Muhammad Arif Sargana Director (Economic Affairs) Pakistan ... WSIS Targets & Digital... ·...

28

Muhammad Arif Sargana Director (Economic Affairs) Pakistan Telecommunication Authority Sept, 2016 Islamabad, Pakistan

-

Upload

hoangkhuong -

Category

Documents

-

view

221 -

download

0

Transcript of Muhammad Arif Sargana Director (Economic Affairs) Pakistan ... WSIS Targets & Digital... ·...

Muhammad Arif Sargana

Director (Economic Affairs)

Pakistan Telecommunication Authority

Sept, 2016

Islamabad, Pakistan

Affordable BB Services o Fast Track right of way o USF to fund BB access in un-served areas o Fast Fiber roll out

Availability of Spectrum o Immediate auction of spectrum in 2100 & 850 MHZ o Spectrum Reframing o Spectrum availability for digital Microwaves

Suitable Backhaul o Improve access to national On-line Services o Diversity of routing o Load sharing on international capacity

Competition in Retail BB

◦ Framing Sector specific Competition Rules

◦ Incumbent obliged to provide last mile

infrastructure

◦ Availability of Wi-Fi Hot spots

◦ Encourage the development of contents

Market Research Organizations (BMI, Gallup, Ericsson Research Lab, etc)

International organizations (ITU, GSMA, World Bank, etc.)

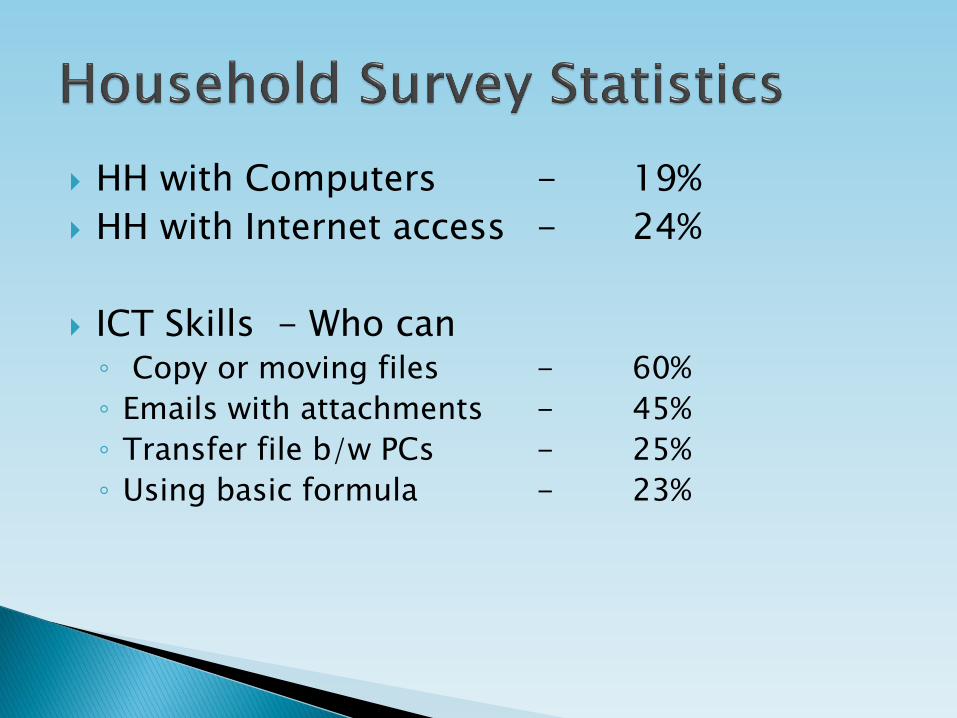

HH with Computers - 19%

HH with Internet access - 24%

ICT Skills - Who can ◦ Copy or moving files - 60%

◦ Emails with attachments - 45%

◦ Transfer file b/w PCs - 25%

◦ Using basic formula - 23%

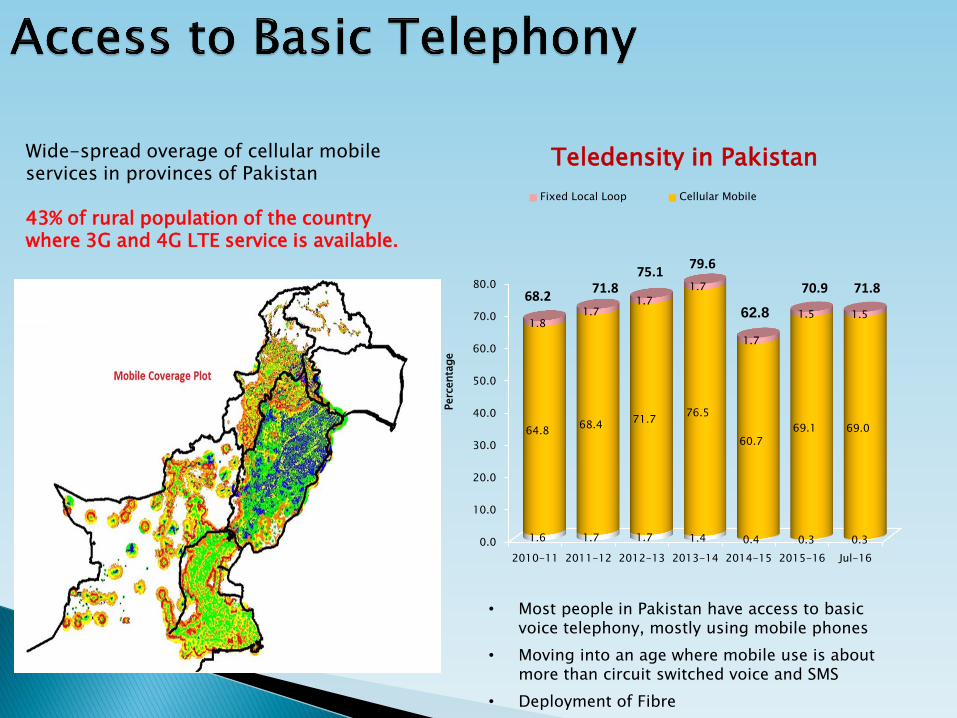

• Most people in Pakistan have access to basic voice telephony, mostly using mobile phones

• Moving into an age where mobile use is about more than circuit switched voice and SMS

• Deployment of Fibre

Wide-spread overage of cellular mobile services in provinces of Pakistan 43% of rural population of the country where 3G and 4G LTE service is available.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 Jul-16

1.6 1.7 1.7 1.4 0.4 0.3 0.3

64.8 68.4

71.7 76.5

60.7

69.1 69.0

1.8 1.7

1.7

1.7

1.7

1.5 1.5

Perc

enta

ge

Fixed Local Loop Cellular Mobile

79.6 75.1

71.8 68.2

70.9

62.8

71.8

Teledensity in Pakistan

78.0

81.5

86.0

74.0

76.0

78.0

80.0

82.0

84.0

86.0

88.0

2013 2014 2015

Perc

enta

ge

(Rural/Urban)

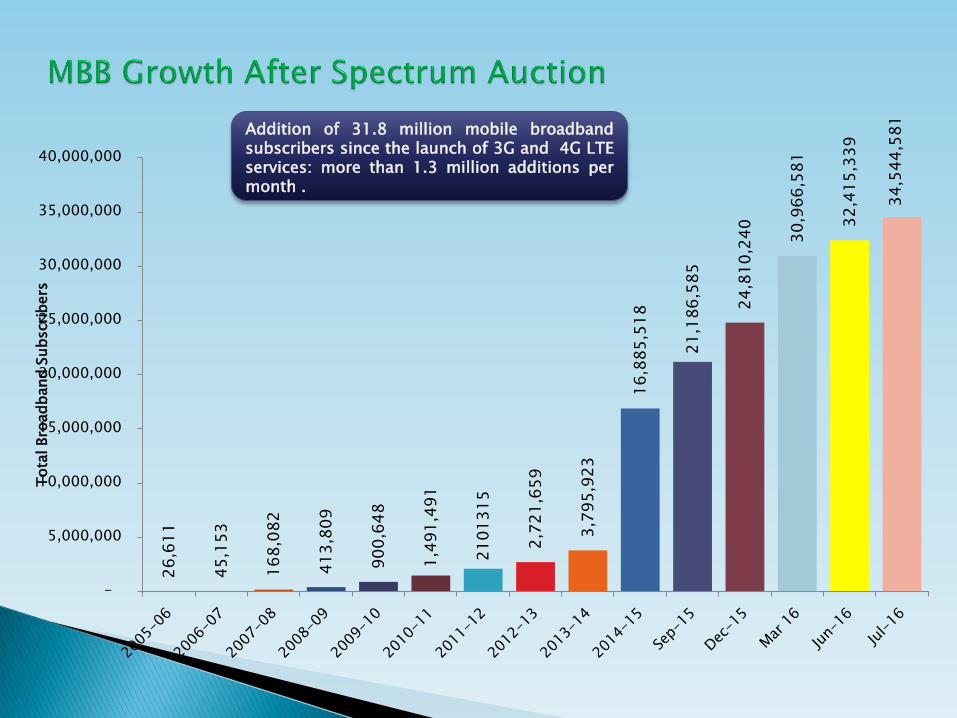

26,6

11

45,1

53

168,0

82

413,8

09

900,6

48

1,4

91,4

91

2101315

2,7

21,6

59

3,7

95,9

23

16,8

85

,51

8

21,1

86

,58

5

24,8

10

,24

0

30,9

66

,58

1

32,4

15

,33

9

34,5

44

,58

1

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

Tota

l Bro

adband S

ubscri

bers

Addition of 31.8 million mobile broadband subscribers since the launch of 3G and 4G LTE services: more than 1.3 million additions per month .

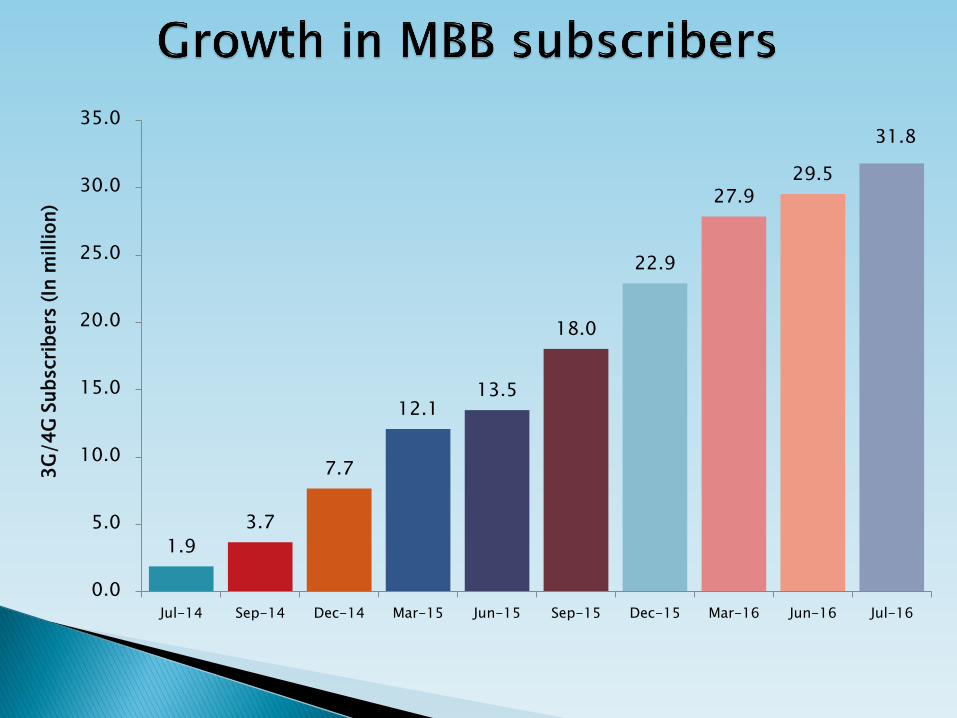

1.9

3.7

7.7

12.1 13.5

18.0

22.9

27.9 29.5

31.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jul-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Jul-16

3G

/4

G S

ub

scri

bers

(In

million)

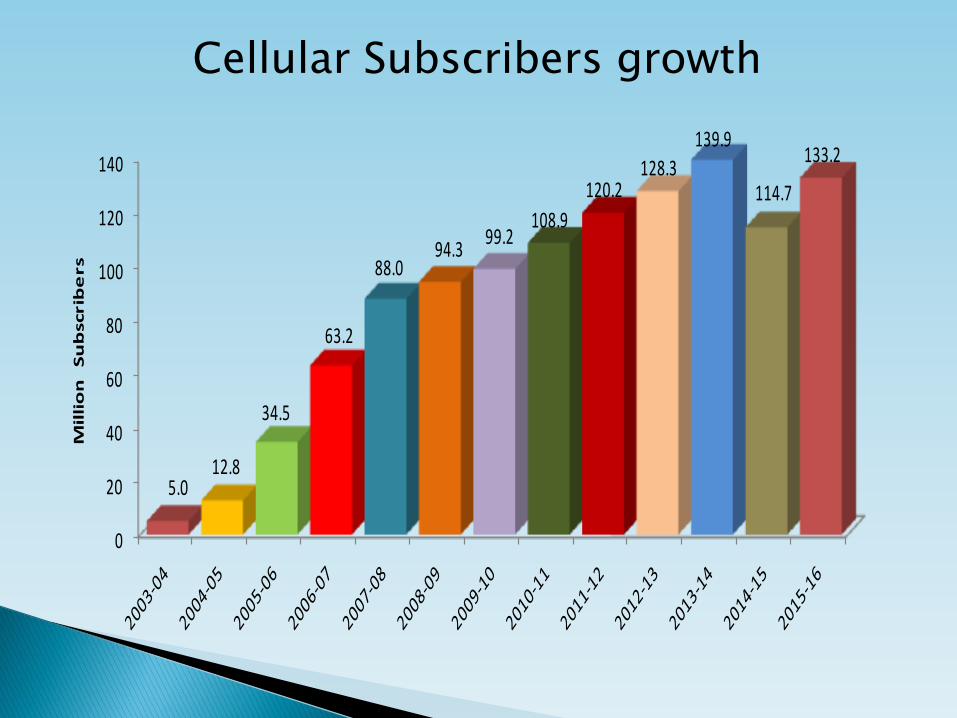

Cellular Subscribers growth

0

20

40

60

80

100

120

140

5.012.8

34.5

63.2

88.094.3

99.2108.9

120.2128.3

139.9

114.7

133.2

Mil

lio

n

Su

bscrib

ers

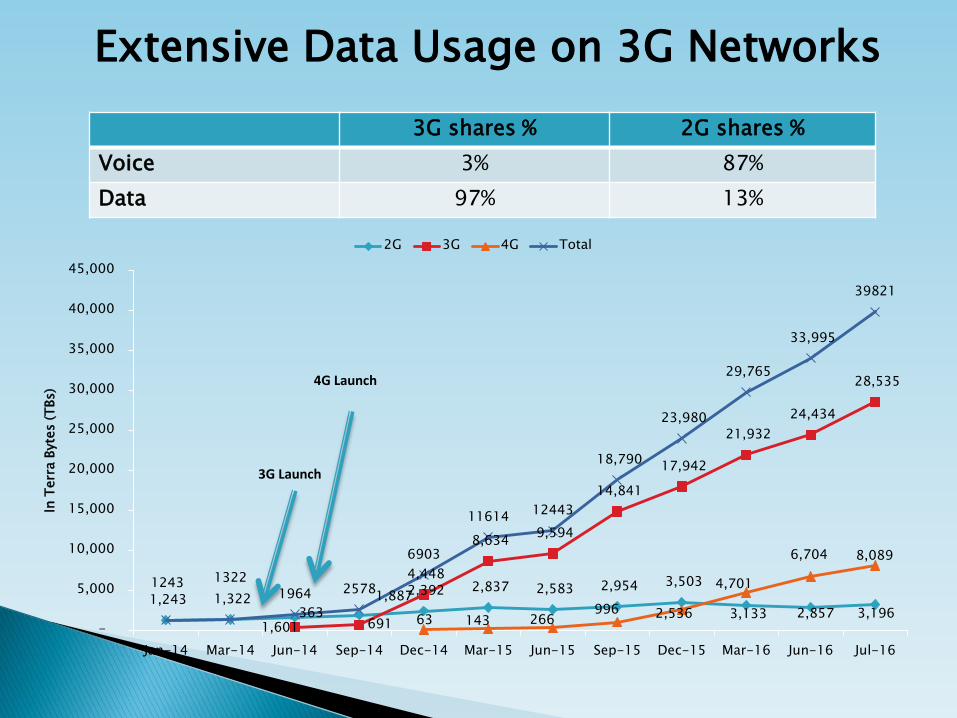

Extensive Data Usage on 3G Networks

3G shares % 2G shares %

Voice 3% 87%

Data 97% 13%

1,243 1,322

1,601

1,887 2,392 2,837 2,583 2,954 3,503

3,133 2,857 3,196 363 691

4,448

8,634 9,594

14,841

17,942

21,932

24,434

28,535

63 143 266 996 2,536

4,701

6,704 8,089

1243 1322 1964 2578

6903

11614 12443

18,790

23,980

29,765

33,995

39821

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Jan-14 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Jul-16

In T

err

a B

yte

s (T

Bs)

2G 3G 4G Total

3G Launch

4G Launch

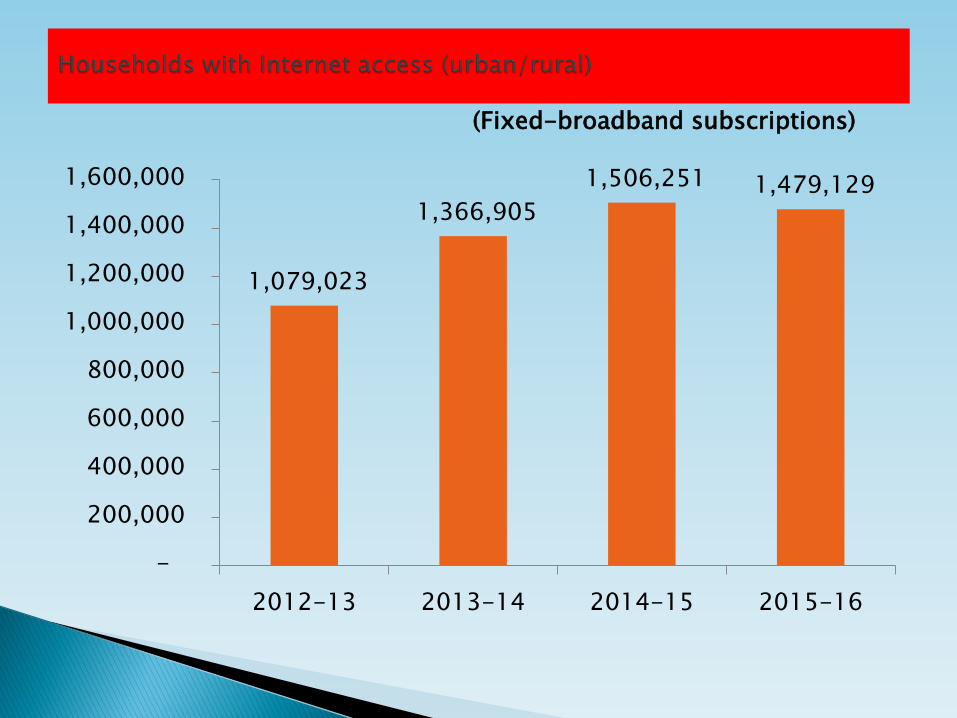

1,079,023

1,366,905

1,506,251 1,479,129

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2012-13 2013-14 2014-15 2015-16

(Fixed-broadband subscriptions)

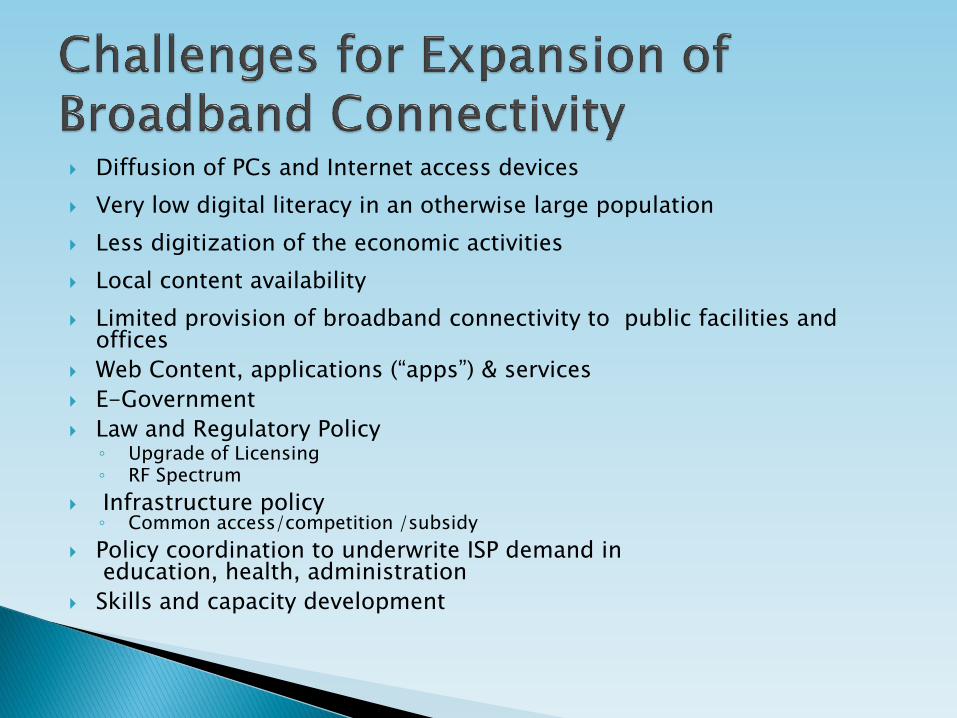

Diffusion of PCs and Internet access devices

Very low digital literacy in an otherwise large population

Less digitization of the economic activities

Local content availability

Limited provision of broadband connectivity to public facilities and offices

Web Content, applications (“apps”) & services

E-Government

Law and Regulatory Policy ◦ Upgrade of Licensing ◦ RF Spectrum

Infrastructure policy ◦ Common access/competition /subsidy

Policy coordination to underwrite ISP demand in education, health, administration

Skills and capacity development

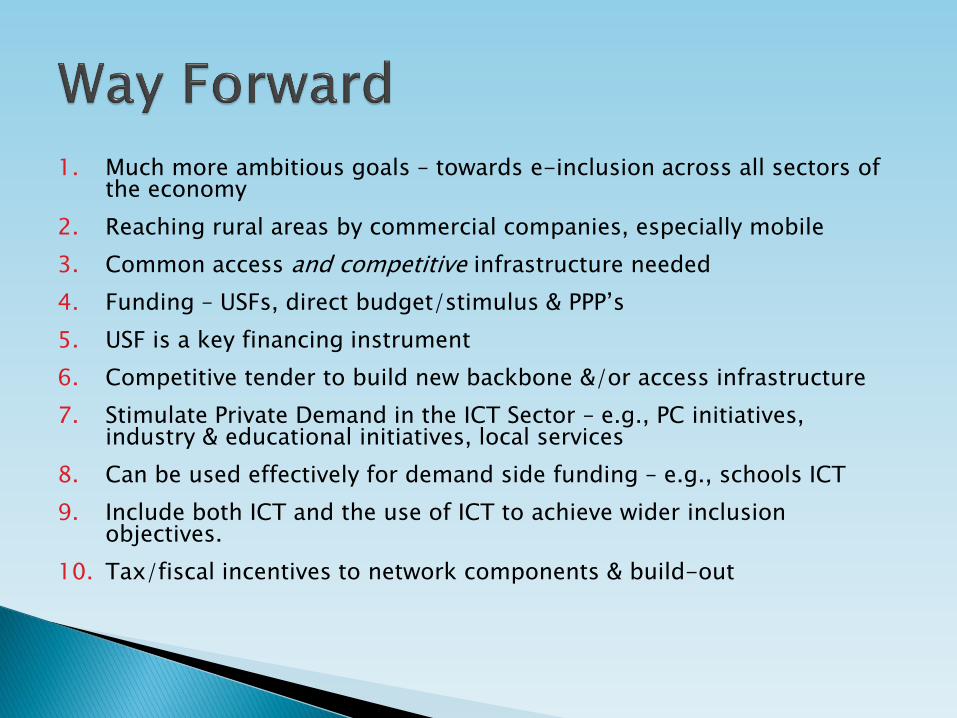

1. Much more ambitious goals – towards e-inclusion across all sectors of the economy

2. Reaching rural areas by commercial companies, especially mobile

3. Common access and competitive infrastructure needed

4. Funding – USFs, direct budget/stimulus & PPP’s

5. USF is a key financing instrument

6. Competitive tender to build new backbone &/or access infrastructure

7. Stimulate Private Demand in the ICT Sector – e.g., PC initiatives, industry & educational initiatives, local services

8. Can be used effectively for demand side funding – e.g., schools ICT

9. Include both ICT and the use of ICT to achieve wider inclusion objectives.

10. Tax/fiscal incentives to network components & build-out

Digital Financial Services: The

Case of Pakistan

16

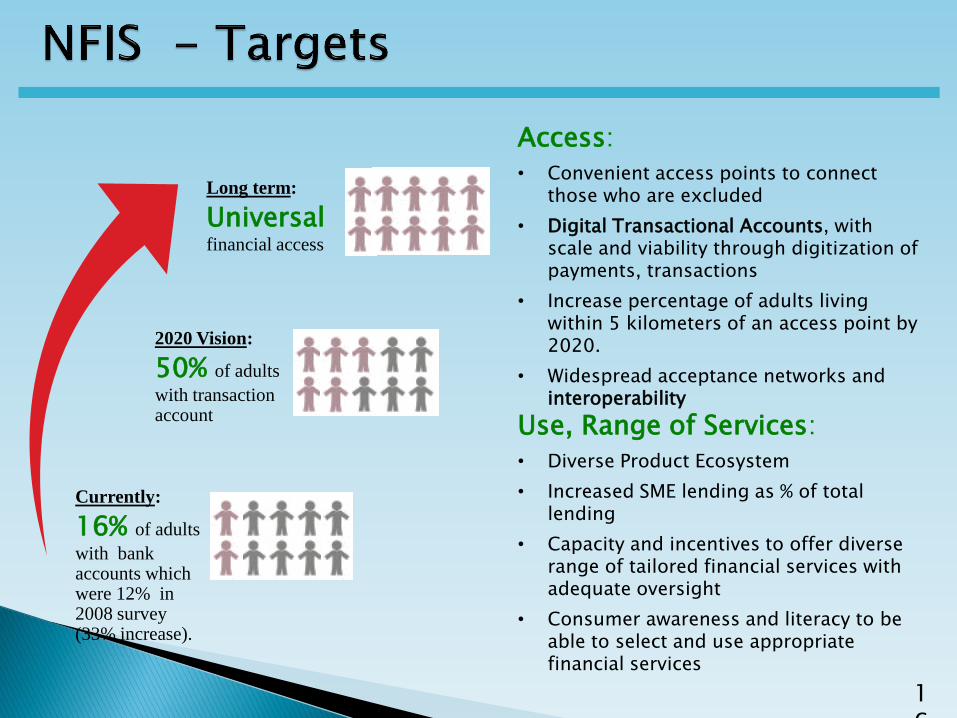

Access:

• Convenient access points to connect those who are excluded

• Digital Transactional Accounts, with scale and viability through digitization of payments, transactions

• Increase percentage of adults living within 5 kilometers of an access point by 2020.

• Widespread acceptance networks and interoperability

Use, Range of Services:

• Diverse Product Ecosystem

• Increased SME lending as % of total lending

• Capacity and incentives to offer diverse range of tailored financial services with adequate oversight

• Consumer awareness and literacy to be able to select and use appropriate financial services

Currently:

16% of adults

with bank accounts which were 12% in 2008 survey (33% increase).

2020 Vision:

50% of adults

with transaction account

Long term:

Universal financial access

Regulatory Environment

Two Regulators- Central bank and Telecom Regulator Working Together

Separate Regulations by Both regulators – Jointly prepared

SBP’s Branchless Banking Regulations, 2008 (updated 2011)

PTA’s Regulations for Technical Implementation of Mobile Banking, 2016

SBP’s Regulations for Mobile Banking Interoperability, 2016

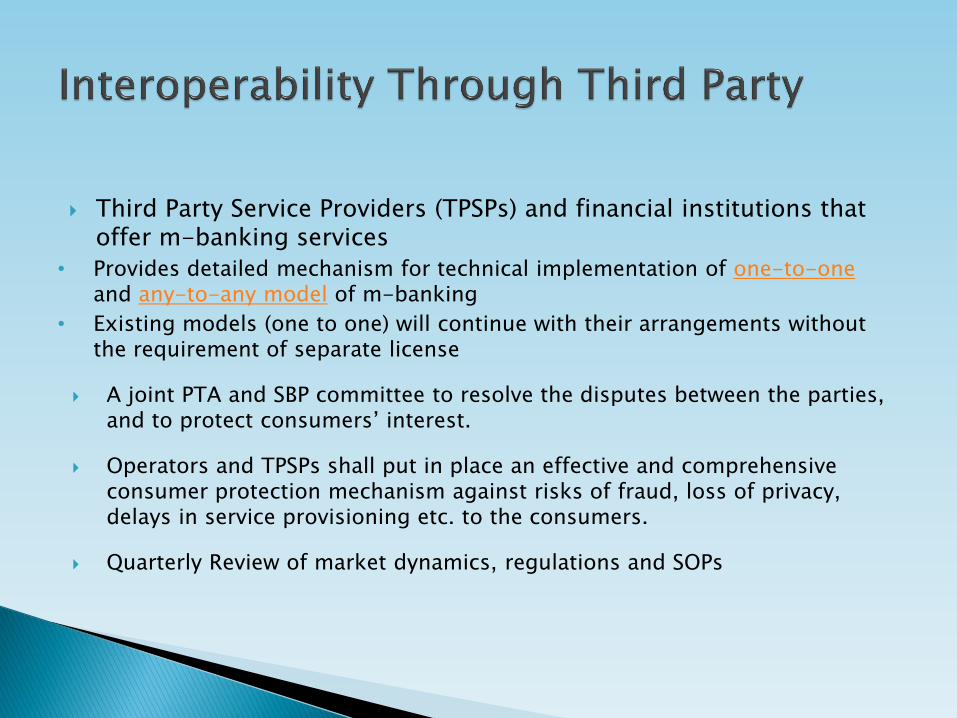

Third Party Service Providers (TPSPs) and financial institutions that offer m-banking services

• Provides detailed mechanism for technical implementation of one-to-one and any-to-any model of m-banking

• Existing models (one to one) will continue with their arrangements without the requirement of separate license

A joint PTA and SBP committee to resolve the disputes between the parties, and to protect consumers’ interest.

Operators and TPSPs shall put in place an effective and comprehensive consumer protection mechanism against risks of fraud, loss of privacy, delays in service provisioning etc. to the consumers.

Quarterly Review of market dynamics, regulations and SOPs

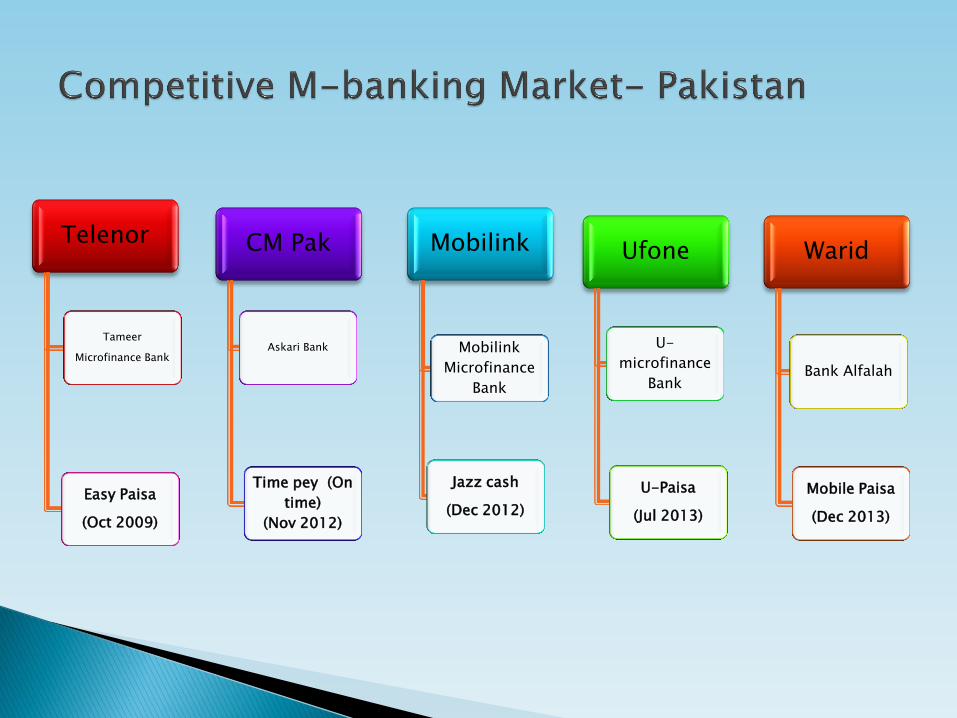

Telenor

Tameer

Microfinance Bank

Easy Paisa

(Oct 2009)

CM Pak

Askari Bank

Time pey (On

time)

(Nov 2012)

Mobilink

Mobilink

Microfinance

Bank

Jazz cash

(Dec 2012)

Ufone

U-

microfinance

Bank

U-Paisa

(Jul 2013)

Warid

Bank Alfalah

Mobile Paisa

(Dec 2013)

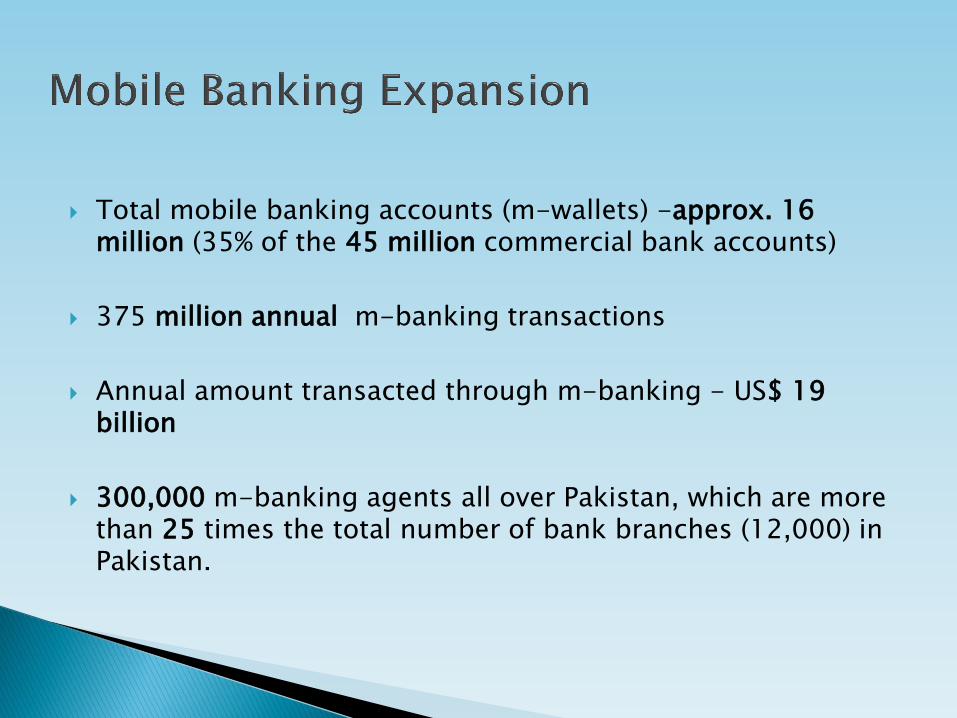

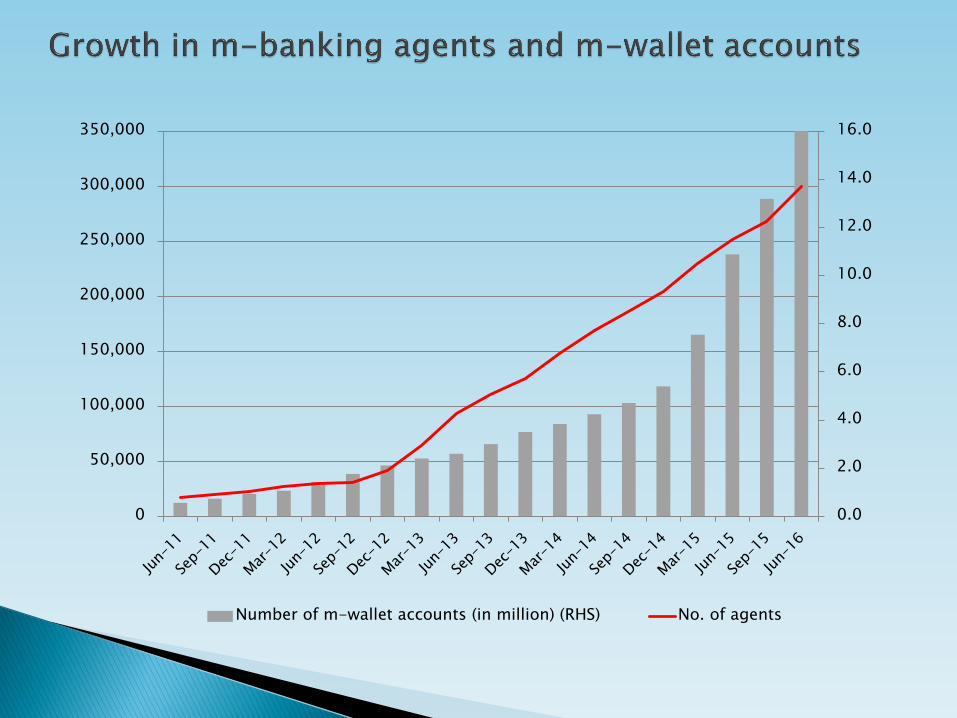

Total mobile banking accounts (m-wallets) -approx. 16 million (35% of the 45 million commercial bank accounts)

375 million annual m-banking transactions

Annual amount transacted through m-banking - US$ 19 billion

300,000 m-banking agents all over Pakistan, which are more than 25 times the total number of bank branches (12,000) in Pakistan.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Number of m-wallet accounts (in million) (RHS) No. of agents

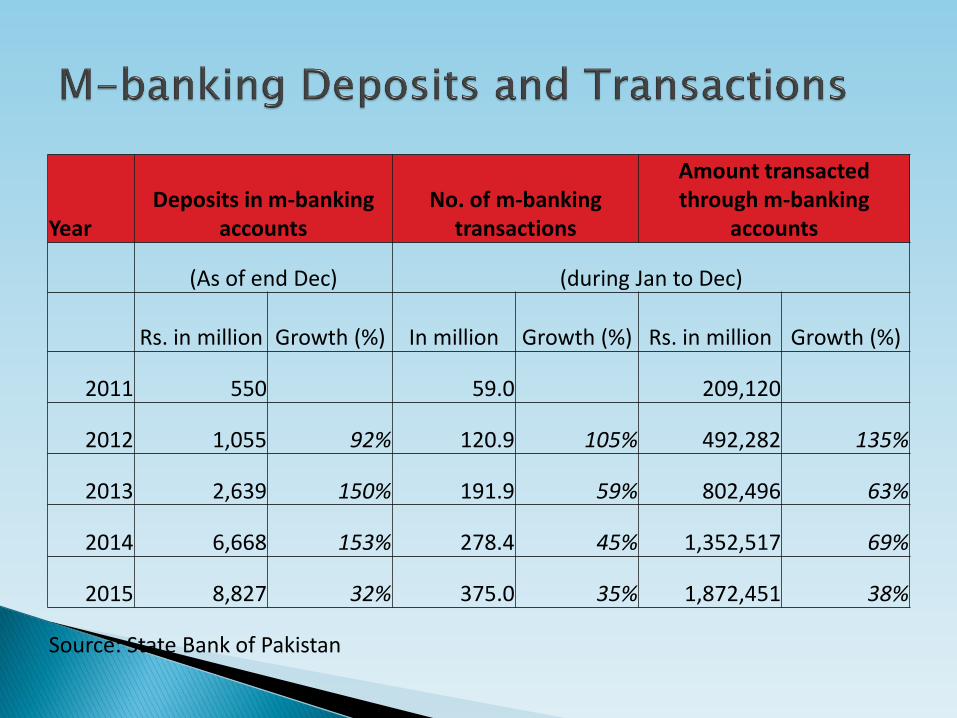

Year Deposits in m-banking

accounts No. of m-banking

transactions

Amount transacted through m-banking

accounts

(As of end Dec) (during Jan to Dec)

Rs. in million Growth (%) In million Growth (%) Rs. in million Growth (%)

2011 550 59.0 209,120

2012 1,055 92% 120.9 105% 492,282 135%

2013 2,639 150% 191.9 59% 802,496 63%

2014 6,668 153% 278.4 45% 1,352,517 69%

2015 8,827 32% 375.0 35% 1,872,451 38%

Source: State Bank of Pakistan

Low usage of m-wallet accounts

◦ Active to total m-wallet accounts ratio is only 40%

Mobile Money users are unable to use their electronic money in their daily lives in the same way they use cash – to buy their essential daily items

Expensive mobile money transactions (mostly through OTC)

Lack of merchant acceptance

High taxes (16% sales tax and 15% WHT on the earnings of agents). Govt. has also imposed additional WHT on the transaction amount of non-filer.

◦ Low Interoperability in payments

Thank you

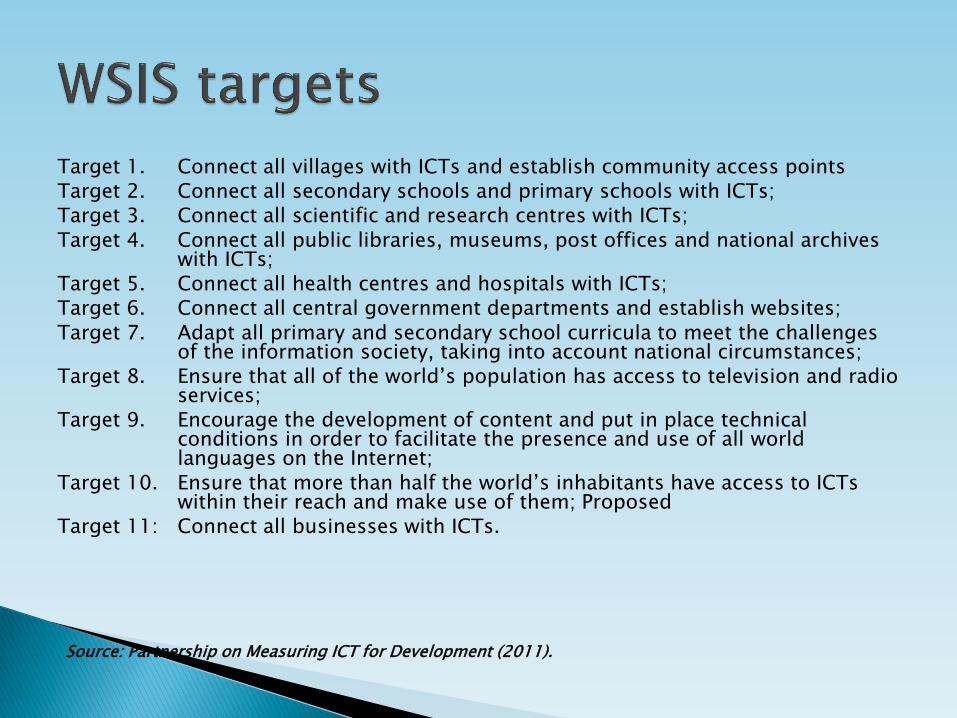

Target 1. Connect all villages with ICTs and establish community access points Target 2. Connect all secondary schools and primary schools with ICTs; Target 3. Connect all scientific and research centres with ICTs; Target 4. Connect all public libraries, museums, post offices and national archives

with ICTs; Target 5. Connect all health centres and hospitals with ICTs; Target 6. Connect all central government departments and establish websites; Target 7. Adapt all primary and secondary school curricula to meet the challenges

of the information society, taking into account national circumstances; Target 8. Ensure that all of the world’s population has access to television and radio

services; Target 9. Encourage the development of content and put in place technical

conditions in order to facilitate the presence and use of all world languages on the Internet;

Target 10. Ensure that more than half the world’s inhabitants have access to ICTs within their reach and make use of them; Proposed

Target 11: Connect all businesses with ICTs.

Source: Partnership on Measuring ICT for Development (2011).

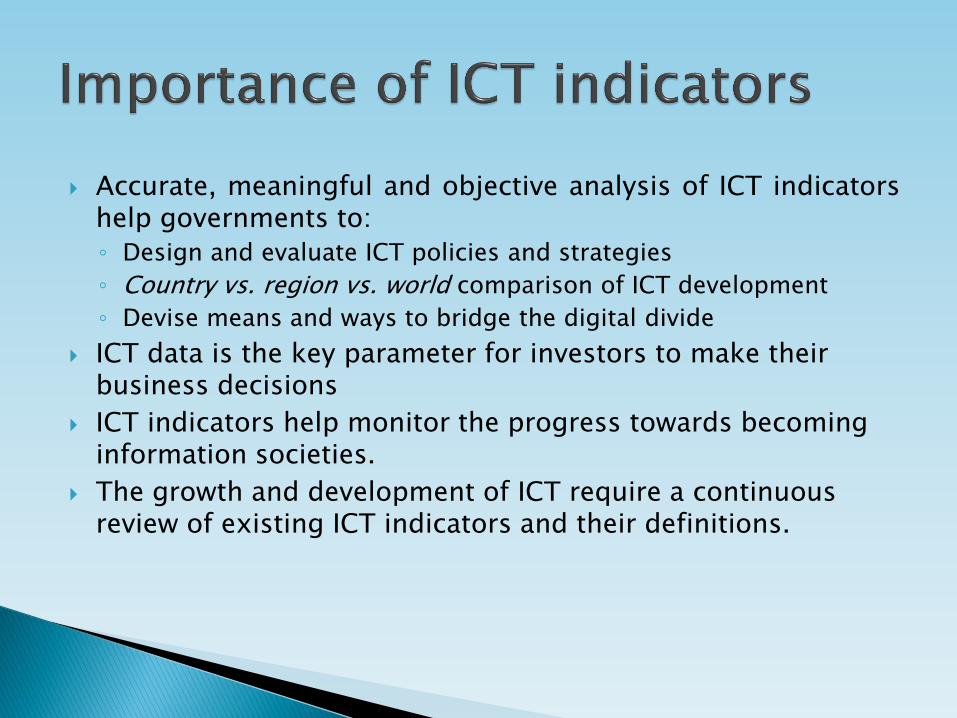

Accurate, meaningful and objective analysis of ICT indicators help governments to:

◦ Design and evaluate ICT policies and strategies

◦ Country vs. region vs. world comparison of ICT development

◦ Devise means and ways to bridge the digital divide

ICT data is the key parameter for investors to make their business decisions

ICT indicators help monitor the progress towards becoming information societies.

The growth and development of ICT require a continuous review of existing ICT indicators and their definitions.

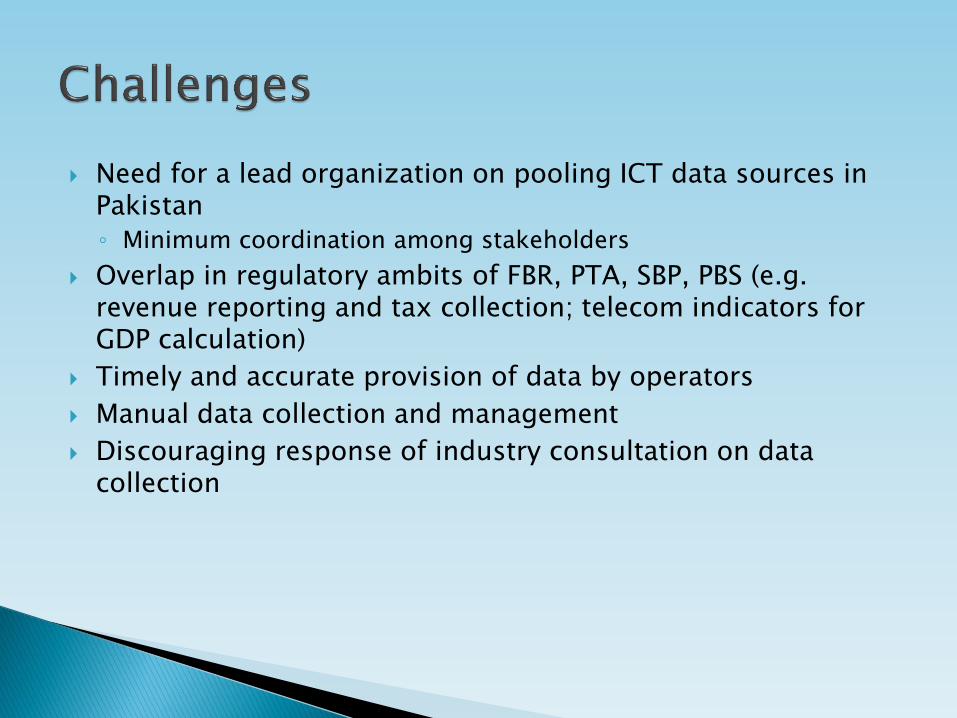

Need for a lead organization on pooling ICT data sources in Pakistan

◦ Minimum coordination among stakeholders

Overlap in regulatory ambits of FBR, PTA, SBP, PBS (e.g. revenue reporting and tax collection; telecom indicators for GDP calculation)

Timely and accurate provision of data by operators

Manual data collection and management

Discouraging response of industry consultation on data collection

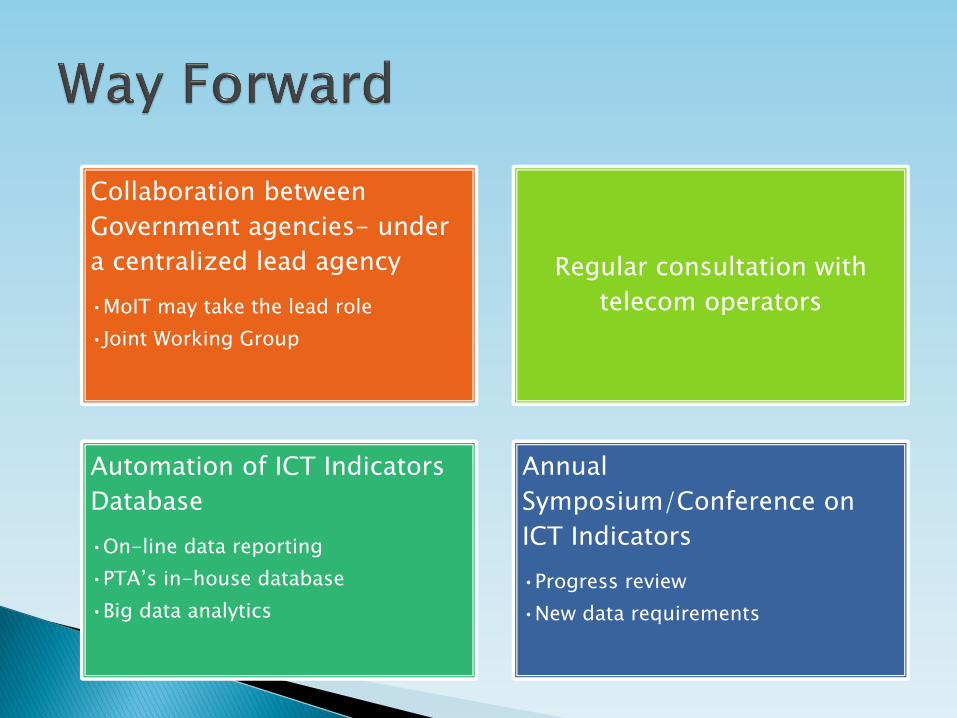

Collaboration between

Government agencies- under

a centralized lead agency

•MoIT may take the lead role

•Joint Working Group

Regular consultation with

telecom operators

Automation of ICT Indicators

Database

•On-line data reporting

•PTA’s in-house database

•Big data analytics

Annual

Symposium/Conference on

ICT Indicators

•Progress review

•New data requirements