved: December 11th, 2014

ii

Partial Copyright Licence

iii

Abstract

No mortality projection model can capture future mortality changes accurately so

that the actual mortality rates are different from the projected ones. The movement

of mortality rates has oppositive impacts on the values of life insurance and annuity

products, which creates a chance of nature hedge for both life insurer and annuity

provider. A life insurer and an annuity provider can swap their life insurance and

annuity business for each other to form their own portfolios for natural hedge. This

project is mainly focused on determining the weights of a portfolio of life insurance

and annuity products by minimizing the variance of the loss function of the portfolio

to reduce mortality and longevity risks for each of the life insurer and the annuity

provider. Four Lee-Carter-based models are applied to model the co-movement

of two populations of life insurance and annuity insureds, and then determine the

weights for comparisons. The block bootstrap method, a model-/parameter-free

approach, is also adopted with numerical illustrations to compare the hedging per-

formances among the four models.

iv

I dedicate this thesis to my parents,

- who always support and cheer me up.

v

Acknowledgments

I would like to express my deepest appreciation to all those who supported and

guided me to complete this project. A special gratitude is given to my supervisor,

Dr. Cary Tsai, who provided me with patient guidance and valuable suggestions

that inspired me and helped me realize self-improvements throughout my two years

of studies in SFU. I will always be grateful to have the opportunity to learn new

ideas and conduct research under his supervision. Without his devoting time to

this project, I wouldn’t have completed the project. I hereby thank you for all your

time spent on guiding me.

Furthermore, I would also like to acknowledge with my great appreciation the

members of my project committee, Dr. Gary Parker, Dr. Yi Lu and Dr. David

Campbell. Thank you for reading my project with your valuable time and giving me

insightful comments and suggestions.

A special thank goes to the whole statistics and actuarial science department,

where I mastered more advanced knowledge that will benefit me forever. Thank

you to all the professors who have ever given me lectures and answered my ques-

tions. You helped me to fulfill a high level academic achievement.

Last but not least, I would like to take this opportunity to thank my family and my

friends who supported me and encouraged me whenever I felt confused and lost.

Especially, I would like to express my appreciation to my fellow graduate students,

Annie, Biljana, Elena, Fei, Huijing, Sabrina, Vicky and Yi, who brought me fresh

ideas and memorable moments during my study.

vi

Contents

Approval ii

Partial Copyright License iii

Abstract iv

Dedication v

Acknowledgments vi

Contents vii

List of Tables ix

List of Figures x

1 Introduction 1

1.1 Motivations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Outline . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

2 Literature Review 4

2.1 Mortality forecasting models . . . . . . . . . . . . . . . . . . . . . . . 4

2.2 Hedging of mortality and longevity risks . . . . . . . . . . . . . . . . 6

3 Introduction of Multi-population Models 9

3.1 Concepts and notations . . . . . . . . . . . . . . . . . . . . . . . . . 9

3.2 Multi-population models and constrains . . . . . . . . . . . . . . . . 11

3.2.1 Independent Lee-Carter model . . . . . . . . . . . . . . . . . 11

3.2.2 Joint-k Lee-Carter model . . . . . . . . . . . . . . . . . . . . 16

3.2.3 Co-integrated model . . . . . . . . . . . . . . . . . . . . . . . 20

vii

3.2.4 Augmented common factor model . . . . . . . . . . . . . . . 23

4 Application in Mortality Swap 28

4.1 Natural hedging and mortality swap . . . . . . . . . . . . . . . . . . 28

4.2 Numerical illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . 33

4.2.1 Assumptions and portfolios . . . . . . . . . . . . . . . . . . . 33

4.2.2 Robustness testing . . . . . . . . . . . . . . . . . . . . . . . . 36

5 Block Bootstrap Method 45

6 Conclusion 56

Bibliography 57

viii

List of Tables

4.1 the median of 50 optimal weights . . . . . . . . . . . . . . . . . . . . 37

4.2 comparisons of sample variances (×1023) and HE’s . . . . . . . . . 38

5.1 p-values for testing stationarity of {dx,t,i} . . . . . . . . . . . . . . . . 48

5.2 comparisons of sample variances (×1023) and HE’s (block bootstrap) 55

ix

List of Figures

3.1 cohort mortality sequence and period mortality sequence . . . . . . 10

3.2 kt,i against t . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3.3 95% predictive intervals on qx,2009+1,i for the Independent model . . . 15

3.4 95% predictive intervals on qx,2009+1,i for the joint-k model . . . . . . 19

3.5 95% predictive intervals on qx,2009+1,2 for the co-integrated and inde-

pendent models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

3.6 95% predictive intervals on qx,2009+1,i for the augmented common fac-

tor model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

3.7 mortality curve comparisons among models and actual rates . . . . 27

4.1 Mortality swap: minimizing V ar(LL) + V ar(LA) . . . . . . . . . . . . 30

4.2 Mortality swap: minimizing V ar(LL) . . . . . . . . . . . . . . . . . . 30

4.3 Mortality swap: minimizing V ar(LA) . . . . . . . . . . . . . . . . . . 30

4.4 age span [25, 100] and year span [1981, 2010] . . . . . . . . . . . . . 35

4.5 optimal weights for the independent and joint-k models . . . . . . . . 39

4.6 optimal weights for the co-integrated and augmented common factor

models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

4.7 variances after swap . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

4.8 simulated loss distributions using (wL+Al , wL+A

a ) . . . . . . . . . . . . 42

4.9 simulated loss distributions using (wLl , w

La ) . . . . . . . . . . . . . . . 43

4.10 simulated loss distributions using (wAl , w

Aa ) . . . . . . . . . . . . . . . 44

5.1 {dx,t,i} for x = 35, 45, 55, 65 . . . . . . . . . . . . . . . . . . . . . . . . 47

5.2 a circle diagram of dt,i’s . . . . . . . . . . . . . . . . . . . . . . . . . 49

5.3 simulated loss distributions using (wL+Al , wL+A

a ) . . . . . . . . . . . . 52

5.4 simulated loss distributions using (wLl , w

La ) . . . . . . . . . . . . . . . 53

5.5 simulated loss distributions using (wAl , w

Aa ) . . . . . . . . . . . . . . . 54

x

Chapter 1

Introduction

1.1 Motivations

Natural hedging is a strategy of hedging two risks responding oppositely to a

change in a common factor. Since life insurers and annuity providers face mor-

tality risk (the actual death probabilities are higher than expected) and longevity

risk (the actual survival probabilities are larger than expected), respectively, both

of them can adopt natural hedging by swapping a portion of their business between

each other to reduce mortality and longevity risks.

In this project, we would like to find the optimal swapped weights of life and

annuity business for a life insurer and an annuity provider, respectively, which min-

imize the variance of a loss function of the life insurer or the annuity provider, or

the sum of the variances of the two loss functions. To reach the goal, we need

some mortality models to forecast mortality rates for life insurance policyholders

and annuitants.

Since life insurance and annuities tend to be issued to different populations,

using the same mortality table to determine the premiums is inappropriate. Fur-

thermore, even though we use two different mortality tables for life insurance pol-

icyholders and annuitants, we cannot ignore the dependence between these two

populations. Generally speaking, two populations within a territory or country are

exposed to the same medical and environmental conditions. Therefore, the mortal-

ity rates for two populations might not be independent. In this project, two different

1

CHAPTER 1. INTRODUCTION 2

mortality tables and four multi-population mortality models are applied to forecast-

ing deterministic and stochastic mortality rates.

The deterministic mortality rates are used to determine the premiums of life and

annuity products, and the stochastic mortality ones are used to simulate the losses

of the life insurer and annuity provider. Then we calculate the sample variances

and sample covariance of the losses of the life insurer and annuity provider for ob-

taining the formulas of the optimal weights. A variance reduction ratio, called hedge

effectiveness, is proposed to compare the performances of hedging mortality and

longevity risks.

This project also carries out the robustness testing to study the sensitivity of

the weights and variances obtained from the simulated mortality rates. Finally, be-

cause all the results are derived based on the parametric mortality models, we are

not sure whether the assumed mortality model is the true one. To avoid the pa-

rameter and model risks, the model-free block bootstrap method is used to project

mortality rates. Then we redo the numerical results which are compared with those

produced by the parametric mortality models.

1.2 Outline

This project consists 5 chapters. Chapter 2 is a review of the previous research on

both mortality projection models and hedging of mortality and longevity risks.

In Chapter 3, some actuarial notations used in this project are provided, fol-

lowed by the introduction of four mortality projection models, the independent Lee-

Carter model, joint-k Lee-Carter model, co-integrated Lee-Carter model and aug-

mented common factor model, among which the last three can model the depen-

dent structure between the mortality rates for two populations. These models can

be used to forecast deterministic and stochastic mortality rates for both life insur-

ance policyholders and annuitants.

CHAPTER 1. INTRODUCTION 3

Chapter 4 focuses on natural hedging with mortality swap. In this chapter, three

pairs of optimal weights for swapping life insurance and annuity business are stud-

ied. Numerical illustrations using the U.S. mortality tables are exhibited. Also, the

robustness testing is conducted to test the sensitivity of the numerical results.

In Chapter 5, the model free block bootstrap method is introduced in details,

which is then applied to testing the results produced by the multi-population models

in Chapter 4.

Chapter 2

Literature Review

The two main parts of this project are mortality projection and natural hedge. The

first section will go through the articles about the mortality forecasting models and

the second section will review those about hedging of mortality and longevity risks.

2.1 Mortality forecasting models

Mortality projection is one of the keys for pricing insurance and annuity products.

The most widely used mortality projection model so far is the Lee-Carter model

(Lee and Carter (1992)). Between 1900 and 1988, the life expectancy in the United

States increased from 47 to 75. Based on the assumption that the life expectancy

would continue to increase, Lee and Carter (1992) applied the time series model to

forecasting long term mortality rates. This model considers two age-varying factors

and one time-varying factor to capture the downward trend in mortality rates. By

empirical mortality data, it is assumed that the time-varying factor is fitted by an

ARIMA (autoregressive integrated moving average) model.

One of the most significant features of the Lee-Carter model is that it is easy to

interpret and its parameters are estimable. Compared to other mortality projection

models, the Lee-Carter model bases its forecast on long term historical data, and

no explicit assumptions or a life span limit is attached to the model. Moreover, the

Lee-Carter model provides confidence regions, which was further proved that the

model is efficient in forecasting mortality rates.

4

CHAPTER 2. LITERATURE REVIEW 5

Afterwards, Lee and Carter (1992) pointed out that in order to forecast the mor-

tality rates for two populations within a territory or country, the same time-varying

index, called joint-k index, should be used so that the same trend of mortality

growth in response to time for the two populations can be reflected. This assump-

tion makes sense because usually two populations in a country have the same

medical service and environmental condition, etc. Thus, when these aspects im-

prove, the life expectancy of each population will increase simultaneously to the

same level.

Lee and Li (2005) extended the original Lee-Carter model by adding an extra

term to the model. They thought that the world is becoming more closely con-

nected by modern communication technology. Thus, in a long term, the forecasted

mortality rates for different populations will converge. They called it the augmented

common factor model, which was developed in two steps. Firstly, Lee and Li (2005)

used a common factor to capture the overall mortality growth; then the mortality

rates of that population are specified by an augmented term which reflects the fea-

ture of that population. This method was applied to forecasting the mortality rates

of Canadian populations. In different provinces, the common factor was used to

realize the long term convergence, and the augmented term was used to separate

the mortality rates for each province.

With the same concern about the long-term convergence problem, Li and Hardy

(2011) suggested the so-called co-integrated Lee-Carter model. By investigating

the time-varying indices of two populations, they noticed that there exists a co-

integrated relationship between the two time indices. In the co-integrated model,

two time-varying indices are modeled by a linear function.

The last three mentioned models based on the Lee-Carter model all take into

consideration the dependent structures among multiple populations; we call them

the multi-population mortality projection models. In this project, because the natu-

ral hedging strategy is adopted by swapping portions of life and annuity business

based on two populations of life insurance policyholders and annuitants, the multi-

population mortality projection models are needed.

CHAPTER 2. LITERATURE REVIEW 6

2.2 Hedging of mortality and longevity risks

Hedging of mortality and longevity risks is one of the most popular research areas

recently in Actuarial Science. Researchers have conducted large amount of study

on how to reduce mortality and longevity risks. Some of the financial instruments

have been applied to hedging these two risks, such as mortality-linked securities,

q-forward, etc. The practice of using mortality-linked securities was first suggested

by Blake and Burrows (2001) by pouring longevity risk into the capital market.

They introduced a survivor bond for which the future coupons are based on the

percentage of the alive retirees at the future coupon payments dates.

In 2003, Swiss Re issued the first mortality-linked security which is to protect

insurers from the loss of catastrophes. The bonds were issued via SPV (special

purpose vehicle). The payments depend on a mortality index. This bond has been

successfully operated for years.

BNP-Paribas and the European Investment Bank in 2004 issued a 25-year

longevity bond to hedge longevity risks. This is the first longevity bond that came

into real business. The coupons were linked to the survivor index based on the

actual mortality rates of England and Welsh males aged 65 in 2002.

In 2006, a pension buyout market attracted a lot of attention in UK. In this market

both the assets and liabilities of a pension plan were transferred to a life insurer.

To realize the transfer, the pension plan has to pay the life insurer the amount of

deficit if the assets are less than the liabilities. On the contrary, the insurer will pay

the surplus to the pension plan if assets exceeds liabilities. Thus, the pension plan

can be secured. This is an efficient method of transferring longevity risk; however,

the pension plan will possibly experience loss since the life insurer tends to re-

evaluate the pension plan by measuring the assets and liability in a way of more

risk aversion.

In 2007, J.P. Morgan introduced q-forwards, another financial derivatives, to

transfer mortality rates to the capital market. The q-forwards are described as a

zero coupon swap between a pre-fixed mortality rate at inception date and the

realized mortality rate at maturity date of the q-forward contract.

CHAPTER 2. LITERATURE REVIEW 7

Not only the pricing and structure of the mortality-linked securities have been

systematically studied but also how to evaluate the hedging methodology. Li and

Ng (2011) pointed out that because of lack of longevity trading index from which to

evolve the market price of the mortality-linked securities, it still remains a question

of how to evaluate the hedging technics. Thus, they proposed a pricing framework

for evaluating the mortality-linked securities based on canonical valuation. To con-

struct the framework, they suggested a nonparametric model, which helps to avoid

the risks from model itself and its parameters.

Gaillardetz et al. (2012) proposed a method of evaluating the hedging error

under a stochastic mortality projection. It is very likely that when catastrophes

occur insurers would experience huge amount of losses. Thus, evaluating the

distribution of hedging error is very important. They applied the regime-switching

model (Milidonis et al. (2011)) to extracting the hedging error and conducted the

error distribution that made the evaluation feasible.

In recent years, another kind of hedging method called natural hedge has be-

come appealing for researchers. Because instead of transferring the risk into fi-

nancial market, natural hedge can reduce mortality and longevity risks simply by

swapping proportions of life and annuity business between a life insurer and an an-

nuity provider. Cox and Lin (2007) are the first to thoroughly introduce this concept

by noticing the empirical evidence that companies adopting natural hedge within

their business usually offer lower premiums than the other companies.

After the proposal of natural hedge, tons of studies have been done in this field.

Wang et al. (2010) suggested that by mortality duration and convexity matching,

the optimal weights for conducting an immunization portfolio can be obtained. Lin

and Tsai (2013) gave more elaborate formulas for mortality duration and convexity,

which can be applied to a two-product or three-product portfolio.

However, some researchers also threw doubt on natural hedging that all the

studies are based on some models, but in reality the future mortality rates might be

totally model free, which may cause the method inefficient. Zhu and Bauer (2014)

used a non-parametric model to test the natural hedge method and came to the

conclusion that higher order variations in mortality rates would affect the efficiency

of natural hedging. Another problem of natural hedging pointed out by Cox and Lin

CHAPTER 2. LITERATURE REVIEW 8

(2007) is that for estimating the future mortality rates, most of the studies use the

same life table for both annuity and life insurance, which is not practical.

This project uses multi-population mortality projection models to forecast future

mortality rates for life insurance policyholders and annuitants separately based

on two life tables. The method of Langrage multipliers is used to help obtain the

optimal weights. Moreover, robust testing, together with model testing based on

the model-free block bootstrap method, is carried out.

Chapter 3

Introduction of Multi-populationModels

In this chapter, we first introduce four mortality models for multi-populations, which

are based on the well known Lee-Carter model. Then we fit the models with mor-

tality data from the Human Mortality Database to get the estimated parameters

which can be applied to forecasting future mortality rates. The deterministic mor-

tality rates can be used to determine the prices of life insurance and annuity prod-

ucts, and the stochastic ones can be used to simulate the realized/actual prices in

Chapter 4.

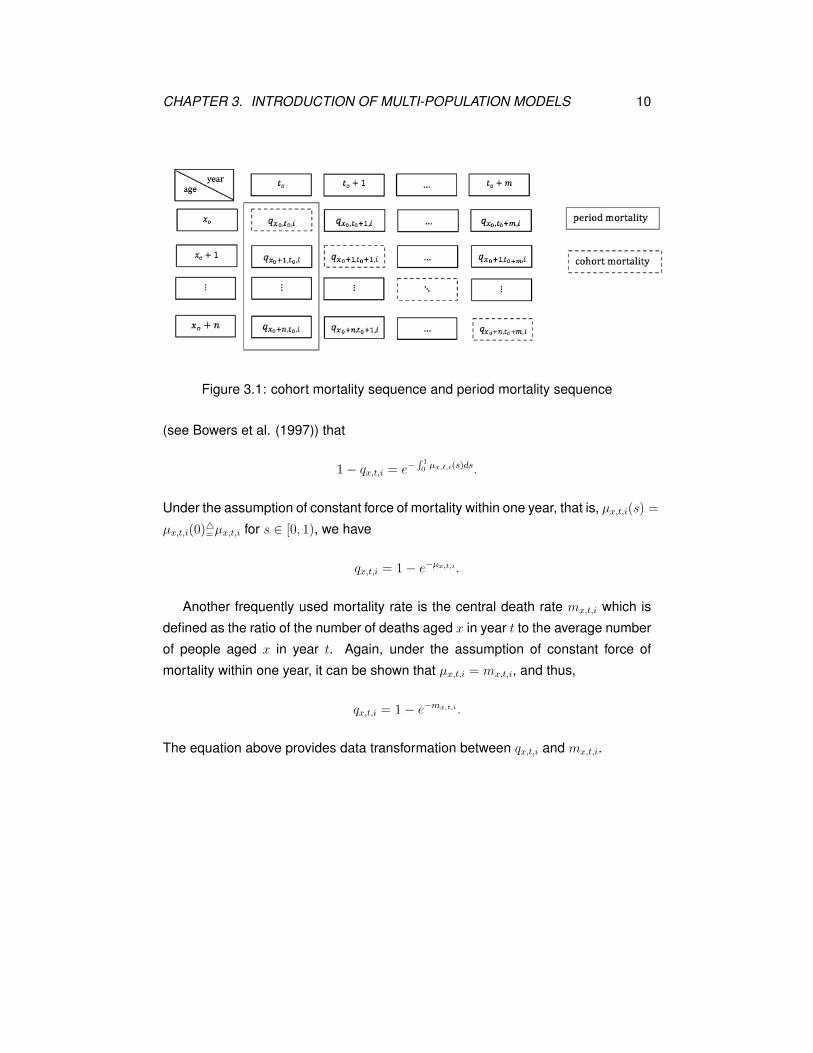

3.1 Concepts and notations

Let qx,t,i denote the probability that an individual aged x in year t for population

i will die within one year. We add an extra subscript i for studying the multi-

population mortality projection models. When forecasting the future mortality rates,

there are mainly two types of mortality sequences. One is the cohort mortality se-

quence {qx0+j,t0+j,i : j = 0, 1, 2, ...}, and the other is the period mortality sequence

{qx0+j,t0,i : j = 0, 1, 2, ...}. In this project, the cohort mortality sequence is used

for pricing. Figure 3.1 shows the difference between the cohort mortality sequence

and the period one.

Next, denote μx,t,i(s) the function of force of mortality, which is an instantaneous

death rate between age x and x+s in year t for population i aged x. It can be shown

9

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 10

Figure 3.1: cohort mortality sequence and period mortality sequence

(see Bowers et al. (1997)) that

1− qx,t,i = e−∫ 10 μx,t,i(s)ds.

Under the assumption of constant force of mortality within one year, that is, μx,t,i(s) =

μx,t,i(0)�=μx,t,i for s ∈ [0, 1), we have

qx,t,i = 1− e−μx,t,i .

Another frequently used mortality rate is the central death rate mx,t,i which is

defined as the ratio of the number of deaths aged x in year t to the average number

of people aged x in year t. Again, under the assumption of constant force of

mortality within one year, it can be shown that μx,t,i = mx,t,i, and thus,

qx,t,i = 1− e−mx,t,i .

The equation above provides data transformation between qx,t,i and mx,t,i.

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 11

3.2 Multi-population models and constrains

3.2.1 Independent Lee-Carter model

Lee and Carter (1992) proposed a model that the natural logarithm of central death

rates can be expressed by two age specific factors and one time specific factor as

follows:

ln(mx,t,i) = ax,i + bx,i × kt,i + εx,t,i,

subject to two constraints,

• ∑x bx,i = 1,

and

• ∑t kt,i = 0,

where

• ax,i is the average age-specific mortality factor at age x for population i,

• kt,i is the general mortality level in year t for population i,

• bx,i is the age-specific reaction to kt,i at age x for population i, and

• εx,t,i is the error term which is assumed independent and identically normally

distributed with mean 0 and variance σ2εx,i

for all t′s.

To fit the model with a given matrix of ln(mx,t,i)′s for population i and estimate

all parameters, we may use the singular value decomposition (SVD) method. How-

ever, there is a close approximation to SVD.

First, ax,i can be derived by the average of the sum of ln(mx,t,i) over a given year

span [t0, t0+n−1] by the second constraint, and kt,i equals the sum of [ln(mx,t,i)−ax,i] over a given age span [x0, x0 +m− 1] by the first constraint. That is,

t0+n−1∑

t=t0

ln(mx,t,i) = n× ax,i + bx,i ×t0+n−1∑

t=t0

kt,i = n× ax,i,

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 12

implying

ax,i =

∑t0+n−1t=t0

ln(mx,t,i)

n, x = x0, x0 + 1, ...., x0 +m− 1.

Similarly,

x0+m−1∑

x=x0

[ln(mx,t,i)− ax,i] = kt,i ×x0+m−1∑

x=x0

bx,i,

yielding

kt,i =

x0+m−1∑

x=x0

[ln(mx,t,i)− ax,i], t = t0, t0 + 1, ..., t0 + n− 1.

Finally, bx,i can be obtained by regressing [ln(mx,t,i) − ax,i] on kt,i without the

constant term involved for each age x. For projecting the future time-varying index

kt,i, a key to project the mortality rates, an ARIMA(0,1,0) time series (a random

walk with drift θi) is used, which is given by

kt,i = kt−1,i + θi + εt,i,

where the error term εt,i follows an independent and identical normal distribution

with mean 0 and variance σ2ε,i for all t′s. The parameter θi can be estimated by

θi =1

n− 1

t0+n−1∑

t=t0+1

(kt,i − kt−1,i) =kt0+n−1,i − kt0,i

n− 1.

Figure 3.2 displays the plots of {kt,i} from year 1981 to year 2009 (t0 = 1981

and n = 29) based on the U.S. male (i = 1) and female (i = 2) mortality rates for

an age span [25, 100] from the Human Mortality Database (www.mortality.org). The

data set is used throughout this chapter. From Figure 3.2 we can see that the {kt,i}for each of male and female populations has a decreasing trend over time.

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 13

Figure 3.2: kt,i against t

The logarithm of the stochastic central death rate for age x in year t0+n− 1+ τ

denoted by mx,t0+n−1+τ,i is

ln(mx,t0+n−1+τ,i) =ax,i + bx,i × (kt0+n−1,i + τ × θi +√τ × εt,i) + εx,t,i

=ln(mx,t0+n−1+τ,i) +√τ × bx,i × εt,i + εx,t,i,

where mx,t0+n−1+τ,i is the deterministic central death rate. Note that ln(mx,t0+n−1+τ,i)

is normally distributed with mean

ln(mx,t0+n−1+τ,i) = ax,i + bx,i × (kt0+n−1,i + τ × θi), τ = 1, 2, ....

and variance σ2(ln(mx,t0+n−1+τ,i)) = τ × b2x,i × σ2ε,i + σ2

εx,i, where {εx,t,i} and {εt,i}

are assumed independent.

Then

mx,t0+n−1+τ,i = exp[ax,i + bx,i × (kt0+n−1,i + τ × θi)],

or

qx,t0+n−1+τ,i = 1− exp[−exp(ax,i + bx,i × (kt0+n−1,i + τ × θi))].

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 14

The estimate of the variance of εx,t,i is given by

σ2εx,i

=1

n− 2

t0+n−1∑

t=t0

ε2x,t,i =

∑t0+n−1t=t0

[ln(mx,t,i)− ax,i − bx,i × kt,i]2

n− 2,

where x = x0, x0 + 1, ..., x0 +m− 1. The estimate of the variance of εt,i is given as

σ2ε,i =

1

n− 2

t0+n−1∑

t=t0+1

ε2t,i =

∑t0+n−1t=t0+1 (kt,i − kt−1,i − θi)

2

n− 2.

Therefore, the estimate of the variance of ln(mx,t0+n−1+τ,i) is obtained by

σ2(ln(mx,t0+n−1+τ,i))�= σ

2x,t0+n−1+τ,i = τ × b2x,i × σ2

ε,i + σ2εx,i

,

and a 100(1− γ)% predictive interval on qx,t0+n−1+τ,i can be constructed as

1− exp[−exp(ln(mx,t0+n−1+τ,i)± z γ2× σx,t0+n−1+τ,i)].

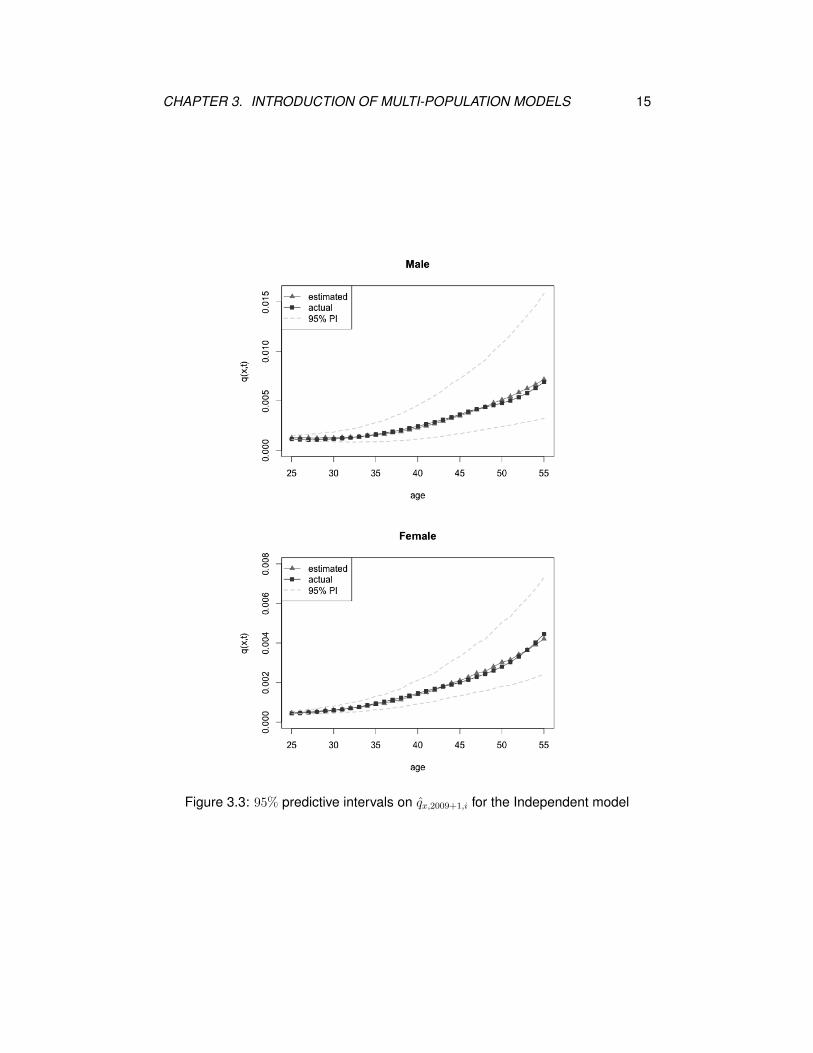

Figure 3.3 shows the projected period mortality rates in year 2010 based on the

central death rates from year 1981 to 2009. It is obvious that the estimated mor-

tality rates are quite close to the actual ones, and a narrower predictive interval on

the female mortality rates than that on the male ones is produced.

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 15

Figure 3.3: 95% predictive intervals on qx,2009+1,i for the Independent model

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 16

3.2.2 Joint-k Lee-Carter model

Apparently, two independent models ignore the co-movements between the mor-

tality rates for two populations. The males and females in a country live in the

same environment, and their mortality rates are affected by some common fac-

tors. To relate one population’s mortality rates to the other’s ones, Carter and

Lee (1992) introduced the joint-k model where the time-varying index kt,i, which

shows the general mortality level over time, is the same for both populations, that

is, kt,1 = kt,2 = Kt. The model can be expressed as

ln(mx,t,i) = ax,i + bx,i ×Kt + εx,t,i, i = 1, 2,

subject to two new constraints:

• ∑2i=1

∑x bx,i = 1

and

• ∑t Kt = 0.

Similarly, ax,i can be derived by the average of the sum of ln(mx,t,i) over a year

span [t0, t0+n−1], and Kt is equal to the sum of [ln(mx,t,i)− ax,i] over an age span

[x0, x0 +m− 1] and the population index. That is,

t0+n−1∑

t=t0

ln(mx,t,i) = n× ax,i + bx,i ×t0+n−1∑

t=t0

Kt,

implying

ax,i =

∑t0+n−1t=t0

ln(mx,t,i)

n, x = x0, x0 + 1, ..., x0 + n− 1;

and2∑

i=1

x0+m−1∑

x=x0

ln(mx,t,i) =2∑

i=1

x0+m−1∑

x=x0

ax,i +2∑

i=1

x0+m−1∑

x=x0

bx,i ×Kt,

giving

Kt =2∑

i=1

x0+m−1∑

x=x0

[ln(mx,t,i)− ax,i], t = t0, t0 + 1, ..., t0 + n− 1.

As for bx,i, it is obtained by regressing [ln(mx,t,i) − ax,i] on Kt without the constant

term involved for each age x. The common time-varying index Kt is also assumed

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 17

to follow a random walk with drift θ. That is

Kt = Kt−1 + θ + εt,

where the error term εt follows an independent and identical normal distribution

with mean 0 and variance σ2ε , and εt is independent of εx,t,i. The parameters θ is

estimated by

θ =Kt0+n−1 − Kt0

n− 1.

The logarithm of the forecasted central death rate for age x in year t0 + n− 1+ τ is

ln(mx,t0+n−1+τ,i) = ax,i + bx,i × (Kt0+n−1 + τ × θ +√τ × εt,i) + εx,t,i

= ln(mx,t0+n−1+τ,i) +√τ × bx,i × εt,i + εx,t,i,

where

ln(mx,t0+n−1+τ,i) = ax,i + bx,i × (Kt0+n−1 + τ × θ), τ = 1, 2, ....

The estimate of the variance of εx,t,i is

σ2εx,i

=

∑t0+n−1t=t0

[ln(mx,t,i)− ax,i − bx,i × Kt]2

n− 2,

and the estimate of the variance of εt is

σ2ε =

∑t0+n−1t=t0+1 (Kt − Kt−1 − θ)2

n− 2.

Thus, the variance of ln(mx,t0+n−1+τ,i) is

σ2x,t0+n−1+τ,i = τ × b2x,i × σ2

ε + σ2εx,i

,

which can be used to construct a 100(1− γ)% predictive interval on qx,t0+n−1+τ,i as

1− exp[−exp(ln(mx,t0+n−1+τ,i)± z γ2× σx,t0+n−1+τ,i)].

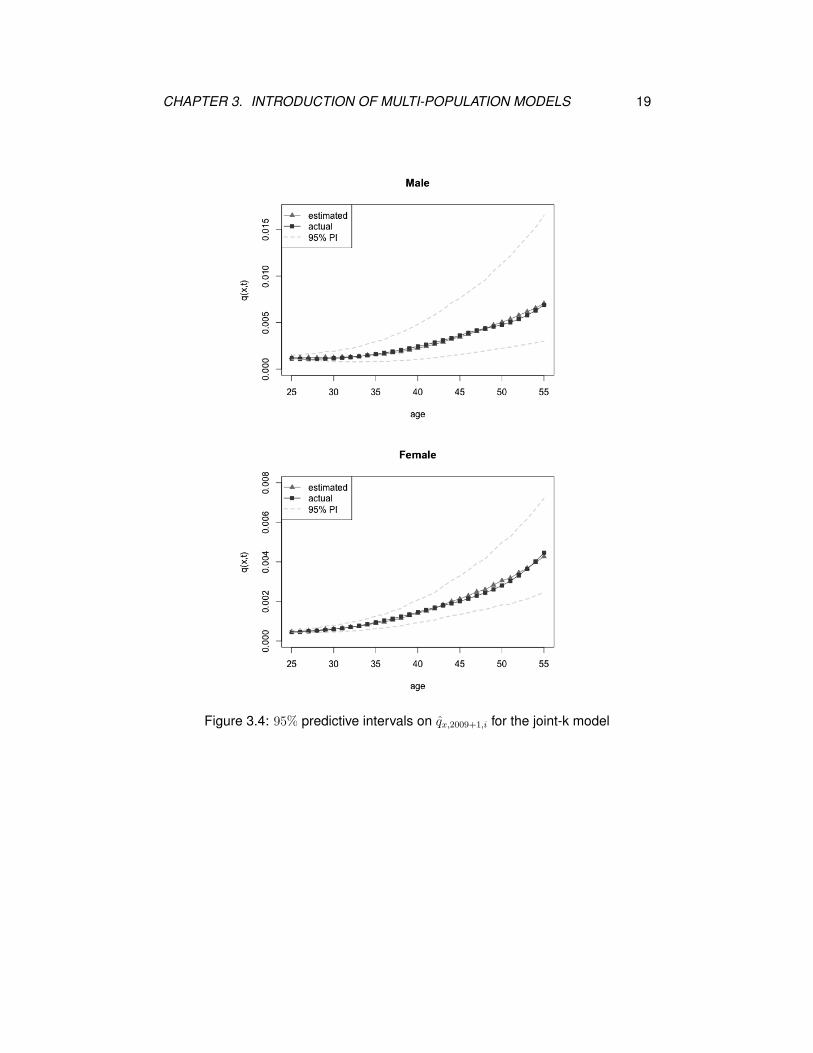

Using the same data set as that for Figure 3.3, we display corresponding forecasted

mortality rates and associated predictive intervals based on the joint-k model in

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 18

Figure 3.4. The projected mortality rates and the predictive interval are almost the

same with those for the independent model, where the estimated mortality rates

are close to actual ones, and the 95% predictive interval on the male mortality rates

is wider than that on the female ones.

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 19

Figure 3.4: 95% predictive intervals on qx,2009+1,i for the joint-k model

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 20

3.2.3 Co-integrated model

In the joint-k model, two populations share the same time-varying index Kt. In the

co-integrated model, the time-varying index for population 2 is a linear function of

the time-varying index for population 1. Specifically, assume the mortality rates for

populations 1 and 2 are modeled by

ln(mx,t,1) = ax,1 + bx,1 × kt,1 + εx,t,1

and

ln(mx,t,2) = ax,2 + bx,2 × kt,2 + εx,t,2.

By fitting the model with given data, kt,1 and kt,2 can be estimated separately in

the same way as those for two independent Lee-Carter models. Under the co-

integrated model, we assume there is a linear relationship plus an error term et

between kt,1 and kt,2, that is,

kt,2 = α + β × kt,1 + et. (3.1)

Since kt,1 and kt,2 are known, the estimates of parameters α and β can be obtained

by simple linear regression method. To build the link between kt,1 and kt,2, the co-

integrated model suggests re-estimating kt,2 to get ˆkt,2 with kt,1 unchanged using

(3.1) by plugging in the values of α and β. That is,

ˆkt,2 = α + β × kt,1.

In the co-integrated model, the estimates of the two variances for population 1,

σ2εx,1

and σ2ε,1, are the same as those for the original Lee-Carter model. However,

for the second population, the drift of the time-varying index is estimated by

θ2 =ˆkt0+n−1,2 − ˆ

kt0,2n− 1

= β × kt0+n−1,1 − kt0,1n− 1

= β × θ1,

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 21

and the estimate of the variance of the error term for the time-varying index is

σ2ε,2 =

∑t0+n−1t=t0+1 (

ˆkt,2 − ˆ

kt−1,2 − θ2)2

n− 2

= β2 ×t0+n−1∑

t=t0+1

(kt,1 − kt−1,1 − θ1)2

n− 2

= β2 × σ2ε,1.

The expression of the predictive interval on qx,t0+n−1+τ,i is still the same as that

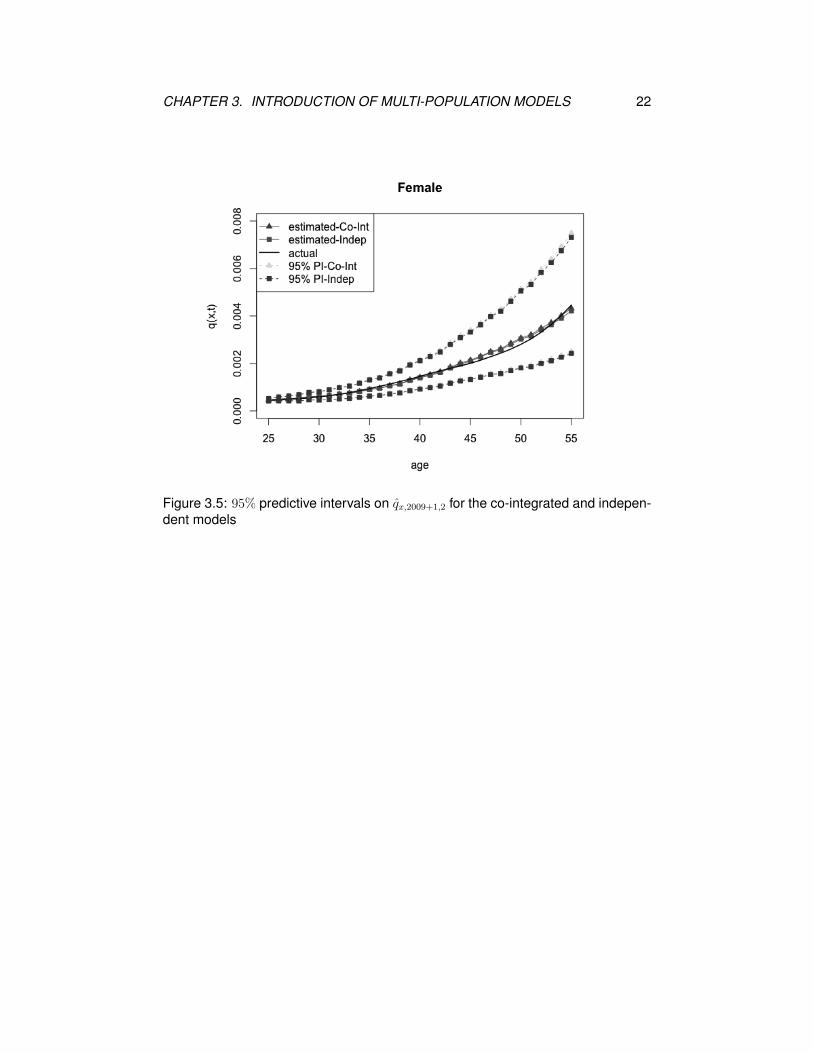

for independent Lee-Carter model. Figure 3.5 is the forecasted mortality rates

qx,2009+1,2 (female, τ = 1) and the associated 95% predictive intervals for the co-

integrated model as well as the corresponding one for the independent model for

comparison. We can see that both the forecasted mortality rates and predictive

intervals for both models are quite close to each other. Starting from age 40, the

forecasted mortality rates for the co-integrated model become slightly higher than

those for the independent model. The predictive intervals for both models almost

overlap.

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 22

Figure 3.5: 95% predictive intervals on qx,2009+1,2 for the co-integrated and indepen-dent models

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 23

3.2.4 Augmented common factor model

To avoid divergence in life expectancy in a long-run, Lee and Li (2005) suggested

adding a common factor to the original model. For the common term, it has the

following features:

• bx,1 = bx,2 = Bx for all x, and

• for the time-varying index, kt,1 = kt,2 = Kt for all t.

Two similar constrains apply, which are

• ∑2i=1

∑x wi × Bx = 1

and

• ∑t Kt = 0,

where w1 and w2 are the weights for populations 1 and 2, respectively, and w1+w2 =

1. Thus, the common factor model can be expressed as

ln(mx,t,i) = ax,i +Bx ×Kt + εx,t,i.

According to Li and Lee (2005), ax,i can still be derived by averaging ln(mx,t,i)

over a year span [t0, t0 + n− 1], that is,

t0+n−1∑

t=t0

ln(mx,t,i) =

t0+n−1∑

t=t0

ax,i +Bx ×t0+n−1∑

t=t0

Kt,

implying

ax,i =

∑t0+n−1t=t0

ln(mx,t,i)

n,

and Kt is obtained by

2∑

i=1

x0+m−1∑

x=x0

wi × [ln(mx,t,i)− ax,i] = Kt ×2∑

i=1

x0+m−1∑

x=x0

wi ×Bx,

yielding

Kt =2∑

i=1

x0+m−1∑

x=x0

wi × [ln(mx,t,i)− ax,i].

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 24

We set w1 = w2 = 0.5 for the U.S. male and female life tables. Since

2∑

i=1

wi × [ln(mx,t,i)− ax,i] = Bx × Kt ×2∑

i=1

wi = Bx × Kt,

we regress∑2

i=1 wi × [ln(mx,t,i) − ax,i] on Kt to get Bx for each age x. To fit the

data better, Li and Lee (2005) added a factor b′x,i × k′t,i for each population to the

common factor model to form the so-called augmented common factor model as

ln(mx,t,i) = ax,i +Bx ×Kt + b′x,i × k

′t,i + εx,t,i, i = 1, 2,

with an extra constrain∑

x b′x,i = 1. Notice that b′x,i and k

′t,i here are different from

bx,i and kt,i in the independent model. The constrain∑

x bx,i = 1 implies that

k′t,i =

x0+m−1∑

x=x0

[ln(mx,t,i)− ax,i − Bx × Kt].

Finally, b′x,i is derived by regressing [ln(mx,t,i) − ax,i − Bx × Kt] on k′t,i without the

constant term involved for each age x.

The logarithm of the forecasted central death rate for age x in year t0+n−1+ τ

is

ln(mx,t0+n−1+τ,i) =ax,i + Bx × (Kt0+n−1 + τ × θ +√τ × εt)

+ b′x,i × (k

′t0+n−1,i + τ × θi +

√τ × εt,i) + εx,t,i

=ln(mx,t0+n−1+τ,i) +√τ × (Bx × εt + b

′x,i × εt,i) + εx,t,i

which is normal with mean

ln(mx,t0+n−1+τ,i) = ax,i + Bx × (Kt0+n−1 + τ × θ) + b′x,i × (k

′t0+n−1,i + τ × θi),

and variance

σ2(ln(mx,t0+n−1+τ,i)) = τ × (Bx × σ2ε + b

′2x,i × σ2

ε,i) + σ2εx,i

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 25

where the three error terms, {εx,t,i}, {εt} and {εt,i}, are assumed independent,

θ =Kt0+n−1 − Kt0

n− 1

and

θ′i =

k′t0+n−1 − k

′t0

n− 1, i = 1, 2.

To construct the predictive intervals and simulate mortality rates, we need the esti-

mates of σ2εx,i

, σ2ε and σ2

ε,i, which are

σ2εx,i

=

∑t0+n−1t=t0

[ln(mx,t,i)− ax,i − Bx × Kt − b′x,i × k

′t,i]

2

n− 3, i = 1, 2,

σ2ε =

∑t0+n−1t=t0+1 (Kt − Kt−1 − θ)2

n− 2,

and

σ2ε,i =

∑t0+n−1t=t0+1 (k

′t,i − k

′t−1,i − θ

′i)

2

n− 2, i = 1, 2.

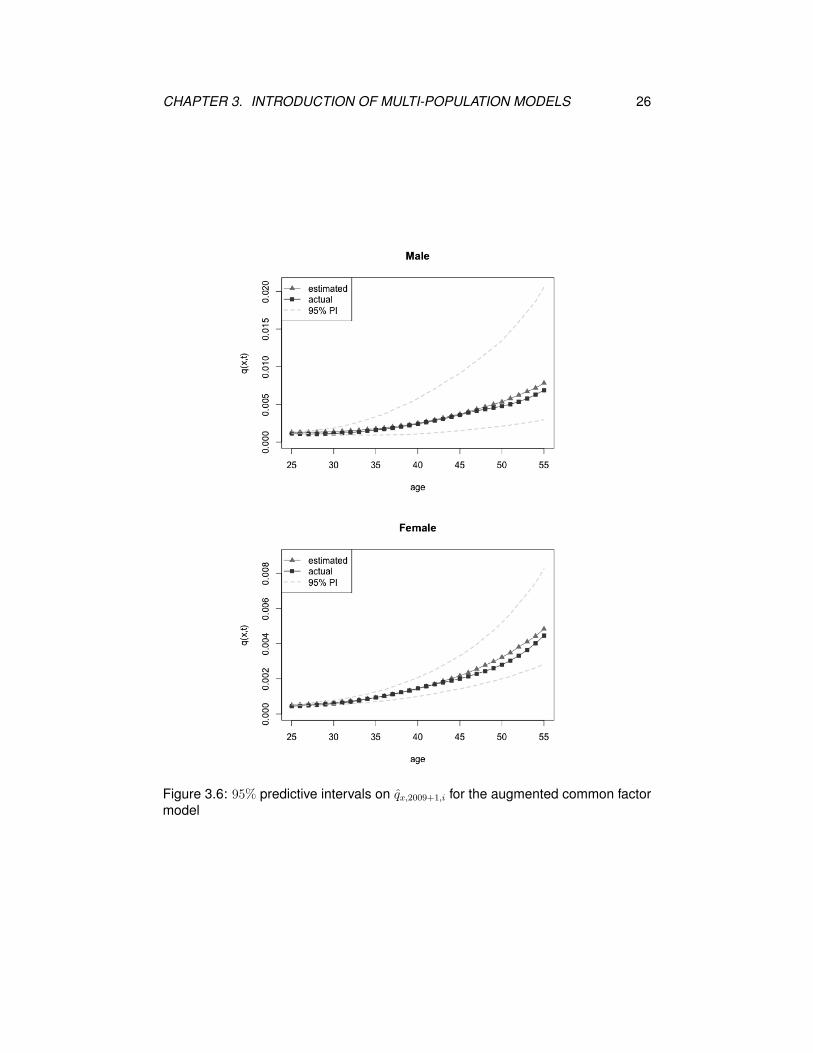

Figure 3.6 displays the forecasted qx,2009+1,i and associated predictive intervals

as well as the actual qx,2009+1,i for the augmented common factor model. When x

is small, the forecasted values are quite close to the true values. However, when

x goes up, the projected mortality rates tend to be higher than the actual ones.

Again, the predicted interval for the females is narrower than that for the males.

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 26

Figure 3.6: 95% predictive intervals on qx,2009+1,i for the augmented common factormodel

CHAPTER 3. INTRODUCTION OF MULTI-POPULATION MODELS 27

Figure 3.7 compares the predicted mortality rates among four models with the

actual mortality rates for year 2010 (τ = 1). It is obvious that all forecasted values

are close to actual ones for small x. We notice that the forecasted values from the

joint-k model are closer to the true values, while the mortality curve constructed

from the augmented common factor model is not as adjacent to the actual mortality

curve as the other models.

Figure 3.7: mortality curve comparisons among models and actual rates

Chapter 4

Application in Mortality Swap

4.1 Natural hedging and mortality swap

Mortality (longevity) risk is the risk that the number of deaths (survivors) is higher

than expected. When there is an unexpected change in mortality rates, either

life insurers or annuity providers will experience a loss. If the mortality rates in-

crease unexpectedly in a year, the number of deaths during the year is higher

than expected so that life insurance companies need to pay more death benefits.

However, in this case, annuity providers gain from the mortality increase. If the

mortality rates decline unexpectedly, the impacts on financial situation of life in-

surers and annuity providers reverse. Natural hedge is a strategy of hedging two

risks responding oppositely to a change in a common factor. Since life insurers

and annuity providers face mortality and longevity risks, respectively, both of them

can adopt natural hedge by swapping a portion of their business each other. When

a life insurer (an annuity provider) owns both life and annuity business at the same

time, the mortality and longevity risks of the portfolio can be offset to a lower level

no matter how the mortality rates change. Now, a question rises: what are the opti-

mal portions of business swapped between the life insurer and the annuity provider

such that the risk of the portfolio is minimized?

Let L denote the loss function at time zero, which is the present value of future

liabilities less the present value of future premium incomes. The values of both

future liabilities and premium incomes depend on the future mortality rates. Before

swapping the business, a life insurer (an annuity provider) has a portfolio of life

28

CHAPTER 4. APPLICATION IN MORTALITY SWAP 29

(annuity) business, and the loss function for the portfolio is denoted by Ll (La). To

hedge mortality (longevity) risk, the life insurer (annuity provider) would like to swap

wl (wa) of life (annuity) business to the annuity provider (life insurer); the resulting

loss functions of the life insurer and annuity provider become

LL = (1− wl)× Ll + wa × La

and

LA = (1− wa)× La + wl × Ll,

respectively, with variances

V ar(LL) =(1− wl)2 × V ar(Ll) + w2

a × V ar(La)

+ 2× (1− wl)× wa × Cov(Ll, La)(4.1)

andV ar(LA) =(1− wa)

2 × V ar(La) + w2l × V ar(Ll)

+ 2× (1− wa)× wl × Cov(Ll, La).(4.2)

There are three aspects to approach the optimal pair of weights which min-

imizes the variance of a loss function or the sum of the variances of two loss

functions. The first pair of weights, (wL+Al , wL+A

a ), is used to minimize V ar(LL) +

V ar(LA) (see Figure 4.1); the second pair of weights, (wLl , w

La ), is used to mini-

mized V ar(LL) (see Figure 4.2), and the third pair of weights, (wAl , w

Aa ), is used to

minimize V ar(LA) (see Figure 4.3), where we place superscripts L+A, L and A on

wl and wa to denote the weights that minimize V ar(LL) + V ar(LA), V ar(LL) and

V ar(LA), respectively.

CHAPTER 4. APPLICATION IN MORTALITY SWAP 30

Figure 4.1: Mortality swap: minimizing V ar(LL) + V ar(LA)

Figure 4.2: Mortality swap: minimizing V ar(LL)

Figure 4.3: Mortality swap: minimizing V ar(LA)

CHAPTER 4. APPLICATION IN MORTALITY SWAP 31

In mathematical optimization, the method of Lagrange multipliers is a strat-

egy for finding the local maximum (minimum) of a function subject to some con-

straint(s). Let Pl (Pa) stand for the present value of the future premiums of all

life (annuity) policies in the portfolio before swap. When the life insurer (annuity

provider) swaps wl (wa) of life (annuity) policies to the annuity provider (life insurer),

the life insurer (annuity provider) loses premium wl×Pl (wa×Pa) and gets premium

wa × Pa (wl × Pl). We set a swap condition wl × Pl = wa × Pa which will be applied

as the constraint in the three optimization problems mentioned above using the

method of Lagrange multipliers. Specifically, we would like to find (wl, wa) which

minimizes f(wl, wa) subject to wl × Pl = wa × Pa where f is V ar(LL) + V ar(LA),

V ar(LL) or V ar(LA).

To obtain (wL+Al , wL+A

a ), define f(wL+Al , wL+A

a ) = V ar(LL) + V ar(LA). By (4.1)

and (4.2),

f(wL+Al , wL+A

a ) =(1− wL+Al )2 × V ar(Ll) + (wL+A

a )2 × V ar(La)

+ 2× (1− wL+Al )× wL+A

a × Cov(Ll, La)

+ (1− wL+Aa )2 × V ar(La) + (wL+A

l )2 × V ar(Ll)

+ 2× (1− wL+Aa )× wL+A

l × Cov(Ll, La).

According to the method of Lagrange multipliers with a constraint wL+Al × Pl =

wL+Aa × Pa, the Lagrange function is defined by

ϕ(wL+Al , wL+A

a , λ) = f(wL+Al , wL+A

a ) + λ(wL+Al × Pl − wL+A

a × Pa),

where λ is called a Lagrange multiplier. To obtain the optimal solution, we differen-

tiate ϕ with respect to wL+Al , wL+A

a , and λ, respectively, and set all results to zero.

That is,

∂ϕ

∂wL+Al

= 4wL+Al Vl − 4wL+A

a σ2 + 2σ2 − 2Vl + λPl = 0,

∂ϕ

∂wL+Aa

= 4wL+Aa Va − 4wL+A

l σ2 + 2σ2 − 2Va − λPa = 0,

CHAPTER 4. APPLICATION IN MORTALITY SWAP 32

and

∂ϕ

∂λ= wL+A

l Pl − wL+Aa Pa = 0,

where Vl = V ar(Ll), Va = V ar(La) and σ2 = Cov(Ll, La). Then (wL+Al , wL+A

a ) can

be solved as

wL+Al =

1

2× Pa × PaVl + PlVa − (Pl + Pa)σ

2

P 2aVl − 2PlPaσ2 + P 2

l Va

(4.3)

and

wL+Aa =

1

2× Pl × PaVl + PlVa − (Pl + Pa)σ

2

P 2aVl − 2PlPaσ2 + P 2

l Va

. (4.4)

Similarly, when f(wLl , w

La ) = V ar(LL) with a constraint wL

l × Pl = wLa × Pa, the

optimal weights, wLl and wL

a , become

wLl =Pa × PaVl − Plσ

2

P 2aVl − 2PlPaσ2 + P 2

l Va

(4.5)

and

wLa =Pl × PaVl − Plσ

2

P 2aVl − 2PlPaσ2 + P 2

l Va

; (4.6)

when f(wAl , w

Aa ) = V ar(LA) with a constraint wA

l ×Pl = wAa ×Pa, the optimal weights

wAl and wA

a are

wAl =Pa × PlVa − Paσ

2

P 2aVl − 2PlPaσ2 + P 2

l Va

(4.7)

and

wAa =Pl × PlVa − Paσ

2

P 2aVl − 2PlPaσ2 + P 2

l Va

. (4.8)

Note that wL+Al = 1

2(wL

l + wAl ) and wL+A

a = 12(wL

a + wAa ). It is very difficult to obtain

the theoretical expressions of Vl, Va and σ2. Instead, we would like to compute the

corresponding sample variances and covariance by simulating thousands of Vl, Va

and σ2.

CHAPTER 4. APPLICATION IN MORTALITY SWAP 33

4.2 Numerical illustrations

4.2.1 Assumptions and portfolios

In practice, a life (an annuity) portfolio consists of a variety of life (annuity) products.

For simplicity, we assume that the portfolio for the life insurer consists of (65 − x)-

payment whole life insurance issued to the insureds aged x = 25 ∼ 64 and the

death benefits are paid at the end of the year of death, and that the portfolio for the

annuity provider is composed of (65−x)-payment and (65−x) years deferred whole

life annuity due issued to the insureds aged x = 25 ∼ 64. Since life insurance

(annuities) are more often purchased by those who have poorer (better) health

conditions, and we have no life (annuity) tables for consecutive years for forecasting

mortality rates with the models proposed in the preceding chapter, we use the U.S.

male (female) mortality table for the life (annuity) insureds. Because the year span

[t0, t0 + n − 1] is used for estimating the parameters of the mortality models, and

forecasting the mortality rates for years t0 + n − 1 + τ , τ = 1, 2, ...., we set the

beginning of year t1 = t0 + n as time 0. Denote lx,t1,i the initial number of insureds

aged x at time 0 for population i (i = 1 for life and i = 2 for annuity) and we

set l25,t1,1 = l25,t1,2 = 107. By lx+1,t1,i = lx,t1,i × px,t1−1,i, x = 25, ..., 63, the initial

numbers of insureds for the entire portfolio can be obtained. The death benefit for

life insurance is Bl = 100, 000 and the annual survival benefit is Ba = 10, 000. Based

on the assumptions, the loss functions of the life insurer and annuity provider at

time zero are

Ll =64∑

x=25

lx,t1,1 × (Ax,1 × Bl − ax:65−x|,1 × Px,l), (4.9)

La =64∑

x=25

lx,t1,2 × (65−x|ax,2 × Ba − ax:65−x|,2 × Px,a), (4.10)

Ax,1 =100−x∑

k=0

kpx,t1,1 · qx+k,t1+k,1 · vk+1, (4.11)

ax:65−x|,i =65−x−1∑

k=0

kpx,t1,i · vk, i = 1, 2, (4.12)

CHAPTER 4. APPLICATION IN MORTALITY SWAP 34

65−x|ax,2 =100∑

k=65

(k−x)px,t1,2 · vk−x, (4.13)

Px,l =Ax,1 × Bl

ax:65−x|,1, (4.14)

andPx,a =

65−x|ax,2 × Ba

ax:65−x|,2, (4.15)

where kpx,t1,i =∏k−1

j=0 px+j,t1+j,i with 0px,t1,i = 1, v = (1 + i)−1 and i = 6% is the

interest rate. Note that we set the limiting age equal to 100 for both populations, that

is, q100,t,i = 1, i = 1, 2. Moreover, Pl and Pa, the total present values of the future

premiums for the life insurer and annuity provider, respectively, in (4.3) ∼ (4.8) are

(see (4.9) and (4.10))

Pl =64∑

x=25

lx,t1,1 × ax:65−x|,1 × Px,l

and

Pa =64∑

x=25

lx,t1,2 × ax:65−x|,2 × Px,a.

The premiums Px,l and Px,a in (4.14) and (4.15), and the total premiums Pl and Pa

are pre-determined and do not respond to a change in mortality rates, whereas

Ax,1, ax:65−x|,i and 65−x|ax,2 in (4.11), (4.12) and (4.13) vary in response to the

realized mortality rates. Therefore, the deterministic mortality rates, qx,t0+n−1+τ ,

τ = 1, 2, ..., are used to calculate the premiums Px,l and Pa,x, and the stochastic

ones, qx,t0+n−1+τ , τ = 1, 2, ..., are used for simulations to compute Ax,1, ax:65−x|,i and

65−x|ax,2. When the realized mortality rates are different from the expected ones,

each of the loss functions Ll and La is either positive or negative. To forecast de-

terministic and stochastic mortality rates for ages 25 ∼ 64 and years 2011 ∼ 2086

using the four models given in Chapter 3, we set the year span [1981, 2010] and age

span [25, 100] (see Figure 4.4) to estimate the parameters with the male and female

mortality data from the Human Mortality Database for the life and annuity policies,

respectively. Specifically, for the independent model, we give the following steps to

forecast deterministic mortality rates for computing the premiums Px,l and Px,a:

CHAPTER 4. APPLICATION IN MORTALITY SWAP 35

Figure 4.4: age span [25, 100] and year span [1981, 2010]

1. compute ln(mx,2010+τ,i) = ax,i + bx,i × (k2010,i + τ × θi), i = 1, 2, τ = 1, 2, ..., 76,

x = 25, ..., 64;

2. transfer ln(mx,2010+τ,i) to qx,2010+τ,i; and

3. take the diagonal entries qx+τ−1,2010+τ,i, i = 1, 2, x = 25, ..., 64, τ = 1, 2, ..., (101−x).

To generate stochastic mortality rates for simulating Ax,1, ax:65−x|,i and 65−x|ax,2, a

similar procedure is given as follows:

1. generate sε,τ,i from N(0, 1) and sε,τ,i from N(0, 1), i = 1, 2, τ = 1, 2, ..., 76;

2. multiply sε,τ,i by σε,i, and sε,τ,i by σεx,i such that sε,τ,i × σε,i ∼ N(0, σ2ε,i) and

sε,τ,i × σεx,i ∼ N(0, σ2εx,i);

3. get simulated ln(mx,2010+τ,i) = ln(mx,2010+τ,i)+√τ×bx,i×sε,τ,i×σε,i+sε,τ,i×σεx,i,

i = 1, 2, τ = 1, 2, ..., 76, x = 25, ..., 64;

4. transfer ln(mx,2010+τ,i) to qx,2010+τ,i;

5. take the diagonal entries qx+τ−1,2010+τ,i, i = 1, 2, x = 25, ..., 64, τ = 1, 2, ..., (101−x); and

6. repeat steps (1) ∼ (5) for N times (N = 1, 000 in this project).

CHAPTER 4. APPLICATION IN MORTALITY SWAP 36

The procedures of forecasting the deterministic and stochastic mortality rates

for the joint-k, the co-integrated and the augmented common factor models are

similar to those above. With {qx+τ−1,2010+τ,i : i = 1, 2, x = 25, ..., 64, τ = 1, ..., (101−x)} and N {qx+τ−1,2010+τ,i : i = 1, 2, x = 25, ..., 64, τ = 1, ..., (101 − x)}’s, we can

calculate N realized values of Ll and La, get the sample variances Vl and Va and

the sample covariance σ2, and obtain the optimal weights with (4.3) ∼ (4.8).

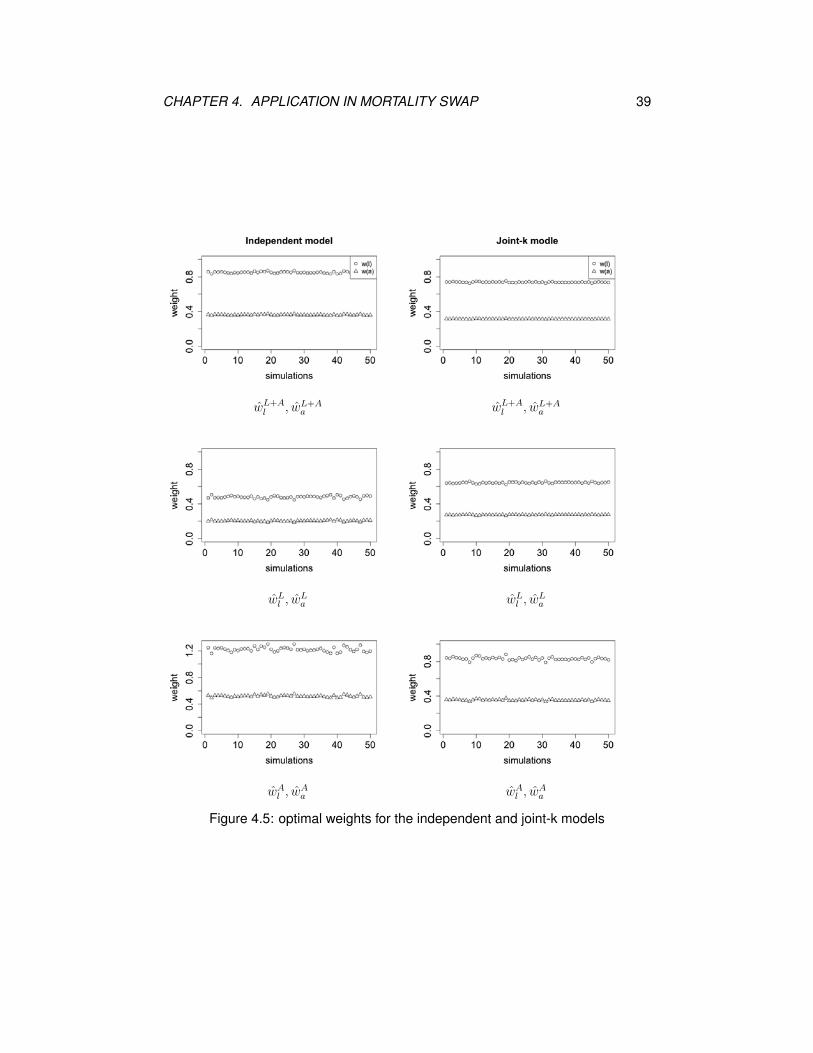

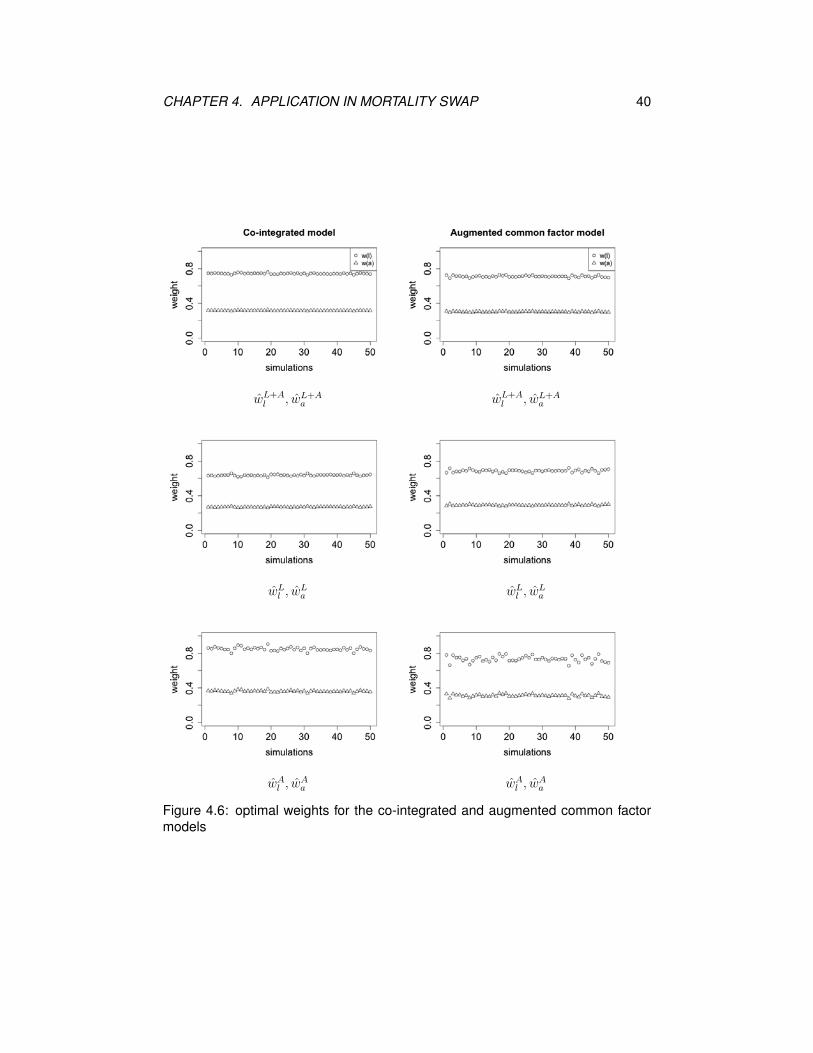

4.2.2 Robustness testing

In the preceding subsection, for each of three optimization problems, a pair of opti-

mal weights for life and annuity portfolios is produced by some stochastic mortality

model which generates N cohort mortality rates from age x to age 100 at time zero

for each of x = 25, ..., 64. If we re-run the procedure and generate another set of

N cohort mortality rates, can we still produce a pair of optimal weights of close

values? In this subsection, we will perform robustness testing. Robustness testing

is originally used in computer science whether a computer system can continue

to work well in case of invalid inputs. In our case, robustness testing is a way to

investigate whether the optimal weights produced by a model is insensitive to the

simulated mortality rates.

To complete the robustness testing, we repeat the simulation procedure M (M

is set to 50) times, and yield M pairs of optimal weights for each model. Figures

4.5 and 4.6 show scatter plots for the optimal weights (wl, wa) generated from each

model, from which we can see that the 50 pairs of weights obtained through 50

simulation procedures for each model are quite close to each other. That means

the four models are robust to simulations. Within each model, the first two pairs

of optimal weights (wL+Al , wL+A

a ) and (wLl , w

La ) seem to be more consistent than

(wAl , w

Aa ).

Table 4.1 summarizes the median values of 50 optimal weights for each type

obtained from the four models. The weight wl is more than twice as big as wa for all

types because wl/wa = Pa/Pl ≈ 2.3. All the optimal weights are within (0, 1) except

for wAl for the independent model. The pairs of optimal weights (wl, wa) from the

joint-k and co-integrated models are quite close to each other. The independent

model produces the largest (wL+Al , wL+A

a ) and (wAl , w

Aa ) but the smallest (wL

l , wLa ),

CHAPTER 4. APPLICATION IN MORTALITY SWAP 37

whereas the augmented common factor model yields the lowest (wL+Al , wL+A

a ) and

(wAl , w

Aa ) but the highest (wL

l , wLa ) among the four models.

IND JK Co-Int ACFwl wa wl wa wl wa wl wa

L+A 0.8505 0.3623 0.7385 0.3146 0.7431 0.3169 0.7110 0.3029L 0.4797 0.2044 0.6459 0.2752 0.6384 0.2723 0.6868 0.2926A 1.2213 0.5203 0.8311 0.3541 0.8479 0.3616 0.7352 0.3132

Table 4.1: the median of 50 optimal weights

Figure 4.7 displays V ar(LL)’s and V ar(LA)’s for four models based on 50 cor-

responding (wL+Al , wL+A

a )’s, (wLl , w

La )’s and (wA

l , wAa )’s, respectively. These figures

further confirm the comments on Table 4.1 above, and show the variability of 50

variances. Under the joint-k and co-integrated models, the variances from 50 runs

of simulations are quite close and smaller, whereas for the independent and aug-

mented common factor models, the sample variances are higher and not as stable

as those based on the joint-k and co-integrated models.

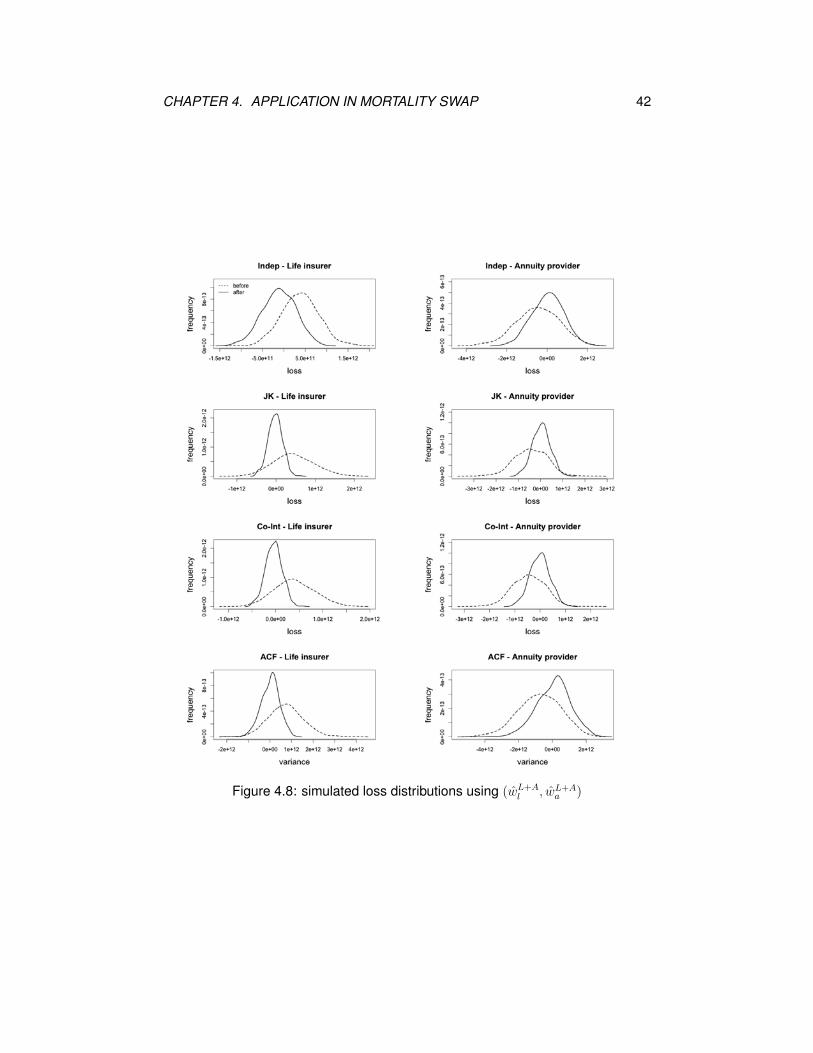

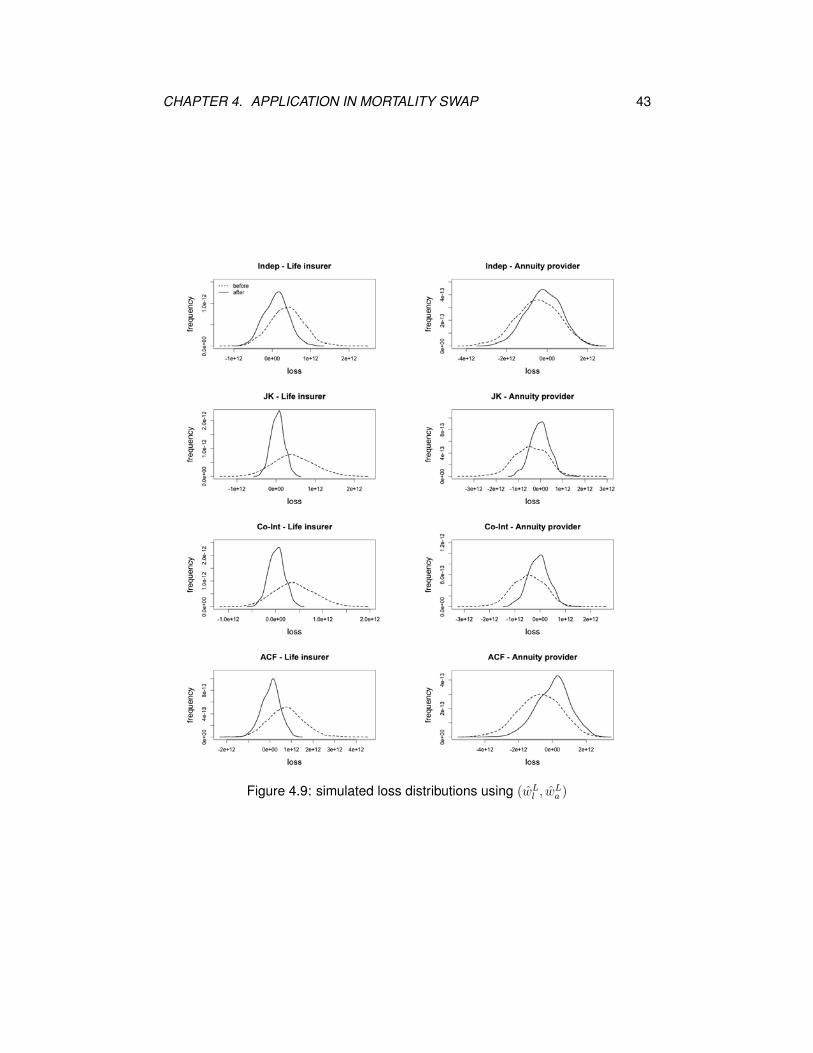

Figures 4.8, 4.9 and 4.10 exhibit the simulated loss distributions before and af-

ter swap using the median optimal weights for all four models. It is obvious that

the loss distributions after swap for the life insurer and annuity provider are al-

most narrowed, which implies that the variance of the loss distribution is reduced

significantly. No matter using (wL+Al , wL+A

a ), (wLl , w

La ) or (wA

l , wAa ), the loss distri-

butions for the joint-k and co-integrated models after swap for the annuity provider

are much narrower than those for the independent and augmented common factor

models, and for the life insurer, there is not much difference in the loss distribu-

tions after swap among the joint-k, co-integrated and augmented common factor

models.

To future quantify and compare the performances of hedging mortality and

longevity risks after swap for the life insurer and annuity provider, respectively,

we give a measure called hedge effectiveness (HE; see Li and Hardy (2011)) as

follows:

HE(L+ A) = 1− V ar(LL) + V ar(LA)

V ar(Ll) + V ar(La),

CHAPTER 4. APPLICATION IN MORTALITY SWAP 38

HE(L) = 1− V ar(LL)

V ar(Ll),

and

HE(A) = 1− V ar(LA)

V ar(La).

The HE measure is a variance reduction (variance of a loss function before hedge

less the variance of the loss function after hedge) ratio. Clearly, the larger the HE

is, the more effective the hedge is. Table 4.2 shows the comparisons of HEs, which

are consistent with the results from Figures 4.8, 4.9 and 4.10. The independent

model overall performs the worst among all models. The HE(L), HE(A) and

HE(L + A) for the joint-k model are the largest among the four models, which

implies that the joint-k model is the most effective in hedging mortality and longevity

risks. However, the co-integrated model produces the smallest variances of the

losses before and after swap for both the life insurer and annuity provider.

Independent V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 1.8904 1.5384 11.2661 6.1193 0.4180 0.1862 0.4568(wL

l , wLa ) 1.8904 1.0158 11.2661 7.6872 0.3385 0.4627 0.3177

(wAl , w

Aa ) 1.8904 23.1063 11.2661 5.5967 0.3385 -0.6433 0.5032

Joint-K V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 2.6716 0.3320 5.5132 1.6081 0.7630 0.8757 0.7083(wL

l , wLa ) 2.6716 0.2829 5.5132 1.7553 0.7510 0.8941 0.6816

(wAl , w

Aa ) 2.6716 0.4792 5.5132 1.5590 0.7510 0.8206 0.7172

Co-Integrated V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 1.8272 0.3185 4.2565 1.5635 0.6906 0.8257 0.6327(wL

l , wLa ) 1.8272 0.2768 4.2565 1.6887 0.6769 0.8485 0.6033

(wAl , w

Aa ) 1.8272 0.4437 4.2565 1.5218 0.6769 0.7572 0.6425

ACF V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 6.3736 1.8738 15.4550 10.2970 0.4424 0.7060 0.3337(wL

l , wLa ) 6.3736 1.8682 15.4550 10.3138 0.4419 0.7069 0.3320

(wAl , w

Aa ) 6.3736 1.8906 15.4550 10.2914 0.4419 0.7034 0.3341

Table 4.2: comparisons of sample variances (×1023) and HE’s

CHAPTER 4. APPLICATION IN MORTALITY SWAP 39

wL+Al , wL+A

a wL+Al , wL+A

a

wLl , w

La wL

l , wLa

wAl , w

Aa wA

l , wAa

Figure 4.5: optimal weights for the independent and joint-k models

CHAPTER 4. APPLICATION IN MORTALITY SWAP 40

wL+Al , wL+A

a wL+Al , wL+A

a

wLl , w

La wL

l , wLa

wAl , w

Aa wA

l , wAa

Figure 4.6: optimal weights for the co-integrated and augmented common factormodels

CHAPTER 4. APPLICATION IN MORTALITY SWAP 41

V ar(LL)

variances using (wL+Al , wL+A

a )

V ar(LA)

variances using (wL+Al , wL+A

a )

variances using (wLl , w

La ) variances using (wL

l , wLa )

variances using (wAl , w

Aa ) variances using (wA

l , wAa )

Figure 4.7: variances after swap

CHAPTER 4. APPLICATION IN MORTALITY SWAP 42

Figure 4.8: simulated loss distributions using (wL+Al , wL+A

a )

CHAPTER 4. APPLICATION IN MORTALITY SWAP 43

Figure 4.9: simulated loss distributions using (wLl , w

La )

CHAPTER 4. APPLICATION IN MORTALITY SWAP 44

Figure 4.10: simulated loss distributions using (wAl , w

Aa )

Chapter 5

Block Bootstrap Method

In the preceding chapter, we forecast deterministic and stochastic mortality rates

with some two-population mortality models to determine the premiums of life and

annuity products and simulate the loss functions of portfolios of life and annuity

business. The weights of business for swap are calculated by the sample variances

and the sample covariance of the loss functions of the life insurer and annuity

provider before swap, which can minimize the risk of the portfolio and produce

high hedge effectiveness. All the great results are based on that the assumed

mortality model is the actual one, which, however, might not be true. Therefore,

both the life insurer and annuity provider face model risk and parameter risk that

will potentially affect the results. In this chapter, a bootstrap method which is model

and parameter free will be applied to generating samples for the future mortality

rates to calculate the weighted loss functions and their variances with the weights

obtained by each of the four models in Chapter 3.

Bootstrap is usually used to resample data with replacement to estimate some

statistic of a population from the sampled data. The procedure of the bootstrap

(naive bootstrap) is as follows:

1. Draw values from the original data set with replacement to form a new data

set of size n∗.

2. Repeat the first step N∗ times to obtain N∗ new data sets.

3. Compute the test statistic using the new data sets.

45

CHAPTER 5. BLOCK BOOTSTRAP METHOD 46

However, the naive bootstrap fails when applied to the mortality rates. First of

all, mortality rates over years can be treated as a time series displaying a decreas-

ing trend because of the improvement of medical and environmental conditions,

which shows mortality rates are not stationary. Secondly, the naive bootstrap is

likely to destroy the dependency of mortality rates on both age and time dimen-

sions. Alternatively, the block bootstrap can solve the problems above. First, re-

garding the non-stationary problem, differencing is a popular and effective method

of removing trend from a time series and making the time series weakly stationary.

The procedure is given below.

• Convert the empirical mortality rates qx,t,i to ln(mx,t,i), i = 1, 2, x = 25, ..., 100,

t = 1981, ..., 2009.

• Devide ln(mx,t+1,i) by ln(mx,t,i) to get the ratio, denoted by rx,t,i, that is, rx,t,i =ln(mx,t+1,i)

ln(mx,t,i), t = 1981, ..., 2009.

• Subtract rx,t,i from rx,t+1,i to get the difference, denoted by dx,t,i, that is, dx,t,i =

rx,t+1,i − rx,t,i, t = 1981, ..., 2008.

Figure 5.1 shows the time series {dx,t,i}, i = 1, 2, for the U.S. males and females

aged 35, 45, 55 and 65, which look stationary.

CHAPTER 5. BLOCK BOOTSTRAP METHOD 47

Figure 5.1: {dx,t,i} for x = 35, 45, 55, 65

CHAPTER 5. BLOCK BOOTSTRAP METHOD 48

To further ensure the time series {dx,t,i} is stationary, the Phillips-Perron (PP)

and the Kwiatkowski-Phillips-Schmidt-Shin (KPSS) hypothesis tests are conducted.

For the PP test where an AR(1) model is assumed, the null hypothesis is that the

time series has a unit root so that the time series is non-stationary, which implies

that a small p-value suggests a stationary time series. For the KPSS test, the null

hypothesis is that the time series is stationary; thus, a big p-value indicates a sta-

tionary time series. Table 5.1 exhibits the results of the hypothesis tests. All the

p-values for the PP test are below 0.05, and the ones for the KPSS test are larger

than 0.1, which all suggest that the time series {dx,t,i} is stationary.

35 45 55 65

Male PP 0.01 0.01 0.01 0.01KPSS >0.1 >0.1 >0.1 >0.1

Female PP 0.01 0.01 0.01 0.01KPSS >0.1 >0.1 >0.1 >0.1

Table 5.1: p-values for testing stationarity of {dx,t,i}

For the second problem regarding dependency, according to Li and Ng (2011),

the two-dimensional mortality rates matrix Mi for population i is converted to a

series of column vectors,

mt,i = (mx0,t,i,mx0+1,t,i, ...,mx0+m−1,t,i)′, t = t0, t0 + 1, ..., t0 + n− 1.

Thus, the matrix can be expressed as Mi = {mt0,i,mt0+1,i, ...,mt0+n−1,i}, which

contains n elements. In this way, the age dependency can be retained. Before

proceeding to the next step, as discussed in the first problem above, the vector

mt,i needs to be converted to ln(mt,i), get the ratio vector rt,i and then form the

difference vector

dt,i = (dx0,t0+t−1,i, dx0+1,t0+t−1,i, ..., dx0+m−1,t0+t−1,i)′, t = 1, 2, ..., n− 2, i = 1, 2.

For the time dependency problem, it’s assumed that k consecutive time series,

dt,i, ...,dt+k−1,i, are dependent. While the dependency between dt,i and dt+k−1,i

gradually becomes weaker as k increases, and it’s going to vanish thoroughly for a

large k. Thus, the block bootstrapping suggests splitting d into n overlapped blocks

CHAPTER 5. BLOCK BOOTSTRAP METHOD 49

Figure 5.2: a circle diagram of dt,i’s

of size k as follows:

D ={(d1,i,d2,i, ...,dk,i),

(d2,i,d3,i, ...,dk+1,i),

(d3,i,d4,i, ...,dk+2,i),

...,

(dn−2,i,d1,i ...,dk−1,i)}

Figure 5.2 gives a circle diagram of dt,i’s. We make all dt,i’s a circle and every con-

secutive k dt,i’s form a block. After the (n−2) blocks of size k, which are numbered

1, 2, ..., (n − 2), have been created, the block number will be drawn with replace-

ment to form a sample. The values within each block don’t change at all so that

the dependent structure among k dt,i’s is maintained. In Chapter 4, we simulate 76

time series of {q2010+τ,i}’s, τ = 1, 2, ..., 76, for computing one value of loss functions

LL and LA. To simulate the same number of time series of {q2010+τ,i}’s with the

block bootstrap method, we need to draw Z = Wk

block numbers with replacement

as a bootstrap sample, where W = 76 and k is the block size. If Wk

is not an integer,

then (z + 1) blocks need to be drawn and take the first s elements of the (z + 1)th

block to make the sample size equal to W where z and s are the integer and the

remainder of Wk

, respectively.

CHAPTER 5. BLOCK BOOTSTRAP METHOD 50

Finally, the block size is determined by the size of observations V . As sug-

gested by Hall et al. (1995), the optimal block size, k, can be V13 , V

14 or V

15 . Since

there are 28 {dt,i}’s (V = n− 2 = 28), a block size of 2 is chosen.

The following is the procedure of the block bootstrap method.

1. Take the logarithm on the real central death rates, ln(mx,t,i), for i = 1, 2,

x = x0, ..., x0 +m− 1, and t = t0, ..., t0 + n− 1.

2. Get rx,t,i =ln(mx,t+1,i)

ln(mx,t,i)and dx,t,i = rx,t+1,i − rx,t,i.

3. Form column vector dt,i = (dx0,t0+t−1,i, dx0+1,t0+t−1,i, ..., dx0+m−1,t0+t−1,i)′, t =

1, ..., n− 2.

4. Form the jth block of size 2, (dj,i,dj+1,i), j = 1, ..., n − 3, and the (n − 2)th

block, (dn−2,i,d1,i).

5. Draw a bootstrap sample of size Z = W2

if W is even, or Z = (W+1)2

if W is

odd to get the block numbers b1, b2,..., bZ (all the indices fall between 1 and

n− 2).

6. Get the indices, b1, b1 +1, b2, b2 +1,..., bZ , bZ +1 if W is even, or b1, b1 +1, b2,

b2 +1,..., bZ if W is odd; if bj = n− 2 for some j, then assign index 1 to bj +1.

Denote the jth index as cj, j = 1, ...,W .

7. Obtain the column vector dcj ,i = (dx0,t0+cj−1,i, ..., dx0+m−1,t0+cj−1,i)′, j = 1, ...,W .

8. Obtain simulated mx,t0+n−1+τ,i by

mx,t0+n−1+τ,i = exp{ln(mx,t0+n−1+τ−1,i)× [ln(mx,t0+n−1,i)

ln(mx,t0+n−2,i)+

τ∑

j=1

dx,t0+cj−1,i]},

i = 1, 2, τ = 1, 2, ..., 76, x = x0, x0 + 1, ..., x0 +m− 1.

9. Convert simulated mx,t0+n−1+τ,i matrix to qx,t0+n−1+τ,i matrix and take the di-

agonal entries to form cohort mortality sequences.

10. Repeat (3)-(9) for N times (N = 1000).

CHAPTER 5. BLOCK BOOTSTRAP METHOD 51

The median weights and premiums calculated in the preceding chapter are

used in simulating the loss functions before and after swap using the block boot-

strap method. By applying the pre-determined premiums and 1000 simulated mor-

tality paths to (4.9) and (4.10), 1000 La’s and Ll’s can be obtained, from which

sample V ar(Ll), V ar(La) and Cov(Ll, La) can be calculated. Plugging V ar(Ll),

V ar(La) and Cov(Ll, La) into (4.1) and (4.2) with the pre-determined weights, the

variances of the loss functions LL and LA after swap, V ar(LL) and V ar(LA), are

obtained.

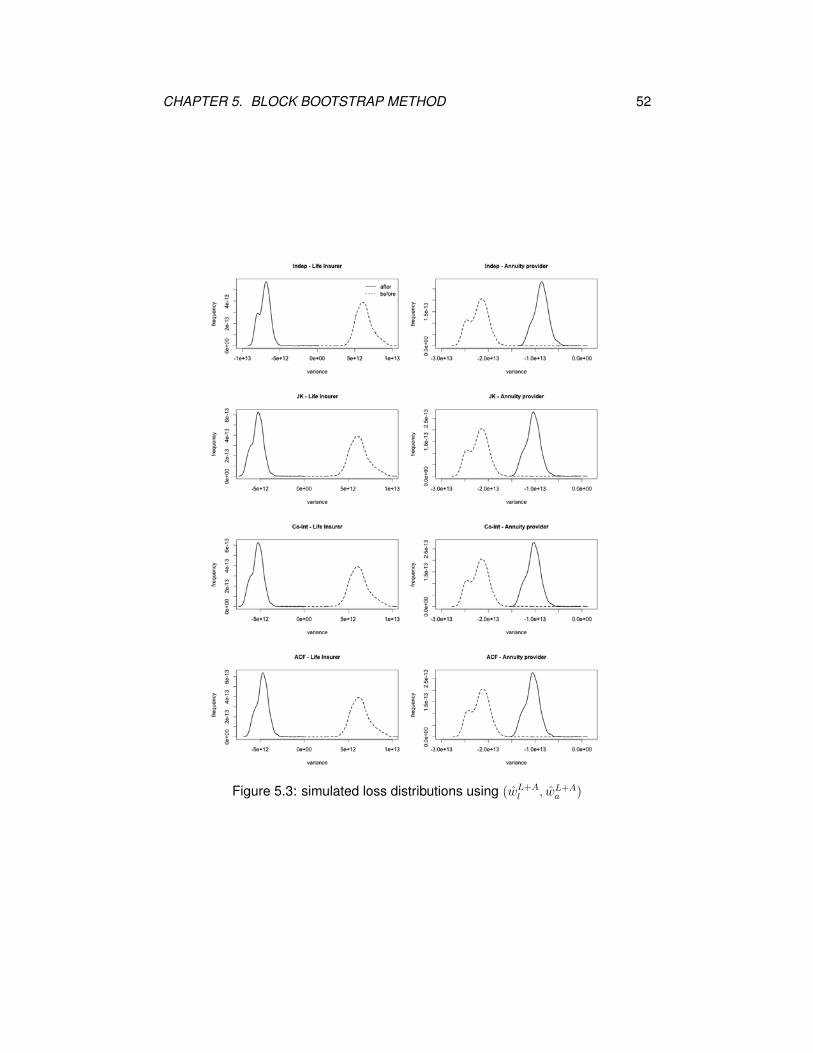

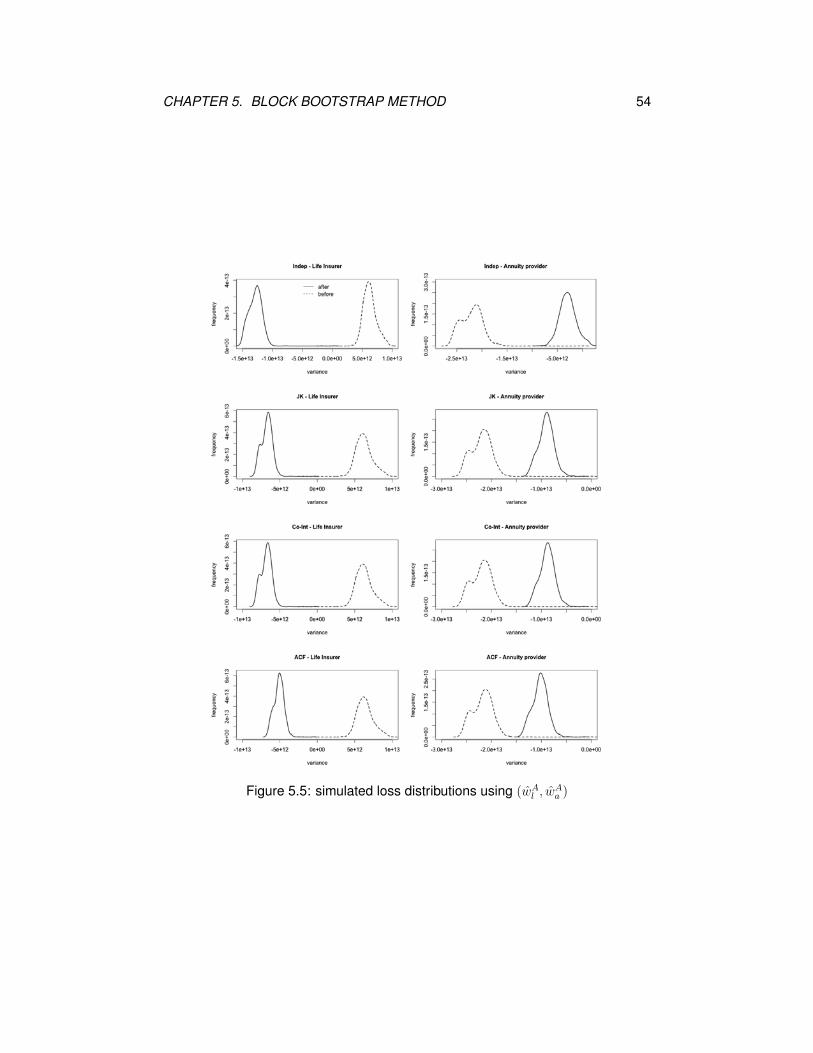

Figures 5.3, 5.4 and 5.5 display the simulated loss distributions before and after

swap. Compared with the loss distributions in Figures 4.8, 4.9 and 4.10, the overlap-

ping between the simulated loss distributions before and after swap becomes far

smaller. The loss distributions before and after swap for the life insurer mainly fall

in the negative (gain) and positive (loss) territories, respectively, whereas those for

the annuity provider largely spread in the negative (gain) territory. Under the block

bootstrap method, the life insurer will benefit more gains from swap and the annuity

provider will suffer more losses (or less gains) from swap than under the parametric

mortality models. Moreover, even though the simulated loss functions generated

from the block bootstrap method exhibit big differences from those based on the

four mortality models, the pre-determined weights still lower down the risks for

both insurance and annuity portfolios, which can be seen from the narrowed loss

distribution curves after swap.

CHAPTER 5. BLOCK BOOTSTRAP METHOD 52

Figure 5.3: simulated loss distributions using (wL+Al , wL+A

a )

CHAPTER 5. BLOCK BOOTSTRAP METHOD 53

Figure 5.4: simulated loss distributions using (wLl , w

La )

CHAPTER 5. BLOCK BOOTSTRAP METHOD 54

Figure 5.5: simulated loss distributions using (wAl , w

Aa )

CHAPTER 5. BLOCK BOOTSTRAP METHOD 55

Similar to Table 4.2, Table 5.2 shows the sample variances and hedge effec-

tiveness (HE) under the block bootstrap method. In this case, the differences

in HE and V ar(L) among four models are not as obvious as those using multi-

population mortality models because the same simulated mortality rates from the

block bootstrap method are applied to the loss functions before and after swap with

different (wl, wa)’s from four mortality models. Compared with the values in Table

4.2, the variances of the loss functions before and after swap for both life insurer

and annuity provider are far enlarged except for V ar(LL) based on (wAl , w

Aa ) for

the independent model. The HEs generally increase for the independent model,

and decrease for the joint-k and co-integrated models. Among the four models,

the co-integrated and independent models achieve the highest and the lowest

hedge effectiveness, respectively, for HE(L + A), HE(L) and HE(A) based on

(wL+Al , wL+A

a ), (wLl , w

La ) and (wA

l , wAa ), respectively. The joint-k model can also pro-

duce high hedge effectiveness. Thus, under model-free block bootstrap method,

the joint-k and co-integrated models still outperform the other two models.

Independent V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 12.1508 5.6147 43.0437 23.2084 0.4778 0.5379 0.4608(wL

l , wLa ) 12.1508 4.4826 43.0437 27.8747 0.4138 0.6311 0.3524

(wAl , w

Aa ) 12.1508 12.9029 43.0437 24.6982 0.3188 -0.0619 0.4262

Joint-K V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 12.1509 4.6247 43.0495 23.9732 0.4819 0.6194 0.4431(wL

l , wLa ) 12.1509 4.2296 43.0495 25.0259 0.4700 0.6519 0.4187

(wAl , w

Aa ) 12.1509 5.4035 43.0495 23.3042 0.4799 0.5553 0.4587

Co-Integrated V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 12.1508 4.6638 43.0511 23.9150 0.4823 0.6162 0.4445(wL

l , wLa ) 12.1508 4.2211 43.0511 25.1140 0.4686 0.6526 0.4166

(wAl , w

Aa ) 12.1508 5.5980 43.0511 23.2074 0.4782 0.5393 0.4782

ACF V ar(Ll) V ar(LL) V ar(La) V ar(LA) HE(L+ A) HE(L) HE(A)

(wL+Al , wL+A

a ) 12.1231 4.4638 43.0398 24.2210 0.4800 0.6318 0.4372(wL

l , wLa ) 12.1231 4.3527 43.0398 24.4902 0.4771 0.6410 0.4310

(wAl , w

Aa ) 12.1231 4.6011 43.0398 23.9780 0.4819 0.6205 0.4429

Table 5.2: comparisons of sample variances (×1023) and HE’s (block bootstrap)

Chapter 6

Conclusion

The strategy of natural hedging in this project shows a significant effect on reducing

risks of insurance and annuity portfolios by swapping business. The robustness

testing exhibits that the optimal weights and the variances of the loss functions after

swap for both life insurer and annuity provider obtained from four multi-population

models are robust to simulations.

The performances of hedging mortality and longevity risks for each model are

compared in two ways; one is based on parametric multi-population mortality mod-

els, and the other is based on non-parametric block bootstrap method. Both ways

suggest that the joint-k and co-integrated models outperform the independent and

augmented common factor models, which implies that the improvement on mortal-

ity rates between two populations tend to become more related, and assuming a

stronger bond between two time-varying factors for two populations seems to be

more reasonable when forecasting future mortality rates.

Although natural hedging can achieve the goal of reducing the variance of the

loss, future research can still be carried out so that it can be further applied to more

practical situations. For example, both a life insurer and an annuity provider won’t

swap their business directly in practice. Generally, companies prefer to transfer

their business to a financial intermediary called SPV (special purpose vehicle) who

is in charge of business swapping. Another problem is that the portfolio of life

(annuity) business in this project consists of only one type of life insurance (annuity)

product, the (65− x)-payment whole life insurance ((65− x)-payment and (65− x)

deferred whole life annuity due), which is too simple to be practical.

56

Bibliography

[1] D. Blake and W. Burrows. Survivor bonds: Helping to hedge mortality risk.Journal of Risk and Insurance, 68:339–348, 2001.

[2] N.L. Bowers, H.U. Gerber, J.C. Hickman, D.A. Jones, and C.J. Nesbitt. Actu-arial mathematics. 2nd ed. The Society of Actuaries, 1997.

[3] S.H. Cox and Y. Lin. Natural hedging of life and annuity mortality risks. NorthAmerican Actuarial Journal, 11:1–15, 2007.

[4] P. Gaillardetz, H.Y. Li, and A. MacKay. Equity-linked products: Evaluation ofthe dynamic hedging errors under stochastic mortality. European ActuarialJournal, 2:243–258, 2012.

[5] P. Hall, J.L. Horowitz, and B.Y. Jing. On blocking rules for the bootstrap withdependent data. Biometrika, 82:561–574, 1995.

[6] R.D. Lee and L.R. Carter. Modeling and forecasting U.S. mortality. Journal ofthe American Statistical Association, 87:659–671, 1992.

[7] J.S. Li and M.R. Hardy. Measuring basis risk in longevity hedges. NorthAmerican Actuarial Journal, 15:177–200, 2011.

[8] J.S. Li and A.C. Ng. Canonical valuation of mortality-linked securities. TheJournal of Risk and Insurance, 78:853–884, 2011.

[9] N. Li and R. Lee. Coherent mortality forecasts for a group of populations: Anextension of the Lee-Carter method. Demography, 42:575–594, 2005.

[10] T. Lin and C.C.L. Tsai. On the mortality/longevity risk hedging with mortalityimmunization. Insurance: Mathematics and Economics, 53:580–596, 2013.

[11] A. Milidonis, Y. Lin, and S.H. Cox. Mortality regimes and pricing. North Amer-ican Actuarial Journal, 15:266–289, 2011.

[12] J.L. Wang, H.C. Huang, S.S. Yang, and J.T. Tsai. An optimal product mix forhedging longevity risk in life insurance companies: The immunization theoryapproach. The Journal of Risk and Insurance, 77:473–497, 2010.

[13] N. Zhu and D. Bauer. A cautionary note on natural hedging of longevity risk.North American Actuarial Journal, 18:104–115, 2014.

57