Natural alpha in Convertibles

42

Michael Revy, MBA Principal and Director of Research Froley, Revy Investment Co. Want Long-Only Alpha? Get Convertibles! MASTER FILE Click to buy NOW! P D F - X C h a n g e w w w . d o c u - t r a c k . c o m Click to buy NOW! P D F - X C h a n g e w w w . d o c u - t r a c k . c o m

-

Upload

michael-revy -

Category

Economy & Finance

-

view

57 -

download

1

Transcript of Natural alpha in Convertibles

1

Michael Revy, MBA

Principal and Director of ResearchFroley, Revy Investment Co.

Want Long-Only Alpha?

Get Convertibles!

MASTER FILE

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

2

Disclaimer

Thank you for the opportunity to discuss the nature of converts.

Before we begin, let me remind you that the views I express are my own andnot necessarily the views of my colleagues at Froley Revy.

This presentation is for information purposes and not a solicitation to buy orsell any security or to enter an investment management contract with Froley,Revy.

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

3

Alpha is in the Asset Class

Alpha Will Persist

Convexity : the Window to Alpha

Good for the Goose; Good for the Gander

Want Long-Only Alpha? Get Convertibles!Clic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

4

Alpha is in the Asset Class

Nature of the instrument ~ Alpha

Nature of the issuer (s) ~ Alpha

Natural referee ~ Alpha

Alpha in many locations!!!

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

5

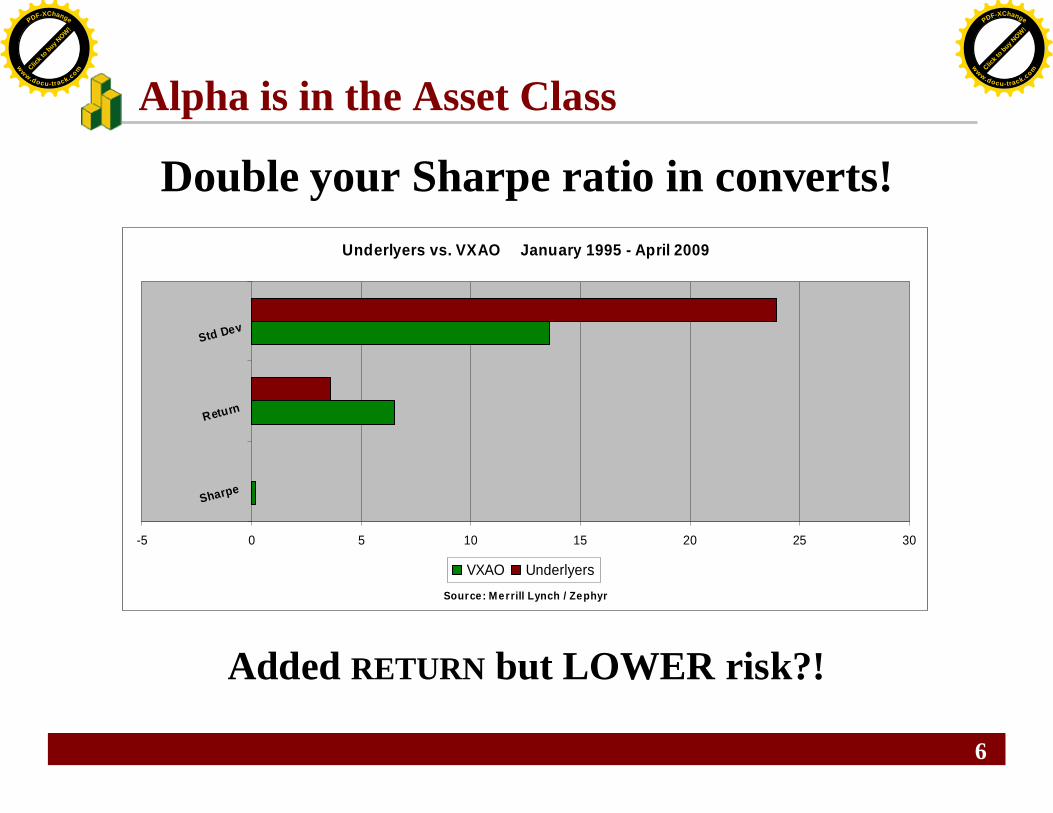

Double your Sharpe ratio in converts

Alpha is in the Asset ClassNature of the Instrument ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

6

Double your Sharpe ratio in converts!

Added RETURN but LOWER risk?!

Alpha is in the Asset Class

Underlyers vs. VXAO January 1995 - April 2009

-5 0 5 10 15 20 25 30

Sharpe

Return

Std Dev

Source: Merrill Lynch / Zephyr

VXAO Underlyers

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

7

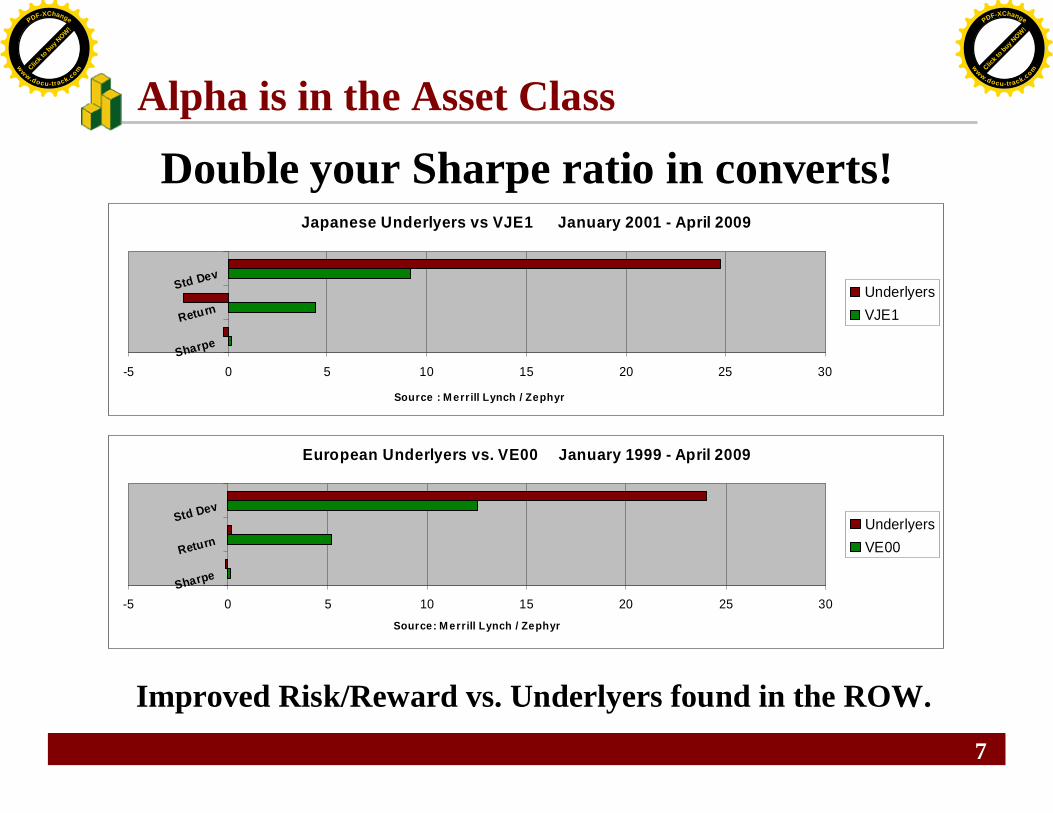

Double your Sharpe ratio in converts!

Improved Risk/Reward vs. Underlyers found in the ROW.

Alpha is in the Asset Class

Japanese Underlyers vs VJE1 January 2001 - April 2009

-5 0 5 10 15 20 25 30Sharpe

Return

Std Dev

Source : Merrill Lynch / Zephyr

UnderlyersVJE1

European Underlyers vs. VE00 January 1999 - April 2009

-5 0 5 10 15 20 25 30Sharpe

Return

Std Dev

Source: M errill Lynch / Zephyr

UnderlyersVE00

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

8

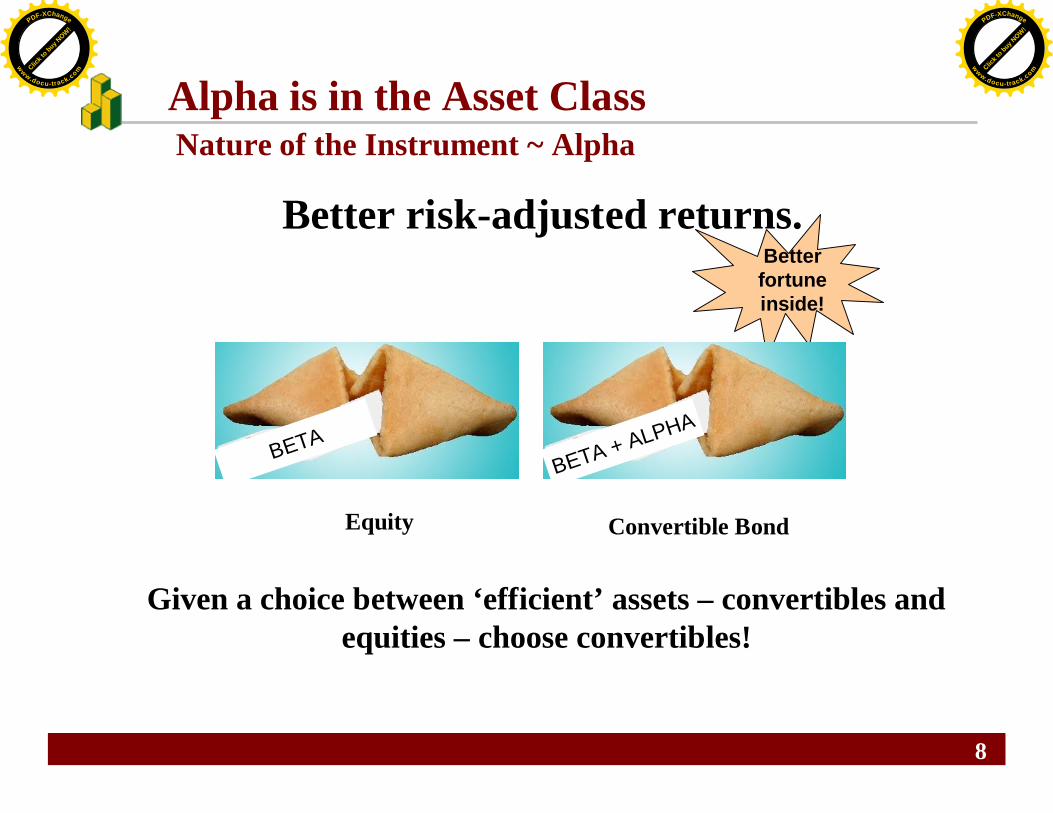

Better risk-adjusted returns.

Equity Convertible Bond

Betterfortuneinside!

Given a choice between ‘efficient’ assets – convertibles andequities – choose convertibles!

Alpha is in the Asset ClassNature of the Instrument ~ Alpha

BETABETA + ALPHA

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

9

Double your Sharpe ratio in converts

Information costs – what markets know

Alpha is in the Asset ClassNature of the Instrument ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

10

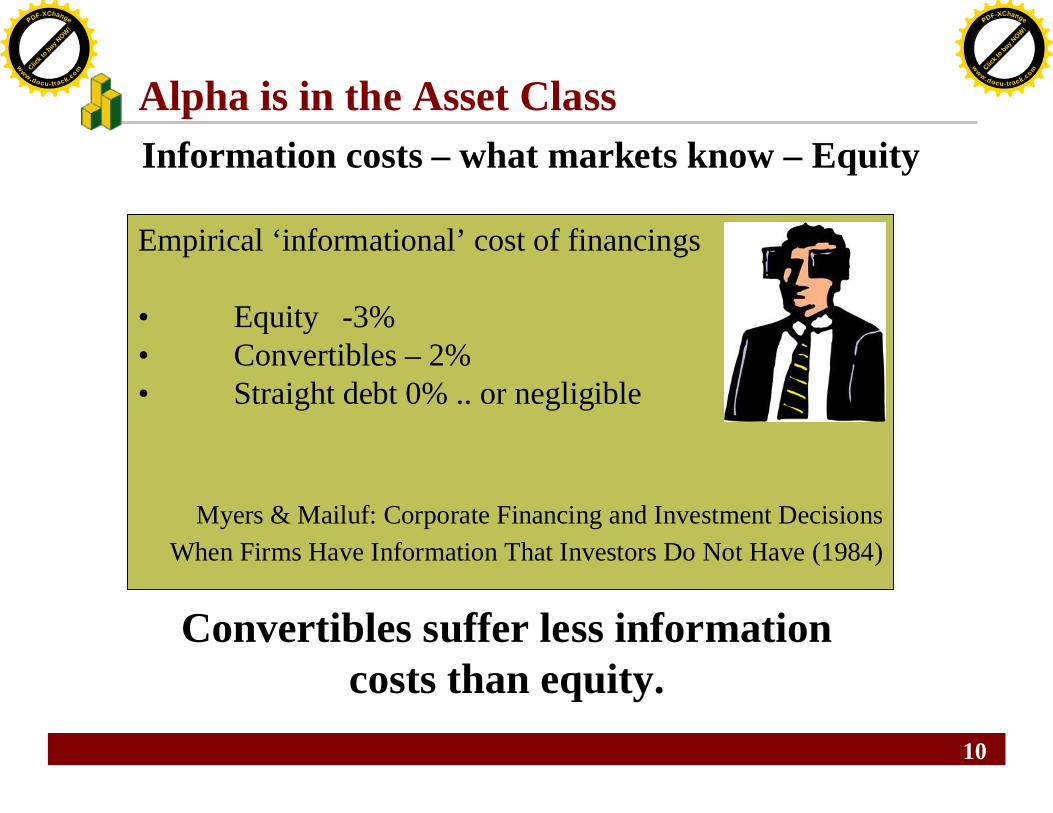

Information costs – what markets know – Equity

Empirical ‘informational’ cost of financings

• Equity -3%• Convertibles – 2%• Straight debt 0% .. or negligible

Myers & Mailuf: Corporate Financing and Investment DecisionsWhen Firms Have Information That Investors Do Not Have (1984)

Convertibles suffer less informationcosts than equity.

Alpha is in the Asset ClassClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

11

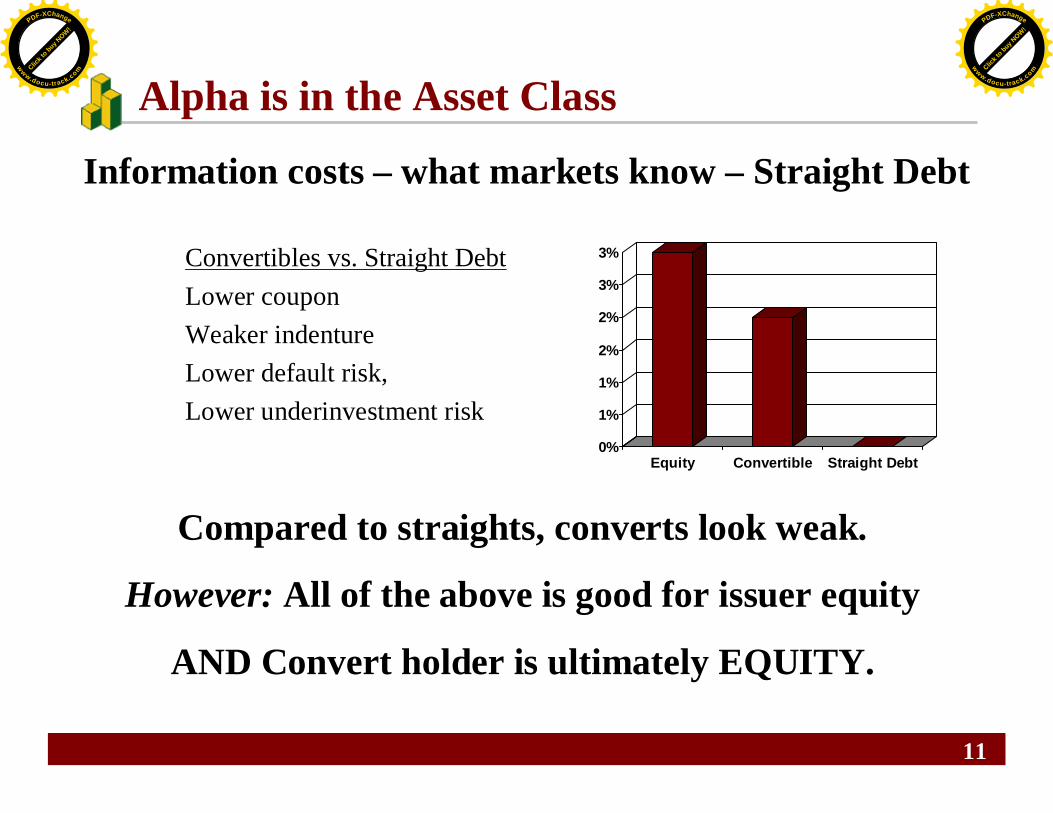

Information costs – what markets know – Straight Debt

0%

1%

1%

2%

2%

3%

3%

Equity Convertible Straight Debt

Convertibles vs. Straight DebtLower couponWeaker indentureLower default risk,Lower underinvestment risk

Compared to straights, converts look weak.

However: All of the above is good for issuer equity

AND Convert holder is ultimately EQUITY.

Alpha is in the Asset ClassClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

12

Double your Sharpe ratio in converts

Information costs – what the markets know

Backdoor equity

Alpha is in the Asset ClassNature of the Instrument ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

13

Backdoor equity

“Companies with limited capital but abundant growthopportunities often find themselves in a bind.”

Jeremy Stein : Convertibles Bonds as Backdoor EquityFinancing (1992)

Converts contribute positivelyto the cost of raising capital.

Alpha is in the Asset ClassNature of the Instrument ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

14

Growth vs. non-growth information costs

Alpha is in the Asset ClassNature of the Issuer (s) ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

15

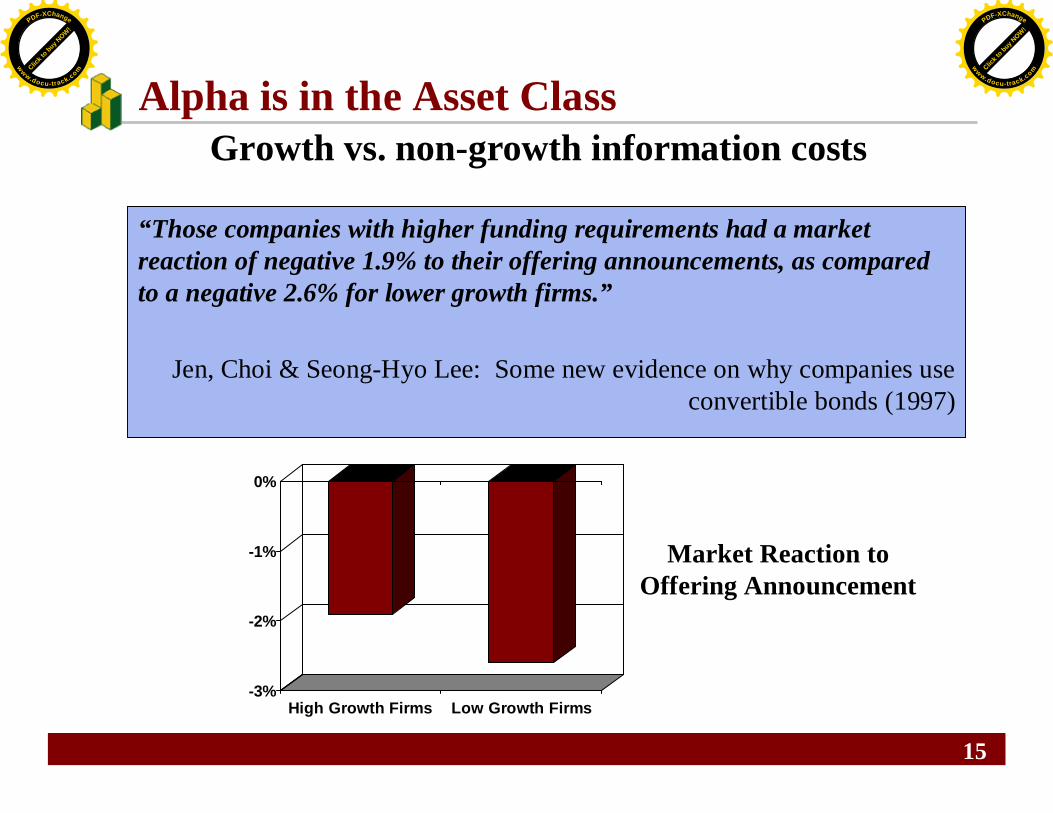

Growth vs. non-growth information costs

-3%

-2%

-1%

0%

High Growth Firms Low Growth Firms

Market Reaction toOffering Announcement

“Those companies with higher funding requirements had a marketreaction of negative 1.9% to their offering announcements, as comparedto a negative 2.6% for lower growth firms.”

Jen, Choi & Seong-Hyo Lee: Some new evidence on why companies useconvertible bonds (1997)

Alpha is in the Asset ClassClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

16

Growth vs. non-growth information costs

Two growth options for one

Alpha is in the Asset ClassNature of the Issuer (s) ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

17

Growth equity option – two growth phases for one

“… today’s future investment opportunities are really“growth options” that may (or may not) be exercised at onepoint in the future.”

David Mayers : Convertible Bonds: Matching Financial & Real OptionsJournal of Applied Corporate Finance (Spring 2000)

2-for-1 sale today!

Alpha is in the Asset ClassClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

18

Growth vs. non-growth information costs

Two growth options for one

Sequenced finance comes at zero cost

Alpha is in the Asset ClassNature of the Issuer (s) ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

19

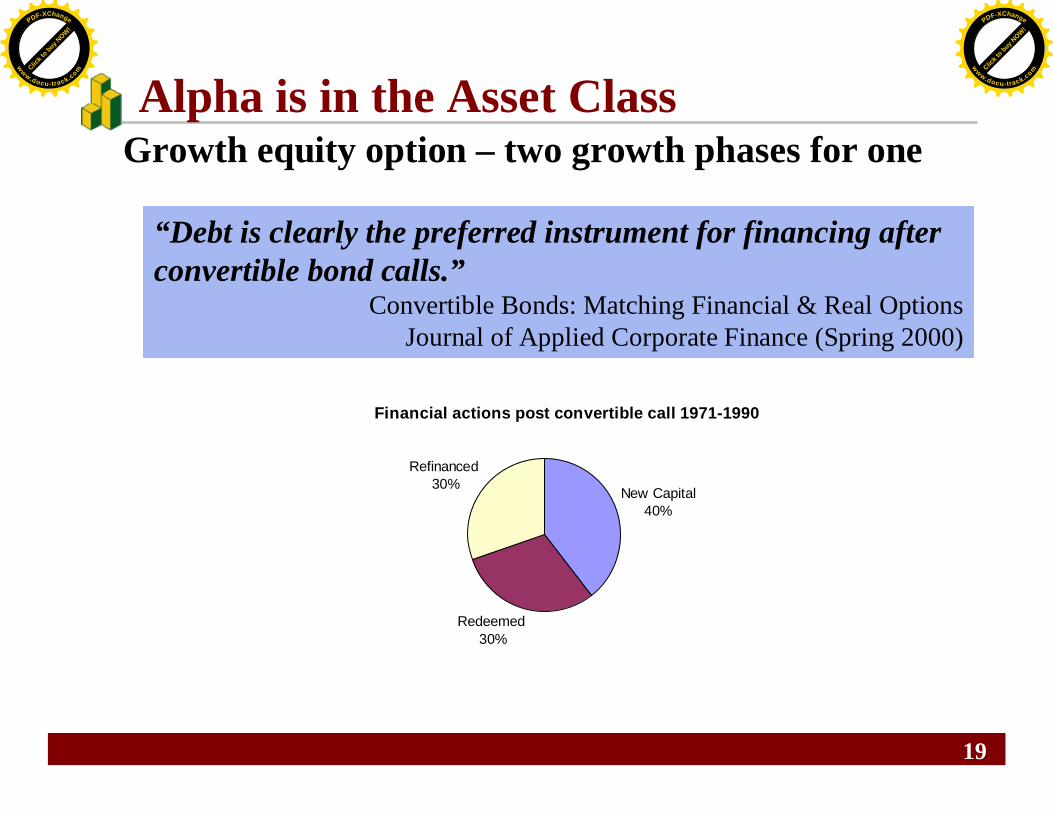

Financial actions post convertible call 1971-1990

New Capital40%

Refinanced 30%

Redeemed 30%

Growth equity option – two growth phases for one

“Debt is clearly the preferred instrument for financing afterconvertible bond calls.”

Convertible Bonds: Matching Financial & Real OptionsJournal of Applied Corporate Finance (Spring 2000)

Alpha is in the Asset ClassClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

20

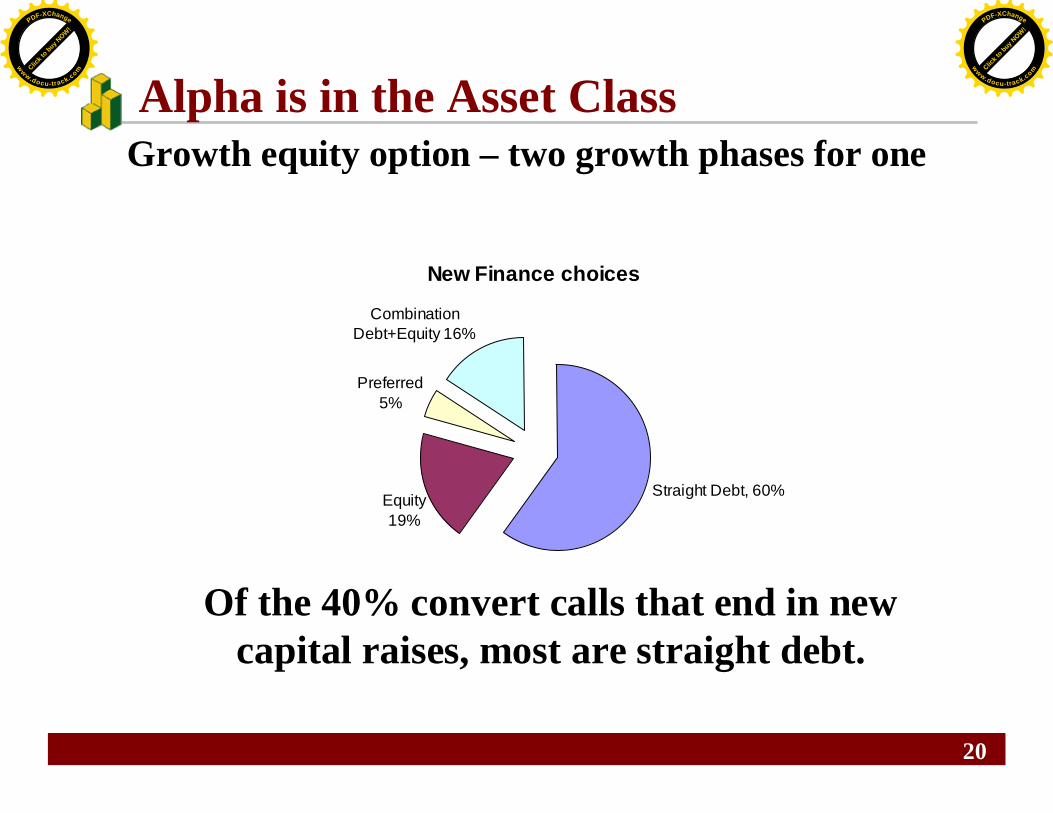

New Finance choices

Straight Debt, 60%

CombinationDebt+Equity 16%

Preferred5%

Equity19%

Growth equity option – two growth phases for one

Of the 40% convert calls that end in newcapital raises, most are straight debt.

Alpha is in the Asset ClassClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

21

Growth vs. non-growth information costs

Two growth options for one

Sequenced finance comes at zero cost

Natural referee: shareholder / bondholderharmony

Alpha is in the Asset ClassNature of the Issuer (s) ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

22

Insensitivity:

•makes the instrument less correlated toits equity or debt.•leads to big changes and big payoffs.

“...the value of convertibles is relatively insensitiveto changes in company risk.”

Brennan & Schwartz: The Case for Convertibles (1981)Chase Financial Quarterly

Alpha is in the Asset ClassNatural Referee: Shareholder / Bondholder Harmony ~ Alpha

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

23

Alpha is in the Asset Class

Alpha Will Persist

Convexity: the Window to Alpha

Good for the Goose; Good for the Gander

Want Long-Only Alpha? Get Convertibles!Clic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

24

Issuance signals confidence

Alpha Will PersistClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

25

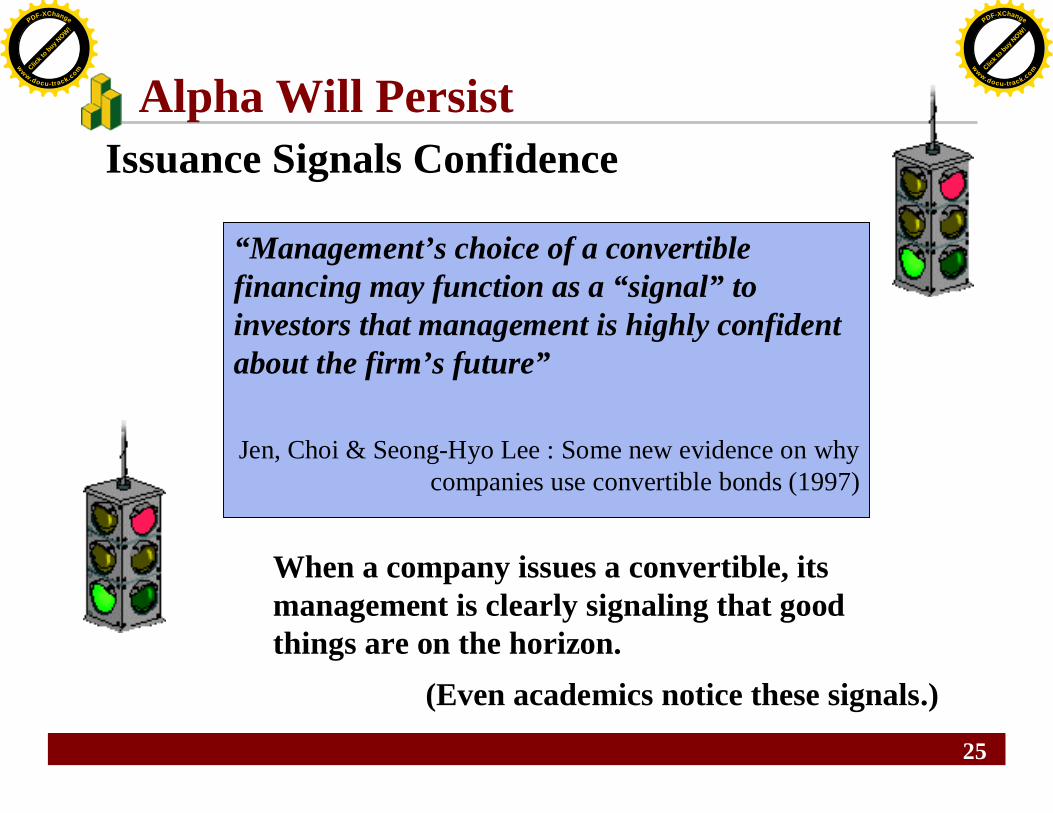

When a company issues a convertible, itsmanagement is clearly signaling that goodthings are on the horizon.

Issuance Signals Confidence

(Even academics notice these signals.)

“Management’s choice of a convertiblefinancing may function as a “signal” toinvestors that management is highly confidentabout the firm’s future”

Jen, Choi & Seong-Hyo Lee : Some new evidence on whycompanies use convertible bonds (1997)

Alpha Will PersistClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

26

Issuance signals confidence

Human endeavor is unquantifiable. Itcannot be arbitraged away.

Alpha Will PersistClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

27

Human endeavor is unquantifiable.

Lowered Costsof Financial Distress

Harmony betweenequity and convertible

debt holders

Growth FundingHypothesis

Confident Management

Backdoor Equity

A Lean, MeanMachine

Given capital and the right levers -- PEOPLE produce alpha.

Alpha Will PersistClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

28

Issuance signals confidence

Human endeavor is unquantifiable. Itcannot be arbitraged away.

Ok..but got any numbers?

Alpha Will PersistClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

29

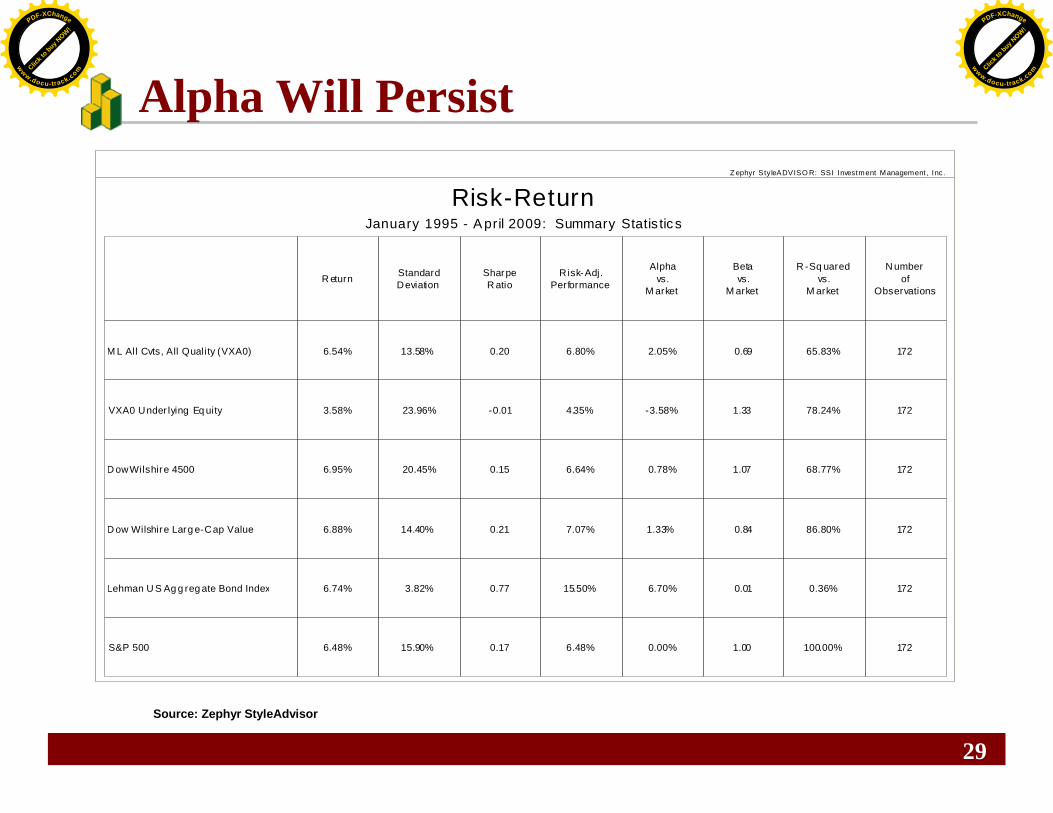

Alpha Will Persist

Source: Zephyr StyleAdvisor

Z ephyr Sty leADVISO R: SSI Investment Management , Inc.

Risk-ReturnJanuary 1995 - A pril 2009: Summary Statis tic s

M L All Cvts, All Quality (VXA0)

R eturn

6.54%

VXA0 Under lying Eq uity 3.58%

StandardDeviation

13.58%

23.96%

SharpeR atio

0.20

-0.01

D ow Wilshire 4500 6.95% 20.45% 0.15

Risk-Adj.Performance

6.80%

4.35%

6.64%

Alphavs.

M arket

2.05%

-3.58%

0.78%

Betavs.

M arket

0.69

1.33

1.07

R -Sq uaredvs.

M arket

65.83%

78.24%

68.77%

N umberof

Observations

172

172

172

D ow Wilshire Larg e-Cap Value 6.88% 14.40% 0.21 7.07% 1.33% 0.84 86.80% 172

Lehman U S Ag g reg ate Bond Index 6.74% 3.82% 0.77 15.50% 6.70% 0.01 0.36% 172

S&P 500 6.48% 15.90% 0.17 6.48% 0.00% 1.00 100.00% 172

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

30

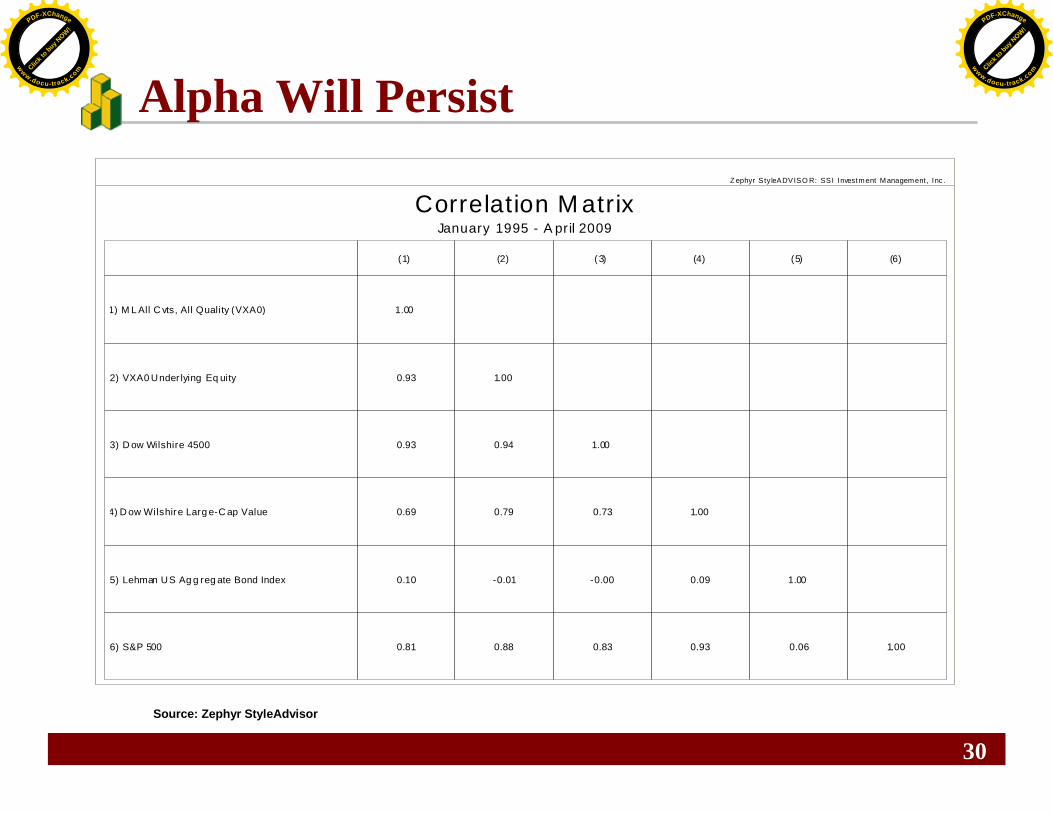

Alpha Will Persist

Source: Zephyr StyleAdvisor

Z ephyr S ty leADVISO R: SSI Investment Management , Inc .

Correlation M atrixJanuary 1995 - A pril 2009

1) M L All C vts, All Quality (VXA0)

(1)

1.00

2) VXA0 Under lying Eq uity 0.93

(2)

1.00

3) D ow Wilshire 4500 0.93 0.94

(3)

1.00

4) D ow Wilshire Larg e-C ap Value 0.69 0.79 0.73

5) Lehman US Ag g reg ate Bond Index 0.10 -0.01 -0.00

(4)

1.00

0.09

(5)

1.00

6) S&P 500 0.81 0.88 0.83 0.93 0.06

(6)

1.00

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

31

Alpha is in the Asset Class

Alpha Will Persist

Convexity : the Window to Alpha

Good for the Goose; Good for the Gander

Want Long-Only Alpha? Get Convertibles!Clic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

32

The best referees are balanced! (convexity)

Convexity : The Window to AlphaClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

33

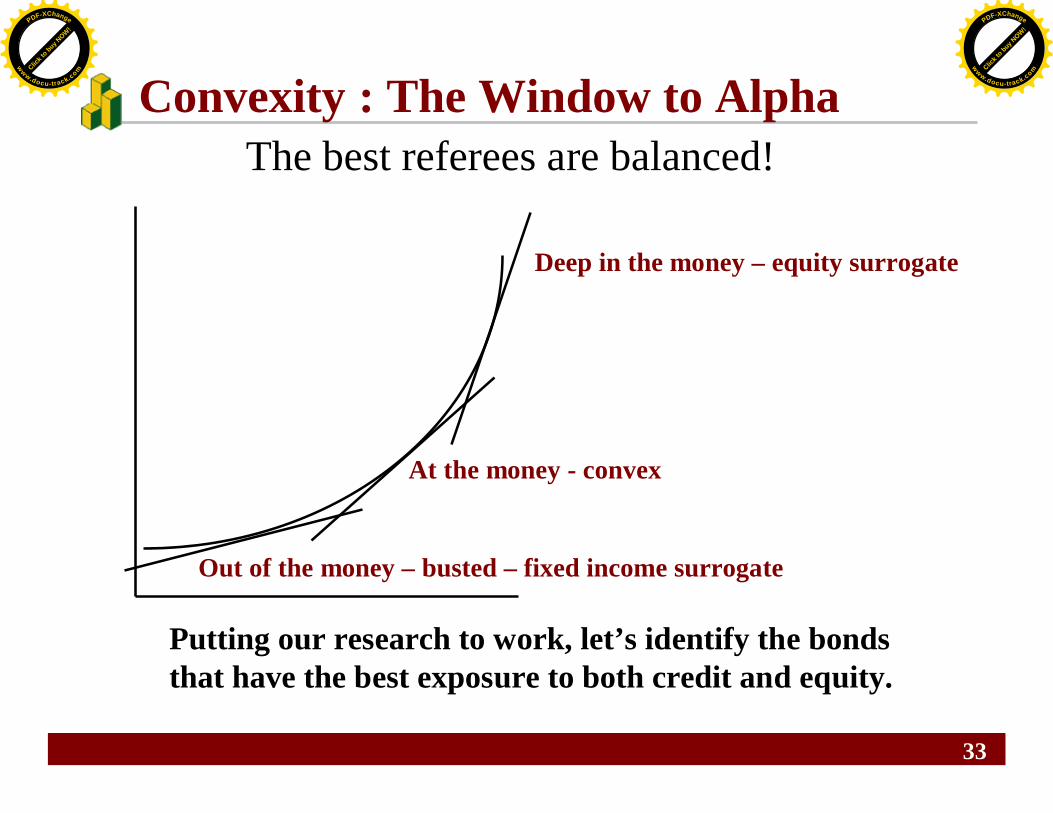

Deep in the money – equity surrogate

At the money - convex

Out of the money – busted – fixed income surrogate

The best referees are balanced!

Putting our research to work, let’s identify the bondsthat have the best exposure to both credit and equity.

Convexity : The Window to AlphaClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

34

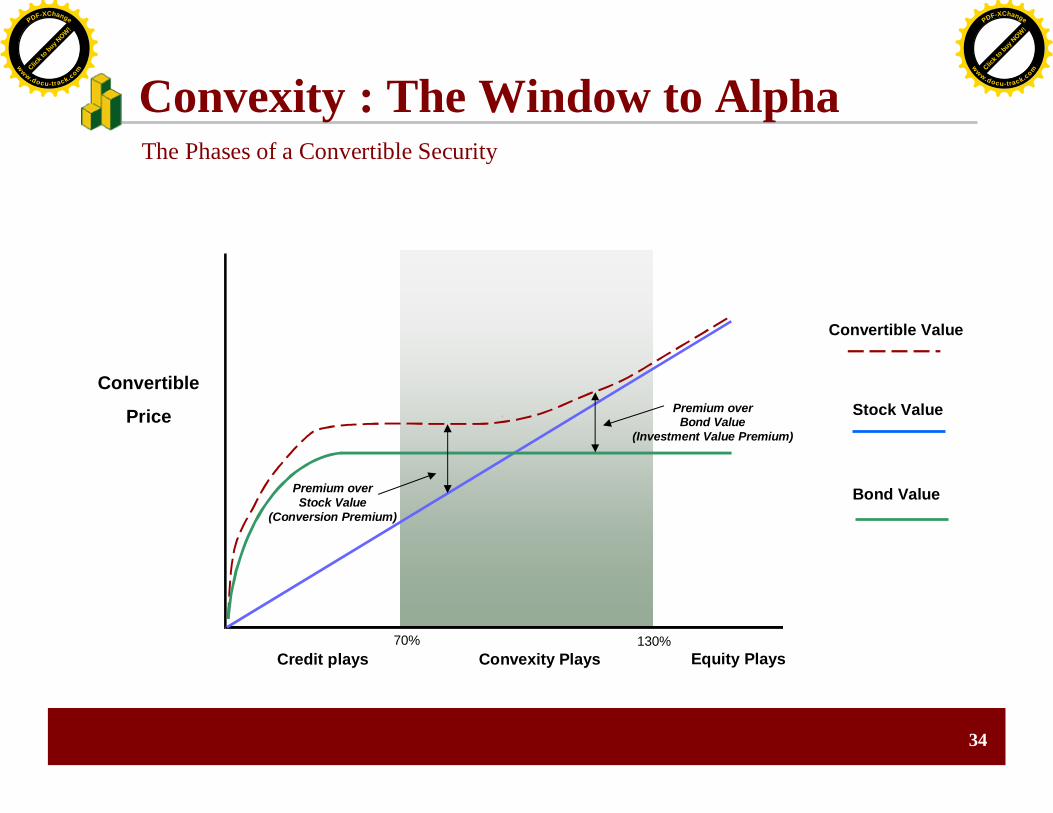

Convexity Plays

Convertible

Price

Premium overStock Value

(Conversion Premium)

Bond Value

Stock Value

Convertible Value

Equity PlaysCredit plays70% 130%

Premium overBond Value

(Investment Value Premium)

The Phases of a Convertible Security

Convexity : The Window to AlphaClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

35

The best referees are balanced! (convexity)

Convexity optimization test

Convexity : The Window to AlphaClic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

36

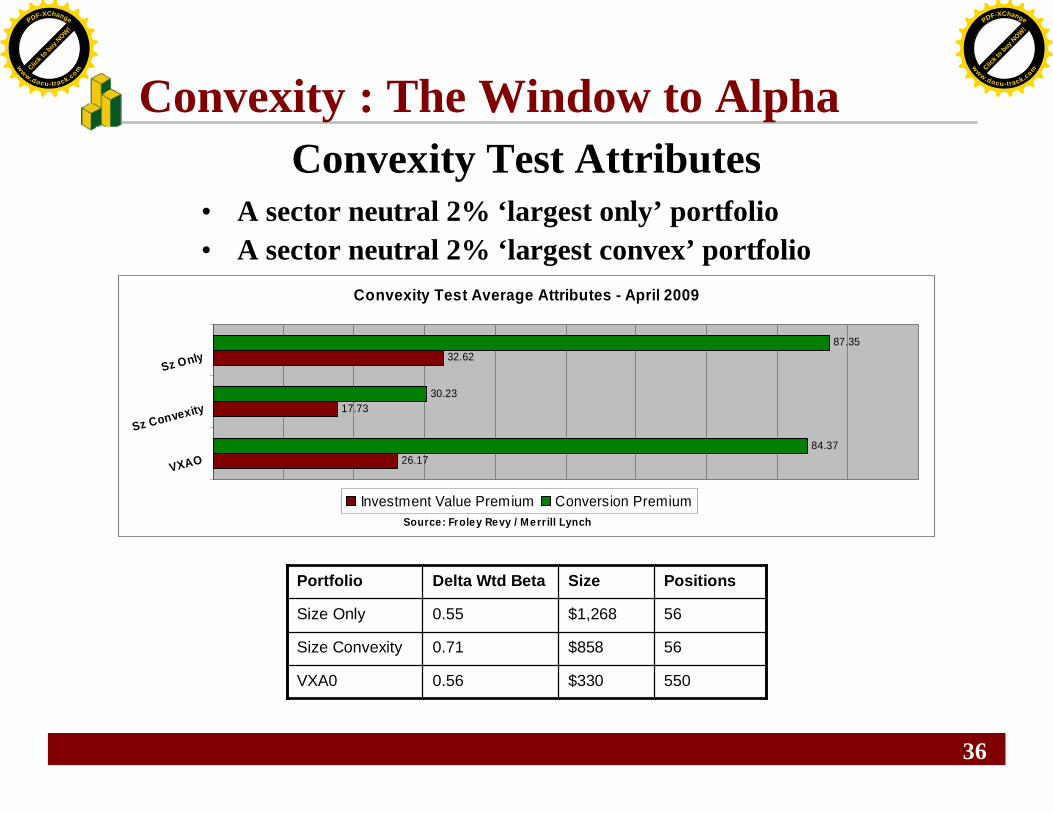

Convexity Test Attributes• A sector neutral 2% ‘largest only’ portfolio• A sector neutral 2% ‘largest convex’ portfolio

Convexity : The Window to Alpha

550$3300.56VXA0

56$8580.71Size Convexity

56$1,2680.55Size Only

PositionsSizeDelta Wtd BetaPortfolio

Convexity Test Average Attributes - April 2009

26.17

17.73

32.62

84.37

30.23

87.35

VXAO

Sz Convexity

Sz Only

Source: Froley Revy / Merr ill Lynch

Investment Value Premium Conversion Premium

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

37

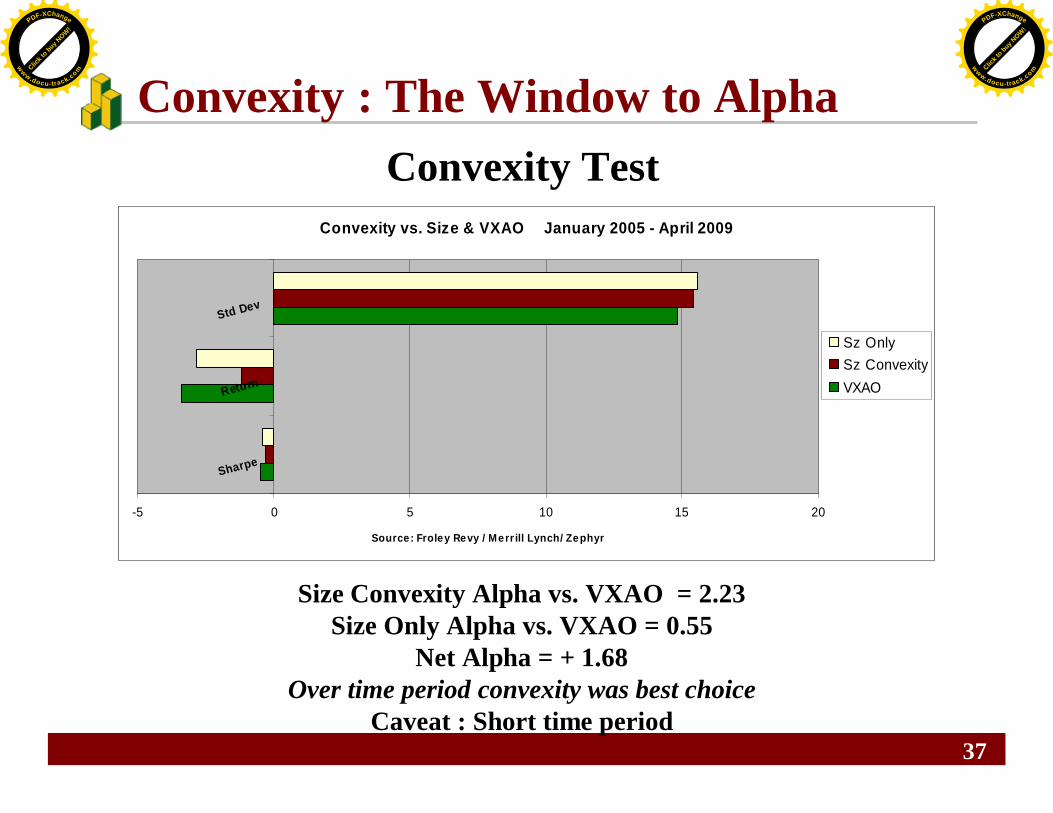

Convexity Test

Size Convexity Alpha vs. VXAO = 2.23Size Only Alpha vs. VXAO = 0.55

Net Alpha = + 1.68Over time period convexity was best choice

Caveat : Short time period

Convexity : The Window to Alpha

Convexity vs. Size & VXAO January 2005 - April 2009

-5 0 5 10 15 20

Sharpe

Return

Std Dev

Source: Froley Revy / Merr ill Lynch/ Zephyr

Sz OnlySz ConvexityVXAO

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

38

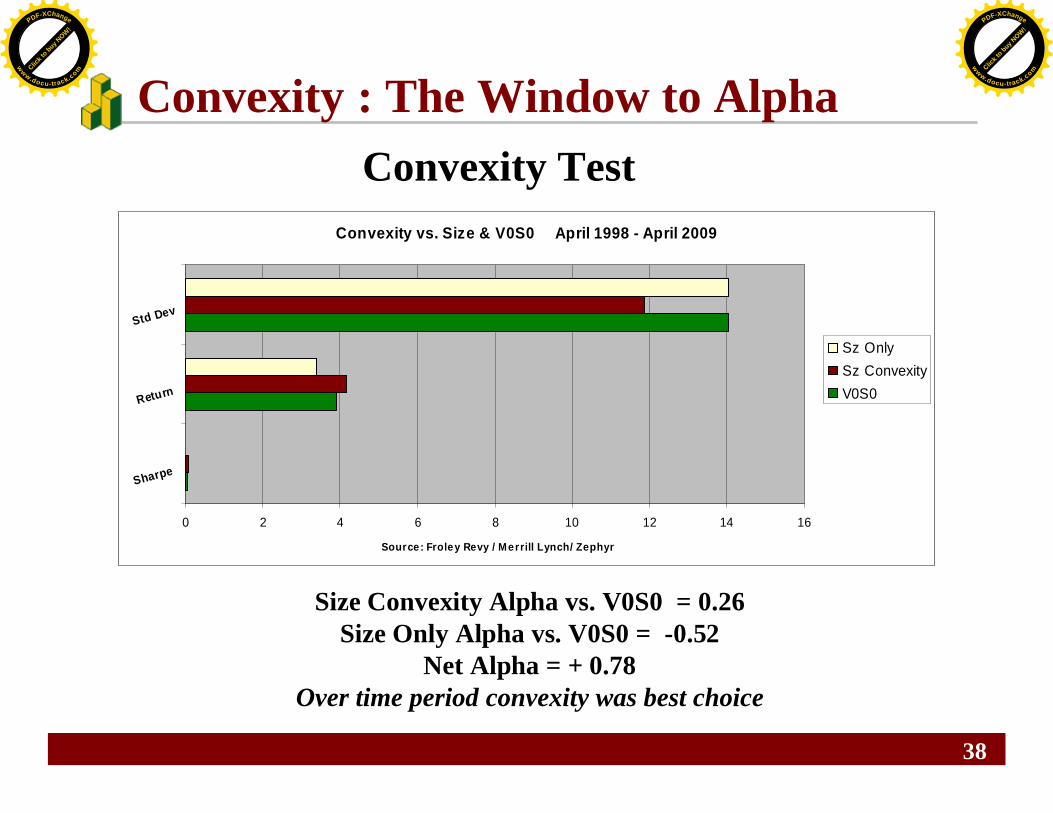

Convexity Test

Size Convexity Alpha vs. V0S0 = 0.26Size Only Alpha vs. V0S0 = -0.52

Net Alpha = + 0.78Over time period convexity was best choice

Convexity : The Window to Alpha

Convexity vs. Size & V0S0 April 1998 - April 2009

0 2 4 6 8 10 12 14 16

Sharpe

Return

Std Dev

Source: Froley Revy / Merrill Lynch/ Zephyr

Sz OnlySz ConvexityV0S0

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

39

Alpha is in the Asset Class

Alpha Will Persist

Convexity: the Window to Alpha

Good for the Goose; Good for the Gander

Want Long-Only Alpha? Get Convertibles!Clic

k to buy N

OW!PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

40

Good for the Goose; Good for the Gander

Nature of the instrument ~ Alpha

Nature of the issuer (s) ~ Alpha

Natural referee ~ Alpha

What is Good for Goose (Issuer) and Gander (Investor)?

Alpha in many locations!!!

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

41

Converts are ONLY instrument convex to a capitalstructure.

And not just any cap structure….

Capital optimizing growth company structures

Growth companies have asymmetric payoffs

Asymmetry means persistent alpha– it means performance.

Good for the Goose; Good for the GanderWhat is Good for Goose (Issuer) and Gander (Investor)?

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com

42

The take - away:

Buy convex convertibles.

Buy convertibles with a growth bias.

Get long-only alpha.

Good for the Goose; Good for the GanderSummary

Click t

o buy NOW!

PDF-XChange

www.docu-track.com Clic

k to buy N

OW!PDF-XChange

www.docu-track.com