Myanmar’s Iron Lady Treads Testing Waters. Issue 2016 EN.pdfAgribusiness Public Corporation. The...

14

The National League for Democracy (NLD) won a landslide victory in Myanmar’s general election on 8 November, taking almost 80% of the contested seats. The party, led by Aung San Suu Kyi, now has an outright majority in both legislative chambers. This gives the NLD the power to control law-making and select the president, although the immensely popular Suu Kyi is constitutionally barred from taking the position. The coming months will be a testing time for the NLD and Myanmar’s nascent democracy – the process of installing a new government will not be resolved until March. The question of who will become president is unresolved: there are suggestions that Suu Kyi will lean towards a low-key figure such as her personal doctor, Tin Myo Win. The military would favour a more experienced and potentially loyal operator. Whoever is appointed will require deft diplomatic skills to work with both Suu Kyi and the military to tackle myriad challenges within Myanmar and beyond. Myanmar’s first stock exchange (YSX) opened in a restored building in Yangon on 9 December, although no companies have yet listed and trading is not expected to begin until March or April 2016. The move symbolises both the country’s determination to develop a modern financial system and the scale of the challenges ahead. Early entrants are expected to include First Myanmar Investment, owned by the tycoon, Serge Pun, Myanmar Citizens Bank (MCB) and Myanmar Thilawa SEZ Holdings. The latter forms part of the new 2,400 hectare Special Economic Zone at Thilawa port south of Yangon, which has received substantial Japanese backing. Other companies in the frame include First Private Bank Limited, Great Hor Kham Public and Myanmar Agribusiness Public Corporation. The legal framework has been developed with Japanese assistance and appears solid, although foreign investors may not participate until the new Myanmar Companies Law is passed (expected in 2016). Please click here to view the full report if you have a Country Insight Snapshot subscription. Country Headlines – Cambodia - Rating downgraded as political turmoil weakens investor sentiment – Indonesia - Economic reform efforts consolidate as growth remains lacklustre – Malaysia - Launch of ASEAN Economic Community will bolster market potential – Philippines - Rising business and consumer sentiment - strong economic outlook – Singapore - Growth differences between goods and service sectors to continue – Thailand - Drought will impact farmers and economic growth in 2016 – Vietnam - The central bank maintains tight control over the currency Click here to check out more analysis on these countries or any of the 130 countries covered worldwide. Myanmar’s Iron Lady Treads Testing Waters ASIA NEWSFLASH February 2016 COUNTRY SPOTLIGHT MYANMAR

Transcript of Myanmar’s Iron Lady Treads Testing Waters. Issue 2016 EN.pdfAgribusiness Public Corporation. The...

The National League for Democracy (NLD) won a landslide victory in Myanmar’s general election on 8 November, taking almost 80% of the contested seats. The party, led by Aung San Suu Kyi, now has an outright majority in both legislative chambers. This gives the NLD the power to control law-making and select the president, although the immensely popular Suu Kyi is constitutionally barred from taking the position. The coming months will be a testing time for the NLD and Myanmar’s nascent democracy – the process of installing a new government will not be resolved until March. The question of who will become president is unresolved: there are suggestions that Suu Kyi will lean towards a low-key figure such as her personal doctor, Tin Myo Win. The military would favour a more experienced and potentially loyal operator. Whoever is appointed will require deft diplomatic skills to work with both Suu Kyi and the military to tackle myriad challenges within Myanmar and beyond.

Myanmar’s first stock exchange (YSX) opened in a restored building in Yangon on 9 December, although no companies have yet listed and trading is not expected to begin until March or April 2016. The move symbolises both the country’s determination to develop a modern financial system and the scale of the challenges ahead. Early entrants are expected to include First Myanmar Investment, owned by the tycoon, Serge Pun, Myanmar Citizens Bank (MCB) and Myanmar Thilawa SEZ Holdings. The latter forms part of the new 2,400 hectare Special Economic Zone at Thilawa port south of Yangon, which has received substantial Japanese backing.

Other companies in the frame include First Private Bank Limited, Great Hor Kham Public and Myanmar Agribusiness Public Corporation. The legal framework has been developed with Japanese assistance and appears solid, although foreign investors may not participate until the new Myanmar Companies Law is passed (expected in 2016).

Please click here to view the full report if you have a Country Insight Snapshot subscription.

Country Headlines

– Cambodia - Rating downgraded as political turmoil weakens investor sentiment

– Indonesia - Economic reform efforts consolidate as growth remains lacklustre

– Malaysia - Launch of ASEAN Economic Community will bolster market potential

– Philippines - Rising business and consumer sentiment - strong economic outlook

– Singapore - Growth differences between goods and service sectors to continue

– Thailand - Drought will impact farmers and economic growth in 2016

– Vietnam - The central bank maintains tight control over the currency

Click here to check out more analysis on these countries or any of the 130 countries covered worldwide.

Myanmar’s Iron Lady Treads Testing Waters

ASIA NEWSFLASH

February 2016

COUNTRY SPOTLIGHT MYANMAR

Vietnam Continues to Look Rosy in 2016

This interview originally appeared in ASEAN Today on 9 January 2016. Click to view online.

The Vietnamese economy is the fastest growing economy of the six major Asean countries and is seen as the one likely to outperform other emerging economies. The gross domestic product (GDP) for 2015 is hovering around 6.5 percent, the highest since 2007.

To give a deeper look at what 2016 has in store for Vietnam, Dun & Bradstreet’s Senior Economist Isaac Leung responded to questions from Asean Today. Below are his responses.

Q: What can we expect from Vietnam this year? Will the performance be as good as last year?

Mr Leung: Overall, Dun & Bradstreet expects the economy to continue to grow at a decent pace over the next couple of years, with a number of factors set to support growth.

The first is strong exports, amid the continued relocation of low-end manufacturing from China to lower-cost regional locations. Even though exports from most emerging markets have contracted so far this year, exports from Vietnam have still grown at close to double-digit pace.

The other factor that will support growth is loose monetary policy. Inflation, which topped 20% in 2011, dropped back dramatically in 2015 and is likely to remain low in 2016. Low inflation has given the central bank scope to keep interest rates low.

Meanwhile, the banking sector is showing gradual signs of gradual recovery. Credit growth is accelerating, while the level of non-performing loans is down sharply.

Q: Or is Vietnam moving too fast?

Mr Leung: While growth of around 6.5 percent over the next few years certainly represents a decent performance, it is still some way short of the 10 percent growth rates that China and other countries in Asia grew at while at a similar level of development to where Vietnam is at the moment. Further structural reforms, in particular of the state-owned sector, are needed in order for Vietnam to reach its full potential.

The Vietnamese dong is likely to experience increased downward pressure with the US Fed interest rate hike for the first time in over eight years. Under Vietnam’s new exchange rate regime, which was established in August, the dong can depreciate (or appreciate) by up to 3 percent from its reference rate.

Although the new regime gives Vietnam’s central bank more flexibility than the previous arrangement, the central bank could be forced to intervene heavily in the event Fed tightening leads to significant capital outflows from emerging markets.

Our latest Business Optimism Index for Quarter 1 2016 shows some seasonal correction in business expectations, after surging consecutively for the last four quarters throughout 2015. The overall index moderated downwards to 22 percent from 45 percent, with some concerns on currency fluctuation weighing on the manufacturing sector.

FOLLOW THE PHILIPPINES SINGAPORE THAILAND

ASIA NEWSFLASH

MARKET INSIGHT

February 2016

By Vanitha Nadaraj | ASEAN Today

ASIA NEWSFLASH

February 2016

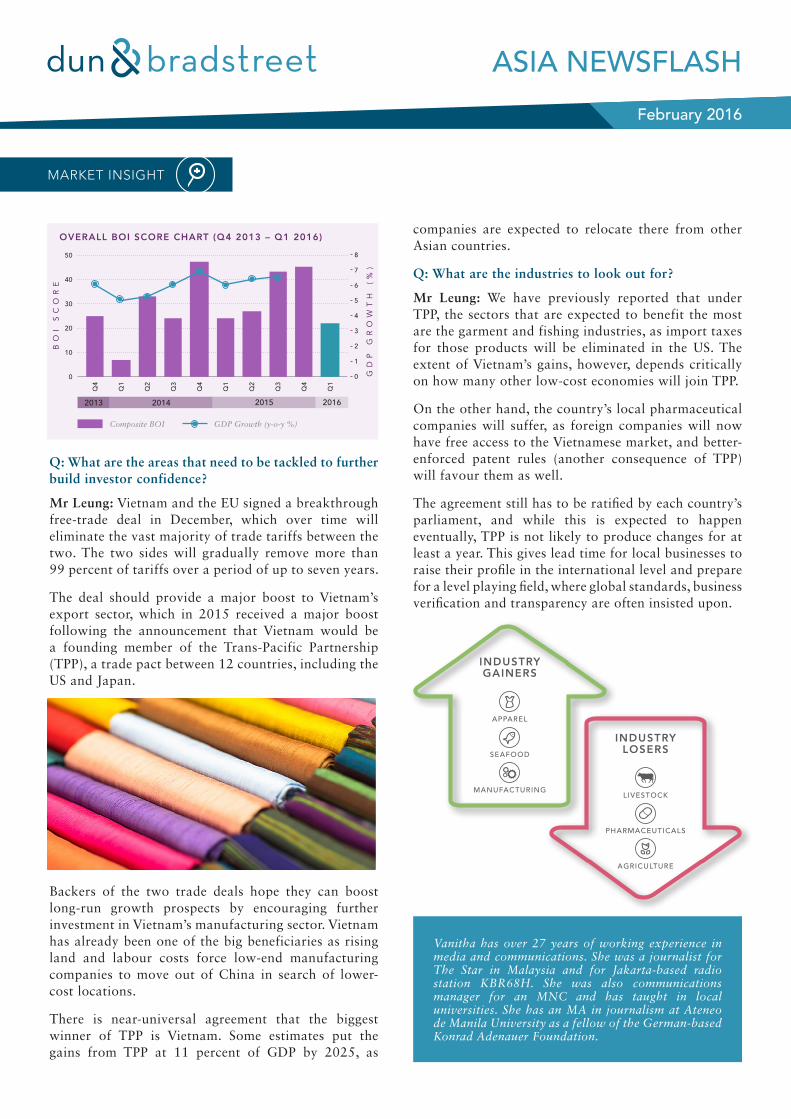

Q: What are the areas that need to be tackled to further build investor confidence?

Mr Leung: Vietnam and the EU signed a breakthrough free-trade deal in December, which over time will eliminate the vast majority of trade tariffs between the two. The two sides will gradually remove more than 99 percent of tariffs over a period of up to seven years.

The deal should provide a major boost to Vietnam’s export sector, which in 2015 received a major boost following the announcement that Vietnam would be a founding member of the Trans-Pacific Partnership (TPP), a trade pact between 12 countries, including the US and Japan.

Backers of the two trade deals hope they can boost long-run growth prospects by encouraging further investment in Vietnam’s manufacturing sector. Vietnam has already been one of the big beneficiaries as rising land and labour costs force low-end manufacturing companies to move out of China in search of lower-cost locations.

There is near-universal agreement that the biggest winner of TPP is Vietnam. Some estimates put the gains from TPP at 11 percent of GDP by 2025, as

companies are expected to relocate there from other Asian countries.

Q: What are the industries to look out for?

Mr Leung: We have previously reported that under TPP, the sectors that are expected to benefit the most are the garment and fishing industries, as import taxes for those products will be eliminated in the US. The extent of Vietnam’s gains, however, depends critically on how many other low-cost economies will join TPP.

On the other hand, the country’s local pharmaceutical companies will suffer, as foreign companies will now have free access to the Vietnamese market, and better-enforced patent rules (another consequence of TPP) will favour them as well.

The agreement still has to be ratified by each country’s parliament, and while this is expected to happen eventually, TPP is not likely to produce changes for at least a year. This gives lead time for local businesses to raise their profile in the international level and prepare for a level playing field, where global standards, business verification and transparency are often insisted upon.

Vanitha has over 27 years of working experience in media and communications. She was a journalist for The Star in Malaysia and for Jakarta-based radio station KBR68H. She was also communications manager for an MNC and has taught in local universities. She has an MA in journalism at Ateneo de Manila University as a fellow of the German-based Konrad Adenauer Foundation.

MARKET INSIGHT

INDUSTRY LOSERS

LIVESTOCK

PHARMACEUTICALS

AGRICULTURE

MANUFACTURING

INDUSTRY GAINERS

APPAREL

SEAFOOD

Q4

50

40

30

20

0

10

Q3

Q3

Q1

Q4

Q1

Q4

Q1

Q2

Q2

2015 201620142013

OVERALL BOI SCORE CHART (Q4 2013 – Q1 2016)

BO

I

SC

OR

E

8

5

7

6

4

3

2

0

1G

DP

G

RO

WT

H

(%

)

Composite BOI GDP Growth (y-o-y %)

ASIA NEWSFLASH

ASIA PERSPECTIVES

Advising exporters on cross-border risk management strategy is tricky business. Credit sales via “open account” may win the most in sales — but what will collection rates look like?

Dun & Bradstreet’s Country Insight team advises customers on minimum and recommended payment methods, ranging from open account to cash in advance, for 132 countries around the world. Of the several grades of risk management or trade terms available to shippers, D&B advised open account terms (where the seller takes all risk) as optimal for 30 countries as of January 2016.

For higher-risk countries, the minimum guidance stood at “sight draft” (also known as documentary collection, or cash against documents) in 26 countries. A letter of credit is advised in 37 countries, while a “confirmed” letter of credit is recommended in 31, and cash in advance for eight.

The five grades are simplifications of commercial practice: There are several varieties of documentary collection (cash against documents, where the importer gets the documents of title to goods in exchange for giving cash to a local bank). Various forms of letter of credit (in which a bank guarantees the importer’s payment) also exist. Then there are the other trade finance flavors and instruments, such as credit insurance, and factoring, where a bank, or nonbank, buys the accounts receivable from the exporter for a discount.

Countries where D&B advises open account terms are an unexciting list dominated by low-growth OECD markets. Hong Kong, Taiwan, and Singapore are on the list. More surprisingly, the list includes five Gulf kingdoms: Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. These 30 countries have an average annual GDP per capita of over $48,000. Those markets where D&B advises cash in advance, with the buyer or importer taking all the risks, include the usual list of countries

under sanctions or subject to deep, chronic political dysfunction. These countries are Afghanistan, Cuba, Iran, Libya, Sudan, Syria, Yemen, and Zimbabwe. They have a median GDP per capita of just over $1,600.

Most new opportunities driven by broad economic growth trends such as rising middle classes will, over the rest of the decade, lie in countries between these extremes. Broadly, the markets where GDP per capita ranges from $3,250, the median for those countries where D&B advises a letter of credit “confirmed” by a bank in the exporter’s country, up to $15,000, the median for the countries where a minimum of cash against documents is recommended.

Choosing the right risk-sharing, trade finance mechanisms to trade with in these markets is where companies can demonstrate commercial acumen that will likely lead to growing market share and enable executives to maximize and defend the value of accounts receivable.

How to Use Trade Terms to Your AdvantageBy Isaac Leung | Dun & Bradstreet Editor

FOLLOW THE PHILIPPINES SINGAPORE THAILAND

February 2016

Isaac Leung is a Senior Economist for Dun & Bradstreet. Based in the UK, he covers China, India and other parts of the Asia Pacific region. His areas of interest include maritime economics.

OA = open accountSD = sight draft

CiA = cash in advanceLC = letter of creditCLC = confirmed letter of credit

CASH IN ADVANCE

CASH IN ADVANCE

CONFIRMED L/C

CONFIRMED L/C

LETTER OF CREDIT LETTER OF CREDIT

SIGHT DRAFT

SIGHT DRAFT

MINIMUM TRADE TERMS

IMPORTERS’ RISK

Higher risk

Lower risk

EXPORTERS’ RISK

OPEN ACCOUNT

OPEN ACCOUNT

This special report is the first of a three-part series on corporate payment practices based on an extensive survey of 8 countries in Asia Pacific, courtesy of Atradius.

SALES ON CREDIT TERMS

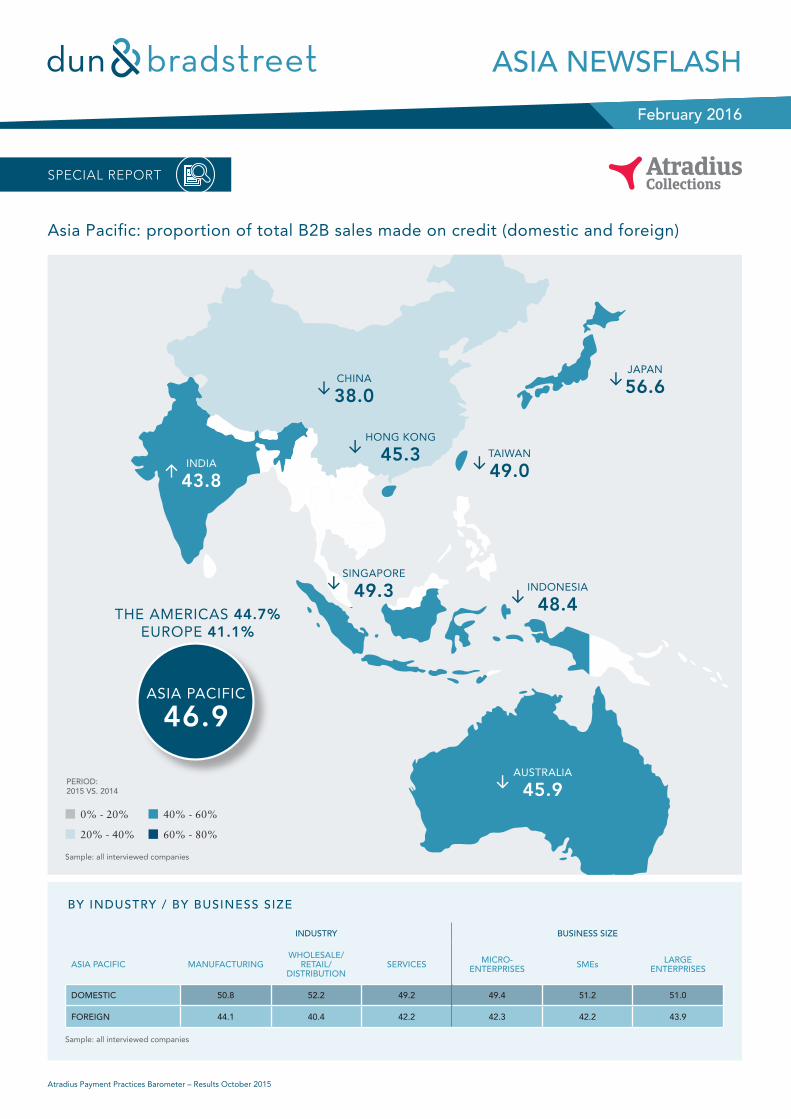

Businesses in Asia Pacific appear to make broad use of trade credit in both domestic and foreign B2B transactions. As our survey reveals, 91% of the respondents across the countries surveyed in the region (Australia, China, Hong Kong, India, Indonesia, Japan, Singapore and Taiwan) reported having granted trade credit to their B2B customers over the past year. This is slightly more than in the Americas (89%) and significantly more than in Europe (76.2%).

By country, Australia and Japan are the most conservative, while India and Hong Kong show the most liberal stance towards offering trade credit terms to their B2B customers. In the remaining countries surveyed, respondents show some selectivity towards their B2B customers, with credit-based sales ranging from between 35% and 60% of their domestic and foreign sales.

A breakdown by percentage of domestic and foreign B2B sales in the region points to a stronger propensity to sell on credit to B2B customers domestically than abroad. This pattern, which indicates an inconsistent perception of payment default risk arising from domestic and foreign trade, is similar to that observed in the Americas and Europe.

On average, 50.6% of the total value of domestic B2B sales in Asia Pacific were made on credit, compared to 42.5% of sales made to foreign B2B customers. The averages for the Americas are 49.3% for domestic sales and 40.1% for foreign sales; while for Europe, the averages are 44.3% domestic and 37.9% foreign. These findings highlight that businesses interviewed in Asia Pacific, the Americas and Europe perceive selling on credit on familiar domestic markets to be less risky, in terms of customers’ payment default, than selling on credit to foreign customers. For export-reliant economies, protecting exports from the risk of payment default due to commercial and political problems comes as no surprise.

Despite the great openness to trade credit shown by respondents in Asia Pacific, there are some differences by country. In China, survey respondents show a clear-cut preference for requesting payment from B2B customers on cash terms or on terms other than trade credit. This selective approach to the use of trade credit particularly applies to sales to B2B customers abroad. 41.8% and 34.2% of the average total value of domestic and foreign B2B sales of Chinese respondents was transacted on credit. The foreign figure for China

B2B Payment Behavior in Asia Pacific (Part 1)

ASIA NEWSFLASH

SPECIAL REPORT

Atradius Payment Practices Barometer – Results October 2015

February 2016

OVER HALF OF THE TOTAL VALUE OF DOMESTIC B2B SALES IN ASIA PACIFIC

WERE MADE ON CREDIT

is the lowest of the countries surveyed in the region. In contrast, Japanese respondents, appear to have the highest value of domestic and foreign B2B sales made on credit. Credit sales averaged 60.4% of the domestic and 52.7% of the foreign B2B sales value in the country.

In most of the remaining countries surveyed, the total value of domestic credit-based B2B sales is almost equal to, or not markedly below, the regional average with Indonesia at 50.5%, Hong Kong at 49.8%, India at 48.2% and Australia at 46.5%. In Singapore and Taiwan, conversely, the domestic figures are above the average of the region (53.3% and 54.3% respectively).

In respect to foreign trade, despite the observations above, the proportions of credit-based sales in India (39.3%) and Hong Kong (40.9%) are lower than the 42.5% regional average. A broader use of trade credit in sales to B2B customers abroad was observed in Taiwan (43.8%), Australia (45.3%), Indonesia (46.3%), and Singapore (45.2%).

Over the past year, the proportion of B2B sales on credit (both domestic and foreign) in the region increased, on average, by 3.2 and 5.5 percentage points respectively. Domestically, the increase in credit-based B2B sales in Hong Kong, Singapore and Taiwan was twice as high as the regional average. As to foreign trade, Japan stands out with a percentage point increase that is three times higher than that for the region. The above mentioned statistics point to a markedly less selective approach in both domestic and foreign trade credit decisions adopted by respondents in these countries, compared to their peers in the region.

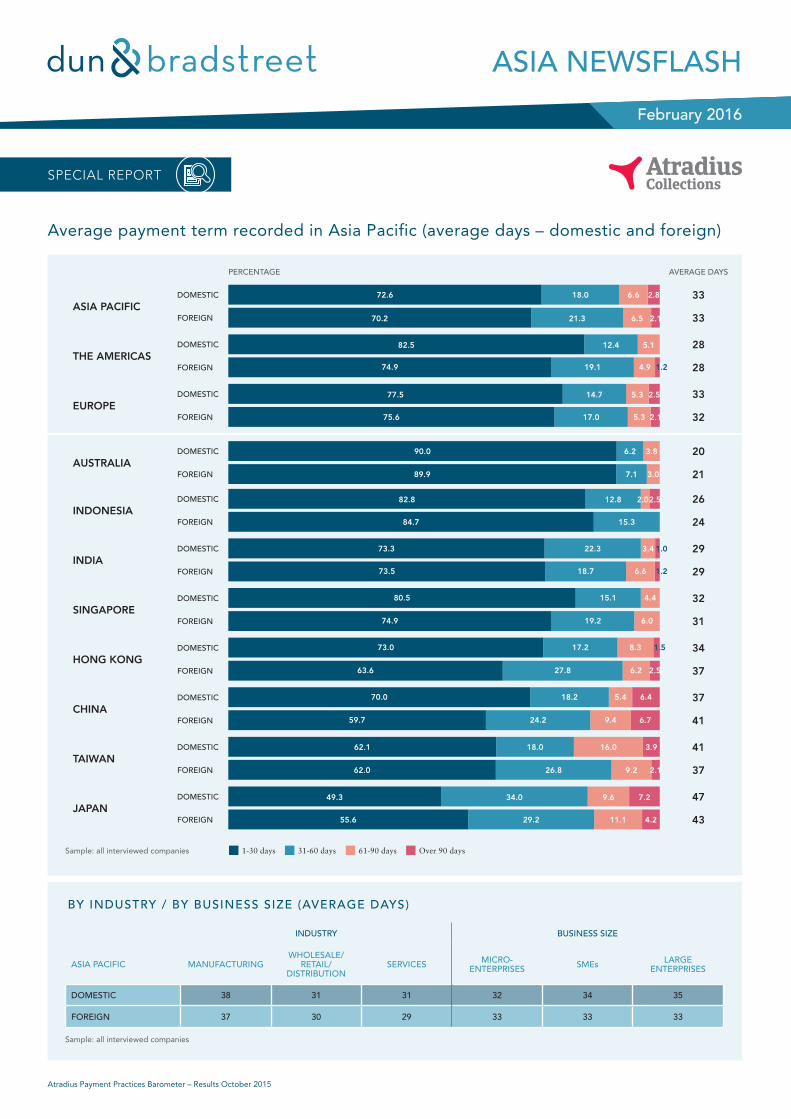

AVERAGE PAYMENT TERM

Both domestic and foreign B2B customers of respondents in Asia Pacific are given an average of 33 days from the invoice date to pay for goods and services purchased on credit (the Americas: 28 days; Europe: 32 days).

By country, respondents in Australia set the shortest payment terms for B2B invoices, averaging 20 days from the invoice date. At the other end of the scale, Japan extends the most relaxed payment terms in the region (averaging 47 days). Notably above the regional average are also the payment terms extended by survey respondents in Taiwan (averaging 41 days). In the remaining countries surveyed, average payment terms range from 26 days in Indonesia to 37 days in China.

Payment terms for domestic and foreign customers vary across countries. In Taiwan and Japan, domestic customers are given slightly longer terms to pay invoices than customers abroad, whereas in China and Hong Kong it is the opposite. In Australia, Singapore, Indonesia and India, no big difference between domestic and foreign payment terms was observed.

Over the past two years, average payment terms in most of the countries surveyed in Asia Pacific have shown marked variations. In Japan and China, invoice payment terms for both domestic and foreign B2B customers are now, on average, up to three weeks longer than two years ago. Respondents in Hong Kong extended longer payment terms than two years ago, particularly in B2B transactions with customers abroad. Indonesia, however, recorded a marked shortening of the payment terms extended to domestic B2B customers, as did India in relation to payment terms offered to customers abroad.

ASIA NEWSFLASH

SPECIAL REPORT

PROPORTION OF SALES MADE ON CREDIT TO TOTAL B2B SALES OF RESPONDENTS IN ASIA PACIFIC

ASIA PACIFIC

50.6%

42.5%

THE AMERICAS

49.3%

40.1%

EUROPE

44.3%

37.9%

Atradius Payment Practices Barometer – Results October 2015

Sample: companies interviewed (active in domestic and foreign markets)Source: Atradius Payment Practices Barometer – October 2015

Domestic customers Foreign customers

February 2016

SPECIAL REPORT

ASIA NEWSFLASH

Atradius Payment Practices Barometer – Results October 2015

February 2016

40% - 60%

60% - 80%

0% - 20%

20% - 40%

PERIOD:2015 VS. 2014

CHINA

38.0

JAPAN

56.6

TAIWAN

49.0INDIA

43.8

AUSTRALIA

45.9

HONG KONG

45.3

SINGAPORE

49.3 INDONESIA

48.4THE AMERICAS 44.7%EUROPE 41.1%

ASIA PACIFIC

46.9

Sample: all interviewed companies

Asia Pacific: proportion of total B2B sales made on credit (domestic and foreign)

BY INDUSTRY / BY BUSINESS SIZE

INDUSTRY BUSINESS SIZE

ASIA PACIFIC MANUFACTURINGWHOLESALE/

RETAIL/ DISTRIBUTION

SERVICES MICRO-ENTERPRISES SMEs LARGE

ENTERPRISES

DOMESTIC 50.8 52.2 49.2 49.4 51.2 51.0

FOREIGN 44.1 40.4 42.2 42.3 42.2 43.9

Sample: all interviewed companies

SPECIAL REPORT

ASIA NEWSFLASH

Atradius Payment Practices Barometer – Results October 2015

February 2016

1-30 days 31-60 days 61-90 days Over 90 days

Average payment term recorded in Asia Pacific (average days – domestic and foreign)

ASIA PACIFIC33

33

DOMESTIC

PERCENTAGE AVERAGE DAYS

FOREIGN

EUROPE33

32

DOMESTIC

FOREIGN

INDONESIA26

24

DOMESTIC

FOREIGN

SINGAPORE32

31

DOMESTIC

FOREIGN

CHINA37

41

DOMESTIC

FOREIGN

THE AMERICAS28

28

DOMESTIC

FOREIGN

AUSTRALIA20

21

DOMESTIC

FOREIGN

INDIA29

29

DOMESTIC

FOREIGN

HONG KONG34

37

DOMESTIC

FOREIGN

TAIWAN41

37

DOMESTIC

FOREIGN

JAPAN47

43

DOMESTIC

FOREIGN

72.6

70.2

77.5

90.0

89.9

75.6

82.8

73.0

63.6

70.0

59.7

62.0

49.3

55.6

62.1

73.3

73.5

80.5

74.9

84.7

82.5

74.9

18.0

21.3

14.7

6.2

7.1

17.0

12.8

17.2

27.8

18.2

24.2

26.8

34.0

29.2

18.0

22.3

18.7

15.1

19.2

15.3

12.4

19.1

6.6

6.5

5.3

3.8

3.0

5.3

2.0

8.3

6.2

5.4

9.4

9.2

9.6

11.1

16.0

3.4

6.6

4.4

6.0

5.1

4.9 1.2

1.0

1.2

1.5

2.8

2.1

2.5

2.1

2.5

2.5

6.4

6.7

2.1

7.2

4.2

3.9

Sample: all interviewed companies

BY INDUSTRY / BY BUSINESS SIZE (AVERAGE DAYS)

INDUSTRY BUSINESS SIZE

ASIA PACIFIC MANUFACTURINGWHOLESALE/

RETAIL/ DISTRIBUTION

SERVICES MICRO-ENTERPRISES SMEs LARGE

ENTERPRISES

DOMESTIC 38 31 31 32 34 35

FOREIGN 37 30 29 33 33 33

Sample: all interviewed companies

D&B’s U.S. Economic Health Tracker Reveals Continued Challenges for Small Businesses Balanced by Positive Job Growth

– Dun & Bradstreet’s Small Business Health Index dropped almost 2.0 points during the latest reporting period, largely due to rising delinquencies. The index also signals deterioration in small business performance compared to the past year, with a decline of approximately 1% on a year-over-year basis.

– We estimate 197,000 new non-farm jobs were added to U.S. payrolls in December 2015. We expect to see gains in the Trade, Transportation and Utilities and Retail sectors, while Manufacturing continues to be in a slump.

–Financial risks among all active and open U.S. businesses continued to diminish in December as the Overall Business Health Index rose 0.3% from the prior month reaching the highest level since the inception of the index in December 2010. The current trend of continuous gradual improvement remains intact.

Click here to read the report.

STATESIDE

ASIA NEWSFLASH

Q1 2016 Business Optimism Index

Interviews

SPECIAL ANNOUNCEMENT

The quarterly Dun & Bradstreet ASEAN BOI is the first and leading business optimism metric for Southeast Asia. An infographic is provided on the next page. To view the report, please contact your local D&B office.

SummaryThe Philippines extends its gains healthily while Vietnam takes a seasonal correction from its fast-paced growth. Things may have finally bottomed out in Malaysia and Indonesia as confidence bounces back in the first quarter, after a prolonged period of decline. Thailand is also seeing bright spots across the economy with stimulus measures in place. The lone exception is Singapore, where weakness in its manufacturing industries push business expectations down to a multi-year low.

Bloomberg TV interviewed Audrey Chia CEO of D&B Singapore on 5th Jan, and Sheila Lina CEO of D&B Philippines on 21st Jan, regarding the BOI survey results. You can view the clips and photos on their respective Facebook pages. A videographic version is also available for Malaysia BOI (click on image below to view).

FOLLOW THE PHILIPPINES SINGAPORE THAILAND

February 2016

ASEAN Business Optimism Index

7th 3rd&largest in the world

largest in Asia

The leading indicator of business confidence for Southeast Asia region

| QUARTER 1, 2016

In 2014, ASEAN economy was

the the

SALES VOLUME

NETPROFIT

SELLING PRICE

INVENTORY EMPLOYMENT

Businesses are asked to give their outlook on six key indicators

ASEAN-6INDONESIA

MALAYSIA

PHILIPPINES

SINGAPORE

THAILAND

VIETNAM

SALES VOLUME

NET PROFIT

SELLING PRICE

NEW ORDERS

INVENTORY

EMPLOYMENT

NEW ORDERS

Source: ASEAN Secretariat

The Business Information You Need That We Have

ASIA NEWSFLASH

INDUSTRY DATAAVAILABLE IN %

INDUSTRY DATAAVAILABLE IN %

SERVICES

SERVICES

RETAIL TRADE

RETAIL TRADE

WHOLESALES TRADE

WHOLESALES TRADE

MANUFAC-TURING

MANUFAC-TURING

AGRICULTURE, FORESTRY AND FISHING

PUBLIC ADMINIS-TRATION

CONSTRUCTION

CONSTRUC-TION

FINANCE, INSURANCE AND REAL ESTATE

FINANCE, INSURANCE AND REAL ESTATE

MINING

TRANSPORTATION, COMMUNICATIONS, ELECTRIC, GAS AND SANITARY SERVICES

TRANSPORTATION, COMMUNICATIONS, ELECTRIC, GAS AND SANITARY SERVICES

31%

21%

19%

34%

20%

9%

16%

7%

1%

5%

8%

9%

8%

1%

1%

5%

5%

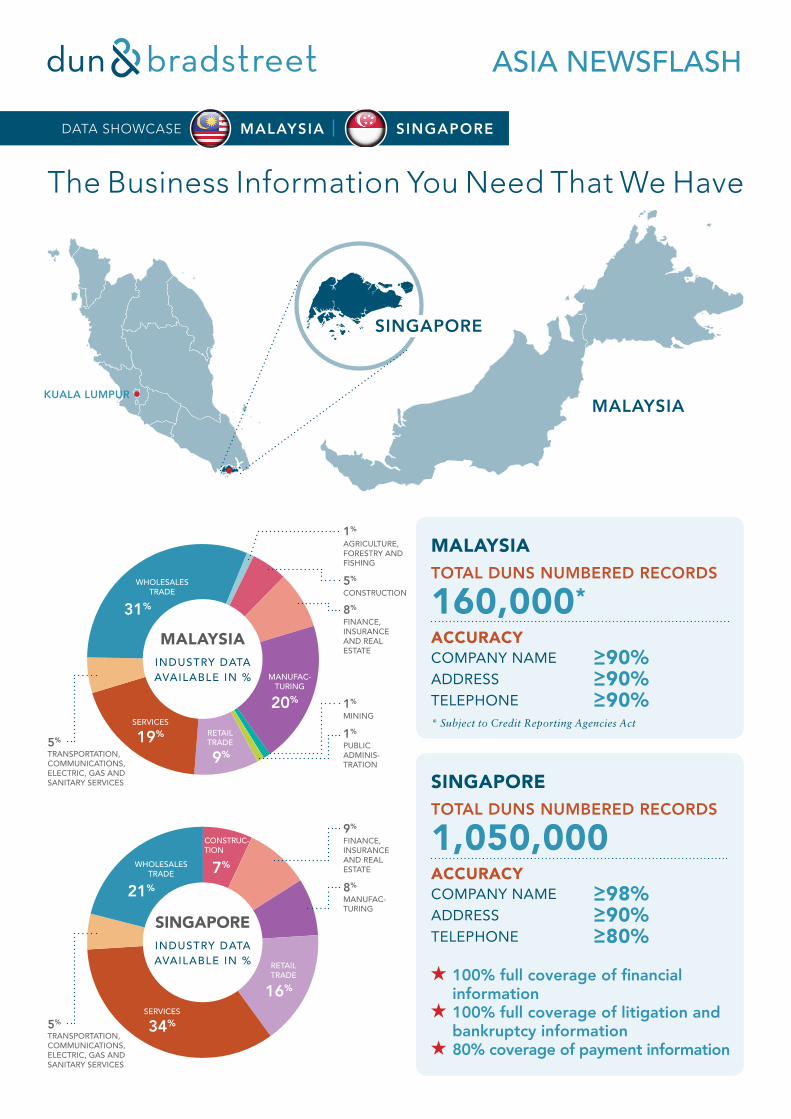

DATA SHOWCASE MALAYSIA SINGAPORE

MALAYSIATOTAL DUNS NUMBERED RECORDS

160,000*

ACCURACYCOMPANY NAME 90%ADDRESS 90%TELEPHONE 90%

SINGAPORETOTAL DUNS NUMBERED RECORDS

1,050,000ACCURACYCOMPANY NAME 98%ADDRESS 90%TELEPHONE 80%

100% full coverage of financial information

100% full coverage of litigation and bankruptcy information

80% coverage of payment information

KUALA LUMPURMALAYSIA

MALAYSIA

SINGAPORE

SINGAPORE

* Subject to Credit Reporting Agencies Act

VIETNAM AUTO SALES FASTEST IN REGION

Vietnam became the fastest growing automobile market in Southeast Asia in 2015 with reported sales of close to 60 percent. The Vietnam Automobile Manufacturers’ Association stated that at least 215,520 vehicles which include SUVs, passenger cars and commercial vehicles, were sold this year. This comes despite consumers having to pay more in tariffs and fees as compared to other countries. Analysts state that one reason for higher sales is easier loans for consumers.

WHAT’S THE BUSINESS OUTLOOK FOR INDIA?

As 2015 came to a close, the Bharatiya Janata Party (BJP)-led National Democratic Alliance (NDA) government was eager to emphasize its successes over the last 18 months. Prime Minister Narendra Modi said his government has brought down inflation while increasing GDP growth and foreign investment. He stressed that India’s economy has continued to grow as a result of his policies despite global economy slowdown. But not all has been smooth sailing…

FULL FOREIGN OWNERSHIP IN E-COMMERCE

Rudiantara, Minister of Communications and Informatics recently said that the government would allow 100% foreign ownership in local e-commerce businesses. New regulations will apply to prominent e-commerce corporations which have received previous rounds of funding and are valued at over US$1 billion. But the government will not allow foreign funding for small and medium enterprises and startups as they believe such firms still require protection.

YANGON STOCK EXCHANGE IS NOW OPEN

On December 9, 2015, Myanmar’s new stock exchange – the Yangon Stock Exchange (YSX) – opened with big expectations. However, despite the grand opening and the US $24 million investment, the bourse will not be operational until February of 2016, or later. So is this really the beginning of a new economic era, or is the new move by the administration being rushed before the country is ready? The success of YSX will ultimately depend on further reforms.

RETAIL INVESTOR CONFIDENCE IS SINKING

Retail investor confidence for the coming six months has dipped sharply. The JP Morgan Investor Confidence Index fell by 15 points to 101 in December, reaching its lowest level since June 2012. Local analysts believe that despite the dip, investment patterns in the country will not change significantly. In fact, 85 percent of respondents stated plans to remain invested in Singapore and only a small number indicated a roll back of investments.

REGIONAL BRIEFING

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

READ MORE

ASIA NEWSFLASH

These articles first appeared in Asia Briefing, a subsidiary of Dezan Shira Group Ltd, and are licensed to post in Asia Newsflash.

February 2016

HEALTH INSURANCE INDUSTRY ON FAST-TRACK

Today, over 95 percent of Chinese citizens are enrolled in various public health insurance plans, thanks to the country’s healthcare reform. However, the scope of public insurance coverage is far less than adequate with low reimbursement rates – patented medicine, usage of high-end medical devices and special needs are usually not covered. The government is also concerned with its ability to sustain the social welfare system due to its rapidly aging population.

DOMESTIC AVIATION GROWTH SET TO SOAR

Vietnam’s aviation market is expected to grow by 19 percent in 2016 equaling 45 million passengers. The domestic sector is forecast to increase by 23.4 percent. In addition, the competition between state-owned and national carrier Vietnam Airlines and private low-cost carrier Vietjet Air is expected to be more intense in the coming year. Centre for Aviation (CAPA) an aviation consultancy stated that Vietjet Air could overtake Vietnam Airlines by March.

HOW TO TERMINATE YOUR MANAGER IN CHINA

When it comes to hiring and firing in China, foreign managers and investors should not hold preconceived ideas about the strictness of China’s laws. Highly publicized cases of worker exploitation might give the impression that China unambiguously favors employers, but this is not so. In fact, China’s laws for firing employees are considerably more rigid than those in the U.S. Here’s a case study on how a successful termination can be made.

NEW INDIA–MYANMAR–THAILAND HIGHWAY

The India–Myanmar–Thailand Trilateral Highway is an ambitious project of 1990 miles (3200 km), and a part of India’s upgraded “Act East” policy which seeks to strategically build India’s link with the Southeast Asia region. The highway which will be completed by 2018, links Moreh in Manipur state (India), via Mandalay city (Myanmar) and to Mae Sot district (Thailand). The project comes off the heels of the the proposed India–ASEAN trade center.

LOOKING AHEAD AT GERMANY’S TRADE WITH ASEAN – PART 1

As 2015 has come to an end, both Germany and ASEAN can reflect back on an impressive year of trade relations. In a climate of global

uncertainty, both geographical regions managed to expand trade and sign several important trade agreements. With its population of roughly 622 million people, the ten ASEAN nations present a stable political environment and a growing middle class, whose purchasing power will rise over the next years. The countries present a formidable export market for German goods, as well as a stable investment climate for production and outward FDI.

Most recently, Germany, as part of the European Union, entered into a Free Trade Agreement with Vietnam. A declaration on the agreement was signed in early December 2015 and entry into force is expected – even by conservative estimates – as soon as 2018. ASEAN still counts as one of the most important growth markets for German industry and there remains untapped potential, especially in the green energy sector. The following will give an overview of the most important ASEAN nations and their trade relationship with Germany. For the next years, growth will undoubtedly continue and businesses will move away from the traditional low cost markets, like China, to ASEAN nations.

Germany benefits from any Free Trade Agreements negotiated and signed by the European Union. Negotiations to extend FTAs with ASEAN nations are of great economic importance to Germany, who sees ASEAN’s economic potential and dynamic business landscape as a largely untapped market. Currently, Germany lags behind bigger players like the United States and Japan, who have had a strong presence for a while and benefit from their own FTAs.

ASEAN is seen as a worthwhile alternative to the BRICS countries, with its modest predicted growth of five percent across the region in 2015-2019. Being able to take advantage of new Free Trade Agreements will surely open the market for higher level of German FDI and production inflow.

READ MORE

READ MORE

READ MORE READ MORE

ASIA NEWSFLASH

These articles first appeared in Asia Briefing, a subsidiary of Dezan Shira Group Ltd, and are licensed to post in Asia Newsflash.

REGIONAL BRIEFING

February 2016

SubscribeIf you wish to stay informed and directly receive industry newsfeeds or market updates regarding specific countries (below) on a regular basis, kindly contact the following:

CHINA : Monthly Market Watch (Chinese) [email protected] : Daily News Headlines (English) [email protected] : Monthly Bankruptcy Trends (Japanese) marketing.tsr-net : TSR Global Economic News (Japanese) marketing.tsr-netMALAYSIA : Weekly News Bites (English) [email protected] : Weekly News Bites (English) [email protected] : Weekly News Bites (English) [email protected]

FeedbackWe welcome your feedback so please send us your comments or email [email protected] to subscribe or unsubscribe to the monthly Newsflash.

DisclaimerThe information in this newsletter is provided “as is” without warranty of any kind. In no event will D&B or its information providers be liable in any way with regard to such information or your use of it. D&B makes no representations, warranties or endorsements with respect to any websites or services that are linked to this newsletter, or information thereon. When you access a non-D&B site, or information from a non-D&B site, you acknowledge that D&B has no control over the content or information at that site, and that it is your responsibility to protect your systems from viruses and other items of a destructive nature.

© 2016 Dun & Bradstreet, Inc.