NAMA - Three years on

32

NAMA - Three years on Brendan McDonagh Chief Executive Officer Wednesday 17 April 2013 www.nama.ie Seminar organised by the Embassy of Ireland in Madrid together with the SIBN

Transcript of NAMA - Three years on

NAMA - Three years on

Brendan McDonagh

Chief Executive Officer

Wednesday 17 April 2013

www.nama.ie

Seminar organised by the Embassy of Ireland in Madrid together with the SIBN

2 2

Response to Irish banking crisis

1 • Irish Government guarantee for banks liabilities of €440 bn - September 2008.

2 • External examination of loan books of all institutions which partook in the

guarantee scheme in October/November 2008.

3 • Recapitalisation of certain financial institutions – December 2008 onwards.

4

• Nationalisation of Anglo Irish Bank - January 2009

5

• Review of options on how to deal with impaired assets – February/March 2009

• Plan to establish NAMA as Asset Management Agency – April 2009

Key milestones

April 2009: Plan to establish NAMA announced

July 2009: Draft Legislation published

September 2009: Legislation introduced into Parliament

November 2009: NAMA Act passed into law

December 2009: Board and CEO appointed

February 2010: EU Commission approval for NAMA scheme under State Aid regime

3

4

EU Approval of NAMA

February 2010

Transfer of the initial largest borrower exposures across

all institutions commenced March 2010

Minister’s decision to exclude sub

€20m loans in AIB and BOI and to

expedite transfers September 2010

Total of €74bn assets

transferred at a cost of €31.8bn (57% discount) October 2011

The NAMA Timetable 2010 / 2011

Preparatory work

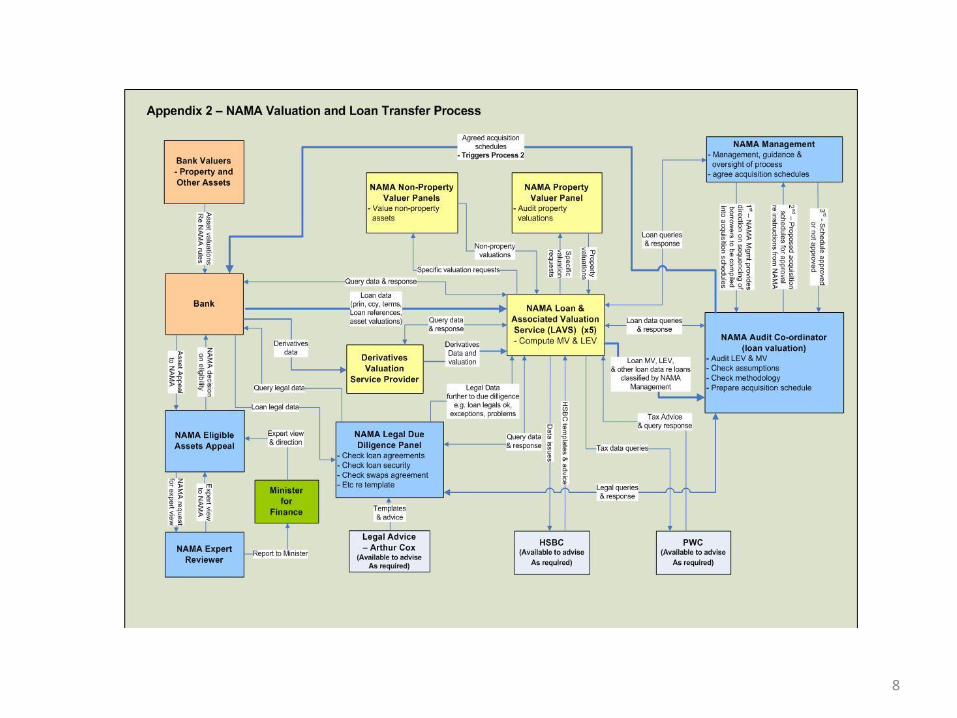

• Appointed a firm to advise on loan valuation methodology

• Set up panel of legal firms – legal due diligence on loans

• Set up panel of property firms to audit and review property valuations

• Set up panel of firms to carry out loan valuations

• Appointed a firm to carry out valuation of derivative transactions

• Appointed a firm to act as Audit Co-ordinator – assurance of consistency and rigour.

NAMA Loan valuation and due diligence

5

Preparatory work (contd.)

• Discussions about eligibility criteria and their implications for the volume of transfers – Autumn 2009. (A debtor eligible by reference to Bank A only but NAMA acquires Bank B and Bank C exposures also)

• Lists of loans likely to be eligible – December 2009

• Five loan valuers assigned to five PIs – January 2010

• Discussions about valuation methodology and due diligence arrangements – early 2010

• Policy guidelines on valuation issues

• First transfers – March 2010.

• Discussions on loan administration arrangements – Master Servicer selected in late 2009.

NAMA engagement

with Participating Institutions

(PI’s)

6

Preparatory work (contd.)

• EU Commission (with D/Finance)

• Eurostat/Central Statistics Office

• UK Treasury/Bank of England/UK FSA

• Non-NAMA banks

• Various lobby groups – banking, construction, etc.

• Potential advisors and other service providers

• Potential investors

• Prospective debtors

NAMA engagement with other

stakeholders

7

8

NAMA €31.8bn

NAMA €32bn

Liquidity to 5 Banks

Total Loss of Liquidity by Irish NAMA banks

since 2008 est. €100bn

NAMA €31.8bn

NAMA provided €31.8bn liquidity to Irish Banking System – it could only ever solve part of the estimated €100bn liquidity lost by banking system since 2008 – ECB reliance now less than €60bn

9

NAMA’s Liquidity Injection into Banks

50% Act Like a Bank

50% Intensive

Asset Management

10

NAMA: What is it?

NAMA Board

Minister For Finance

CEO NAMA

Audit Committee

Risk Committee

Finance and Operating Committee

Credit Committee

Northern Ireland Advisory Committee

Planning Advisory Committee

NTMA Services: IT/Treasury/Market Risk/HR/Office

Services

Head of Asset Management

Head of Asset

Recovery

CFO

Head of Strategy and Communication

Head of Legal

NAMA Organisation Structure

Head of Audit and Risk Head of Treasury Tax Financial

Control Operations

Systems

Board Chairman

11

NAMA Recruitment Over 2,000 CVs received within six months of announcement

12

7

54

100

145

194

217

0

50

100

150

200

250

Jan

-10

Feb

-10

Mar

-10

Ap

r-1

0

May

-10

Jun

-10

Jul-

10

Au

g-1

0

Sep

-10

Oct

-10

No

v-1

0

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

Dec

-11

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

13

189 Debtors

€61bn Par debt

Intensively managed by NAMA

Key credit decisions and relationship management

carried out by NAMA multi-disciplinary teams

Loan administration performed by Participating

Institutions

586 Debtors

€13bn Par debt

Relationship management performed by the Participating Institutions NAMA Units through NAMA

Delegated Authority

NAMA has a presence in each of the bank units overseeing the management of the portfolio

Relationship management and loan administration carried out by Participating Institutions within NAMA

policy & procedures

NAMA paid €31.8bn to acquire 12,000 loans to 775 debtor groups. These loans were secured by more than 10,000 properties containing over 56,000 units

NAMA Portfolio

14

Location of Irish Property – end 2012

94% in Dublin and contiguous counties plus Cork, Galway and Limerick

Dublin 67%

Dublin Commuter Belt

11%

Cork 10%

Galway 4%

Limerick 2% Rest of ROI

6%

0.00% 0.10% 0.20% 0.30% 0.40% 0.50% 0.60% 0.70%

Sligo

Waterford

Wexford

Westmeath

Carlow

Clare

Laois

Tipperary

Kerry

Donegal

Mayo

Kilkenny

Offaly

Roscommon

Cavan

Leitrim

Longford

Monaghan

15

Location of UK Property end 2012

London 64%

Midlands 13%

Wales & South West 3%

Scotland & North 11%

South East 9%

0%

UK Portfolio split by Region

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

Midlands

South East

North West

Scotland

West Midlands

South West

North East

Wales

Rest of UK Portfolio split by Locality

16 16

1 • Each borrower was asked to prepare a realistic and concise Business Plan

2 • NAMA assessed each Business Plan to evaluate whether it is realistic

3 • NAMA met major borrowers to discuss proposed plans

4

• If no agreement reached, or the debtor does not wish to cooperate with NAMA, they were asked to repay debts in full and, failing this, enforcement action was considered. NAMA has declined to appoint in a significant number of other cases

5 • Focus now is on actively implementing the approved strategy for each debtor

Debtor Business Plan Process – Work Completed

17

Consensual Connection

Non - Consensual Connection

Borrower sells real estate assets in accordance with

Business Plan

Enforce

No Enforcement

Sell single assets

Create portfolios of assets (sector /

location) for sale /refinance

Sell entire connection’s loans as a portfolio

Sell standalone, non recourse loans

Complete value add strategies then sell

Fixed Charge Receiver /

Administrator Holds

NAMA Owns

NAMA’s Approach to Debtor Management

NAMA Debtor Loan Restructure

NAMA pursues one of five restructure options with debtors: (i) Full restructuring (new security and loan documentation) (ii) Limited Restructuring (existing security and legal documentation) (iii) Letter of support (iv) Disposal (v) Enforcement Full restructuring is typically progressed with compliant debtors and increases the potential monetising options for future recovery/disposal.

18

Debtor Debt Restructuring

19

Cash Generation to 28/02/2013

Disposals €7bn & Non-Disposals €4bn since inception (35 MONTHS)

20

Cash Generation vs. Bond Repayment Target

• Total cash inflows of €11bn generated since inception

• 2010: €1.0bn

• 2011: €5.1bn

• 2012: €4.5bn

• 2013: €0.4bn

• Bond redemption target of €7.5bn by end 2013 – Troika target

• To date Bond Redemptions of €4.75bn

• Remaining redemptions

• 2013: €2.75bn

21

Location Value €Bn

Dublin 0.5

Rest of ROI 0.3

London 4.3

Rest of UK 1.1

N.I 0.1

EU, USA and Other 0.7

Total 7.0

Disposals since Inception to end 2012

Dublin 0.5 7%

Rest of ROI 0.3 4%

London 4.3

62%

Rest of UK 1.1

16%

N.I 0.1 1%

EU, USA and Other 0.7

10%

Sales Proceeds Received by Asset Location

22

A significant amount of work is done behind the scenes to deliver these results involving day to day

intensive management

• 775 Business Plan reviews completed by end 2012 which are reviewed quarterly by NAMA

• 3,900 asset sales transactions

• €100m per month recurring income on portfolio despite €7bn of asset sales

• 20,000 credit decisions made since inception. €1bn new money drawdowns

• Response times improved despite increasing volumes

4.6 4.3 4.7 4.7 4.9 4.6 4.4

1.00

3.00

5.00

7.00

June July Aug Sept Oct Nov Dec

Average Turnaround Working Days in NAMA

How the €11bn cash was achieved

• NAMA has €780m of enforced property listed for sale on its website and is pursuing sales in all markets

• There is a further €750m of property for sale in the Irish Market by NAMA debtors

• Significant individual transactions in recent months e.g. Millennium Park in Naas for Kerry Group creating 1,000 jobs, promoting SDZ in Dublin Docklands, finish off 2 large apartment blocks in South Dublin €25m capex – strong proven rental market.

• As the economy picks up and as finance becomes available NAMA will increase the flow of Irish property to the market

• It does not make sense for NAMA to flood the market – we were established with a ten year horizon – orderly and phased disposal

23

NAMA Actively Selling - But Responsibly

• Cautious optimism for the medium term

• Irish property market will probably not recover in a homogeneous way

• Recovery will be in main urban centres first and investment grade properties

• Good for NAMA given the urban centric location(94%) and quality of the Irish portfolio

• Renewed interest in NAMA’s Irish property portfolio – perception the country is improving. Emerging demand in some key areas, interest in NAMA Vendor Finance and take up of NAMA Deferred Mortgage offerings

24

Market Outlook

• Deferred Residential Mortgage Payment Initiative – Offers price protection to residential buyers. Extended in March 2013 to include 400 family homes nationally. Sales agreed to date of €21m on 115 units. Extending on a phased basis up to a maximum of 750 units

• Social Housing - Offers long-term leasing options to local authorities. More than 4,000 units identified (local authorities determine suitability). NAMA facilitates direct engagement between Local Authorities and Debtors (or Receivers) and Housing Agency.

• NAMA Development capital – Investing in assets to enhance value. NAMA committed to €2bn investment in Irish assets in May 2012 - planning resolution takes time everywhere!

• NAMA Vendor Finance - Offers medium-term finance to purchasers of commercial assets or loans with €2bn in vendor finance available to prospective purchasers

25

NAMA Strategic Initiatives

• REITs – Real Estate Investment Funds – another vehicle for attracting capital to the Irish market. NAMA considering its role.

• Asset Management – NAMA established a dedicated team whose brief includes the appraisal, financing and delivery of development projects in Ireland and Britain. Delivery mechanisms will include joint ventures.

• Rent Abatements – 212 applications for rent abatement approved (97%) with an aggregate value of €13.5m per annum

26

Strategic Initiatives (continued)

• NAMA Debtors have an interest in less than 15% of hotels in Ireland, i.e. in 118 of approximately 900 hotels

• NAMA Debtors have an interest in less than 5% of golf courses in Ireland, i.e. in 20 of approximately 400 golf clubs (17 golf courses are attached to 4/5 star hotels)

• NAMA Debtors have an interest in about 10% of unfinished housing estates in Ireland, i.e. in 160 out of the 1,500 worst unfinished estates

• NAMA actively engages with local authorities and is committed to resolving the issues caused by unfinished housing estates, development levies, planning etc

• NAMA supports debtors who directly employ an estimated 10,000 people, providing for appropriate current and capital expenditure

27

Debunking the NAMA Myths

• NAMA Senior Debt redemption is on target. Cumulative redemptions €4.75bn have been made to date and an additional €2.75bn will be repaid by the end of 2013 – meeting the €7.5bn target that is key for Troika

• Total cash flows of €11bn have been generated since March 2010, and NAMA currently

has €4bn of cash on hand • Non-disposal cash flows of approximately €100m per month are being generated, in

addition to sales proceeds

• NAMA has a low cost base

• The €4bn in funding between development capital and vendor financing has to come from NAMA resources

• NAMA continues to generate Operating Profits after Impairment charges, despite unfavourable property price market movements since end 2009

28

Financial KPI’s

29

• Continue to build significant organisational capability, while running a business that

has delivered outstanding results

• Work-out strategy and platform in place for debtor connections

• Strategy implementation and delivering key asset management enhancement and

completion of projects

• Property Portfolio is relatively well located which in time should facilitate orderly

disposal of assets

• NAMA has independent funding availability

NAMA – 2013 and Beyond

• Continuing difficult Irish market with other institutions deleveraging

• Market liquidity

• Recent IBRC liquidation

• Status as a public body means less flexibility than banks

• Staff retention

30

NAMA faces a number of key challenges

Commercial Book Consumer Book

While the initial portfolio data shows 5 different loan type segments, when considering portfolio management options there are 2 distinct categories

evident:-

Commercial Book:- 85% of the NEW portfolio.

Commercial – Leisure is likely to be hotels & pubs, remainder a mixture of development & investment of offices/shopping centres/industrial

Residential - development and commercial investment activities.

Business Banking - SME/cashflow business

Consumer Book:- 15% of the NEW portfolio.

Mortgage & Personal loans grouped together as both personal lending products governed by Central Bank codes of conducts.

31

€bn Commercial Residential

Business

Banking Mortgages Other

Leisure Industrial Mixed Retail Office Other

Sub

Total Development Investment Sub Total PDH Buy to Let Personal

Fund

Investment

Portfolio

Total

RoI 2.16 0.24 0.70 3.20 2.98 1.10 0.33 0.51 2.85 1.42 0.41 2.07 0.37

UK 3.19 0.41 0.77 1.98 1.28 0.30 0.13 0.36 0 0 0 0.02 0

US 0 0 0.10 0.08 0.20 0 0.11 0 0 0 0 0.003 0

Total 5.35 0.65 1.57 5.26 4.46 1.40 18.70 0.57 0.87 1.64 2.85 1.42 0.41 2.09 0.37 27.1

Impairment -6.4 -0.70 -1.78 -0.38 -0.12 -1.19 -0.21 -10.78

Net 12.3 0.94 1.07 1.04 0.30 0.9 0.16 16.71

Provision % 34% 43% 62% 28% 28% 57% 57% 39%

Non NAMA Portfolio @ 30th June 2012

IBRC Portfolio at 30/06/2012

• NAMA is financially robust meeting every key target - cash, profitability

• We are part of the solution in the property market and tailoring strategies

• NAMA will make funding available for development projects with commercial

rationale

• A tremendous amount achieved in less than 3 years

• Next part – IBRC loan book integration?

32

Summary – 3 years on