N952-00-007 13 July 1998 Copyright © 1998 Oliver, Wyman & Company London New York Paris Frankfurt...

31

N952-00-007 13 July 1998 Copyright © 1998 Oliver, Wyman & Company London New York Paris Frankfurt Madrid Toronto Singapore Confidential & Proprietary DYNAMIC FINANCIAL ANALYSIS SEMINAR

-

Upload

cornelius-carson -

Category

Documents

-

view

214 -

download

0

Transcript of N952-00-007 13 July 1998 Copyright © 1998 Oliver, Wyman & Company London New York Paris Frankfurt...

N952-00-007

13 July 1998

Copyright © 1998 Oliver, Wyman & CompanyLondon New York Paris Frankfurt Madrid Toronto Singapore

Confidential & Proprietary

DYNAMIC FINANCIAL ANALYSIS SEMINAR

N952-00-007

CONFIDENTIALITY

The financial services industry is extremely competitive. The confidentiality of companies’ plans and data is obviously critical. Oliver, Wyman & Company will protect the confidentiality of all such client information.

Similarly, management consulting is a competitive business. We view our approaches and insights as proprietary and therefore look to our clients to protect Oliver, Wyman & Company’s interests in our presentations, methodologies and analytical techniques. Under no circumstances should this material be shared with any third party without the written consent of Oliver, Wyman & Company.

Copyright © 1998 Oliver, Wyman & Company

N952-00-007

I.DFA DRIVES CAPITAL MANAGEMENT

II.DFA UNCOVERS SKEWS IN RISK-ADJUSTED PROFITABILITY

III. DFA SUPPORTS BUSINESS MODEL EVOLUTION

IV. DFA CAN INTEGRATE MODELS DEVELOPED FOR BANKING

INTRODUCTION

Oliver, Wyman & CompanyN952-00-007

– 4 –

INTRODUCTION

Oliver, Wyman & CompanyN952-00-007

– 5 –

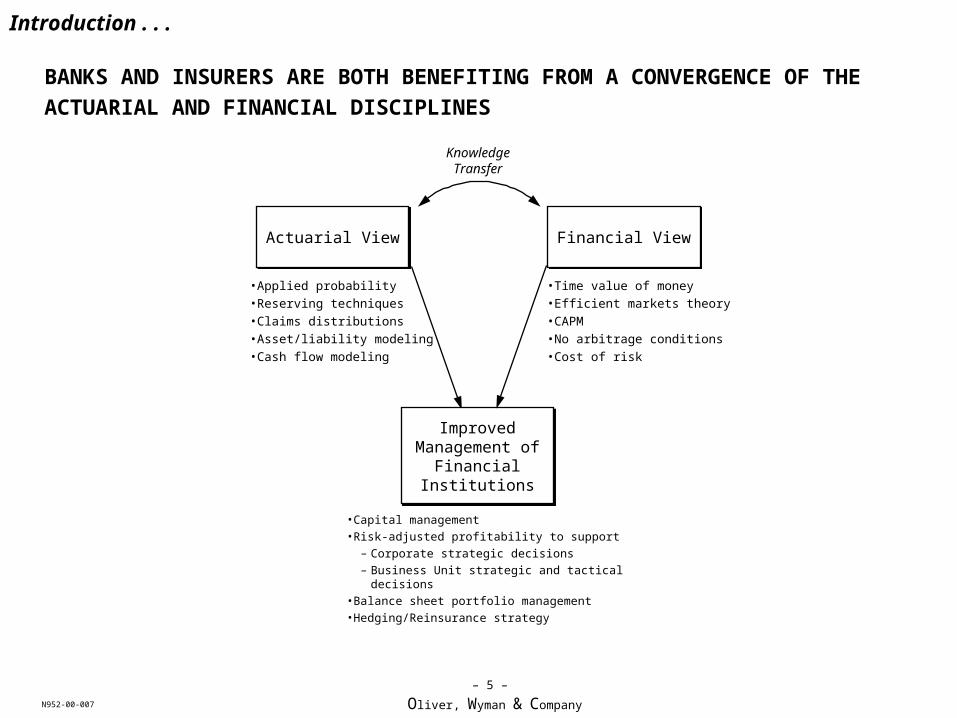

BANKS AND INSURERS ARE BOTH BENEFITING FROM A CONVERGENCE OF THE

ACTUARIAL AND FINANCIAL DISCIPLINES

KnowledgeTransfer

Introduction . . .

Actuarial ViewActuarial View Financial ViewFinancial View

Improved Management of

Financial Institutions

Improved Management of

Financial Institutions

• Applied probability• Reserving techniques• Claims distributions• Asset/liability modeling• Cash flow modeling

• Time value of money• Efficient markets theory• CAPM• No arbitrage conditions• Cost of risk

• Capital management• Risk-adjusted profitability to support

– Corporate strategic decisions– Business Unit strategic and tactical decisions

• Balance sheet portfolio management• Hedging/Reinsurance strategy

Oliver, Wyman & CompanyN952-00-007

– 6 –

TODAY WE DISCUSS HOW DFA HAS SUPPORTED DECISIONS IN BOTH BANKING

AND LIFE INSURANCE, AND DISCUSS ITS APPLICABILITY TO P&C INSURANCE

Introduction . . .

Applications (Decisions)

Applications (Decisions)

ReportsReports

MethodologiesMethodologies SystemsSystemsDataData

Oliver, Wyman & CompanyN952-00-007

– 7 –

I. DFA DRIVES CAPITAL MANAGEMENT

Oliver, Wyman & CompanyN952-00-007

– 8 –

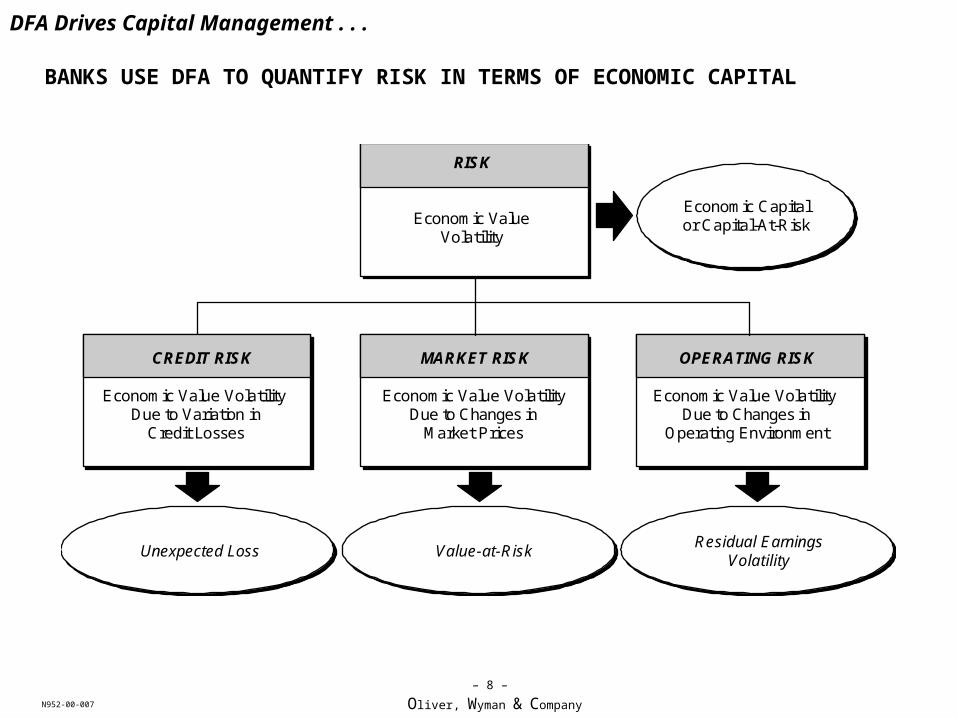

BANKS USE DFA TO QUANTIFY RISK IN TERMS OF ECONOMIC CAPITAL

DFA Drives Capital Management . . .

Economic Capitalor Capital-At-Risk

RISK

Economic ValueVolatility

CREDIT RISK

Unexpected Loss

MARKET RISK

Value-at-Risk

OPERATING RISK

Residual EarningsVolatility

Economic Value Volatility Due to Variation in

Credit Losses

Economic Value VolatilityDue to Changes in

Market Prices

Economic Value Volatility Due to Changes in

Operating Environment

Oliver, Wyman & CompanyN952-00-007

– 9 –

ECONOMIC CAPITAL MEASURES THE CAPITAL REQUIRED TO ACHIEVE A TARGET

SOLVENCY STANDARD

DFA Drives Capital Management . . .

ExpectedLoss

Probability

Losses ($)

Economic Capital for

“AAA” solvency standard

Solvency Standard

A AA AAA

.07% .03% .01%

Oliver, Wyman & CompanyN952-00-007

– 10 –

Capital You Have

COMPARING ECONOMIC CAPITAL TO AVAILABLE CAPITAL PROVIDES A VIEW OF

CAPITAL ADEQUACY

A AA AAA Available Capital

$ BN

Solvency Standard 7 bp 3 bp 1 bp

Corresponding S&P Rating A AA AAA

Capital You Need

DFA Drives Capital Management . . .

ExcessCapital

Oliver, Wyman & CompanyN952-00-007

– 11 –

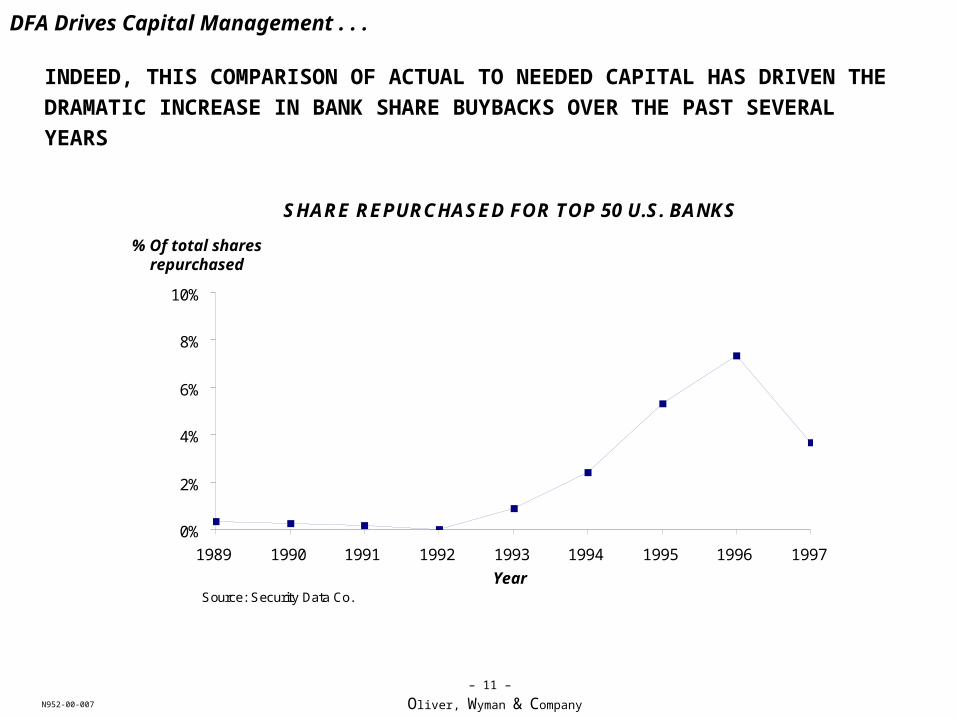

INDEED, THIS COMPARISON OF ACTUAL TO NEEDED CAPITAL HAS DRIVEN THE

DRAMATIC INCREASE IN BANK SHARE BUYBACKS OVER THE PAST SEVERAL

YEARS

DFA Drives Capital Management . . .

SHARE REPURCHASED FOR TOP 50 U.S. BANKS

0%

2%

4%

6%

8%

10%

1989 1990 1991 1992 1993 1994 1995 1996 1997

YearSource: Security Data Co.

% Of total shares repurchased

Year

Oliver, Wyman & CompanyN952-00-007

– 12 –

THIS SERVES AS AN INPUT TO A DISCIPLINED CAPITAL MANAGEMENT PROCESS

DFA Drives Capital Management . . .

1. Formulate capital investment plan to determine a business mix that maximizes the Bank’s long-term value to its shareholders based upon evaluation of the risk, return and growth characteristics of available opportunities

2. Determine target solvency standard given the mix of business activities implicit in the investment plan

3. Align capital structure to be consistent with #1 and #2 by taking appropriate actions (capital issuance, buyback, etc.)

4. Set risk limits and targets that reflect the investment plan and ensure compliance with the target rating

5. Set business unit RAROC and growth targets and the investment consequences of achieving (or not achieving) them

6. Measure performance by monitoring actual RAROC, capital usage, and growth against targets and limits

Oliver, Wyman & CompanyN952-00-007

– 13 –

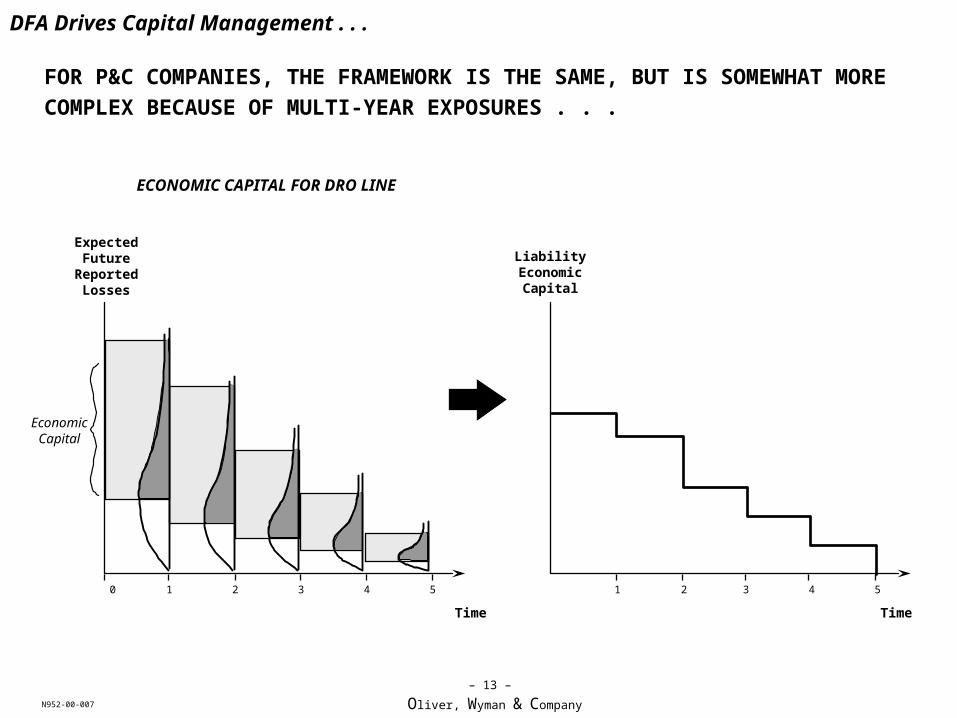

FOR P&C COMPANIES, THE FRAMEWORK IS THE SAME, BUT IS SOMEWHAT MORE

COMPLEX BECAUSE OF MULTI-YEAR EXPOSURES . . .

Economic Capital

Time

0 1 2 3 4 5

Expected Future

ReportedLosses

Liability Economic

Capital

Time

1 2 3 4 5

ECONOMIC CAPITAL FOR DRO LINE

DFA Drives Capital Management . . .

Oliver, Wyman & CompanyN952-00-007

– 14 –

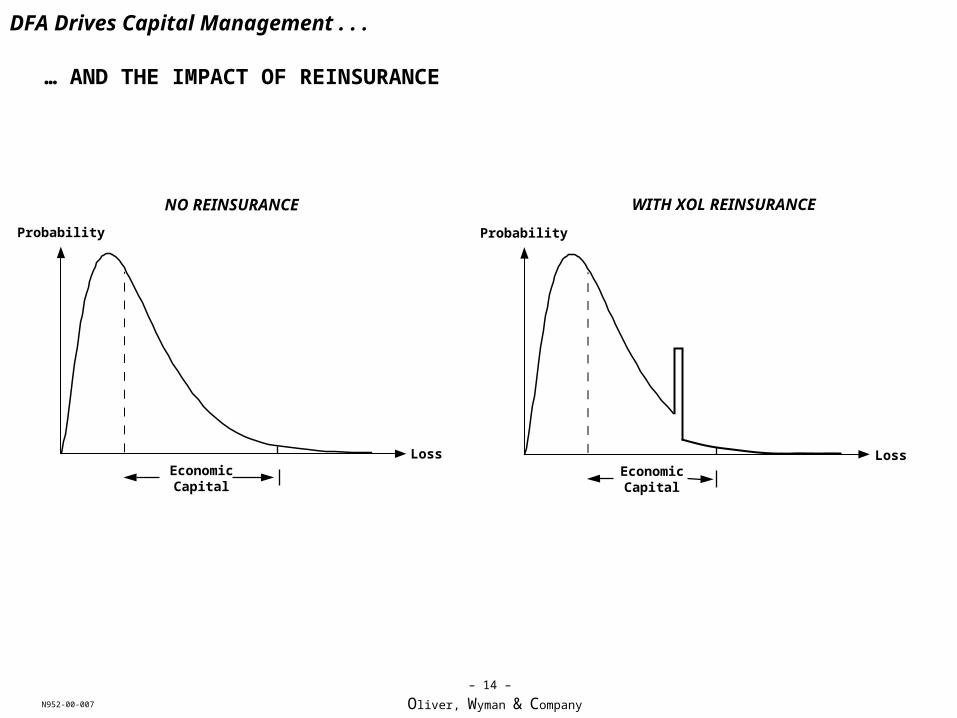

… AND THE IMPACT OF REINSURANCE

WITH XOL REINSURANCE

DFA Drives Capital Management . . .

Economic Capital

NO REINSURANCE

Probability

Loss

Probability

Economic Capital

Loss

Oliver, Wyman & CompanyN952-00-007

– 15 –

II. DFA UNCOVERS SKEWS IN RISK-ADJUSTED PROFITABILITY

Oliver, Wyman & CompanyN952-00-007

– 16 –

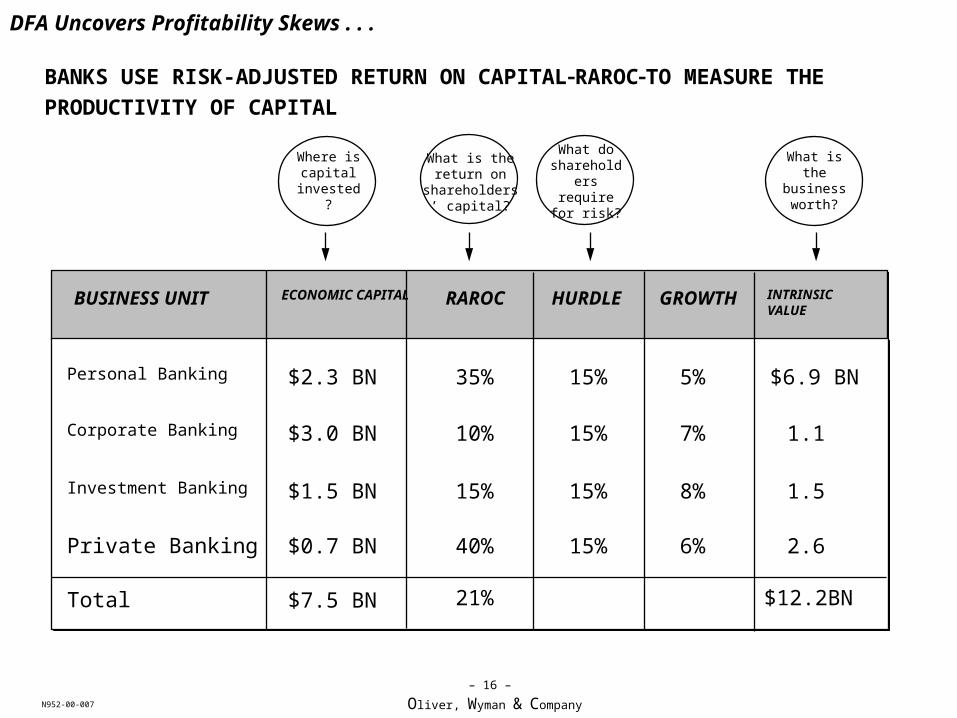

BUSINESS UNIT ECONOMIC CAPITAL

RAROC HURDLE GROWTH INTRINSIC VALUE

DFA Uncovers Profitability Skews . . .

BANKS USE RISK-ADJUSTED RETURN ON CAPITALRAROCTO MEASURE THE

PRODUCTIVITY OF CAPITAL

Personal Banking

Corporate Banking

What is the return on

shareholders’ capital?

What do shareholders

require for risk?

What is the business worth?

Where is capital

invested?

Investment Banking

Private Banking

Total

$2.3 BN

$3.0 BN

$1.5 BN

$0.7 BN

$7.5 BN

15%

15%

15%

15%

35%

10%

15%

40%

21%

5%

7%

8%

6%

$6.9 BN

1.1

1.5

2.6

$12.2BN

Oliver, Wyman & CompanyN952-00-007

– 17 –

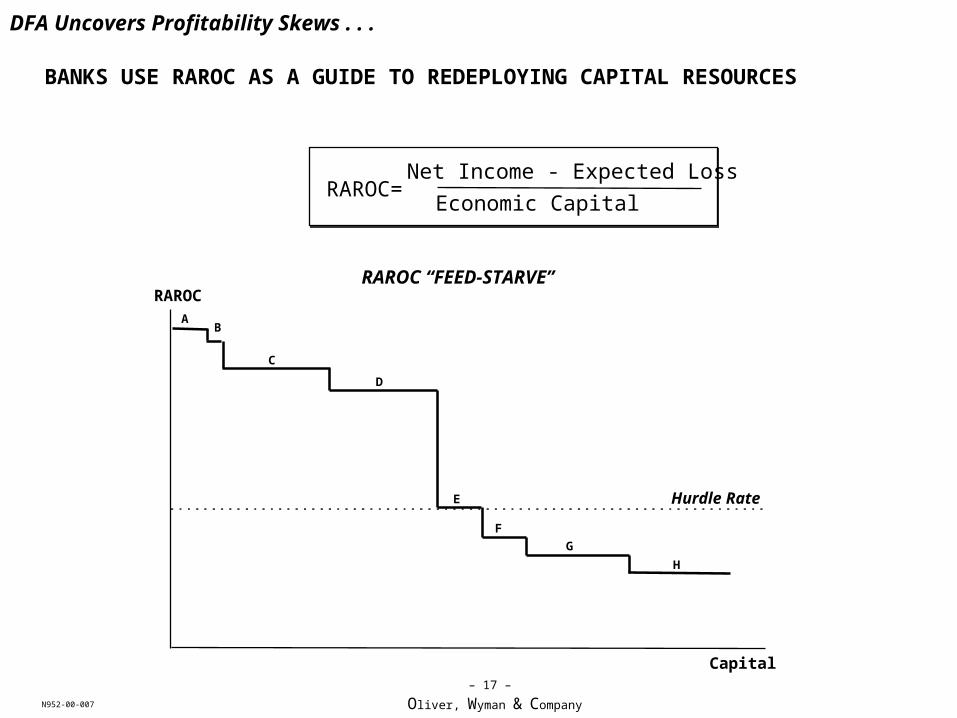

RAROC= Net Income - Expected Loss

Economic Capital

RAROC “FEED-STARVE”RAROC

Capital

AB

C

D

E

F

G

H

Hurdle Rate

DFA Uncovers Profitability Skews . . .

BANKS USE RAROC AS A GUIDE TO REDEPLOYING CAPITAL RESOURCES

Oliver, Wyman & CompanyN952-00-007

– 18 –

DFA Uncovers Profitability Skews . . .

LEADING FINANCIAL INSTITUTIONS ARE USING RAROC TO DRIVE KEY DECISIONS

• CEO Martin Taylor stated in Barclays’ annual report: “. . . we continue to refine our risk management techniques and focus on the return on economic capital, shifting capital away from areas of low or particularly unpredictable return and taking into account the contribution of each business to the Group’s overall volatility of earnings”

• Most commentators have stated that relatively poor risk-adjusted returns is the main rationale for Barclays selling BZW’s investment banking business

• Still more banks could learn from Barclays’ example– “The sorry fact is that those European banks that have chosen to stay in the game (of

investment banking) are, almost without exception, either more tolerant of low returns than Barclays, or less sophisticated at measuring how low those returns are” (Financial Times, October 6, 1997)

Oliver, Wyman & CompanyN952-00-007

– 19 –

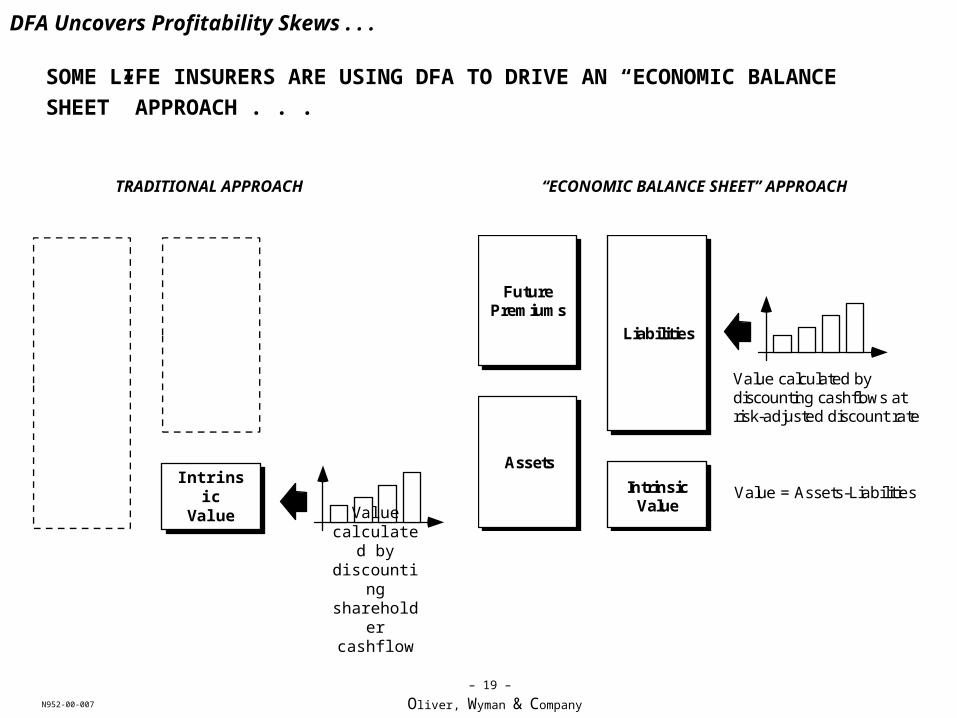

SOME LIFE INSURERS ARE USING DFA TO DRIVE AN “ECONOMIC BALANCE

SHEET” APPROACH . . .

TRADITIONAL APPROACH “ECONOMIC BALANCE SHEET” APPROACH

DFA Uncovers Profitability Skews . . .

Value = Assets-LiabilitiesIntrinsicValue

FuturePremiums

Assets

Liabilities

Value calculated bydiscounting cashflows atrisk-adjusted discount rate

Intrinsic Value

Value calculated by discounting shareholder

cashflow

Oliver, Wyman & CompanyN952-00-007

– 20 –

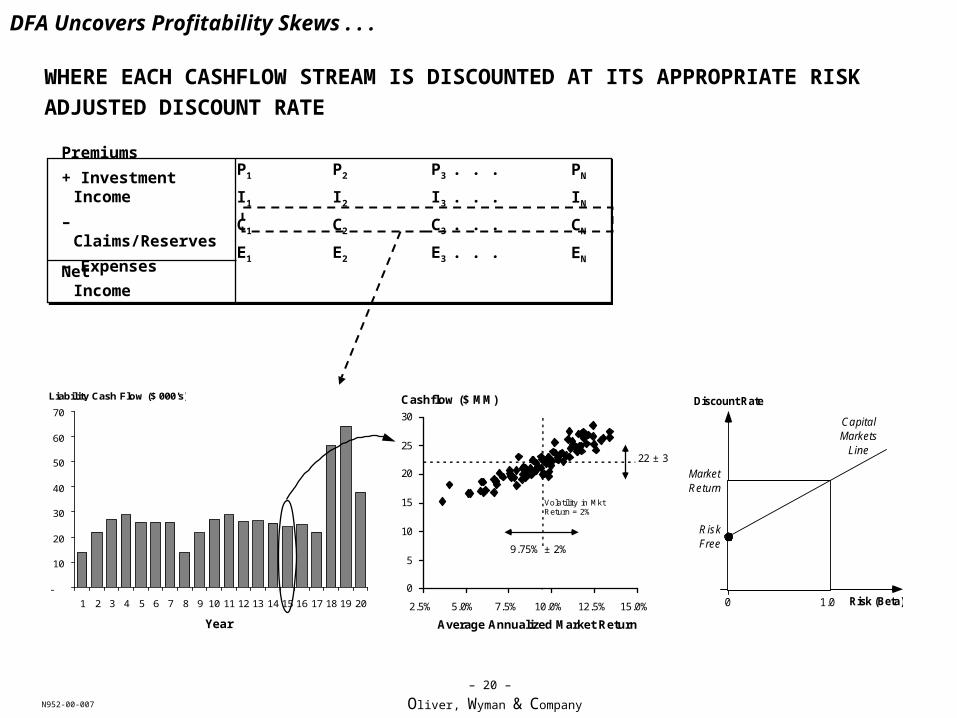

WHERE EACH CASHFLOW STREAM IS DISCOUNTED AT ITS APPROPRIATE RISK

ADJUSTED DISCOUNT RATE

Discount Rate

Risk (Beta)0 1.0

RiskFree

MarketReturn

CapitalMarkets

Line

-

10

20

30

40

50

60

70

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Liability Cash Flow ($ 000's)

0

5

10

15

20

25

30

2.5% 5.0% 7.5% 10.0% 12.5% 15.0%

Average Annualized Market Return

Cashflow ($ MM)

Volatility in MktReturn = 2%

22 ± 3

9.75% ± 2%

Premiums

+ Investment Income

– Claims/Reserves

– Expenses

Net Income

P1 P2 P3 . . .

I1 I2 I3 . . .

C1 C2 C3 . . .

E1 E2 E3 . . .

DFA Uncovers Profitability Skews . . .

Year

PN

IN

CN

EN

Oliver, Wyman & CompanyN952-00-007

– 21 –

THIS RISK-ADJUSTED VIEW REVEALED DRAMATIC VALUE CREATIONS SKEWS

ACROSS PRODUCTS

BEFORE RISK-ADJUSTMENT AFTER RISK-ADJUSTMENT

50

0

-50

-100

-150

-200

-250

100

A B C D E F TOTAL

Value of New Business

B D E C A F TOTAL

Value of New Business

Long-termSavings Products

50

0

-50

-100

-150

-200

-250

100

PRODUCT VALUE MEASUREMENT

DFA Uncovers Profitability Skews . . .

Oliver, Wyman & CompanyN952-00-007

– 22 –

A TOP-DOWN ANALYSIS OF FOURTEEN TOP PROPERTY AND CASUALTY

INSURERS REVEALS THAT ECONOMIC CAPITAL CAN DIFFER SUBSTANTIALLY

FROM TRADITIONAL MEASURES OF CAPITAL ADEQUACY

DFA Uncovers Profitability Skews . . .

ECONOMIC VS. STATUTORY VIEWS OF CAPITAL ADEQUACY

0.00

0.50

1.00

1.50

2.00

2.50

3.00

0.00 0.50 1.00 1.50 2.00 2.50

Premium-to-Economic Capital

Premium-to-Surplus

Economic Capital= Surplus

Oliver, Wyman & CompanyN952-00-007

– 23 –

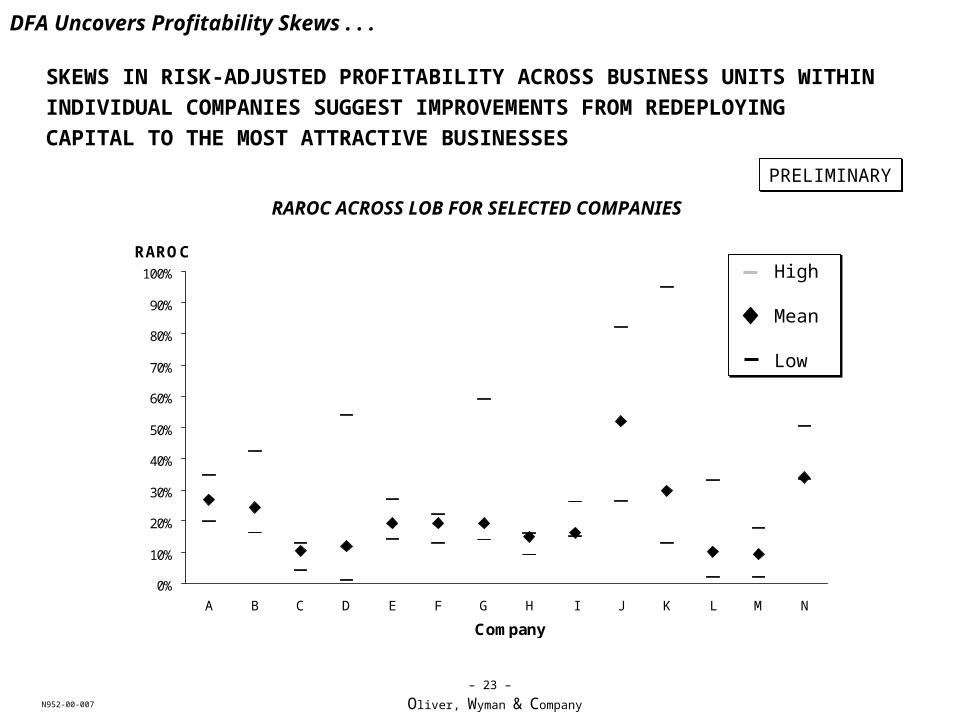

SKEWS IN RISK-ADJUSTED PROFITABILITY ACROSS BUSINESS UNITS WITHIN

INDIVIDUAL COMPANIES SUGGEST IMPROVEMENTS FROM REDEPLOYING

CAPITAL TO THE MOST ATTRACTIVE BUSINESSES

DFA Uncovers Profitability Skews . . .

RAROC ACROSS LOB FOR SELECTED COMPANIES

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

A B C D E F G H I J K L M N

RAROC

Company

PRELIMINARYPRELIMINARY

High

Mean

Low

High

Mean

Low

Oliver, Wyman & CompanyN952-00-007

– 24 –

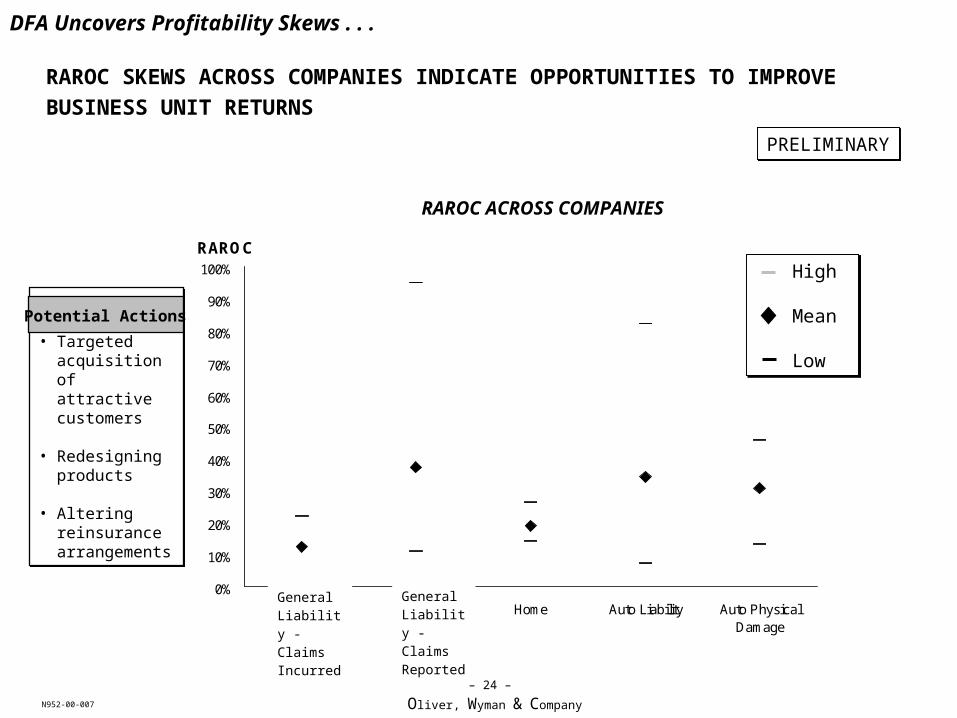

RAROC SKEWS ACROSS COMPANIES INDICATE OPPORTUNITIES TO IMPROVE

BUSINESS UNIT RETURNS

DFA Uncovers Profitability Skews . . .

PRELIMINARYPRELIMINARY

• Targeted acquisition of attractive customers

• Redesigning products

• Altering reinsurance arrangements

• Targeted acquisition of attractive customers

• Redesigning products

• Altering reinsurance arrangements

Potential Actions

RAROC ACROSS COMPANIES

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

XSU D&O Home Auto Liability Auto PhysicalDamage

RAROC

High

Mean

Low

High

Mean

Low

General Liability - Claims Incurred

General Liability - Claims Reported

Oliver, Wyman & CompanyN952-00-007

– 25 –

III. DFA SUPPORTS BUSINESS MODEL EVOLUTION

Oliver, Wyman & CompanyN952-00-007

– 26 –

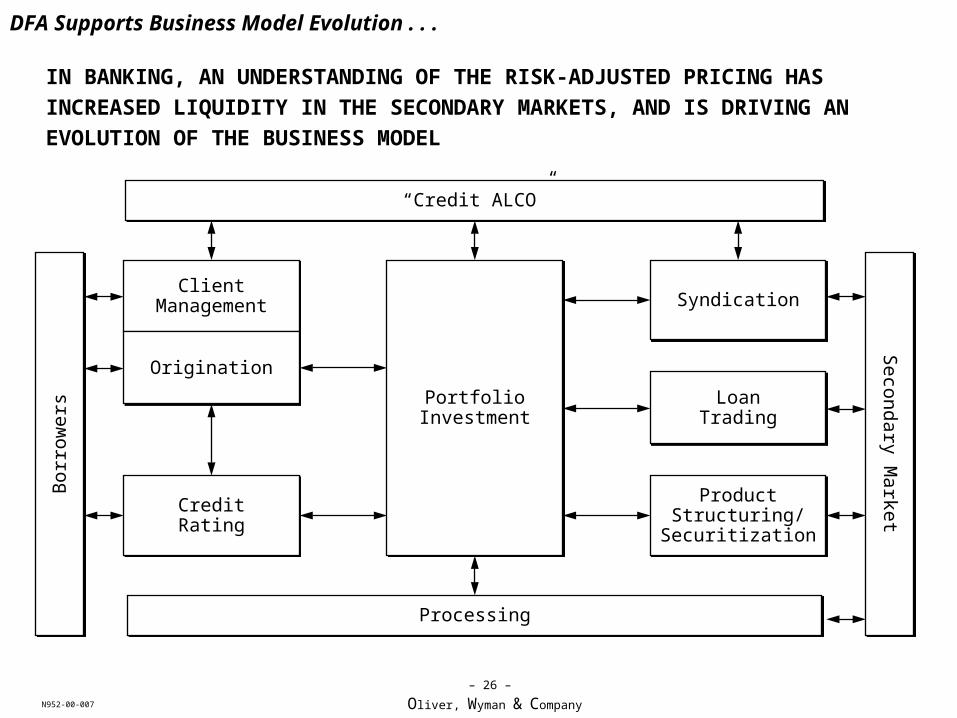

IN BANKING, AN UNDERSTANDING OF THE RISK-ADJUSTED PRICING HAS

INCREASED LIQUIDITY IN THE SECONDARY MARKETS, AND IS DRIVING AN

EVOLUTION OF THE BUSINESS MODEL

DFA Supports Business Model Evolution . . .

ProcessingProcessing

“Credit ALCO”“Credit ALCO”

PortfolioInvestmentPortfolio

Investment

ClientManagement

ClientManagement SyndicationSyndication

OriginationOrigination

CreditRatingCreditRating

LoanTradingLoan

Trading

ProductStructuring/

Securitization

ProductStructuring/

Securitization

Bor

row

ers

Bor

row

ers

Second

ary Market

Second

ary Market

Oliver, Wyman & CompanyN952-00-007

– 27 –

THIS MODEL IS LIKELY TO EVOLVE IN THE INSURANCE MARKET AS WELL, AS

PRICING STANDARDS DEVELOP AND CAPITAL MARKETS BECOME MORE LIQUID

Servicing & ProcessingServicing & Processing

ClientManagement

ClientManagement

OriginationOrigination

UnderwritingUnderwriting

Ins

ure

ds

Ins

ure

ds

Ca

pita

l Ma

rke

tsC

ap

ital M

ark

ets

Packaging &Distribution

Reinsurance

RetainedPortfolio

WarehousePortfolio

Sales &Trading

DFA Supports Business Model Evolution . . .

Oliver, Wyman & CompanyN952-00-007

– 28 –

IV. DFA CAN INTEGRATE MODELS DEVELOPED FOR BANKING

Oliver, Wyman & CompanyN952-00-007

– 29 –

IN BANKING, CREDIT RISK IS MOST OFTEN CALCULATED ANALYTICALLY . . .

DFA Can Integrate Banking Models . . .

Solvency Standard

ExpectedLoss

EconomicCapital

Probability

CreditLoss ($)Unexpected

Loss

• Default Probability• Loan Characteristics

DefaultCorrelations

Calculate ExpectedLoss (µ) by Loan

Calculate UnexpectedLoss () assumingcorrelated Bernoulli

variables

Fit (µ) and ( ) toemprically determined

distribution

Calculate tailpercentile asmultiple of

Oliver, Wyman & CompanyN952-00-007

– 30 –

… AND MARKET RISK IS MOST OFTEN MEASURED USING PARAMETRIC

VALUE-AT-RISK (VaR)

DFA Can Integrate Banking Models . . .

CorrelationsBetween

Market Risks

$/Peso

Exposure

3 MoLIBOR

Exposure

SpotOil

Exposure

X =

X =

X =

MARKET INDEXDISTRIBUTIONS

VALUEDISTRIBUTION

EXPOSURETO INDICES

OVERALLVALUE

DISTRIBUTION

ILLUSTRATIVE

THESE RISKS ARE THEN AGGREGATED USING INTER-RISK CORRELATION ESTIMATES

Oliver, Wyman & CompanyN952-00-007

– 31 –

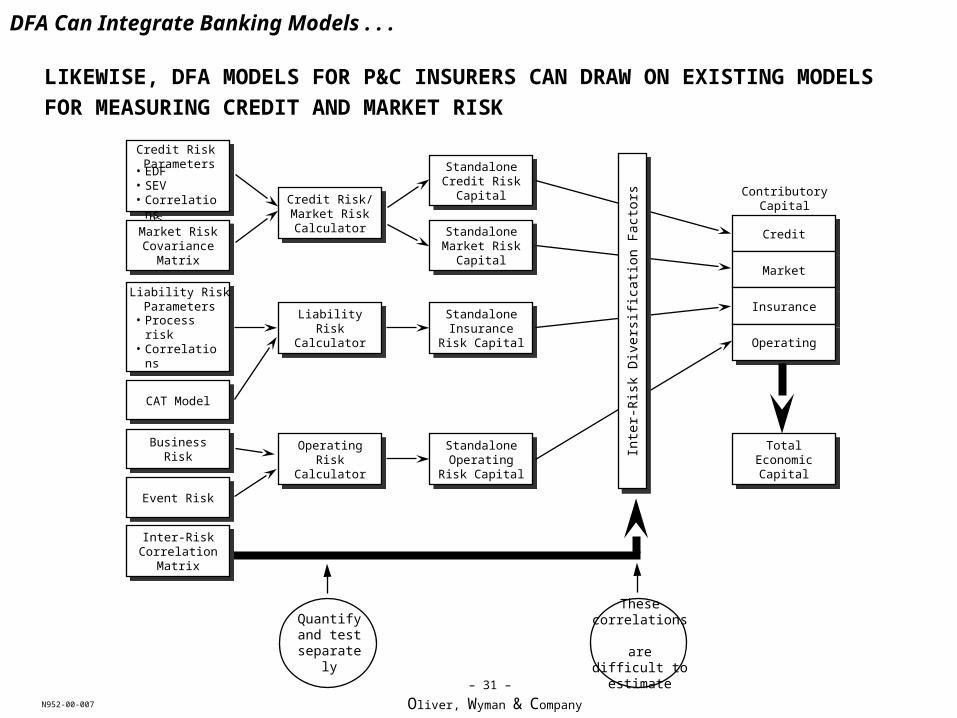

LIKEWISE, DFA MODELS FOR P&C INSURERS CAN DRAW ON EXISTING MODELS

FOR MEASURING CREDIT AND MARKET RISK

• EDF• SEV• Correlations

• EDF• SEV• Correlations

Market Risk Covariance

Matrix

Market Risk Covariance

Matrix

• Process risk• Correlations

• Process risk• Correlations

CAT ModelCAT Model

Event RiskEvent Risk

Inter-Risk Correlation

Matrix

Inter-Risk Correlation

Matrix

Credit Risk/Market Risk Calculator

Credit Risk/Market Risk Calculator

Liability Risk Calculator

Liability Risk Calculator

Operating Risk Calculator

Operating Risk Calculator

Standalone Credit Risk

Capital

Standalone Credit Risk

Capital

Standalone Insurance Risk

Capital

Standalone Insurance Risk

Capital

Standalone Operating Risk

Capital

Standalone Operating Risk

Capital

Standalone Market Risk

Capital

Standalone Market Risk

Capital

CreditCredit

MarketMarket

InsuranceInsurance

OperatingOperating

TotalEconomic

Capital

TotalEconomic

Capital

ContributoryCapital

Inte

r-R

isk

Div

ersi

ficat

ion

Fac

tors

Inte

r-R

isk

Div

ersi

ficat

ion

Fac

tors

Credit Risk Parameters

Liability RiskParameters

Business RiskBusiness Risk

DFA Can Integrate Banking Models . . .

These correlations are difficult to

estimate

Quantify and test

separately