M&S 463, Capturing value1 Topic 6: Capturing value in competitive markets A. Conventional view of...

21

M&S 463, Capturing value 1 Topic 6: Capturing value in competitive markets • A. Conventional view of imitator/innovator – Reverse engineering & imitation – Competitive tactics • B. Capturing value as an innovator or imitator – Co-specialized assets – The evolving perspective on the use of secrecy, patents, lead-time • C. Sell-out to an incumbent or commercialize? – Capturing value in markets for ideas or organizations

-

date post

21-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of M&S 463, Capturing value1 Topic 6: Capturing value in competitive markets A. Conventional view of...

M&S 463, Capturing value 1

Topic 6: Capturing value in competitive markets

• A. Conventional view of imitator/innovator– Reverse engineering & imitation

– Competitive tactics

• B. Capturing value as an innovator or imitator– Co-specialized assets

– The evolving perspective on the use of secrecy, patents, lead-time

• C. Sell-out to an incumbent or commercialize?– Capturing value in markets for ideas or organizations

M&S 463, Capturing value 2

A. Strategies about imitation: Reverse Engineering

• Two different examples– Wrebbit: the inventor out-smarts the imitators

– Compaq: the imitator out-smarts the innovator

• Not a tale where good guy always wins– Sometimes imitators win, sometimes innovators

– “It depends.” It depends on what? Luck, strategy, etc.

– Must always go through calculations about when imitation is worthwhile, about likelihood of being imitated, market conditions, etc.

M&S 463, Capturing value 3

A. Wrebbit: an example where the innovator wins

• The idea for the 3-d puzzle– What is the scarce resource? The ideas or the know-

how to implement?

– What precedent did the players have to use?

• How easy is it for an established player to imitate the basic elements of the idea?

• What kind of deal can Wrebbit make?– What assets do they bring to the table?

– What assets does Milton Bradley bring to the table?

M&S 463, Capturing value 4

A. Compaq: An example where the imitator wins

• The idea for the Compaq computer– What is the scarce resource? The idea or the resources

to implement?– What precedent did the players use?

• How easy was it for the player to imitate the basic elements of the IBM computer?

• Compaq had to solve one problem to realize their goal. Was it easy/hard to do?– Did their solution influence/inspire others to pursue

related ideas?

M&S 463, Capturing value 5

A. The basics behind the innovator/imitator situation

• The costs of imitating an innovation– What is in the public domain? What is privately held?– Tacit/codified knowledge hard/easy to acquire or imitate– Easy/hard to hire necessary talent or acquire key assets

• Speed and order of entry– One strategy: First, fast and in front (also free?)– The strategy of the “fast second”

• Situation happening once? Are events regularly happening as part of product/technology cycle? – Featuritis among long time rivals

M&S 463, Capturing value 6

A. Basic and obvious tactics

• Innovators try to raise the costs to imitators– Keep knowledge out of public domain– Keep knowledge tacit, not codified– Keep talented individuals away from rivals

• Innovators identify the sources of rivalry– Where do potential imitators come from?– How to soberly evaluate ability of imitator to succeed?

• Imitators use assets/technical talent to move quickly– The hard part: knowing when & what to imitate– How to be a fast-second? Who can do this? Why?

M&S 463, Capturing value 7

A. More tactics: It depends on industry/market situation

• Large variation across industries– Imitation usually costs a fraction of invention costs– Imitation arrives quickly in most markets, not always. Why?– Why is imitation so hard in some markets? What is so special

about those situations?

• What firms use to protect their innovations– Patents/copyright, secrecy, first to market or first

mover/complementary assets– Effectiveness differs across industries– More on this later

M&S 463, Capturing value 8

B. What is missing from simple tactics? Who captures value?

• Teece’s framework emphasizes complementary assets set inside the dominant design paradigm

• Appropriability conditions– Tight: Patents work, can keep secrets, tacit knowledge– Loose: Mostly public and codified knowledge

• Pre and post paradigmatic industries– Are consumer tastes known?– Are assets and modes of business established?– How firms make investments in anticipation of

emergence of dominant design

M&S 463, Capturing value 9

B. Co-specialized assets

• What is a co-specialized asset?– It is complementary to commercializing technology– All commercialization used in conjunction with business

assets and market focus– Assets which lose substantial value in other use– The “hold-up” problem

• Teece: Own co-specialized assets at the outset– If not, then build new division in firm – Or contract for them – The many hazards of developing new assets (more later)

M&S 463, Capturing value 10

B. The framework in tight regime

• Capturing value in tight appropriability regime– Innovator wins most of the time– May share profits with co-specialized asset owners if

innovator in poor bargaining position (but this depends on bargaining abilities of parties involved, so unpredictable)

• Examples– Pharmaceuticals is strong, classic example– Biotech is becoming example where bargains are made and

profits are typically shared (similar to Wrebbit)– Note: a bit vague on the contractual & bargaining details

M&S 463, Capturing value 11

B. The framework in loose regime

• Who is positioned to strike a tough bargain? – If both or neither is in good position

• If innovator better than imitator– Innovator wins, but makes contracts or builds own assets– Consumer electronics, “building own web page”

• If innovator worse than imitator– If both strong, then either could win, depends on bargain– Microsoft today, IBM in the past– If both weak, then innovator should give up– Wrebbit w/o patent protection

M&S 463, Capturing value 12

B. Implications now a routine part of strategy curriculum

• A likely loser: Good technology alone– Building or contracting for co-specialized assets essential

• A winner: Control co-specialized assets– Example: Cable co. & the pipe bottleneck for ISPs, Local

telephone firms & DSL after-sale service/quality assurance– Strategy: Identify co-specialized assets, but how do you

know which assets these are? And which will be valuable?

• Predicting winners/losers on the basis of uniquely situated co-specialized assets– Example: IBM and its marketing contact– Example: Microsoft and API protocols

M&S 463, Capturing value 13

B. What’s missing from Teece? Firm strategy contains nuance

• Surveys show that there are three “types” of appropriation strategies– Secrecy (includes non-disclosure, non-compete)– Patenting/copyright & other IP tends to be enforceable– Complementary assets/first to market works sometimes– Not mutually exclusive strategies: Often used together

• The limits/benefits to contracting not articulated– How firms use hold-up ability in bargains.– The key differences between facing a bottleneck when

innovating and not facing a bottleneck.

M&S 463, Capturing value 14

C. Selling out to an incumbent or commercialize on own

• G&S: Focus on decision by small firm to compete in output mrkt or sell “ideas market” – Note: Small firms usually choose one or other, not both– Note: Small = approx 50 employees or less.

• Cooperating w/incumbent takes many forms– Marketing/distribution agreement (e.g., biotech/pharma)– Outright sale of unit (to e.g., Cisco)

• Commercialization on own takes many forms– Build all dimensions of the business in dist, brand, manu…– Then compete with incumbent in output market

M&S 463, Capturing value 15

C. The “drivers”: Excluding others, complementary assets

• Can the inventor/start-up preclude effective development by incumbent?– If any of three types of appropriation strategies are effective

• Would agreement with incumbent for use of their complementary assets enhance value proposition?

• Bargaining problems that make agreement difficult– Disclosure: Price depends on revelation of info, but

revelation makes owner of idea too exploitable– Contingency: Value depends on future (e.g., demand)– Perception: Value debatable prior to market experience

M&S 463, Capturing value 16

C: A synopsis of the frameworkDo the incumbent’s complementary assets have value?

No Yes

Can the start-up exclude development by the incumbent?

No Head-to-head competition

Disk drives

Incumbent sets the bargaining tone

AOL, Yahoo, MS

Yes Green-field market

development

Transistors

Market & contracts for ideas

Biotechnology

M&S 463, Capturing value 17

C: When complementary assets have little value

• No strong IP (or its equivalent)– Intensely competitive product market w/no sustainable leads

except through renewal of inventiveness– Effective bargain b/w entrant & incumbent unlikely– Entrants look for novel value proposition & aspire to rebuild

many existing assets under own roof– Ex: Disk drives & other electronic component markets

• Strong IP (rare: almost greenfield development)– Possibility for licensing an upstream “architecture”– Ex: Transistors, Qualcom & wireless?– Patent about basic science: DNA or university discovery– Too many firms wrongly think they live in this situation

M&S 463, Capturing value 18

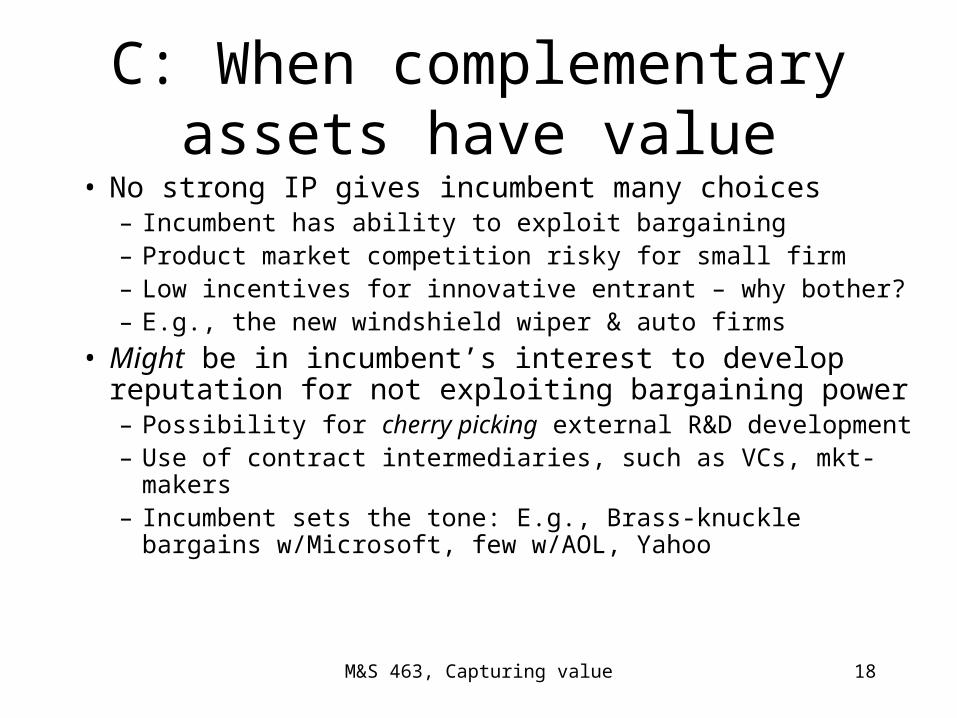

C: When complementary assets have value

• No strong IP gives incumbent many choices– Incumbent has ability to exploit bargaining– Product market competition risky for small firm– Low incentives for innovative entrant – why bother?– E.g., the new windshield wiper & auto firms

• Might be in incumbent’s interest to develop reputation for not exploiting bargaining power– Possibility for cherry picking external R&D development– Use of contract intermediaries, such as VCs, mkt-makers– Incumbent sets the tone: E.g., Brass-knuckle bargains

w/Microsoft, few w/AOL, Yahoo

M&S 463, Capturing value 19

C: Outcomes when complementary assets have value

• W/strong IP– Incumbents look to coopt potential entrants– Entrants deliberately establish firm to sell-out (but price

depends critically on bargaining power)– Entrants compete for priority w/incumbent– Frequent source of innovativeness, not market leadership– E.g., Biotechnology

• New invention reinforces extant platform– Tend not to see challenges to existing platform– Except if “perception” of incumbent/entrant wildly differ

about value of invention, which interferes w/bargain

M&S 463, Capturing value 20

C: Implications from this approach

• Ability to hold strong IP makes contracting feasible– Issue is often “when”, not “if. Waiting for prototype…– W/o explicit contracting commercialize on own– W/o right tone from incumbent small firm may avoid a

deal and develop on own

• Incumbent firms can influence direction of entrant– Committing to a path (MS announces ahead of time)– Commitment to soft bargain (Cisco’s purchase pattern)

• Existing assets have value b/c alter bargain price– Shadow cast by “potential product competition”– Shadow cast by “potential R&D productivity”

M&S 463, Capturing value 21

Learning Points

• Understanding the innovator/imitator– Often incumbent/entrant, though not always

• Capturing value from innovation– The importance of complementary assets

– Bargaining for co-specialized assets

• The option to sell-out instead of compete– Bargaining for ideas

– Value of assets arises from their use in a bargain as well as in direct product market competition