NAPTP 2015 MLP Investor Conference

36

NAPTP 2015 MLP Investor Conference May 2015

-

Upload

irjpenergy -

Category

Investor Relations

-

view

1.238 -

download

0

Transcript of NAPTP 2015 MLP Investor Conference

NAPTP 2015 MLP Investor Conference

May 2015

Disclaimers

2

Forward Looking StatementsThis presentation contains forward‐looking statements. These statements discuss future expectations, contain projections of results of operations or of financial condition or state other forward‐looking information. These statements are based upon various assumptions, many of which are based, in turn, upon further assumptions, including examination of historical operating trends made by the management of the Partnership. Although the Partnership believes that these assumptions were reasonable when made, because assumptions are inherently subject to significant uncertainties and contingencies, which are difficult or impossible to predict and are beyond its control, the Partnership cannot give assurance that it will achieve or accomplish these expectations, beliefs or intentions. These forward‐looking statements involve risks and uncertainties. When considering these forward‐ looking statements, you should keep in mind the risk factors and other cautionary statements in the Partnership’s 10‐K and other documents on file with the Securities and Exchange Commission. The risk factors and other factors noted in the Partnership’s public filings could cause the Partnership’s actual results to differ materially from those contained in any forward‐looking statement.

This document includes certain non‐GAAP financial measures as defined under SEC Regulation G. A reconciliation of those measures to most directly comparable GAPP measures is provided in the appendix to this presentation.

Non‐GAAP MeasuresAdjusted EBITDA is defined as net income (loss) plus (minus) interest expense (income), income tax expense (benefit), depreciation and amortization expense, asset impairments, (gains) losses on asset sales, certain non‐cash charges such as non‐cash equity compensation and non‐cash vacation expense, non‐cash (gains) losses on commodity derivative contracts (total (gain) loss on commodity derivatives less net cash flow associated with commodity derivatives settled during the period) and selected (gains) charges and transaction costs that are unusual or non‐recurring and other selected items that impact comparability.

We define distributable cash flow as Adjusted EBITDA less net cash interest paid, income taxes paid and maintenance capital expenditures.

JP Energy Partners LP (JPEP) Overview

3

• NYSE Listed: JPEP• Formed in May 2010; IPO in October 2014• JPEP is a publicly traded, diversified master limited partnership with operations including:

• Crude Oil Pipelines and Storage• Refined Products Terminals and Storage• NGL Distribution and Sales• Crude Oil Supply and Logistics

• JPEP Trading Summary (1)

• Unit Price: $13.34• Units Outstanding: 36.4mm• Market Cap: $486mm• Current Yield: 9.7%

___________________________1. As of May 15, 2015 close. Assumes $1.30 annual distribution

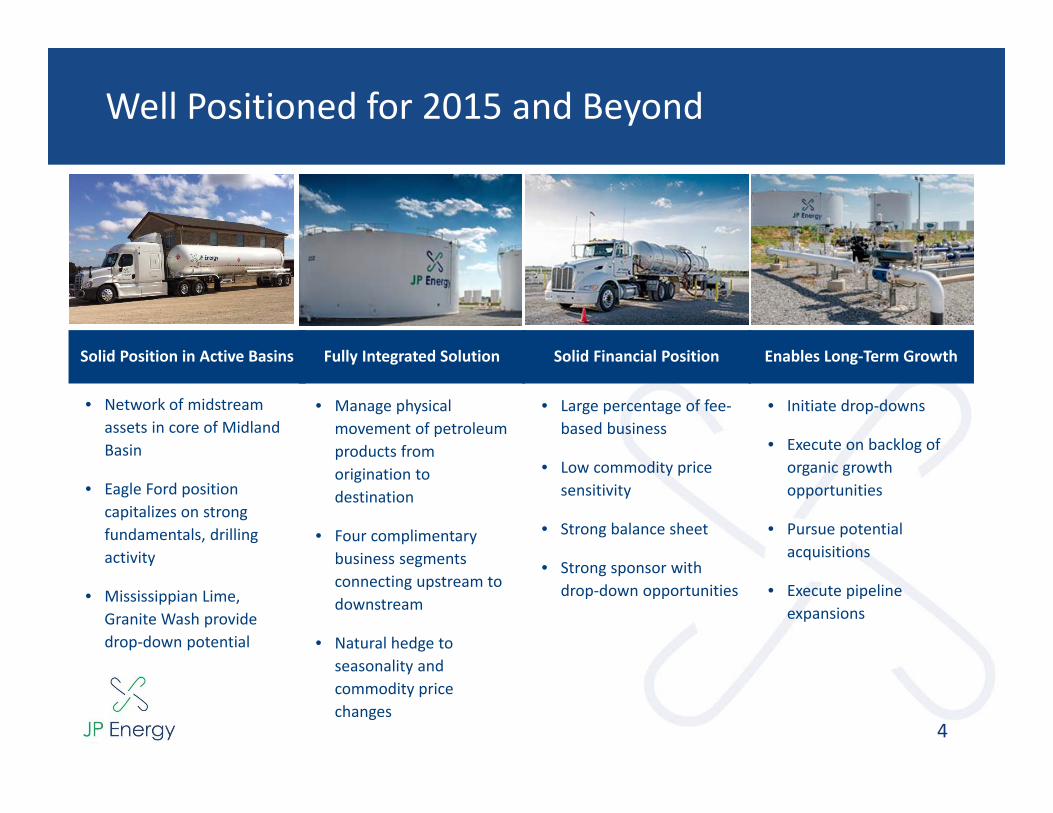

Well Positioned for 2015 and Beyond

4

Solid Position in Active Basins Fully Integrated Solution Solid Financial Position

• Network of midstream assets in core of Midland Basin

• Eagle Ford position capitalizes on strong fundamentals, drilling activity

• Mississippian Lime, Granite Wash provide drop‐down potential

• Manage physical movement of petroleum products from origination to destination

• Four complimentary business segments connecting upstream to downstream

• Natural hedge to seasonality and commodity price changes

• Large percentage of fee‐based business

• Low commodity price sensitivity

• Strong balance sheet

• Strong sponsor with drop‐down opportunities

Enables Long‐Term Growth

• Initiate drop‐downs

• Execute on backlog of organic growth opportunities

• Pursue potential acquisitions

• Execute pipeline expansions

Business Diversification

Cylinder Exchange (National)

Geographically Diversified Midstream Platform

6

Crude Oil Pipelines and Storage

Crude Oil Supply and Logistics

Refined Products Terminals and Storage

NGL Sales, NGL Transportation

Diversified Offering From Upstream to Downstream

Integrated logistics solutions from the wellhead to the end‐user

Crude Oil

Producers Refiners

Truck

Pipeline Gathering

Injection Station Pipeline Terminal/Storage/Exchange Location

Pipeline

Refined ProductsNatural Gas LiquidsRefineries

OFS and Agriculture

Gas Stations

Barge

Common Carrier Pipelines

Tanker

Storage

Rail

Diluent for Heavy Crude

Producers

Refinery Produced LPG

Spec Products

Retail Distributor

Storage

7

8

Growing, Fee‐Based Cash Flows with High Quality Customer Base

Refined Products Terminals and Storage– Fixed fees for throughput and storage– Fixed fees for blending services, injection of additives and ancillary

services, including product handling and transfer services– Rollup strategy and optimization

NGL Distribution and Sales– Recent acquisition of NGL truck services from JP Development with

fixed fees based on distance and volume transported Crude Oil Pipelines and Storage

– Fixed storage and throughput or minimum volume commitment fees

– Growing volumes in the Southern Wolfcamp from existing contracted producers with long‐term fee‐based commitments

– Pursuing additional customer acreage and MVC within JP Energy’s capture area

– Expansion of Silver Dollar Pipeline Crude Oil Supply and Logistics

– Crude oil trucking and “fee equivalent” lease gathering

Focused on

Growing Fee‐ba

sed Ca

sh Flows NGL

Distribution and Sales

Refined Products Terminals and Storage

Crude Oil Pipelines & Storage

2014 Adjusted EBITDA Mix

NGL Distribution and Sales

28%

Refined Products Terminals and

Storage19%

Crude Oil Pipeline and Storage

36%

Crude Oil Supply and Logistics

17%

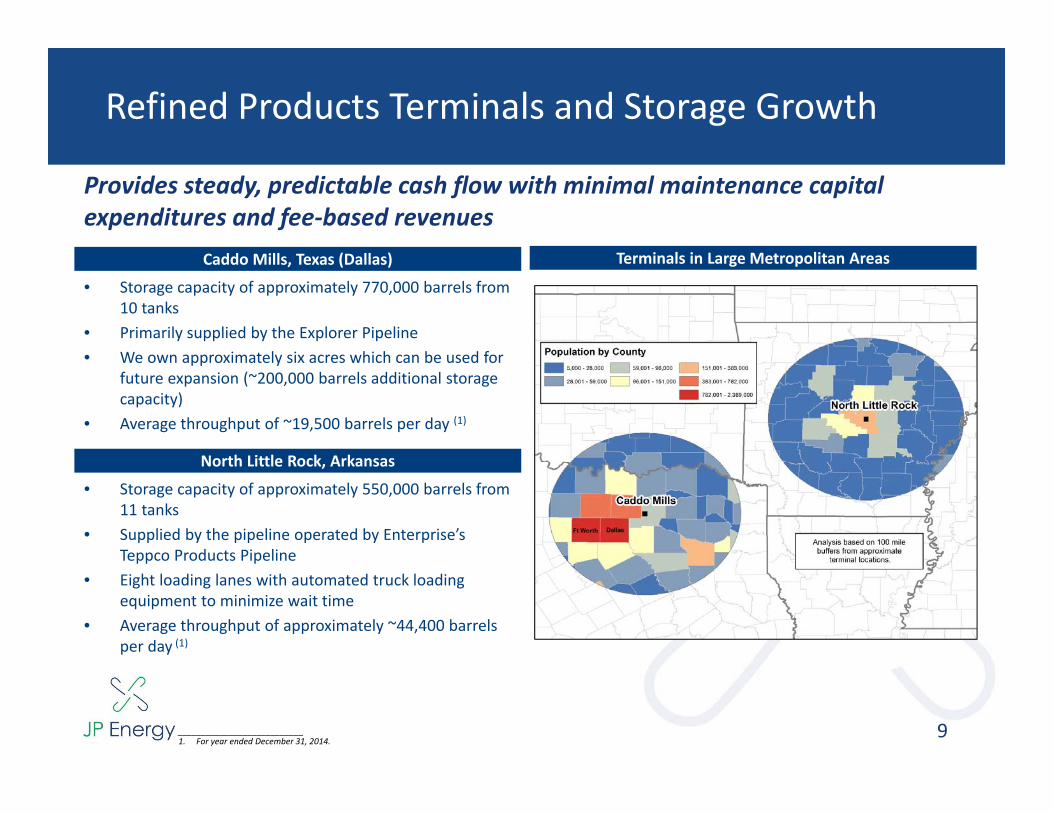

Refined Products Terminals and Storage Growth

• Storage capacity of approximately 770,000 barrels from 10 tanks

• Primarily supplied by the Explorer Pipeline• We own approximately six acres which can be used for

future expansion (~200,000 barrels additional storage capacity)

• Average throughput of ~19,500 barrels per day (1)

Caddo Mills, Texas (Dallas) Terminals in Large Metropolitan Areas

9

• Storage capacity of approximately 550,000 barrels from 11 tanks

• Supplied by the pipeline operated by Enterprise’s Teppco Products Pipeline

• Eight loading lanes with automated truck loading equipment to minimize wait time

• Average throughput of approximately ~44,400 barrels per day (1)

North Little Rock, Arkansas

Provides steady, predictable cash flow with minimal maintenance capital expenditures and fee‐based revenues

___________________________1. For year ended December 31, 2014.

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

40%

50%

Jan‐87

Sep‐87

May‐88

Jan‐89

Sep‐89

May‐90

Jan‐91

Sep‐91

May‐92

Jan‐93

Sep‐93

May‐94

Jan‐95

Sep‐95

May‐96

Jan‐97

Sep‐97

May‐98

Jan‐99

Sep‐99

May‐00

Jan‐01

Sep‐01

May‐02

Jan‐03

Sep‐03

May‐04

Jan‐05

Sep‐05

May‐06

Jan‐07

Sep‐07

May‐08

Jan‐09

Sep‐09

May‐10

Jan‐11

Sep‐11

May‐12

Jan‐13

Sep‐13

May‐14

Jan‐15

TTM U.S Total Gasoline Sales by Refiner YoY Change TTM Average YoY Price Change

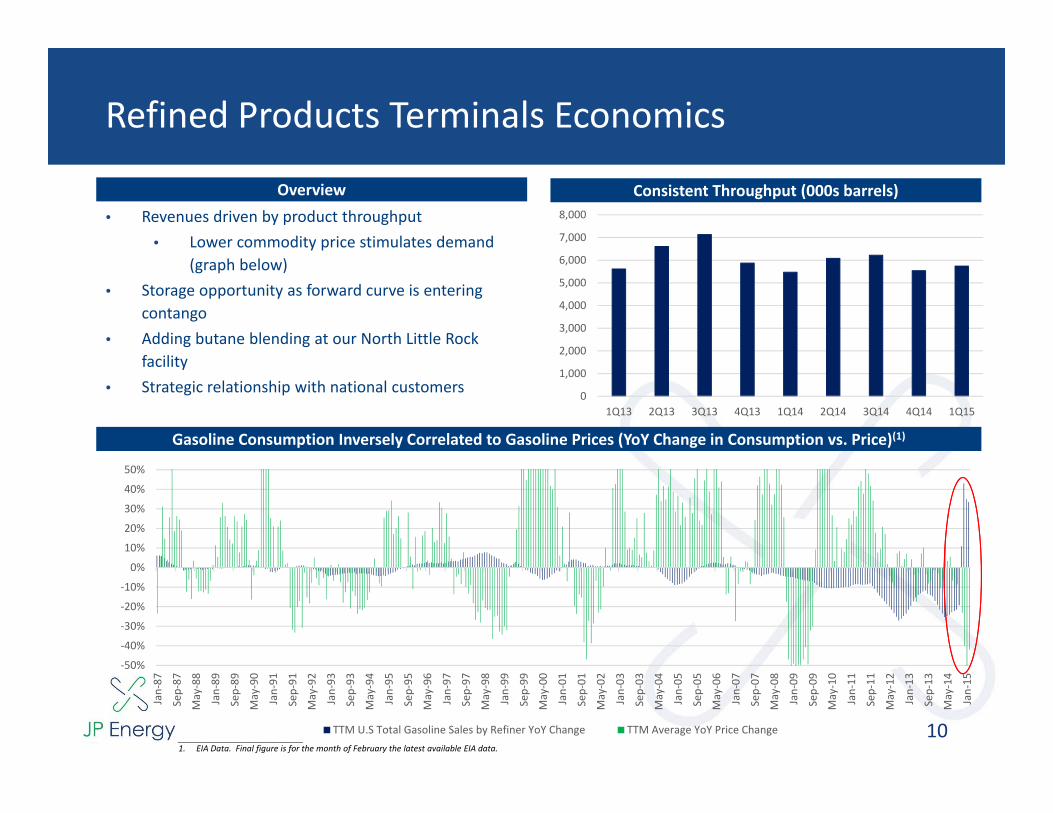

• Revenues driven by product throughput• Lower commodity price stimulates demand

(graph below)• Storage opportunity as forward curve is entering

contango• Adding butane blending at our North Little Rock

facility• Strategic relationship with national customers

Refined Products Terminals Economics

10

Overview

Gasoline Consumption Inversely Correlated to Gasoline Prices (YoY Change in Consumption vs. Price)(1)

Consistent Throughput (000s barrels)

___________________________1. EIA Data. Final figure is for the month of February the latest available EIA data.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

Crude Oil Storage

11

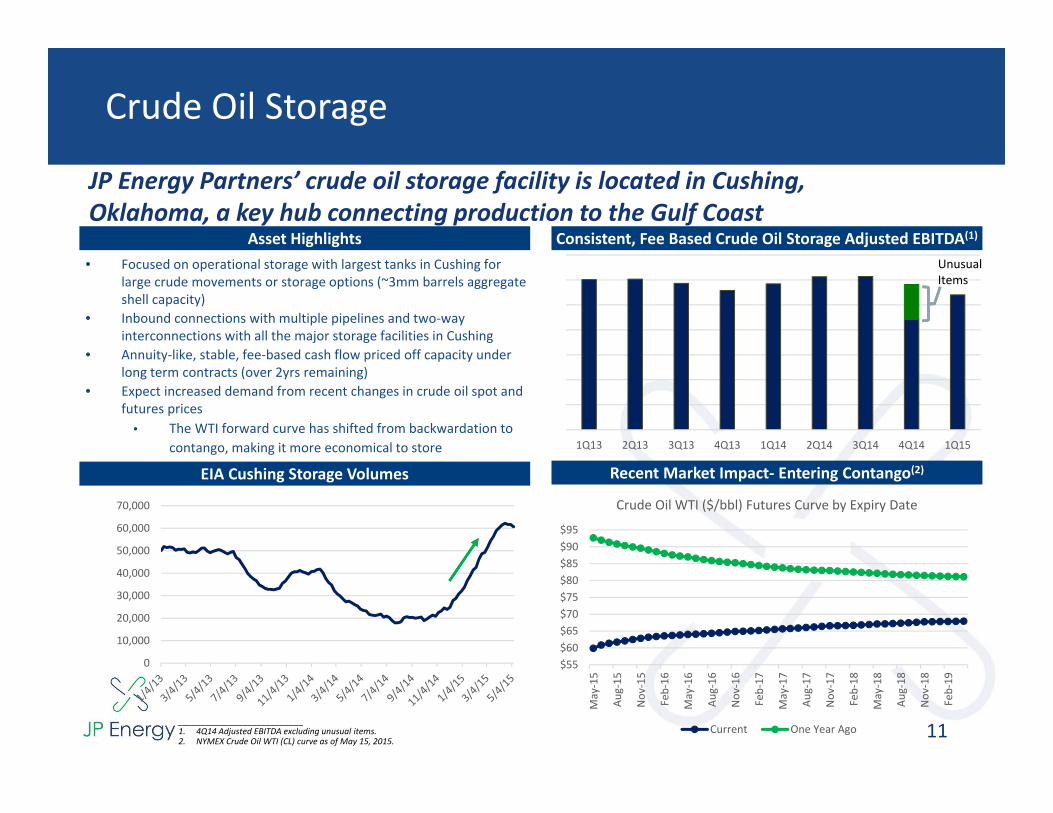

JP Energy Partners’ crude oil storage facility is located in Cushing, Oklahoma, a key hub connecting production to the Gulf Coast

Asset Highlights• Focused on operational storage with largest tanks in Cushing for

large crude movements or storage options (~3mm barrels aggregate shell capacity)

• Inbound connections with multiple pipelines and two‐way interconnections with all the major storage facilities in Cushing

• Annuity‐like, stable, fee‐based cash flow priced off capacity under long term contracts (over 2yrs remaining)

• Expect increased demand from recent changes in crude oil spot and futures prices

• The WTI forward curve has shifted from backwardation to contango, making it more economical to store

Recent Market Impact‐ Entering Contango(2)

Consistent, Fee Based Crude Oil Storage Adjusted EBITDA(1)

EIA Cushing Storage Volumes

___________________________1. 4Q14 Adjusted EBITDA excluding unusual items.2. NYMEX Crude Oil WTI (CL) curve as of May 15, 2015.

Unusual Items

$55$60$65$70$75$80$85$90$95

May‐15

Aug‐15

Nov

‐15

Feb‐16

May‐16

Aug‐16

Nov

‐16

Feb‐17

May‐17

Aug‐17

Nov

‐17

Feb‐18

May‐18

Aug‐18

Nov

‐18

Feb‐19

Crude Oil WTI ($/bbl) Futures Curve by Expiry Date

Current One Year Ago

NGL Distribution and Sales

12

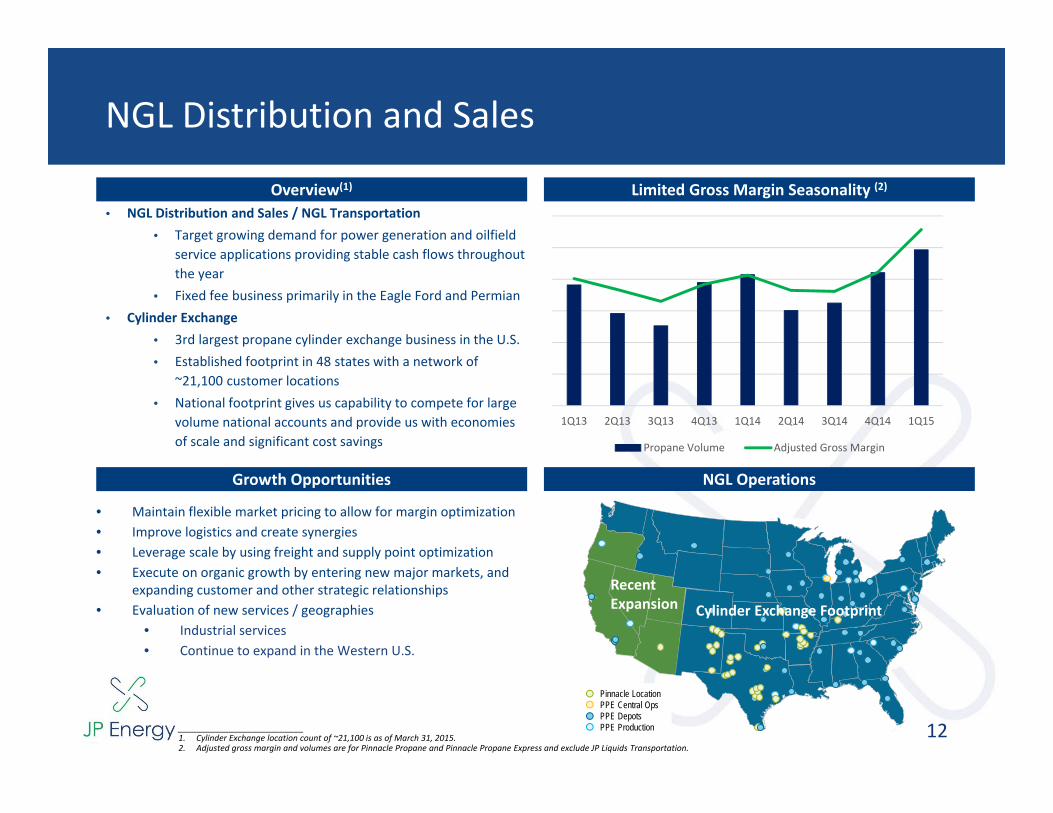

Limited Gross Margin Seasonality (2)Overview(1)

• NGL Distribution and Sales / NGL Transportation• Target growing demand for power generation and oilfield

service applications providing stable cash flows throughout the year

• Fixed fee business primarily in the Eagle Ford and Permian• Cylinder Exchange

• 3rd largest propane cylinder exchange business in the U.S.• Established footprint in 48 states with a network of

~21,100 customer locations• National footprint gives us capability to compete for large

volume national accounts and provide us with economies of scale and significant cost savings

• Maintain flexible market pricing to allow for margin optimization• Improve logistics and create synergies• Leverage scale by using freight and supply point optimization• Execute on organic growth by entering new major markets, and

expanding customer and other strategic relationships• Evaluation of new services / geographies

• Industrial services• Continue to expand in the Western U.S.

Growth Opportunities NGL Operations

Cylinder Exchange Footprint

Recent Expansion

Pinnacle LocationPPE Central OpsPPE DepotsPPE Production___________________________

1. Cylinder Exchange location count of ~21,100 is as of March 31, 2015.2. Adjusted gross margin and volumes are for Pinnacle Propane and Pinnacle Propane Express and exclude JP Liquids Transportation.

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

Propane Volume Adjusted Gross Margin

NGL Distribution and Sales Economics

13

Overview• Two primary businesses reduce seasonality

• Propane Sales and Distribution business is winter weighted, although decreasing seasonality due to growth in industrial and oilfield services

• Propane Cylinder Exchange business summer weighted

• Margins tend to expand as commodity prices fall• Longer dated sales contracts

Limited Seasonality (1)

___________________________1. Based on adjusted gross margin for the year ended December 31, 2014. Winter includes three months ending March 31, 2014 and December 31, 2014 , and summer includes the

three months ending June 30, 2014 and September 30, 2014.2. NYMEX Propane Non‐LDH Mt. Belvieu (OPIS) front month and NYMEX WTI Front Month through May 15, 2015.

Mt. Belvieu ($/gal) Correlated With NYMEX WTI ($/bbl)(2)

Winter, 54%Summer, 46%

$0

$20

$40

$60

$80

$100

$120

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

12/4/13

1/4/14

2/4/14

3/4/14

4/4/14

5/4/14

6/4/14

7/4/14

8/4/14

9/4/14

10/4/14

11/4/14

12/4/14

1/4/15

2/4/15

3/4/15

4/4/15

5/4/15

NYMEX Propane Mt. Belvieu (OPIS) WTI NYMEX

Silver Dollar Anchored by Active Producers and Provides Access to Multiple End‐Markets

JP Energy Partners’ crude oil pipeline system is base loaded by three customers with over 350,000 contiguous acres in the Permian Basin

14

~5 years remaining on

minimum volume commitment

~9 years remaining with 110,000 acre dedication

Major Customer A

Major Customer B

10 years with53,000 acreage dedication

Major Customer C

Irion

Reagan

Crockett

Upton

Sterling

Schleicher

Tom Green

Glasscock

Pecos

Midland

JPE - Silver Dollar Pipeline

LegendReagan Lateral Station

Future Station

Stations

Take Away Options

Reagan Pipeline

Rail

Major Highways

Counties

UTM Zone 1405/18/15

0 105 Miles

Oxy Barnhart Station (Centurion Interconnect

to Colorado City)

Owens Station(Plains Interconnect

to Midland)

MidwayTruck

Station

Future TruckStation

Future TruckStation

TruckStation

TruckStation

Magellan Barnhart Station (Longhorn Interconnect to E. Houston – Q3 2015)

Silver Dollar Pipeline Continuing To Grow

15

Overview

• Volume growth from the core of the Permian continues in current oil price environment

• Connection to Cline Shale immediately expanded system capacity

• Customers remain committed to developing Permian acreage

• Most stated break‐evens look to be in high‐$40s• Area producers expect year over year growth

despite declining rig counts• Substantial optionality with three connections

• Oxy Cline Shale• Plains Owens• Magellan Longhorn

• Trucking stations create synergies with Crude Oil Supply and Logistics segment

• Increases capture area of the system

Volume Growth Accelerating

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15

Pipeline Volumes (Barrels Per Day)

16

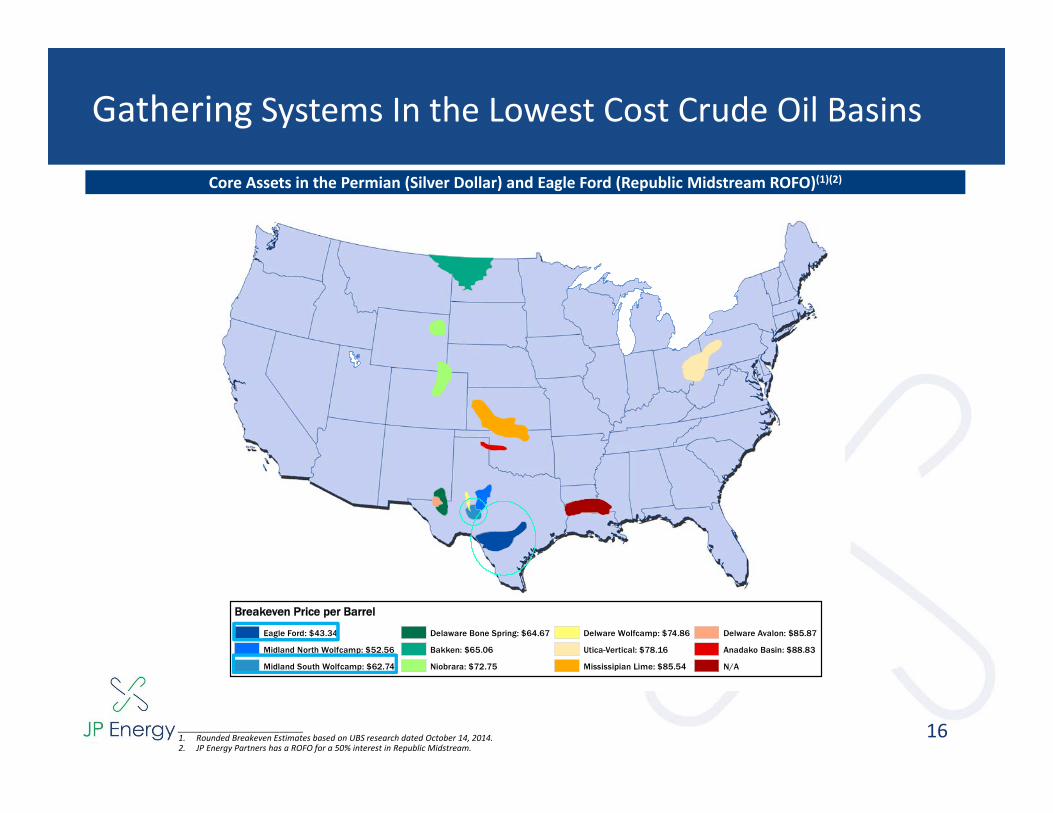

Gathering Systems In the Lowest Cost Crude Oil Basins

Core Assets in the Permian (Silver Dollar) and Eagle Ford (Republic Midstream ROFO)(1)(2)

___________________________1. Rounded Breakeven Estimates based on UBS research dated October 14, 2014.2. JP Energy Partners has a ROFO for a 50% interest in Republic Midstream.

JP Energy Focus Areas

Breakeven Price per Barrel

Eagle Ford: $43.34

Midland North Wolfcamp: $52.56

Midland South Wolfcamp: $62.74

Delaware Bone Spring: $64.67

Bakken: $65.06

Niobrara: $72.75

Delware Wolfcamp: $74.86

Utica-Vertical: $78.16

Mississipian Lime: $85.54

Delware Avalon: $85.87

Anadako Basin: $88.83

N/A

________________

____________________________

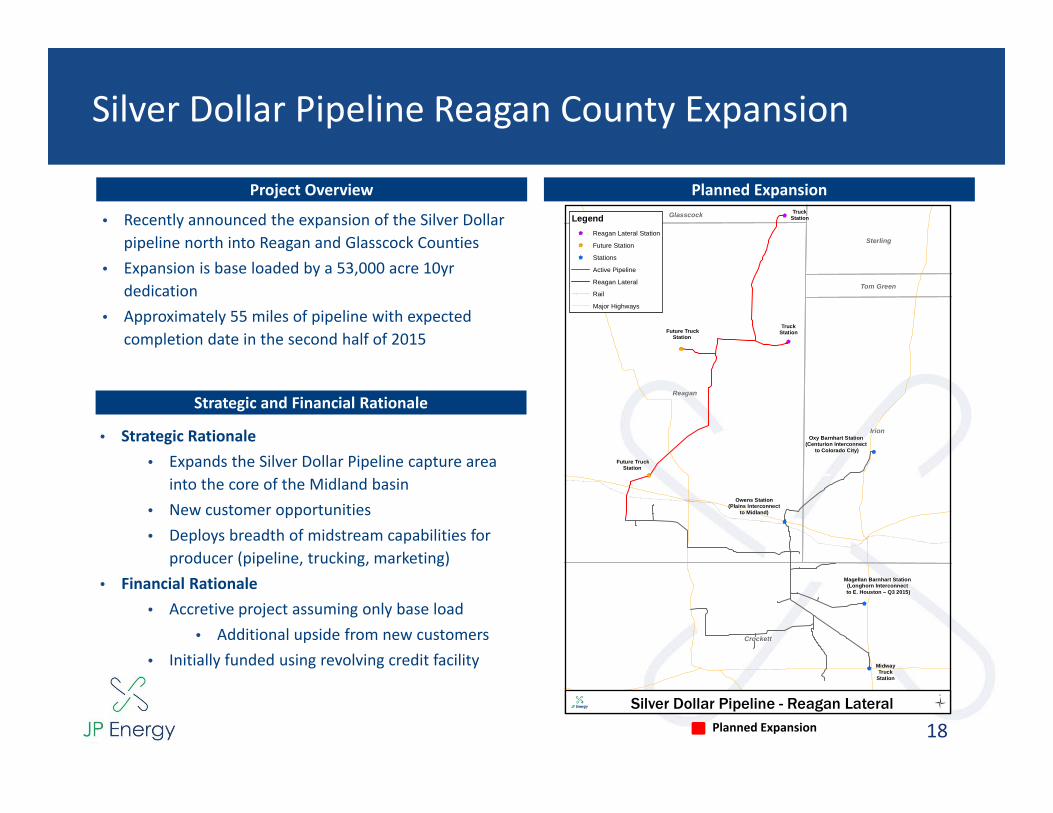

Recent Project Updates

18

Silver Dollar Pipeline Reagan County Expansion

Project Overview

• Recently announced the expansion of the Silver Dollar pipeline north into Reagan and Glasscock Counties

• Expansion is base loaded by a 53,000 acre 10yr dedication

• Approximately 55 miles of pipeline with expected completion date in the second half of 2015

Planned Expansion

Strategic and Financial Rationale

• Strategic Rationale• Expands the Silver Dollar Pipeline capture area

into the core of the Midland basin• New customer opportunities• Deploys breadth of midstream capabilities for

producer (pipeline, trucking, marketing)• Financial Rationale

• Accretive project assuming only base load• Additional upside from new customers

• Initially funded using revolving credit facility

Planned Expansion

Reagan

Irion

Crockett

Sterling

Glasscock

Tom Green

Silver Dollar Pipeline - Reagan Lateral

LegendReagan Lateral Station

Future Station

Stations

Active Pipeline

Reagan Lateral

Rail

Major Highways

Oxy Barnhart Station (Centurion Interconnect

to Colorado City)

Owens Station(Plains Interconnect

to Midland)

MidwayTruck

Station

Future TruckStation

Future TruckStation

TruckStation

TruckStation

Magellan Barnhart Station (Longhorn Interconnect to E. Houston – Q3 2015)

19

Magellan Longhorn Interconnection

Project OverviewProject Overview

• In April, JP Energy executed an interconnection agreement with an affiliate of Magellan Midstream Partners, L.P. (“Magellan”)

• The agreement connects our Silver Dollar Pipeline System to Magellan’s Longhorn pipeline at Barnhart Terminal in Crockett County, TX

• Expected to be in service by the third quarter of 2015

Multiple Take‐Away OptionsMultiple Take‐Away Options

Strategic and Financial RationaleStrategic and Financial Rationale

• Strategic Rationale• Provide producers with a third take‐away option

• Optionality helps producers find the most attractive end markets and avoid congestion at any given market

• Provide producers with direct access from the core of the Midland Basin to Houston end markets

• Attractive selling point for current and future potential customers

Colorado City

Houston

Midland

PlainsOxy Cline’s Centurion

Magellan Longhorn

Silver Dollar Pipeline

20

Southern Propane Acquisition

Project OverviewProject Overview

• In April, JP Energy announced it entered into a definitive agreement to acquire substantially all of the assets of Southern Propane Inc. (“Southern”) for $14.9mm, subject to certain adjustments

• The transaction closed on May 8th

• Southern Propane services mostly industrial and commercial clients in the greater Houston area

• Transaction was largely funded with cash from our revolver as well as a ~267,000 unit issuance to the Seller

Complementary FootprintComplementary Footprint

Strategic and Financial RationaleStrategic and Financial Rationale

• Strategic Rationale• Non‐heating degree day dependent

commercial/industrial propane gallons• Complementary footprint should reduce travel

times across busy Houston roads and increase route density

• Strengthen footprint in attractive Houston Industrial market

• Southern has displayed a strong growth profile• Financial Rationale

• Immediately accretive

• Southern storage tank

• JPEP storage facilities

Strong Equity Sponsorship

JP Energy Family Overview

22

JP Energy Partners has a strategic partnership with JP Development and Republic Midstream

JP Development• Founded in July 2012 to support JP

Energy’s growth

• JP Development projects may be dropped down to us

– In February 2014, we completed our first drop down valued at $319 million

• JP Development has extended us a right of first offer (ROFO) for the five years following the IPO on all of JP Development’s current and future assets

JP Energy Partners• Founded in May 2010 to own,

operate, develop and acquire a diversified portfolio of midstream energy assets

• Operations currently consist of four business segments:

– Crude Oil Pipelines and Storage

– Crude Oil Supply and Logistics

– Refined Products Terminals and Storage

– NGL Distribution and Sales

Republic Midstream• Formed with $400 million

commitment from ArcLight to design, build and operate a crude gathering system for Penn Virginia in the Eagle Ford shale

– Managed by JPEP and American Midstream

– JPEP has a ROFO for 18 months following the IPO for a 50% interest in the joint venture

Permian

NorthBarnett

Combo Play

Eagle Ford

MississippianLime

GraniteWash Woodford

Woodford

Woodford-SCOOP

Management & ArcLight have created near term drop‐down opportunities

Crude Oil Drop‐Down Opportunities

• ArcLight has demonstrated the ability to invest broadly and profitably across the energy industry

• ArcLight has a substantial equity commitment to JP Energy Partners / JP Development

• Right of First Offer with JP Development & Republic Midstream

ArcLight Sponsorship

23

Great Salt Plains Pipeline• ~115 mile crude oil pipeline• Transports Mississippian Lime

supply to Cushing, Oklahoma• Ability to expand capacity from

27 Mbbls/d to 40 Mbbls/d

Red River Pipeline• ~75 mile crude oil pipeline that

transports oil from N. Texas to Garvin City, Oklahoma

• Current capacity of 5 Mbbls/d

Republic Midstream• 180‐mile crude oil gathering

system in Gonzales & Lavaca counties, Texas

• Central delivery point (“CDP”) with storage and blending capacity

• 30‐mile takeaway pipeline

Potential Drop‐Downs

Financial Strategy

Available Liquidity ($mm)(1)

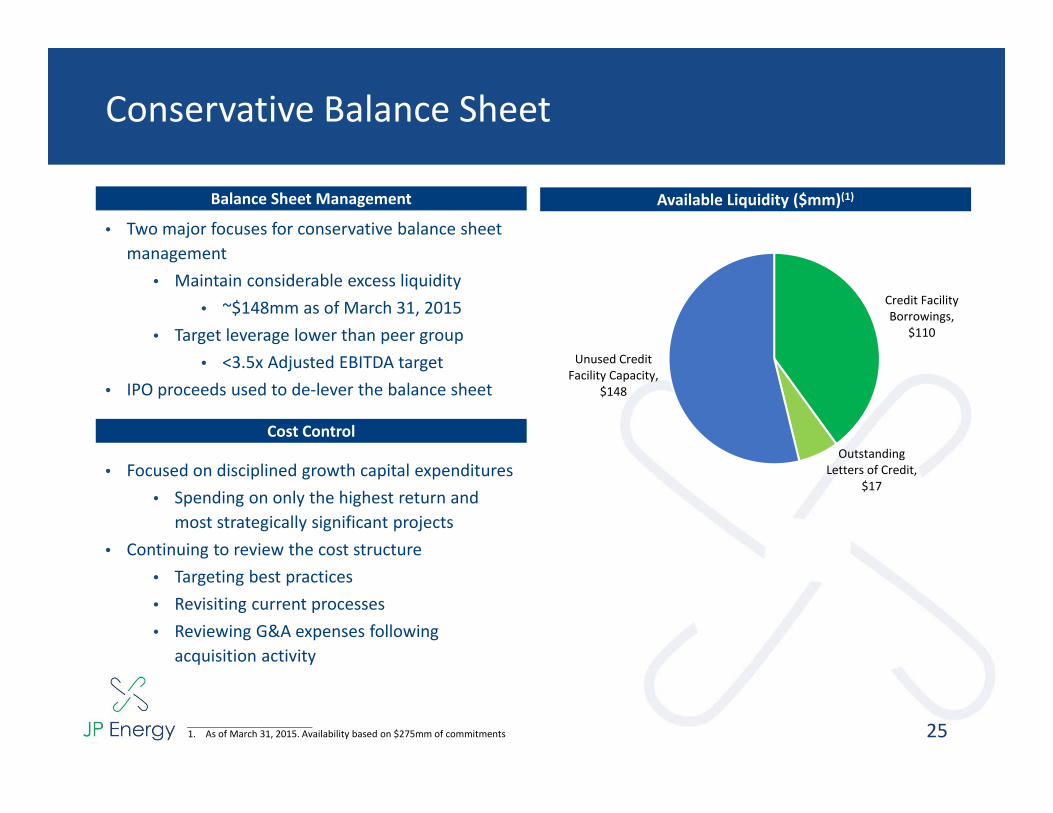

Conservative Balance Sheet

25

Balance Sheet Management

• Two major focuses for conservative balance sheet management

• Maintain considerable excess liquidity• ~$148mm as of March 31, 2015

• Target leverage lower than peer group• <3.5x Adjusted EBITDA target

• IPO proceeds used to de‐lever the balance sheet

Cost Control

• Focused on disciplined growth capital expenditures• Spending on only the highest return and

most strategically significant projects• Continuing to review the cost structure

• Targeting best practices• Revisiting current processes • Reviewing G&A expenses following

acquisition activity

Credit Facility Borrowings,

$110

Outstanding Letters of Credit,

$17

Unused Credit Facility Capacity,

$148

___________________________1. As of March 31, 2015. Availability based on $275mm of commitments

Fee Based, 47%

Fixed Margin, 10%

Variable Margin, 43%

Fee Based, 47%

Fixed Margin, 3%

Variable Margin, 49%

Stable Cash Flows

Business

26

2014 Adjusted EBITDA Mix(1)

___________________________1. Based on Adjusted EBITDA for the year ended December 31, 20142. Based on planned Adjusted EBITDA for the year ended December 31, 2015. Includes 1Q15 actual results

Contract Description

Crude Oil Pipelines & Storage

• Pipeline throughput fees• Crude Oil Storage fees

Refined Products Terminals • Throughput volume fees

Crude Oil & NGL Trucking • Fee based trucking for third parties

Fixed

Margin NGL Fixed Margin Product

Sales• NGL sales under fixed price contracts that are financially hedged

Crude Oil and NGL Supply & Logistics

• Typically back to back transactions at index‐based prices creating fee equivalent gross margin

NGL Variable Margin Product Sales

• NGL sales at market prices

Refined Products Sales • Product sales that vary with market prices

Fee Based

Varia

ble Margin

2015 Plan Adjusted EBITDA Mix(2)

Recent Financial Updates & Project Highlights

27

Q1 2015 RecapQ1 2015 Recap

• Adj. EBITDA growth vs. prior year (+79%) and sequentially (+26%1)• Q1 2015 distribution of $0.325/unit2, equivalent to MQD • Distributable cash flow of $13.3 mm, equates to 1.1x coverage• Strong volume growth across segments from new/existing customers

Recent Project

Highlights

Recent Project

Highlights

• Announced extension of Silver Dollar Pipeline into the core of the Midland Basin in February

• Executed agreement to connect Silver Dollar Pipeline to Magellan’s Longhorn Pipeline in April

• Completed immediately accretive $14.9 million acquisition of Southern Propane assets in May

2015 Guidance2015

Guidance

• Reiterated 2015 Adjusted EBITDA guidance of $50‐60 million• Remain on track for Republic Midstream drop down in 2H 2015• Forecast distribution coverage of 1.2x by Q4 2015

___________________________1. Excludes $2.1 million of non‐recurring charges in Q4 20142. Paid May 14, 2015 to unitholders of record on May 7, 2015. Note: Guidance includes Silver Dollar extension into the Midland Basin. Guidance excludes Silver

Dollar interconnection with Magellan’s Longhorn Pipeline and the recent Southern Propane acquisition

Financial Strategy

28

Long term contracts for our crude oil pipelines Refined products and NGL segments offer diversification in mature markets

but with considerable growth opportunities

Near‐term organic growth projects already being pursued in existing businesses

Strategic drop‐downs from JP Development and Republic Midstream could further bolster growth

Remain open to acquisition opportunities that are strategic to the platform

Revolver has ~$148 million in availability Target 3.5x leverage over the long‐term

Established risk management policies and procedures to monitor and manage the market risks associated with commodity prices, counterparty credit and interest rates

Commodity price exposure is minimized through fixed‐fee contracts or margin‐based arrangements

Maintain Stable Cash Flows

Comprehensive Risk Management

Commitment to Financial Flexibility

Deliver Consistent Distribution Growth

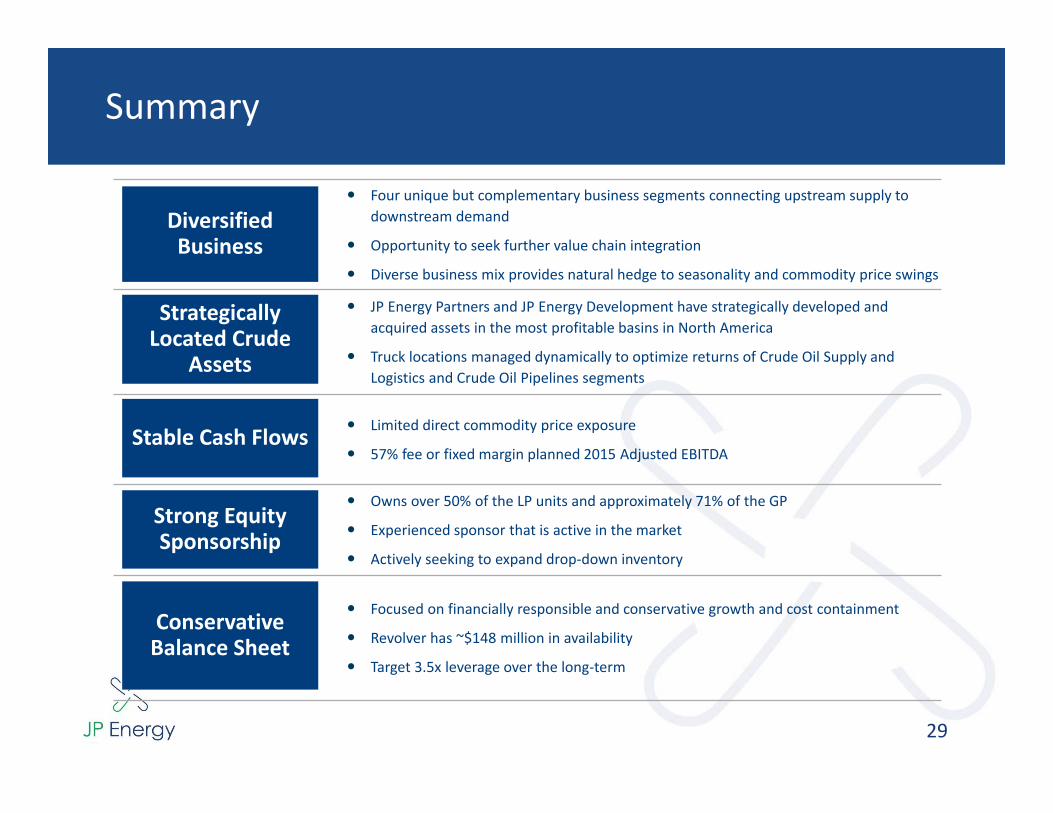

Summary

29

Four unique but complementary business segments connecting upstream supply to downstream demand

Opportunity to seek further value chain integration

Diverse business mix provides natural hedge to seasonality and commodity price swings

JP Energy Partners and JP Energy Development have strategically developed and acquired assets in the most profitable basins in North America

Truck locations managed dynamically to optimize returns of Crude Oil Supply and Logistics and Crude Oil Pipelines segments

Limited direct commodity price exposure

57% fee or fixed margin planned 2015 Adjusted EBITDA

Owns over 50% of the LP units and approximately 71% of the GP

Experienced sponsor that is active in the market

Actively seeking to expand drop‐down inventory

Focused on financially responsible and conservative growth and cost containment

Revolver has ~$148 million in availability

Target 3.5x leverage over the long‐term

Conservative Balance Sheet

Stable Cash Flows

Diversified Business

Strategically Located Crude

Assets

Strong Equity Sponsorship

Appendix

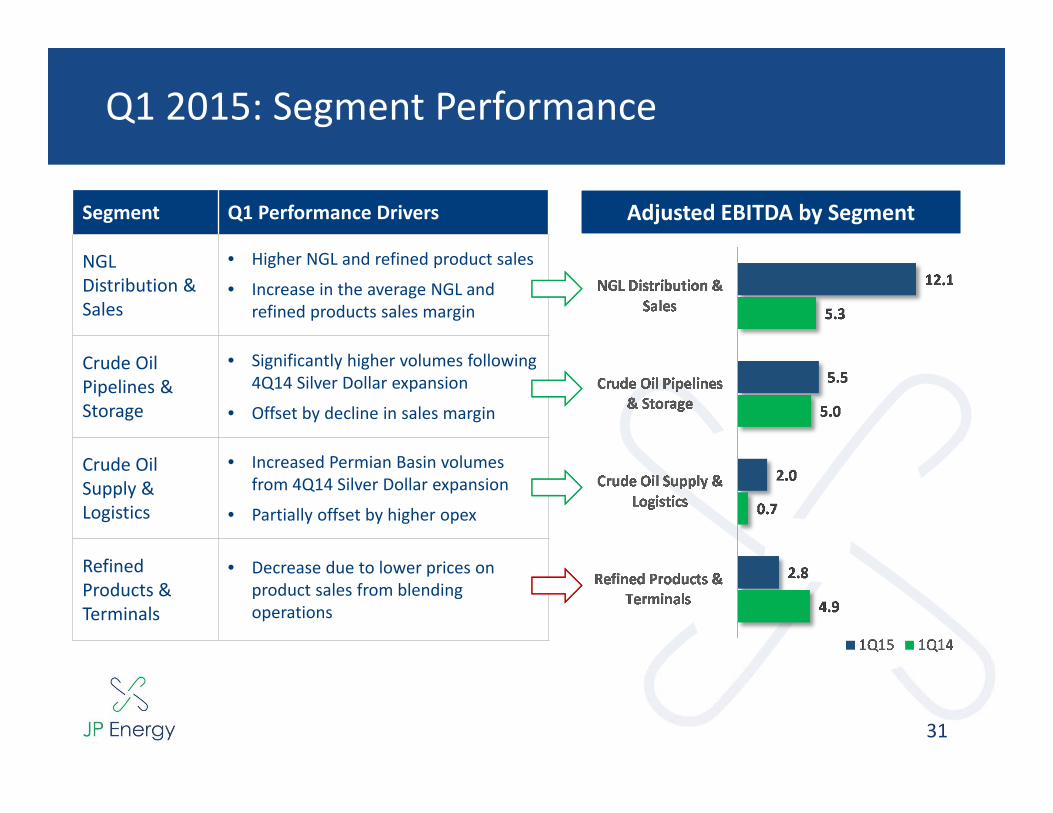

Q1 2015: Segment Performance

31

Adjusted EBITDA by SegmentAdjusted EBITDA by SegmentSegment Q1 Performance Drivers

NGL Distribution & Sales

• Higher NGL and refined product sales

• Increase in the average NGL and refined products sales margin

Crude Oil Pipelines & Storage

• Significantly higher volumes following 4Q14 Silver Dollar expansion

• Offset by decline in sales margin

Crude Oil Supply & Logistics

• Increased Permian Basin volumes from 4Q14 Silver Dollar expansion

• Partially offset by higher opex

Refined Products & Terminals

• Decrease due to lower prices on product sales from blending operations

Q1 2015: Operational Summary

32

Key Operational Data Q1 2015 Q1 2014 YoY % Change

Crude oil pipeline throughput (bpd) 28,329 18,129 +56%

Crude oil sales (bpd) 73,779 43,356 +70%

Terminal and storage throughput (bpd) 63,787 61,619 +4%

NGL and refined product sales (bpd) 6,524 5,619 +16%

Q1 2015: Balance Sheet & Liquidity

33

Strong Metrics, Access to CapitalStrong Metrics, Access to Capital

• Maintained conservative leverage of 2.9x

‒ Leverage ratio remains below peer average and JPEP long‐term target of ~3.5x

• $148 million unused credit facility capacity1

• Strong interest coverage of 5.0x

• Ample liquidity and balance sheet capacity to support capital needs

Available Liquidity ($mm)1Available Liquidity ($mm)1

Available debt capacity expected to fully support planned 2015 organic capex

Credit Facility Borrowings,

$110

Outstanding Letters of Credit,

$17

Unused Credit Facility Capacity,

$148

___________________________1. As of March 31, 2015

Non‐GAAP Reconciliation – Adjusted EBITDA

34

2015 2014

Segment Adjusted EBITDACrude oil pipelines and storage 5,476$ 4,968$ Crude oil supply and logistics 1,982 695 Refined products terminals and storage 2,822 4,853 NGLs distribution and sales 12,098 5,252 Discontinued operations - 79 Corporate and other (7,189) (7,349)

Total Adjusted EBITDA 15,189 8,498 Depreciation and amortization (11,339) (10,094) Interest expense (1,173) (3,259) Loss on extinguishment of debt - (1,634) Income tax (expense) benefit (22) 57 Loss on disposal of assets, net (130) (356) Unit-based compensation (431) (282) Total gain on commodity derivatives 771 135

3,192 (633) Non-cash inventory costing adjustment (2,915) - Transaction costs and other (2,477) (536) Discontinued operations - (484)

Net income (loss) 665$ (8,588)$

Three months ended March 31,

(in thousands)

Net cash (receipts) payments for commodity derivatives settled during the period

Non‐GAAP Reconciliation – Distributable Cash Flow

35

Three months ended

March 31, 2015

(in thousands)Net cash provided by operating activities 3,440$

Depreciation and amortization (11,339) Derivative valuation changes 4,008 Amortization of deferred financing costs (227) Unit-based compensation (431) Loss on disposal of assets (130) Bad debt expense (467) Other non-cash items (71) Changes in assets and liabilities 5,882

Net income 665$ Depreciation and amortization 11,339 Interest expense 1,173 Income tax expense 22 Loss on disposal of assets, net 130 Unit-based compensation 431 Total gain on commodity derivatives (771)

(3,192) Non-cash inventory costing adjustment 2,915 Transaction costs and other 2,477

Adjusted EBITDA 15,189$ Less: Cash interest paid, net of interest income 887 Maintenance capital expenditures 990

Distributable cash flow 13,312$ Less: Distributions 11,966

Amount in excess of distributions 1,346$ Distribution coverage 1.11x

Net cash receipts (payments) for commodity derivatives settled during the period

Consolidated Income Statement

36

Three Months Ended March 31,2015 2014

(in thousands, except unit and per unit data)REVENUES:

231,917$ 341,005$ Gathering, transportation and storage fees 6,951 8,096

54,185 63,801 3,108 2,663

Other revenues 3,125 3,102 Total revenues 299,286 418,667

COSTS AND EXPENSES:Cost of sales, excluding depreciation and amortization 254,890 382,889 Operating expense 16,611 16,153 General and administrative 14,475 12,633 Depreciation and amortization 11,339 10,094 Loss on disposal of assets, net 130 356

Total costs and expenses 297,445 422,125

OPERATING INCOME (LOSS) 1,841 (3,458)

OTHER INCOME (EXPENSE)Interest expense (1,173) (3,259) Loss on extinguishment of debt - (1,634) Other income, net 19 111

LOSS FROM CONTINUING OPERATIONS BEFORE INCOME TAXES 687 (8,240)

Income tax (expense) benefit (22) 57

INCOME (LOSS) FROM CONTINUING OPERATIONS 665 (8,183)

DISCONTINUED OPERATIONS- (405)

NET INCOME (LOSS) 665$ (8,588)$

Crude oil sales

NGL and refined product salesRefined products terminals and storage fees

Net loss from discontinued operations