MPR October 211009. Figure 1.1. Repo rate Per cent, quarterly averages Source: The Riksbank Note....

106

MPR October 211009

-

Upload

sophie-cole -

Category

Documents

-

view

215 -

download

1

Transcript of MPR October 211009. Figure 1.1. Repo rate Per cent, quarterly averages Source: The Riksbank Note....

MPR October211009

Figure 1.1. Repo ratePer cent, quarterly averages

-2

-1

0

1

2

3

4

5

6

7

04 05 06 07 08 09 10 11 12-2

-1

0

1

2

3

4

5

6

790%75%50%OutcomeForecast

Source: The RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.2. GDP with uncertainty bandsAnnual percentage change, seasonally-adjusted data

-8

-6

-4

-2

0

2

4

6

04 05 06 07 08 09 10 11 12-8

-6

-4

-2

0

2

4

6

90%

75%

50%

Otcome

Forecast

Sources: Statistics Sweden and the Riksbank

Figure 1.3. CPI with uncertainty bandsAnnual percentage change

-2

-1

0

1

2

3

4

5

6

7

04 05 06 07 08 09 10 11 12-2

-1

0

1

2

3

4

5

6

790%75%50%OutcomeForecast

Sources: Statistics Sweden and the Riksbank

Figure 1.4. CPIF with uncertainty bandsAnnual percentage change

-1

0

1

2

3

4

04 05 06 07 08 09 10 11 12-1

0

1

2

3

490%75%50%OutcomeForecast

Sources: Statistics Sweden and the Riksbank

Figure 1.5. GDP-growth abroadAnnual percentage change

-2

-1

0

1

2

3

4

5

6

7

70 74 78 82 86 90 94 98 02 06 10-2

-1

0

1

2

3

4

5

6

7

Sources: IMF and the RiksbankNote. Striped bars represent the Riksbank’s forecast.

Figure 1.6. Difference between interbank rates and government bond rates (TED

spread)Basis points

0

50

100

150

200

250

300

350

400

450

500

Jan-07

Apr-07

Jul-07

Oct-07

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

0

50

100

150

200

250

300

350

400

450

500Sweden

Euro area

USAUnited Kingdom

Sources: Reuters EcoWin and the Riksbank

Figure 1.7. Difference between intebank rates and expected monetary policy (Basis

spread)Basis points

0

50

100

150

200

250

300

350

400

Jan-07

Apr-07

Jul-07

Oct-07

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

0

50

100

150

200

250

300

350

400Sweden

Euro area

USA

United Kingdom

Sources: Reuters EcoWin and the Riksbank

Figure 1.8. Stock market movementsIndex, 04.01.99 = 100

40

60

80

100

120

140

160

180

200

220

99 00 01 02 03 04 05 06 07 08 0940

60

80

100

120

140

160

180

200

220Sweden (OMXS)

Euro area (Euro Stoxx)

USA (S&P 500)

Source: Reuters EcoWin

Figure 1.9. Stock market implied volatilityPer cent

0

10

20

30

40

50

60

70

80

90

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09

0

10

20

30

40

50

60

70

80

90OMX30 (Sweden)

EuroStoxx (Euro area)

VIX (USA)

Sources: Chicago Board Option Exchange, Reuters EcoWin and STOXX Limited

Figure 1.10. Consumer confidence in Sweden, the euro area and the USA

Net figures and index, 1985 = 100

-50

-40

-30

-20

-10

0

10

20

30

00 01 02 03 04 05 06 07 08 090

20

40

60

80

100

120

140

160

Sweden (left scale)

Euro area (left scale)

USA (right scale)

Sources: The Conference Board, European Commission and National Institute of Economic Research

Figure 1.11. Households’ net wealth and saving ratio in the USA

Percentage of disposable income

300

350

400

450

500

550

600

650

50 55 60 65 70 75 80 85 90 95 00 05 100

2

4

6

8

10

12

14

Net wealth (left scale)Saving ratio (right scale)

Sources: Federal Reserve and Department of Commerce Analysis, Eurostat, Statistics Sweden and the Riksbank

Figure 1.12. GDP for the USA and the euro area

Quarterly changes in per cent calculated in annualised terms, seasonally-adjusted data

-10

-8

-6

-4

-2

0

2

4

6

8

10

00 01 02 03 04 05 06 07 08 09 10 11 12 13-10

-8

-6

-4

-2

0

2

4

6

8

10

Euro area

USA

Sources: Bureau of Economic Analysis, Eurostat and the Riksbank

Figure 1.13. TCW-weighted exchange rate Index, 18.11.92 = 100

Source: The Riksbank

120

125

130

135

140

145

150

155

160

04 05 06 07 08 09 10 11 12

120

125

130

135

140

145

150

155

160

October

September

Figure 1.14. Comparison of recovery in Sweden, the euro area and USA

GDP-level, index 2007 quarter 4 = 100

92

94

96

98

100

102

104

106

108

110

07 08 09 10 11 1292

94

96

98

100

102

104

106

108

110USA

Euro area

Sweden

Sources: Bureau of Economic Analysis, Eurostat, Statistics Sweden and the Riksbank.

Figure 1.15. Comparison of recovery following various recessions, GDP Sweden

Index in the quarter preceding the beginning of the recession = 100

92949698

100102104106108110112114116118

-4 -2 0 2 4 6 8 10 12 14 16 1892949698100102104106108110112114116118

1990 Q2

1996 Q1

2000 Q3

2008 Q1

Sources: Statistics Sweden and the Riksbank

Figure 1.16. GDPQuarterly changes in per cent calculated in annualised

terms, seasonally-adjusted data

-20

-15

-10

-5

0

5

10

00 01 02 03 04 05 06 07 08 09 10 11 12-20

-15

-10

-5

0

5

10

September

October

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.17. Households’ consumption, disposable incomes and saving ratio

Annual percentage change, fixed prices and percentage of disposable income

-2

-1

0

1

2

3

4

5

6

7

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-4

-2

0

2

4

6

8

10

12

14

Consumption (left scale)Disposable income (left scale)Saving ratio (right scale)

Sources: Statistics Sweden and the RiksbankNote. Broken lines and striped bars represent the Riksbank’s forecast.

Figure 1.18. Confidence indicator and saving ratio for households

Net figures and per cent

-30

-20

-10

0

10

20

30

40

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09-12

-8

-4

0

4

8

12

16

Saving ratio (right scale)

Confidence indicator (left scale)

Sources: National Institute of Economic Research and Statistics Sweden

Figure 1.19. Swedish exports and world market for Swedish exports

Annual percentage change

Sources: Statistics Sweden and the RiksbankNote. Dots represent the Riksbank's forecast for the whole year.

-20

-15

-10

-5

0

5

10

15

20

80 85 90 95 00 05 10

-20

-15

-10

-5

0

5

10

15

20

Swedish exports

World market for Swedish exports

Figure 1.20. Gross fixed capital formationQuarterly changes in per cent calculated in annualised

terms, seasonally-adjusted data

-50-45-40-35-30-25-20-15-10-505

101520

04 05 06 07 08 09 10 11 12-50-45-40-35-30-25-20-15-10-505101520

September

October

Sources: Statistics Sweden and the Riksbank

Figure 1.21. Labour force and number of employed

Thousands, seasonally-adjusted data

3800

4000

4200

4400

4600

4800

5000

80 85 90 95 00 05 103800

4000

4200

4400

4600

4800

5000Employed, 16-64 yearsEmployed, 15-74 yearsLabour force, 16-64 yearsLabour force, 15-74 years

Sources: Statistics Sweden and the Riksbank

Figure 1.22. Employment rateEmployment as a percentage of the population, 16-64

year, seasonally-adjusted data

70

72

74

76

78

80

82

84

80 85 90 95 00 05 1070

72

74

76

78

80

82

84September

October

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.23. UnemployedPercentage of the labour force, seasonally-adjusted data

0

2

4

6

8

10

12

14

80 85 90 95 00 05 100

2

4

6

8

10

12

14

Unemployment, 16-64 years

Unemployment, 15-74 years

OctoberSeptember

Sources: Statistics Sweden and the Riksbank

Figure 1.24. Actual and trend productivity growth in

the economy as a wholeAnnual percentage change, seasonally-adjusted data

-5

-4

-3

-2

-1

0

1

2

3

4

5

80 85 90 95 00 05 10-5

-4

-3

-2

-1

0

1

2

3

4

5

October

HP-trend

September

Sources: Statistics Sweden and the Riksbank

Figure 1.25. Estimated gapsPercentage deviation from the HP trend

-5

-4

-3

-2

-1

0

1

2

3

4

5

80 85 90 95 00 05 10-5

-4

-3

-2

-1

0

1

2

3

4

5GDP

Hours worked

Employment

Sources: Statistics Sweden and the Riksbank

Figure 1.26. Nominal wages Annual percentage change

0

2

4

6

8

10

12

80 85 90 95 00 05 100

2

4

6

8

10

12September

October

Sources: National Mediation Office, Statistics Sweden and the Riksbank

Figure 1.27. Unit labour costs for the economy as a whole

Annual percentage change, fixed prices and per cent of disposable income

-2

-1

0

1

2

3

4

5

6

7

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-2

-1

0

1

2

3

4

5

6

7

ProductivityLabour cost per hourUnit labour cost

Sources: Statistics Sweden and the Riksbank

Figure 1.28. CPI, CPIF and CPIF excluding energy

Annual percentage change

-2

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10 11 12-2

-1

0

1

2

3

4

5CPI

CPIF

CPIF excluding energy

Sources: Statistics Sweden and the Riksbank

Figure 1.29. CPIF excluding energy and unit labour costs

Annual percentage change

-4

-2

0

2

4

6

8

10

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13-4

-2

0

2

4

6

8

10Unit labour cost

CPIF excluding energy

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.30. Oil price, Brent crudeUSD per barrel

0

20

40

60

80

100

120

140

00 01 02 03 04 05 06 07 08 09 10 11 120

20

40

60

80

100

120

140

OutcomeFutures, average up to and including 10 OctoberFutures, September

Sources: Intercontinental Exchange and the Riksbank

Figure 1.31. HICP in Sweden and in the euro area

Annual percentage change

-1

0

1

2

3

4

5

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-1

0

1

2

3

4

5Sweden

Euro area

Sources: Eurostat, Statistics Sweden and the Riksbank Note. Broken lines represent the Riksbank’s forecast.

Figure 1.32. Repo ratePer cent, quarterly averages

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

00 01 02 03 04 05 06 07 08 09 10 11 120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0September

October

Source: The RiksbankNote. Broken lines represent the Riksbank’s forecast.

Figure 1.33. Real repo ratePer cent, quarterly averages

-2

-1

0

1

2

3

04 05 06 07 08 09 10 11 12-2

-1

0

1

2

3September

October

Source: The Riksbank

Figure 1.34. CPIFAnnual percentage change

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

00 01 02 03 04 05 06 07 08 09 10 11 120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0September

October

Sources: Statistics Sweden and the Riksbank

Figure 2.1. GDP abroadTCW-weighted, quarterly changes in per cent calculated

in annualised terms

-10

-8

-6

-4

-2

0

2

4

6

04 05 06 07 08 09 10 11 12-10

-8

-6

-4

-2

0

2

4

6

Main scenario

Higher level of international growth

Sources: National sources and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.2. Labour market gap (hours worked)

Percentage deviation from the HP trend

-3

-2

-1

0

1

2

3

4

5

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-3

-2

-1

0

1

2

3

4

5Higher level of international growth

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.3. CPIFAnnual percentage change

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

04 05 06 07 08 09 10 11 120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0Higher level of international growth

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.4. Repo ratePer cent, quarterly averages

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

04 05 06 07 08 09 10 11 120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Main scenario

Higher level of international growth

Source: the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.5. GDPQuarterly averages in per cent calculated in annualised

terms

-20

-16

-12

-8

-4

0

4

8

04 05 06 07 08 09 10 11 12-20

-16

-12

-8

-4

0

4

8

Higher level of international growthMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.6. GDPQuarterly averages in per cent calculated in annualised

terms

-20

-16

-12

-8

-4

0

4

8

04 05 06 07 08 09 10 11 12-20

-16

-12

-8

-4

0

4

8

Increased labour productivity

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.7. CPIFAnnual percentage change

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

04 05 06 07 08 09 10 11 120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0Increased labour productivity

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.8. Labour market gap (hours worked)

Percentage deviation from the HP trend

-3

-2

-1

0

1

2

3

4

5

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-3

-2

-1

0

1

2

3

4

5Increased labour productivity

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.9. Repo ratePer cent, quarterly averages

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

04 05 06 07 08 09 10 11 12-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Main scenario

Increased labour productivity

Source: the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.10. Repo ratePer cent, quarterly averages

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

04 05 06 07 08 09 10 11 12-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0Main scenarioLower interest rateHigher interest rate

Source: the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.11. GDPQuarterly averages in per cent calculated in annualised

terms

-20

-16

-12

-8

-4

0

4

8

04 05 06 07 08 09 10 11 12-20

-16

-12

-8

-4

0

4

8

Lower interest rateHigher interest rate

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.12. Production gapPercentage deviation from the HP trend

-5

-4

-3

-2

-1

0

1

2

3

4

5

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-5

-4

-3

-2

-1

0

1

2

3

4

5Lower interest rate

Higher interest rate

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.13. Labour market gap (hours worked)

Percentage deviation from the HP trend

-3

-2

-1

0

1

2

3

4

5

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12-3

-2

-1

0

1

2

3

4

5Lower interest rate

Higher interest rate

Main scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 2.14. CPIFAnnual percentage change

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

04 05 06 07 08 09 10 11 120.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0Lower interest rateHigher interest rateMain scenario

Sources: Statistics Sweden and the RiksbankNote. Broken lines represent the Riksbank's forecast.

Figure 3.1. Long-term interest ratesPer cent

0

1

2

3

4

5

6

04 05 06 07 08 090

1

2

3

4

5

6

SwedenEuro area (Germany)USAUnited Kingdom

Source: Reuters EcoWinNote. Government bonds with approximately 10 years left to maturity.

Figure 3.2. Government bonds in various euro countries (difference compared to

Germany)Percentage points

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

07 08 09-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5SwedenUnited KingdomGreeceIrelandSpainItaly

Source: Reuters EcoWinNote. Government bonds with approximately 10 years left to maturity.

Figure 3.3. Two-year interest ratesPer cent

0

1

2

3

4

5

6

04 05 06 07 08 090

1

2

3

4

5

6

SwedenEuro areaUSAUnited Kingdom

Source: Reuters EcoWinNote. Government bonds with approximately 2 years left to maturity.

Figure 3.4. Monetary policy expectations in the Euro area and the USA

Per cent

0

1

2

3

4

5

6

06 07 08 09 10 11 120

1

2

3

4

5

6ECB

ECB 03-09-2009

ECB 15-10-2009

FED

FED 03-09-2009

FED 15-10-2009

Sources: Reuters Ecowin and the Riksbank

Figure 3.5. Monetary policy expectations in Sweden according to money market

participants Per cent

Sources: Reuters Ecowin, Prospera Research AB and the Riksbank

0

1

2

3

4

5

06 07 08 09 10 11 12

0

1

2

3

4

5Repo rateForward rate 03-09-2009Forward rate 15-10-2009Survey, Prospera averages, 16-09-2009

Figure 3.6. Monetary baseBillion SEK

0

50

100

150

200

250

300

350

400

450

jan/08 apr/08 jul/08 okt/08 jan/09 apr/09 jul/090

50

100

150

200

250

300

350

400

450The banks’ holdings of Riksbank certificatesDeposits including fine tuningBanknotes and coins in circulation

Source: The Riksbank

Figure 3.7. Households' and non-financial companies' total borrowing from credit

institutionsAnnual percentage change

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09 10-10

-5

0

5

10

15

20Households

Companies

Sources: Statistics Sweden and the Riksbank

Figure 3.8. Manufacturing companies’ borrowing on the credit market

Billion USD and EUR

0

100

200

300

400

500

600

00 01 02 03 04 05 06 07 08 090

100

200

300

400

500

600Bond issues denominated in USD

Bond issues denominated in EUR

Sources: Bloomberg and the Riksbank

Figure 3.9. Long-term mortgage rates in SwedenPer cent

0

1

2

3

4

5

6

7

04 05 06 07 08 09

0

1

2

3

4

5

6

7Listed mortgage rate 5 yearsGovernment bond 5 yearsMortgage bond 5 years

Sources: Nordea, Reuters EcoWin, SBAB, SEB, Spintab, Stadshypotek, Statistics Sweden and the Riksbank

Figure 3.10. Single-family dwelling pricesPurchase price coefficient, whole country

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

03 04 05 06 07 08 09 101.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

Source: Statistics Sweden

Figure 3.11. Money supplyAnnual percentage change

-4

0

4

8

12

16

20

24

00 01 02 03 04 05 06 07 08 09-4-2024681012141618202224

Banknotes and coins

M2

M3

Sources: Statistics Sweden and the Riksbank

Figure 3.12. Exchange ratesSEK per euro and dollar

5

6

7

8

9

10

11

12

04 05 06 07 08 095

6

7

8

9

10

11

12SEK/EUR

SEK/USD

Source: Reuters EcoWin

Figure 3.13. World Trade Monitor IndexIndex, 2000 = 100, seasonally adjusted data

0

25

50

75

100

125

150

175

90 92 94 96 98 00 02 04 06 08 100

25

50

75

100

125

150

175

Source: Netherlands Bureau for Economic Policy Analysis

Figure 3.14. Purchasing mangarer's index in the manufacturing industry

Index

30

35

40

45

50

55

60

65

00 01 02 03 04 05 06 07 08 09 1030

35

40

45

50

55

60

65Euro area

USA

Sources: Institute for Supply Management and NTC Research Ltd

Figure 3.15. ExportIndex, 2006 quarter 1 = 100

60

80

100

120

140

160

00 01 02 03 04 05 06 07 08 09 1060

80

100

120

140

160

USA

Euro area

Sources: National sources and the Riksbank

Figure 3.16. Consumer prices Annual percentage change

-3

-2

-1

0

1

2

3

4

5

6

00 01 02 03 04 05 06 07 08 09 10-3

-2

-1

0

1

2

3

4

5

6USAEuro areaTCW (100%)

Sources: Bureau of Labor Statistics, Eurostat and OECD

Figure 3.17. Commodity pricesIndex 2000 = 100, USD

50

100

150

200

250

300

350

00 01 02 03 04 05 06 07 08 09

50

100

150

200

250

300

350TotalMetalsOther agricultural productsFood

Source: The Economist

Figure 3.18. The Economic Tendency Indicator

Index, mean = 100

70

75

80

85

90

95

100

105

110

115

120

00 01 02 03 04 05 06 07 08 09 1070

75

80

85

90

95

100

105

110

115

120

The Economic Tendency IndicatorMean+/- one standard deviation

Source: National Institute of Economic Research

Figure 3.19. Confidence indicators for the business sector

Seasonally adjusted net figures

-80

-60

-40

-20

0

20

40

60

00 01 02 03 04 05 06 07 08 09 10-80

-60

-40

-20

0

20

40

60

Manufacturing industryConstruction industryRetail tradePrivate service industriesTotal business sector

Source: National Institute of Economic Research

Figure 3.20. Manufacturing output and orders

Index 2005 = 100, seasonally adjusted data

50

60

70

80

90

100

110

120

130

00 01 02 03 04 05 06 07 08 0950

60

70

80

90

100

110

120

130Manufacturing outputOrders

Source: Statistics Sweden

Figure 3.21. Disposable income and savings

Annual percentage change and per cent of disposable income

-12-10-8-6-4-202468

101214

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08-12-10-8-6-4-202468101214

Savings ratioReal disposable income

Sources: Statistics Sweden and the Riksbank

Figure 3.22. Retail sales and household consumption

Annual percentage change, calendar adjusted data

-4

-2

0

2

4

6

8

10

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10-4

-2

0

2

4

6

8

10

Households' consumption of retail goodsRetail salesHouseholds' total consumption

Source: Statistics SwedenNote. Non-calendar-adjusted data.

Figure 3.23. Households' expectations for the futureNet figures

-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

94 96 98 00 02 04 06 08 10-90

-75

-60

-45

-30

-15

0

15

30

45

60

75

Unemployment

Confidence Indicator

Source: National Institute of Economic Research

Figure 3.24. General government net lending

Per cent of GDP

-12

-10

-8

-6

-4

-2

0

2

4

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10-12

-10

-8

-6

-4

-2

0

2

4

Source: Statistics Sweden

Figure 3.25. Gross fixed capital formationAnnual percentage change

-40

-30

-20

-10

0

10

20

30

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10-40

-30

-20

-10

0

10

20

30

Business sector excluding housingHousingPublic authorities

Source: Statistics Sweden

Figure 3.26. Foreign trade with goods in fixed prices

Three-month changes in per cent calculated in annualised terms, seasonally adjusted data

-75

-50

-25

0

25

50

75

80 85 90 95 00 05 10-75

-50

-25

0

25

50

75Export

Import

Sources: Statistics Sweden and the Riksbank

Figure 3.27. New export ordersNet figures and annual percentage change

-60

-40

-20

0

20

40

60

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10-60

-40

-20

0

20

40

60

Orders, NIER (net figures)

Orders, Statistics Sweden (annual percentage change)

Sources: National Institute of Economic Research and Statistics Sweden

Figure 3.28 Employment rate, labour force and unemployment

Thousands, seasonally adjusted data

4000

4200

4400

4600

4800

5000

00 01 02 03 04 05 06 07 08 090

2

4

6

8

10Employment rate (left)Labour force (left)Unemployment (right)

Sources: Employment service and the Riksbank

Figure 3.29. New and unfilled vacant jobs and redundancy notices

Thousands, seasonally adjusted data

0

20

40

60

80

100

88 90 92 94 96 98 00 02 04 06 08 100

4

8

12

16

20New vacancies (left scale)Unfilled vacancies (left scale)

Redundancy notices (right scale)

Source: Employment service and the Riksbank

Figure 3.30. Proportion of companies reporting a shortage of labour

Per cent, seasonally adjusted data

0

10

20

30

40

50

60

70

91 95 99 03 07 110

10

20

30

40

50

60

70Manufacturing industryConstruction sectorRetail tradePrivate sector industriesBusiness sector

Source: National Insitute of Economic Research

Figure 3.31. Employees in the business sector, expectations and outcome

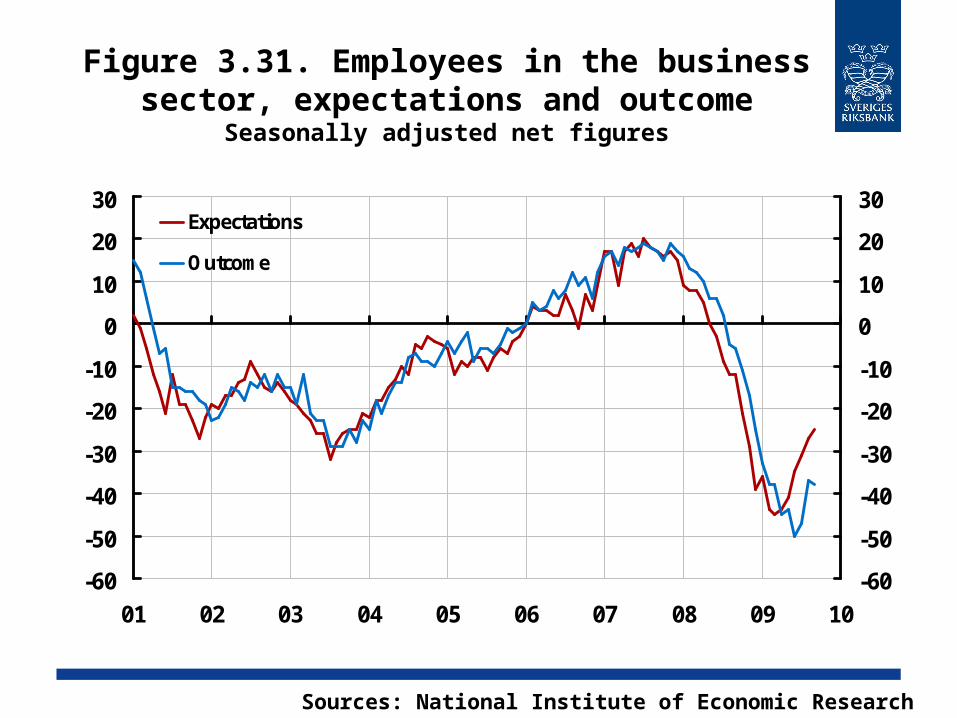

Seasonally adjusted net figures

-60

-50

-40

-30

-20

-10

0

10

20

30

01 02 03 04 05 06 07 08 09 10-60

-50

-40

-30

-20

-10

0

10

20

30Expectations

Outcome

Sources: National Institute of Economic Research

Figure 3.32. Capital utilisation in industryPer cent, seasonally adjusted data

70

75

80

85

90

95

80 85 90 95 00 05 1070

75

80

85

90

95

Statistics Sweden, actual capacity utilisation

NIER, current capacity utilisation

Sources: National Institute of Economic Research and Statistics Sweden

Figure 3.33. WagesAnnual percentage change

0

1

2

3

4

5

6

7

8

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 100

1

2

3

4

5

6

7

8Public sector

Business sector

Sources: National Mediation Office and the Riksbank

Figure 3.34. Wages in the business sectorAnnual percentage change

1

2

3

4

5

6

00 01 02 03 04 05 06 07 08 09 101

2

3

4

5

6

Construction sector

Service sector

Industry

Sources: National Mediation Office and the Riksbank

Figure 3.35. Expectations of inflation one year ahead

Per cent

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

00 01 02 03 04 05 06 07 08 09 100.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0Households (NIER)

Companies (NIER)

All (Prospera)

Sources: National Institute of Economic Research and TNS Prospera

Figure 3.36. All respondents' expectations of inflation one, two and five years ahead

Per cent

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

96 98 00 02 04 06 08 100.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.01 year2 years5 years

Source: TNS Prospera

Figure 3.37. The difference between nominal and real five-year rates (break-

even inflation)Percentage points

0.0

0.5

1.0

1.5

2.0

2.5

3.0

00 01 02 03 04 05 06 07 08 09 100.0

0.5

1.0

1.5

2.0

2.5

3.0

Source: The Riksbank

Figure 3.38. Prices of goods and services in the CPI

Annual percentage change

-3

-2

-1

0

1

2

3

4

00 01 02 03 04 05 06 07 08 09 10

-3

-2

-1

0

1

2

3

4

Services (43,5 %)Goods excluding energy and food (26,3 %)

Source: Statistics SwedenNote. The weight of CPI of the respective components is given in brackets.

Figure 3.39. Food, energy and mortgage costs in the CPI

Annual percentage change

-50

-40

-30

-20

-10

0

10

20

30

00 01 02 03 04 05 06 07 08 09 10-50

-40

-30

-20

-10

0

10

20

30

Food (16.8 %)Energy (8.9 %)Mortgage costs (4.5 %)

Source: Statistics SwedenNote. The weight of CPI of the respective components is given in brackets.

Figure B1. Mean square gaps for the forecast of inflation and resource

utilisation REVISEDAverage squared deviation during the forecast horizon

Source: The Riksbank

Main scenario

Lower rate

Higher rate

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8Inflation

Res

ourc

e ut

ilisa

tion

Figure B2. Money supply (M2), monetary base and credit multiplierSEK billion and ratio respectively

0

200

400

600

800

1000

1200

1400

1600

1800

2000

02 03 04 05 06 07 08 09 10

0

2

4

6

8

10

12

14

16

18

20M2 (left scale)

Monetary base (left scale)

Credit multiplier (right scale)

Sources: Statistics Sweden and the Riksbank

Figure B3. Single-family dwelling prices and household lending

Annual percentage change

-16

-12

-8

-4

0

4

8

12

16

91 93 95 97 99 01 03 05 07 09-16

-12

-8

-4

0

4

8

12

16

House prices

Household lending

Sources: Statistics Sweden and the Riksbank

Figure B4. Housing investmentsPercentage of GDP, current prices

0

1

2

3

4

5

6

86 88 90 92 94 96 98 00 02 04 06 080

1

2

3

4

5

6

Source: Statistics SwedenNote. Four-quarter moving average

Figure B5. Real house prices in Sweden and abroad

Index, 1980 =100

0

50

100

150

200

250

300

350

400

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 100

50

100

150

200

250

300

350

400Denmark

Norway

Spain

Sweden

United Kingdom

USA

Source: Reuters EcoWinNote. Single-family dwelling prices deflated using consumer price index.

Figure B6. Households' new loans broken down into different maturities

Per cent

0%

20%

40%

60%

80%

100%

96 97 98 99 00 01 02 03 04 05 06 07 08 09

Variable rate Fixed rate < 5 years Fixed rate > 5 years

Source: The Riksbank

Table A1. Repo rate forecastPer cent, quarterly average values

Q2 2009 Q3 2009 Q4 2009 Q4 2010 Q4 2011 Q4 2012

Repo rate 0.6 0.3 (0.3) 0.3 (0.3) 0.4 (0.4) 2.4 (2.4) 4.1

Source: The Riksbank

Table A2. Inflation, annual average

Annual percentage change

2008 2009 2010 2011 2012

CPI 3.4 -0.4 (-0.3) 0.9 (1.2) 3.3 (3.3) 3.7

CPIF 2.7 1.8 (1.9) 1.3 (1.6) 1.9 (1.9) 2.1

CPIF excl. energy 2.0 2.3 (2.3) 1.6 (1.8) 1.7 (1.9) 2.0

HICP 3.3 1.8 (1.9) 1.2 (1.6) 1.8 (1.9) 2.0

Sources: Statistics Sweden and the Riksbank

Table A3. Inflation, 12-month average

Annual percentage change

Dec -08 Dec -09 Dec -10 Dec-11 Dec-12

CPI 0.9 0.4 (0.6) 1.9 (2.0) 4.0 (4.2) 3.3 CPIF 1.6 2.1 (2.3) 1.6 (1.8) 2.0 (2.1) 2.2

CPIF excl. energy 1.7 2.2 (2.2) 1.5 (1.8) 1.8 (2.0) 2.1

HICP 2.1 2.2 (2.5) 1.5 (1.7) 1.9 (2.0) 2.1

Sources: Statistics Sweden and the Riksbank

Table A4. Summary of financial forecasts

Annual average, per cent, unless otherwise specified

2008 2009 2010 2011 2012

Repo rate 4.1 0.7 (0.7) 0.3 (0.3) 1.6 (1.6) 3.6

10-year rate 3.9 3.3 (3.3) 3.9 (3.9) 4.5 (4.5) 4.9 Exchange rate, TCW-index, 1992-11-18=100

127.2 139.7 (139.5)

129.6 (130.9)

128.3 (129.5)

128.2

General government net lending* 2.5 -2.2 (-2.5) -2.5 (-3.5) -1.0 (-2.1) 0.2

Sources: Statistics Sweden and the Riksbank

Table A5. International conditionsAnnual percentage change, unless otherwise specified

GDP 2008 2009 2010 2011 2012

Euro area 0.6 -4.0 (-4.1) 1.0 (0.7) 1.7 (1.7) 2.3 USA 0.4 -2.6 (-2.9) 2.4 (1.5) 3.3 (3.3) 2.9

Japan -0.7 -5.9 (-5.9) 1.2 (1.2) 2.0 (2.0) 1.8

OECD 0.6 -3.6 (-3.7) 1.8 (1.3) 2.6 (2.7) 2.7

TCW-weighted 0.5 -3.8 (-4.0) 1.1 (0.8) 2.0 (2.0) 2.3

World 3.2 -1.0 (-1.1) 3.3 (2.8) 4.2 (3.9) 4.4

2008 2009 2010 2011 2012

Crude oil price, USD/barrel Brent 97 60 (62) 74 (78) 78 (81) 80 Swedish export market growth 0.5 -9.2 (-10.7) 5.7 (3.2) 7.8 (7.5) 8.3

Sources: Eurostat, IMF, Intercontinental Exchange, OECD and the Riksbank

CPI 2008 2009 2010 2011 2012

Euro area (HICP) 3.3 0.4 (0.4) 1.2 (1.2) 1.7 (1.7) 2.0 USA 3.8 -0.5 (-0.5) 1.8 (1.8) 2.0 (2.0) 2.1 Japan 1.4 -1.3 (-1.2) -0.7 (-0.6) 0.5 (0.5) 0.5 OECD 3.6 0.5 (0.5) 1.6 (1.7) 2.0 (1.9) 2.1

TCW-weighted 3.3 0.5 (0.5) 1.3 (1.3) 1.7 (1.7) 2.0

Table A6. GDP by expenditureAnnual percentage change, unless

otherwise specified

2008 2009 2010 2011 2012

Private consumption -0.2 -0.7 (-1.1) 2.0 (1.8) 2.1 (2.0) 2.2 Public consumption 1.5 1.5 (1.1) 0.6 (0.6) 0.6 (0.6) 1.1 Gross fixed capital formation 2.7 -17.3 (-17.1) -1.8 (-5.7) 5.7 (5.4) 6.9 Inventory investment* -0.6 -1.4 (-0.9) 1.1 (0.5) 0.2 (0.2) 0.1 Exports 1.8 -12.8 (-14.7) 4.6 (4.2) 7.3 (7.0) 8.2 Imports 3.0 -15.0 (-16.1) 4.1 (1.9) 6.2 (6.0) 7.4 GDP -0.2 -4.6 (-4.9) 2.5 (1.9) 3.4 (3.2) 3.7 GDP, calendar-adjusted -0.4 -4.4 (-4.7) 2.2 (1.6) 3.4 (3.2) 3.7 Final figure for domestic demand* 0.8 -3.3 (-3.5) 0.9 (0.1) 2.1 (2.0) 2.5 Net exports* -0.4 0.1 (-0.4) 0.6 (1.3) 1.1 (1.0) 1.1 Current account (NA)** 6.1 7.6 (7.2) 7.7 (8.1) 8.3 (8.6) 8.7

Sources: Statistics Sweden and the Riksbank

Table A7. Production and employmentAnnual percentage change, unless otherwise stated

2008 2009 2010 2011 2012

Population, aged 16-64 0.8 0.6 (0.6) 0.3 (0.3) 0.2 (0.2) -0.1 GDP, calendar-adjusted -0.4 -4.4 (-4.7) 2.2 (1.6) 3.4 (3.2) 3.7 Number of hours worked, calendar-adjusted 0.9 -3.0 (-3.2) -1.7 (-2.0) 0.6 (0.5) 1.3 Employed (EU-definition) 1.2 -2.4 (-2.4) -2.6 (-2.9) -0.1 (-0.3) 1.2 Labour force (EU-definition) 1.3 0.0 (0.1) -0.6 (-0.6) -0.2 (-0.3) 0.3 Unemployment, aged 15-74 (EU-definition) * 6.2 8.5 (8.6) 10.3 (10.8) 10.3 (10.7) 9.4

Sources: Employment Service, Statistics Sweden and the Riksbank

Table A8. Wages and unit labour cost for the economy as a wholeAnnual percentage change, calendar-adjusted data

2008 2009 2010 2011 2012

Hourly wage, NMO 4.3 3.4 (3.3) 2.2 (2.2) 2.4 (2.4) 2.9 Hourly wage, NA 4.8 3.8 (3.5) 2.1 (2.1) 2.6 (2.6) 3.2 Employer’s contribution* -0.7 -0.5 (-0.4) 0.1 (0.1) 0.1 (0.1) 0.1 Hourly labour cost, NA 4.1 3.3 (3.2) 2.2 (2.2) 2.6 (2.7) 3.2

Productivity -1.3 -1.4 (-1.6) 4.0 (3.7) 2.8 (2.6) 2.3 Unit labour cost 5.5 4.8 (4.8) -1.7 (-1.5) -0.1 (0.0) 0.9

Sources: National Mediation Office, Statistics Sweden and the Riksbank

Table A9. Higher level of international growthAnnual percentage change, unless otherwise specified

2008 2009 2010 2011 2012

TCW- weighted GDP 0.5 -3.8 (-3.8) 2.1 (1.1) 2.5 (2.0) 1.9 (2.3) TCW- weighted CPI 3.3 0.5 (0.5) 1.5 (1.3) 2.1 (1.7) 2.3 (2.0)

TCW-weighted interest rate, per cent 3.8 1.0 (1.0) 1.3 (1.0) 3.2 (2.6) 4.6 (3.9) GDP, calendar adjusted -0.4 -4.4 (-4.4) 2.5 (2.2) 3.4 (3.4) 3.5 (3.7)

CPIF 2.7 1.9 (1.8) 1.7 (1.3) 2.4 (1.9) 2.1 (2.1)

Labour market gap, per cent 3.2 -0.1 (-0.1) -1.8 (-2.1) -1.4 (-1.8) -0.8 (-1.0)

Repo rate, per cent 4.1 0.7 (0.7) 0.7 (0.3) 2.6 (1.6) 4.4 (3.6)

Sources: National Sources Office, Statistics Sweden and the Riksbank

Table A10. Scenario with increased labour productivityAnnual percentage change, unless otherwise specified

2008 2009 2010 2011 2012 GDP, calendar adjusted -0.4 -4.4 (-4.4) 2.7 (2.2) 4.0 (3.4) 4.1 (3.7)

CPIF 2.7 1.8 (1.8) 1.1 (1.3) 1.8 (1.9) 2.0 (2.1)

Labour market gap, per cent 3.2 -0.1 (-0.1) -2.5 (-2.1) -1.9 (-1.8) -1.0 (-1.0)

Productivity -1.3 -1.4 (-1.4) 4.9 (3.9) 3.1 (2.8) 2.6 (2.3)

Repo rate, per cent 4.1 0.7 (0.7) 0.0 (0.3) 1.2 (1.6) 3.3 (3.6)

Sources: Statistics Sweden and the Riksbank

Table A11. Scenario with higher repo rate Annual percentage change, unless otherwise specified

2008 2009 2010 2011 2012 GDP, calendar adjusted -0.4 -4.4 (-4.4) 2.0 (2.2) 2.8 (3.4) 4.1 (3.7) CPIF 2.7 1.8 (1.8) 1.1 (1.3) 0.9 (1.9) 1.5 (2.1)

Labour market gap, per cent 3.2 -0.1 (-0.1) -2.3 (-2.1) -2.7 (-1.8) -1.4 (-1.0)

Repo rate, per cent 4.1 0.7 (0.7) 0.8 (0.3) 2.2 (1.6) 3.1 (3.6)

Sources: Statistics Sweden and the Riksbank

Table A12. Scenario with lower repo rate Annual percentage change, unless otherwise specified

Sources: Statistics Sweden and the Riksbank

2008 2009 2010 2011 2012 GDP, calendar adjusted -0.4 -4.4 (-4.4) 2.4 (2.2) 3.3 (3.4) 3.7 (3.7) CPIF 2.7 1.9 (1.8) 1.5 (1.3) 2.1 (1.9) 2.1 (2.1)

Labour market gap, per cent 3.2 -0.1 (-0.1) -1.9 (-2.1) -1.7 (-1.8) -1.0 (-1.0)

Repo rate, per cent 4.1 0.6 (0.7) 0.1 (0.3) 1.6 (1.6) 3.6 (3.6)

![Cecilia Skingsley: Should the Riksbank issue e-krona? · 1 [10] Should the Riksbank issue e-krona?1 Should the Riksbank issue electronic means of payment in the same way as we now](https://static.fdocuments.us/doc/165x107/5ec82f088662860afc5de461/cecilia-skingsley-should-the-riksbank-issue-e-krona-1-10-should-the-riksbank.jpg)