National Audit Office Value For Money Report 2012 ... report provides an overview of the National...

48

National Audit Office Value For Money Report 2012: Financial Management 20 th June 2012 Paul Brown Director

Transcript of National Audit Office Value For Money Report 2012 ... report provides an overview of the National...

National Audit Office

Value For Money Report 2012:

Financial Management

20th June 2012

Paul Brown

Director

This report provides an overview of the National Audit

Office’s (NAO) approach to financial management. The

work has taken place as part of the annual Value For

Money review undertaken by RSM Tenon, the External

Auditor. The approach of the NAO has been assessed

using the model developed by the NAO for review of

financial management within Government departments.

This report is prepared solely for the use of National Audit Office (NAO)and the Public Accounts Commission (TPAC) of the House of Commons Details may be made to

specified external agencies, but otherwise the report should not be quoted or referred to in whole or in part without prior consent. No responsibility to any third party is accepted

as the report has not been prepared, and is not intended for, any other purpose.

Whilst every care has been taken to ensure that the information provided in this report is as accurate as possible, based on the information provided and documentation

reviewed, no complete guarantee or warranty can be given with regard to the advice and information contained herein.

This report is provided on the basis that it is for NAO and TPAC‟s information and usage only. For this reason, we do not consider it appropriate for the report to be made

available, in part or in full, to third parties without our written prior consent. Nor do we accept responsibility for any reliance that third parties may place upon the report. Insofar as

this report refers to matters of law, it should not be taken as expressing any formal opinion whatsoever.

Please refer to our letter of engagement for full details of responsibilities and other terms and conditions. RSM Tenon Limited is a member of RSM Tenon Group. RSM Tenon

Limited is an independent member firm of RSM International an affiliation of independent accounting and consulting firms. RSM International is the name given to a network of

independent accounting and consulting firms each of which practices in its own right. RSM International does not exist in any jurisdiction as a separate legal entity.

RSM Tenon Limited (No 4066924) is registered in England and Wales. Registered Office 66 Chiltern Street, London W1U 4GB, England.

03 Scope &

Approach

Page 15 to 16

10 Appendices

- Definitions of Financial Information by NAO staff

- NAO’s Financial Management Maturity Model – Level Scoring

- User guide graphs in the report

Page 44 to 48

Confidential

3

04 Background &

Governance

Page 17 to 19

07 Finance for

decision-making

Page 32 to 36

08 Financial

Monitoring &

Forecasting

Page 37 to 42

01 Executive

Summary

Page 4 to 10

02 Summary of

Recommendations

Page 11 to 14

05 Financial

Governance &

Leadership

Page 20 to 27

06 Financial

Planning

Page 28 to 31

09 Financial and

Performance

Reporting

Page 43

Overall Value For Money Conclusion

We find that financial management processes in the NAO are sound and that there is a high level of

engagement and ownership by the Board and Leadership Team with good levels of engagement by other

managers and staff.

Summary of Findings:

The NAO is striving to instill a culture of performance improvement across the organisation. The importance of this task has been

raised by Management‟s commitment to take cost out of the business. We found that there is a determination by the Board and the

Leadership Team to ensure that the quality of the audit is maintained, despite the reduction in resources.

There is a recognition that NAO staff need to be supported, trained and developed in financial management. The majority of staff

recognise this support. A minority of managers struggle to understand the information and the NAO should seek to help this minority

enhance their skills and confidence in the management of financial resources.

Financial management has an appropriately high profile in the organisation. There is evidence of this in the papers and through

questioning of Board members, the Leadership Team, managers and a large number of staff.

We say „appropriately‟ because the NAO is a relatively straightforward organisation: It does not have complex costing structures and

income is relatively fixed, one year to another. So whilst more complex organisations have more sophisticated financial management

systems and processes, the NAO‟s approach is appropriate to its complexity and the management information needed.

As the cultural change takes place, there are still some managers who find the new responsibilities and accountabilities more difficult

to accept - inevitable in our experience of this type of change. This manifests itself in some managers failing to provide all the

information required by central finance to monitor the full range of KPIs. The Board needs to support the management team in ensuring

that all managers comply with their full range of financial management responsibilities

The Board and Leadership team review risks and consider the risk register. We recommend that an action log is created to help the

monitoring process and to enable the management team to hold its managers to account

Overall we found that there is a high awareness by NAO staff of the importance of a strong financial discipline and that all leaders and

the majority of managers and staff are engaged in the process of financial management. This is a solid baseline for the NAO to

continue with its programme of cultural change and to further develop the financial maturity of the organisation.

Confidential

4

1 Executive Summary

The Context For This Study

We present our findings in the format of the Financial Management Maturity Model - a tool designed and used by the NAO in the

delivery of the audits it undertakes. For each area of the matrix we provide commentary and a view on the level or levels that apply to

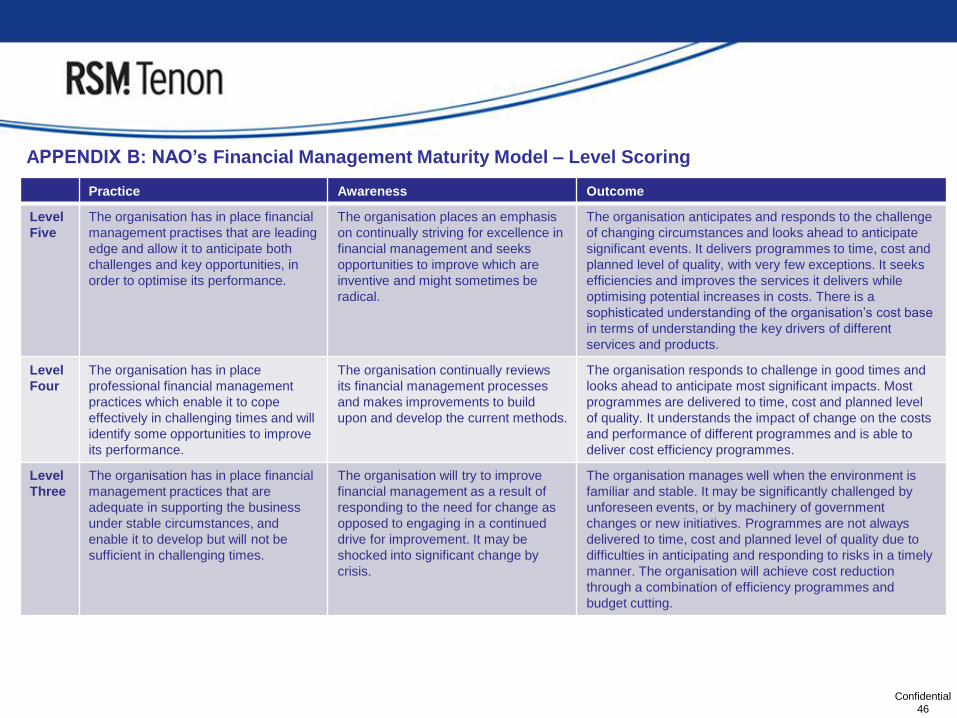

the NAO at this time. The five levels defined by the model are attached as Appendix A and summarised below.

The key context for this review is that the NAO is a professional services organisation. As such, its financial and managerial systems

are relatively simple. The Maturity Model is a flexible tool that allows the evaluation of the financial maturity of an organisation in the

specific context of that organisation.

Confidential

5

Level 3

Level 4

Level 2

Level 5

Level 1

Leading edge financial management in place that enables the organisation to anticipate challenges and optimize performance

Professional financial management in place that allows the organisation to cope in challenging times

Financial management processes are in place that are adequate in a stable environment

Basic financial management processes in place

Some financial management processes in place but they are inadequate

The Model sets out the definitions for each

level across a variety of dimensions and allows

the identification of a score of 1 to 5. The

evaluator needs to take into account the

context of that organisation. So for some of the

dimensions, for example, a score of 5 would

require real-time financial information. In

certain organisations this would be needed to

maintain financial control, but in others, and

the NAO is an example of this, it would be

inappropriate to have financial systems of that

complexity in operation.

So in the sections that follow we use the Model

to evaluate the performance of the NAO

against the sixteen dimensions. For each we

comment on whether there is room for

improvement given the needs of the NAO or

whether the NAO is at the most appropriate

level, given that it is a professional services

organisation.

Summary of Findings

Confidential

6

Aspiration Evidence Level

A culture of

collective

responsibility

The Board and the Leadership team are strongly aligned and focused on the delivery of a high

performing organisation. There is challenge, although the evidence of NED challenge could be

improved through the keeping of more detailed records of Board discussions 4 / 5

High quality

systems of internal

control, governance

and risk

management

Systems of internal control and governance are generally strong. The culture is one of caution and

we would judge the risk appetite to be relatively low. Whilst moving to a risk-taking culture would

not be appropriate to the type of organisation that the NAO is, the taking of informed risks that

seek to improve the performance of the organisation should be welcomed, so as to liberate a

culture of innovation.

The Risk Register is up-to-date and monitored regularly by the Board.

4

Strong financial

management

capability

The Board and leadership team has a great deal of experience, with high calibre people who have

worked in senior positions in public and private sectors. The skills and capabilities of managers

are improving but there is still a way to go to ensure that the desired culture of strong financial

management is shared by every member of the NAO. The finance function has the appropriate

blend of skills.

To attain an even higher score the NAO needs to improve the depth of skills in its managers. The

leadership given by the Board gives confidence that this is attainable.

4

Programmes for

training and

continuous

professional

development

Some budget managers and staff feel that there is a need to enhance training and support. In

striving for high utilisation and performance, it is possible that some of the needs and aspirations

of staff are not being fully met and there is room to improve in this area.

Senior management and the Board see the development of people as a key target.

3 / 4

Confidential

7

Aspiration Evidence Level

Financial planning

and monitoring

information is fully

integrated

The NAO has a clear approach to strategic planning and this is fully aligned to the financial

planning process. The financial planning horizon is three year and the focus is largely internal,

but given the context of the NAO this is appropriate.

Therefore, we judge that the NAO is at level 4 which is the highest level appropriate given the

context of the organisation.

4

Robust financial

planning systems

Systems are appropriate for the context of the NAO. The NAO is not a complex organisation

financially, and the systems provide the information appropriate to the need.

In terms of the maturity model, the NAO is at level 3 and that is appropriate to the type and

context of the organisation

3

Financial

information

supports the

business

Given the type of organisation that the NAO is, financial information is relatively straight forward

and levels 4 and 5 of the maturity model apply more to complex organisations with the potential

for significant financial volatility.

Hence the score of 3 represents an appropriate level for the NAO, since information systems are

fit for purpose.

3

Wide

understanding of

expenditure and

cost drivers

The cost drivers of the NAO are relatively straightforward. At a Board level there is a high level of

understanding of these drivers. At a local level, there is a sizeable majority where there is a good

understanding, but a significant minority who stated that they do not understand the expenditure

and cost drivers.

Through the ongoing work to improve financial awareness, the NAO will improve its rating in this

area.

2 / 3

Confidential

8

Aspiration Evidence Level

Wide

understanding of

income streams

and pricing

The Board and Leadership Team understand the relationship between income and costs and the

reports enable this to be monitored and tracked. The survey information shows that whilst the

majority of people receive information, understand the position and what is expected of them and

feel listened to, there is still a sizeable minority who do not.

In more complex organisations there would need to be a more sophisticated understanding of

future income trends and the factors influencing that income, however in the context of the NAO

the relationship is relatively simple and the reports are appropriate to that relationship.

3

Costs and benefits

of investments are

evaluated and

understood

The NAO is a relatively straight forward organisation. The majority of the costs are staff and so

financial management is about achieving the right balance of staff, skills, experience and

therefore cost, to meet the needs of the audits being delivered.

Skills in the appraisal of capital projects is therefore less crucial, however improving the skills of

the managers in this area would help their general approach to financial management and the

adoption of best practice techniques

2 / 3

Financial

information is of a

high quality,

accurate and timely

The general level of awareness of budgets and the need for good financial management is

strong. The Board and the Leadership team are clear on the importance of this task and the

information they receive appears to be of a good quality, accurate and timely.

There would be little gained by moving to real-time information as the current information is

appropriate to the context of the organisation.

4

Financial and non-

financial indicators

are appropriate

There is good use of financial and other information to manage the business. The Board and

Leadership team consider other matters, such as enablers to the running of the business (time

sheet completion, data capture) and follow up on non-compliance. 4

Confidential

9

Aspiration Evidence Level

High quality

financial

management and

operational

systems in place

Financial information is fit for purpose. The drill-down capability and the skills of managers to

interrogate information could be enhanced further - the data warehouse under development will

offer users the ability to access the information they need. These are matters that need to be

taken forward as part of the organisational training programme.

3 / 4

Reports are

tailored to

individual needs

Reports are generally suitable for the purpose intended. However, as the maturity of the

organisation develops, and as the demands for financial information increase in line with the

pressures flowing from cost reduction, there is a need to improve the sophistication and

“usability” of financial reporting, for example, to increase the level of predictive reporting.

This will be about improving skills in finance (training users and designing new standard reports)

and in users developing the capability to better interrogate information and write their own

reports.

3

Reports are timely Information is timely in the context of the NAO. Real time information and weekly information

would be unnecessary and costly. Controlling costs is largely about the payroll and so the key is

to ensure that the right balance of skills and costs are recruited and retained to enable the

delivery of high quality audits within budget. Complex financial systems are not required for this

task.

So the assessment of level 3 is appropriate for the NAO.

3

Reports are clear

and concise

We found the reports to be clear and concise. Through interviews and the questionnaire it was

apparent that the majority of users understood the information and received the reports they

received. The extent and requirement for external reporting is limited so a score of 4 is the most

appropriate score for the NAO. 4

Confidential

10

Key Conclusions

Our key conclusions are set out below. In bold type we repeat the objectives we were set by the Audit Committee and against

each we report our high level conclusions:

Establish whether the goals set out in the NAO strategy with regard to financial management are widely understood

by all managers with responsibility for the management of resources. We find that there is a good level of

understanding and that the NAO is doing well in this area. There is, however, still a sizeable minority of staff who say that

they do not get the information they need and do not appear to fully understand the NAO costing model. From the evidence

we reviewed, information is sent to all managers and staff and so we conclude that management need to identify the group

of managers who are struggling, and provide them with additional support to ensure that they are equipped to meet their

responsibilities.

Test the extent to which the principles of good financial management are consistently applied across all Areas of

the NAO. Applying the Maturity Model we found that financial management is consistently applied across the organisation.

Financial management is coordinated centrally and systems and processes are common throughout. However, evidence on

compliance with information requirements shows that some parts of the business comply to a greater extent than others.

Assess whether the information provided to senior management is appropriate, accurate and informative. There is

satisfaction from the Board that they receive the information they need. The approach is to empower the leadership team to

manage the business, and only intervene when things go wrong. There is a high level of confidence from the Board about

the leadership team. Generally the survey showed that there is satisfaction from managers and staff in the organisation

about the information they receive, although there are still some gaps to plug.

Assess whether the NAO is setting appropriate budgets, controlling costs, testing for value for money from

outsourcing and recovering costs through fees. The NAO has achieved financial targets in all the last three years

reviewed and at a corporate level all costs are recovered. Income is generated for c20% of costs thus reducing the gross

estimate requirement.

Advise on whether financial information is used appropriately to drive and inform strategic decision making across

the organisation. The NAO is not a complex organisation and so whilst the use of financial information is relatively

simplistic, the approach is appropriate to the context of the NAO. There is evidence that information is used by the Board, the

Leadership team and the organisation to manage its affairs. Improving the quality of data for the supporting KPIs will help the

NAO further improve in this area.

2 - Summary of Recommendations

Number Recommendation Management Response

Responsible Manager

and Timescale for

Implementation

Finance Governance and Leadership

1

Board minutes need to be more detailed to include questions posed

and responses received in order to provide evidence of appropriate

challenge and scrutiny.

We will ensure that Board minutes fully

reflect the nature of the discussion, the

specific challenges raised and the

responses, including details of any action

required.

Head of Governance

June 2012

2

An action log should be included within the explanatory notes to the

NAO Dashboard presented to the Board which shows progress

against previous actions to date.

Accepted. We will include an action log with

the Dashboard each month.

Head of Finance

June 2012

3 An action log should be created to support the risk report which details

progress against all actions and their due date.

The new format risk report introduced for the

2012-13 financial year will include a column

setting out actions in hand to address each

risk. Any further actions required will be

recorded in the formal actions log of the

Leadership Team and Board meetings.

Head of Governance

June 2012

4

All budget holders should be involved in the identification of risks

relevant to their area. All budget holders should be aware of the area‟s

risk register and how this links in to the corporate risk register.

Plans are in place to incorporate risk

assessments into performance reports

against area accountability statements.

Head of Governance

September 2012

5

A review should be undertaken to identify the type of financial

management training that budget holders and other staff need and,

subject to the availability of funds, additional training should be

provided.

Accepted. Finance and HR teams will

develop a formal, structured financial

management training programme.

Head of Finance

Head of Training

31 December 2012

Confidential

11

2 - Summary of Recommendations

Number Recommendation Management Response

Responsible Manager

and Timescale for

Implementation

Finance Governance and Leadership

6

Financial Management should be fully integrated into budget holder‟s

personal objectives and performance monitored to emphasize its

importance in the management of operations of the NAO.

Our 2012-13 Financial Management

Guidance clearly states the key

responsibilities of all staff and in particular,

principal budget holders, Directors and

Managers. We are currently reviewing our

staff appraisal guidance and will ensure that

this also includes guidance for appraising

performance in respect of financial

management.

Director of HR

31 December 2012

7

The evaluation form on the bid template should be further expanded

to include a version control with responses between finance and

budget holders being recorded up until the budget is approved or

errors have been resolved. This will provide a) transparency in the

budget setting process, b) accountability of the budget holder in that

they have been involved in the process, and c) a learning tool to

understand mistakes or to track significant changes to budgets.

The bid templates are locked down on a date

agreed with budget holders. This means that

only Finance are able to make changes

subsequently and we have used the

functionality within our current electronic data

records management system to record a

summary of changes made. It is however

possible to include a more detailed record and

we will ensure that we do this from the next

planning round. We will also review the

lessons learned to inform the following year‟s

planning process.

Head of Finance

November 2012

Confidential

12

Summary of Recommendations, continued

Number Recommendation Management Response

Responsible Manager

and Timescale for

Implementation

Financial Planning

8

Significant cash flow and balance sheet movements are unlikely,

however should these occur they should be reported to the Board in the

month that they occur.

We monitor cash flow movements very

closely each month and in particular

during the last two months of the financial

year. Any significant movements on the

balance sheet would be related to the

building which is revalued annually. We

will report any significant issues to the

Leadership Team and Board should they

arise.

Head of Finance

June 2012

Finance for Decision Making

9

The Board should consider whether the collection and review of

benchmarking information from other professional accountancy practices

would assist the on-going financial management of the NAO.

Accepted. We will ensure that this is

included in the Board Programme and

consider the possibility of starting this

process with benchmarking the NAO

against RSM Tenon.

Head of Governance

October 2012

10

A clear line of reporting and accountability should be defined in the terms

of reference between the Core Team and Project Board and improved

clarity in the objectives of the Project Board and the Core Team should

be agreed.

Accepted. We will review the terms of

reference and add further clarity in terms

of roles and responsibilities where

appropriate.

Head of Programme

Office

July 2012

Confidential

13

Summary of Recommendations, continued

Number Recommendation Management Response

Responsible Manager

and Timescale for

Implementation

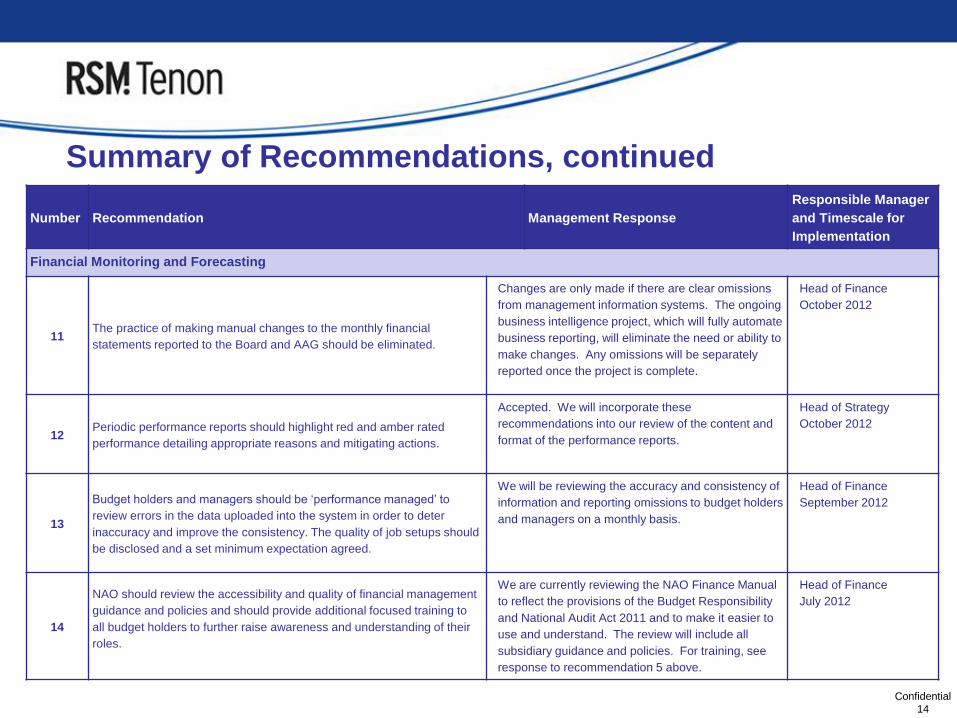

Financial Monitoring and Forecasting

11 The practice of making manual changes to the monthly financial

statements reported to the Board and AAG should be eliminated.

Changes are only made if there are clear omissions

from management information systems. The ongoing

business intelligence project, which will fully automate

business reporting, will eliminate the need or ability to

make changes. Any omissions will be separately

reported once the project is complete.

Head of Finance

October 2012

12 Periodic performance reports should highlight red and amber rated

performance detailing appropriate reasons and mitigating actions.

Accepted. We will incorporate these

recommendations into our review of the content and

format of the performance reports.

Head of Strategy

October 2012

13

Budget holders and managers should be „performance managed‟ to

review errors in the data uploaded into the system in order to deter

inaccuracy and improve the consistency. The quality of job setups should

be disclosed and a set minimum expectation agreed.

We will be reviewing the accuracy and consistency of

information and reporting omissions to budget holders

and managers on a monthly basis.

Head of Finance

September 2012

14

NAO should review the accessibility and quality of financial management

guidance and policies and should provide additional focused training to

all budget holders to further raise awareness and understanding of their

roles.

We are currently reviewing the NAO Finance Manual

to reflect the provisions of the Budget Responsibility

and National Audit Act 2011 and to make it easier to

use and understand. The review will include all

subsidiary guidance and policies. For training, see

response to recommendation 5 above.

Head of Finance

July 2012

Confidential

14

3.1 Background

The NAO Strategy for 2011-12 to 2013-14 sets out three key goals with regard to the development of a public sector service

improvement ethos: developing and applying the NAO‟s knowledge; increasing the influence of the NAO; and delivering high

performance.

In order to deliver against this strategy it is important that the financial management arrangements in place across the NAO are of

the highest standard. Financial management contributes to all aspects of the NAO Strategy, but particularly the delivery of high

performance. In the strategy document approved by the Public Accounts Commission in November 2010 it is stated that “…there

is still much to do to create the dynamic, high-performing organisation that would add maximum value to our clients and to

Parliament. We must continue to reduce our costs, and we propose to cut these by a further 15 percent of the coming three years”.

This ambition will only be achieved with a strong culture of financial management, and with high quality financial information

informing decision making.

This Value For Money review assesses the current situation with regard to the provision and use of financial management

information and makes practical suggestions to management on how to improve both the quality of the information and the way it

is used by the Board, Committees and management. As part of this review consideration is given to the extent to which the NAO is

budgeting effectively and controlling its costs. At a high level, the review tests whether the NAO is recovering all costs.

To make this assessment and to allow the development of helpful, practical recommendations, the work approaches the task both

from the perspective of the quality and timeliness of the financial information provided and the extent to which this is used

appropriately by management.

Confidential

15

3 – Scope & Approach

In undertaking this review we have adopted the principles of NAO‟s financial management maturity model. Our evidence

emanated from three key sources:

Structured interviews with key people such as Board members, Non-Executives, senior managers, finance staff, management

information systems staff, Internal Audit, Human Resources (Training Lead), Head of Programme Office & Enterprise Architect

and Head of Strategy.

Review of key documents including board finance reports, board minutes, budgeting and forecasting working papers, project

documentation, management accounts, annual accounts, performance reporting, risk reports, internal audit reports, strategic

planning documents and the finance manual.

We issued web-enabled questionnaires to three groups of employees, all budget holders, finance staff and remaining

employees excluding trainees. A 100% response rate was received from finance staff, 49% of all budget holders responded (18

out of 37) and 45% of all employees (266 responses from c600 employees, excluding trainees, finance staff and budget

holders). (NB. From here on reference to „all employees‟ questionnaire results will mean all employees excluding trainees,

finance staff and budget holders).

Hence we have been able to collect some very rich data for this study. The results are shown in Pie Charts with data from all staff

in purple, data from Budget Managers in lighter blue and data from Finance Staff in darker blue.

This information is reported after applying the Financial Management Maturity Model, in five key sections:

Financial governance and leadership;

Financial Planning;

Finance for Decision-Making;

Financial Monitoring and Forecasting; and

Financial and Performance Reporting.

Confidential

16

3.2 Approach

4.1 About the NAO

The National Audit Office assist Parliament in holding the Government to account for the way it utilises public money. They scrutinise

central government departments and bodies spending of public money and thereby safeguard the interest of taxpayers.

The NAO audit the financial statements of all government departments and a wide range of other public bodies, and conduct value for

money reviews, which look at how government projects, programmes and initiatives have been implemented and recommend how they

can improve.

The National Audit Office is headed by the Comptroller and Auditor General, an officer of the House of Commons appointed to carry out

the external audit of central government departments, executive agencies and other public bodies including public sector companies. The

Comptroller and Auditor General is wholly independent of government..

Funding and Distribution of Resources

The NAO receive their budget directly from Parliament through the approval of the Supply Estimate from the Public Accounts Commission

(PAC), a House of Commons Committee. The majority of this resource is used to employ c880 staff, outsource parts of the financial audit

and value for money work, and provide the infrastructure and support necessary to operate the organisation effectively.

The Definition of Financial Management

In our on-line questionnaire we asked respondents to define „Financial Management‟. There were a large number who took the time to

respond, and the results are captured in Appendix A. This analysis demonstrates that there is a wide range of opinion on the definitions of

financial management amongst those in the accountancy profession.

Confidential

17

4 – Background and Governance

Source: National Audit Office Annual Report 2010/11

4.2 Distribution of

resource

The diagram depicts how the

NAO resource was focused on

each area of government in the

year to 31st March 2011. Work

is distributed across different

areas which reflects:

The number of accounts

audited;

The relative amount of public

expenditure and revenue;

The complexity and risk

associated with each area;

and

Issues of particular interest

to PAC.

The size of each circle in the

diagram indicates the total cost

of NAO work in that area,

including financial audit, value

for money and performance

improvement work.

Confidential

18

Governance

FY11 was the first full year in which the NAO Board operated in its current form, following the agreement of improved government

arrangements by the PAC in 2009. The NAO Board is comprised of a majority of non-executive members and is supported by the Audit

Committee and Remuneration Committee. Both committees consist of solely non-executive members.

The Leadership Team support the Comptroller and Auditor General by providing executive management and governance to the

operations and delivery of the NAO. The Leadership Team is chaired by the Comptroller and Auditor General and attended by the Chief

Operating Officer and four Assistant Auditors General. The Leadership Team meet monthly and are supported by two committees, the

Operational Capability Committee and the Audit Practice and Quality Committee.

The Operational Capability Committee has delegated authority to deliver the appropriate resources, infrastructure and human capital to

achieve the NAO‟s business objectives. The Audit Practice and Quality Committee operate to review the comprehensiveness, reliability

and integrity of the framework supporting the technical quality of the NAO‟s audit work.

Confidential

19

5.1 NAO Board and Leadership Team

Confidential

20

Key Findings and Issues:

The past few years have been a period of significant challenge for the NAO. More recently, as austerity measures have started to bite,

resources have become far more heavily constrained. Consequently the NAO has been going through a cultural change, moving from an

organisation with a principal aim to deliver audits, to one where this objective has to be married with the need to reduce costs.

Our findings are that the NAO is responding well to this challenge. The Board stand full square behind the leadership team in the delivery of

the strategy and they back the desire to „practice what we preach‟ in utilising resources wisely. Through interviews with members of the

Board it was evident to us that there is a culture of collective responsibility and an appropriate level of delegation of financial management

responsibilities to the executive team.

As the NAO makes its transition from an organisation with relatively few financial challenges to one with real pressures, management are

trying to get greater ownership of budgets and responsibilities on the part of the Audit Directors. Our survey demonstrates significant

commitment and buy-in to this strategy by NAO staff, although there is still some way to go as evidenced (detailed in section 8.2 of this

report) by the poor response by some Audit Directors to information required for input into the financial management systems. As a result

of the greater independence of the Comptroller & Auditor General as compared to most comparable organisations, the Board dynamic is

different. That said, the Board appears to operate effectively and the NAO Board recognises that it has an assurance role, with the

leadership team being empowered to make decisions.

The leadership team are trying to respond positively to this agenda, for example, there was a need to speed up the audit process given

tighter audit timetable and the expected impact of the Olympics. As a result, a five point plan was created and applied which included zero

based budgets. This was overseen by the Leadership Team and reported to the NAO Board.

In addition, following from our discussions with members of the Board and Leadership Team, we note that both groups take their financial

management responsibilities seriously. The Board reviews financial performance and risk monthly, and the NEDs feel that they have the

right level of information. They recognise that in the financial sense, the NAO is not a complex business and therefore the level of

information and scrutiny is appropriate. The NAO strategy is reviewed annually and financial issues are included within this review.

5 – Financial Governance & Leadership

5.2 Board Meetings and Finance Board Papers

Confidential

21

Key Findings and Issues:

Finance reports are provided and discussed at each board meeting. From our review of these documents which were presented to the

Board and the Leadership Team, we note that they hold sufficient detail for appropriate challenge and scrutiny.

The NAO dashboard details actual performance against target for the agreed twenty-two key performance indicators (KPIs). The

explanatory notes support the NAO dashboard by providing reasons for red or amber rated KPIs and other issues and risks with supporting

actions. The documents used for reporting are easy to understand and follow and provide a snapshot and summary of the NAO‟s

performance against its strategic objectives. However, we identified that in some instances actions recorded in the explanatory notes

continued to be reported as an action in the following month (e.g. 2.7 Correspondence KPI). However there is no action log on the

explanatory notes to show progress to date on actions and this would be an important discipline to allow the capture of actions and a tool to

aid in the monitoring of compliance.

Through review of the minutes we note that the Board reviews the finance papers . The minutes are not very detailed in terms of the extent

of challenge, however NEDs were able to give tangible examples of challenges they had raised, and executives felt that challenge was

robust, but appropriately supportive. Such detailed challenge information was only recorded in the board minutes during the review of the

budget and estimate for the year. From review of the Leadership Team meeting minutes we note that appropriate discussion and challenge

is recorded of the NAO dashboard and explanatory notes. Hence we conclude that the Board minutes summarise the discussions and so

going forward it is important that fuller minutes are agreed that demonstrate the areas of challenge, the response by management and the

agreed resolutions.

We note that actions are recorded in the Board and Leadership Team minutes and progress is reviewed against these actions at the start of

each meeting.

Recommendations and Suggestions:

Board minutes need to be more detailed to include questions posed and responses received surrounding the NAO dashboard and

explanatory notes, in order to provide evidence of appropriate challenge and scrutiny.

An action log to be included within the explanatory notes which shows progress against previous actions to date.

5.3 Financial Information received by employees

Confidential

22

Key Findings and Issues:

A large amount of information is made available to budget

managers, including the finance manual, procedure notes for

completing budget and forecast templates, business plan

guidance setting out the responsibilities of managers, and there is

an established help line and web site with frequently asked

questions. Employees have access to the finance manual, are

notified of changes to procedures and all financial information is

published on the intranet.

However, as shown in the chart opposite, over a third said that

they never receive information and views were mixed and varied

from those who said that they do receive it, in terms of the

frequency.

In terms of Budget Managers, over 80% consider the information

they receive to be relevant. Importantly, a half recognised that the

challenge they receive on their financial performance is helpful or

very helpful, with only 6% finding it unhelpful. These are good

results for any organisation and indicate that the balance between

challenge and support is broadly appropriate.

Recommendations and Suggestions:

Management should identify those budget holders who state

that they do not receive financial information and updates from

the Board / Executive Team and explain to them the meaning

of the information that is routinely sent out.

5.4 Internal Controls and Risk Management

Confidential

23

Key Findings and Issues:

Policies and Procedures:

Our review found that policies and procedures are widely circulated to

Budget Managers and all employees through the intranet – see previous

section. We found that records are maintained of receipt and agreement to

key documents. The NAO Finance Manual covers the majority of the

financial policies and procedures which is available to all employees through

the intranet and subsequent procedures are provided by the Finance

Department as required. However, the vast majority of managers said that

they are aware of these policies – although it was concerning that 6% said

they were „unaware‟ of the financial management policies. Furthermore, only

half stated that they are made aware when polices are reviewed.

Over two thirds of managers felt that the NAO welcomes their challenge of

policies and 40% of all employees, a very good result indicating that most

staff feel able to speak out when they need to.

Recommendations and Suggestions:

Policies and Procedures:

Management should identify those employees and managers who state that

they are unaware of all their responsibilities and remind them of the policies

and procedures in place across the NAO that they have already

acknowledged and accepted.

Given that only half of managers felt that they are notified each time a

policy is updates, there is a need for management to consider the

communication concerning policy updates

5.4 Internal Controls and Risk Management

Confidential

24

Key Findings and Issues:

Risk Management:

Risk Management is recorded and reported through the organisational and individual area /

project risk register, and supporting monthly and detailed quarterly risk reports are

presented to the Board.

We reviewed the Risk Register and Risk Reports of the NAO and consider that they are

sufficiently detailed. They include risks surrounding external and business strategy . All risks

are RAG rated with supporting actions, including an identified risk owner. Although actions

are recorded on the documents, progress against these actions is not recorded and not

included as part of the report to the Leadership Team and the Board. An action log would

ensure that the appropriate focus is given to this task.

Our questionnaire results identified that 72% of budget holders were aware of the risk

management strategy, with 39% saying they were unaware of the business risks within the

risk register, and only 50% stating they did contribute to the identification of risks. 78%

stated that they were not aware of an area risk register.

Internal audit reports surrounding financial management as reported to the Audit Committee

during 2011 showed that adequate controls are in place to mitigate risks. The annual internal

audit reports for FY11 addressed that the NAO had „satisfactory risk management, control

and governance arrangements that provide reasonable, but not absolute assurance

regarding delivery of its strategic outcomes and business objectives.‟

Recommendations and Suggestions:

Risk Management:

An action log should be created to support the risk report which details progress against

all actions and their due date.

We recommend that all budget holders are involved in the identification of risks relevant

to their area and these are incorporated within the area and corporate risk register. All

budget holders should be aware of the area‟s risk register and how this links in to the

corporate risk register.

5.5 Finance Skills

Confidential

25

Key Findings and Issues:

The NAO has four non-executive members on the Board and a non-executive Chairman.

There is a high quota of qualified accountants and all have extensive financial, business or

legal backgrounds. Together this represents a high and impressive level of financial

expertise and a far higher proportion of qualified accountants than in most of your clients.

This is a strength in terms of financial management, but could be seen as a problem if this

resulted in the Board wanting to get into too much detail or spending too much time on

financial matters, at the expense of other items on the agenda. However we found that the

approach is a sensible one of empowering the executives to manage the finances of the

organisation, whilst reserving the right to intervene on matters by exception, where this

would be necessary.

The financial management team of the NAO consists of nine members of staff covering c852

employees, thus one member of finance staff for every c94 employees. 63% of the financial

management team of the NAO hold professional qualifications. The financial management

team have a background in audit and come through from the audit department of the NAO

either on secondment of transfer and therefore a fully sound in the requirements of financial

management.

83% of budget managers hold professional qualification, with two thirds of Budget Managers

said that they are „extremely‟ or „very‟ confident in dealing with financial information,

indicating that the majority have had the support and training they need to do the job. Only

6% said that they were only a „little comfortable‟ and so it is this minority that management

needs to focus on to improve their skills and confidence.

In our view the financial management team and majority of the budget managers have the

capabilities and skills required to undertake their financial management responsibilities.

5.6 Financial Management Training

Confidential

26

Key Findings and Issues:

Financial Management training is provided to all staff as part of their induction

course. In addition, financial management seminars are held and financial system

training is also provided, although only circa a third of directors and managers

have attended the financial management seminars to date. Frequently asked

questions are published on the intranet and updated following seminars. A recent

new approach to provide training on financial systems has been adopted whereby

„champions‟ are created across the NAO and training is provided to these people

to cascade the information across their areas. This is a positive initiative and

management should be encouraged to press on with its implementation.

In addition, there are several personal development courses (including some on

financial management) available through the intranet provided by the Human

Resources (HR) team to which employees can book themselves on to. External

training can be attended following the approval of the employee‟s line manager

and HR. Further qualifications can also be gained through presentation of a

business case to the HR team who assess the need for the qualification and

authorise the training with the employee‟s line manager.

There are more than half the managers who have not received training on

financial management in the past year – although there were opportunities for

them to do so. Half say they want some training. More concerning, only a third say

that financial management is properly integrated into their personal performance

plan and this is a matter that does need attention.

The NAO financial management team are either qualified accountants or

undertaking their accountancy exams. The qualified accountants attended

courses based on the need, which is assessed by the Head of Finance and

authorised accordingly. In addition, the financial management team have access

to the general staff personal development courses as mentioned above.

5.6 Financial Management Training

Confidential

27

Key Findings and Issues continued:

54% of employees felt that the NAO creates opportunities and

incentives to drive continuous improvement. Responses showed that

all in all there was an appreciation of the NAO‟s drive for better and

more efficient working processes through review and assessment of

work completed. It was felt that to enable this goal to be met the NAO

should seek to provide sufficient training courses and seminars for its

staff. 75% of finance felt that they are supported by the NAO to obtain

further financial management qualifications.

The NAO already provides extensive training and in a cash

constrained environment, there are limitations to how far this can be

expanded. Our view is that training to ensure core skills is already in

place and therefore additional support should be considered and then

provided if resources allow. It is vital that financial management

responsibilities are fully articulated and monitored through personal

performance targets.

Recommendations and Suggestions:

A review should be undertaken to identify the type of financial

management training that budget holders require and, subject to

the availability of funds, management should seek to address that

need.

Financial Management should be fully integrated into budget

holder‟s personal performance objectives to emphasize its

importance in the management of operations of the NAO.

• The overall strategy which includes the inbuilt 15% savings across the 3 years

• The strategic plan is developed through the use of financial models with a starting point of last years performance and incorporating adjustments.

• Reviewed by the Head of Finance, Director General of Finance, Leadership Team and the Board.

3 Year Strategy,

Approved by TPAC in December

• The estimate identified in the strategy is confirmed through a detailed planning process.

• Bids from each principal budget holder are gathered through their completion of a standard template, identifying the budget they require for the year. All bids are reviewed and scrutinised and re-iterated until a final version is agreed.

• All bids are automatically consolidated and reviewed in line with the strategy and estimate to ensure they are in line with expectations. A Corporate Delivery Budget is approved on this basis.

Financial Year Estimate & Budgets

Approved by TPAC in March

• The Corporate Delivery Budget is input in RMS by 30th April following approval at the end of March.

Input of Corporate Delivery Budget

April

• The Corporate Delivery Budget is revisited in September. All principal budget holders are required to input budget information directly into RMS.

• This is reviewed and scrutinised by the finance staff until a final forecast is agreed.

• All forecasts are presented for approval by the Board and consolidated to create a Revised Corporate Delivery Budget, in line with the approved estimate. This is then presented to the Board for approval.

Income and Expenditure Review

September / December

6.1 The budget setting and financial planning process

Confidential

28

6 – Financial Planning

6.2 Strategic & Business Planning Process

Confidential

29

Key Findings and Issues:

The NAO‟s strategy focuses on three strategic objectives:

1. Developing and applying our knowledge;

2. Increasing our influence; and

3. Delivering high performance.

All surrounding the requirement to improve public service.

The Business Plan supports the strategy by detailing the use of the workforce, technology,

infrastructure, including financials to achieve the corporate objectives.

Each area is required to complete an Area Accountability Statement (AAS) which briefly outlines their overall budget, which is based on the

government department family audited and other cross cutting audit areas. The AAS supports the business plan by defining the results each

area is aiming for, and the specific outputs to be delivered. They include high level income and expenditure budgets on a per audit / value for

money review basis. There are also sufficient non-financial objectives including stakeholder analysis.

We note that training and guidance is provided to all budget holders on the process of how to complete templates and a financial

management team helpline is available for all to access. As shown in the diagram on the previous page, this process takes place over

several months, and yet 11% of Budget Managers thought it occurred within two months of the start of the year.

In September a review of the budget is undertaken to identify forecast income and expenditure and the budget is revised as a result.

Our questionnaire responses show that all budget holders confirm that they are involved in the budget setting process. 78% of budget

holders state they are able to scrutinise their budget before final board agreement, with 17% stating they are not. In addition, 89% of

budget holders believe the budget setting process begins over 3 months before the following financial year, yet there are still 5% who

believe it begins only 2 – 3 weeks before the following financial year.

75% of finance staff stated the budget setting process is reviewed annually, with 13% stating when required so.

Recommendations and Suggestions:

Management should identify the minority of Budget Holders who state that they are unaware of the budget setting process and

timetable and ensure that they are aware of their responsibilities.

6.3 Systems of financial planning

Confidential

30

Recommendations and Suggestions:

The evaluation form on the bid templates is further expanded to

include a version control with responses between finance and

budget holders being recorded up until the budget is approved or

errors have been resolved. This will provide a) transparency in

the budget setting process, b) accountability of the budget holder

in that they have been involved in the process, and c) a learning

tool to understand mistakes or to track significant changes to

budgets.

Key Findings and Issues:

From our review of the financial planning documentation known as the budget setting process we noted the following issues:

The budget values are said to always round to the nearest £‟000 with a £500 de-minimis. This has the risk of missing budget if there a

significant number of individual expenditure items within this margin.

The briefing document indicates that the budgets are not agreed until 30th April yet from our discussions we are aware that it is agreed by

31st March and uploaded on the system by 30th April, therefore revision of the document for clarity is required.

The bid template that budget holders are required to complete is well structured as it allows the assessment of a budget bid by an Area.

Evidence viewed shows scrutiny of the bids is undertaken and responses are recorded through the evaluation form. We note that there is

also feedback and clarification of the information e.g. loss making bids and increases in costs over previous years. This demonstrates

involvement of service delivery staff in budget setting and a two-way process. However, there is no record of any responses or the outcomes

surrounding scrutiny and feedback of bids to understand how the issues were resolved.

Our questionnaire responses show that all budget holders are aware of their financial forecasts and are involved in setting their forecasts. In

addition, all budget holders say that they notify finance when they are underspent in order for funds to be allocated elsewhere, however our

responses from finance staff showed that 25% felt that this was the case always, whereas 63% believed they were only notified sometimes.

6.4 Coverage of financial planning

Confidential

31

Key Findings and Issues:

All forecasts are purely Income and Expenditure based, but as part of the Estimate, the balance sheet and cash flow forecast is

produced for each year. This is reviewed by the Director of Finance and Head of Finance. The Leadership Team view the finalised

estimate. The final Estimate goes to the Board for approval and the minutes record that this is approved.

A monthly cash flow forecast has been recently introduced. This builds in the capital expenditure that is based on the annual estimate

and approval process, however this was still in its early stages of development and is work in progress.

The monthly Board report does not include this cash flow or balance sheet information. Whilst it is appropriate that these matters are

dealt with by the executive, there should be a formal process so that the full Board is notified of any major swings or issues to the

balance sheet or the cash flow. We recommend that this is achieved by way of an exception report, rather than cluttering up the

financial report with additional appendices that will show only minor movements, month-to-month. However, it is good practice for the

Board to review both cash flow and balance sheet periodically, as this process of challenge can be helpful to ensure that management

continues to track movements of a regular basis.

Recommendations and Suggestions:

Significant cash flow and balance sheet movements should be included and reported as exceptions as part of the monthly Board

report.

7.1 Understanding of Income Expenditure

Confidential

32

Key Findings and Issues:

The Assistant Auditors General (AAG) reports that are provided to each AAG on a monthly basis

detail summarised information on expenditure. This is provided by finance staff for review and

decision making purposes. These reports consist of a Business Report and supporting Annexes.

They comprise the following detail:

A portfolio NAO dashboard per the KPIs of the NAO, which compares NAO overall performance

to that of the AAG portfolio, indicating differences in RAG ratings.

Provides detail on target versus actual performance for all areas of work.

The annexes to the business report provide detailed listings of transactions which link into the

summary data within the business reports.

The NAO dashboard and explanatory notes are updated monthly, to show Income and Expenditure

actual versus target as part of the NAO KPIs performance review.

Through interviews we were satisfied that the leadership team and the Board understand the

expenditure drivers of the NAO. However, less than half of Budget Managers said that they

understand the costing methods used. Whilst the majority of managers were confident that all

staffing costs were fully reflected in their budgets, 11% were not. Given the information that we

have examined that is provided to managers, this is a surprising result and so management needs

to establish whether this is because there is a lack of understanding of how to reconcile staffing

levels in the budget or because there is a concern that staffing costs are omitted.

Recommendations and Suggestions:

Management should identify those budget holders who state they are unaware of costing

methods used by the NAO and support them to ensure that they are equipped to fulfill their

responsibilities.

Management should identify those budget holders who state they are unsure whether their

budgets include all staff costs and complete a reconciliation to ensure that all staff costs are

included in the correct budget

7 – Finance for Decision Making

7.1 Understanding of Income and Expenditure, continued

Confidential

33

Key Findings and Issues:

As a resource driven organisation there are some areas of work where the NAO

generate income. In FY11 the NAO generated £20.2m income which was £0.7m

higher than the FY11 Estimate, and represented c21% of the gross estimate

resource (£96.1m).

Income along with expenditure as discussed in section 7.1 previously, is reported to

the Board on a monthly basis and the details are provided within the monthly AAG

reports.

Benchmarking is not regularly used in managing the business, although we accept

that this is more applicable to organisations operating in a competitive environment.

That said, the NAO has a lot in common with professional accountancy practices in

terms of levels of utilisation of staff, inputs to complete audits and staff pay levels,

and the Board should consider whether benchmarking information would be

beneficial in the financial management of the NAO going forward.

The NAO monitor their income against costs through their AAG reports and overall

monitoring is undertaking by the financial management team when they review the

information on the system and question the budget manager. High level review is

undertaken at leadership level through review of the NAO Business Reports.

Recommendations and Suggestions:

The Board should consider whether the collection and review of benchmarking

information from other professional accountancy practices would assist the on-

going financial management of the NAO

7.3 Investment Appraisal and Project Management Process

Key Findings and

Issues:

The NAO have a

Programme Office

(PO) which covers

internal change

improvement projects

that are primarily IT

based. We discussed

the process with the

Head of Programme

Office and Enterprise

Architecture which is

noted in the diagram

opposite:

Projects are identified as part of the annual business planning process, where opportunities are identified and project outlines are created.

Project proposals are then created which depict high level estimates of resources and solutions. These are collated together and a bid is placed for the budget to be provided to the

individual areas.

All project proposals are ranked by the PO using criteria set based on

strategic fit, improvement in services and internal efficiency, risks of

completion and other factors are also considered.

These ranked project proposals are then presented and discussed with Directors, where projects are then

prioritised, and the capacity to deliver the projects are reviewed.

Following an agreed ranking a Portfolio Deliverable Plan is created.

Each project in the Portfolio Deliverable Plan is assessed for feasibility to justify the business

case produced. The business case production is created by the project

managers with support of the business analyst of the PO.

The PO undertake a peer review of the business case using a standard

template of evaluation.

The final approval level of projects is based on the financial value of the

project over its lifetime. Director General of Finance approves

projects under £250k and above £250k is approved by the Chief

Operating Officer.

The PO effectively recommend projects to the Director General of

Finance and Chief Operating Officer for approval. Both of whom have the

support of the PO Core Team, Leadership Team and Operational Capability Committee to assist in

making the decision.

Where projects are non-compliance based then a post benefit analysis is

done on project closure.

Confidential

34

7.3 Investment Appraisal and Project Management Process

Confidential

35

Key Findings and Issues:

The PO have tailored the Prince2 Project Management methodology to fit the NAO.

This has involved the use of project lifecycles, standard gateway reviews and NAO

dashboard reporting on progress to date. The NAO dashboard reporting approach is

populated by the Head of Programme Office and Enterprise Architecture through the

collation of information from various sources. Through the collation of this data the

consolidated NAO dashboard report is produced monthly and reviewed by project

managers for accuracy before being presented to the Operational Capability

Committee (OCC) and the Programme Office Board (POB) who review progress and

deal with any issues.

We reviewed the PO terms of reference and noted the following issues:

It is unclear whether the Programme Core Team and Board deliver the projects of

work on the Programme Board for business change delivery.

There is no clear link between the POB and the Programme Core Team for

reporting lines and governance structure.

The Core Team‟s terms of reference do not set out clearly their objectives.

We reviewed the Programme Office consolidated NAO dashboard and noted that:

There is no split of budgets between capital investment and revenue expenditure,

to depict what has been capitalised.

There are no supporting data numbers to the bar charts in section 2 for

transparency of values.

The projects that are red or amber rated are not highlighted within the NAO

dashboard with their supporting mitigating actions.

We selected a sample of project documentation for review from the project portfolio

documentation and noted they were sufficiently detailed and provided detailed

information of expected project costs, and options appraisals. Our questionnaire

results show that a significant majority of budget holders were aware of the PO and

22% had utilised the PO to secure funding.

Recommendations and Suggestions:

Programme Office terms of reference:

A clear line of reporting and accountability should

be defined in the terms of reference between the

Core Team and Project Board and improved

clarity in the objectives of the Project Board and

the Core Team should be agreed

7.4 Outsourcing

Confidential

36

Key Findings and Issues:

As part of the work undertaken by the NAO some work has to be outsourced as required. The NAO outsource work to their framework

partners, but only those who have been assessed under the procurement policy and arrangements of the NAO. Framework partners are

chosen in line with the NAO‟s procurement policy which states the following:

“The NAO should seek innovation and value for money, including identifying cost reduction opportunities, in what and how

they buy, encouraging collaboration, including the use of public sector Framework Agreements where possible.”

The Central Procurement Team (CPT) is responsible for providing support and best practice advice on procurement activities, as follows:

Above £25,000 - CPT must be involved in the tender evaluation panel, management of the procurement exercise and all contact with

suppliers.

Below £25,000 – Advice should be sought from CPT on a case by case basis.

Buying decisions in the NAO are made jointly by business areas and procurement staff, and the CPT must confirm on the „Request for

Approval to Award Contract Form‟ that appropriate procurement strategies and processes, which include up to date professional

procurement practices, have been followed.

The NAO‟s Procurement Strategy details a robust tendering and approval process.

8.1 Financial Monitoring

Confidential

37

As already reported, financial

monitoring is exercised through a

monthly review of the NAO

Dashboard.

The tables opposite show the

Statement of Comprehensive Net

Expenditure for the last three years

and the Comparison of Outturn with

Estimate for FY11.

The NAO has managed within the

Estimate across this strategic

period.

Source: National Audit Office Annual Report 2010/11 & 2009/10

Statement of Comprehensive Net Expenditure

FY11 FY10 FY09

£000s £000s £000s

Administation Costs

Staff Costs 57,432 57,770 55,171

Other administrations costs 35,050 57,026 67,922

Gross administation costs 92,482 114,796 123,093

Operating Income (20,235) (19,896) (19,966)

Net Operating Cost 72,247 94,900 103,127

Other comprehensive expenditure

Net gain on revaluation of property, plant and equipment (3,261) (32,813)

Total comprehensive expenditure 68,986 62,087 103,127

Comparison of Outturn with Estimate FY11

Estimate Forecast Outturn

Saving

against

Estimate

Saving

against

Forecast

£000s £000s £000s £000s £000s

Gross Resource requirement 96,100 93,600 92,578 3,522 1,022

Income (19,500) (19,500) (19,500)

Net resource requirement 76,600 74,100 73,078 3,522 1,022

Capital Expenditure 1,430 1,430 1,345 85 85

Net Cash requirement 75,443 68,165 7,278

8 – Financial Monitoring and Forecasting

8.2 Quality, accuracy and timeliness of financial management and forecasting information

Confidential

38

Key Findings and Issues:

From discussions we were informed that producing the monthly financial monitoring reports (AAG Business Reports and Annexes and the NAO

dashboard) takes a working week . This is because reports cannot be created automatically from the system. Once data is downloaded from

the system this is then reconciled to confirm accuracy of the information to be reported. This data cleansing exercise takes time due incorrect

coding on the system, or not incorporating all costs of the job, or timesheets not being completed on time, etc. Therefore, data downloads are

manually adjusted following review before information can be consolidated and reports created. All reports are reviewed prior to submission.

We have concerns over these manual adjustments as this could lead to errors in reporting.

As a result of our discussions we obtained reports from the NAO identifying the level of errors and non-compliance by managers in recording

complete information on the RMS. The goal is to reduce manual data cleansing and increase the accuracy of all information extracted from

RMS system to facilitate the appropriate analysis.

We analysed the data on the total number of jobs with missing information (either target dates, budget data or income quotes) across the

months and then split by area. This shows the following:

Jobs with missing information range from 14% - 25% of total jobs of the NAO.

There was a peak in missing information in December 2011 and January 2012, although this has subsequently dropped in February 2012.

The highest area where the proportion of jobs are missing information are WGA , VFM and Performance Improvement. The Other Financial

Audit Outputs significantly increased the proportion of missing information from May 2011 with 8.8% to February 2011 to 61.1

8.2 Quality, accuracy and timeliness of financial management and forecasting information

Confidential

39

Key Findings and Issues:

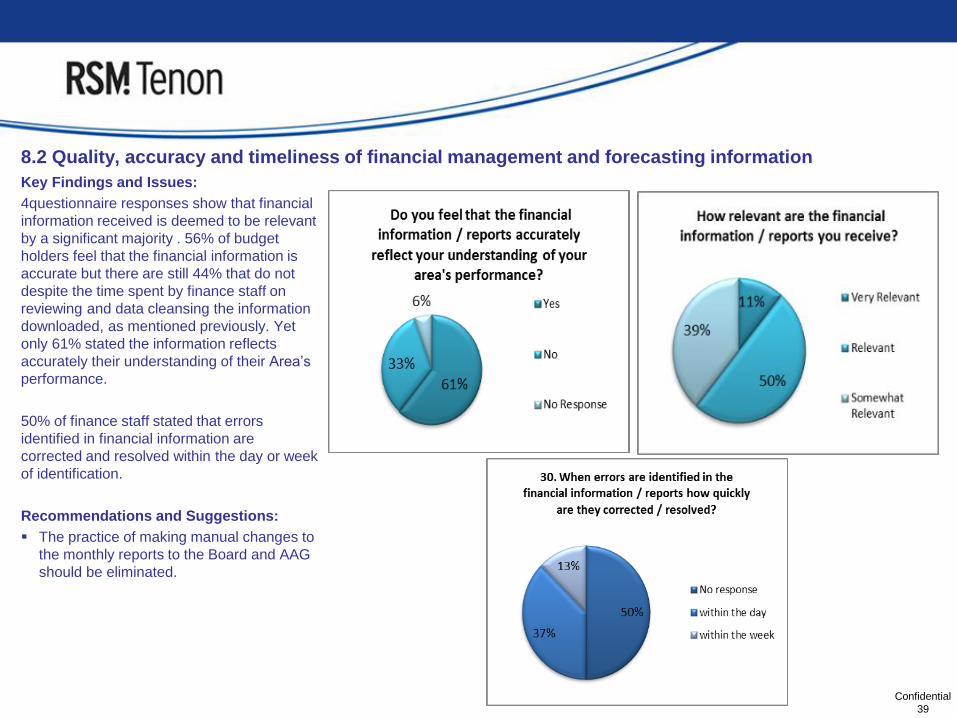

4questionnaire responses show that financial

information received is deemed to be relevant

by a significant majority . 56% of budget

holders feel that the financial information is

accurate but there are still 44% that do not

despite the time spent by finance staff on

reviewing and data cleansing the information

downloaded, as mentioned previously. Yet

only 61% stated the information reflects

accurately their understanding of their Area‟s

performance.

50% of finance staff stated that errors

identified in financial information are

corrected and resolved within the day or week

of identification.

Recommendations and Suggestions:

The practice of making manual changes to

the monthly reports to the Board and AAG

should be eliminated.

8.3 Coverage of financial and non-financial indicators of performance

Confidential

40

Key Findings and Issues:

Performance against the six strategic performance

indicators are reported to the Board each quarter.

These are detailed in the opposite table with the

latest reported position.

On each Area Accountability Statement (AAS), key

performance indicators are identified which are

reviewed and challenged by the AAG responsible.

Every four months a review of the performance

against the Area KPIs is undertaken and a report

compiled by the AAG for their portfolio, which they

self-assess and RAG rate. This self-assessment

combined with the information in the table opposite

is used by the Head of Strategy to populate and

create the Performance Report presented to the

Board.

From this, it is noted that the majority of the

information used to report on is qualitative rather

than a mixture of qualitative and quantitative. Given

the nature of the audits, we conclude that this is an

appropriate approach.

Source: National

Audit Office

Performance

Report Sept 11 –

Nov 11

8.3 Coverage of financial and non-financial indicators of performance

Confidential

41

Key Findings and Issues

The performance reports detail qualitative findings supported by

RAG rated status pie charts for each KPI. However the RAG pie

charts do not summarise what criteria are being measured to

assess the performance measures. In addition, red and amber

rated performance is not discussed within the reports to highlight

reasons and mitigating actions.

This self-assessment information is useful, however there is a

concern that there is no independent review, and perhaps an

external assessment on an annual basis would strengthen the

analysis.

83% of budget holders have their Area‟s performance assessed

against financial and non-financial criteria. The vast majority

(89%) believe that the non-financial criteria used to measure

performance are appropriate.

Recommendations and Suggestions:

Periodic performance reports should highlight red and amber

rated performance detailing appropriate reasons and

mitigating actions.

8.4 Financial management and operational performance management systems

Confidential

42

Key Findings and Issues

There are three different systems used for financial management as follows:

RMS – logs timesheet and expenses information by job, for which each Principal Budget Holder and manager are responsible to

review.

PARIS – is the NAO‟s finance system.

RAS – provides level of staff utilisation analysis which is undertaken by the Human Resources department.

All the financial reports prepared utilise information from the above sources. All reports created are saved on to the KeyStone system of

the NAO to which every employee has access to view. In addition, all NAO employees are able to view standard reports from RMS in

order to review job performance which they can run themselves. The finance team provide data analysis following the data cleansing. All

reports prepared by finance are emailed to their users as they are non-standard reports and cannot be automatically downloaded by users

themselves due to the manual adjustments undertaken, as noted in section 8.2, if this was corrected then the reports produced by the

system would be more robust.