NARTD | The Past, Present and...

48

NARTD NARTD | The Past, Present and Future May 19 th 2008 Steve Miranda Senior Manager | The Nielsen Compan Senior Manager | The Nielsen Company

Transcript of NARTD | The Past, Present and...

NARTDNARTD | The Past, Present and Future

May 19th 2008

Steve MirandaSenior Manager | The Nielsen CompanSenior Manager | The Nielsen Company

Agenda

• The general Grocery environment.

• Looking back at the Grocery beverage market over the last 10 years.

• How has the market changed?• What brands have come and gone?• What trends have emerged?

• The current retail environment.• Channel and Segment shares.• What drives consumer purchase?p

• Looking ahead.• How will mega trends impact beverages?

Information SourcesInformation Sources

• Nielsen | ScanTrack– Measures scan sales through all supermarkets and grocery stores (warehouse

withdrawals for independents)

• Nielsen | Homescan Consumer Panel– Captures all in-home consumption of packaged and fresh grocery products

purchased from all supermarketsp p– 10,000 representative households across metro and regional Australia– Understanding consumer behaviour driving why the market behaves as it does.

• Nielsen Shopper Trends Report 2008– Online study, March 2008

• Nielsen Omnibus

Grocery environmentyOverall growth slips in 2007, NPD drives category growth

2007 Defined Grocery growth slightly behind 2006.2007 Defined Grocery growth slightly behind 2006.

Growth Rate Over Time For Total Defined GroceryGrowth Rate Over Time For Total Defined GroceryDefined Packaged Grocery - % value change vs YA - Australia

8.9 8.8

10.02001 2002 2003 2004 2005 2006 2007

6.3

7.7

6.4

7.9

6.86.6

6.9

6.3

6.8

6.2

7.3

6 0

6.7

6.1

7.0

6.46.16 0

6.4

8.0

6.2

7.17.4

8

6.86.76.8

6.2 6.1

6.9

8.0

s YA

5.1

5.6

3.9

5.6

5.0

6.0 6.0

4.7

5.65.85.45.3

5.15.5

5.25.24.8

4.44.7

4.54.8

3.6

4.54.7

5.2

4.54.64.8

4.2

4.8

5.7

4.4

5.5

4.7

4.03.83.6

5.7

5.0

4.0 3.8

5.75.8

5.14.8

3 4

5.24.84.8

3.84.0

4.0

6.0

Valu

e C

hang

e vs

2.62.4

2.7

3.2

2.72.5 2.4

3.4

2.0

% V

Average growth rate of 5.5% in 2006 d li i t 4 6% i 2007

0.4

0.0

2006 declining to 4.6% in 2007

Source: Nielsen ScanTrack

However strong year on year growth for Confec / However strong year on year growth for Confec / Beverages is ahead of the market.Beverages is ahead of the market.

Australia - Packaged Grocery % value growth vs. YADepartment Summary

8

MAT TO 02/07/2006MAT TO 01/07/2007

6.7

6 5 9

8

7.1 7 7

4.6 4.4

5.3

3.8

5.1

4.23 6

5.9

4.3

3.23.6

2.5 2.4

PACKAGEDGROCERY

DRY GROCERY HEALTH/BEAUTY PETFOOD/ACCESSORIES

HOUSEHOLD DAIRY CASE CONFEC/DRINKS FROZEN FOODS TOBACCOPRODUCTS

Source: Nielsen ScanTrack

Total Packaged Grocery CPI has rebounded after a Total Packaged Grocery CPI has rebounded after a steep declined in late 2007.steep declined in late 2007.

CPI in Packaged Groceries & LiquorCPI in Packaged Groceries & LiquorBased on a fixed basket of 28,750 grocery and 12,500 liquor products, measured through national supermarkets, liquor

stores, hotels and bottleshops (source: ScanTrack | Grocery & ScanTrack | Liquor)

6.0

4.0

5.0

YA

1 0

2.0

3.0

% c

hang

e vs

-1.0

0.0

1.0

Total Packaged Grocery Total Packaged Grocery excl Tobacco Total Packaged Liquor

source: ScanTrack | Grocery & ScanTrack | Liquor)

This was driven by aggressive price discounting by This was driven by aggressive price discounting by the retailers within Beverages.the retailers within Beverages.

CPI i F d & BCPI in Food & BeveragesBased on a fixed basket of food and beverage products, measured through national supermarkets and grocery stores (source:

ACNielsen ScanTrack)

8 0

9.0

5.0

6.0

7.0

8.0

YA

2.0

3.0

4.0

5.0

% c

hang

e vs

Y

-1.0

0.0

1.0

%

-2.0

Chilled Dairy Only Frozen Only Drinks & Snacks Dry Grocery & Bakery

source: ScanTrack | Grocery & ScanTrack | Liquor)

CSD’s and Mixers are ranked #2 in the list of CSD’s and Mixers are ranked #2 in the list of categories that contribute to dollar Grocery growth.categories that contribute to dollar Grocery growth.

Top 10 Categories with highest dollar growth contributionTop 10 Categories with highest dollar growth contributionAustralia MAT to 01/07/2007 vs YA - based on dollar growth in $m

$298.5CIGARETTES

$134.7

$107.7

SOFT DRINKS/MIXERS

VALUE ADDED PRODUCE

$99.1

$96.5

CHEESE

ICE CREAM

$ th t ib ti$67.4

$65.8

COFFEE INSTANT

CHOCOLATECONFECTIONERY

$m growth contribution

$60.9

$60.2

FROZEN MEALS

SMALLGOODS

$59.7SNACK FOODS

Source: Nielsen ScanTrack

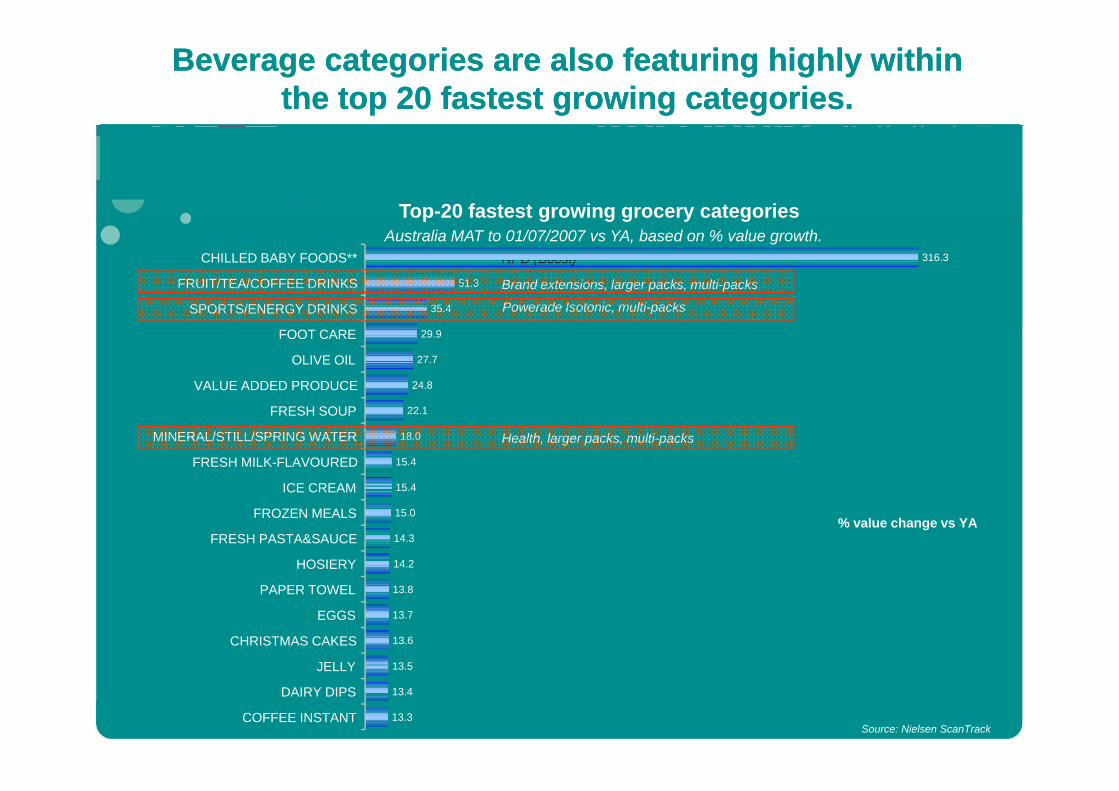

Beverage categories are also featuring highly within Beverage categories are also featuring highly within the top 20 fastest growing categories. the top 20 fastest growing categories.

Top-20 fastest growing grocery categories

NPD (Boost)

Brand extensions, larger packs, multi-packs

Powerade Isotonic multi packs

Top 20 fastest growing grocery categoriesAustralia MAT to 01/07/2007 vs YA, based on % value growth.

316.3

51.3

35 4

CHILLED BABY FOODS**

FRUIT/TEA/COFFEE DRINKS

SPORTS/ENERGY DRINKS Powerade Isotonic, multi-packs35.4

29.9

27.7

24.8

SPORTS/ENERGY DRINKS

FOOT CARE

OLIVE OIL

VALUE ADDED PRODUCE

Health, larger packs, multi-packs

22.1

18.0

15.4

15 4

FRESH SOUP

MINERAL/STILL/SPRING WATER

FRESH MILK-FLAVOURED

ICE CREAM 15.4

15.0

14.3

14.2

ICE CREAM

FROZEN MEALS

FRESH PASTA&SAUCE

HOSIERY

% value change vs YA

13.8

13.7

13.6

13 5

PAPER TOWEL

EGGS

CHRISTMAS CAKES

JELLY 13.5

13.4

13.3

JELLY

DAIRY DIPS

COFFEE INSTANTSource: Nielsen ScanTrack

NARTD over the last decadeNARTD over the last decadeSegment changes, top brands and private label

Evolution of beveragesTimeline of segment changes

34%

77%

597%

76.1pp

77%

69.1pp

1997 20072000 2002 2004Source: Nielsen ScanTrack

Carbonates share loss equates to 136.7M Litres in 2007.

This shift has resulted in emerging segments like This shift has resulted in emerging segments like Water, Energy and Sports gaining share.Water, Energy and Sports gaining share.

National Grocery | Trended Volume Share of NARTD Volume = Litres (000's)

6 4 8 28.1 8.7 9.4 10.525.0

30.0

35.0

1.0 0.9 0.9 0.90.9 0.9 0.9

1.1 1.3 1.7 1.84.0 5.3 5.9 6.1

6.4 7.4 8.2

15.0

20.0

25.0

18.7 18.3 18.2 18.4 19.7 18.5 18.1 19.4 18.7 18.4 16.9

0 0

5.0

10.0

0.0YEAR1997

YEAR1998

YEAR1999

YEAR2000

YEAR2001

YEAR2002

YEAR2003

YEAR2004

YEAR2005

YEAR2006

YEAR2007

TOTAL ENERGY DRINKS TOTAL FRUIT JUICE & DRINK TOTAL SPORTS DRINKS

TOTAL STILL WATER NON PURE TOTAL STILL WATER PURE TOTAL TEASource: Nielsen ScanTrack

The Top 10 Brands1997 2007 b d V l1997 vs. 2007 based on Value

1 16 6

28

27 7

83 8 3

49

8

94

5 5

4

10

9

10

NEWNEW

NEWNEW5 510 10Source: Nielsen ScanTrack

The Top 10 Brands1997 2007 b d V l1997 vs. 2007 based on Volume

1 16 6

28

27 7

8

NEWNEW

3 8

93

4

8

9NEWNEW

4

5 10

4

5

9

10 NEWNEW5 10 5 10Source: Nielsen ScanTrack

NEWNEW

PL growth has consistently been ahead of the Total PL growth has consistently been ahead of the Total Market, accelerating in recent periods.Market, accelerating in recent periods.

Trended Growth Rate | Total Grocery vs. PL | Value % Chg vs. YA

14.0

16.0

18.0

8.0

10.0

12.0

2.0

4.0

6.0

0.04W/E

14/05/20064W/E

06/08/20064W/E

29/10/20064W/E

21/01/20074W/E

15/04/20074W/E

08/07/20074W/E

30/09/20074W/E

23/12/20074W/E

16/03/2008

Source: Nielsen ScanTrack

TOTAL DEF PACKAGED GROCERY (EXC TOBACCO) TOTAL PRIVATE LABEL

Along with this, consumer use and acceptance of PL Along with this, consumer use and acceptance of PL is also increasing year on year.is also increasing year on year.

Private Label Brands bought in P4W 28

2428

21

Coles

Woolworths Select

Non- ents

23

20

16

10

24

19

You'll Love Coles

Homebrand

Woolworths

Buyers of Private Label in

P4W

Non-Buyers of

Private Label16% f r

espo

nd

13

126

1419

19Farmland

Coles $mart Buys

Bl k & G ldP4W84%

% o

f 12

5

5

13

8

8

Black & Gold

IGA

Persona4

4

4

10

7

7

Bi-Lo

Reliance

Savings

2007

2006

Ref: Q59bBase: All Supermarket / Hypermarket shoppers 2007( n=993), 2006(n=994)

Source: Shopper Trends 2008

7g 2006

Share gains have been driven through consumers Share gains have been driven through consumers spending more on PL. Up $14.90c per household in the spending more on PL. Up $14.90c per household in the

l t t QTR YAl t t QTR YAlatest QTR vs. YA.latest QTR vs. YA.

National PL KPI’s and Market Share Trend

National Supermarkets

$128.70 $125.10

$137.50$146.70 $145.70

$135.80$143.50

$148.20 $151.50

120

140

160

20

25

99.4 99.2 99 99.1 99.1 99.2 99.1 99.1 99.280

10015

18.4 19 19.8 19.4 19.6 19.9 20.4 20.818.1

40

60

5

10

0

20

QTR TO24/12/05

QTR TO25/03/06

QTR TO24/06/06

QTR TO23/09/06

QTR TO23/12/06

QTR TO24/03/07

QTR TO23/06/07

QTR TO22/09/07

QTR TO22/12/07

0

24/12/05 25/03/06 24/06/06 23/09/06 23/12/06 24/03/07 23/06/07 22/09/07 22/12/07

Value Market Share Penetration Avg Spend Per Buyer ($ AWOP)

Source: ACNielsen Homescan

PL share growth has also been driven through Aldi. Aldi PL share growth has also been driven through Aldi. Aldi is also successfully attracting new shoppers through is also successfully attracting new shoppers through

new store openingsnew store openings

ALDI PL KPI’s and Market Share Trend

new store openings.new store openings.

ALDI PL KPI s and Market Share Trend

Total Aldi

$153.90$144 30 $146 20

160 100$141.90

$132.00

$143.50 $143.80

$131.10 $133.80

$144.30 $146.20

120

140

707580859095

92.4 91.9 93.1 92.5 92.5 91.2 91.4 93.190.680

100

40455055606570

20

40

60

152025303540

15 16.5 17.2 18.4 19.8 20.2 21.2 23.2 24.1

0

20

QTR TO24/12/05

QTR TO25/03/06

QTR TO24/06/06

QTR TO23/09/06

QTR TO23/12/06

QTR TO24/03/07

QTR TO23/06/07

QTR TO22/09/07

QTR TO22/12/07

0510

Value Market Share Penetration Avg Spend Per Buyer ($ AWOP)

Source: ACNielsen Homescan

So what is the secret to Aldi’s success, besides their So what is the secret to Aldi’s success, besides their price?price?

ff fEfficient / Time Saving No Confusing Decisions

59% of regular shoppers agree that they do not need to spend long in store at Aldi.

50% of regular shoppers agree that they are not distracted to buy things they don’t need at Aldi.

Source: Nielsen Omnibus, September 2007

at Aldi.

and how is this impacting NARTD?

Overall however we are not seeing PL gain share Overall however we are not seeing PL gain share within the Beverages category in Grocery.within the Beverages category in Grocery.

f | 1997| 2007The impact of PL on NARTD | 1997| 2007

Branded Beverages

PL Bevs11.9%share

Branded Beverages

PL Bevs9.0%share

88.1% shareBranded Beverages

91.0% share

Source: Nielsen ScanTrack

We are though seeing certain segments where PL is We are though seeing certain segments where PL is gaining ground. gaining ground.

The impact of PL on NARTD | 1997 s 2007The impact of PL on NARTD | 1997 vs. 2007

Branded Mineral Water76.4% share

Branded Mineral Water64.9% share

Branded Water87.8% share

Branded Water83.6% share

Branded Juice91.5% share

Branded Juice87.5% share

2007 2007 20071997 1997 1997

PL MW23.6%share

PL MW35.1%share

PL Water12.2%share

PL Water16.4%share

PL Juice8.5%share

PL Juice12.5%share

Source: Nielsen ScanTrack

And its easy to see why….And its easy to see why….

14c / 100ml 9c / 100ml

5c / 100ml 20c / 100ml

14c / 100ml 11c / 100ml

Source: Coles Online

Brand BuyerBrand BuyerBrand BuyerBrand Buyer

Promotional BuyerPromotional Buyer

Private Label BuyerPrivate Label Buyer

Aldi BuyerAldi Buyer

Health is another key issue facing the marketHealth is another key issue facing the market

And as a result, Diet items are growing significantly And as a result, Diet items are growing significantly ahead of non diet beverages.ahead of non diet beverages.

National Grocery | Volume % Change vs. YAVolume = Litres (000's)

16 718.0

12.0

16.7

12.0

14.0

16.0

6 86 7

10.29.2

7.18.18.0

10.0

6.1

2.1

6.16.8

4.5

2.1

5.86.7

4.93.3

4.7

2.0

4.0

6.0

-0.2-1.4

0.9

-2.0

0.0YEAR1998

YEAR1999

YEAR2000

YEAR2001

YEAR2002

YEAR2003

YEAR2004

YEAR2005

YEAR2006

YEAR2007

-4.0

TOTAL NON-DIET TOTAL DIETSource: Nielsen ScanTrack

Which has resulted in Diet gaining over 10 share Which has resulted in Diet gaining over 10 share points over the last 10 years.points over the last 10 years.

National Grocery | Diet vs. Non Diet Share of NARTD Volume = Litres (000's)( )

70%80%90%

100%

40%50%60%70%

26.0 27.0 27.9 27.7 27.0 28.1 29.5 29.7 31.4 35.1 36.010%20%30%40%

0%YEAR1997

YEAR1998

YEAR1999

YEAR2000

YEAR2001

YEAR2002

YEAR2003

YEAR2004

YEAR2005

YEAR2006

YEAR2007

Source: Nielsen ScanTrackdiet non diet

Current landscapeNational consumption, segment shares and segment profiles

Homescan per capitaHomescan, per capita consumption nationally.p y

AVG 116 8LAVG - 116.8L

AVG 111 2L

AVG – 98.4L

AVG – 111.2L

AVG – 102 8LAVG – 127.0L

AVG – 102.8L

AVG – 78.7L

Price per litre driving value share in Route and Price per litre driving value share in Route and Convenience.Convenience.

Volume and Value NARTD Share of Trade Volume = litres (000's), Value = $ (000's)

14.1

33 3

3.2 7.6

80.0

90.0

100.0

33.3

50.0

60.0

70.0

82.7

59.1

20.0

30.0

40.0

0.0

10.0

VOL % SHR OF TRADE VAL % SHR OF TRADE

Grocery Traditional Route P&C

Source: Nielsen ScanTrack

While the emerging segments value share is higher While the emerging segments value share is higher than their volume share due to the higher price.than their volume share due to the higher price.

Value and Volume Segment Share of NARTD Volume = Litres (000's), Value = $ (000's)

70 080.0

90.0

100.0

10.9%

11.3%16.1%

7 5%

40.0

50.0

60.0

70.016.9%

19.7%

7.5%

0 0

10.0

20.030.0 60.9%56.7%

0.0

VAL % SHARE VOL % SHARE

TOTAL SOFT DRINKS TOTAL FRUIT JUICE & DRINK TOTAL STILL WATER

TOTAL ENERGY DRINKS TOTAL SPORTS DRINKS TOTAL MIXERSTOTAL ENERGY DRINKS TOTAL SPORTS DRINKS TOTAL MIXERSTOTAL MINERAL WATERS TOTAL TEA

Source: Nielsen ScanTrack

Cola Flavoured Carbonated Beverages

25 – 54 year olds25 54 year olds

Married with kids, older and younger families

Lower blue collar occupation

Skewed towards QLD families

Source: Nielsen Omni

Fruit Juice and Drinks

55+ year olds55+ year olds

Married with no kids

Upper White Collar / no occupation (retired)

Higher Income

NSW skew, outside of Sydney metro area

Source: Nielsen Omni

Still Bottled Water

FemaleFemale

18 - 24 year olds

Skewed towards the Sydney metro area

Source: Nielsen Omni

Non Cola Flavoured Carbonated Beverages

55+ year olds55+ year olds

No Kids

Retired

Low to Medium Income

Source: Nielsen Omni

Iced Tea

18 - 24 year olds18 24 year olds

No Kids

Skewed towards metro areas

Source: Nielsen Omni

Sports Drinks

MalesMales

18-39 year olds

Blue Collar

Low to Medium income

Perth and Queensland area

Source: Nielsen Omni

Energy Drinks

18 -24 year olds18 24 year olds

Single with no kids

Upper blue collar

Skewed towards Melb, QLD and SA

Source: Nielsen Omni

More often the driver of purchase

Less often the driver of purchase

QuenchPopular Taste

p

QThirst

Availability

Fizzy

Give Energy

Health

Sweet

Flavour

Brand

taste Importance of product attributes across all NARTD

Natural

Make meFeel good Often on

PromoGood ValueHydrationGood

Size

FunctionalPackaging

Feel good

Size

Source: Nielsen Omni

This is reflected in the advertising and products in This is reflected in the advertising and products in the market.the market.

Taste

The Experience

Functional Benefits

Pre and Post Performance

Looking forward | consumer trendsMega Trends

Mega TrendsMega TrendsMega TrendsMega TrendsS i th Pl t Aff d bl l i Ev da T h lSaving the Planet Affordable luxuries Everyday Technology

• Local sourcing • Added value services• Local sourcing

• Natural production/organic

• Sustainable manufacturing

• Added value services

• Premium product/quality

• Customisation/one offs/exclusivity

• Brand information access

• Media selection & relevance to target consumer/shopper

Sustainable manufacturing

• Protects scarce energy/water resources

Customisation/one offs/exclusivity

• Speciality sourced/expert endorsement

• Simple messages/cut through

• Product benefits not ingredients

• Recyclable materials • Mobile lifestyles

Mega TrendsMega TrendsMega TrendsMega TrendsIllness to Wellness Time povertyIllness to Wellness Time poverty

• Labelling & honesty (to help me choose & take control)

• Time savers

• Packaging functionality•Good stuff to support diet

•Hydration giving

Packaging functionality•

•Standout in store•

•Make it easy for me•Natural and organic

•Energy giving

y•

•Where I am spending my time/living my life

Summing up the Summing up the pastpast, present and future, present and future

• In the past we have seen share gains from the emerging p g g gsegments of Energy, Sports and Water.– These segments have also been key in driving growth for

Beverages over the last 10 yearsBeverages over the last 10 years.

• Over the last few years we have seen a shift towards PL within T t l G ll t i BTotal Grocery as well as some segments in Beverages. – The major threat is towards Natural or non Flavoured products

which are used as moderators.

• Health has also become a major factor within beverages.Banning some drinks in schools shows like The Biggest Loser etc– Banning some drinks in schools, shows like The Biggest Loser etc have changed consumers perceptions, which has resulted in strong growth for Diet Beverages.

Summing up the past, Summing up the past, presentpresent and futureand future

• Currently South Australians are the heaviest per capita y p pconsumers of Beverages.

Th h l lit G ti f th 8L i• The channel split sees Grocery accounting for more than 8L in every 10L purchased.– From a value point of view however Convenience and Route

account for about 40% of the market.

• The most common driver for purchase across all beverages isThe most common driver for purchase across all beverages is Taste with Thirst Quench and Availability also important.– From a segment level however these do change.

Summing up the past, present and Summing up the past, present and futurefuture

• Going forward there will be renewed pressure on manufacturers g pand retailers to provide consumers with more.

There will be a focus on health and the environment through natural– There will be a focus on health and the environment through natural products and packaging.

– Consumer Generated Media will be an important data source for manufacturers to understand how consumers feel and interact withmanufacturers to understand how consumers feel and interact with their brands.

– Consumers will look to manufacturers to provide them more from th k t i t it i d t h l th f lthe same pack, more nutrients, vitamins and more to help them feel better.

– And finally, how will manufacturers provide consumers with a d t th t th th t ith th i li ?product that they can use as they get on with their lives?

• Functional Packaging, in store media / theatre and assisting consumers in making it easy.

Thank You