Msc Presenters Copy

54

CHAPTER ONE: INTRODUCTION 1.1 Background Agriculture remains the backbone of the Kenyan economy. It is the single most important sect or in the economy, con tr ibut ing appr oximat ely 25 per cent of the GDP, and employing 75per cent of the national labour force (GOK, 2005). Over 80 per cent of the Keny an popu lat ion liv e in the rur al areas and derive their livel ihoods, dir ect ly or indirectly from agriculture or agriculture related activities. The national baseline survey of the MSE sector revealed that there were 1.3 million such enterprises employing 2.4 million Kenyans (GOK, 1999). Given its importance, the performance of the sector is the ref ore ref lected in the per formance of the whol e economy. The developme nt of agriculture is also important for poverty reduction since most of the vulnerable groups like pastoralists, the landless, and subsistence farmers, also depend on agriculture as their main source of livelihood. Growth in the sector is therefore expected to have a greater impact on a larger section of the population than any other sector. The development of the sector is therefore important for the development of the economy as a whole. The provision of agricultural finance has increasingly been regarded as an important tool for raising the incomes of rural populations, mainly by mobilizing resources to more productive uses. One question that arises is the extent to which credit can be offered to the rur al poor to fac il ita te the ir tak ing advant age of the deve loping ent repreneur ial activities. The generation of self-employment in non-farm activities requires investment in working capital. More than one third of the enterprises die young due to inadequate working capital (Head, 2003, Watson et al , 1996) However, at low levels of income, the accumulation of such capital may be difficult. The government has also identified lack of credit as the second severest problem faced by MSEs the most being lack of markets and competition (GOK, 2005). Formal financial institutions such as commercial banks fail to cater for the credit needs of smallholders, however, mainly due to their lending terms and conditions. (Ngobo, 1995)

Transcript of Msc Presenters Copy

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 1/54

CHAPTER ONE: INTRODUCTION

1.1 Background

Agriculture remains the backbone of the Kenyan economy. It is the single most important

sector in the economy, contributing approximately 25 per cent of the GDP, and

employing 75per cent of the national labour force (GOK, 2005). Over 80 per cent of the

Kenyan population live in the rural areas and derive their livelihoods, directly or

indirectly from agriculture or agriculture related activities. The national baseline survey

of the MSE sector revealed that there were 1.3 million such enterprises employing 2.4

million Kenyans (GOK, 1999). Given its importance, the performance of the sector is

therefore reflected in the performance of the whole economy. The development of

agriculture is also important for poverty reduction since most of the vulnerable groups

like pastoralists, the landless, and subsistence farmers, also depend on agriculture as their

main source of livelihood. Growth in the sector is therefore expected to have a greater

impact on a larger section of the population than any other sector. The development of

the sector is therefore important for the development of the economy as a whole.

The provision of agricultural finance has increasingly been regarded as an important tool

for raising the incomes of rural populations, mainly by mobilizing resources to more

productive uses. One question that arises is the extent to which credit can be offered to

the rural poor to facilitate their taking advantage of the developing entrepreneurial

activities. The generation of self-employment in non-farm activities requires investment

in working capital. More than one third of the enterprises die young due to inadequate

working capital (Head, 2003, Watson et al , 1996) However, at low levels of income, the

accumulation of such capital may be difficult. The government has also identified lack of

credit as the second severest problem faced by MSEs the most being lack of markets andcompetition (GOK, 2005).

Formal financial institutions such as commercial banks fail to cater for the credit needs of

smallholders, however, mainly due to their lending terms and conditions. (Ngobo, 1995)

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 2/54

indicates small enterprise owners cannot easily access finance to expand business and

they are usually faced with problems of collateral, application requirements and the

unexplained bank charges. The financial access survey by the central bank reveals that 38

per cent of the country’s bankable population is excluded from financial services and

related products (CBK, 2007). It is generally the rules and regulations of the formal

financial institutions that have created the myth that the poor are not bankable, and since

they can’t afford the required collateral, they are considered uncreditworthy (Alila, 1991).

1.2 Statement of the research problem

SMEs in Kenya form a very crucial sector in terms of employment generation, wealth

creation, welfare improvement and their immense contribution to the national GDP.

However, SMEs are generally undercapitalized due to operational difficulties in

accessing finance. Lack of working capital and low liquidity limit the entrepreneur’s

ability to purchase productivity enhancing inputs like seeds, fertilizers and pesticides and

more stock (Nyoro, 2002). The average production efficiency levels are higher among

producers who have access to finance in agricultural related enterprises in Kenya

(Kibaara, 2005).

The lack of finance is one of the most binding constraints in the growth of SMEs, as only

14 percent of SMEs might resort to borrowing, out of which two thirds was for capital

Investment. Many SMEs are not going to banks to meet financial needs due to various

reasons including lack of knowledge regarding bank products, low market penetration by

banks, lengthy and difficult loan procedures, lack of security, lengthy documentation, and

social as well as religious reasons.

Within the context of the agriculture industry, there is a great need for credit for in order

to accelerate the growth of MSEs. The demand for rural credit has outstripped the supply

over time. The current annual demand is estimated at Kenya shillings 75 billion while the

supply stands at 18–22 billion Kenya shillings (MoA, 1995; Kimuyu and Omiti, 2000).

The various intermediaries for finance and credit include commercial banks, non-bank

financial institutions, the Agricultural Finance Corporation, agricultural boards, non-

governmental organizations and rural-urban savings societies. The proportion of credit

2

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 3/54

for agriculture constitutes only 10–12 per cent of the total loan advances from these

institutions.

The majority of the world’s poor live in rural areas. Yet most lack access to the range of

financial services they need. Financial services available to them are relatively costly or rigid, whether from formal or informal financial providers or traders and agricultural

processors offering input credit. Financial institutions seeking to work in rural areas face

numerous constraints, such as poor infrastructure and high loan administration costs

Moreover, the main products of many microfinance institutions short-term working

capital loans with frequent expected repayments are not well-suited to seasonal or longer-

term agricultural activities.

Agricultural finance is notoriously risky. Many farmers need credit to purchase seeds and

other inputs, as well as to harvest, process, market and transport their crops. While

borrowing on the basis of anticipated crop production might seem logical where collateral

assets are few, such loans expose the lender to production and price risk. Natural

disasters, a decline in market prices, unexpectedly low yields, the lack of buyers of

agricultural produce, or loss due to poor storage conditions are only some of the factors

that can result in lower than-expected revenues. Such a fall in revenues can often lead to

high default rates on agricultural loans. The overwhelming failure of state development

banks that provided billions of dollars in subsidized agricultural finance to farmers in the

1970s and 1980s, combined with scant rural penetration by risk-averse commercial

financial institutions, has led to a widespread dearth of agricultural credit.(CGAP, 2005).

In order to realize economic growth and implement vision 2030 four critical economic

sectors have been identified i.e. wholesale and retail trade, agriculture, manufacturing and

financial services. The integrated household budget survey reveals that 45.6 per cent of

households get credit from neibhours or friends. Another 13 per cent obtain credit from

grocery or local merchants and 11.9 per cent from SACCOS. (GOK, 2007).

Agricultural productivity can be increased, farmers incomes raised, more people fed and

in deed, the general economic welfare enhanced In order to improve smallholder farm

3

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 4/54

productivity as well as increase incomes; smallholder farming must be changed from

producing for subsistence to commercial profitable businesses. It will then attract private

entrepreneurs willing to invest therein and employ modern farming techniques necessary

to achieve increased productivity. When agriculture is technology-led, not only is food

security achievable but also poverty alleviation is also possible. Inability to afford new

and readily available farming technology, however, is partly blamed on poor access to

financial resources, especially in a nation where the majority, and not only farmers, are

poor and the financial markets have not developed to support agricultural investment.

(Alila, 2006).

Improving the availability of finance to this sector is one of the incentives that have been

proposed for stimulating its growth and the realization of its potential contribution to the

economy (GOK, 1994). Despite this emphasis, the effects of existing institutional

problems, especially the lending terms and conditions on access to credit facilities, have

not been addressed. In addition, there is no empirical study indicating the potential role of

improved lending policies by both formal and informal credit institutions in alleviating

problems of access to credit. Knowledge in this area, especially a quantitative analysis of

the effects of lending policies on the choice of finance sources by entrepreneurs, is

lacking for the rural financial markets of Kenya (Kibaara, 2005).

Access to finance for SMEs is still a major problem, despite the fact that Kenya has a

relatively well-developed banking system. Risks associated with farming business,

coupled with complicated land laws and tenure systems that limit the use of land as

collateral, makes the financing of agriculture and the off farm enterprises by the formal

banking industry unattractive. In addition, corruption, political interference in the

operations particularly of state-owned banks and dysfunctional court system in the past,

gave rise to culture of default, thereby leading to high levels of non-performing loan

portfolio in the balance sheets of the banking institution affected. This development

forced many banks to change prohibitively high interest rates to their customers,

including farmers in order to remain afloat (Nyoro, 2002). This study therefore seeks to

4

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 5/54

examine the role of agricultural finance on the growth of MSEs in Kenya and the

constraints to provision of agricultural finance in Kenya.

1.3 Research objectives1.3.1 General Objective

The main objective of this study is to examine the role of agricultural finance in MSE

growth. The study seeks to find out whether agricultural finance has played any role or no

role in MSE growth.

1.3.2 Specific objectives of the study are:

a) Review the lending procedures of agricultural finance institutions.

b) Assess the effect of agricultural finance on MSE expansion and growth.

c) To analyze the major constraints hindering the availability of agricultural finance

to small and micro enterprises in the study area.

d) To evolve policy recommendations that will improve the administration of

agricultural finance to small-scale enterprises in Kenya.

1.4 Research questions

The study seeks to answer the following questions

a) Do lending procedures of AFC affect the availability of agricultural finance?

b) What is the effect of agricultural finance on SME expansion and growth?

c) What constraints hinder the availability of agricultural credit in the study area?

d) What policy suggestions should be recommended to ease administration of

agricultural finance to small scale enterprises in Kenya?

1.5 Importance and justification of the study

The study is important as a means of finding out ways of supporting the agricultural

SMES through the provision of agricultural finance. The study will provide additional

knowledge on agricultural finance and its role on MSE growth.

5

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 6/54

Policy makers

The findings of this research will enable policy makers in government formulate

constructive and effective policies. The SMES in the agricultural sector are critical to

economic growth and sound policies that facilitate provision of agricultural finance are

critical for economic growth.

Research institutions

The study will benefit scholars to further understand the linkage between agricultural

finance and economic growth and the use of agricultural finance to target the unbanked in

the society and the relationship to SME growth.

Community

Agricultural finance services allow the community to reallocate expenditure across time.

Entrepreneurs need finances for startup, growth and expansion of SMEs hence the

community can understand the role agricultural finance plays in the improvement of their

economic wellbeing.

Entrepreneurs

This study will benefit owners of small and micro enterprises to identify sources and the

cost of agricultural finance and look at factors that work to their advantage to maximize

profit and expand their businesses. It will also reduce the operational difficulties

encountered in accessing credit by the entrepreneurs.

Civil society organizations

The research will enhance civil society’s role of building farmers’ capacity to organize,

generate and utilize resources more effectively. Results will also assist the civil societies

carry out roles of advocacy which will ensure that barriers to credit access such as

ownership of collateral by women and children are addressed.

6

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 7/54

1.6 Scope of the study

The study population will be SMEs operating in Machakos district. The study will focus

on agro-based enterprises both farm and off-farm. The study will focus on SMEs

employing between 1 and 50 people and have been in operation for more than 18 months.

1.7 Limitations of the study

Since the cost of carrying out the study requires adequate finance, the financial

constraints of the researcher will not permit to facilitate more in-depth investigations of

the problem. Such facilitation could have been in form of a research assistants,

convenient transport and ample communication amenities. Apart from limited time

frame, the accessibility of some key respondents in the target population may not be easy

leading to a lot of time spent than will be necessary, due to such limitations, it is therefore

assumed that the results obtained from the branch will be used to generalize the broader

spectrum of the entire Agricultural Finance Corporation branch network.

1.8 Conceptual framework

In view of existing literature on agricultural finance three hypotheses will be tested.

Lending procedures have no effect on availability of agricultural finance to SMEs, lack of

finance does not hinder growth of SMEs and government policies have no influence on

growth performance of SMEs (Namusonge, 1999).

Two main theoretical paradigms have been advanced to explain the existence of this

fragmentation: the policy-based explanation and the structural-institutional explanations

(Aryeetey et al., 1997). According to the policy-based explanation, fragmented credit

markets (in which favoured borrowers obtain funds at subsidized interest rates, while

others seek funds from expensive informal markets) develop due to repressive policies

that raise the demand for funds. Unsatisfied demand for investible funds forces credit

rationing using non interest rate criteria, while an informal market develops at

uncontrolled interest rates.

According to the structural-institutional explanations, imperfect information on

creditworthiness, as well as cost of screening, monitoring and contract enforcement

7

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 8/54

among lenders, results in market failure due to adverse selection and moral hazard, which

undermines the operation of financial markets. As a result, lenders may resort to credit

rationing in the face of excess demand, thus establishing equilibrium even in the absence

of interest rate ceilings and direct allocations. Market segmentation then results. Market

segments that are avoided by the formal institutions due to institutional and structural

factors are served by informal agents who use personal relationships, social sanctions and

collateral substitutes to ensure repayment. An extended view of this explanation is that

structural barriers result in monopoly power, which perpetuates segmentation.

Independent variables Dependent Variable

INSTITUTIONAL

LENDING PROCEDURES

TYPE AND SOURCE OF SME GROWTH

AGRICULTURAL FINANCE

GOVERNMENT LENDING

POLICIES

Figure 1: Conceptual framework

The following variables have influence on MSE growth.

(a)Institutional lending procedures

Institutional lending procedures determine ease of access of finance. Where the

procedures are cumbersome borrowers are not able to meet the requirements of the

institution and shy away from the institution. The procedures also may determine the time

from application to disbursement and since most of the activities have a time frame.

Clients want to deal with institutions that disburse funds in the shortest time possible.

Funds are also required for purchase of new equipment, hiring of extra labour and

8

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 9/54

purchase of extra stock .All these requires to be done quickly hence simplicity in terms of

institutional lending procedures is critical.

(b) Type and source of agricultural finance

This determines the rate of SME growth in that some agricultural finance service

providers provide both cash credit and credit in form of stocks and inputs. This has an

effect in that the client has no control on the cost of inputs this affects the profitability of

the enterprise. Credit source is also important in that government organizations may offer

cheaper credit as well as NGOs depending on the cost of the finances. Empirical evidence

however indicates that a commercial, market-based approach is most likely to reach large

numbers of clients on a sustained basis (Kibaara, 2005).

(c)Government lending policies

Agricultural financial services are part of an interactive system of financial institutions,

financial infrastructure, legal and regulatory frameworks, and social and cultural norms.

Government has a role to play in establishing a favourable or “enabling” policy

environment, infrastructure and information systems, and supervisory structures to

facilitate markets, but it should play a more limited role in direct interactions. Lending

policies therefore determine the growth rate of SMEs as this determines the cost of doing

business.

1.9 Summary

The chapter provides the background and statement of the problem. The research

problem being investigated is the effect of agricultural finance on small and medium

enterprises and the factors that affect the availability of agricultural finance. Research

questions are generated from the problem and the study seeks to answer these questions.

The study is of significance to policy makers, donor agencies, civil society organizations,

financial institutions, development agencies, entrepreneurs and other stakeholders.

9

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 10/54

CHAPTER TWO: LITERATURE REVIEW

2.1 Introduction

This chapter reviews both empirical and theoretical literature concerning agricultural

finance with specific in-depth focus on its role in SME growth. The role of agriculture in

economic growth is analyzed, the entrepreneurial finance needs at various stages of

business growth and constraints facing the agriculture sector in Kenya. We also examine

the typology of financial institutions offering agricultural finance in Kenya and in Africa.

The chapter also looks at the constraints facing agricultural finance institutions as a

source of entrepreneurial finance.

2.2 Role of agriculture in national development

Kenya’s economy is heavily dependent on agriculture. The agricultural sector directly

contributes 25 per cent of the gross domestic product (GDP) and indirectly an additional

27 per cent through linkages with manufacturing, distribution and the service sector.

(GOK, 2007) Evidence shows that there is a direct and positive relationship between

growth of the agricultural sector and the entire economy. Wherever the agricultural sector

has performed well, the economy has invariably performed well. This could be due to

several factors, including the relatively large share of the sector in the gross domestic

product. A large proportion of the population is thus trapped in a vicious circle of low

income and low assets. This persists from generation to generation, rendering a low GDP

per capita inevitable. The situation is exacerbated by a physical infrastructure that

impedes the effective distribution and marketing of agricultural goods, by degraded soil

fertility, by uncertain land tenure, by lack of access to credit, and by limited irrigation

possibilities, worsened still further by growing competition for scarce water and the

threat of climate change. These are compounded by the disastrous effect of HIV/AIDS on

the adult community in rural populations (McDonald and Roberts, 2006; Corrigan et al .,

2005; Misselhorn, 2005).

Agricultural investment provides the catalyst for the development of essential

infrastructure, including transport, communication, education and health services

(Turnock, 2001). Agriculture and food production is a high-volume, low-cost enterprise

10

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 11/54

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 12/54

2.3 Constraints to agriculture sector growth in Kenya

Several constraints have been identified as hindering growth of SMEs in the agricultural

sector. The main constraints identified include:

2.3.1 Unfavorable macro-economic environment

Stable macro-economic environment is vital for sustained growth and investment.

Although in the recent past the government has made considerable progress in stabilizing

the macro-economic environment, persistent large public sector borrowing requirements,

high lending interest rates, and overvalued and volatile shilling exchange rates has

discouraged investment in the agricultural sector. Many farmers have been impoverished

by the high debt service and non-performing loans. This has made agricultural finance

unavailable to institutions such as the AFC and other farmer organizations .The lack of finance hampers growth of the agri-based SMEs (GOK, 2004)

2.3.2 Unfavourable external environment. Deterioration in terms of trade due to a

decline in the world commodity prices has particularly impacted negatively on the

incomes from coffee, tea, sisal and pyrethrum farming. Tariffs and non-tariffs barriers

imposed by developed countries have made it difficult for developing countries to access

their markets. SMEs that rely on these commodities are not able to expand due to limited

markets and lack of finances for value addition and supporting entrepreneurs.

2.3.3 Inappropriate legal and regulatory framework .

This is seen in outdated legal and regulatory framework that has served only to constrain

agricultural development, trade and effective competition. Outdated business laws inhibit

growth of entrepreneurs.

2.3.4 Lack of capital and access to affordable credit.

The main factor which farmers, particularly small farmers, points out as causing low

productivity in agriculture is inadequate credit to finance inputs and capital investment in

the past, the government through the AFC, the cooperative bank of Kenya and the

cooperative movement, provided affordable credit to farmers. Due to mismanagement

12

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 13/54

and political patronage and interference, most of these institutions have collapsed or

failed to provide the services, thus leaving farmers without source of affordable credit. A

number of micro-finance institutions are however operating in some areas, but they reach

only a small proportion of smallholder farmers, provide very short-term credit and their

effective lending rates are very high. The formal banking system is yet to develop credit

facilities that particularly suit small scale farming business.

2.3.4 Frequent droughts and floods.

Most crop and livestock farming in Kenya is rain-fed, and therefore, is susceptible to

weather fluctuations. Over the last three decades the frequency of droughts and floods has

increased, resulting in crop failures and loss of livestock. Furthermore, with increasing

land degradation, land resilience has been reduced and the effects of drought and floods

exacerbated.

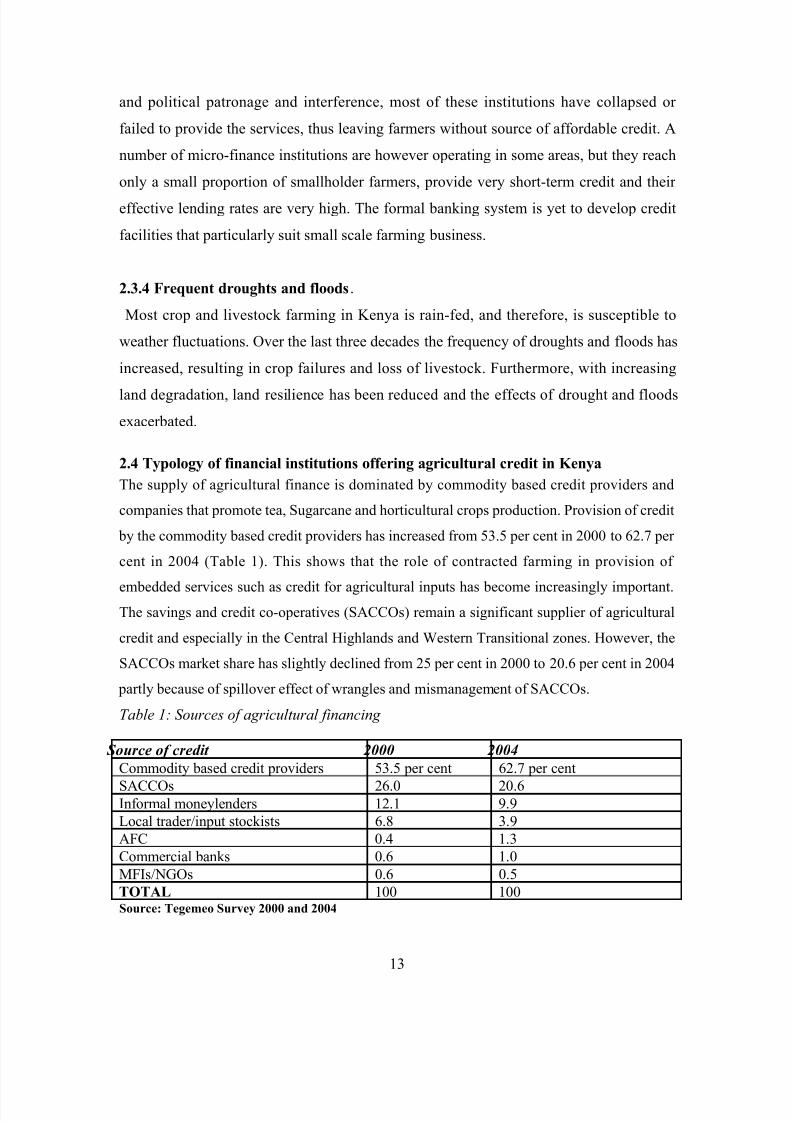

2.4 Typology of financial institutions offering agricultural credit in Kenya

The supply of agricultural finance is dominated by commodity based credit providers and

companies that promote tea, Sugarcane and horticultural crops production. Provision of credit

by the commodity based credit providers has increased from 53.5 per cent in 2000 to 62.7 per

cent in 2004 (Table 1). This shows that the role of contracted farming in provision of

embedded services such as credit for agricultural inputs has become increasingly important.

The savings and credit co-operatives (SACCOs) remain a significant supplier of agricultural

credit and especially in the Central Highlands and Western Transitional zones. However, the

SACCOs market share has slightly declined from 25 per cent in 2000 to 20.6 per cent in 2004

partly because of spillover effect of wrangles and mismanagement of SACCOs.

Table 1: Sources of agricultural financing

Source of credit 2000 2004

Commodity based credit providers 53.5 per cent 62.7 per cent

SACCOs 26.0 20.6Informal moneylenders 12.1 9.9

Local trader/input stockists 6.8 3.9

AFC 0.4 1.3

Commercial banks 0.6 1.0

MFIs/NGOs 0.6 0.5

TOTAL 100 100Source: Tegemeo Survey 2000 and 2004

13

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 14/54

Jointly, the informal money lenders and local traders/input stockists are more important

than the formal commercial banking institutions, providing 20 per cent of the agricultural

credit to the rural households in Kenya. The government owned Agricultural Finance

Corporation has increased its agricultural credit provision from 0.4 per cent in 2000 to 1.3

per cent in 2004. This gain is partly attributed to financial revamp by the government and

the current restructuring of the institution. (AFC, 2007)

Provision of agricultural credit through the mainstream commercial banks has increased

slightly as a result of recent innovative products associated with retail banking such as

loans to tea and dairy farmers. In addition, there is reduced bureaucracy, excess liquidity

as investment opportunities are thinned following the reduction of government/treasury

bills which was estimated to contribute 50 per cent of the bank’s income. However, the

commercial bank’s contribution to agricultural credit is insignificant. The Micro Finance

Institutions (MFIs) provide agricultural credit to a mere 0.6 per cent of the rural

households. MFIs have been in existence for the last 20 years, focusing on the

economically active but poor entrepreneurs and have played a pivotal role in helping the

low-income earners access non-agricultural loans. (Kibaara, 2005)

2.5 The Equity Bank model

Equity Bank Limited provides retail Banking and microfinance services in various parts

of the country. The bank has a total branch network of 50 branches and 200 ATMs.The

bank has been instrumental in the provision of agricultural finance products .The bank

offers credit to entrepreneurs engaged in agricultural activities such as milk production

maize, coffee, tea, horticulture, and SMEs engaged in trade and service activities. In

order to increase outreach the bank provides mobile banking services with 44 village

mobile banks. The bank as has flexible security requirements and loan appraisals are

based on the ability to pay vis-à-vis collateral based. The bank has also ensured quick disbursement of loan with crop advance loans taking less than a day to disburse (Equity,

2006).

Due to the above innovative products including catering for the financial needs of women

the bank in partnership with UNDP recently launched the women enterprise fund that

14

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 15/54

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 16/54

through their lending policies. This is displayed in the form of prescribed minimum loan

amounts, complicated application procedures and restrictions on credit for specific

purposes (Schmidt and Kropp, 2003). For small-scale enterprises, reliable access to short-

term and small amounts of credit is more valuable, and emphasizing it may be more

appropriate in credit programmes aimed at such enterprises.

Schmidt and Kropp, (2003) further argue that the type of financial institution and its

policy will often determine the access problem. Where credit duration, terms of payment,

required security and the provision of supplementary services do not fit the needs of the

target group, potential borrowers will not apply for credit even where it exists and when

they do, they will be denied access.

The Grameen Bank experience shows that most of the conditions imposed by formal

credit institutions like collateral requirements should not actually stand in the way of

smallholders and the poor in obtaining credit. The poor can use the loans and repay if

effective procedures for disbursement, supervision and repayment have been established.

Notable disadvantages of the formal financial institutions are their restriction of finance

to specific activities, making it difficult to compensate for losses through other forms of

enterprises, and their use of traditional collateral like land. There is need for a broad

concept of rural finance to encompass the financial decisions and options of rural

economic units, to consider the kind of financial services needed by households, and

which institutions are best suited to provide them.

2.8 Characteristics of financial markets in Africa

Credit markets in Africa have mainly been characterized by the inability to satisfy the

existing demand for credit in rural areas. However, whereas for the informal sector the

main reason for this inability is the small size of the resources it controls, for the formal

sector it is not an inadequate lending base that is the reason (Aryeetey, 1996).Rather, the

reasons are difficulties in loan administration like screening and monitoring, high

transaction costs, and the risk of default. Credit markets are characterized by information

16

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 17/54

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 18/54

Commercial banks

Commercial Banks are the very heart of the financial market, providing the greatest

number and variety of loans To SMEs. Banks tend to be conservative in their lending

practices and prefer to make to established small businesses than to high risk startups.

They have stringent application procedures, high interest rates and elitist lending target

portfolio. The major banks include Kenya Commercial Bank, Barclays Bank, Standard

Chartered Bank, and Equity Bank which has experienced phenomenal growth and is

currently controlling more than a third of all bank accounts in Kenya with 1,347,578

active bank accounts (CBK, 2007)

Savings and credit cooperative societies (SACCOS):

The SACCOS rely on members’ savings to provide loans and other services. Members

are provided with loans based on share contribution as well as guarantors’ shares.

Members can borrow up to specific number of times of the value of share contribution

with a repayment period of up to 36 months. Loan repayment and interest are deducted

from the salary or from the marketed produce. SACCOs are an important source of

agricultural finance where there are guaranteed markets for farm produce.

Development Finance Institutions (DFIs)

Other than commercial banks another set of financial institutions that have historically

been the most active in financing SMEs in Kenya, are DFIs. By 1995, the total number of

DFIs in the country was nine, all operating in the industrial and commercial sector. The

GOK started DFIs to promote industrial development. Some key DFIs include the

Industrial and Commercial Development Corporation (ICDC), the Development

Financial Corporation of Kenya (DFCK), the Kenya Industrial Estates (KIE) and

Industrial Development Bank (IDB). DFIs provide long-term finance of up to 10 years

with grace period of up to two years. Unlike commercial banks and NBFIs that insist on

100per cent security, DFIs lending is based on the viability of projects being funded and

security is based on the fixed asset being financed. They also provide non-financial

18

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 19/54

services, such as appraisal, implementation, monitoring of projects and training of

entrepreneurs. (Namusonge, 2004)

Micro finance institutions (MFIs)

Micro finance institutions use the group pressure model where members interested in

financing arrangements form solidarity groups that serve as security for the money

borrowed. Group pressure is critical in ensuring loan repayments through imposition of

sanctions. The MFIs are an important source of entrepreneurial finance and funding new

ventures. Examples include Kenya Women Finance Trust., K-REP BIMAS, Sunlink and

FAULU KENYA

2.9 The role of AFC in the provision of entrepreneurial finance

The Agricultural Finance Corporation (AFC) is a wholly owned state corporation

established through an act of parliament (Cap 323 of the Laws of Kenya).Its mandate is

to support the development of agriculture and agricultural industries by making loans to

farmers, co-operative societies, incorporated group representatives, private companies,

public bodies, local authorities and any other persons engaging in agriculture or

agricultural industries.

The Agricultural Finance Corporation (AFC) has traditionally been the single largest

agricultural credit institution in the country and has been instrumental in the development

of agriculture by providing an average of the total credit to the sector sine independence.

The organization has developed a strong physical presence countrywide with a branch

network of 31 branches country wide. The corporation has been instrumental in the

implementing many government and donor supported programs such as mechanization of

the agricultural sector, livestock development programs, the Guarantee Minimum Return,

the Seasonal Crop Credit and the Emergency Livestock Off-take Program. Since early

1990’s, the corporation started experiencing operational difficulties due to poor governance, political interference and effects of economic liberalization that led to

subsequent collapse of some agricultural marketing bodies. By 1992, the non-performing

loan portfolio reached 89 per cent (AFC, 2005). The government and other donors

stopped funding AFC and the recovered money was used for recurrent expenditure. AFC

officially stopped lending from 1997 to 2001(AFC, 2007)

19

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 20/54

The National Rainbow Coalition (NARC) government pledged to improve access to rural

credit and financial services from 2003. Since then, the government has implemented

some of its pledges as stated in the Strategy for Revitalizing Agriculture (SRA). The

government has restructured AFC by writing off bad debts and refinancing. The

corporation has resumed lending for seasonal crop credit and value addition loans at

10per cent and 15per cent respectively. As at 2004/2005, the corporation had advanced a

total of one billion Kenya shillings to 5253 farmers. Seasonal loans account for 52per

cent of the total loans, while development accounts for 48 per cent (AFC, 2007)

Kenya has however not developed a comprehensive rural financial services strategy. The

rural financial sector is governed by the Banking Act, Building Society Act and the Post

Bank Act. The proposed SACCO Societies Regulatory Bill 2004 is still to be debated in

parliament. Through the Economic Recovery Strategy for Wealth and Employment

Creation (ERSWC) the government has identified poor access to farm credit and financial

services as a contributing factor to the decline in agricultural productivity. The Strategy

for Revitalizing Agriculture (SRA) proposes to encourage an orderly development of

micro-finance institutions through the enactment of facilitative legislation, encourage

commercial banks to set up operations in the rural areas by providing appropriate

incentives, encourage banks to lend to agriculture by reviewing and repealing legal

provisions that have undermined lending to the sector, recapitalize and streamline the

management of Agricultural Finance Corporation so that it can perform its function of

providing affordable credit to farmers ( GOK, 2004). As a follow up on SRA, the

Agricultural Sector Co-ordination Unit (ASCU) has fast-tracked the rural financial

services by establishing a thematic group on inputs and rural financial services with an

overall objective of developing an Integrated Farm Input Strategy.

3.0 Constraints of agricultural finance institutions

Commercial banks and other formal institutions fail to cater for the credit needs of

smallholders, due to their lending terms and conditions. It is generally the rules and

regulations of the formal financial institutions that have created the myth that the poor are

20

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 21/54

not bankable, and since they can’t afford the required collateral, they are considered

uncreditworthy (Adera, 1995).

In the recent past, there has been an increased tendency to fund credit programmes in the

developing countries aimed at small-scale enterprises. In Kenya, despite emphasis on

increasing the availability of credit to small and micro enterprises (SMEs), access to

credit by such enterprises remains one of the major constraints they face. A 1995 survey

of small and micro enterprises found that up to 32.7per cent of the entrepreneurs

surveyed mentioned lack of capital as their principal problem, while only about 10per

cent had ever received credit (Daniels et al ., 1995). Although causality cannot be inferred

a priori from the relationship between credit and enterprise growth, it is an indicator of

the importance of credit in enterprise development. The failure of specialized financial

institutions to meet the credit needs of such enterprises has underlined the importance of

a needs oriented financial system for rural development.

Experience from informal finance shows that the rural poor, especially women, often

have greater access to informal credit facilities than from formal sources (Schrieder and

Cuevas, 1992; Adams, 1992). The same case has also been reported by surveys of credit

markets in Kenya (Raikes, 1989; Alila, 1991; Daniels et al ., 1995). A relevant question

then becomes: Why do informal financial institutions often succeed even where formal

institutions have failed? Lack of an empirical analysis of the relationship between lending

policies and the problem of access makes it difficult to answer such a question. This

study is aimed at empirically analyzing the credit policies in the agricultural finance

sector with the view of establishing their role in determining the access of small-scale

enterprises to financial services with the role of AFC coming under sharp focus given its

mandated role in funding the thriving agriculture sector.

The lending policies used by the main credit institutions in Kenya do not ensure efficient

and profitable use of credit funds, especially by farmers, and also result in a disparity

between credit demand and supply (Atieno, 1994). This view is further supported by a

1995 KREP survey showing that whereas credit is an important factor in enterprise

21

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 22/54

expansion, it will most likely lead to enterprise contraction when not given in adequate

amounts (Daniels et al ., 1995). Hence, despite the existence of a sophisticated financial

system, it has not guaranteed the access to credit by small-scale enterprises.

Although not much is known about the informal financial sector in the country, there is a

consensus that it is an important source of finance to the small-scale entrepreneurs in the

country (Aleke Dondo, 1994). (Ouma, 1991) found that 72 per cent of the sample

surveyed saved with and borrowed from informal sources. Whereas in the formal credit

market only a selected few qualify for the predetermined loan portfolios, in the informal

market the diversified credit needs of borrowers are better satisfied. The problems of

formal financial institutions, especially security, loan processing, inadequate loans given,

unclear procedures in loan disbursement and high interest rates, all underscore the

importance of informal credit and the need to investigate the dynamics of its operations,

especially with respect to how these factors determine the access to and the use of credit

facilities. Informal credit sources in Kenya comprise traders, relatives and friends,

ROSCAs, welfare associations, and moneylenders.

3.11 Supply and demand of entrepreneurial finance

The 1993 baseline survey indicated that only 9per cent of the MSME had accessed

microfinance and only 4per cent of this finance was obtained from formalized financial

channels. The survey noted that the bulk of the SME credit(69.1per cent) come from the

informal credit and savings associations, mainly rotating savings and credit

associations(ROSCAS), friends and relatives. These findings compare favourably with

the 1995 baseline survey which showed that 10.8 of the SMEs had accessed microfinance

and that only 3.4 per cent of those received credit from formal financial sources

(Namusonge 2006).Thus the supply of entrepreneurial finance which includes

agricultural finance is very low compared to the aggregate demand.

3.12 Impact of entrepreneurial finance

Entrepreneurial finance is critical in creating a source of business capital for persons

excluded from the formal banking sector and this fosters their self determination and

economic self-reliance. Support for capital formation through savings schemes managed

22

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 23/54

by people themselves enables the beneficiaries to raise capital for growth of businesses.

This leads to growth and expansion of the enterprises and hence overall economic

growth.

3.13 SummaryThis literature review has attempted to analyze the role of agricultural credit and its effect

on SME growth. The role of agriculture is critically examined as well as constraints

facing the agricultural sector. The review also analyses the typology of financial

institutions and the issue of access to finance. It also critically examines the role of AFC

in the provision of agricultural finance. An understanding of the role of finance in growth

of SMEs is critical to development to small-scale enterprises.

23

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 24/54

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction

This section highlights the research design, target population and sample size, methods of

data collection, and data analysis.

3.2 Research design

The research design used in the study would be exploratory-descriptive research design.

It is exploratory in that the major emphasis would be on the discovery ad trying to get

more insight on the effect of agricultural finance on SME growth. The design would also

be descriptive as the effect of the finance on the growth of SMEs would be explained.

3.3Target population

The study targeted entrepreneurs engaged in farming, wholesale and retail trade, and

primary processing of agricultural products. The sample size was 120 respondents drawn

from six administrative divisions of Machakos district.

3.4 Geographical scope

The study was carried out in March 2008 in six divisions of Machakos district where the

clients are located. Machakos district has 9840 registered businesses (GOK, 2007). The

A.F.C. branch here is one of the oldest branches offering agricultural finance and the

impact of the organization is also focus of the study.

3.4 Sampling and sample size

This includes both credit and noncredit users. The researcher selected 120 small-scale.

The entrepreneurs identified the available formal and informal sources of credit from

which they had benefited. There are six administrative divisions in Machakos district

.Each administrative division was allocated 20 respondents giving a total number as 120.

Purposive sampling was then applied in the selection of respondents who were willing

and satisfied the set criteria of being in business for more than 18 months with 1-50

employees. The required sample size was selected using the proportionate stratified

sampling and judgmental sampling respectively.

3. 5 Data collection methods

Data collection methods include the use of questionnaires, observation and discussions.

24

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 25/54

3.5.1 Primary Data collection

The main data collection instrument used in the study was a questionnaire. Respondents

who are literate were asked to fill tone or the same was used as an interview

schedule for illiterate respondents. This was administered in Kiswahili for ease of

understanding.

Pre-testing the questionnaire was done to five respondents to remove ambiguous and

confusing questions and make the necessary amendments. Data was then collected by the

researcher assisted by six research assistants over a period of four days.

The researcher also used observation method to complement data generated from thequestionnaire. This data from the observation was used for correlation purposes to

enhance data reliability.

3.5.2 Secondary data collection

This was mainly done using data from the Central bureau of statistics and ministry of

trade and industry data on registered businesses in Machakos district.

3.6 Data analysis

Data was analyzed using both qualitative and quantitative methods. Data was first codedand organized into concepts from which generalizations were made fro the entire

population. Data was then tabulated and frequencies calculated on each variable under

study and interpretations made from the collected finding in the field. Measures of central

tendency such as mean, mode and median and measures of dispersion like standard

deviation and percentages were calculated and interpretations made. Data is then

presented in form of tables and pie-charts and graphs.

The analyzed data was then converted into descriptive statements and/inferences about

relationships.

25

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 26/54

CHAPTER FOUR: RESEARCH FINDINGS

4.1 Introduction

The data for this research was collected in Machakos district in March 2008.the

respondents were reached through a sample frame provided by the ministry of industry

which has a database of registered businesses in the district. The researchers took four

days to collect data in the six (6) divisions and two days to analyze the data and one week

to write the report. Data was collected on background of the entrepreneurs, business

profile of the enterprises information on agricultural finance and the role of A.F.C. on the

provision of agricultural credit. Suggestions on the role of the government in the

provision of agricultural finance was provided .The research targeted business that had

been in operation for more than 18 months and in rural areas.

4.2 Demographic characteristics of the respondents

This section deals with the demographic and educational factors that may determine the

entrepreneurs’ choice of agricultural finance. The factors are gender, age, educational

background and level of training and experience in business.

4.1.1 Distribution by gender

Respondents were asked to indicate their gender. Out of the 120 respondents interviewed

78 respondents (representing 65per cent) were male and 42 respondents (representing

35per cent were female. This indicates a generally higher frequency of male

entrepreneurs in the study. This can be attributed to the fact that females face more

hurdles in starting the businesses and are not able to access seed capital. Further, women

tend to concentrate on maternal responsibilities and business concerns come second.

These cultural beliefs which have been internalized by women have made them poor

competitors against stronger (men) forces in the society.

26

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 27/54

Distribution of respondents by

gender

65%

35%

male

female

Fig 2 Distribution of respondents by gender

4.1.2 Distribution by age

Respondents were asked to indicate their age. The highest frequency of the respondents is

in the age brackets of over 44 years with a mean age of 39 years. This is an indicator that

entrepreneurs engaging in agro-based SMEs have pursued other interests before engaging

in the present activity such as formal employment. Further for entrepreneurs engaging in

commercial production ownership of productive land is essential and this age bracket has

inherited the land from the parents or mobilized resources for purchase of land.

Age is critical in business performance in that it takes time to acquire the necessary skills

and startup capital for the business. Further, where self-employment is not taken as a first

option many of the respondents had either been previously employed.

27

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 28/54

The distribution of respondents by age is analyzed in the table 2.

Distribution by age

Age in years Frequency per cent

16-19 1 120-25 10 8

26-30 15 13

31-35 18 1536-40 14 12

41-44 26 22

Over 44 36 30

TOTAL 120 100

Table 2: Distribution by age

4.1.3 Distribution of responses by educational level

The level of education is important as it determines the channels of communication used

by the respondent, degree of confidence and the ease of acquisition of new managerial

skills. The education level also determines the level of confidence in approaching

financial institutions. In order to determine the education levels respondents were asked

to indicate their education levels and the results are tabulated in table 3

Distribution of respondents by educational level

Level of education Frequency per cent No formal Education 3 3

Primary level 26 22Secondary level 64 53

Polytechnic level 20 17

College/university 7 6

TOTAL 120 100

Table 3: Distribution of respondents by level of education

The higher education levels are critical in the entrepreneurs’ understanding of the effect

of agricultural finance on the growth of their individual enterprises hence better

opportunities for business growth. The frequencies indicate that over 76 per cent of the

respondents have received education beyond secondary school level. This shows that

entrepreneurship is increasingly becoming a choice of many Kenyans in the absence of

formal employment.

28

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 29/54

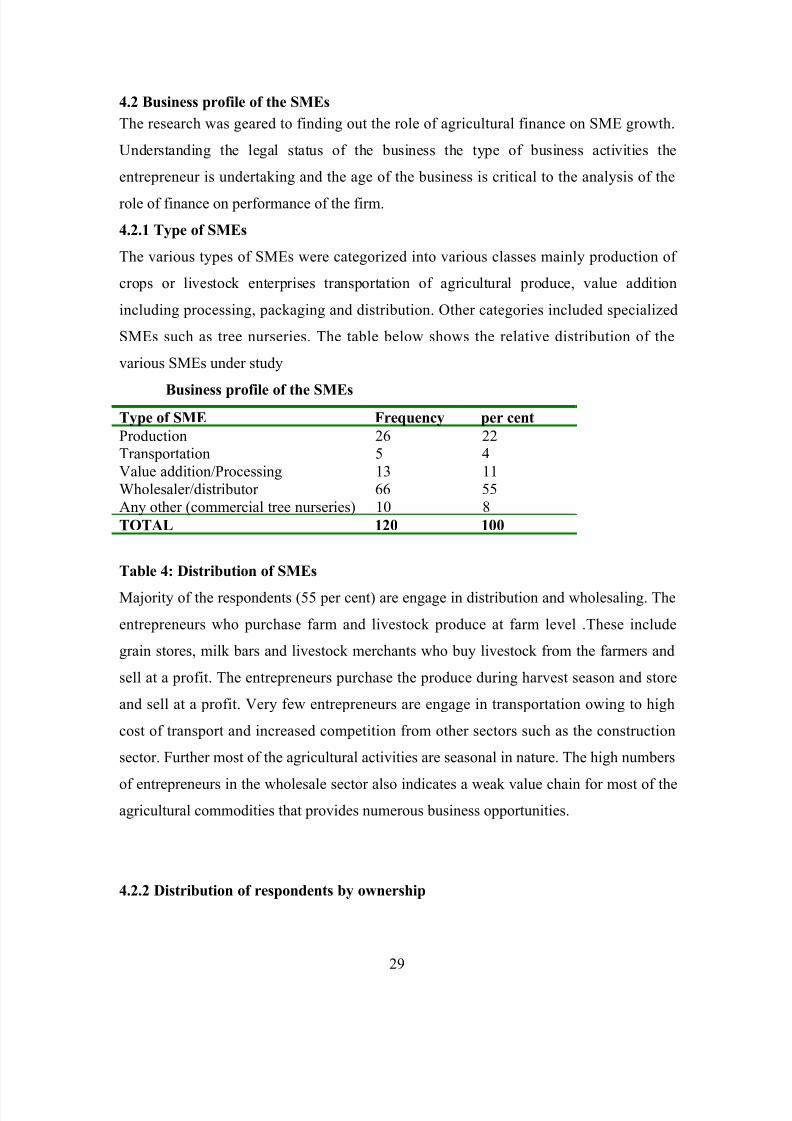

4.2 Business profile of the SMEs

The research was geared to finding out the role of agricultural finance on SME growth.

Understanding the legal status of the business the type of business activities the

entrepreneur is undertaking and the age of the business is critical to the analysis of the

role of finance on performance of the firm.

4.2.1 Type of SMEs

The various types of SMEs were categorized into various classes mainly production of

crops or livestock enterprises transportation of agricultural produce, value addition

including processing, packaging and distribution. Other categories included specialized

SMEs such as tree nurseries. The table below shows the relative distribution of the

various SMEs under study

Business profile of the SMEs

Type of SME Frequency per cent

Production 26 22Transportation 5 4

Value addition/Processing 13 11

Wholesaler/distributor 66 55

Any other (commercial tree nurseries) 10 8

TOTAL 120 100

Table 4: Distribution of SMEs

Majority of the respondents (55 per cent) are engage in distribution and wholesaling. The

entrepreneurs who purchase farm and livestock produce at farm level .These include

grain stores, milk bars and livestock merchants who buy livestock from the farmers and

sell at a profit. The entrepreneurs purchase the produce during harvest season and store

and sell at a profit. Very few entrepreneurs are engage in transportation owing to high

cost of transport and increased competition from other sectors such as the construction

sector. Further most of the agricultural activities are seasonal in nature. The high numbers

of entrepreneurs in the wholesale sector also indicates a weak value chain for most of the

agricultural commodities that provides numerous business opportunities.

4.2.2 Distribution of respondents by ownership

29

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 30/54

Entrepreneurs found at the business were asked to indicate the nature of the ownership of

the business. This was defined as sole proprietorship, partnership, limited company and

any other form of ownership. No responses were received from any other form of

ownership. Overwhelmingly most of the businesses are sole proprietorship. The

frequency is indicated in the chart below.

Business ownership

0 10 20 30 40 50 60 70

Sole propreitership

Limited company

Partnership

o w

n e r s h i p f o r m

percentage

Fig 3: Business ownership

Majority of the businesses (63 per cent) are sole proprietorship while the 33 per cent of

the other business are partnership between family members or relatives. Many of the

business are capital intensive and entrepreneurs obtain seed capital from personal savings

accumulated over time. The entrepreneurs found other forms of businesses ownership

cumbersome and expensive or were unaware of their existence.

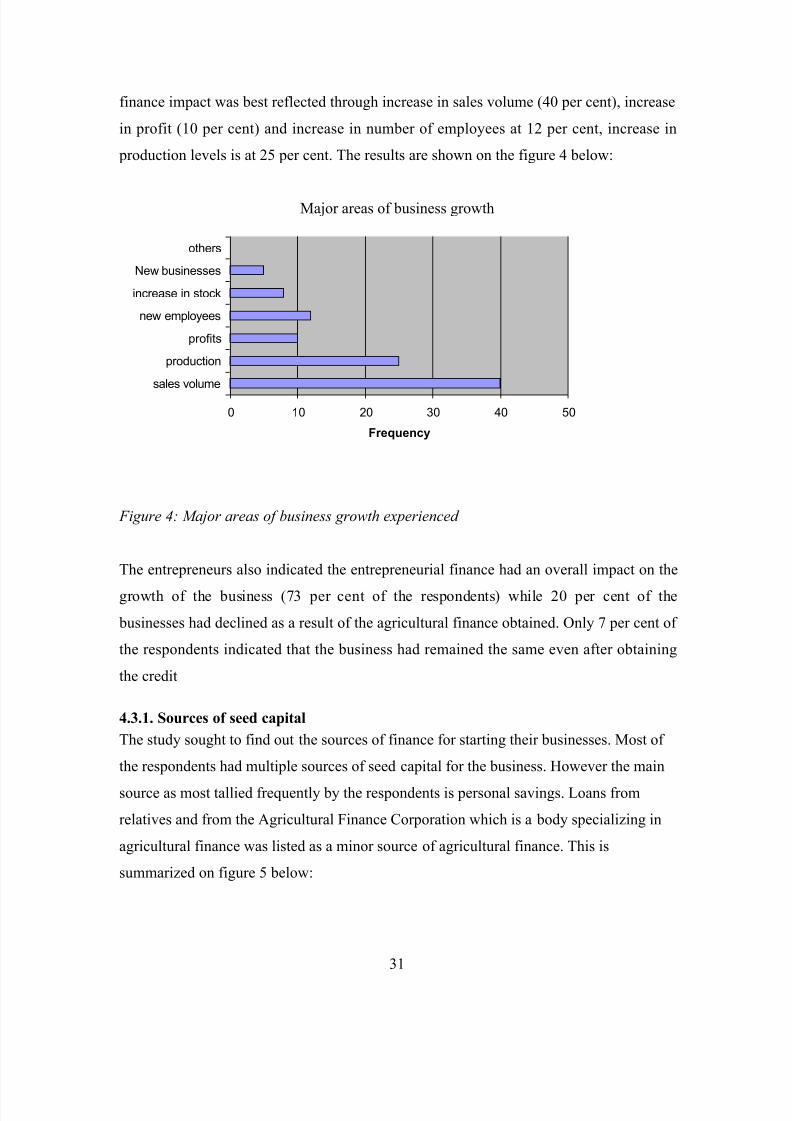

4.3 Effect of agricultural finance on SMEs growth

Agricultural finance is critical for SME growth. Finance is required for purchase of

additional stock, acquisition of new production facilities and tools, purchase of raw

materials and hiring of more employees. In an effort to establish the availability of other

sources of agricultural finance that businesses may use for growth and expansion the

researcher sought to know whether the business had experienced any growth and the

effect of any agricultural finance on business growth and performance. Agricultural

30

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 31/54

finance impact was best reflected through increase in sales volume (40 per cent), increase

in profit (10 per cent) and increase in number of employees at 12 per cent, increase in

production levels is at 25 per cent. The results are shown on the figure 4 below:

Major areas of business growth

0 10 20 30 40 50

sales volume

production

profits

new employees

increase in stock

New businesses

others

Frequency

Figure 4: Major areas of business growth experienced

The entrepreneurs also indicated the entrepreneurial finance had an overall impact on the

growth of the business (73 per cent of the respondents) while 20 per cent of the

businesses had declined as a result of the agricultural finance obtained. Only 7 per cent of

the respondents indicated that the business had remained the same even after obtaining

the credit

4.3.1. Sources of seed capital

The study sought to find out the sources of finance for starting their businesses. Most of

the respondents had multiple sources of seed capital for the business. However the main

source as most tallied frequently by the respondents is personal savings. Loans from

relatives and from the Agricultural Finance Corporation which is a body specializing in

agricultural finance was listed as a minor source of agricultural finance. This is

summarized on figure 5 below:

31

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 32/54

Sources of starting capit

0 10 20 30 40 50 60 70

Personal savings

Loans from relatives

Commercial Bank

A.F.C.

Sale of personal assets

Others

S o u r c e

Frequency

Figure 5: Sources of starting capital

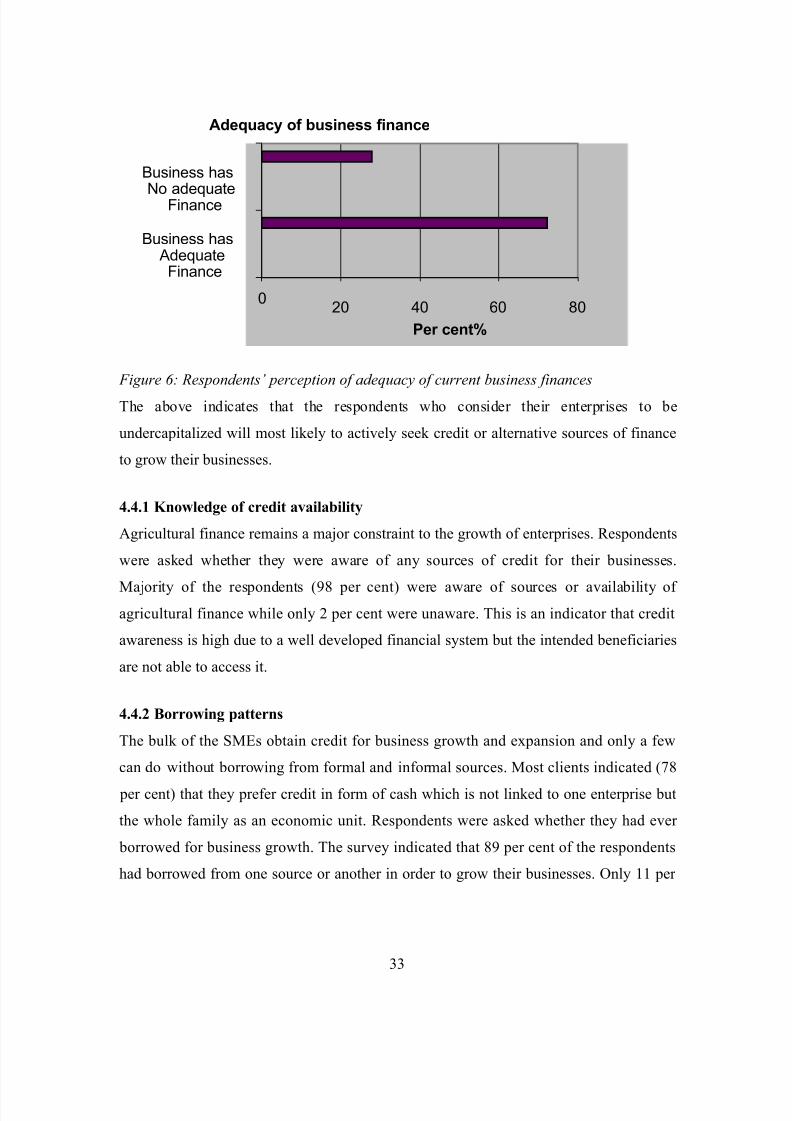

4.4 Perception of adequacy of business financing

Adequate finances are critical for growth of enterprises. Finances are required for

expansion of the businesses, purchase of new stock, hiring of new employees, and for

graduation into bigger enterprises. Respondents were asked to indicate whether they had

adequate agricultural finance for their business operations and whether the capital

resources they had were adequate for their needs.87 respondents representing 72 per cent

of the total considered their capital resources inadequate while 23 respondents

representing 28 per cent of the total considered their resources adequate.

The frequency of these responses is illustrated in figure 6.

32

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 33/54

Figure 6: Respondents’ perception of adequacy of current business finances

The above indicates that the respondents who consider their enterprises to be

undercapitalized will most likely to actively seek credit or alternative sources of finance

to grow their businesses.

4.4.1 Knowledge of credit availability

Agricultural finance remains a major constraint to the growth of enterprises. Respondents

were asked whether they were aware of any sources of credit for their businesses.

Majority of the respondents (98 per cent) were aware of sources or availability of

agricultural finance while only 2 per cent were unaware. This is an indicator that credit

awareness is high due to a well developed financial system but the intended beneficiaries

are not able to access it.

4.4.2 Borrowing patterns

The bulk of the SMEs obtain credit for business growth and expansion and only a few

can do without borrowing from formal and informal sources. Most clients indicated (78

per cent) that they prefer credit in form of cash which is not linked to one enterprise but

the whole family as an economic unit. Respondents were asked whether they had ever

borrowed for business growth. The survey indicated that 89 per cent of the respondents

had borrowed from one source or another in order to grow their businesses. Only 11 per

Adequacy of business finance

020 40 60 80

Business hasAdequateFinance

Business has

No adequateFinance

Per cent%

33

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 34/54

cent of the respondents had never borrowed from any institution to support their

businesses.

4.5 Effect of lending proceduresLending procedure determine the ease of access to agricultural finance from application

to disbursement of the funds. Complicated lending procedure and tiresome bureaucratic

requirements deter potential borrowers from accessing the much needed funds.

Agricultural finance thrives on the principles that more cash is preferred to less, cash

sooner is preferred to cash later and that less risky cash is preferred to more risky cash.

Respondents were interviewed on issues related to amounts borrowed sources of

borrowed funds in the study area and characteristics of lending institutions.

4.5.1 Amounts borrowed from financial institutions

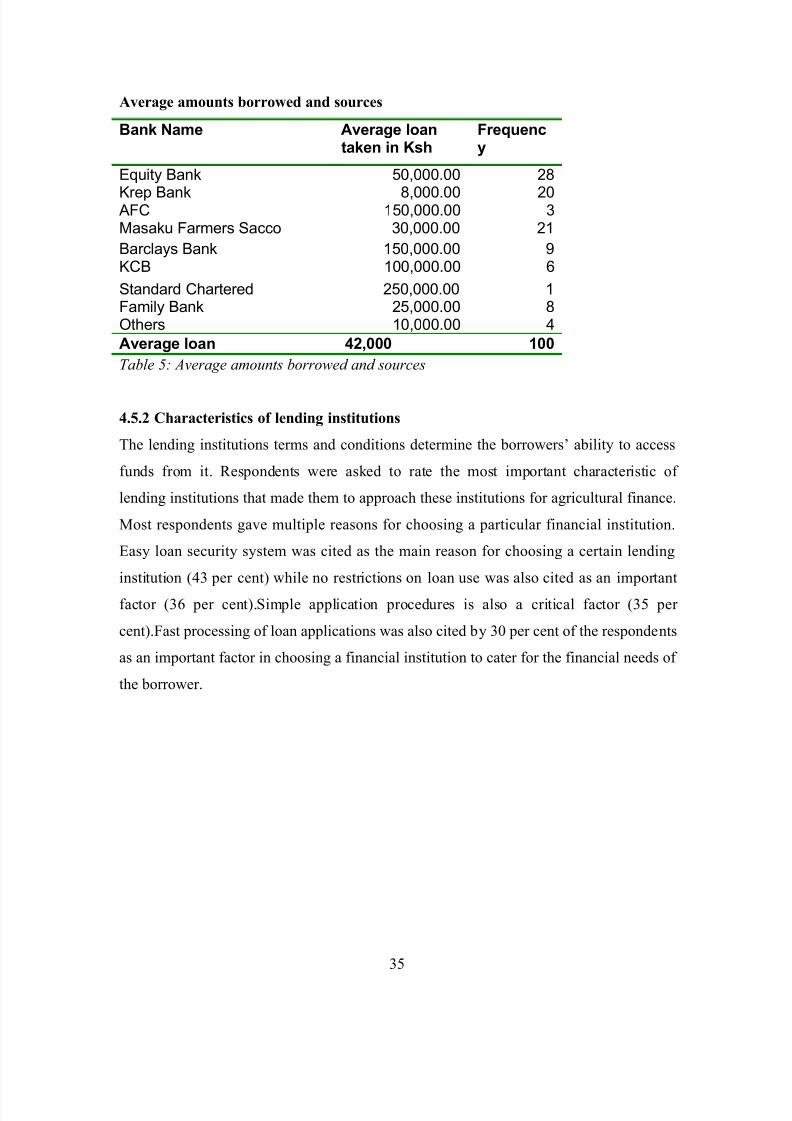

Many of the respondents interviewed had borrowed severally from different financial

institutions and different loan amounts depending on the cash flow needs of the business.

The average amount obtained from financial institution was Ksh 30,000.However some

respondents had obtained as much as Ksh 300,000 from the Agricultural Finance

corporation and KREP Bank. Equity Bank emerged as an upcoming lender to small

enterprises having loaned 28 respondents out of the sample of 120 respondents

interviewed.Equity bank was mentioned by the respondents as reliable lender due to its flexible

collateral requirements ease of disbursement and assessment of the owner as an economic

unit and not the individual enterprise. There is need therefore to develop agricultural

finance products that meet the needs of the clients. The Agricultural Finance Corporation

still remains an important lender to agro based enterprises disbursing large amounts for

enterprise expansion.

Table 5 shows the tally of the average amounts borrowed and the source.

34

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 35/54

Average amounts borrowed and sources

Bank Name Average loantaken in Ksh

Frequency

Equity Bank 50,000.00 28

Krep Bank 8,000.00 20AFC 150,000.00 3Masaku Farmers Sacco 30,000.00 21

Barclays Bank 150,000.00 9KCB 100,000.00 6

Standard Chartered 250,000.00 1Family Bank 25,000.00 8Others 10,000.00 4

Average loan 42,000 100

Table 5: Average amounts borrowed and sources

4.5.2 Characteristics of lending institutions

The lending institutions terms and conditions determine the borrowers’ ability to access

funds from it. Respondents were asked to rate the most important characteristic of

lending institutions that made them to approach these institutions for agricultural finance.

Most respondents gave multiple reasons for choosing a particular financial institution.

Easy loan security system was cited as the main reason for choosing a certain lending

institution (43 per cent) while no restrictions on loan use was also cited as an important

factor (36 per cent).Simple application procedures is also a critical factor (35 per

cent).Fast processing of loan applications was also cited by 30 per cent of the respondents

as an important factor in choosing a financial institution to cater for the financial needs of

the borrower.

35

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 36/54

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 37/54

Corporation shows that out of the 5000 loan applications made in 2007 they had only

managed to process 1235 applications out of which only 1100 were disbursed due to

technicalities such as the entrepreneurs ability to raise the 25 per cent required in cash or

kind for the applications made.

4.7 Policy suggestions regarding agricultural finance

Financial services are part of an interactive system of financial institutions, financial

infrastructure, legal land regulatory frameworks, and social and cultural norms.

Government has a role to play in establishing a favourable or policy environment,

infrastructure and information systems, and supervisory structures to facilitate the

availability of cheap agricultural finance.

Respondents felt that there was a need to change policies so that credit that was available

in the market became cheaper. Most entrepreneurs interviewed in the retrospect realized

that the so called cheap credit availed by some Micro finance institutions is actually

expensive as commercial banks loan and that these institutions applied a lot of pressure

on the individuals to pay up regardless of the business performance. Other major policy

changes that they wished made were in regard to flexible repayment plans to enable themrepay their loans in line with business profitability. Respondents also suggested a major

shift allowing payments after the cropping season as in the tea sector where the bulk of

the payments are dome after the final annual payment.

4.8 Summary of the findings

The majority of the respondents interviewed are male with a mean age of 39 years. Many

of the enterprises are sole proprietorship and the average entrepreneur has at least

secondary education. Many of the entrepreneurs had experienced growth as a result of use of agricultural finance. The most notable increase was in sales volume at 40 per cent.

Business financing was viewed as one of the most challenging factors affecting business

growth with 72 per cent considering their capital resources inadequate.

Lending procedures of financial institutions are critical in determining the availability of

agricultural finance. This is exemplified by looking at the characteristics of the lending

37

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 38/54

institutions. Respondents cited easy loan security system (43 per cent), no restrictions on

loan use (36 per cent) and fast processing of loans (35 per cent) as characteristics that

determine the choice of a lending institution.

The respondents suggested policy changes including increased government role in

making agricultural finance more affordable and flexible repayment plans that take care

of seasonal production patterns.

38

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 39/54

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

5.1 Introduction

The research was carried out to find out whether agricultural finance has played any role

or no role in MSE growth. The researcher obtained data from 120 respondents in six

administrative divisions of Machakos district. Data was analyzed and the findings based

on the study objectives and research questions of the study.

5.2 Summary

The modern entrepreneur has secondary school education. 76 per cent of the respondents

had above secondary school education while 93 per cent of the respondents have at least

primary school education. Only 7 per cent of the respondents had no formal education.

There was no evidence that borrowing is tied to the level of education of the entrepreneur

since almost all the entrepreneurs had ever borrowed finances at one stage or another to

meet their personal or business needs. However the highly educated individuals generally

have a higher access to alternative sources of investment finance due to their ability to

negotiate for alternative sources and the ability to follow the requirements that are needed

to obtain agricultural finance.

There are currently more males than female entrepreneurs in the study area with males

constituting 65 per cent and females taking 35 per cent. The study found that the

entrepreneur borrows largely on personal rather than on business basis. This is because

many entrepreneurs are running businesses that are sole proprietorship in nature with no

formal structures for their businesses. In this respect they have not developed a

comprehensives business plan for their businesses. Formal financial institutions are

currently lending to individuals under the personal loan system without the stringent

application procedures and elaborate collateral system requirements. Accessibility to

agricultural finances is still limited, the application procedures difficult and many

institutions still demand for collateral.

Microfinance institutions are filling this gap by presenting borrowing opportunities under

the group lending approaches. This approach prefers lending to an individual and

39

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 40/54

applying group pressure on the individuals to service their loans regardless of their

business performance. In this respect entrepreneurs continue facing problems of

inadequacy of capital for growing their businesses. The cost of credit is the main

determinant of choice of sourcing for finances for entrepreneurs with 60 per cent of the

entrepreneurs interviewed generally considering the current interest rates charged by

financial institutions as prohibitive and high.

When choosing financial institutions to approach for credit, 56 per cent of potential

borrowers would look at the interest rates charged by the lender from the findings of the

research. On establishing that they are relatively cheap in the market, then they would

consider the following issues in order of priority .30 per cent of the respondents would

first consider whether the lending institution would consider adjusting the repayment

premiums in this respect) therefore they would prefer MFIs which would penalize the

group members to cover for this shortfall rather than sell the individuals assets.32 per

cent of the respondents consider the speed of processing loans third is what collateral the

institutions would ask for then fourth whether the lender might consider rescheduling the

loan in times of misfortunes. Application procedures, proximity to offices or their officers

and size of loan available rank fifth sixth and seventh respectively. A significant minority

of entrepreneurs are happy with the way things are.

5.1Conclusions

The process of transforming traditional and subsistence agricultural production system

into commercial production system through the introduction of improved agricultural

technologies demands the availability agricultural finance. This is quite justified as the

prevailing subsistence agriculture can not produce surplus income beyond family

consumption and social obligations. The gap in time frame between the investment in

agricultural production and acquiring the income is another factor that calls for the

availability of agricultural finance.

40

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 41/54

Financial institutions offering agricultural finance must tailor their products to meet the

needs of their clients. There is need to develop lending policies that recognize that

financial services are part of an interactive system of financial institutions, financial

infrastructure, legal and regulatory framework, social and cultural norms. There is need

to simplify lending procedures and develop unique loan products that cater for the needs

of the entrepreneurs in the agricultural sector.

5.2 Policy Recommendations.

A favorable legal and regulatory framework should be established to facilitate availability

of agricultural finance. The government cannot ignore that MSEs in the agriculture are

crucial plank in meting its employment and development agenda. It should therefore

facilitate the growth of this sector by developing a vibrant lending industry.

5.2.1 Management recommendation

All the stakeholders must build and enhance the business skill of the entrepreneurs in

order to increase their growth potential .When the business capacity of the entrepreneurs

is high, the can visualize the direction which they want their business to grow in the

future. As a result, with increased capacity, they can be able to develop comprehensive

business plans to achieve that vision and as a result increase the demand for credit in the

market , improve productivity and employment and generally assist the government to

meet its development agenda. Treating the farm household as a financial unit integrating

a variety of economic activities, and basing lending decisions on repayment capacity

rather than how funds are utilized is also important to ensure more flow of funds to the

MSEs that require agricultural finance.

5.2.2 Institutional recommendationsLending institutions must review their policies to focus on the vibrant MSE sector. The

current lending environment favours personal lending rather than business lending. As a

result the entrepreneurs are unable to access agricultural finance in levels that can satisfy

their business needs. This capital is therefore not tied to the performance of the business.

41

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 42/54

8/8/2019 Msc Presenters Copy

http://slidepdf.com/reader/full/msc-presenters-copy 43/54

REFERENCES

Adams, D.W. (1992).Taking a fresh look at informal finance In D.W. Adams and D.A.

Fitchett, eds., Informal Finance in Low Income Countries, Boulder Westview Press.Development, vol. 20, no. 10:63–70.