Muni bond buyers_conf_2014

16

61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com The Interest Rate Risk of Municipal Bonds February 24, 2014

-

Upload

kalotayanalytics -

Category

Economy & Finance

-

view

2.375 -

download

0

Transcript of Muni bond buyers_conf_2014

61 Broadway New York, NY 10006 212.482.0900 www.kalotay.com

The Interest Rate Risk of Municipal Bonds

February 24, 2014

2

Challenges of Managing Munis

Today’s topic:

Gains and losses are subject to complex tax treatmentTaxes affect value, interest rate risk, and OAS of bonds

currently or potentially selling at a discount

Need analytics for hedging and scenario analysis

Standard systems ignore taxes when calculating effective

duration (exception: Investortools)

Topic for another day:

Active managers could achieve superior after-tax return by

strategic tax-loss harvestingEvery muni is a potential candidate

Need to determine resulting benefit and optimum time to sell

3

Tax Considerations of Discount Munis

Gain at maturity is taxableTaxed as ordinary income if purchased below de minimis

(for individuals as high as 43.4%)

Above de minimis taxed as capital gains at 23.8%

Rates above include Obamacare surcharge

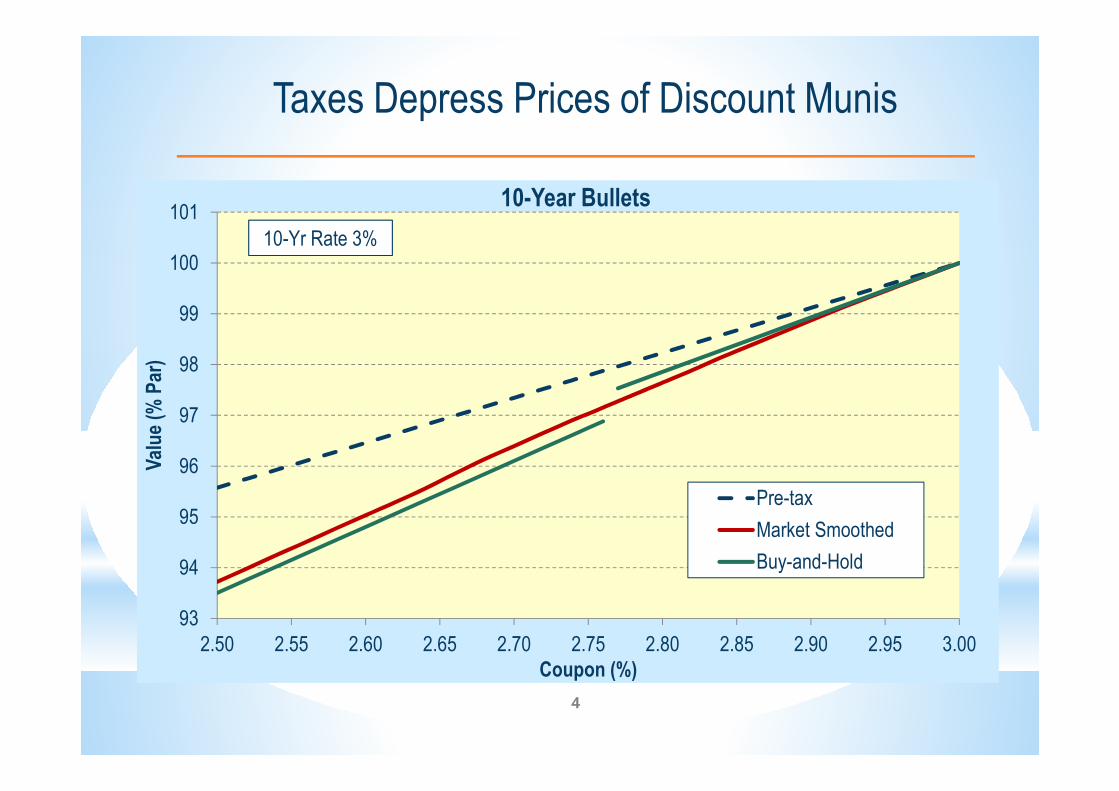

Tax on gain depresses market price (see next slide)When rates rise performance based on mark-to-market suffers

unduly (corroborated by EMMA prices – see Ang, et. al.,

Journal of Finance, 2010)

However ‘hold value’ is investor-specificTax paid by current holder depends on purchase date and price

Hold value can far exceed market price

4

Taxes Depress Prices of Discount Munis

93

94

95

96

97

98

99

100

101

2.50 2.55 2.60 2.65 2.70 2.75 2.80 2.85 2.90 2.95 3.00

Val

ue

(% P

ar)

Coupon (%)

10-Year Bullets

Pre-tax

Market Smoothed

Buy-and-Hold

10-Yr Rate 3%

5

When Rates Rise Price of Muni Declines MoreThan Predicted by Pre-Tax Analytics

93

94

95

96

97

98

99

100

101

2.95 3.05 3.15 3.25 3.35 3.45

% P

ar

10-Year Rate (%)

10-Year 3% Bond

Pre-tax Value

Price

6

When Rates Rise Prices Will Fall More Than ExpectedBond Buyer, March 18, 2013

Single-A

Par Bonds

Rates Rise 100bps

Standard Approach Kalotay ApproachMistake by

Standard Approach

Price Yield Price Yield PriceYield

(bps)

2-yr 0.90% 98.05 1.90 96.82 2.54 -1.23 64

5-yr 1.65% 95.35 2.65 92.84 3.21 -2.51 56

10-yr 3.00% 91.82 4.00 88.94 4.38 -2.88 38

7

Investors Punish Low Coupon Bonds

… buyers demanded an additional 40 basis points for 4% coupon bonds,

industry analysts estimated, … [and] … they demanded

an additional 80 basis points for 3% coupons [relative to 5% bonds].

8

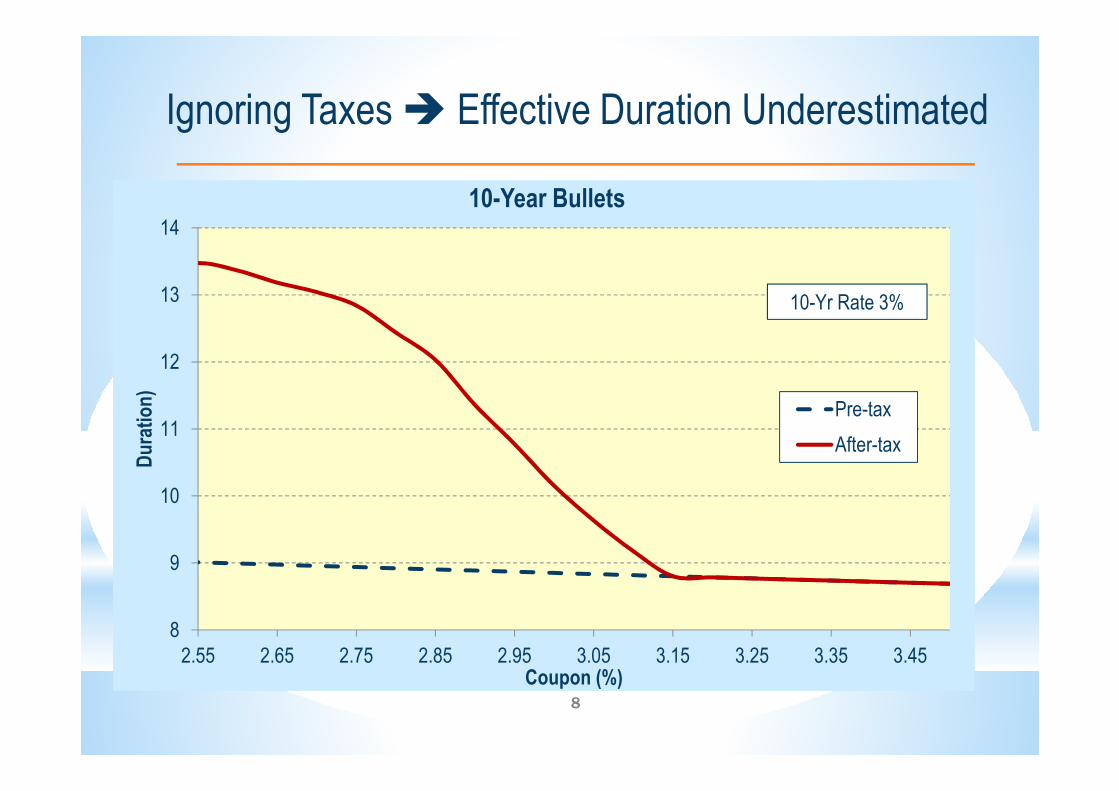

9

10

11

12

13

14

2.55 2.65 2.75 2.85 2.95 3.05 3.15 3.25 3.35 3.45

Du

rati

on

)

Coupon (%)

10-Year Bullets

Pre-tax

After-tax

Ignoring Taxes � Effective Duration Underestimated

10-Yr Rate 3%

8

9

Ignoring Taxes �OAS Overestimated

0

20

40

60

80

100

120

140

160

88 90 92 94 96 98 100

OA

S (

bp

s)

Price (% par)

3% 10-Year Bullet

After-tax

Pre-tax

10-Yr Rate 3%

10

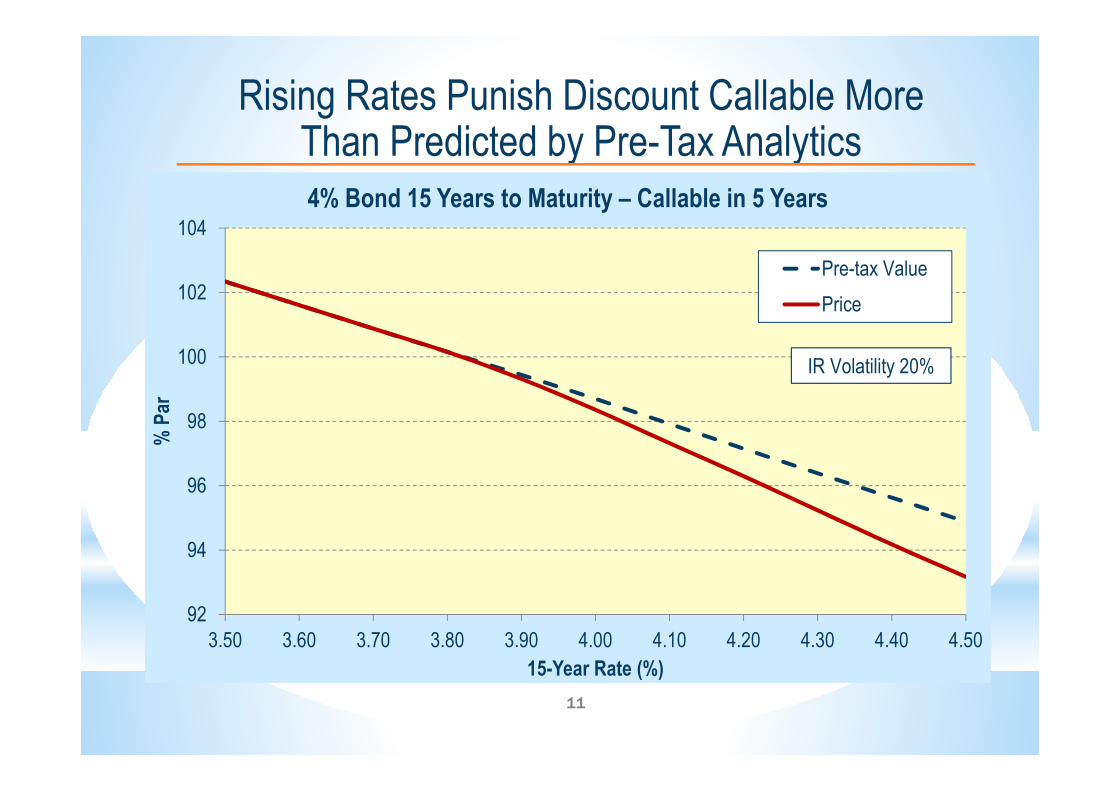

Callable Bonds Get Hit by a Double WhammyWhen Rates Rise

Because likelihood of refunding is reduced, expected life of

bond is extended and price declines accordinglyTaxables are no exception

But steeply upward-sloping muni curve exacerbates impact

When price falls below par, taxes make matters worse Unique to munis

11

Rising Rates Punish Discount Callable More Than Predicted by Pre-Tax Analytics

92

94

96

98

100

102

104

3.50 3.60 3.70 3.80 3.90 4.00 4.10 4.20 4.30 4.40 4.50

% P

ar

15-Year Rate (%)

4% Bond 15 Years to Maturity – Callable in 5 Years

Pre-tax Value

Price

IR Volatility 20%

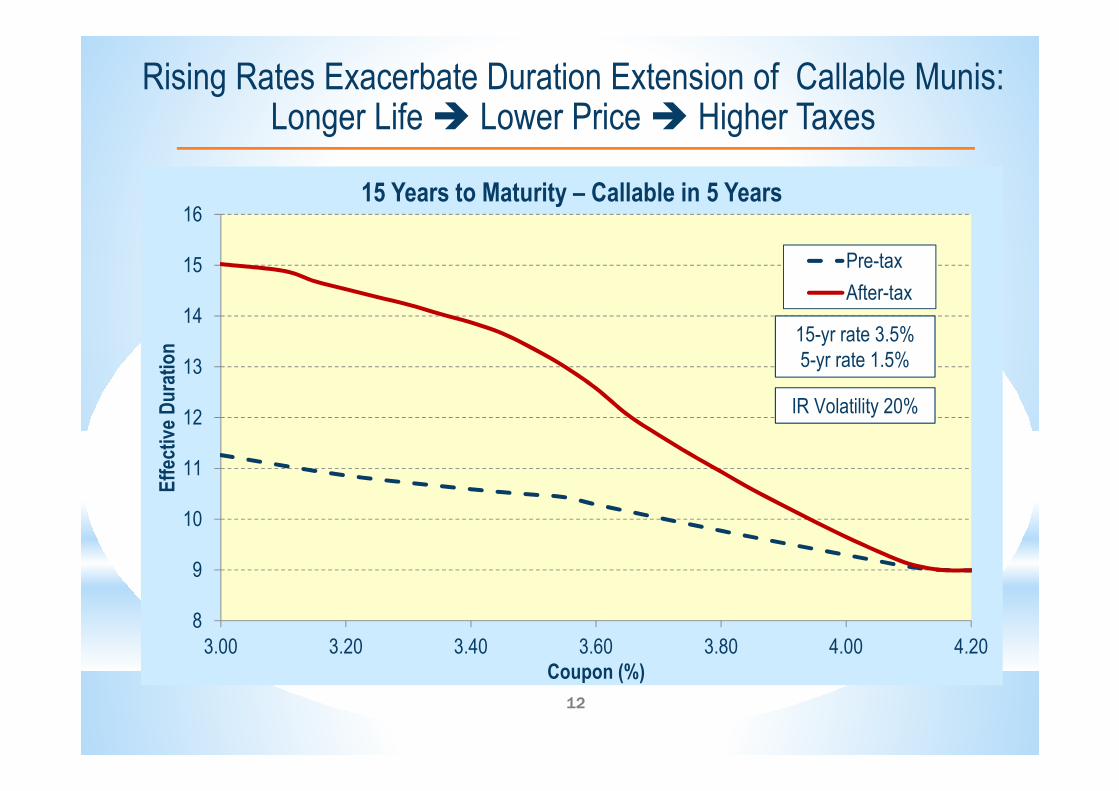

8

9

10

11

12

13

14

15

16

3.00 3.20 3.40 3.60 3.80 4.00 4.20

Eff

ecti

ve D

ura

tio

n

Coupon (%)

15 Years to Maturity – Callable in 5 Years

Pre-tax

After-tax

IR Volatility 20%

15-yr rate 3.5%

5-yr rate 1.5%

12

Rising Rates Exacerbate Duration Extension of Callable Munis:Longer Life � Lower Price � Higher Taxes

13

Analytical Approach: Overlay Taxes on Standard OAS Framework

Capital gains and losses are taxableTreatment of callables and OID’s is particularly challenging

Investors assumed to be in the top tax bracket

Key concepts: tax-neutral ‘fair’ price and OASFair price equals the PV after-tax cashflows, including tax

payable at maturity; determined iteratively

Tax-neutral OAS adjusts for both call option and taxes

Essential for managing interest rate risk and to enhance

after-tax performance

14

Recap: Taxes Affect Effective Duration and OAS

Discount bonds are much more sensitive to interest rates

than reported by standard analytics systemsUnpleasant surprise when rates rise

Wider than normal spread for a discount bond does not

mean that bond is cheap For rigorous rich-cheap analysis use tax-neutral OAS

15

References

“The Interest Rate Sensitivity of Tax-Exempt Bonds Under Tax-Neutral Valuation”

The Journal of Investment Management (First Quarter 2014)

“The Tax Option in Municipal Bonds”

The Journal of Portfolio Management (Winter 2014)

“How to Take a Tax Loss and Then Profit from Obamacare”

The Bond Buyer, December 11, 2013

“For Investors, Stress-testing Munis is Easier Said Than Done”

The Bond Buyer, March 18, 2013.

“The Allure of 5% Bonds: Coupon Levitation Creates Magical Savings”

The Bond Buyer, January 27, 2012

"Taxes on Tax-Exempt Bonds,” Ang, A., V. Bhansali, and Y. Xing,

Journal of Finance 65 (No. 2), 565-60, 2010

See kalotay.com/research