NAMIBIA UNIVERSITY OF SCIENCE...

10

NAMIBIA UNIVERSITY OF SCIENCE AND TECHNOLOGY FACULTY OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE QUALIFICATION : BACHELOR OF TECHNOLOGY ACCOUNTING AND FINANCE QUALIFICATION CODE: 23BACF LEVEL: 7 COURSE CODE: TAX312S COURSE NAME: TAXATION 3B SESSION: JUNE 2018 PAPER: THEORY DURATION: 3 HOURS MARKS: 100 SECOND OPPORTUNITY EXAMINATION QUESTION PAPER EXAMINER(S) Mr. CHIKAMBI S J K MODERATOR: Mr. C. KOTZE. INSTRUCTIONS This question paper is made up of five (5) questions. Answer ALL the questions and in blue or black ink. Start each question on a new page in your answer booklet. Questions relating to this examination may be raised in the initial 30 minutes after the start of the paper. Thereafter, candidates must use their initiative to deal with any perceived error or ambiguities & any assumption made by the candidate should be clearly stated. pe Wo I Es THIS QUESTION PAPER CONSISTS OF 9 PAGES (Including this front page)

Transcript of NAMIBIA UNIVERSITY OF SCIENCE...

NAMIBIA UNIVERSITYOF SCIENCE AND TECHNOLOGY

FACULTY OF MANAGEMENTSCIENCES

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION : BACHELOR OF TECHNOLOGY ACCOUNTING AND FINANCE

QUALIFICATION CODE: 23BACF LEVEL: 7

COURSE CODE: TAX312S COURSE NAME: TAXATION 3B

SESSION: JUNE 2018 PAPER: THEORY

DURATION: 3 HOURS MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S) Mr. CHIKAMBI S J K

MODERATOR: Mr. C. KOTZE.

INSTRUCTIONS

This question paper is made up offive (5) questions.

AnswerALL the questions and in blue orblackink.

Start each question on a new pagein your answer booklet.

Questions relating to this examination may beraised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error or

ambiguities & any assumption madeby the candidate should be clearly stated.

peWoI

Es

THIS QUESTION PAPER CONSISTS OF 9 PAGES(Including this front page)

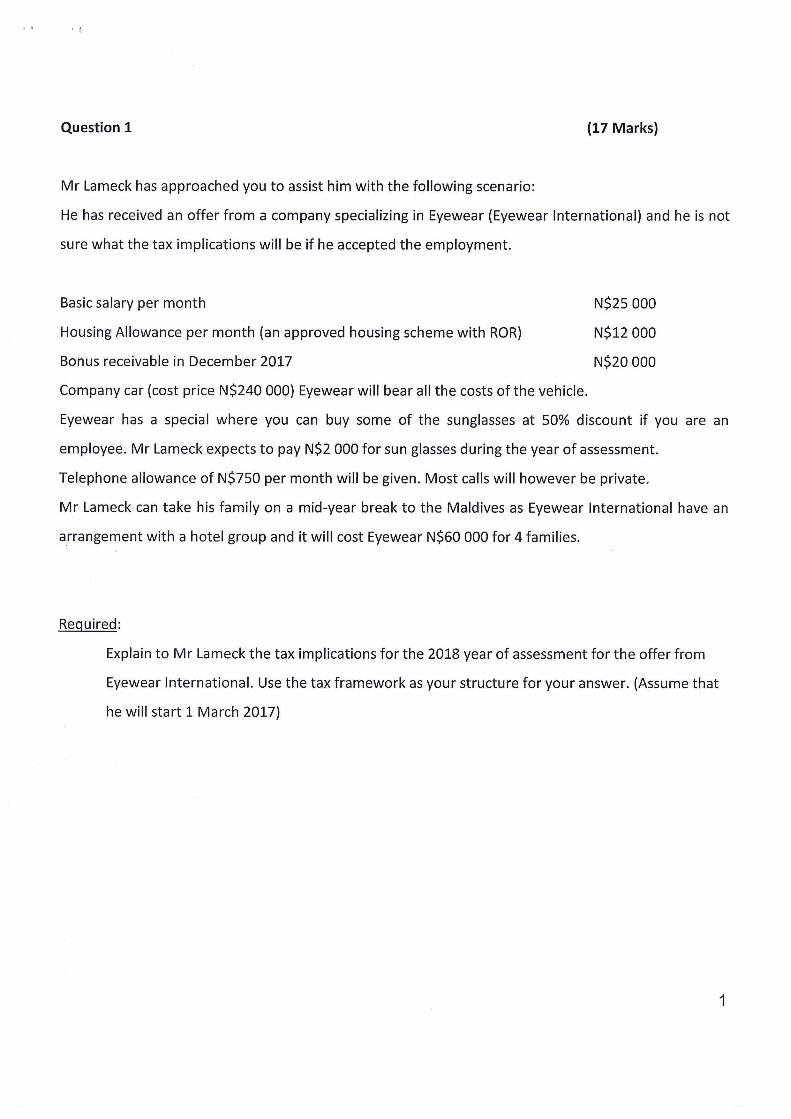

Question 1 (17 Marks)

Mr Lameck has approached youto assist him with the following scenario:

He has received an offer from a companyspecializing in Eyewear (EyewearInternational) and he is not

sure what the tax implicationswill be if he accepted the employment.

Basic salary per month NS25 000

Housing Allowance per month(an approved housing scheme with ROR) NS12 000

Bonusreceivable in December 2017 NS20 000

Companycar (cost price NS240 000) Eyewearwill bearall the costs of the vehicle.

Eyewear has a special where you can buy someof the sunglasses at 50% discount if you are an

employee. Mr Lameck expects to pay NS$2 000 for sun glasses during the year of assessment.

Telephoneallowance of NS750 per monthwill be given. Most calls will however be private.

Mr Lameck can take his family on a mid-year break to the Maldives as Eyewear International have an

arrangementwith a hotel group andit will cost Eyewear NS60 000 for4 families.

Required:

Explain to Mr Lameckthe tax implications for the 2018 year of assessmentfor the offer from

Eyewear International. Use the tax frameworkas your structure for your answer. (Assumethat

he will start 1 March 2017)

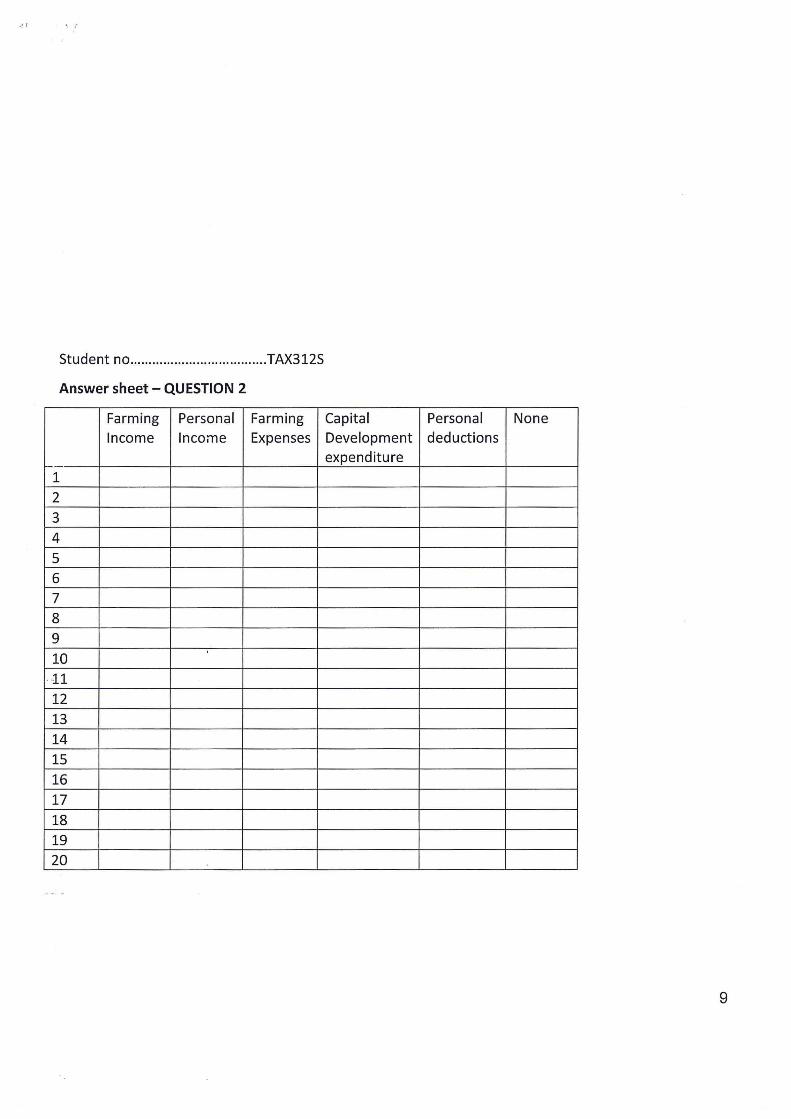

Question 2 (20 Marks)

Following are expenses and revenue incurred by Mr Mushonga a bona fide farmer whois also

employed at Agro Forest Cooperative. You are required to group these amounts in farming income,

personal income, farming expenses, capital development expenditure or personal deductions. If none

of the options are correct, you may choose “noneof the above”

Use the answersheet and only mark the correct answer with a X

Salaries paid to farm workers

Private consumption- livestock

Rations to farm workers- livestock

Irrigation system

Diesel engine for pumping waterfrom the borehole

New borehole pipes

Bookkeeping fees

Salary from Agro

se

SNao

oOFFSY

Building of anew dam

bh

Oo . Wagesincurred for the farm workers to build the dam

a bb . Removal oflivestock to Angola

hbN . Opening stock — livestock

bbvu . Birth of 20 calves.

. Removalof livestock from Rundu to Katima

PR

Oo

££

. New farm road

b a . House for farm worker

b SN . Fuel and Oil

bb

oo . Donation — cash to charity organization (certificate was obtained)

hb

WO . Government subsidy

N oO . Land rentals

Question 3 (8 Marks)

Read the following paragraph and fill in the missing words. Only indicate the missing words in your

answer book.

VATis levied in Namibia at either(1) .....% or (2).......%.

Whensupplies are not subject to VAT,it is called (3).......... Supplies.

VATis an (4)..........0 Tax which meansthat the tax is not levied on a person, but on a transaction.

VATof(5)......... is charged on fuel that is subject to the fuel levy.

There are 2 accounting bases on which VATcan be charged. Onebasis is the Payment bases and the

otheris the (6) ......... Basis. The one normally used in Namibiais the. (7)............. basis.

The VAT charged andpaid overto the Receiver of Revenueis called (8)...........VAT.

Question 4 (40 marks)

Maria and John, who are both married taxpayers, carry on business in Motorcycle parts. They practice

under the name “European Parts.” The partners share profits and losses equally.

Their bookkeeper has prepared the following income statement in respect of the year ended 28

February 2018.

Income statementfor the year ended 28 February 2018

Income

Grossprofit 810 000

Bad debts recovered(note 1) 3 500

Dividends accrued (note 2) 4 500

Interest accrued

-on fixed deposit account 3.225

821 225

Less: Expenditure

Annuities paid (note 3) 38 000

Bad debts (note1) 4500

Computer purchased (note 4) 36 000

Computeruser course costs (note 5) 2 500

Computer programs purchased 18 000

Donations made(note 9) 15 000

Goodwill paid (note 10) 50 000

Insurance paid (note 11) 16 500

Legal expenses(note 8) 1 500

Motorvehicle running expenses 17 550

Parking bay costs (note 7) 2 250

Premium paid (note 6) 7 500

Rental paid (note 6) 15 000

Retirement annuity find contributions

- Maria 15 000

- John 12 000

Staff salaries and wages 72 000

Shares purchased (note 2) 60 000

Stationery and printing 2 450

Sundry deductible expenses 16 649

Taxation paid (provisional payment)

- Maria 40 000

- John 27 500

469 899

Net profit 351 326

Net profit — Maria 175 663

Net profit — John 175 663

351 326

Notes:

1. The bad debts recovered of NS3 500 wererecovered from a former debtor of Maria’s when she had

been trading on her own,twoyearspreviously. Of the bad debts of NS4 500, an amount of N$2 000

relates to debts that the partners took over whenthey purchased the business from Mr. Asia. The

balance of the bad debtsis in respect of present clients who havefailed to pay their accounts.

2. During the 2018 year of assessmentthe partners decided to invest their surplus cash funds and they

purchased 6 000 sharesin Trustline, a Namibian registered company, at N$10 a share. The company

paid a dividend of 75 cents a share on 31 December2017.

3. The following annuities were paid during the year to dependants of deceased former employees:

° The widowof Mr. Honda andher twochildren 14 500

e The widow of Mr. Kawasaki, a former messenger 23 500

38 000

It is not the policy of the partners to make payments of this nature. Yet these payments were madein

orderto assist the recipients whoareall in poor financial circumstances.

4. No depreciation has been provided in the income statementin respect of the computer, which was

purchased and broughtinto use on 1 May 2017

5. In order to keep up to date with new developments, Maria attended a computer course to introduce

latest technology in motorcycle parts in Johannesburg. The expenses incurred by Maria were paid by

the partnership. They wereasfollows:

e Course costs 1 000

e Travelling expenses — incurred 450

¢ Hotel and accommodation 1050

2 500

6. On 1 March 2017, the partners had entered into an agreement with a taxpayerto lease office

premises togetherwith the vacant land situated adjacent to the office premises. The lease agreement

which wasfor ten years provided for a premium of NS$7 500to be paid by the lessee at the

commencementof the lease, a monthly rental of NS1 250 to be paid by the lesseefor the office and

contained an improvement clause wherebythe partners (the lessees) must effect improvements on

the property to the value of NS88 500. The leased office premises were used as from 1 March 2017

while the improved section came into use on 1 May 2017 once the improvements were completed at

the said cost on 30 April 2017.

7. After the improvements had been completed, the remainderof the land wascleared and turnedinto

a parking area at a cost to the partners of NS22 500. The accountant howeverconfirmed that NS22 500

is the correct amountpaid for the parking area.

8. An examination of the legal charges revealed that NS500 wasfor drawing up the lease agreementin

respect of the office premises and the land leased by the partnership, and N$1 000 wasfor the

collection of outstanding fees.

9, During the 2018-year of assessment the partners made one donation. An amount of N$15 000 was

donated to the N U ST to establish a bursary to be granted to a promising accountancy student whois

in need offinancial assistance. (A tax certificate was obtained from N U ST)

10. Goodwill paid of NS50 000is in respect of the final instalment due to previous ownerin respect

of the purchase consideration paid to take over the business.

11. Insurance premiumspaid during the year were in respect of the following policies:

e Professional indemnity policy 9 000

e Partners survivorship policy 7500

16 500

12. Otherrelative partnership information: Maria John

Salaries payable 87 500 87 500

Interest on capital 12 000 9000

Drawings 75 000 54 000

YOU ARE REQUIREDTOcalculate the taxable incomeof each partner for the 2018 year of assessment.

Start your answerwith the net profit of NS351 326

You mustindicate the reason for each adjustment that is made to the net profit to earn a mark for the

adjustment. If no adjustmentis required for a particular amount, you needto record the description of

the amount to earn a markfor such a expenseandindicate it with a dash - ).

Question 5 (15 marks)

5.1 Pleaselist the requirements of the general deduction formula. (6)

5.2 Namethethree ways through which payment of normal taxliability takes place (3)

5.3 Whatfactors will play a role in the consideration if an item is of Capital of Nature. (6)

END OF PAPER

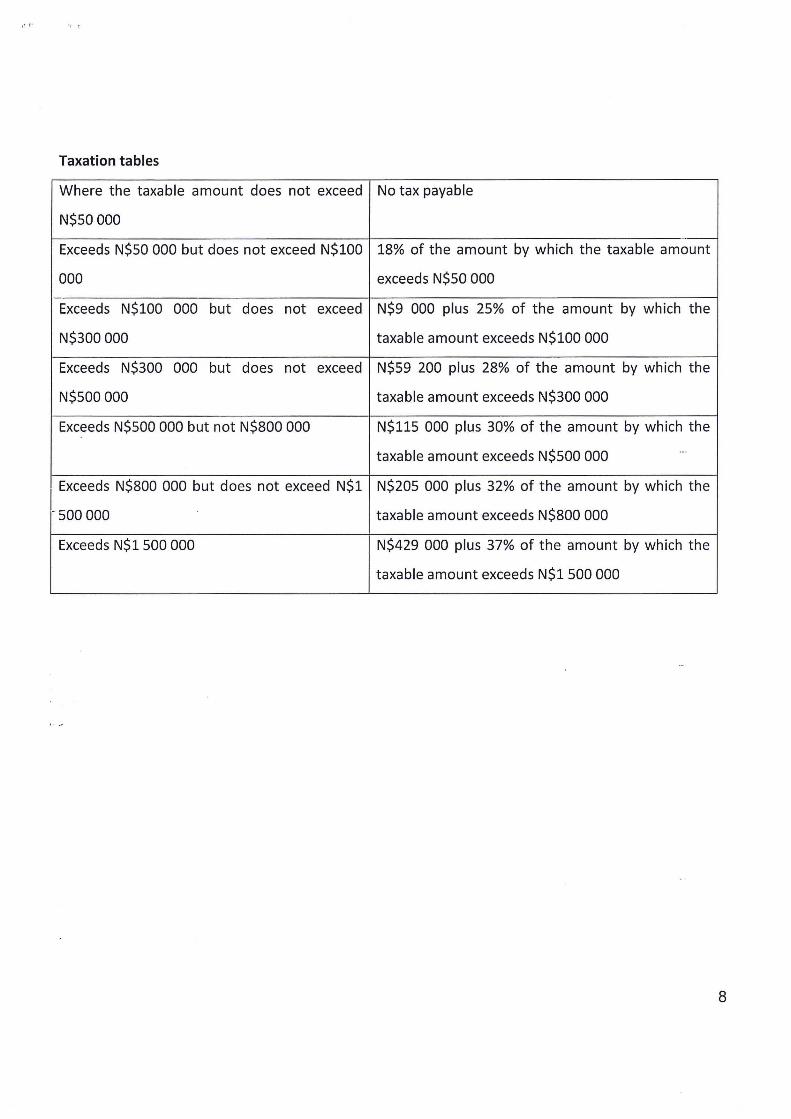

Taxation tables

Where the taxable amount does not exceed

NS50 000

No tax payable

Exceeds NS50 000 but does not exceed NS100

000

18% of the amount by which the taxable amount

exceeds NS50 000

Exceeds NS100 000 but does not exceed

NS300 000

NS9 000 plus 25% of the amount by which the

taxable amount exceeds N$100 000

Exceeds NS300 000 but does not exceed

NS500 000

NS59 200 plus 28% of the amount by which the

taxable amount exceeds NS300 000

Exceeds NS500 000 but not NS800 000 N$115 000 plus 30% of the amount by which the

taxable amount exceeds NS500 000

Exceeds NS800 000 but does not exceed NS1

- 500 000

NS205 000 plus 32% of the amount by which the

taxable amount exceeds NS800 000 Exceeds NS1 500 000 NS$429 000 plus 37% of the amount by which the

taxable amount exceeds NS1 500 000

STUCGENT NO...cece ceeeescesssseeeseeceeeeesTAX312S

Answersheet — QUESTION 2

Farming Personal Farming Capital Personal None

Income Income Expenses Development deductions

enditure

1

2

]4

5

6

7

8

9

NiplelPlEleElel

elpils/E

O/WO/WOINID/MIHBI/WIN]R|O

![OF SCIENCE ANDTECHNOLOGYexampapers.nust.na/greenstone3/sites/localsite/collect... · 2019-02-14 · (d) Namethe2 autoregressive modelswhichare rationalisations ofthe Koyckmodel? [2]](https://static.fdocuments.us/doc/165x107/5e69207fde429478f829a9eb/of-science-and-2019-02-14-d-namethe2-autoregressive-modelswhichare-rationalisations.jpg)

![[Question2]yasril syaf](https://static.fdocuments.us/doc/165x107/5559d0c2d8b42a93208b4b67/question2yasril-syaf.jpg)

![NAMIBIA UNIVERSITY OF SCIENCE ANDTECHNOLOGYexampapers.nust.na/greenstone3/sites/localsite/collect... · 2020-04-08 · Question1 [25 marks] a) Adepartmentstoreis consideringadoptinga](https://static.fdocuments.us/doc/165x107/5f07f4777e708231d41f9914/namibia-university-of-science-and-2020-04-08-question1-25-marks-a-adepartmentstoreis.jpg)