National Commercial Bank Investor Presentation 2Q … 2Q... · NCB Investor Relations ... National...

52

NCB Investor Relations 2Q 2017 Investor Presentation 1 National Commercial Bank Investor Presentation 2Q 2017 Results

Transcript of National Commercial Bank Investor Presentation 2Q … 2Q... · NCB Investor Relations ... National...

NCB Investor Relations2Q 2017 Investor Presentation 1

National Commercial Bank

Investor Presentation

2Q 2017 Results

NCB Investor Relations2Q 2017 Investor Presentation 2

Disclaimer

The National Commercial Bank (NCB) prepared this presentation on a proprietary basis as general background information about the activities of NCB. The information contained herein is given in summary form and for discussion purposes only. Some of the information that is relied upon by NCB is obtained from sources believed to be reliable, but NCB (nor any of its directors, officers, employees, agents, affiliates or subsidiaries) does not guarantee the accuracy or completeness of such information, and disclaims all liability or responsibility for any loss or damage caused by any act taken as a result of the information. This presentation including the information covered therein is not intended either to be relied upon or construed as an advertisement for, or an offer, solicitation or invitation to sell or issue, or to subscribe, underwrite or otherwise acquire any securities in any jurisdiction. It should and must not be treated as giving tax, legal, investment or other specialist advice or a recommendation to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. Neither shall any part of this information nor the fact of its distribution form part of or be relied on in connection with any contract or investment decision or commitment relating thereto, nor does it constitute a recommendation regarding the subject of this presentation.

All statements included in this presentation other than statements of historical facts, including, without limitation, those regarding financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives) are forward-looking statements and may thus include words like "anticipate", "believe", "intend", "estimate", "expect", "will", "may", "project", "plan" and such other words of similar meaning. Such forward-looking statements are based on numerous assumptions regarding present and future business strategies and the relevant future business environment. Any forward-looking statements speak only as of the date of this presentation and NCB expressly disclaims to the fullest extent permitted by law any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any change in expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Nothing in the foregoing is intended to or shall exclude any liability for, or remedy in respect of, fraudulent misrepresentation. Due to rounding, numbers and percentages presented throughout this presentation may not add up precisely to the totals provided.

NCB is not under any obligation to update, complete, amend, revise or keep current the information contained herein, and any opinions expressed herein are subject to change materially without notice. Accordingly, no representation or warranty, express or implied, is or will be made by NCB, their respective advisors or any such persons’ directors, officers or employees, or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this presentation, and any reliance you place on them will be at your sole risk. Investors must rely solely on their own examinations of the Offering and relevant documentation in making a determination as to whether to invest in the securities described. An investor should seek independent professional advice when deciding if an investment is appropriate. Securities that may be discussed herein may not be suitable for all investors. Investors are required to make their own independent investigation and appraisal of the business and financial condition of NCB and its subsidiaries, the nature of the securities and the merits or suitability of the securities or any transaction to any investor’s particular situation and objectives, including the possible risks and benefits of purchasing any securities. Any such determination should involve an assessment of the legal, tax, accounting, regulatory, financial, credit or other related aspects of the offering or the securities. Without prejudice to the foregoing, NCB, their advisors and any such persons’ directors, officers or employees expressly disclaim any liability whatsoever, in negligence or otherwise, for any loss howsoever arising, directly or indirectly, from use of, or reliance on, this presentation or its contents or otherwise arising in connection therewith.

NCB Investor Relations2Q 2017 Investor Presentation 3

Investor Presentation

Contents

04

12

18

28

43

51

NCB – The leading KSA bank

Grow with KSA. Grow with NCB.

Strategy Overview

Financial Results

Segmental Overview

Additional Information

NCB Investor Relations2Q 2017 Investor Presentation 4

National Commercial Bank

The Leading KSA Bank

2Q 2017 Results

NCB Investor Relations2Q 2017 Investor Presentation 5

NCB is the leading banking group in Saudi Arabia

Established in 1953; IPO in 2014

NCB Snapshot

Jeddah HQ

>8m Clients12,310Employees

441bn Assets

316bn Deposits

>100bn Market Cap

Wholesale branch in BahrainOffices: Singapore, Seoul, Shanghai

Subsidiary in Turkey:Türkiye Finans Katılım Bankası

Subsidiary in KSA:NCB Capital

NCB Investor Relations2Q 2017 Investor Presentation 6

NCB is the leading banking group in Saudi Arabia

NCB has a strong market and financial position

Financial Position KSA GCC

Assets #1 #4

Financing #1 #4

Deposits #1 #3 tied

Investments #1 #1

Total Operating Income #1 #3

Net Income #1 #3

Market Position by KSA

Overall banking Assets #1

Corporate banking Financing #1

Retail banking Financing #2

Treasury Investments #1

Asset Management AUMs #1

Brokerage Value Traded #3

441

340

231 218 203

0

100

200

300

400

500

NCB Rajhi Samba Riyad BSF

Assets (SRbn)

254 225

143 129 125

0

50

100

150

200

250

300

NCB Rajhi Riyad BSF Samba

Financing (SRbn)

316

273

172 158 157

0

50

100

150

200

250

300

350

NCB Rajhi Samba BSF Riyad

Deposits (SRbn)

NCB Investor Relations2Q 2017 Investor Presentation 7

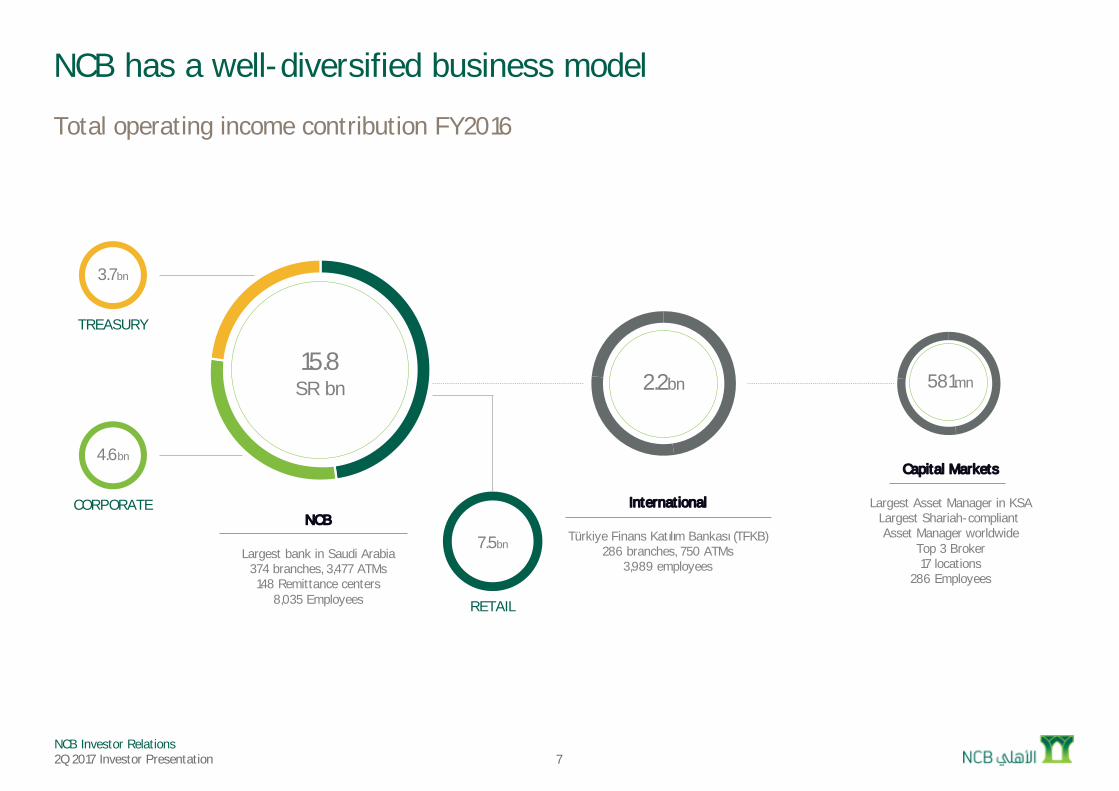

NCB has a well-diversified business model

Total operating income contribution FY2016

Capital Markets

Largest Asset Manager in KSALargest Shariah-compliant Asset Manager worldwide

Top 3 Broker17 locations

286 Employees

15.8SR bn

NCB

Largest bank in Saudi Arabia374 branches, 3,477 ATMs148 Remittance centers

8,035 Employees

7.5bn

4.6bn

3.7bn

RETAIL

CORPORATE

TREASURY

2.2bn 581mn

International

Türkiye Finans Katılım Bankası (TFKB)286 branches, 750 ATMs

3,989 employees

NCB Investor Relations2Q 2017 Investor Presentation 8

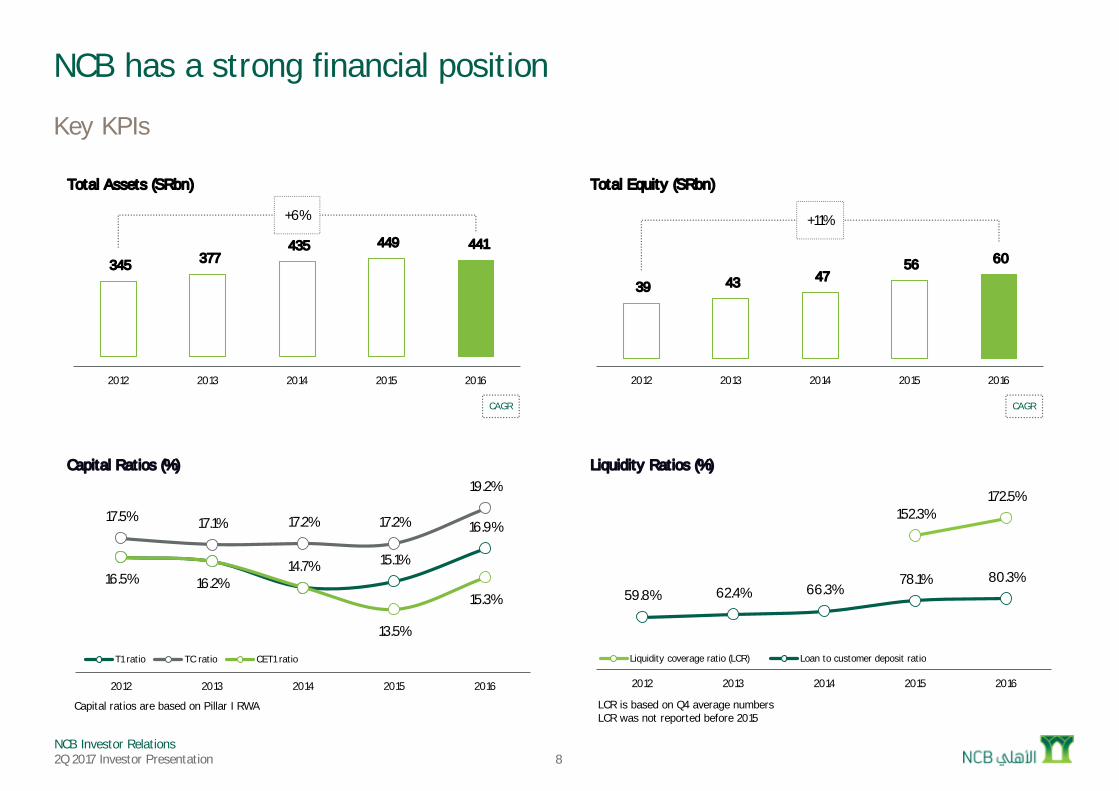

NCB has a strong financial position

Key KPIs

14.7% 15.1%

16.9%17.5% 17.1% 17.2% 17.2%

19.2%

16.5% 16.2%

13.5%

15.3%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

2012 2013 2014 2015 2016

Capital Ratios (%)

T1 ratio TC ratio CET1 ratio

39 43 47 56 60

+11%

0

20

40

60

80

100

2012 2013 2014 2015 2016

Total Equity (SRbn)

345 377 435 449 441

+6%

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016

Total Assets (SRbn)

CAGR CAGR

LCR is based on Q4 average numbersLCR was not reported before 2015

Capital ratios are based on Pillar I RWA

152.3%172.5%

59.8% 62.4% 66.3%78.1% 80.3%

0

0

0

1

1

1

1

1

2

2

2

2012 2013 2014 2015 2016

Liquidity Ratios (%)

Liquidity coverage ratio (LCR) Loan to customer deposit ratio

NCB Investor Relations2Q 2017 Investor Presentation 9

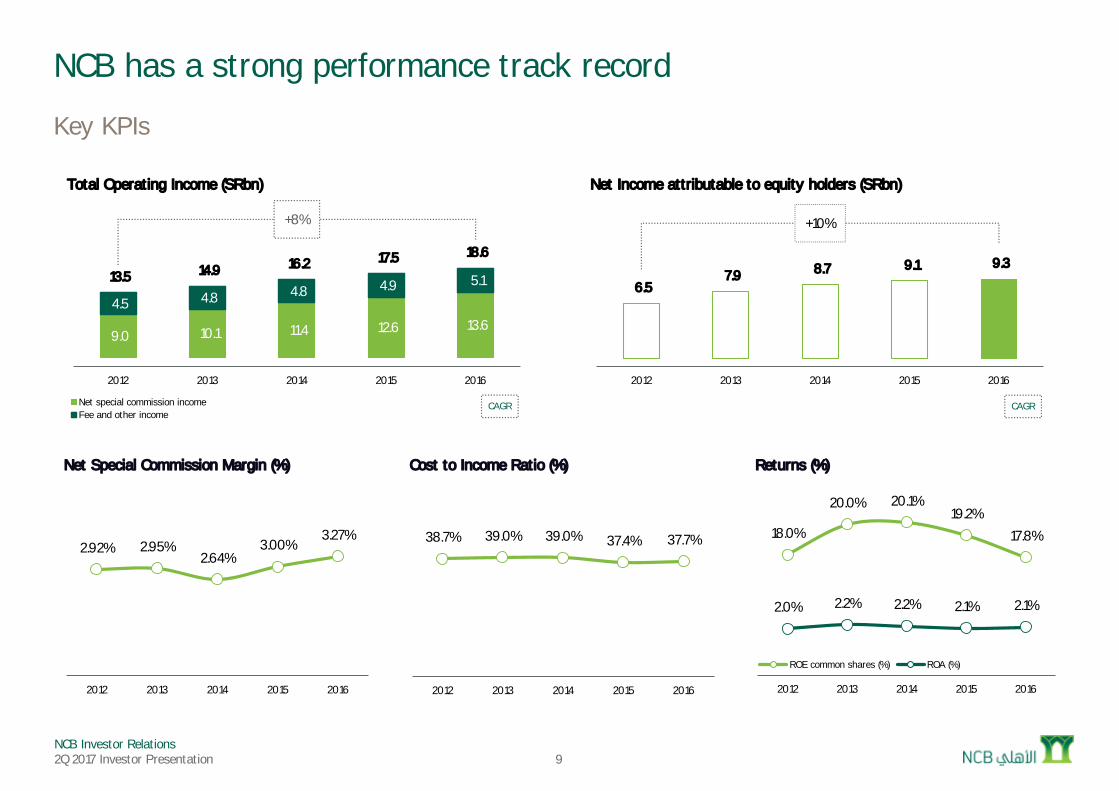

NCB has a strong performance track record

Key KPIs

9.0 10.1 11.4 12.6 13.6 4.5 4.8 4.8 4.9 5.1 13.5 14.9 16.2 17.5 18.6

+8%

0

5

10

15

20

25

30

2012 2013 2014 2015 2016

Total Operating Income (SRbn)

Net special commission incomeFee and other income

2.92% 2.95%2.64%

3.00%3.27%

0

0

0

0

0

0

2012 2013 2014 2015 2016

Net Special Commission Margin (%)

38.7% 39.0% 39.0% 37.4% 37.7%

0

0

0

0

0

1

1

2012 2013 2014 2015 2016

Cost to Income Ratio (%)

CAGR CAGR

6.5 7.9 8.7 9.1 9.3

+10%

0

2

4

6

8

10

12

14

16

18

2012 2013 2014 2015 2016

Net Income attributable to equity holders (SRbn)

18.0%

20.0% 20.1%19.2%

17.8%

2.0% 2.2% 2.2% 2.1% 2.1%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

0

0

0

0

0

0

2012 2013 2014 2015 2016

Returns (%)

ROE common shares (%) ROA (%)

NCB Investor Relations2Q 2017 Investor Presentation 10

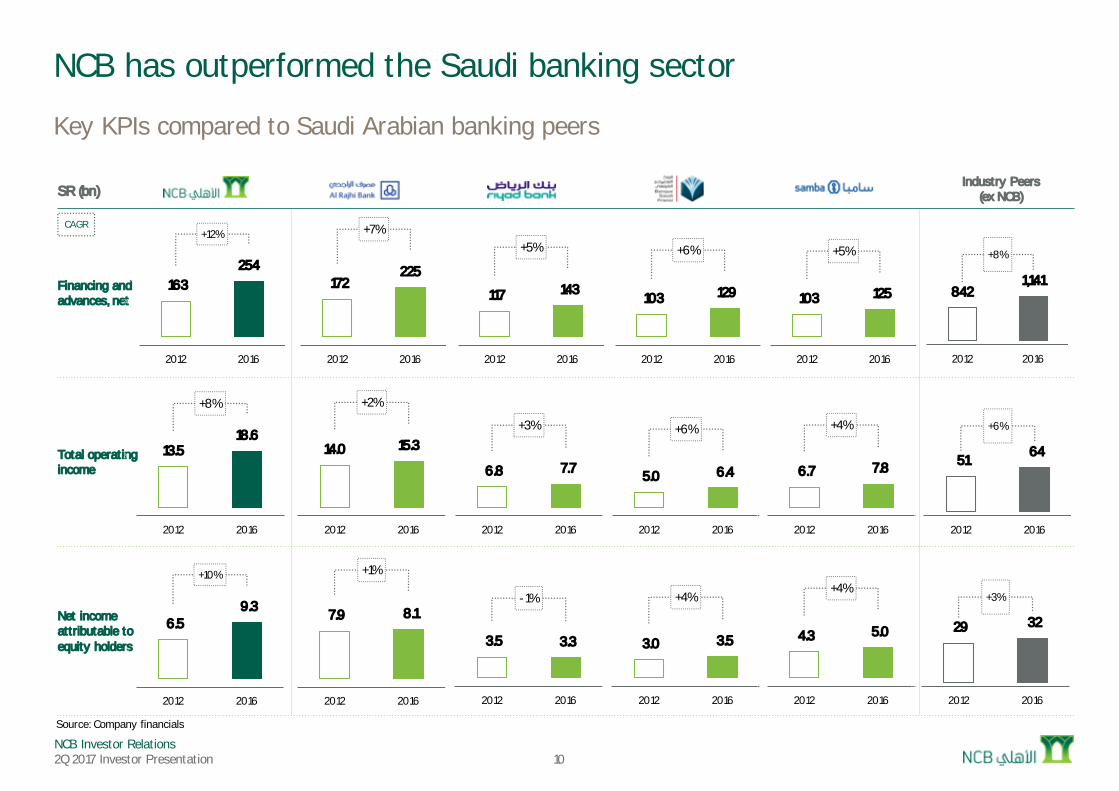

NCB has outperformed the Saudi banking sector

Key KPIs compared to Saudi Arabian banking peers

SR (bn)

Financing and advances, net

Total operating income

Net income attributable to equity holders

Source: Company financials

CAGR

163 254

+12%

0

100

200

300

400

500

2012 2016

172 225

+7%

0

100

200

300

400

500

2012 2016

117 143

+5%

0

100

200

300

400

500

2012 2016

103 129

+6%

0

100

200

300

400

500

2012 2016

103 125

+5%

0

100

200

300

400

500

2012 2016

13.5 18.6

+8%

0

5

10

15

20

25

30

35

40

2012 2016

14.0 15.3

+2%

0

5

10

15

20

25

30

35

40

2012 2016

6.8 7.7

+3%

0

5

10

15

20

25

30

35

40

2012 2016

5.0 6.4

+6%

0

5

10

15

20

25

30

35

40

2012 2016

6.7 7.8

+4%

0

5

10

15

20

25

30

35

40

2012 2016

7.9 8.1

+1%

0

2

4

6

8

10

12

14

16

18

20

2012 2016

3.5 3.3

-1%

0

2

4

6

8

10

12

14

16

18

20

2012 2016

3.0 3.5

+4%

0

2

4

6

8

10

12

14

16

18

20

2012 2016

4.3 5.0

+4%

0

2

4

6

8

10

12

14

16

18

20

2012 2016

6.5 9.3

+10%

0

2

4

6

8

10

12

14

16

18

20

2012 2016

842 1,141

+8%

0

500

1,000

1,500

2,000

2,500

2012 2016

51 64

+6%

0

20

40

60

80

100

120

140

2012 2016

29 32

+3%

0

10

20

30

40

50

60

70

2012 2016

Industry Peers(ex NCB)

NCB Investor Relations2Q 2017 Investor Presentation 11

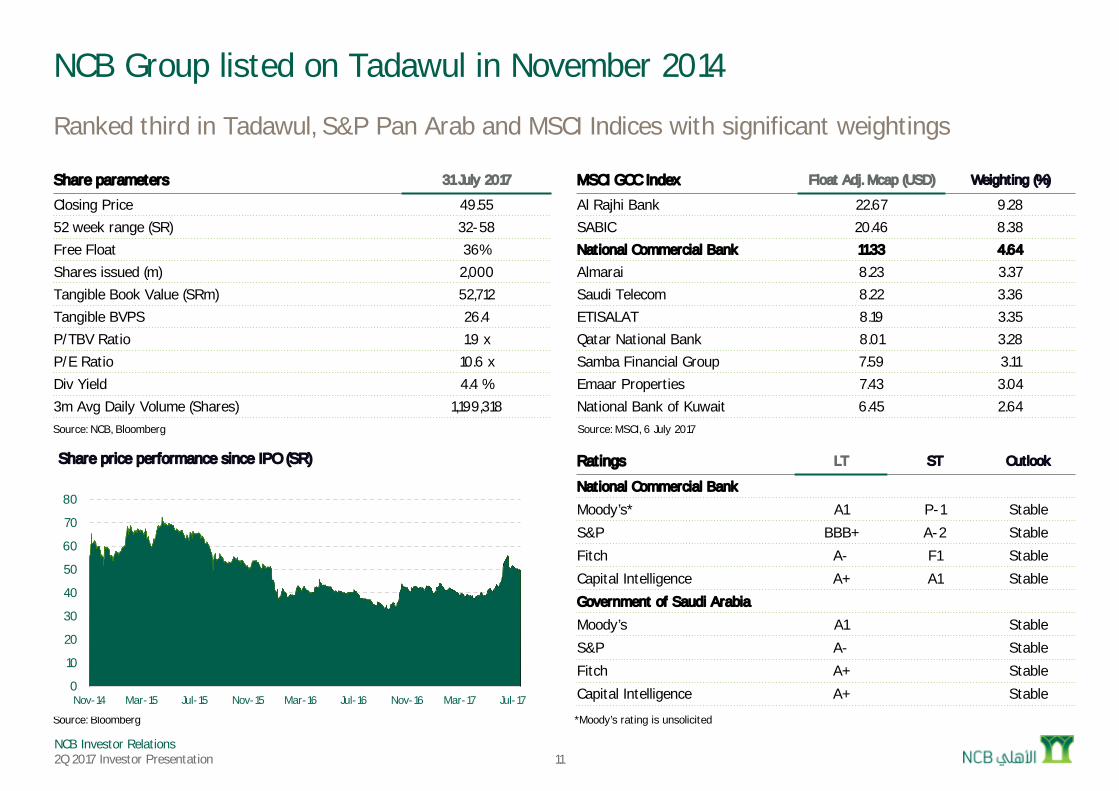

NCB Group listed on Tadawul in November 2014

Ranked third in Tadawul, S&P Pan Arab and MSCI Indices with significant weightings

Share parameters 31 July 2017

Closing Price 49.5552 week range (SR) 32-58Free Float 36%Shares issued (m) 2,000Tangible Book Value (SRm) 52,712Tangible BVPS 26.4P/TBV Ratio 1.9 xP/E Ratio 10.6 xDiv Yield 4.4 %3m Avg Daily Volume (Shares) 1,199,318

MSCI GCC Index Float Adj. Mcap (USD) Weighting (%)

Al Rajhi Bank 22.67 9.28SABIC 20.46 8.38National Commercial Bank 11.33 4.64

Almarai 8.23 3.37Saudi Telecom 8.22 3.36ETISALAT 8.19 3.35Qatar National Bank 8.01 3.28Samba Financial Group 7.59 3.11Emaar Properties 7.43 3.04National Bank of Kuwait 6.45 2.64

Ratings LT ST Outlook

National Commercial Bank

Moody’s* A1 P-1 Stable

S&P BBB+ A-2 Stable

Fitch A- F1 Stable

Capital Intelligence A+ A1 StableGovernment of Saudi Arabia

Moody’s A1 Stable

S&P A- Stable

Fitch A+ Stable

Capital Intelligence A+ Stable

*Moody’s rating is unsolicited

Source: MSCI, 6 July 2017

Source: Bloomberg

Source: NCB, Bloomberg

0

10

20

30

40

50

60

70

80

Nov-14 Mar-15 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17

Share price performance since IPO (SR)

NCB Investor Relations2Q 2017 Investor Presentation

National Commercial Bank

Grow with KSA. Grow with NCB.

2Q 2017 Results

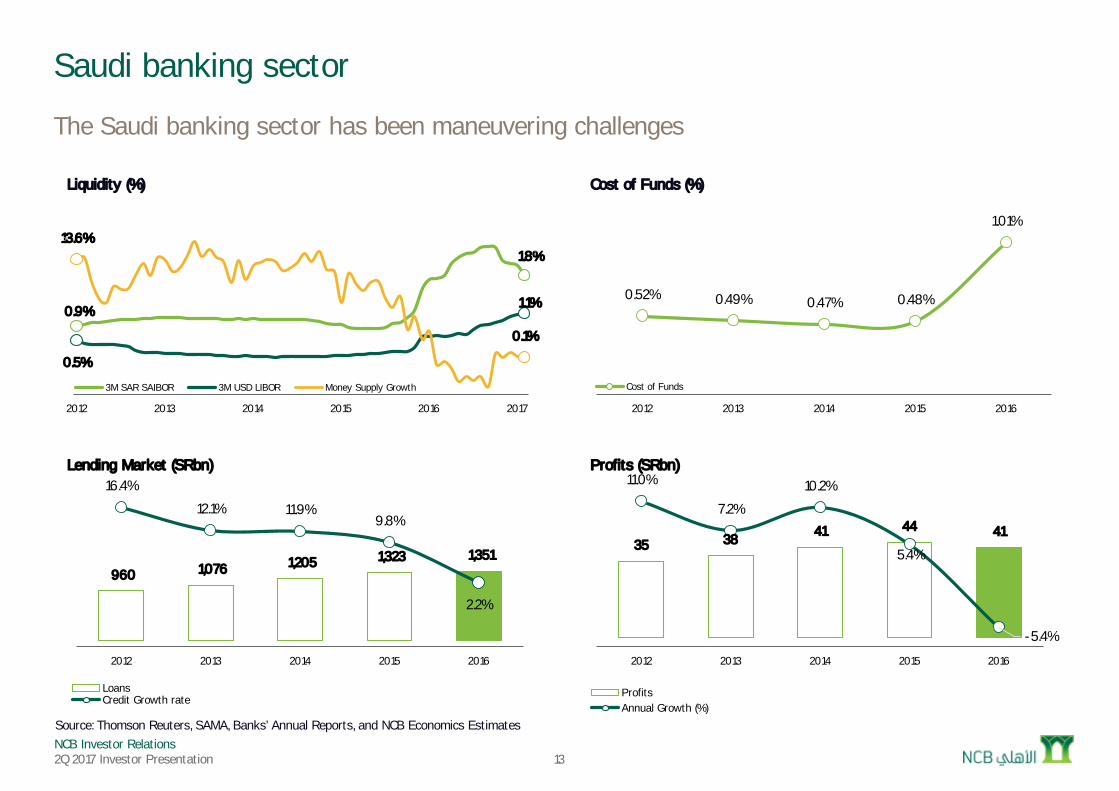

NCB Investor Relations2Q 2017 Investor Presentation 13

Saudi banking sector

The Saudi banking sector has been maneuvering challenges

0.9%

1.8%

0.5%

1.1%

13.6%

0.1%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

(0)

0

0

0

0

0

0

0

2012 2013 2014 2015 2016 2017

Liquidity (%)

3M SAR SAIBOR 3M USD LIBOR Money Supply Growth

35 38 41 44 41

11.0%

7.2%

10.2%

5.4%

-5.4%-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

10

20

30

40

50

60

70

2012 2013 2014 2015 2016

Profits (SRbn)

ProfitsAnnual Growth (%)

Source: Thomson Reuters, SAMA, Banks’ Annual Reports, and NCB Economics Estimates

0.52% 0.49% 0.47% 0.48%

1.01%

0

0

0

0

0

0

0

2012 2013 2014 2015 2016

Cost of Funds (%)

Cost of Funds

960 1,076 1,205 1,323 1,351

16.4%

12.1% 11.9%9.8%

2.2%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0

500

1,000

1,500

2,000

2,500

3,000

2012 2013 2014 2015 2016

Lending Market (SRbn)

LoansCredit Growth rate

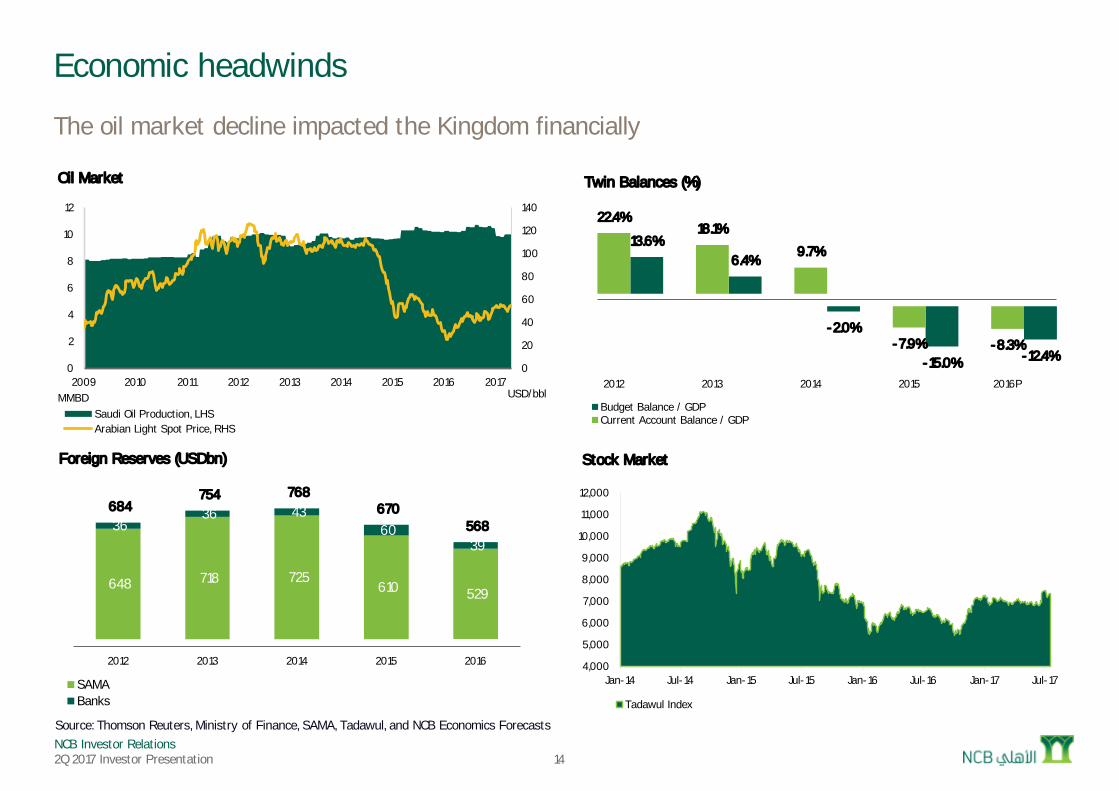

NCB Investor Relations2Q 2017 Investor Presentation 14

Economic headwinds

The oil market decline impacted the Kingdom financially

0

20

40

60

80

100

120

140

0

2

4

6

8

10

12

2009 2010 2011 2012 2013 2014 2015 2016 2017USD/bblMMBD

Oil Market

Saudi Oil Production, LHSArabian Light Spot Price, RHS

648 718 725 610 529

36 36 43

60 39

684 754 768

670 568

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016

Foreign Reserves (USDbn)

SAMABanks

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

Stock Market

Tadawul Index

Source: Thomson Reuters, Ministry of Finance, SAMA, Tadawul, and NCB Economics Forecasts

13.6%6.4%

-2.0%

-15.0% -12.4%

22.4%18.1%

9.7%

-7.9% -8.3%-25.0%

-15.0%

-5.0%

5.0%

15.0%

25.0%

2012 2013 2014 2015 2016P

Twin Balances (%)

Budget Balance / GDPCurrent Account Balance / GDP

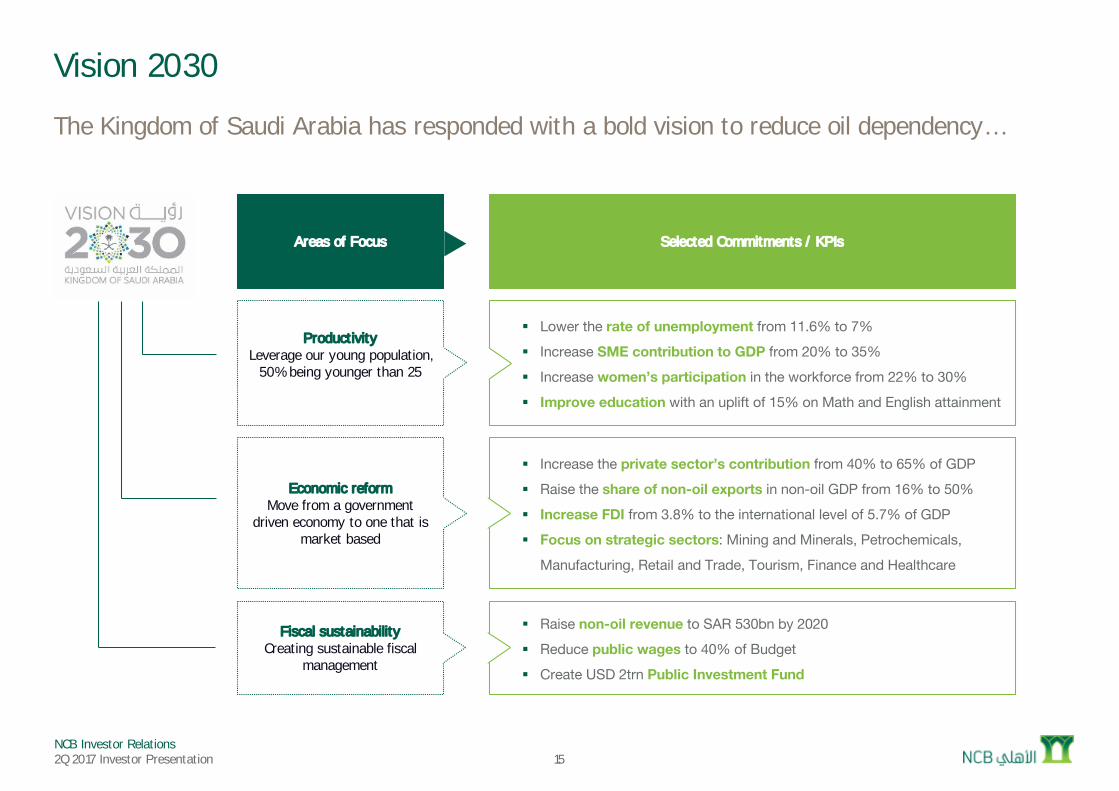

NCB Investor Relations2Q 2017 Investor Presentation 15

Vision 2030

The Kingdom of Saudi Arabia has responded with a bold vision to reduce oil dependency…

Economic reformMove from a government

driven economy to one that is market based

§ Increase the private sector’s contribution from 40% to 65% of GDP§ Raise the share of non-oil exports in non-oil GDP from 16% to 50%§ Increase FDI from 3.8% to the international level of 5.7% of GDP§ Focus on strategic sectors: Mining and Minerals, Petrochemicals,

Manufacturing, Retail and Trade, Tourism, Finance and Healthcare

Fiscal sustainabilityCreating sustainable fiscal

management

§ Raise non-oil revenue to SAR 530bn by 2020§ Reduce public wages to 40% of Budget§ Create USD 2trn Public Investment Fund

ProductivityLeverage our young population,

50% being younger than 25

§ Lower the rate of unemployment from 11.6% to 7%§ Increase SME contribution to GDP from 20% to 35%§ Increase women’s participation in the workforce from 22% to 30%§ Improve education with an uplift of 15% on Math and English attainment

Areas of Focus Selected Commitments / KPIs

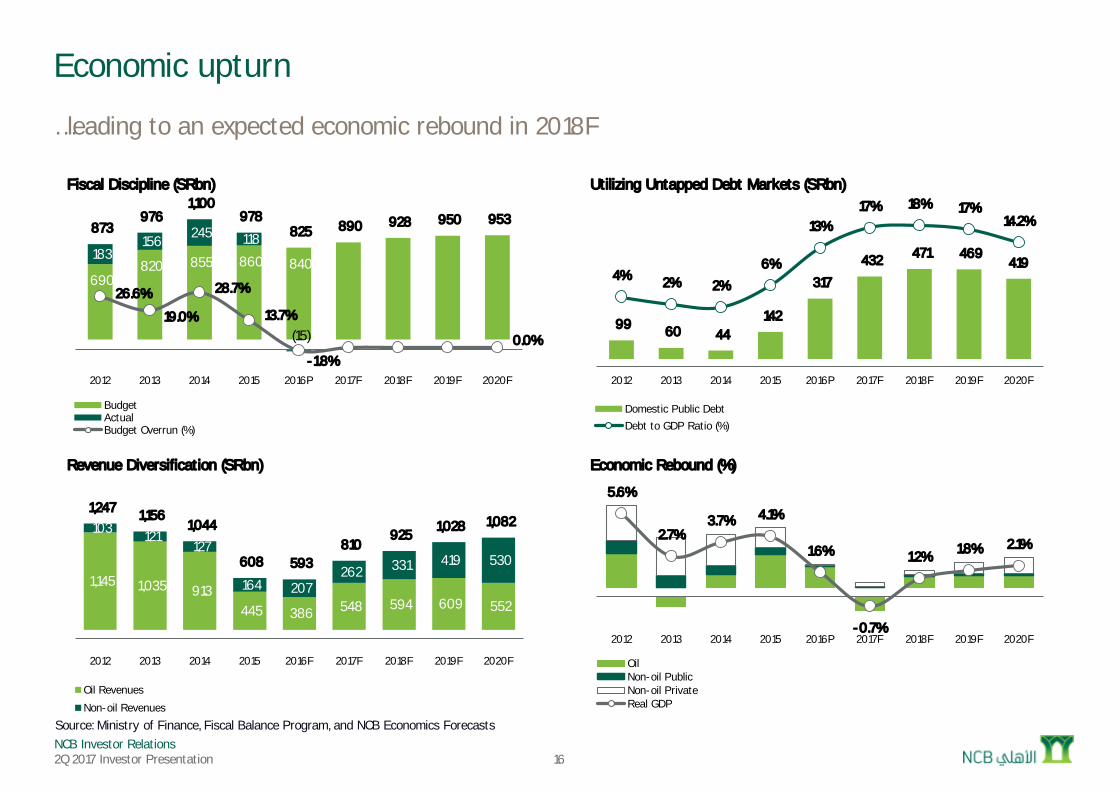

NCB Investor Relations2Q 2017 Investor Presentation 16

Economic upturn

…leading to an expected economic rebound in 2018F

Source: Ministry of Finance, Fiscal Balance Program, and NCB Economics Forecasts

99 60 44 142

317

432 471 469 419

4% 2% 2%

6%

13%17% 18% 17%

14.2%

-10%

-5%

0%

5%

10%

15%

20%

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016P 2017F 2018F 2019F 2020F

Utilizing Untapped Debt Markets (SRbn)

Domestic Public DebtDebt to GDP Ratio (%)

(

1,145 1,035 913 445 386 548 594 609 552

103 121 127

164 207 262 331 419 530

1,247 1,156 1,044

608 593 810

925 1,028 1,082

(100)

100

300

500

700

900

1,100

1,300

1,500

1,700

2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Revenue Diversification (SRbn)

Oil Revenues

Non-oil Revenues

690 820 855 860 840

183 156 245 118

(15)

873 976

1,100 978

825 890 928 950 953

26.6%

19.0%

28.7%

13.7%

-1.8%0.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

(150)

50

250

450

650

850

1,050

1,250

2012 2013 2014 2015 2016P 2017F 2018F 2019F 2020F

Fiscal Discipline (SRbn)

BudgetActualBudget Overrun (%)

5.6%

2.7%3.7% 4.1%

1.6%

-0.7%

1.2% 1.8% 2.1%

(0)

(0)

0

0

0

0

0

0

0

0

2012 2013 2014 2015 2016P 2017F 2018F 2019F 2020F

Economic Rebound (%)

OilNon-oil PublicNon-oil PrivateReal GDP

NCB Investor Relations2Q 2017 Investor Presentation 17

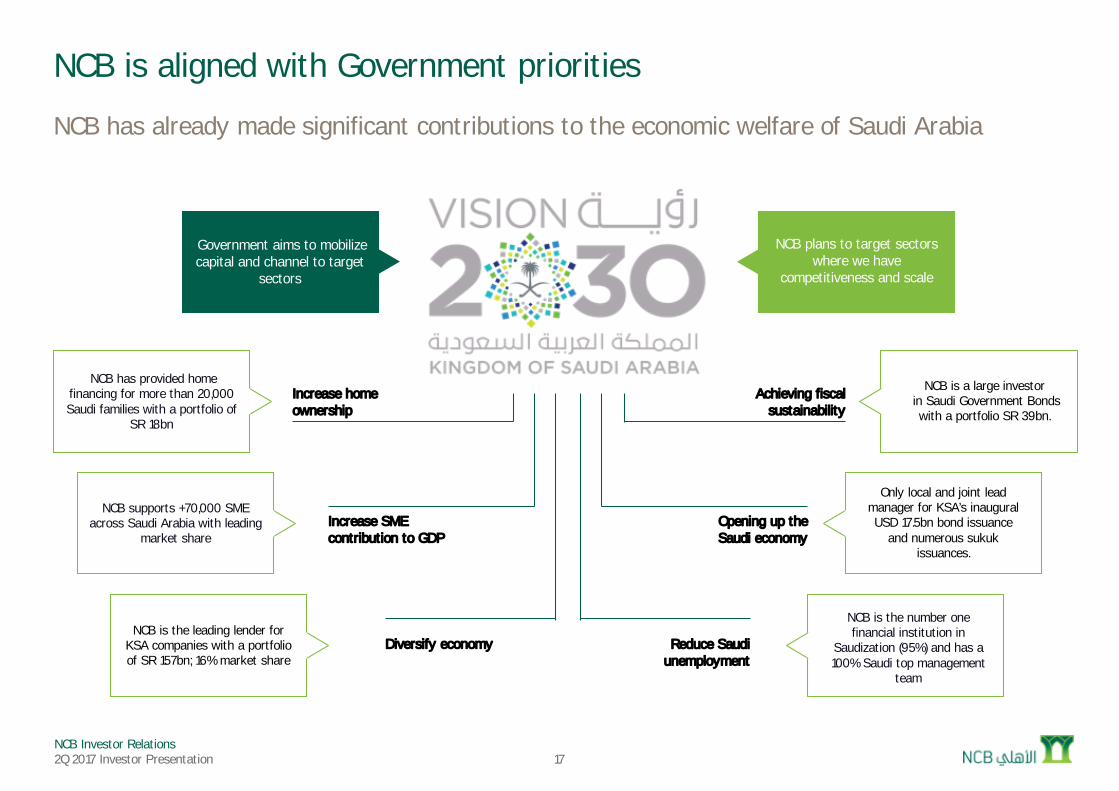

NCB is aligned with Government priorities

NCB has already made significant contributions to the economic welfare of Saudi Arabia

Government aims to mobilize capital and channel to target

sectors

NCB plans to target sectors where we have

competitiveness and scale

NCB supports +70,000 SME across Saudi Arabia with leading

market share

Only local and joint lead manager for KSA’s inaugural USD 17.5bn bond issuance

and numerous sukukissuances.

NCB is a large investorin Saudi Government Bonds with a portfolio SR 39bn.

NCB has provided home financing for more than 20,000 Saudi families with a portfolio of

SR 18bn

Achieving fiscalsustainability

Opening up the Saudi economy

Increase SME contribution to GDP

Increase homeownership

Reduce Saudi unemployment

Diversify economyNCB is the leading lender for

KSA companies with a portfolio of SR 157bn; 16% market share

NCB is the number one financial institution in

Saudization (95%) and has a 100% Saudi top management

team

NCB Investor Relations2Q 2017 Investor Presentation

National Commercial Bank

Strategic overview

2Q 2017 Results

NCB Investor Relations2Q 2017 Investor Presentation 19

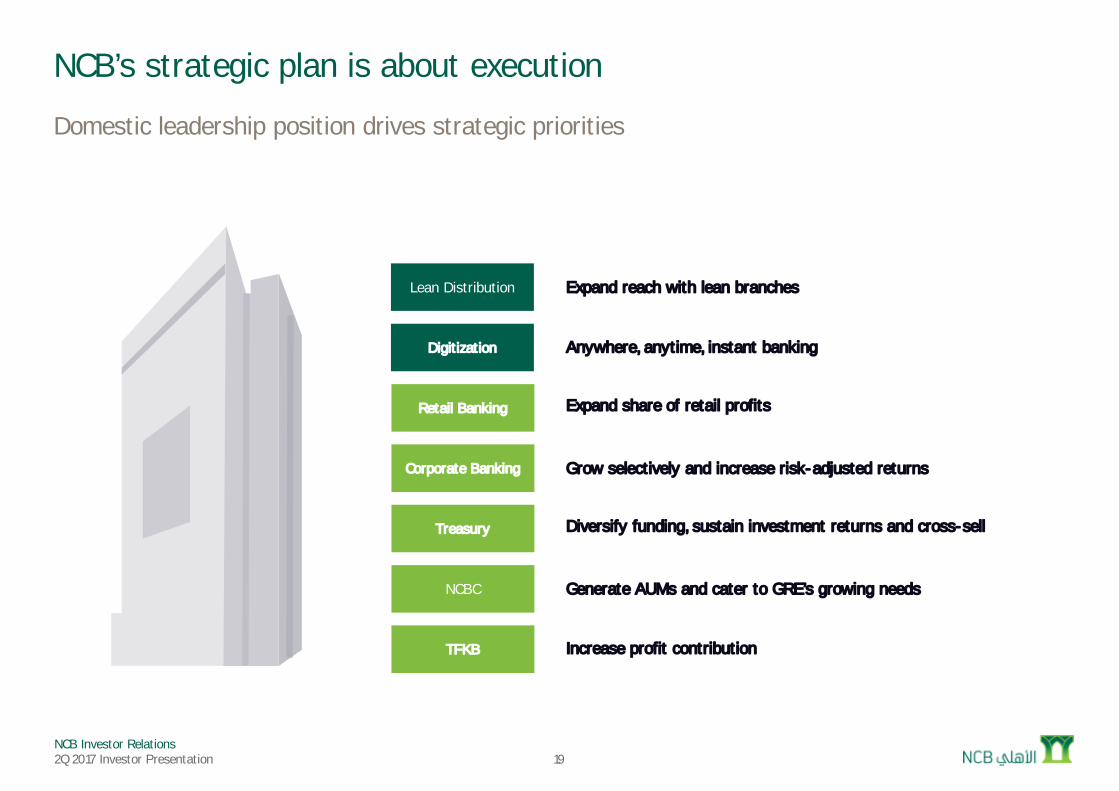

NCB’s strategic plan is about execution

Domestic leadership position drives strategic priorities

Retail Banking Expand share of retail profits

Corporate Banking Grow selectively and increase risk-adjusted returns

TFKB Increase profit contribution

Treasury Diversify funding, sustain investment returns and cross-sell

NCBC Generate AUMs and cater to GRE’s growing needs

Lean Distribution

Digitization

Expand reach with lean branches

Anywhere, anytime, instant banking

NCB Investor Relations2Q 2017 Investor Presentation 20

Distribution expansion

We accelerated expansion of our distribution platform in Saudi Arabia…

299 322 342 352 374

+6%

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016

Number of branches

28 57

97

138 148

+52%

0

50

100

150

200

250

2012 2013 2014 2015 2016

Remittance Centers

1,960 2,252 2,643

3,107 3,477

+15%

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016

Number of ATMs

12,775 14,075

26,514 30,803

39,132

+32%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2012 2013 2014 2015 2016

Point of Sale

CAGR CAGR

CAGR CAGR

NCB Investor Relations2Q 2017 Investor Presentation

60%69%

+15%

0

0

0

1

1

1

1

2014 2016

Front / Back Office Ratio (%)

21

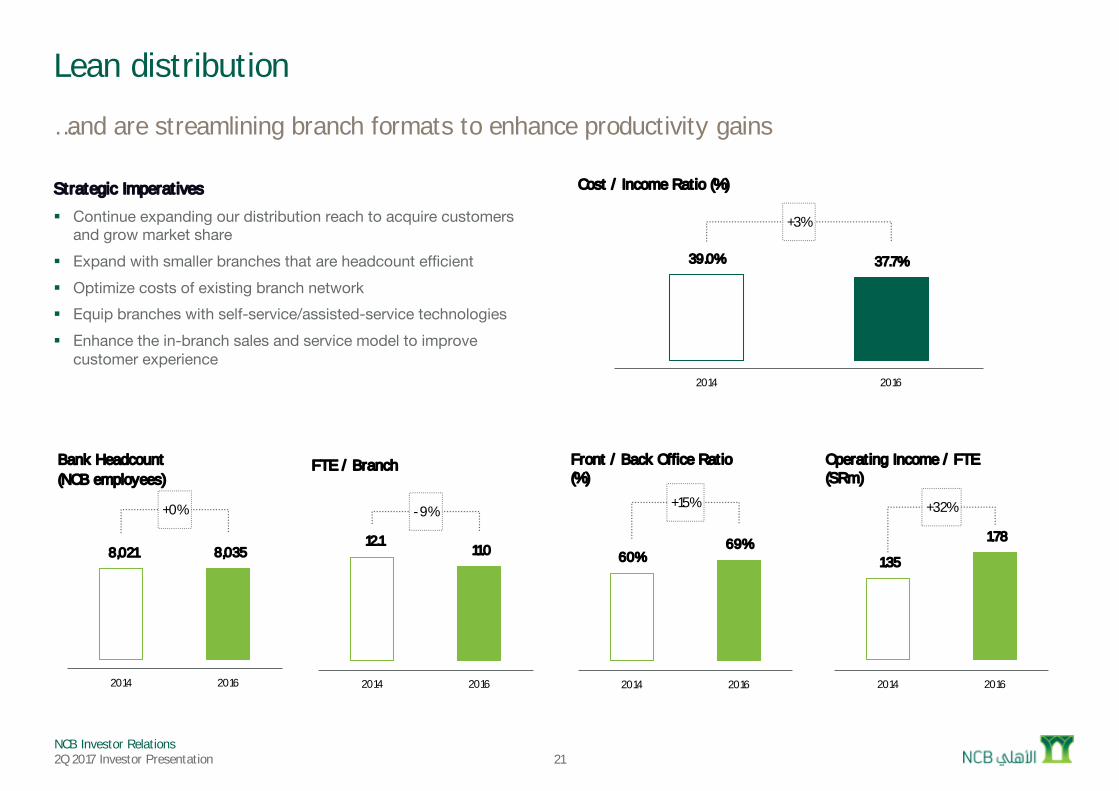

Lean distribution

…and are streamlining branch formats to enhance productivity gains

Strategic Imperatives

§ Continue expanding our distribution reach to acquire customers and grow market share

§ Expand with smaller branches that are headcount efficient§ Optimize costs of existing branch network§ Equip branches with self-service/assisted-service technologies§ Enhance the in-branch sales and service model to improve

customer experience

39.0% 37.7%

+3%

0

0

0

0

0

1

1

1

2014 2016

Cost / Income Ratio (%)

1.35

1.78

+32%

0

1

1

2

2

3

2014 2016

Operating Income / FTE (SRm)

12.1 11.0

-9%

0

2

4

6

8

10

12

14

16

18

20

2014 2016

FTE / Branch

8,021 8,035

+0%

(1,000)

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

2014 2016

Bank Headcount (NCB employees)

NCB Investor Relations2Q 2017 Investor Presentation 22

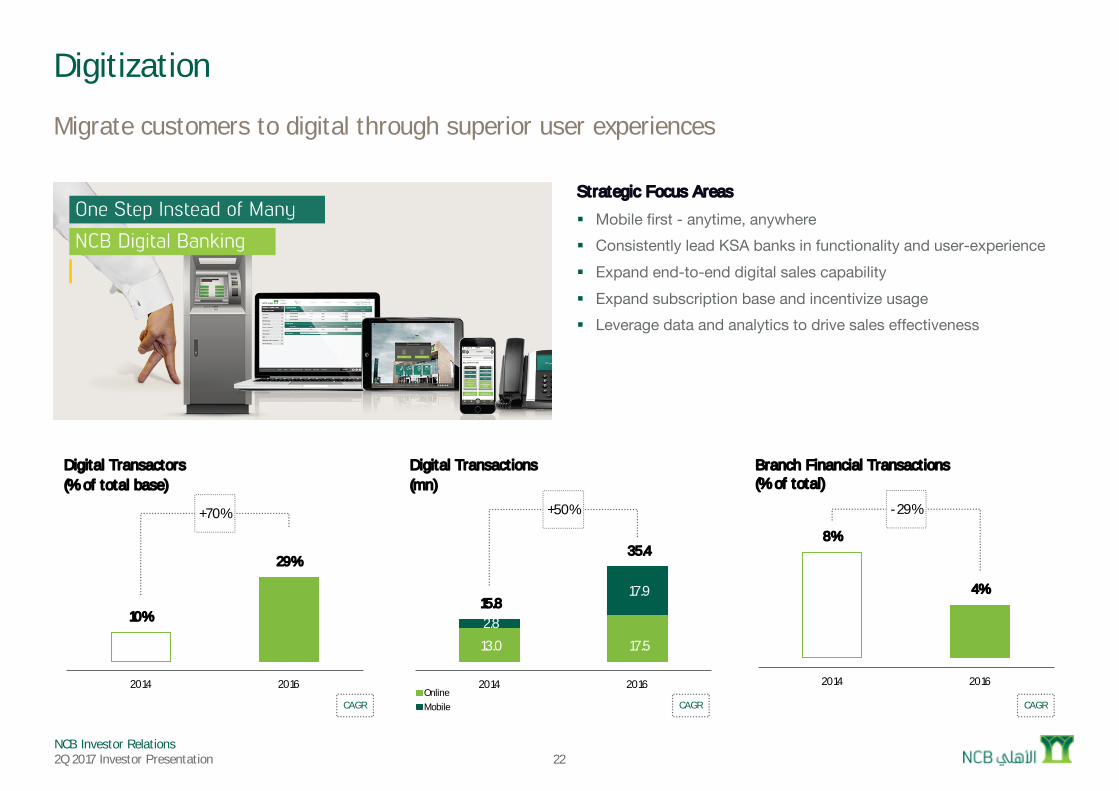

Digitization

Migrate customers to digital through superior user experiences

Strategic Focus Areas

§ Mobile first - anytime, anywhere§ Consistently lead KSA banks in functionality and user-experience § Expand end-to-end digital sales capability§ Expand subscription base and incentivize usage§ Leverage data and analytics to drive sales effectiveness

10%

29%

+70%

0

0

0

0

0

1

1

2014 2016

Digital Transactors(% of total base)

CAGR CAGR CAGR

13.0 17.5

2.8

17.9 15.8

35.4

+50%

0

10

20

30

40

50

60

2014 2016

Digital Transactions (mn)

OnlineMobile

8%

4%

-29%

0

0

0

0

0

0

0

2014 2016

Branch Financial Transactions (% of total)

NCB Investor Relations2Q 2017 Investor Presentation

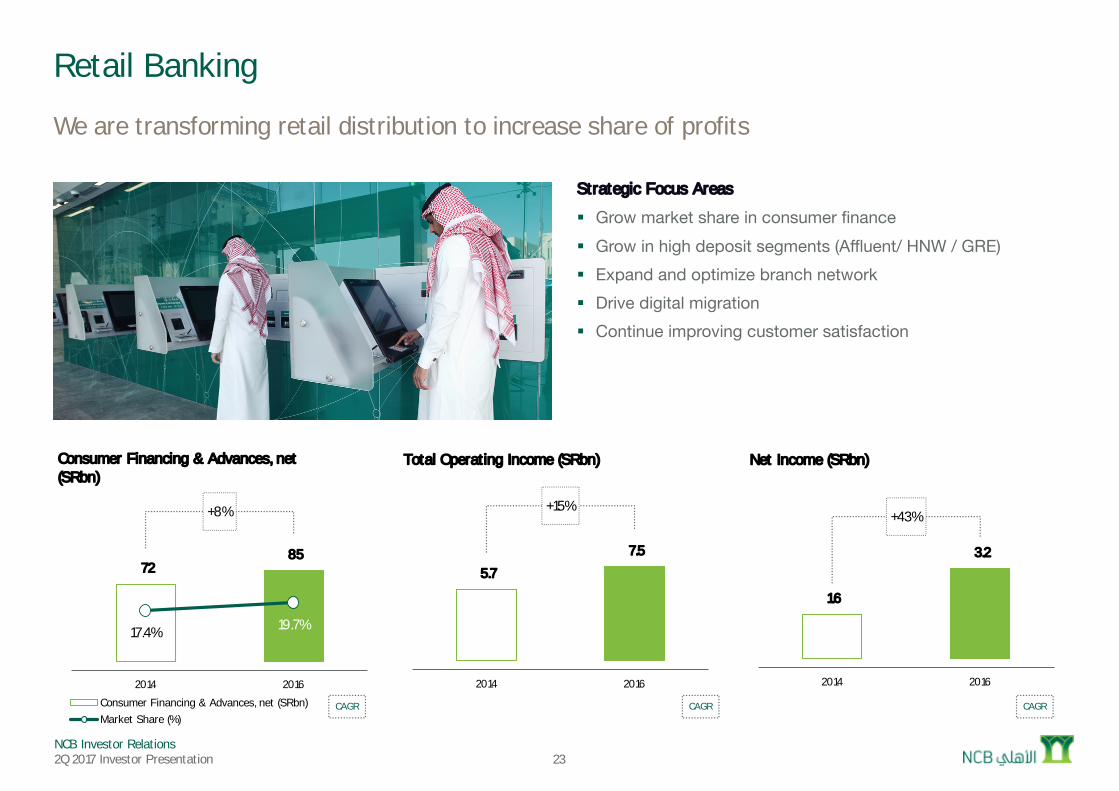

Retail Banking

We are transforming retail distribution to increase share of profits

Strategic Focus Areas

§ Grow market share in consumer finance§ Grow in high deposit segments (Affluent/ HNW / GRE) § Expand and optimize branch network§ Drive digital migration§ Continue improving customer satisfaction

CAGR CAGR CAGR

5.7

7.5

+15%

0

2

4

6

8

10

12

14

2014 2016

Total Operating Income (SRbn)

1.6

3.2

+43%

0

1

2

3

4

5

6

2014 2016

Net Income (SRbn)

23

72 85

17.4% 19.7%

+8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

0

20

40

60

80

100

120

140

160

2014 2016

Consumer Financing & Advances, net (SRbn)

Consumer Financing & Advances, net (SRbn)Market Share (%)

NCB Investor Relations2Q 2017 Investor Presentation 24

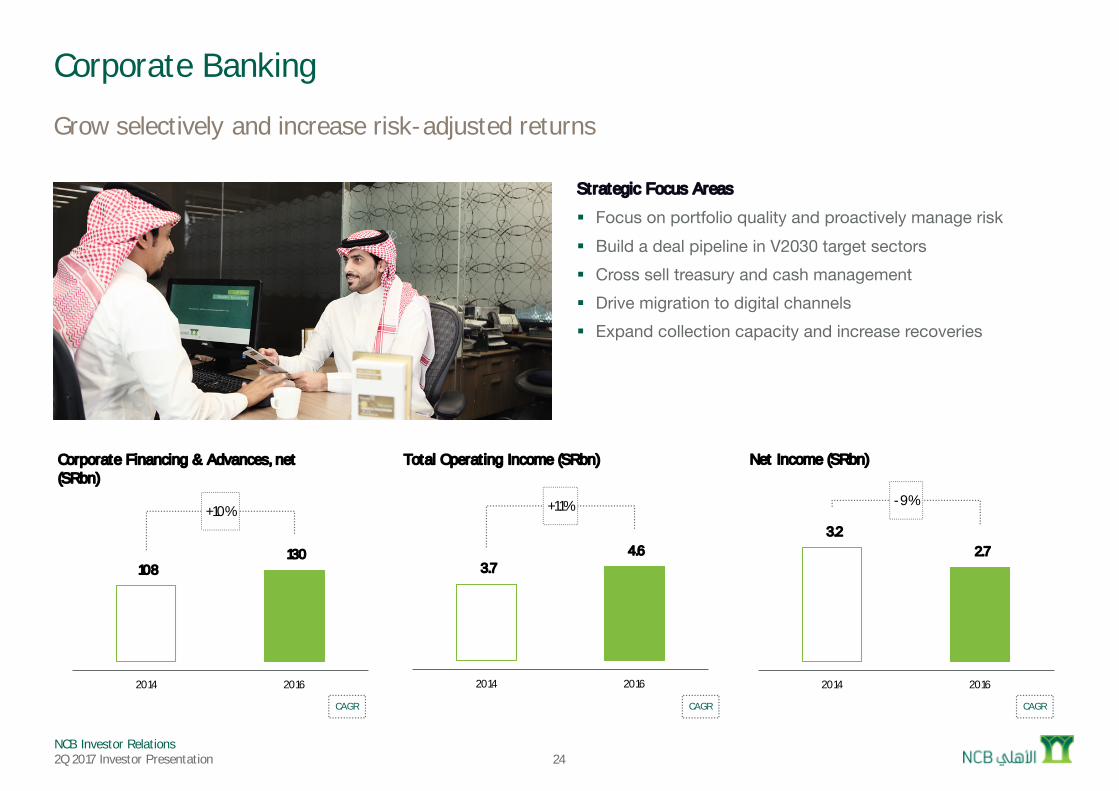

Corporate Banking

Grow selectively and increase risk-adjusted returns

Strategic Focus Areas

§ Focus on portfolio quality and proactively manage risk§ Build a deal pipeline in V2030 target sectors § Cross sell treasury and cash management§ Drive migration to digital channels§ Expand collection capacity and increase recoveries

CAGR CAGR CAGR

108 130

+10%

0

50

100

150

200

250

2014 2016

Corporate Financing & Advances, net (SRbn)

3.7 4.6

+11%

0

1

2

3

4

5

6

7

8

2014 2016

Total Operating Income (SRbn)

3.2 2.7

-9%

0

1

1

2

2

3

3

4

4

5

5

2014 2016

Net Income (SRbn)

NCB Investor Relations2Q 2017 Investor Presentation

35%

25%

-15%

0

0

0

0

0

0

0

0

0

0

1

2014 2016

Investments as % of Total Assets

25

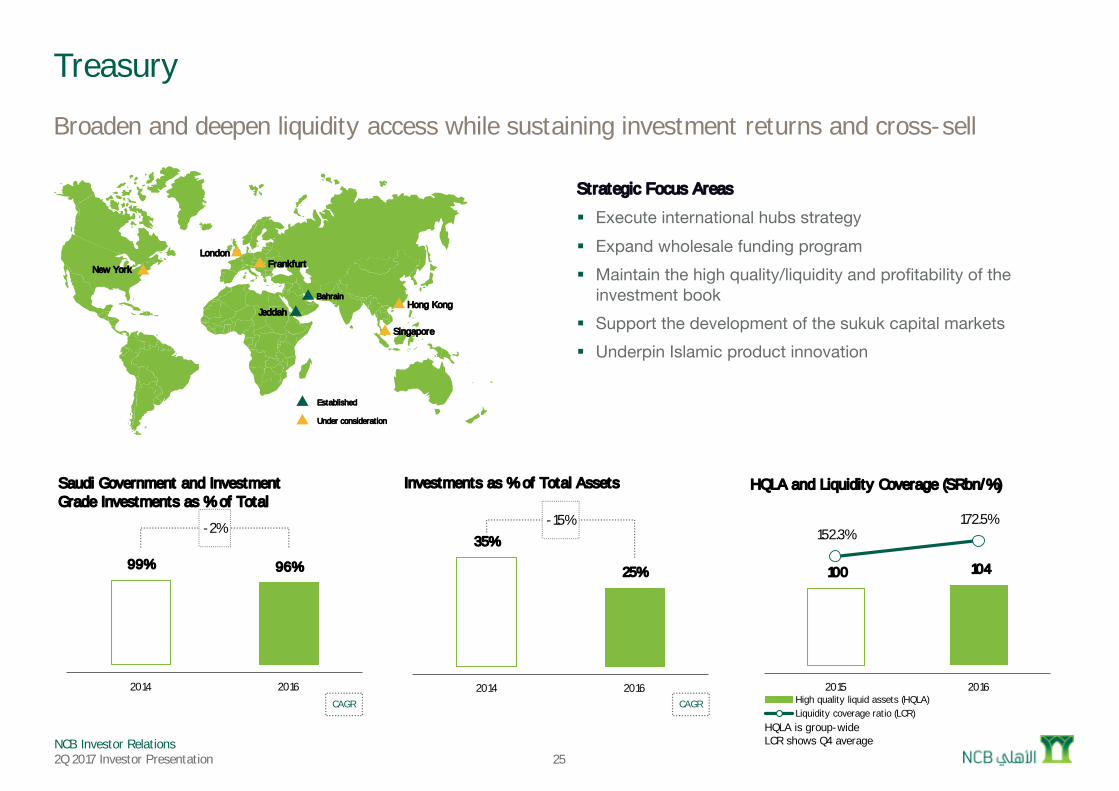

Treasury

Broaden and deepen liquidity access while sustaining investment returns and cross-sell

Strategic Focus Areas

§ Execute international hubs strategy § Expand wholesale funding program§ Maintain the high quality/liquidity and profitability of the

investment book§ Support the development of the sukuk capital markets § Underpin Islamic product innovation

100 104

152.3%172.5%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

200.0%

0

20

40

60

80

100

120

140

160

180

200

2015 2016

HQLA and Liquidity Coverage (SRbn/%)

High quality liquid assets (HQLA)Liquidity coverage ratio (LCR)

London

Bahrain

Singapore

Jeddah

Established

Under consideration

CAGR CAGR

HQLA is group-wideLCR shows Q4 average

FrankfurtNew York

Hong Kong

99% 96%

-2%

0

0

0

1

1

1

1

1

2

2

2014 2016

Saudi Government and Investment Grade Investments as % of Total

NCB Investor Relations2Q 2017 Investor Presentation 26

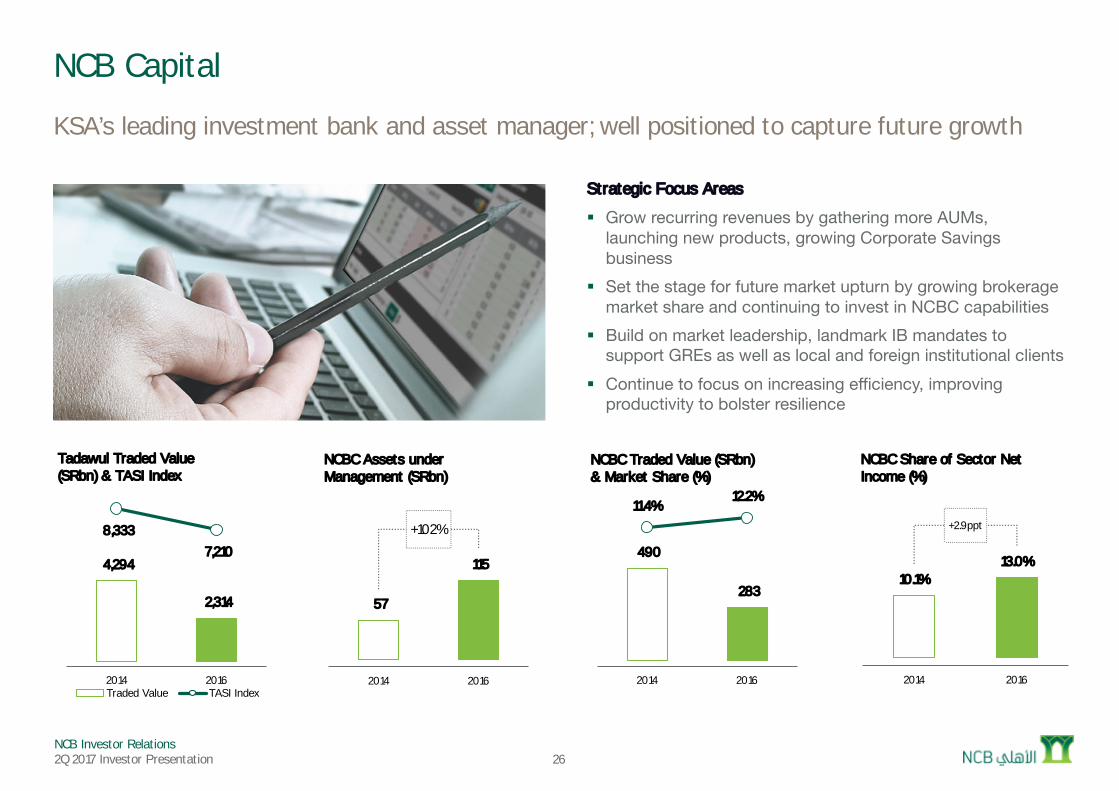

NCB Capital

KSA’s leading investment bank and asset manager; well positioned to capture future growth

Strategic Focus Areas

§ Grow recurring revenues by gathering more AUMs, launching new products, growing Corporate Savings business

§ Set the stage for future market upturn by growing brokerage market share and continuing to invest in NCBC capabilities

§ Build on market leadership, landmark IB mandates to support GREs as well as local and foreign institutional clients

§ Continue to focus on increasing efficiency, improving productivity to bolster resilience

57

115

+102%

0

50

100

150

200

250

2014 2016

NCBC Assets under Management (SRbn)

4,294

2,314

8,333 7,210

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2014 2016

Tadawul Traded Value (SRbn) & TASI Index

Traded Value TASI Index

490

283

11.4%12.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

100

200

300

400

500

600

700

800

900

2014 2016

NCBC Traded Value (SRbn) & Market Share (%)

10.1%13.0%

+2.9ppt

0

0

0

0

0

0

2014 2016

NCBC Share of Sector Net Income (%)

NCB Investor Relations2Q 2017 Investor Presentation

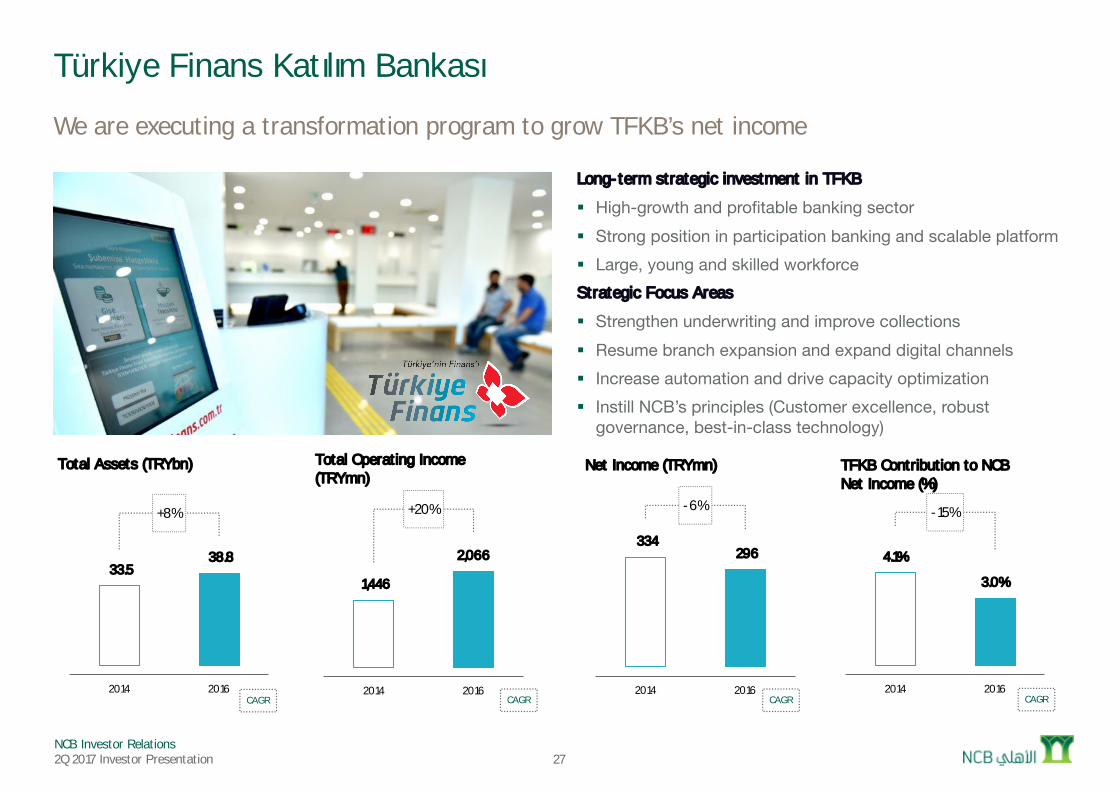

334 296

-6%

0

100

200

300

400

500

2014 2016

Net Income (TRYmn)

33.5 38.8

+8%

0

10

20

30

40

50

60

70

2014 2016

Total Assets (TRYbn)

27

Türkiye Finans Katılım Bankası

We are executing a transformation program to grow TFKB’s net income

Long-term strategic investment in TFKB

§ High-growth and profitable banking sector§ Strong position in participation banking and scalable platform§ Large, young and skilled workforceStrategic Focus Areas

§ Strengthen underwriting and improve collections§ Resume branch expansion and expand digital channels § Increase automation and drive capacity optimization § Instill NCB’s principles (Customer excellence, robust

governance, best-in-class technology)

CAGRCAGRCAGRCAGR

4.1%

3.0%

-15%

0

0

0

0

0

0

0

0

0

2014 2016

TFKB Contribution to NCB Net Income (%)

1,446

2,066

+20%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2014 2016

Total Operating Income (TRYmn)

NCB Investor Relations2Q 2017 Investor Presentation

National Commercial Bank

Financial Results Highlights

2Q 2017 Results

NCB Investor Relations2Q 2017 Investor Presentation 29

Profitability and balance sheet driversNet income stable as improved efficiency offset lower fee incomeBalance sheet growth reflective of a more subdued economic environment

Management Commentary

§ Growth in total assets (+2%) and financing (+1%) year to date was in line with the more subdued economic environment.

§ Total operating income declined 4% YoY. Domestically, total operating income was stable YoY as healthy net commission margin and income growth was offset by lower fee and investment income.

§ Total operating income from International operations declined by 33% YoY primarily due to a 20% avg. depreciation of the Turkish Lira.

§ 2Q net income stable YoY as improved operational efficiency offset declining fee and investment-related income.

254 254 257

112 108 115 63 71 60

441 449 450

+2%

0

100

200

300

400

500

600

700

800

4Q 16 1Q 17 2Q 17

Total Assets (SRbn)

Financing and advances, netInvestments, netCash and bank balancesOther assets

2.44

0.13

(0.31)

0.30

(0.08)(0.06)

2.42

0

0

0

0

0

1

1

1

1

1

2Q 16 NSCI Non-NSCI Income

Expenses Impairments Other 2Q 17

Net income Attributed to Equity Holders Movement (SRbn)

4.66

0.19

(0.18)

4.67

(0.19)

4.48

0

0

0

1

1

1

1

1

2Q 16 NSCI Non-NSCI Income Excl. Intn'l International 2Q 17

Total Operating Income Movement (SRbn)

NCB Investor Relations2Q 2017 Investor Presentation

Retail42%

Corporate25%

Treasury21%

Capital Market3%

International9%

Total Operating Income by Segment (SRbn)

30

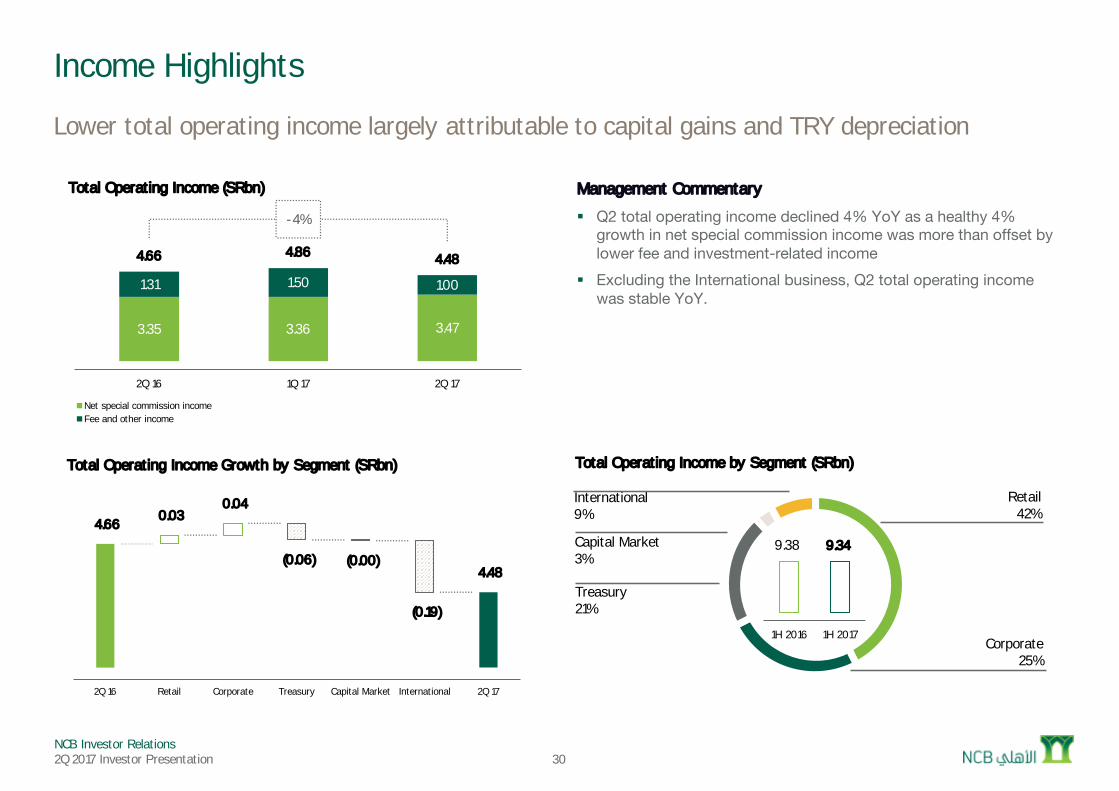

Income Highlights

Management Commentary

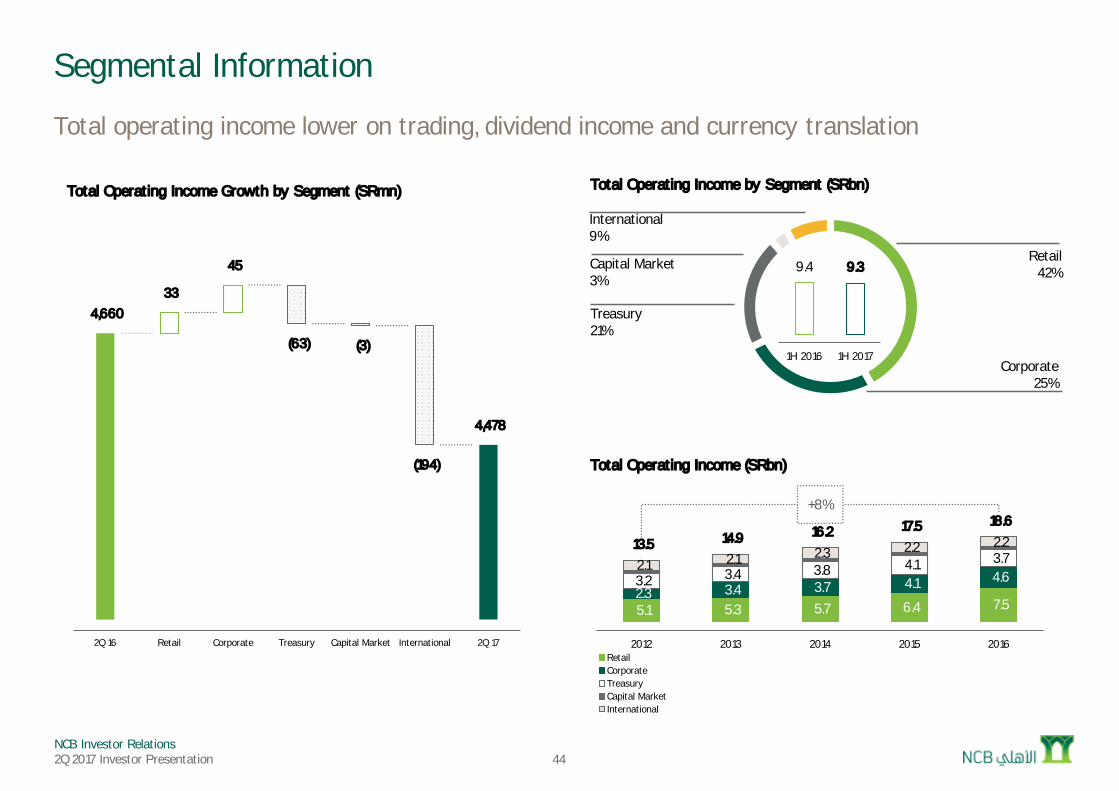

§ Q2 total operating income declined 4% YoY as a healthy 4% growth in net special commission income was more than offset by lower fee and investment-related income

§ Excluding the International business, Q2 total operating income was stable YoY.

Lower total operating income largely attributable to capital gains and TRY depreciation

3.35 3.36 3.47

1.31 1.50 1.00

4.66 4.86 4.48

-4%

0

1

2

3

4

5

6

7

8

2Q 16 1Q 17 2Q 17

Total Operating Income (SRbn)

Net special commission incomeFee and other income

9.38 9.34

0

2

4

6

8

10

12

14

1H 2016 1H 2017

4.66 0.03

(0.06)

0.04

(0.00)

(0.19)

4.48

0

0

0

0

0

1

1

1

2Q 16 Retail Corporate Treasury Capital Market International 2Q 17

Total Operating Income Growth by Segment (SRbn)

NCB Investor Relations2Q 2017 Investor Presentation 31

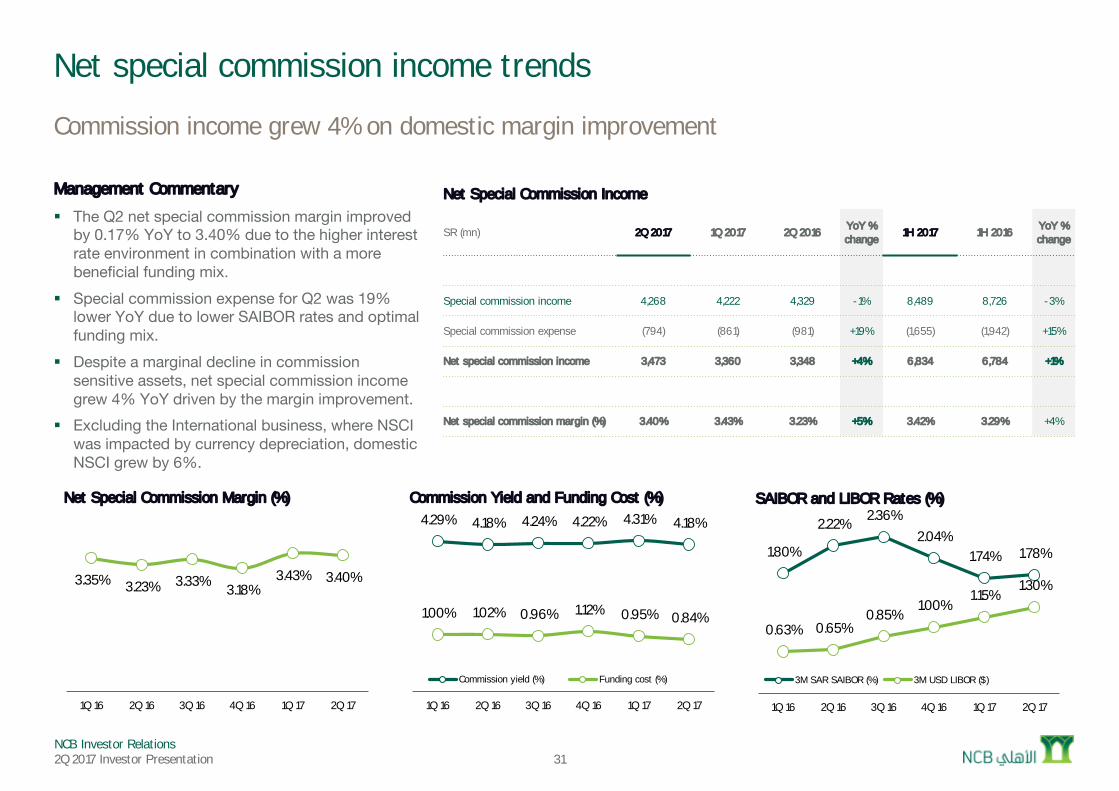

Net special commission income trends

Commission income grew 4% on domestic margin improvement

Management Commentary

§ The Q2 net special commission margin improved by 0.17% YoY to 3.40% due to the higher interest rate environment in combination with a more beneficial funding mix.

§ Special commission expense for Q2 was 19% lower YoY due to lower SAIBOR rates and optimal funding mix.

§ Despite a marginal decline in commission sensitive assets, net special commission income grew 4% YoY driven by the margin improvement.

§ Excluding the International business, where NSCI was impacted by currency depreciation, domestic NSCI grew by 6%.

Net Special Commission Income

SR (mn) 2Q 2017 1Q 2017 2Q 2016 YoY % change

1H 2017 1H 2016 YoY % change

Special commission income 4,268 4,222 4,329 -1% 8,489 8,726 -3%

Special commission expense (794) (861) (981) +19% (1,655) (1,942) +15%

Net special commission income 3,473 3,360 3,348 +4% 6,834 6,784 +1%

Net special commission margin (%) 3.40% 3.43% 3.23% +5% 3.42% 3.29% +4%

4.29% 4.18% 4.24% 4.22% 4.31% 4.18%

1.00% 1.02% 0.96% 1.12% 0.95% 0.84%

(0)

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Commission Yield and Funding Cost (%)

Commission yield (%) Funding cost (%)

3.35% 3.23% 3.33% 3.18%3.43% 3.40%

0

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Net Special Commission Margin (%)

1.80%

2.22% 2.36%2.04%

1.74% 1.78%

0.63% 0.65%0.85%

1.00%1.15%

1.30%

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

SAIBOR and LIBOR Rates (%)

3M SAR SAIBOR (%) 3M USD LIBOR ($)

NCB Investor Relations2Q 2017 Investor Presentation 32

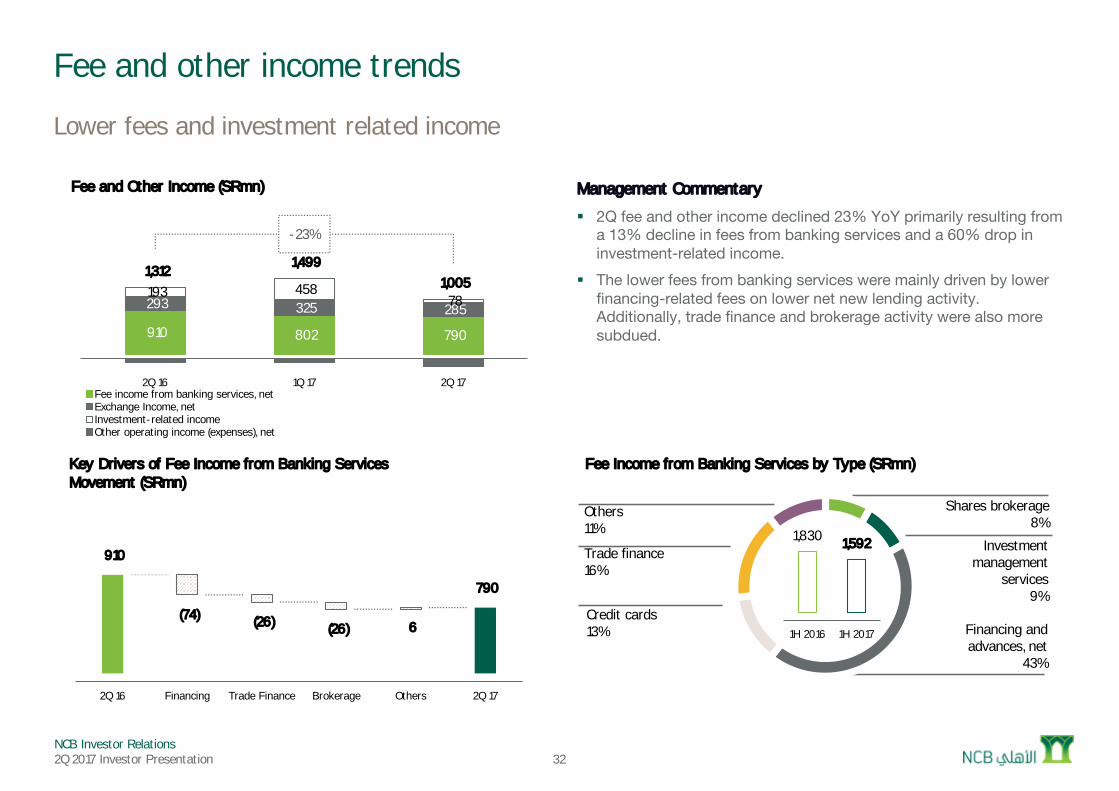

Fee and other income trends

Management Commentary

§ 2Q fee and other income declined 23% YoY primarily resulting from a 13% decline in fees from banking services and a 60% drop in investment-related income.

§ The lower fees from banking services were mainly driven by lower financing-related fees on lower net new lending activity. Additionally, trade finance and brokerage activity were also more subdued.

Lower fees and investment related income

910 802 790

293 325 285 193 458

78

1,312 1,499

1,005

-23%

(200)

300

800

1,300

1,800

2,300

2,800

2Q 16 1Q 17 2Q 17

Fee and Other Income (SRmn)

Fee income from banking services, netExchange Income, netInvestment-related incomeOther operating income (expenses), net

910

(74) (26) (26) 6

790

0

100

200

300

400

500

600

700

2Q 16 Financing Trade Finance Brokerage Others 2Q 17

Key Drivers of Fee Income from Banking Services Movement (SRmn)

Shares brokerage8%

Investment management

services9%

Financing and advances, net

43%

Credit cards13%

Trade finance16%

Others11%

Fee Income from Banking Services by Type (SRmn)

1,830 1,592

0

500

1,000

1,500

2,000

2,500

1H 2016 1H 2017

NCB Investor Relations2Q 2017 Investor Presentation 33

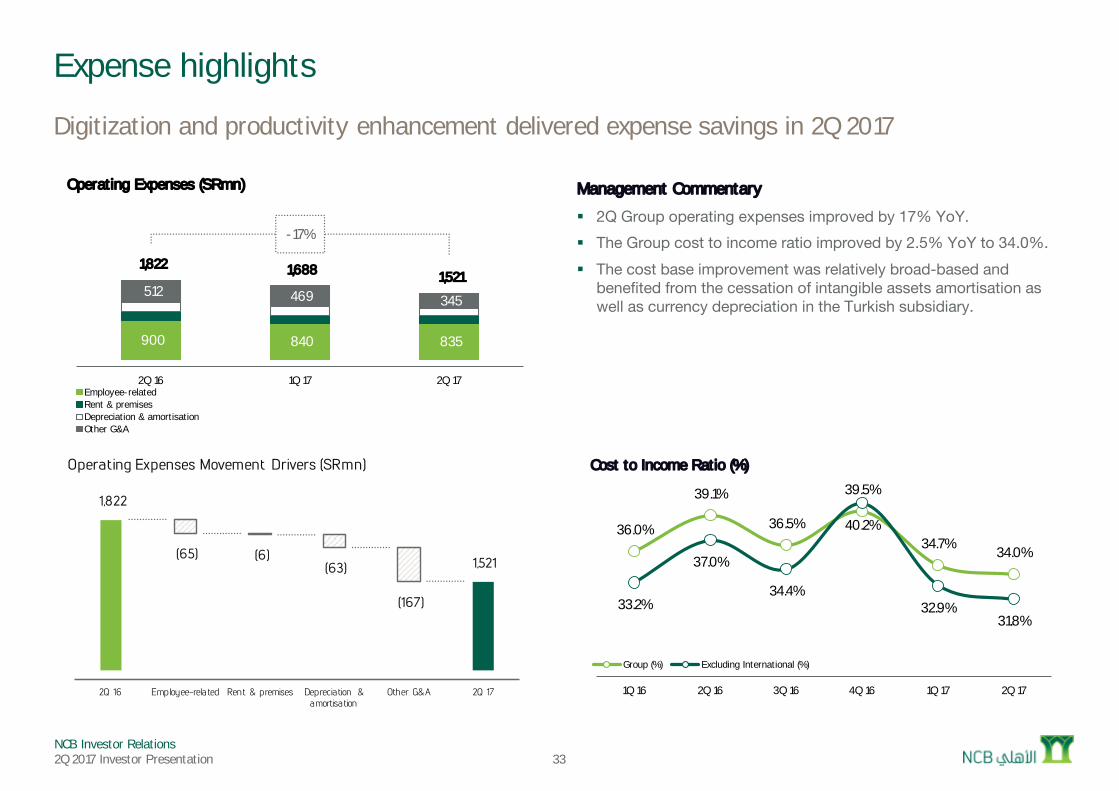

Expense highlights

Digitization and productivity enhancement delivered expense savings in 2Q 2017

Management Commentary

§ 2Q Group operating expenses improved by 17% YoY.§ The Group cost to income ratio improved by 2.5% YoY to 34.0%. § The cost base improvement was relatively broad-based and

benefited from the cessation of intangible assets amortisation as well as currency depreciation in the Turkish subsidiary.

36.0%

39.1%

36.5%

39.5%

34.7% 34.0%

33.2%

37.0%

34.4%

40.2%

32.9%31.8%

0

0

0

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Cost to Income Ratio (%)

Group (%) Excluding International (%)

900 840 835

512 469 345

1,822 1,688 1,521

-17%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2Q 16 1Q 17 2Q 17

Operating Expenses (SRmn)

Employee-relatedRent & premisesDepreciation & amortisationOther G&A

1,822

(65)(63)

(6)

(167)

1,521

0

100

200

300

400

500

600

700

800

900

2Q 16 Employee-related Rent & premises Depreciation & amortisation

Other G&A 2Q 17

Operating Expenses Movement Drivers (SRmn)

NCB Investor Relations2Q 2017 Investor Presentation

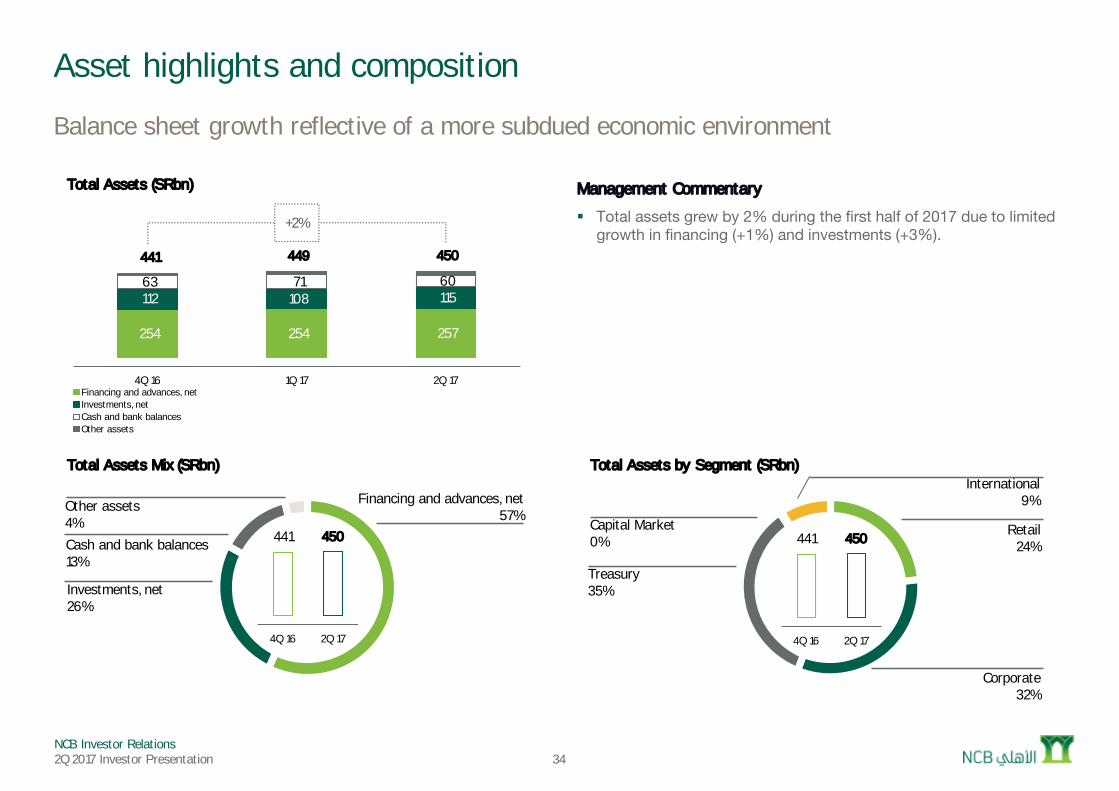

Retail24%

Corporate32%

Treasury35%

Capital Market0%

International9%

Total Assets by Segment (SRbn)

34

Asset highlights and composition

Balance sheet growth reflective of a more subdued economic environment

254 254 257

112 108 115 63 71 60

441 449 450

+2%

0

100

200

300

400

500

600

700

800

4Q 16 1Q 17 2Q 17

Total Assets (SRbn)

Financing and advances, netInvestments, netCash and bank balancesOther assets

Financing and advances, net57%

Investments, net26%

Cash and bank balances13%

Other assets4%

Total Assets Mix (SRbn)

Management Commentary

§ Total assets grew by 2% during the first half of 2017 due to limited growth in financing (+1%) and investments (+3%).

441 450

0

100

200

300

400

500

600

4Q 16 2Q 17

441 450

0

100

200

300

400

500

600

4Q 16 2Q 17

NCB Investor Relations2Q 2017 Investor Presentation

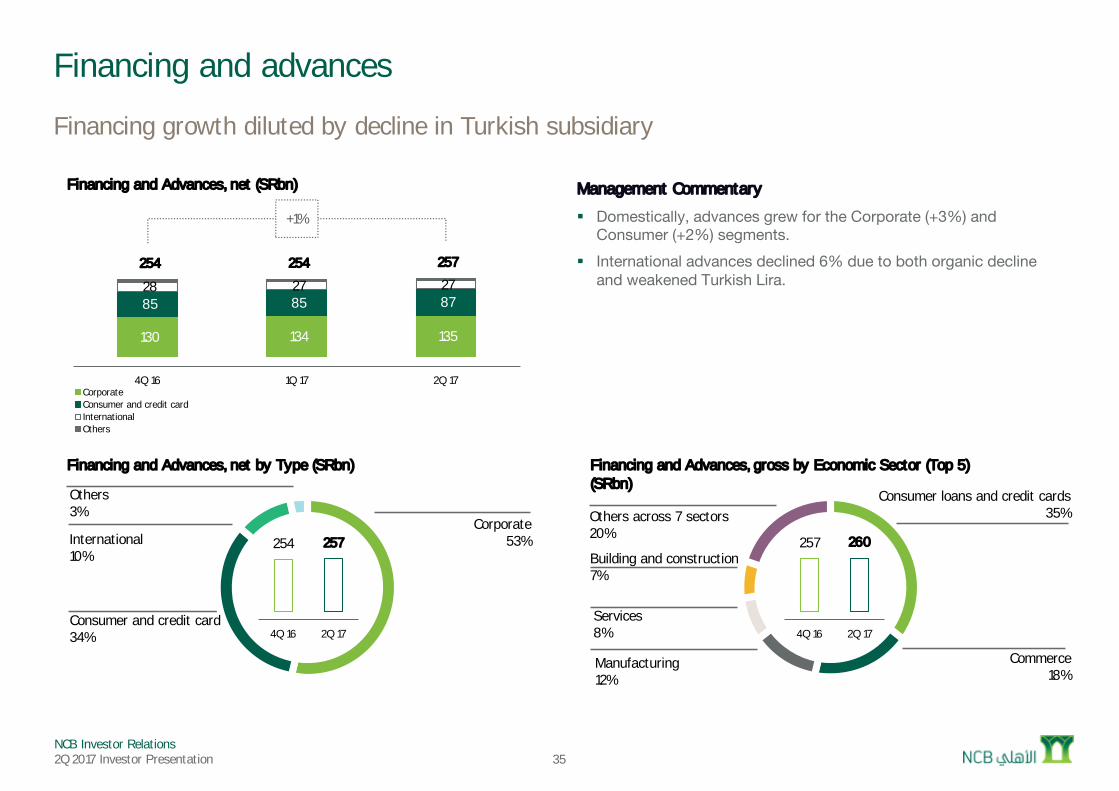

Consumer loans and credit cards35%

Commerce18%

Manufacturing12%

Services8%

Building and construction7%

Others across 7 sectors20%

Financing and Advances, gross by Economic Sector (Top 5) (SRbn)

35

Financing and advances

Financing growth diluted by decline in Turkish subsidiary

Management Commentary

§ Domestically, advances grew for the Corporate (+3%) and Consumer (+2%) segments.

§ International advances declined 6% due to both organic decline and weakened Turkish Lira.

254 257

0

50

100

150

200

250

300

350

400

4Q 16 2Q 17

130 134 135

85 85 87 28 27 27 254 254 257

+1%

0

50

100

150

200

250

300

350

400

450

500

4Q 16 1Q 17 2Q 17

Financing and Advances, net (SRbn)

CorporateConsumer and credit cardInternationalOthers

Corporate53%

Consumer and credit card34%

International10%

Others3%

Financing and Advances, net by Type (SRbn)

257 260

0

50

100

150

200

250

300

350

400

4Q 16 2Q 17

NCB Investor Relations2Q 2017 Investor Presentation 36

Financing and advances credit quality (1)

Rise in Corporate NPLs and impairment allowances partly offset by Retail and International

0.08 0.15 0.20 0.18 0.26 0.25 0.11 0.02

0.41 0.08 0.17 0.15 0.21

0.24

0.21 0.08 0.05 0.35 0.38

0.84

0.36 0.42 0.47

+24%

0

0

0

1

1

1

1

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Impairment Charge (SRbn)

CorporateConsumer and credit cardInternationalOthers

2.77 2.72 3.15 3.03 3.06 3.23

3.02 2.84 2.97 2.90 3.09 3.27

5.79 5.56 6.12 5.93 6.15 6.50

+17%

0

2

4

6

8

10

12

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Impairment Allowances (SRbn)

Portfolio (collective) allowancesSpecific allowances

2.88 2.93 3.14 3.41 3.68 3.92 1.38 1.27 1.44 1.22 1.16 1.24 1.49 1.32 1.50 1.26 1.27 1.29 5.79 5.56 6.12 5.93 6.15 6.50

+17%

0

2

4

6

8

10

12

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Impairment Allowances (SRbn)

CorporateConsumer and credit cardInternationalOthers

1.57 1.65 1.74 1.93 2.13 2.34 0.53 0.56 0.62 0.51 0.49 0.49 1.86 1.62 1.82 1.48 1.48 1.50

3.96 3.83 4.17 3.93 4.10 4.33

+13%

0

1

2

3

4

5

6

7

8

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NPL (SRbn)

CorporateConsumer and credit cardInternationalOthers

NCB Investor Relations2Q 2017 Investor Presentation 37

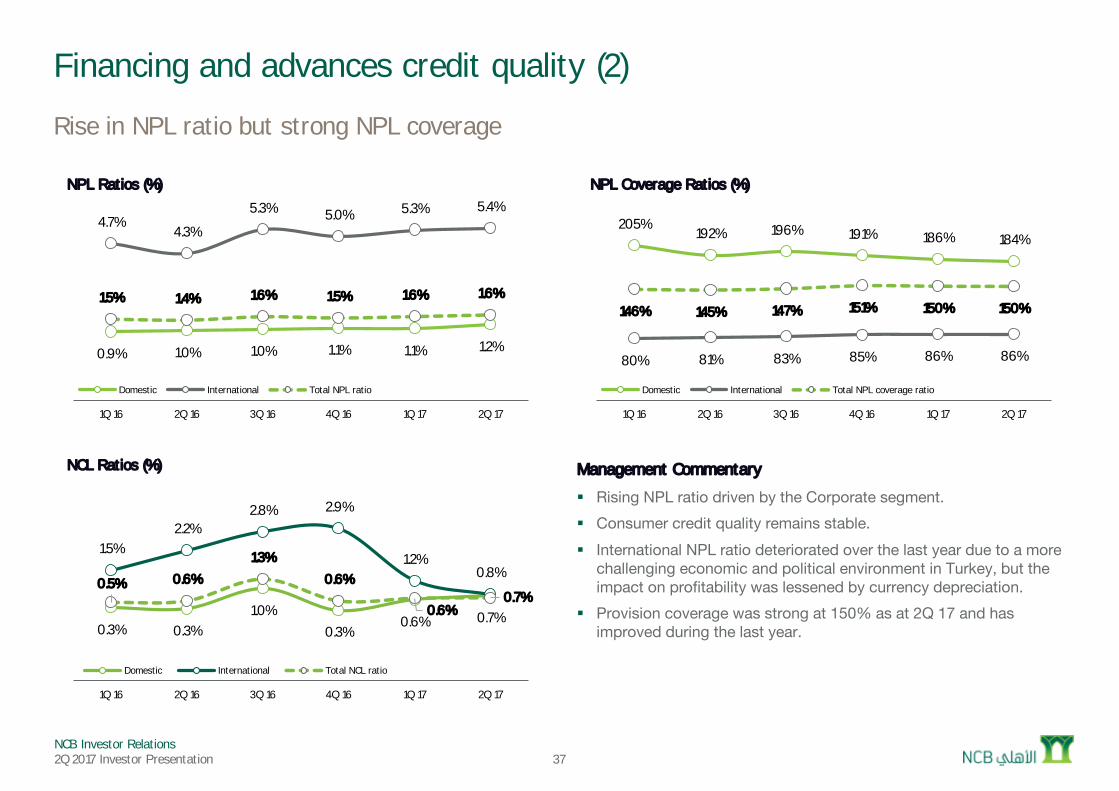

Financing and advances credit quality (2)

Rise in NPL ratio but strong NPL coverage

Management Commentary

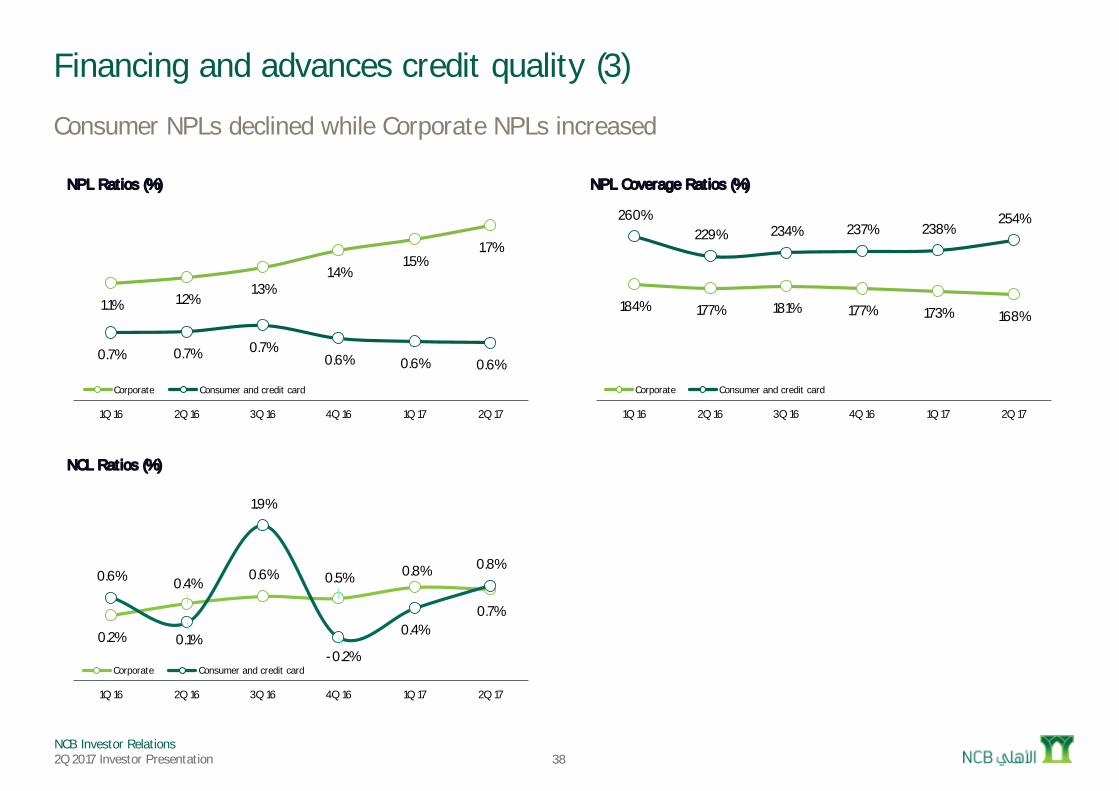

§ Rising NPL ratio driven by the Corporate segment.§ Consumer credit quality remains stable.§ International NPL ratio deteriorated over the last year due to a more

challenging economic and political environment in Turkey, but the impact on profitability was lessened by currency depreciation.

§ Provision coverage was strong at 150% as at 2Q 17 and has improved during the last year.

205%192% 196% 191% 186% 184%

80% 81% 83% 85% 86% 86%

146% 145% 147% 151% 150% 150%

(0)

0

1

1

2

2

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NPL Coverage Ratios (%)

Domestic International Total NPL coverage ratio

0.9% 1.0% 1.0% 1.1% 1.1% 1.2%

4.7%4.3%

5.3% 5.0% 5.3% 5.4%

1.5% 1.4% 1.6% 1.5% 1.6% 1.6%

(0)

(0)

0

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NPL Ratios (%)

Domestic International Total NPL ratio

0.3% 0.3%1.0%

0.3%0.6% 0.7%

1.5%2.2%

2.8% 2.9%

1.2%0.8%

0.5% 0.6%

1.3%

0.6%

0.6%0.7%

(0)

(0)

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NCL Ratios (%)

Domestic International Total NCL ratio

NCB Investor Relations2Q 2017 Investor Presentation 38

Financing and advances credit quality (3)

Consumer NPLs declined while Corporate NPLs increased

1.1% 1.2%1.3%

1.4%1.5%

1.7%

0.7% 0.7% 0.7%0.6% 0.6% 0.6%

0

0

0

0

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NPL Ratios (%)

Corporate Consumer and credit card

184% 177% 181% 177% 173% 168%

260%229% 234% 237% 238%

254%

(0)

0

1

1

2

2

3

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NPL Coverage Ratios (%)

Corporate Consumer and credit card

0.2%

0.4%0.6% 0.5% 0.8%

0.7%

0.6%

0.1%

1.9%

-0.2%

0.4%

0.8%

(0)

(0)

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

NCL Ratios (%)

Corporate Consumer and credit card

NCB Investor Relations2Q 2017 Investor Presentation

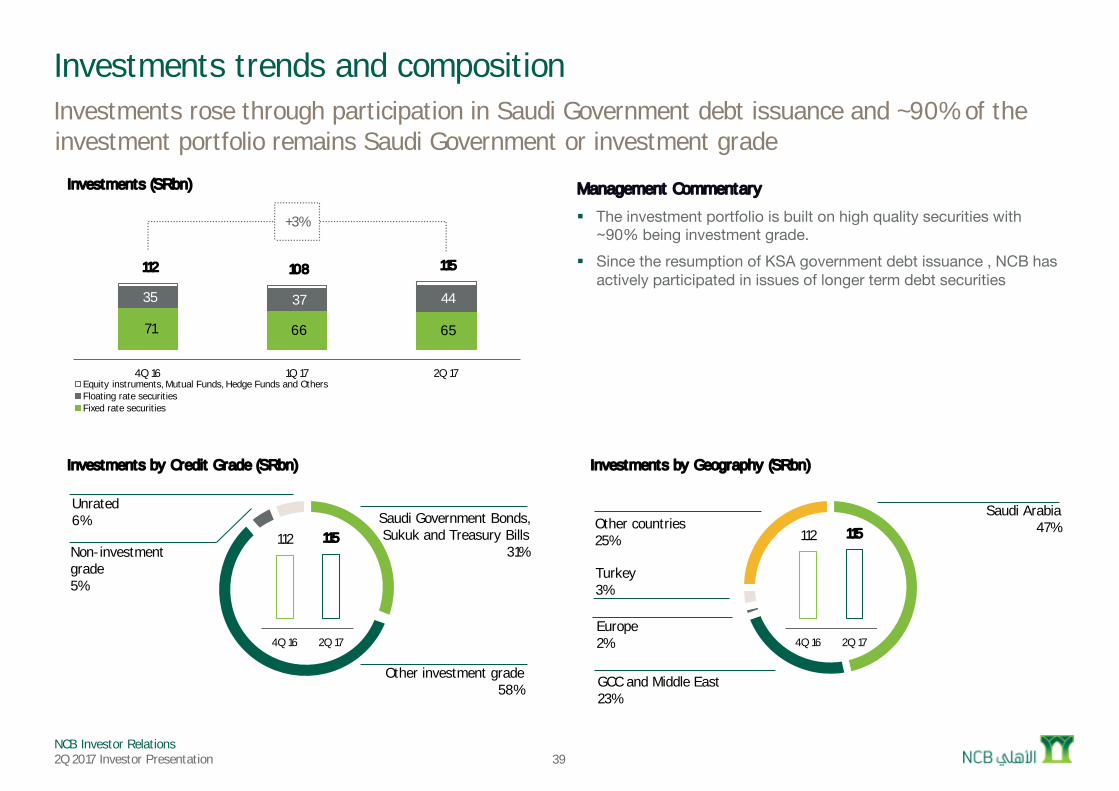

Saudi Arabia47%

GCC and Middle East23%

Europe2%

Turkey3%

Other countries25%

Investments by Geography (SRbn)

Investments trends and compositionInvestments rose through participation in Saudi Government debt issuance and ~90% of the investment portfolio remains Saudi Government or investment grade

112 115

0

20

40

60

80

100

120

140

160

4Q 16 2Q 17

Management Commentary

§ The investment portfolio is built on high quality securities with ~90% being investment grade.

§ Since the resumption of KSA government debt issuance , NCB has actively participated in issues of longer term debt securities

Saudi Government Bonds, Sukuk and Treasury Bills

31%

Other investment grade58%

Non-investment grade5%

Unrated6%

Investments by Credit Grade (SRbn)

112 115

0

20

40

60

80

100

120

140

160

180

4Q 16 2Q 17

39

71 66 65

35 37 44

112 108 115

+3%

0

50

100

150

200

250

4Q 16 1Q 17 2Q 17

Investments (SRbn)

Equity instruments, Mutual Funds, Hedge Funds and OthersFloating rate securitiesFixed rate securities

NCB Investor Relations2Q 2017 Investor Presentation 40

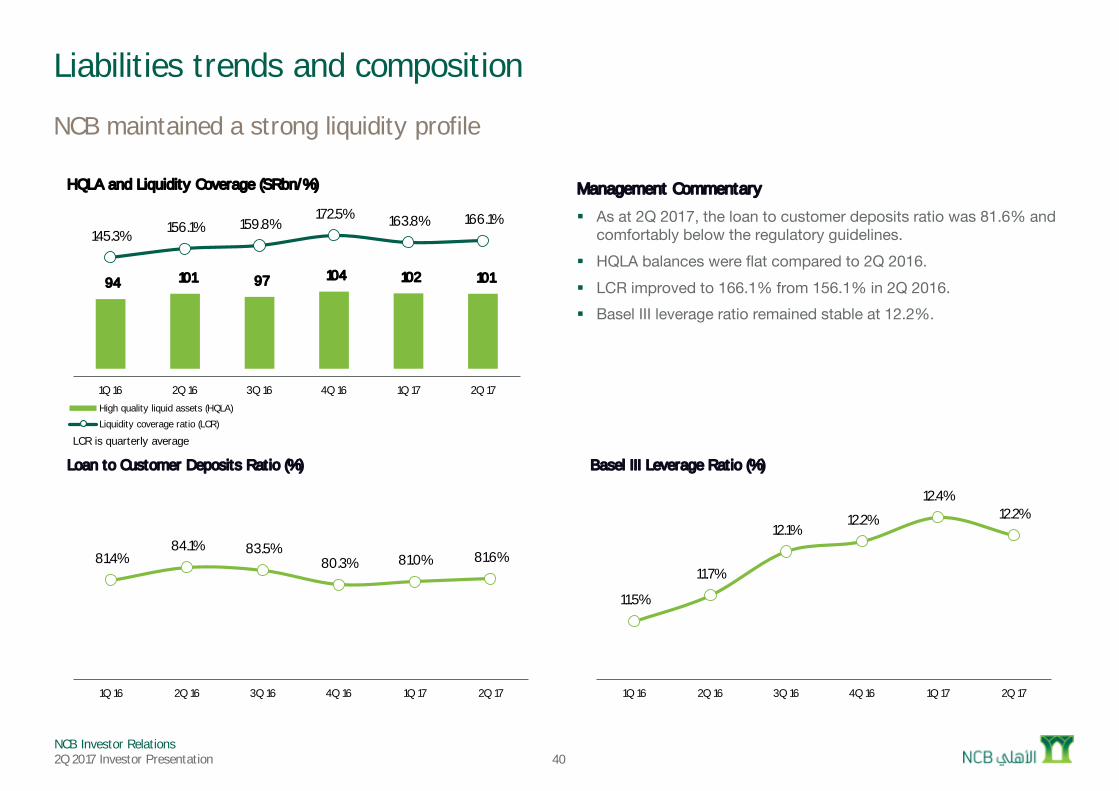

Liabilities trends and composition

NCB maintained a strong liquidity profile

Management Commentary

§ As at 2Q 2017, the loan to customer deposits ratio was 81.6% and comfortably below the regulatory guidelines.

§ HQLA balances were flat compared to 2Q 2016.§ LCR improved to 166.1% from 156.1% in 2Q 2016.§ Basel III leverage ratio remained stable at 12.2%.

81.4%84.1% 83.5%

80.3% 81.0% 81.6%

1

1

1

1

1

1

1

1

1

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Loan to Customer Deposits Ratio (%)

11.5%

11.7%

12.1%12.2%

12.4%12.2%

0

0

0

0

0

0

0

0

0

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Basel III Leverage Ratio (%)

LCR is quarterly average

94 101 97 104 102 101

145.3% 156.1% 159.8%172.5% 163.8% 166.1%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

200.0%

0

50

100

150

200

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

HQLA and Liquidity Coverage (SRbn/%)

High quality liquid assets (HQLA)

Liquidity coverage ratio (LCR)

NCB Investor Relations2Q 2017 Investor Presentation

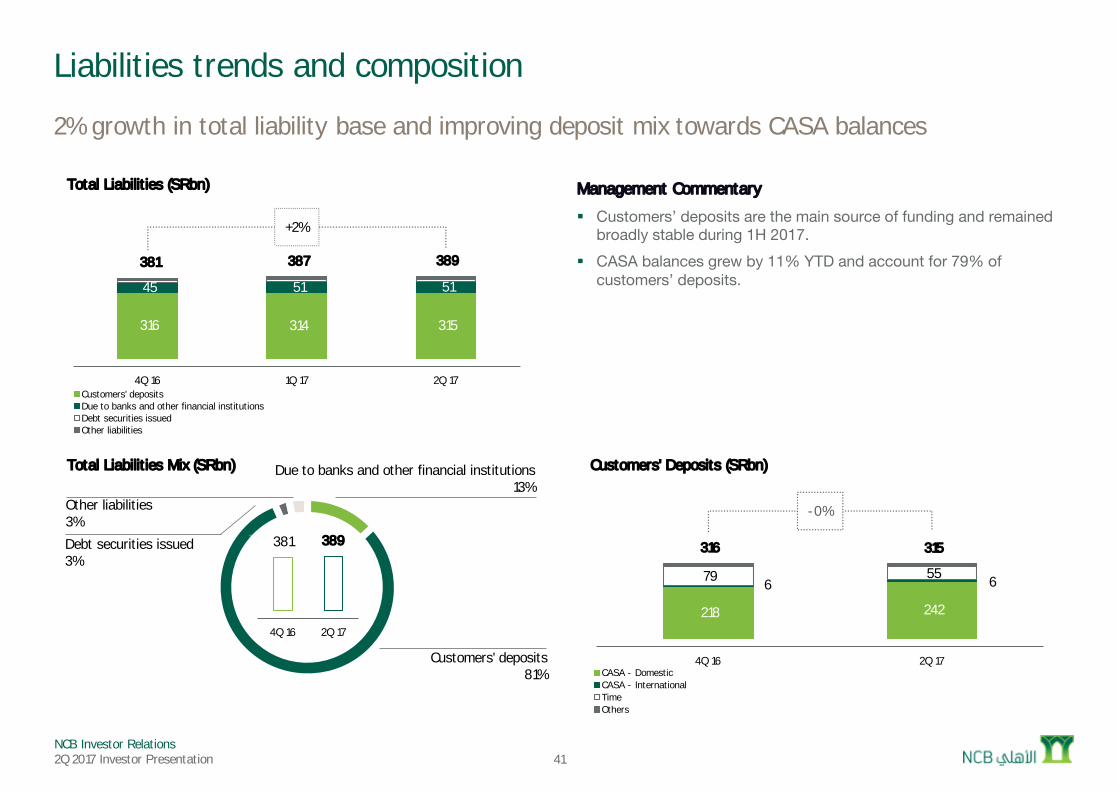

Due to banks and other financial institutions13%

Customers' deposits81%

Debt securities issued3%

Other liabilities3%

Total Liabilities Mix (SRbn)

41

Liabilities trends and composition

2% growth in total liability base and improving deposit mix towards CASA balances

Management Commentary

§ Customers’ deposits are the main source of funding and remained broadly stable during 1H 2017.

§ CASA balances grew by 11% YTD and account for 79% of customers’ deposits.

316 314 315

45 51 51

381 387 389

+2%

0

100

200

300

400

500

600

700

4Q 16 1Q 17 2Q 17

Total Liabilities (SRbn)

Customers' depositsDue to banks and other financial institutionsDebt securities issuedOther liabilities

381 389

0

100

200

300

400

500

600

4Q 16 2Q 17

218 242

6 6 79 55

316 315

-0%

0

100

200

300

400

500

600

4Q 16 2Q 17

Customers' Deposits (SRbn)

CASA - DomesticCASA - InternationalTimeOthers

NCB Investor Relations2Q 2017 Investor Presentation

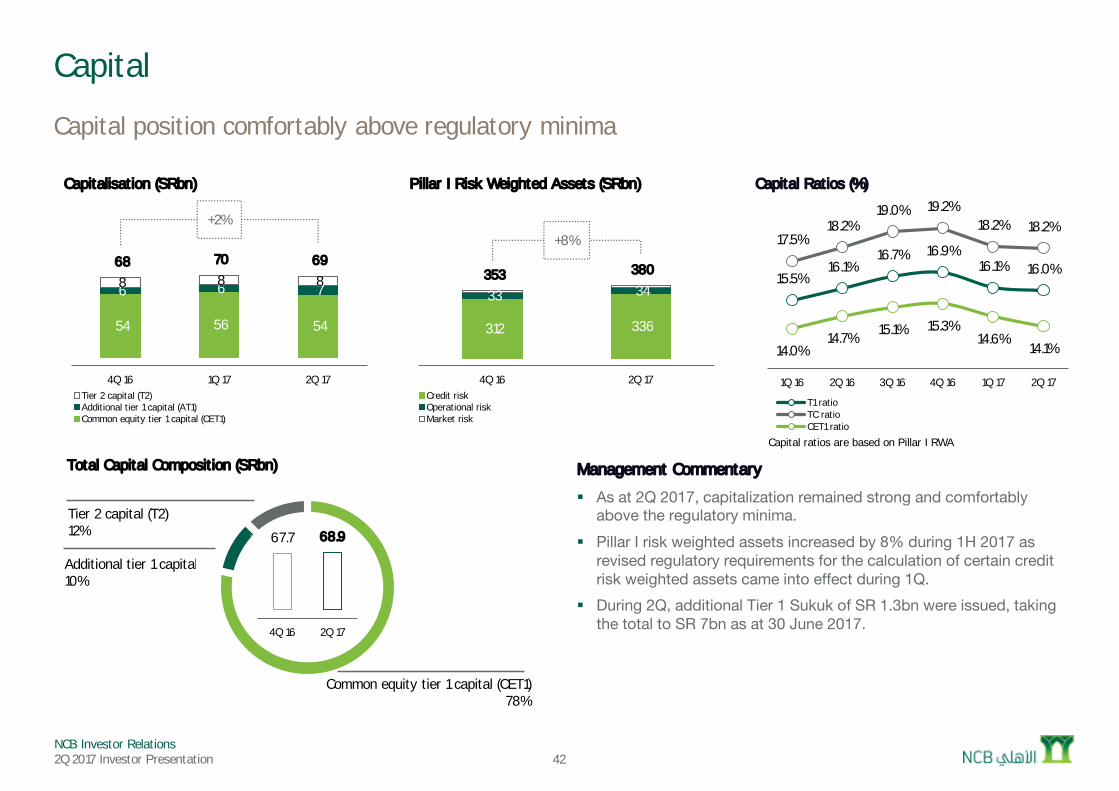

Management Commentary

§ As at 2Q 2017, capitalization remained strong and comfortably above the regulatory minima.

§ Pillar I risk weighted assets increased by 8% during 1H 2017 as revised regulatory requirements for the calculation of certain credit risk weighted assets came into effect during 1Q.

§ During 2Q, additional Tier 1 Sukuk of SR 1.3bn were issued, taking the total to SR 7bn as at 30 June 2017.

Common equity tier 1 capital (CET1)78%

Additional tier 1 capital (AT1)10%

Tier 2 capital (T2)12%

Total Capital Composition (SRbn)

42

Capital

Capital position comfortably above regulatory minima

67.7 68.9

0

10

20

30

40

50

60

70

80

90

100

4Q 16 2Q 17

Capital ratios are based on Pillar I RWA

15.5%16.1%

16.7% 16.9%16.1% 16.0%

17.5%18.2%

19.0% 19.2%18.2% 18.2%

14.0%14.7% 15.1% 15.3%

14.6%14.1%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17

Capital Ratios (%)

T1 ratioTC ratioCET1 ratio

312 336

33 34 353 380

+8%

0

100

200

300

400

500

600

700

800

4Q 16 2Q 17

Pillar I Risk Weighted Assets (SRbn)

Credit riskOperational riskMarket risk

54 56 54

6 6 7 8 8 8 68 70 69

+2%

0

20

40

60

80

100

120

4Q 16 1Q 17 2Q 17

Capitalisation (SRbn)

Tier 2 capital (T2)Additional tier 1 capital (AT1)Common equity tier 1 capital (CET1)

NCB Investor Relations2Q 2017 Investor Presentation

National Commercial Bank

Segmental Review

2Q 2017 Results

NCB Investor Relations2Q 2017 Investor Presentation

Retail42%

Corporate25%

Treasury21%

Capital Market3%

International9%

Total Operating Income by Segment (SRbn)

44

Segmental Information

Total operating income lower on trading, dividend income and currency translation

9.4 9.3

0

2

4

6

8

10

12

14

1H 2016 1H 2017

5.1 5.3 5.7 6.4 7.5 2.3 3.4 3.7 4.1 4.6 3.2 3.4 3.8 4.1 3.7 2.1 2.1 2.3 2.2 2.2 13.5 14.9 16.2 17.5 18.6

+8%

0

5

10

15

20

25

30

2012 2013 2014 2015 2016

Total Operating Income (SRbn)

RetailCorporateTreasuryCapital MarketInternational

4,660 33

(63)

45

(3)

(194)

4,478

0

100

200

300

400

500

600

2Q 16 Retail Corporate Treasury Capital Market International 2Q 17

Total Operating Income Growth by Segment (SRmn)

NCB Investor Relations2Q 2017 Investor Presentation

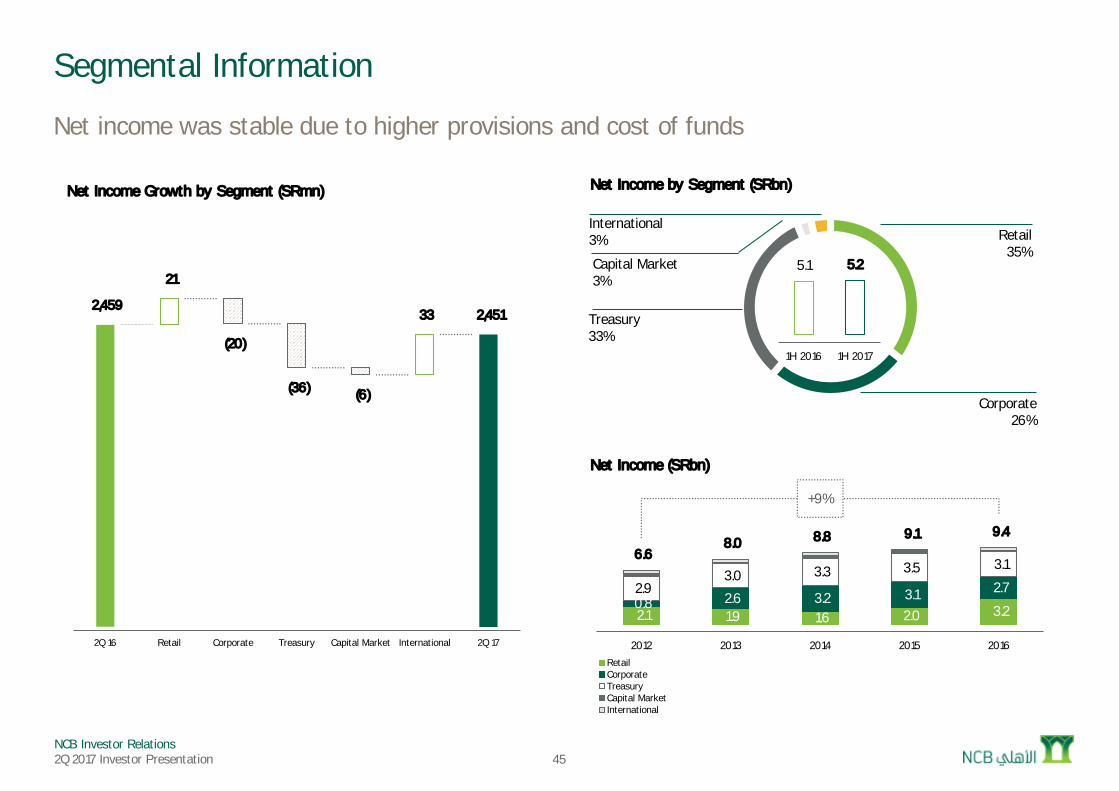

Retail35%

Corporate26%

Treasury33%

Capital Market3%

International3%

Net Income by Segment (SRbn)

45

Segmental Information

Net income was stable due to higher provisions and cost of funds

2.1 1.9 1.6 2.0 3.2 0.8 2.6 3.2 3.1 2.7 2.9 3.0 3.3 3.5 3.1

6.6 8.0 8.8 9.1 9.4

+9%

0

2

4

6

8

10

12

14

16

2012 2013 2014 2015 2016

Net Income (SRbn)

RetailCorporateTreasuryCapital MarketInternational

5.1 5.2

0

1

2

3

4

5

6

7

8

1H 2016 1H 2017

2,459

21

(36)

(20)

(6)

33 2,451

0

50

100

150

200

250

300

2Q 16 Retail Corporate Treasury Capital Market International 2Q 17

Net Income Growth by Segment (SRmn)

NCB Investor Relations2Q 2017 Investor Presentation 46

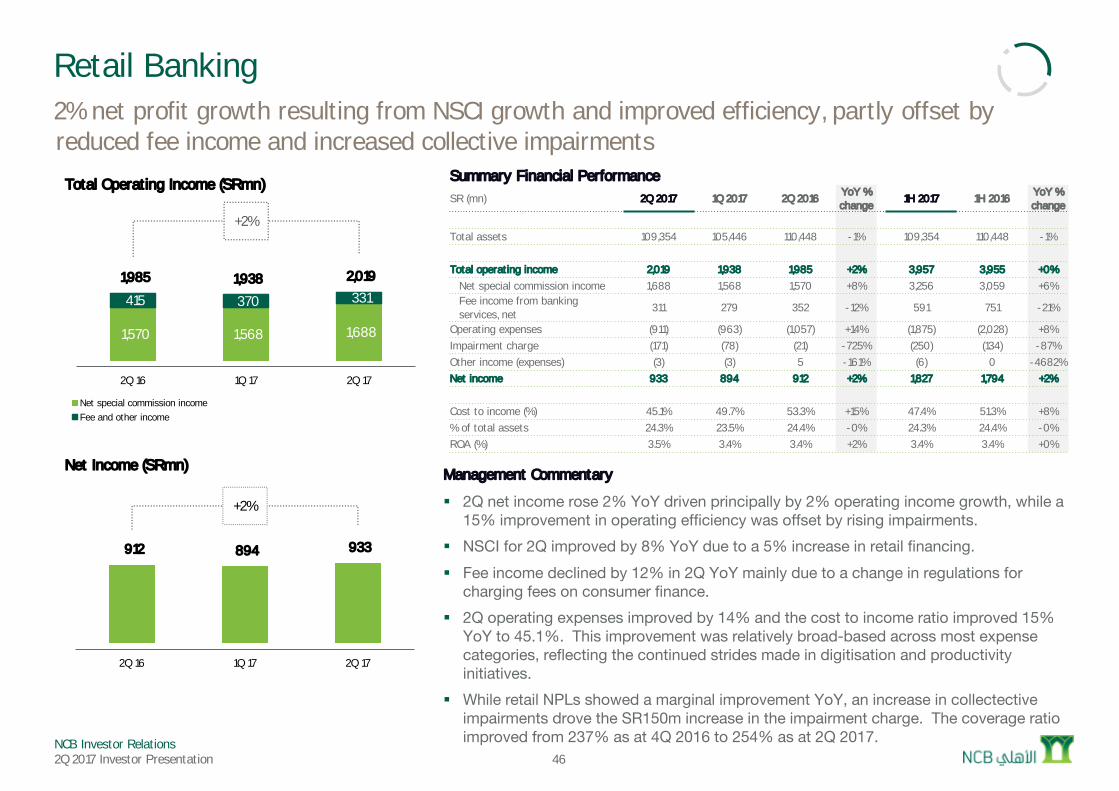

Retail Banking2% net profit growth resulting from NSCI growth and improved efficiency, partly offset by reduced fee income and increased collective impairments

Management Commentary

§ 2Q net income rose 2% YoY driven principally by 2% operating income growth, while a 15% improvement in operating efficiency was offset by rising impairments.

§ NSCI for 2Q improved by 8% YoY due to a 5% increase in retail financing.§ Fee income declined by 12% in 2Q YoY mainly due to a change in regulations for

charging fees on consumer finance.§ 2Q operating expenses improved by 14% and the cost to income ratio improved 15%

YoY to 45.1%. This improvement was relatively broad-based across most expense categories, reflecting the continued strides made in digitisation and productivity initiatives.

§ While retail NPLs showed a marginal improvement YoY, an increase in collectective impairments drove the SR150m increase in the impairment charge. The coverage ratio improved from 237% as at 4Q 2016 to 254% as at 2Q 2017.

1,570 1,568 1,688

415 370 331 1,985 1,938 2,019

+2%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2Q 16 1Q 17 2Q 17

Total Operating Income (SRmn)

Net special commission incomeFee and other income

912 894 933

+2%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2Q 16 1Q 17 2Q 17

Net Income (SRmn)

Summary Financial PerformanceSR (mn) 2Q 2017 1Q 2017 2Q 2016 YoY %

change1H 2017 1H 2016 YoY %

change

Total assets 109,354 105,446 110,448 -1% 109,354 110,448 -1%

Total operating income 2,019 1,938 1,985 +2% 3,957 3,955 +0%Net special commission income 1,688 1,568 1,570 +8% 3,256 3,059 +6%Fee income from banking services, net

311 279 352 -12% 591 751 -21%

Operating expenses (911) (963) (1,057) +14% (1,875) (2,028) +8%Impairment charge (171) (78) (21) -725% (250) (134) -87%Other income (expenses) (3) (3) 5 -161% (6) 0 -4682%Net income 933 894 912 +2% 1,827 1,794 +2%

Cost to income (%) 45.1% 49.7% 53.3% +15% 47.4% 51.3% +8%% of total assets 24.3% 23.5% 24.4% -0% 24.3% 24.4% -0%ROA (%) 3.5% 3.4% 3.4% +2% 3.4% 3.4% +0%

NCB Investor Relations2Q 2017 Investor Presentation 47

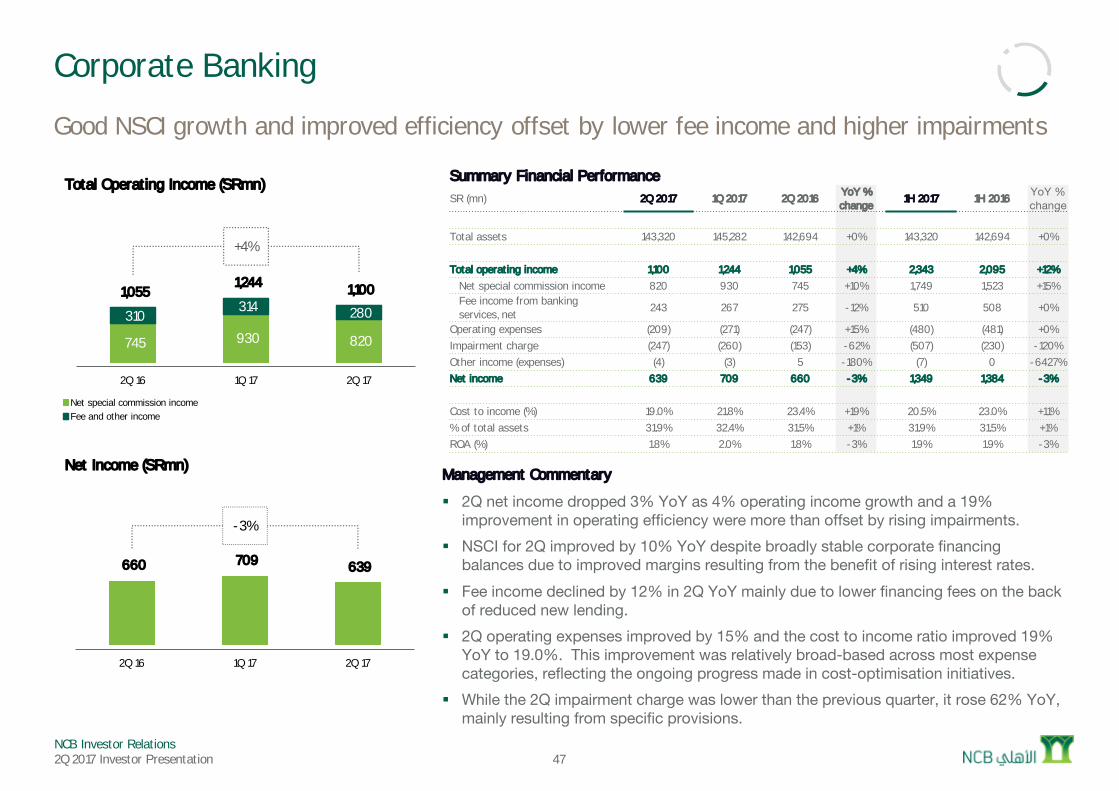

Corporate Banking

Good NSCI growth and improved efficiency offset by lower fee income and higher impairments

Management Commentary

§ 2Q net income dropped 3% YoY as 4% operating income growth and a 19% improvement in operating efficiency were more than offset by rising impairments.

§ NSCI for 2Q improved by 10% YoY despite broadly stable corporate financing balances due to improved margins resulting from the benefit of rising interest rates.

§ Fee income declined by 12% in 2Q YoY mainly due to lower financing fees on the back of reduced new lending.

§ 2Q operating expenses improved by 15% and the cost to income ratio improved 19% YoY to 19.0%. This improvement was relatively broad-based across most expense categories, reflecting the ongoing progress made in cost-optimisation initiatives.

§ While the 2Q impairment charge was lower than the previous quarter, it rose 62% YoY, mainly resulting from specific provisions.

745 930 820

310 314 280

1,055 1,244 1,100

+4%

0

500

1,000

1,500

2,000

2,500

3,000

2Q 16 1Q 17 2Q 17

Total Operating Income (SRmn)

Net special commission incomeFee and other income

660 709 639

-3%

0

200

400

600

800

1,000

1,200

1,400

1,600

2Q 16 1Q 17 2Q 17

Net Income (SRmn)

Summary Financial PerformanceSR (mn) 2Q 2017 1Q 2017 2Q 2016 YoY %

change1H 2017 1H 2016 YoY %

change

Total assets 143,320 145,282 142,694 +0% 143,320 142,694 +0%

Total operating income 1,100 1,244 1,055 +4% 2,343 2,095 +12%Net special commission income 820 930 745 +10% 1,749 1,523 +15%Fee income from banking services, net

243 267 275 -12% 510 508 +0%

Operating expenses (209) (271) (247) +15% (480) (481) +0%Impairment charge (247) (260) (153) -62% (507) (230) -120%Other income (expenses) (4) (3) 5 -180% (7) 0 -6427%Net income 639 709 660 -3% 1,349 1,384 -3%

Cost to income (%) 19.0% 21.8% 23.4% +19% 20.5% 23.0% +11%% of total assets 31.9% 32.4% 31.5% +1% 31.9% 31.5% +1%ROA (%) 1.8% 2.0% 1.8% -3% 1.9% 1.9% -3%

NCB Investor Relations2Q 2017 Investor Presentation 48

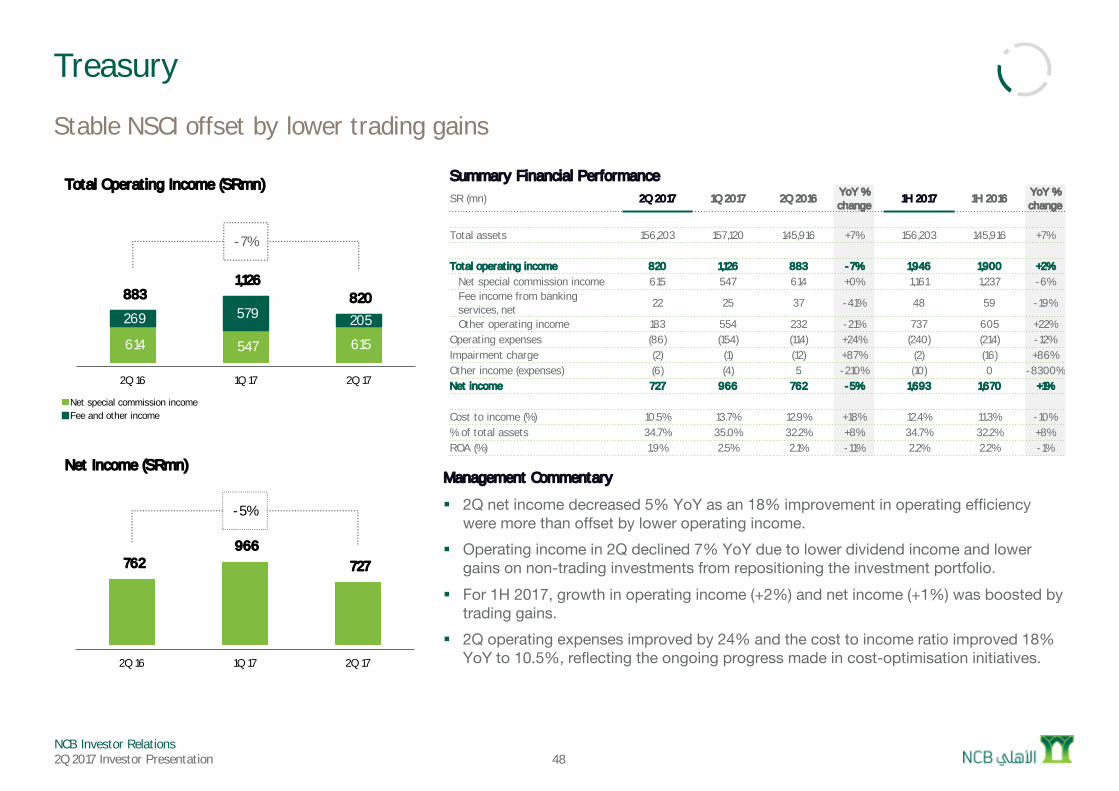

Treasury

Stable NSCI offset by lower trading gains

Management Commentary

§ 2Q net income decreased 5% YoY as an 18% improvement in operating efficiency were more than offset by lower operating income.

§ Operating income in 2Q declined 7% YoY due to lower dividend income and lower gains on non-trading investments from repositioning the investment portfolio.

§ For 1H 2017, growth in operating income (+2%) and net income (+1%) was boosted by trading gains.

§ 2Q operating expenses improved by 24% and the cost to income ratio improved 18% YoY to 10.5%, reflecting the ongoing progress made in cost-optimisation initiatives.

614 547 615

269 579 205

883 1,126

820

-7%

0

500

1,000

1,500

2,000

2,500

2Q 16 1Q 17 2Q 17

Total Operating Income (SRmn)

Net special commission incomeFee and other income

762 966

727

-5%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2Q 16 1Q 17 2Q 17

Net Income (SRmn)

Summary Financial PerformanceSR (mn) 2Q 2017 1Q 2017 2Q 2016 YoY %

change1H 2017 1H 2016 YoY %

change

Total assets 156,203 157,120 145,916 +7% 156,203 145,916 +7%

Total operating income 820 1,126 883 -7% 1,946 1,900 +2%Net special commission income 615 547 614 +0% 1,161 1,237 -6%Fee income from banking services, net

22 25 37 -41% 48 59 -19%

Other operating income 183 554 232 -21% 737 605 +22%Operating expenses (86) (154) (114) +24% (240) (214) -12%Impairment charge (2) (1) (12) +87% (2) (16) +86%Other income (expenses) (6) (4) 5 -210% (10) 0 -8300%Net income 727 966 762 -5% 1,693 1,670 +1%

Cost to income (%) 10.5% 13.7% 12.9% +18% 12.4% 11.3% -10%% of total assets 34.7% 35.0% 32.2% +8% 34.7% 32.2% +8%ROA (%) 1.9% 2.5% 2.1% -11% 2.2% 2.2% -1%

NCB Investor Relations2Q 2017 Investor Presentation 49

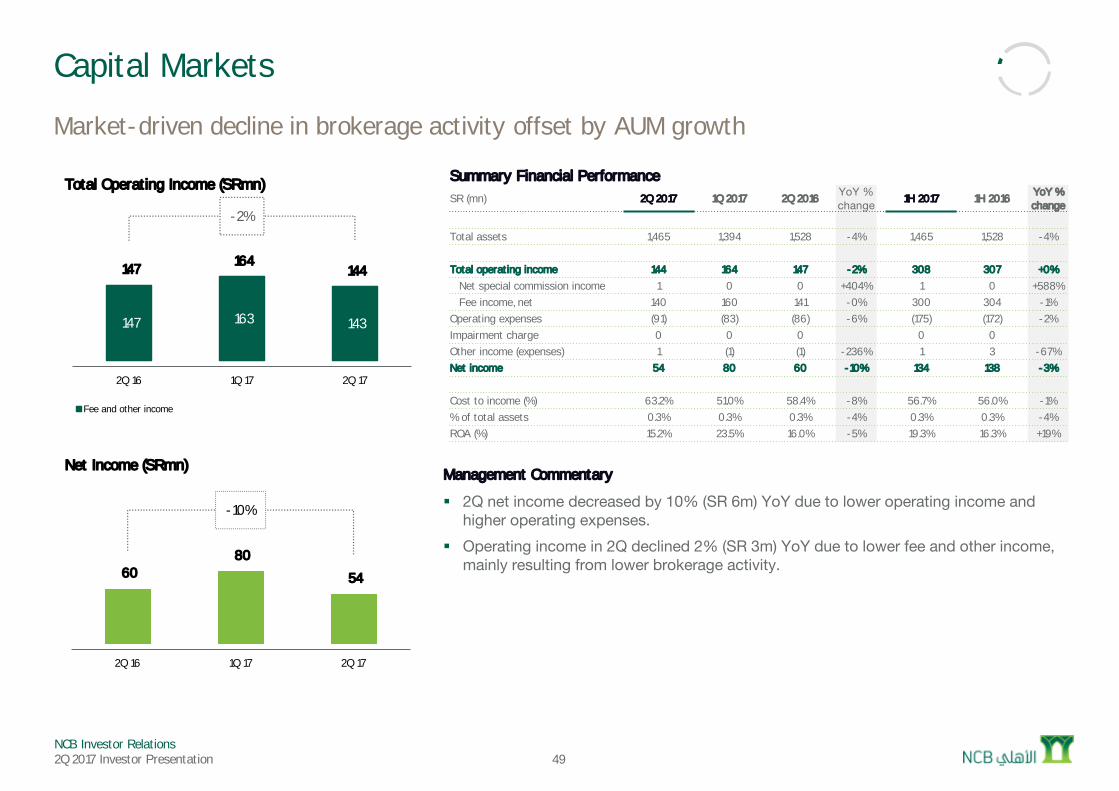

Capital Markets

Market-driven decline in brokerage activity offset by AUM growth

Management Commentary

§ 2Q net income decreased by 10% (SR 6m) YoY due to lower operating income and higher operating expenses.

§ Operating income in 2Q declined 2% (SR 3m) YoY due to lower fee and other income, mainly resulting from lower brokerage activity.

147 163 143

147 164 144

-2%

0

50

100

150

200

250

300

2Q 16 1Q 17 2Q 17

Total Operating Income (SRmn)

Fee and other income

60 80

54

-10%

0

20

40

60

80

100

120

140

160

2Q 16 1Q 17 2Q 17

Net Income (SRmn)

Summary Financial PerformanceSR (mn) 2Q 2017 1Q 2017 2Q 2016 YoY %

change 1H 2017 1H 2016 YoY % change

Total assets 1,465 1,394 1,528 -4% 1,465 1,528 -4%

Total operating income 144 164 147 -2% 308 307 +0%Net special commission income 1 0 0 +404% 1 0 +588%Fee income, net 140 160 141 -0% 300 304 -1%

Operating expenses (91) (83) (86) -6% (175) (172) -2%Impairment charge 0 0 0 0 0 Other income (expenses) 1 (1) (1) -236% 1 3 -67%Net income 54 80 60 -10% 134 138 -3%

Cost to income (%) 63.2% 51.0% 58.4% -8% 56.7% 56.0% -1%% of total assets 0.3% 0.3% 0.3% -4% 0.3% 0.3% -4%ROA (%) 15.2% 23.5% 16.0% -5% 19.3% 16.3% +19%

NCB Investor Relations2Q 2017 Investor Presentation 50

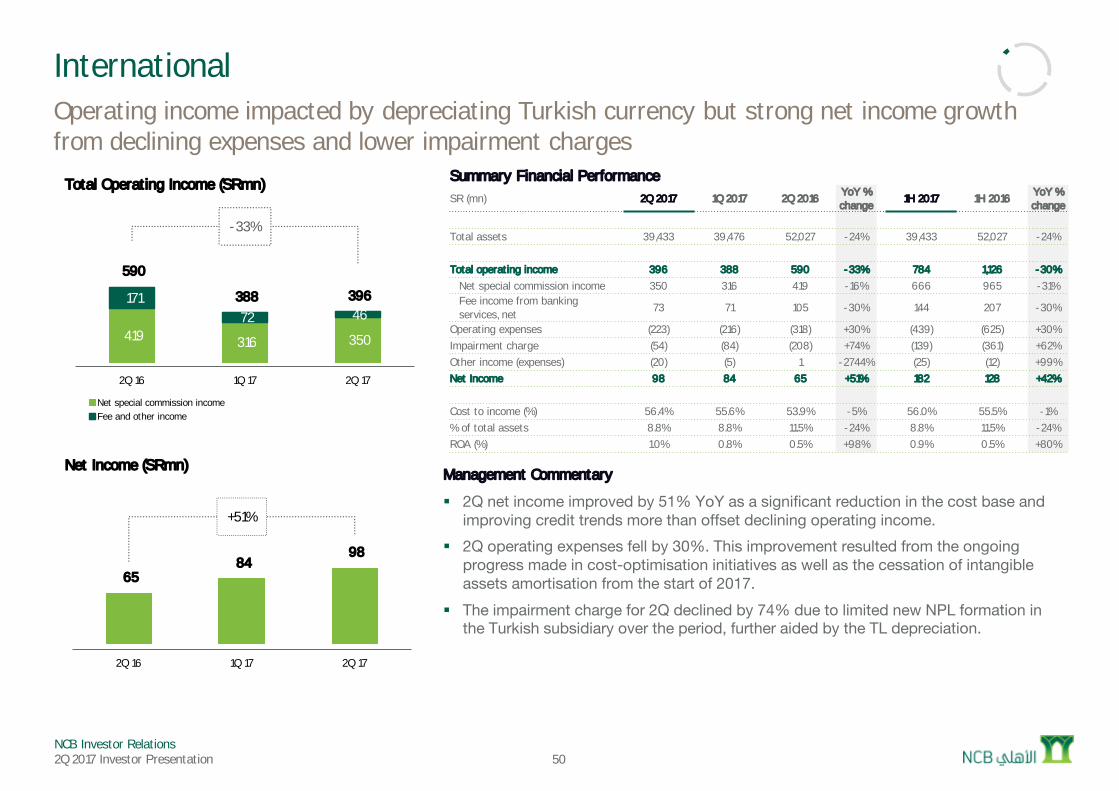

InternationalOperating income impacted by depreciating Turkish currency but strong net income growth from declining expenses and lower impairment charges

Management Commentary

§ 2Q net income improved by 51% YoY as a significant reduction in the cost base and improving credit trends more than offset declining operating income.

§ 2Q operating expenses fell by 30%. This improvement resulted from the ongoing progress made in cost-optimisation initiatives as well as the cessation of intangible assets amortisation from the start of 2017.

§ The impairment charge for 2Q declined by 74% due to limited new NPL formation in the Turkish subsidiary over the period, further aided by the TL depreciation.

419 316 350

171 72 46

590

388 396

-33%

0

200

400

600

800

1,000

1,200

2Q 16 1Q 17 2Q 17

Total Operating Income (SRmn)

Net special commission incomeFee and other income

65 84

98

+51%

0

20

40

60

80

100

120

140

160

180

200

2Q 16 1Q 17 2Q 17

Net Income (SRmn)

Summary Financial PerformanceSR (mn) 2Q 2017 1Q 2017 2Q 2016 YoY %

change1H 2017 1H 2016 YoY %

change

Total assets 39,433 39,476 52,027 -24% 39,433 52,027 -24%

Total operating income 396 388 590 -33% 784 1,126 -30%Net special commission income 350 316 419 -16% 666 965 -31%Fee income from banking services, net

73 71 105 -30% 144 207 -30%

Operating expenses (223) (216) (318) +30% (439) (625) +30%Impairment charge (54) (84) (208) +74% (139) (361) +62%Other income (expenses) (20) (5) 1 -2744% (25) (12) +99%Net Income 98 84 65 +51% 182 128 +42%

Cost to income (%) 56.4% 55.6% 53.9% -5% 56.0% 55.5% -1%% of total assets 8.8% 8.8% 11.5% -24% 8.8% 11.5% -24%ROA (%) 1.0% 0.8% 0.5% +98% 0.9% 0.5% +80%

NCB Investor Relations2Q 2017 Investor Presentation

National Commercial Bank

Additional Information

2Q 2017 Results

NCB Investor Relations2Q 2017 Investor Presentation 52

Additional Information

Please don’t hesitate to contact NCB Group Investor Relations

More information

Download copies of National Commercial Bank’s:

§ Financial statements

§ Earnings release

§ Investor presentation

§ Financial data pack (Excel)

Visit: http://www.alahli.com/en-us/Investor_Relation

Mr. Abdulbadie Alyafi

Head, Investor Relations

P: +966 12 646 3988

National Commercial Bank

P.O. Box 3555

21481 Jeddah, Kingdom of Saudi Arabia