National Transformation in the Middle East –A Digital...

16

National Transformation in the Middle East – A Digital Journey Executive Summary

Transcript of National Transformation in the Middle East –A Digital...

National Transformation in theMiddle East – A Digital JourneyExecutive Summary

2

Abstract

Download the full version @

e.huawei.com/ae/edm/global/NationalTransformationInTheMiddleEast

Digital is having a profound impact on Middle Eastern economies, societies and

future sustainability. In light of this, Deloitte has worked with Huawei to develop a

white paper regarding the Digital Transformation initiatives being undertaken by

government entities in the GCC region in the context of global trends and by

analyzing drivers and challenges.

ICT and Digital Transformation technologies have an increasingly significant role in

enabling national transformation plans, especially as they gain maturity and new

applications are developed. It is estimated that every 20 percent increase in ICT

investment results in an over 1 percent growth in a country’s GDP. Middle East

government entities are expected to spend over US$15 billion in 2018 in Digital

Transformation enabling technologies, whilst even the most advanced countries in

the region still lag behind other global economies in terms of Digital Government

according to National ICT indices.

The paper deep dives into six key themes that are considered of high priority to local

policymakers whilst providing global experiences for successfully undertaking Digital

Transformation across these themes. It subsequently, provides a roadmap and

recommendations for regional government agencies to help them overcome

roadblocks in their digital journey and unlock opportunities.

While the study is based on Deloitte and Huawei research, international Digital

Government surveys, interviews with regional governments and subject matter

experts, we do not however presume that ours is the last word on any given topic:

our intent is to catalyze discussions and positive developments in the area in the best

interest of regional governments, businesses and civil society alike.

Saudi Arabia

Oman

KuwaitQatar

Bahrain

UAESwitzerlandFrance

New ZealandAustralia

United States

Brasil

>79%70-79%60-69%50-59%<50%

Source: Deloitte research and analysis, based on various published national indices and indicators from World Economic Forum

Chile

Canada Sweden

Netherlands

Norway

United Kingdom

Algeria

Egypt

Nigeria

South Africa

Finland

GCCSouth KoreaGermany

Estonia

Denmark

Russia

China

India

Japan

SingaporePakistan

01

The impact of digital and ICT in Public

Sector transformation

Demographic changes, new societal

behaviours, and technological

breakthroughs are among the key drivers

transforming the Public Sector today.

While the drivers of Public Sector

disruption are manifold, this paper chose

to place a particular emphasis on the role

of digital in governmental transformation

due to its large potential impact. It is

estimated that Digital Transformation

technologies globally will represent close

to US$ 1.2 trillion in 2017, with half of IT

spending dedicated to new technologies

that enable Digital Transformation1.

ICT and Digital Transformation

technologies have an increasingly

significant impact on the economy, society

and sustainability, especially as they gain

maturity and new applications are

developed. To give a sense of the scale of

Digital Transformation’s potential benefits,

it is estimated that every 20 percent

increase in ICT investment results in

more than 1 percent growth in a

country’s GDP2, 3.

Beyond its direct contribution to economic

impact, digitizing Public Sector entities

and services can bring about major

improvements for governments, citizens,

and businesses; this, in turn, can

contribute to the competitiveness of an

entire nation. According to Deloitte’s

National ICT Index*, the GCC has made

significant progress in recent years, but

on average, lags behind other developed

economies in terms of Digital Government

capablities.

Digital Transformation in the Public Sector

Figure 1: National ICT Index – Scores

*The National ICT Index measures Telecommunications Infrastructure Adoption (e.g. fixed and mobile broadband penetration, smartphone

penetration), Political and Regulatory ICT Environment, Government ICT Adoption4, Social ICT Impact and National ICT Knowledge

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

The convergence of four prominenttechnologies: social applications, mobile technologies, big data analyticsand cloud infrastructure represent a combined global market ofapproximately US$1.2 trillion in 2017.

02

Key themes for Digital Transformation

– from a global to GCC focus

As part of a recent global report “Gov2020:

A Journey into the Future of Government”5,

Deloitte identified 204 public sector

trends which will shape the future of the

Public Sector in the coming years. For the

purpose of this paper, these trends were

grouped into key themes which were in

turn filtered using two dimensions

(relevance to Middle East and impact on

economy, society and sustainability) to

arrive at six key themes:

• Next Generation Care: use of ICT to

provide pervasive, preventative, efficient,

and personalized care

• Classroom of the Future:

transformation of traditional education

systems to digitally-enabled learning

• Smart Government: use of integrated

ICT in government policies, services, and

processes

• Future of Mobility: frictionless,

automated, personalized travel on

demand

• Smart City: cities that use smart

technologies, data analysis, and

innovation to improve quality of life

• Smart Tourism: use of ICT to promote

travel and tourism by enhancing the

visitor experience.

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

Governments around the

world are in the midst of

a historic transformation

as they abandon analog

operating models in favor

of digital systems.

03

New ambitions and the imperative for

change

GCC countries, at various points in time,

have been confronted with a sense of

urgency to diversify their largely

hydrocarbon-dependent economies. This

has prompted a wave of national vision

upgrades, the most recent of which

includes the Saudi Vision 2030 unveiled in

2016, the New Kuwait 2035 vision

launched earlier this year, as well as the

Qatar National Vision 2030 and UAE Vision

2021 established earlier6.

A number of ‘digital-ICT-first’ sub-

strategies and programs have already

been formulated across the GCC. The UAE

ICT 2021 Strategy and UAE National

Innovation Strategy prioritize digital

technology as one of the top seven

national sectors. In KSA, Digital

Transformation is a top-four priority in the

National Transformation Plan (NTP) 2020,

which highlights 29 essential digital

initiatives for key sectors as well as funding

for national digital assets. In Qatar, the

Qatar Digital Government 2020 Strategy

targets efficient and transparent delivery

of government services, while Kuwait has

also revealed an updated e-government

program.

Digital at the heart ofGCC’s transformation

Bahrain National Planning

Development Strategy

Oman National Program for Enhancing

Economic Diversification

GCC national visions and plans

Saudi ArabiaKuwait Qatar UAEBahrain Oman

• e-government program (e.g. national datacenter, government data network, smart card)

• ICT 2020 program (e.Oman)

• e-government program

• Digital Government 2020 strategy• National ICT plan• e-government 2020 strategy (Hukoomi)

• ICT 2021 strategy• Innovation strategy• UAE TRA strategy

• NTP ICT programs (e.g. broadband expansion, ICT human capital, e-commerce)

National visions

National plans

ICT and digitalprograms

Figure 2: ICT and digital programs in GCC national visions and plans

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

A number of 'digital-ICT-

first' sub-strategies and

programs have already

been formulated across

the GCC.

04

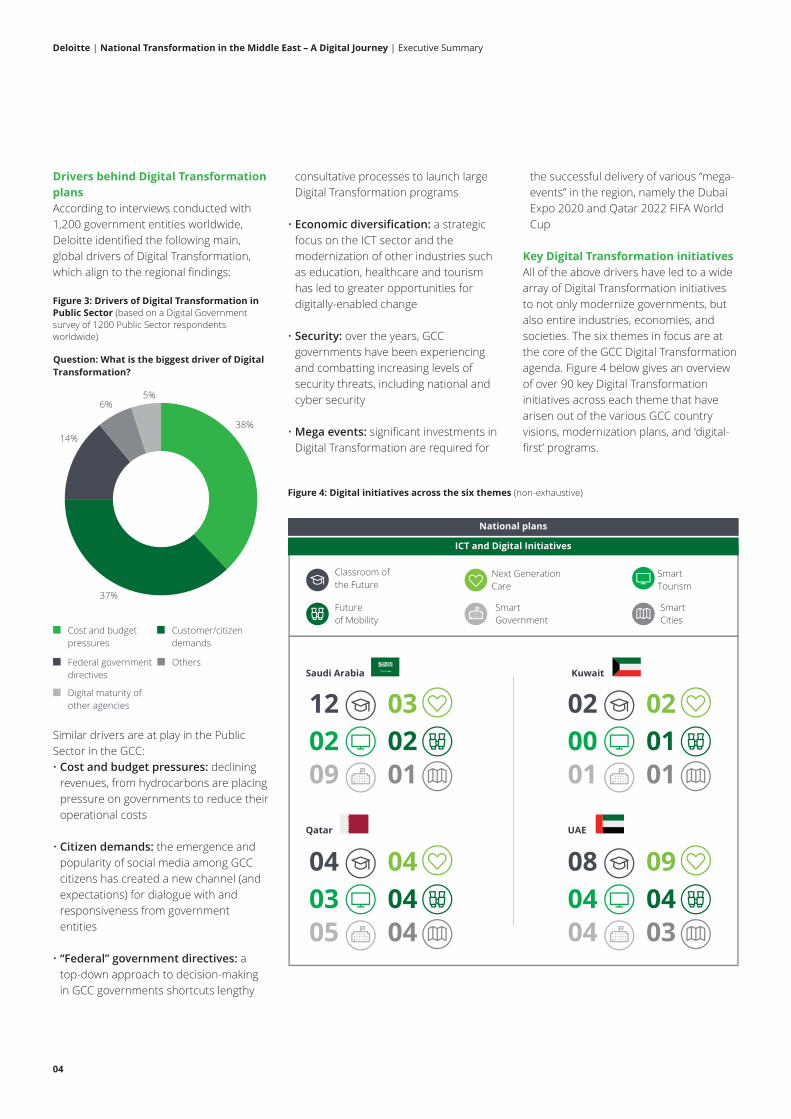

Drivers behind Digital Transformation

plans

According to interviews conducted with

1,200 government entities worldwide,

Deloitte identified the following main,

global drivers of Digital Transformation,

which align to the regional findings:

Figure 3: Drivers of Digital Transformation in

Public Sector (based on a Digital Government

survey of 1200 Public Sector respondents

worldwide)

Similar drivers are at play in the Public

Sector in the GCC:

• Cost and budget pressures: declining

revenues, from hydrocarbons are placing

pressure on governments to reduce their

operational costs

• Citizen demands: the emergence and

popularity of social media among GCC

citizens has created a new channel (and

expectations) for dialogue with and

responsiveness from government

entities

• “Federal” government directives: a

top-down approach to decision-making

in GCC governments shortcuts lengthy

consultative processes to launch large

Digital Transformation programs

• Economic diversification: a strategic

focus on the ICT sector and the

modernization of other industries such

as education, healthcare and tourism

has led to greater opportunities for

digitally-enabled change

• Security: over the years, GCC

governments have been experiencing

and combatting increasing levels of

security threats, including national and

cyber security

• Mega events: significant investments in

Digital Transformation are required for

the successful delivery of various “mega-

events” in the region, namely the Dubai

Expo 2020 and Qatar 2022 FIFA World

Cup

Key Digital Transformation initiatives

All of the above drivers have led to a wide

array of Digital Transformation initiatives

to not only modernize governments, but

also entire industries, economies, and

societies. The six themes in focus are at

the core of the GCC Digital Transformation

agenda. Figure 4 below gives an overview

of over 90 key Digital Transformation

initiatives across each theme that have

arisen out of the various GCC country

visions, modernization plans, and ‘digital-

first’ programs.

Question: What is the biggest driver of Digital Transformation?

38%

37%

Cost and budget pressures

Customer/citizen demands

Federal government directives

14%

6%5%

Digital maturity of other agencies

OthersSaudi Arabia

12 0302 0209 01

Kuwait

Qatar

Classroom of the Future

Next GenerationCare

Smart Tourism

Future of Mobility

Smart Government

Smart Cities

UAE

02 0200 0101 01

04 0403 0405 04

08 0904 0404 03

National plans

ICT and Digital Initiatives

Figure 4: Digital initiatives across the six themes (non-exhaustive)

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

05

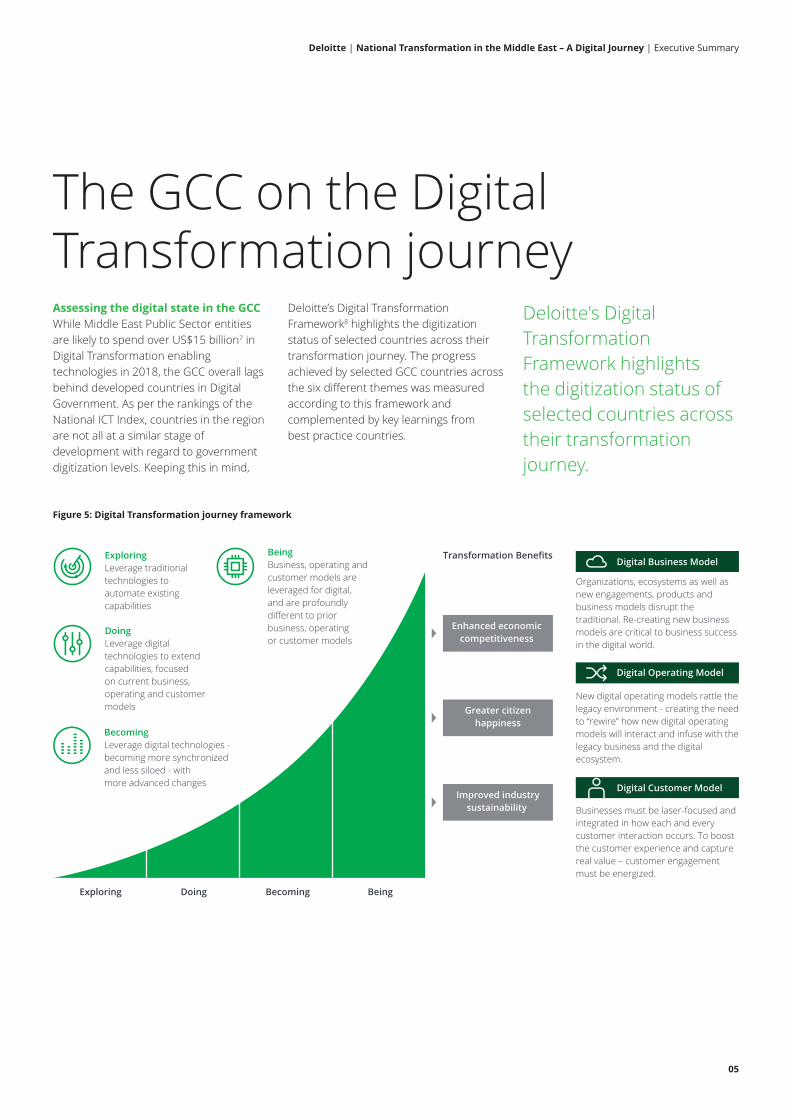

Assessing the digital state in the GCC

While Middle East Public Sector entities

are likely to spend over US$15 billion7 in

Digital Transformation enabling

technologies in 2018, the GCC overall lags

behind developed countries in Digital

Government. As per the rankings of the

National ICT Index, countries in the region

are not all at a similar stage of

development with regard to government

digitization levels. Keeping this in mind,

Deloitte’s Digital Transformation

Framework8 highlights the digitization

status of selected countries across their

transformation journey. The progress

achieved by selected GCC countries across

the six different themes was measured

according to this framework and

complemented by key learnings from

best practice countries.

The GCC on the DigitalTransformation journey

ExploringLeverage traditional technologies to automate existing capabilities

Transformation Benefits

DoingLeverage digital technologies to extend capabilities, focused on current business, operating and customer models

BecomingLeverage digital technologies - becoming more synchronized and less siloed - with more advanced changes

BeingBusiness, operating and customer models are leveraged for digital, and are profoundly different to prior business, operating or customer models

Exploring Doing Becoming Being

Organizations, ecosystems as well as new engagements, products and business models disrupt the traditional. Re-creating new business models are critical to business success in the digital world.

New digital operating models rattle the legacy environment - creating the need to “rewire” how new digital operating models will interact and infuse with the legacy business and the digital ecosystem.

Businesses must be laser-focused and integrated in how each and every customer interaction occurs. To boost the customer experience and capture real value – customer engagement must be energized.

Digital Business Model

Enhanced economic competitiveness

Greater citizenhappiness

Improved industrysustainability

Digital Operating Model

Digital Customer Model

Figure 5: Digital Transformation journey framework

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

Deloitte's Digital

Transformation

Framework highlights

the digitization status of

selected countries across

their transformation

journey.

06

With more than 60 percent of the Saudi population under the age of 30, the Kingdom is putting great focus on its education sector

The UAE is introducing innovative services and solutions in becoming a smart government

Dubai has launched an ambitious Smart City program with the aim to become the smartest city by 2017

In addition to Dubai’s Smart City plan, the UAE overall is introducing innovative transport solutions

With the recent launch of TASMU, Qatar is going through transformational changes especially in the healthcare sector

With the NTP and an increased focus on religious tourism, multiple digital initiatives are being set up

Classroom ofthe Future

SmartGovernment

SmartCities

Future ofMobility

Next GenerationCare

Smart Tourism

CommentsSelected countries

Exploring Doing Becoming Being

Figure 6: Digital maturity assessment of selected countries across the six themes

While the Middle East Public Sector entities are likely tospend over US$15 billion in Digital Transformation enablingtechnologies in 2018, the GCC overall lags behind manydeveloped countries in Digital Government. Countries in theregion are not all at a similar stage of development withregard to government digitization levels.

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

07

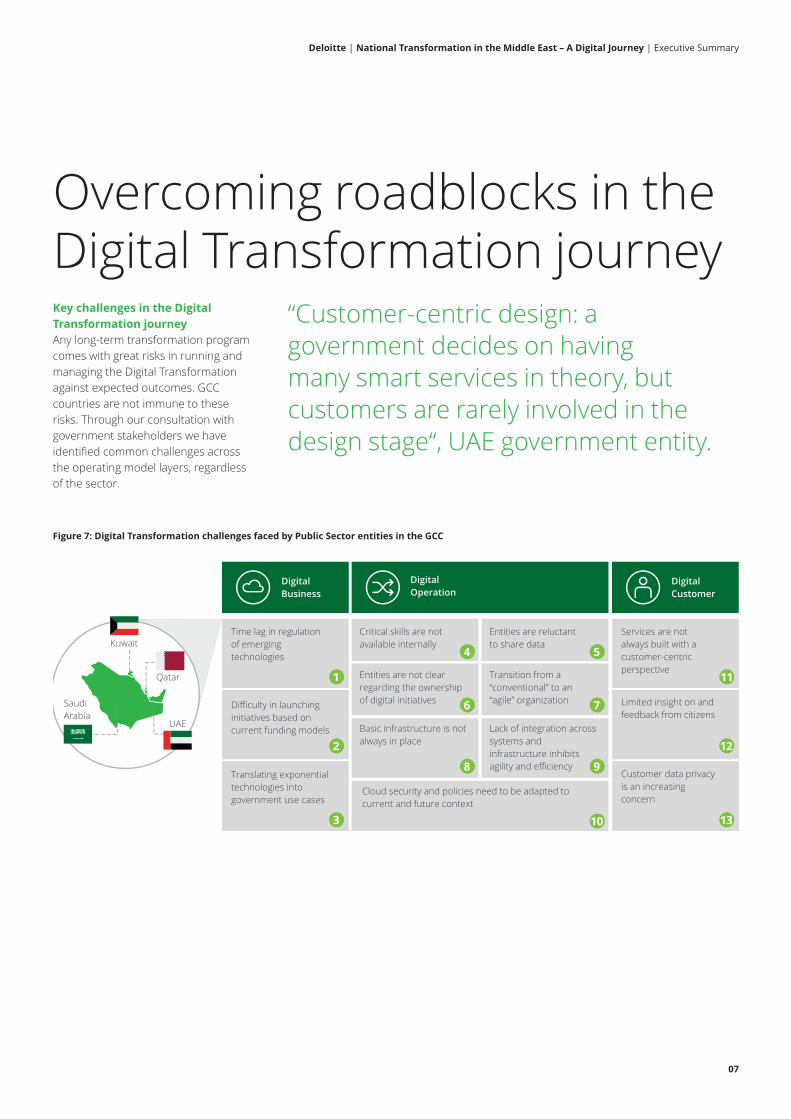

Key challenges in the Digital

Transformation journey

Any long-term transformation program

comes with great risks in running and

managing the Digital Transformation

against expected outcomes. GCC

countries are not immune to these

risks. Through our consultation with

government stakeholders we have

identified common challenges across

the operating model layers, regardless

of the sector.

Overcoming roadblocks in theDigital Transformation journey

11

12

13

DigitalBusiness

DigitalOperation

DigitalCustomer

Time lag in regulation of emerging technologies

Difficulty in launching initiatives based on current funding models

Translating exponential technologies into government use cases

Services are not always built with a customer-centric perspective

Limited insight on and feedback from citizens

Customer data privacy is an increasing concern

Critical skills are not available internally

Entities are not clear regarding the ownership of digital initiatives

Basic infrastructure is not always in place

Cloud security and policies need to be adapted to current and future context

Entities are reluctant to share data

Transition from a “conventional” to an “agile” organization

Lack of integration across systems and infrastructure inhibits agility and efficiency

1

2

3

4 5

6 7

8 9

10

Kuwait

SaudiArabia

Qatar

UAE

“Customer-centric design: agovernment decides on having many smart services in theory, butcustomers are rarely involved in thedesign stage“, UAE government entity.

Figure 7: Digital Transformation challenges faced by Public Sector entities in the GCC

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

08

Implementing Digital Transformation

- a phased approach

Migrating an organization from legacy to

digital operations and systems is a journey

that requires time, patience, and most

importantly a clear vision complemented

by rigorous execution. Based on Deloitte’s

maturity assessment across the six Digital

Transformation themes in the GCC and

the challenges identified, we have

developed a high-level roadmap with

corresponding interventions to help

government towards “being digital”. In

figure 8 below, each intervention is

mapped to a specific challenge.

Play to win - aim for a digital leadership position across private and public sectors

Collaborate with ICT players to define next gen policies for emerging tech

Co-create with digital value chain players on government services

Instill a culture of innovation and start applying agile on pilot new/improved services

Promote digital literacy through tailored trainings. Develop incentive mechanisms to attract digital talent

Create a governance body in charge of the digital agenda and empower to execute

Promote national infrastructure rollouts. Develop national platforms to facilitate integration

Listen to customers in service design to create a bespoke experience and favor adoption

Implement systems to capture real-time data and draw insights to enhance services

Digitalstrategy

DigitalBusiness

Model

DigitalOperation

Model

DigitalCustomer

Model

Regulation

Customerinvolvement

Customerfeedback

Current status of digital maturity in GCC (average based on four focus countries)

Potential digital maturity in GCC (average based on four focus countries) if roadmap adopted

Roadmap steps mapped to challenges addressed

Ecosystem

Digitaloperations

Digitaltalent

Digitalgovernance

Technology

Exploring Doing Becoming Being

1

3

7

4

8

6

9 10

11

11 12

Figure 8: Roadmap to unlock GCC specific challenges in Digital Transformation*

* The interventions have been proposed for a subset of challenges

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

Migrating an organization

from legacy to digital is a

journey that requires

time, patience, and most

importantly a clear vision

complemented by

rigorous execution.

09

The Role of a Digital Value Office in

the Digital Transformation lifecycle

Digital Transformation implementation

programs need to have strong

governance, delivery, and innovation

capabilities in place. A powerful

combination of these attributes can be

found in the concept of a Digital Value

Office (DVO) – a dedicated governing body

for Digital Transformation.

Responsible for the overall

implementation of Digital Transformation

in a Public Sector organization, the DVO

will deliver success across the lifecycle

using two key approaches: firstly, it

governs all stages and enables the

digitalization of functions; secondly, it

applies rapid innovation via the

introduction of minimum viable products

(MVP) to ensure the feasibility, viability, and

desirability of digital outcomes.

The DVO is set up to incubate all the

enablers required for the successful

Digital Transformation of an entity,

addressing the broad categories of key

challenges.

These enablers include: identifying

strategic direction, understanding citizen

needs and trends, instilling innovative

cultures in organizations, regulating

policies, developing agile solutions,

monitoring digital maturity, and securing

suitable technological and ICT

infrastructure and partnerships.

Through these enablers, the DVO acts as

the custodian of entities’ digital maturity

and the prime authority responsible for

delivering the digital outcomes.

Digital factory – OperationsDigitisation – Initiation

Blueprint Sourcing Development Scaling

Value Proposition MinimumViable Product

Strategy articulation

Consult key stakeholders

Determine governancestructure

Secure funding

Prioritize initiatives and develop roadmap

Outside-in

Digital ValueOffice

Ideas in

Initial DigitalSteercom Review

ChangeManagement

DigitalMaturity

PartnerEcosystem

Design &Assurance

Technology & Platforms

BusinessCase

ExecutiveApproval

Funding &Implementation

Track & Measure Benefits

PredefinedAnnual Budget

Concept to MVP MVP to Reality

Figure 9: Overview of the DVO

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

The DVO acts as the

custodian of entities’

digital maturity and

the prime authority

responsible for delivering

the digital outcomes.

10

Public Service in its broaderecosystem

Supp

ort

acti

viti

esCo

re a

ctiv

itie

s

Supp

ort

acti

viti

esCo

re a

ctiv

itie

s

Current Public Sector Value Chain – Technology as support New Public Sector Value Chain – Technology at the core

Human Resources Management

Financial Management

Procurement

Technology

People

Employeeengagement

Service

Client satisfaction

Trust

Citizentrust

People

Employeeengagement

Service

Client satisfaction

Trust

Citizentrust

Infrastructure

Government Service Management with Data visualization

Data Analytics & Information Management

Financial Management

Cyber security

HR and Procurement

Integrated ICT Infrastructure

Dig

ital

tech

nolo

gies

API

… …

Public Sector Applications

Future of Mobility

Classroom of the Future

SmartGovernment

SmartTourism

Smart Cities

Next Generation

Care

Digital Ecosystem Platform

Amazon

HorizontalVertical

Tourism:Airbnb,

Hoojoozat

Mobility:Uber,

Careem

Other Ministries

Hub

MoIHub

MoHHub

MoEHub

Other Platforms

Big DataPlatform

IoTPlatform

AIPlatform Noon

APIAPI

Whole of Government Platform Technology as a Platform

API

CloudPipeDevice

Figure 10: Legacy and future Public Sector value chain

Figure 11: Platform of Platforms

The role of ICT in the Public Sector service

delivery value chain will dramatically

change in the digital age. This role is being

rapidly redefined from that of a passive,

supporting enabler to that of a matrix that

feeds the entire value chain while actively

driving how governments operate and

serve their citizens.

In this new value chain, governments and

regulators face the daunting task of

coping with the fast moving pace of

emerging technologies, especially when it

comes to identifying their relevance in

policy making or service delivery.

How can governments overcome the

complexity of fast evolving technologies as

the digital ecosytem becomes increasingly

complex? How can they best address

stakeholder management challenges

with multiple government agencies and

scattered data? One element of response

is the concept of Platform of Platforms.

By easing the integration between

government stakeholders, digital private

sector providers and technology players,

the Platform of Platforms concept

addresses a number of the key roadblocks

of Digital Transformation.

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

11

The opportunities presented by digital

technologies are substantial and have the

potential to drive significant value in

Middle Eastern economies. The potential

contribution of digital to GDP in these

countries could double in the years to

come if it were to reach the level of other

markets (e.g. the US). For the GCC alone,

this could represent a US$50 billion

increment10, to be compared with the

US$15 billion of investment11 in Digital

Transformation enabling technologies in

these countries.

Going forward, national digital strategies

must be underpinned by four key

principles:

• Riding the disruption wave: Public

Sector entities should adopt disruption

not only as a mode of operation, but as a

way of formulating policies

• Creating new horizons: Making sense

of new technologies is not always easy.

Exponential technologies open up new

avenues and applications that have the

potential to dramatically change the way

services are being delivered

• Delivering an experience: Bringing

customers into the heart of innovation

will change the entire service delivery

concept from that of traditional service

delivery, to that of experience delivery.

• Fail fast, adjust quickly: Incorporating

strategies for agile methods of “concept

to service” development when designing

a new service translates into enhanced

delivery speed, and ultimately greater

satisfaction and adoption.

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

Ecosystem

Technologies

Concept to Service

National government

Stateleadership

Businessand citizens

Telcos & service providers

Professional services

Feasibilityconcept

Buildprototype

Launch minimumviable product

Scale successfully

Concept Reality

Creation lab

Sensors Robotics SDN 3D printing AR/VR Blockchain Machine LearningArtificial Intelligence

Cloud Big Data Analytics Integrated platforms Internet of Things NextGen security 5G Data Dashboard

Figure 13: Delivering Digital Transformation from concept to reality12

In a platform oriented world, supported by

a new digital ecosystem, the flow of value

and relationships between governments,

citizens and private entites will be

redefined around the “government cloud”

as described in the figure on the right:

In a platform orientated

world, supported by a

new digital ecosystem,

the flow of value and

relationships between

governments, citizens

and private entities will

be redefined around the

“government cloud”.

Figure 12: Flow of value in an ecosystem based government services model9

Traditional Government Services Model

Application Platforms Industry Solutions Services Orchestration

Association

Association

Future Government Services Model – Ecosystem Curation

Flow of value

Government Government

Citizen Citizen

Third PartyGovernment

CloudPlatform

Ecos

yste

m 1 Ecosystem

2

Ecos

yste

m 4

Ecosystem 3

Contacts

References

Deloitte | National Transformation in the Middle East – A Digital Journey | Executive Summary

1. “IDC Forecasts $1.2 Trillion in Worldwide

Spending on Digital Transformation

Technologies in 2017”, IDC (23 Feb 2017):

www.idc.com/getdoc.jsp?containerId=prUS4232

7517

2. “Jones Lang LaSalle’s “Connected City” Study

Ties Cities’ Smart Grid Use to Economic Drivers”,

Jones Lang LaSalle (8 Oct 2012): www.us.jll.com

3. “20% increase in ICT investment = 1% growth in

GDP”, TM Forum (23 Jul 2015):

inform.tmforum.org

4. United Nations E-Government Survey,

Department of Economic and Social Affairs

(2016)

5. “Gov2020: A Journey into the Future of

Government” report, “Gov2020: Explore the

Future of Government 2020” website, Deloitte

University Press: government-

2020.dupress.com/

6. Official government websites and press

releases. See: Saudi Arabia Vision 2030 –

www.vision2030.gov.sa/en; UAE Vision 2021 –

www.vision2021.ae/en; Qatar Vision 2030 –

www.mdps.gov.qa/en/qnv1/Pages/default.aspx;

Kuwait vision and plans –

www.newkuwait.gov.kw/en/

7. Monitor Deloitte research and analysis

8. “Being Digital” Framework, Deloitte Digital

9. Monitor Deloitte research and analysis; Huawei

research and analysis; “Huawei’s cloud vison

unfolds as it hosts annual showcase”, ITP (6 Sep

2017): www.itp.net/614562-huaweis-cloud-

vison-unfolds-as-it-hosts-annual-showcase;

“Digital Spillover Measuring the true impact of

the digital economy”, Huawei (5 Sep 2017)

10. Monitor Deloitte research and analysis, based

also on data from multiple sources:

Euromonitor, IDC, UN, World Bank, McKinsey

11. Monitor Deloitte research and analysis, based

also on data from IDC

12. Monitor Deloitte research and analysis; Huawei

concept to service lab: “Building an open and

diverse ecosystem for shared success in the

Middle East”, Huawei (3 Oct 2017):

www.linkedin.com/pulse/building-open-diverse-

ecosystem-shared-success-middle-charles-

yang/?trackingId=csiZysQOGhsmwCMGseJfkQ%

3D%3D; “Digital Spillover Measuring the true

impact of the digital economy”, Huawei (5 Sep

2017)

Authors

Emmanuel Durou

TMT ME Industry Leader and

Partner at Monitor Deloitte

Deloitte & Touche (M.E.)

Hasan Iftikhar

Senior Manager, TMT

Deloitte & Touche (M.E.)

Adil Parvez

Manager, TMT, Monitor Deloitte

Deloitte & Touche (M.E.)

Guilherme Oliveira

Manager, TMT

Deloitte & Touche (M.E.)

Researched and written by:

Jean Louis Prevost

Senior Consultant, TMT,

Monitor Deloitte

Deloitte & Touche (M.E.)

Yasmeen Salah

Senior Consultant, Monitor Deloitte

Deloitte & Touche (M.E.)

Laura Shupp

Consultant, Monitor Deloitte

Deloitte & Touche (M.E.)

Qusay Alonaizan

Business Analyst

Deloitte & Touche (M.E.)

Contributors

Aydin Akca

Partner, Monitor Deloitte

Deloitte & Touche (M.E.)

Mounir Ariss

Partner, Monitor Deloitte

Deloitte & Touche (M.E.)

Muhannad Tayem

Partner

Deloitte & Touche (M.E.)

Jamil Hamati

Senior Manager

Deloitte & Touche (M.E.)

This publication has been written in general terms and therefore cannot be relied on to cover specific

situations; application of the principles set out will depend upon the particular circumstances involved and

we recommend that you obtain professional advice before acting or refraining from acting on any of the

contents of this publication. Deloitte & Touche (M.E.) would be pleased to advise readers on how to apply the

principles set out in this publication to their specific circumstances. Deloitte & Touche (M.E.) accepts no duty

of care or liability for any loss occasioned to any person acting or refraining from action as a result of any

material in this publication.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by

guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member

firms and their related entities are legally separate and independent entities. DTTL (also referred to as

“Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about to learn more

about our global network of member firms.

Deloitte provides audit, consulting, financial advisory, risk advisory, tax and related services to public and

private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies

through a globally connected network of member firms in more than 150 countries and territories bringing

world-class capabilities, insights, and high-quality service to address clients’ most complex business

challenges. To learn more about how Deloitte’s approximately 245,000 professionals make an impact that

matters, please connect with us on Facebook, LinkedIn, or Twitter.

Deloitte & Touche (M.E.) is a member firm of Deloitte Touche Tohmatsu Limited (DTTL) and is a leading

professional services firm established in the Middle East region with uninterrupted presence since 1926.

DTME’s presence in the Middle East region is established through its affiliated independent legal entities

which are licensed to operate and to provide services under the applicable laws and regulations of the

relevant country. DTME’s affiliates and related entities cannot oblige each other and/or DTME, and when

providing services, each affiliate and related entity engages directly and independently with its own clients

and shall only be liable only for its own acts or omissions and not those of any other affiliate.

Deloitte provides audit, tax, consulting, financial advisory and risk advisory services through 25 offices in 14

countries with more than 3,300 partners, directors and staff. It is a Tier 1 Tax advisor in the GCC region since

2010 (according to the International Tax Review World Tax Rankings). It has also received numerous awards in

the last few years which include best Advisory and Consultancy Firm of the Year 2016 in the CFO Middle East

awards, best employer in the Middle East, the Middle East Training & Development Excellence Award by the

Institute of Chartered Accountants in England and Wales (ICAEW), as well as the best CSR integrated

organization.

© 2017 Deloitte & Touche (M.E.). All rights reserved.