RBEs and MPCs in MSC.Nastran A Rip-Roarin’ Review of Rigid Elements.

Upload

sirene-sarminiCategory

view

12download

1

MGT 6263

MANAGEMENT POLICY AND CORPORATE

STRATEGY

STRATEGY CASE

Presented by:

Lujja Sulaiman G1217141

Sirin Alsarmini G1224192

Muhammad Afiq bin Mohd Nordin

G1212639

Nuzaihan bin Majidi G1214123

Habib M.A. Abuomer G1214733

PRESENTATION OUTLINE

1. Introduction

2. External Analysis

3. Internal Analysis

4. Identification of Strategies

5. Problems and Challenges

6. Implementation Issues

7. Recommendations

8. Conclusion

INTRODUCTION

The History of Palm Oil Industry in Malaysia

• Palm plant has been grown for over 1000 years in West Africa.

• In 1917 the crop was introduced into Malaysia by the British colonial rulers.

• Oil palm is one of the main drivers of Malaysia’s agriculture sector (71% of national agricultural land bank).

1885

• UP founder Mr. Aage Westenholz, served in the Danish Army as an Artillery Officer living in Bangkok and formed Siam Electric Co.

1906

• Mr. Westenholz established Jendarata Rubber Estate of 809 hectares followed by Corner, Raja Una and Westenholz Brothers Coconut Estates in Selangor.

1911

• Mr. Westenholz retired and was succeeded by his younger cousin, Commander William Lennart Grut,

1917

• all the above companies were merged to become United Plantations Limited.

1918

• Commander Grut acquired 2,428 hectares above Bernam River, and established Bernam Oil Palms, one of the pioneers of the Malaysian Palm Oil Industry.

The History of United Plantations

1932

• Bernam Oil Palms got listed on the Copenhagen Stock.

1966

• the two companies, United Plantations Ltd. and Bernam Oil Palms Ltd. were incorporated into United Plantations Berhad.

1969

• United Plantations Berhad got listed on the Kuala Lumpur Stock Exchange.

2004

• UP acquired Socfin’s Lima Blas Estate (totaled land bulk of 40,874 hectares).

2006

• UP acquired 2 Indonesian plantation companies, i.e., PT. Surya Sawit Sejati and PT. Mirza Pratama Putra - 40,000 hectares of plantation land in Indonesia.

The History of United Plantations

United Plantations’ Group Philosophy

“We strive towards being recognized as second to none within the plantation industry, producing high quality products, always focusing

on the sustainability of our practices and our employees’ welfare whilst attaining acceptable returns for our shareholders.”

BUSINESS MODEL

Company primary business is cultivation of oil palm and other plantation crops and their processing.

How UP generates income?

• Production and sell of semi-finished goods e.g. CPO.• Research and Development - high yielding palm products.• Derivatives trading e.g. CPO futures - hedge against

losses.• Effectiveness and efficiency company - best quality

product - premium price.

PRODUCTS OF UNITED PLANTATIONS

• Plantation– Crude Palm Oil (CPO)– Crude Palm Kernel Oil (CPKO)

• Refinery– Cocoa Butter Substitute– Palm Acid Oil– Biomass/Biodiesel

• Manufacturing– Margarine– Cooking Oil

EXTERNAL ANALYSIS

PESTEL ANALYSIS• ETP: 8 EPP to sustain Malaysian Palm Oil Industry• Palm Oil Industrial Cluster in ECERPolitical

• Global demand for oils and fat increased by an average of 7% from 2000 till 2010. Palm oil increased by 10%

• FTA’s : Negotiations for TTP/ India-Malaysia FTA in 2011Economic/Global

• Awareness about the benefits of palm oil is increasing• Malaysian population base is small- fertility rate is -2.2 POI is

export oriented • Government is building Iskandar Malaysia with a planned

population of 3mn

Socio-cultural

• Malaysia is recognized world wide for its R&D activities • Patent laws are set by the MPOB; however, there’s a need for

stricter enforcement of intellectual property rights.Technological

• Deforestation, pollution, threat of habitat to indigenous groups and some animals

• RSPO: Roundtable on Sustainable Palm Oil (only oil with sustainable certification)

• MSPO: Malaysian Sustainable Palm Oil certification expected in 2014

Environmental

• Well regulated by Malaysian Palm Oil Board• MPOB serves as technical advisory and research institutions• Tax incentives, strict labor law for foreign workers

Legal & Regulatory

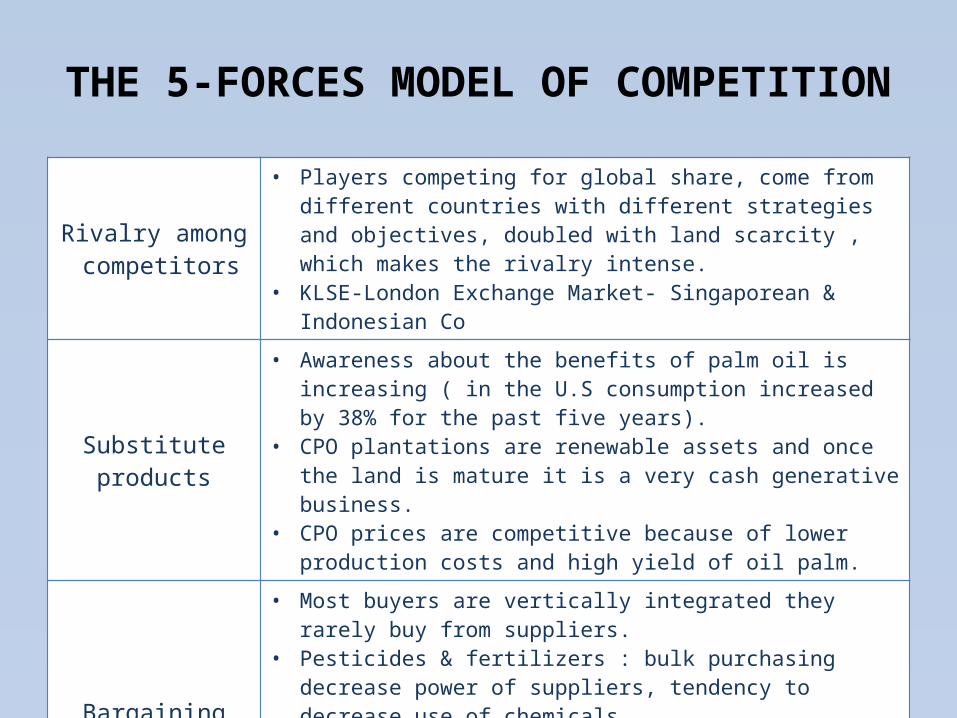

THE 5-FORCES MODEL OF COMPETITION

Rivalry among competitors

• Players competing for global share, come from different countries with different strategies and objectives, doubled with land scarcity , which makes the rivalry intense.

• KLSE-London Exchange Market- Singaporean & Indonesian Co

Substitute products

• Awareness about the benefits of palm oil is increasing ( in the U.S consumption increased by 38% for the past five years).

• CPO plantations are renewable assets and once the land is mature it is a very cash generative business.

• CPO prices are competitive because of lower production costs and high yield of oil palm.

Bargaining power of suppliers

• Most buyers are vertically integrated they rarely buy from suppliers.

• Pesticides & fertilizers : bulk purchasing decrease power of suppliers, tendency to decrease use of chemicals.

• Engineering companies: their numbers is larger than plantations, some plantations have their own Eng. Co.

• Funding is easy: many banks would offer loans (strong banking system), this industry is less risky than others and profitable.

THE 5-FORCES MODEL OF COMPETITION

Bargaining power of buyers

• Five main countries buys in trillion tons annually thus they can exert bargaining power over plantations; however, demand is on the rise, while supply is restricted which moderates the power of buyers.

• Indonesia offers more competitive CPO prices.

Threat of new entrants

• Scarcity of land. • Palm oil is capital intensive and takes long time to achieve

economies of scale• Vertical integration of the major players is a major hurdle.• Technological and managerial expertise are not easy to be

obtained and takes long time to accumulate.

THE 5-FORCES MODEL OF COMPETITION

Rivalry among

CompetitorsHigh

Bargaining Power of suppliers

Low

Threat of entryLow

Threat of substitute ProductsModerateBargaining

Power of BuyersModerate

DRIVERS OF CHANGE

Industry's long- term

growth

Cost Efficiencies, increases in productivity

Product& Marketing innovation

Technological change &

manufacturing change process

Regulatory influences & government

policy changes Attractive industry

STRATEGIC GROUP MAPPINGIt is important to understand the complexity of this industry, many

ramifications are present through the manufacturing process, it starts from preparing the land and nursing the seedlings, and then

harvesting the FFB, and it goes up until the production of palm kernel

Mature harvested Area

FFBHow many

fruit bunches

you can get from a tree

FFB yieldHow much

oil you can get from a bunch

CPO Producti

onFrom pulp of the fruit

Palm Kernel

Production

From nut of the fruit

Extracted Value

STRATEGIC GROUP MAPPINGQ

ual

ity/

Pri

ce

EV/Ha

HIGHMEDIUMLOW

HIG

HM

ED

IUM

LO

W

Legend: Malaysia- Singapore- Indonesia

Sime Darby

35 EV/ha

p

kLk

G Wilmar127 EV/ha

IOIIndo10

Ev/ha

FGV A

Strategic Group Mapping

INTERNAL ANALYSIS

FINANCIAL RATIOS ANALYSIS

PROFITABILITY

2005 2006 2007 2008 2009 2010 2011 2012Operating Margin 29.4349 31.8729 33.5052 39.3375 40.7536 35.0878 33.7837 38.4551Profit Margin 22.3832 25.1075 26.6097 29.0573 34.466 27.2717 26.7416 28.9204Return on assets 11.508 12.4816 13.8776 19.9202 16.1671 13.7547 17.78 14.9724Return on Equity 14.2387 14.632 15.8161 22.7848 18.3304 15.5009 19.8464 16.505

LIQUIDITY

2005 2006 2007 2008 2009 2010 2011 2012Cash ratio 1.35 1.90 0.09 0.08 3.30 3.19 5.08 6.10Quick ratio 1.56 2.45 0.54 0.49 3.48 3.44 5.73 6.79Current Ratio 2.32 3.71 3.83 4.17 4.83 4.67 7.68 8.40

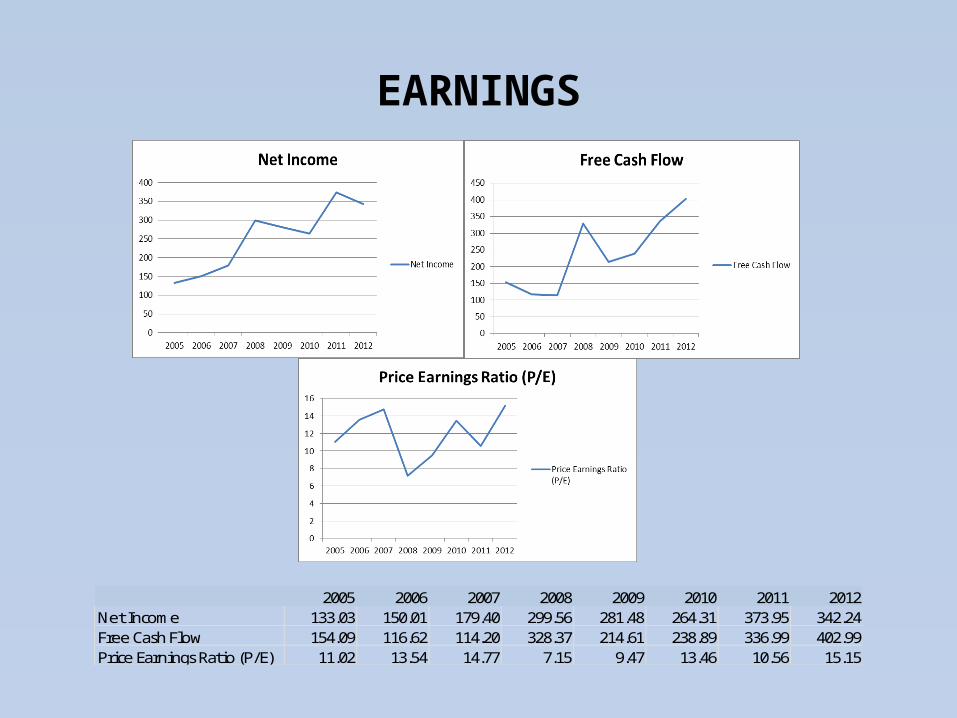

EARNINGS

2005 2006 2007 2008 2009 2010 2011 2012Net Income 133.03 150.01 179.40 299.56 281.48 264.31 373.95 342.24Free Cash Flow 154.09 116.62 114.20 328.37 214.61 238.89 336.99 402.99Price Earnings Ratio (P/E) 11.02 13.54 14.77 7.15 9.47 13.46 10.56 15.15

ACTIVITY

2005 2006 2007 2008 2009 2010 2011 2012Inv Raw Materials 0.70 0.38 6.77 5.79 7.85 6.50 5.44 23.73Inventory Finished Goods 61.43 50.92 84.67 85.95 89.64 95.66 134.99 114.29Inventory to Sales 14.36 14.06 17.51 13.53 16.55 14.47 12.95 15.10

SWOT ANALYSIS

Strengths Higher Quality Production Cost efficiency Big emphasis on TQM, JIT Good Corporate Social

Responsibility

Weaknesses Difficulty obtaining skilled Sales

and Marketing Professionals Inability to create better Sales

and Marketing Opportunities in Malaysia

Small amounts of plantable land

Opportunities Availability of land in Indonesia

and Africa Market expansion to new

markets due to TPPA Higher acceptance due to health

concerns

Threats Environmental issues and Smear

campaigns Climate change and natural disasters

VALUE-CHAIN ANALYSIS

KEY SUCCESS FACTORS & COMPETITIVE STRENGTH ASSESSMENT

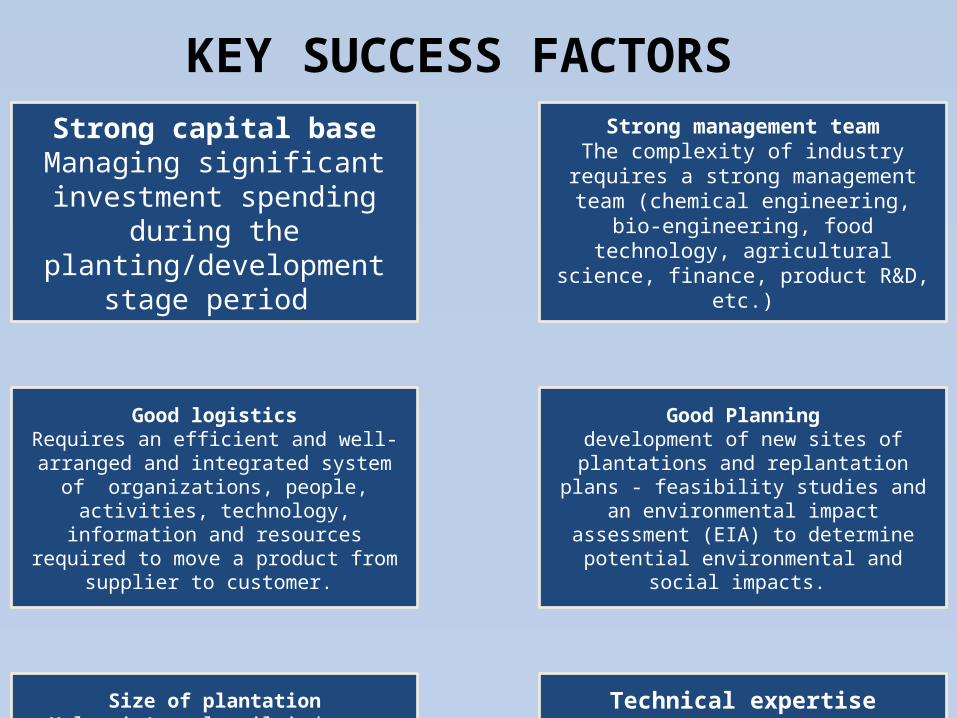

KEY SUCCESS FACTORS

Strong capital baseManaging significant

investment spending during the planting/development

stage period

Strong management teamThe complexity of industry requires

a strong management team (chemical engineering, bio-

engineering, food technology, agricultural science, finance,

product R&D, etc.)

Good logisticsRequires an efficient and well-

arranged and integrated system of organizations, people, activities,

technology, information and resources required to move a

product from supplier to customer.

Good Planningdevelopment of new sites of

plantations and replantation plans - feasibility studies and an

environmental impact assessment (EIA) to determine potential

environmental and social impacts.

Size of plantationMalaysia’s palm oil industry faces

a major threat of limitation of cultivable lands due to concerns of deforestation and environmental

degradation. - expanding in Indonesia and Africa.

Technical expertiseRequire a strong expertise in the technical know-how in the food and health segment - Upstream products comprise 81.5% of the

total palm oil exports.

COMPETITIVE STRENGTH ASSESSMENT

KSF WeightsUnited

PlantationsGenting

PlantationsSime Darby

Plantation Size 0.30 5 1.50 5 1.50 9 2.70Good Planning 0.20 7 1.40 6 1.20 7 1.40Good Logistics 0.18 8 1.44 6 1.08 7 1.26Capital Base 0.15 5 0.75 6 0.90 8 1.20

Strong Management

team0.10 6 0.60 6 0.60 8 0.80

Technical expertise

0.07 6 0.42 7 0.49 8 0.56

1.00 6.11 5.77 7.921 = very weak; 5 = average; 10 = very strong • United Plantation is in the middle not enjoying a competitive advantage

and not suffering the competitive disadvantage.• United Plantation is competitive in 1) Good Logistics 2) Good Planning • However, UP has to improve on these areas; 1) Plantation size, by

acquiring more land for expansion in Indonesia and Africa, 2) Capital base, by raising more funds through selling more shares and bonds.

IDENTIFICATION OF STRATEGIES

CORPORATE-LEVEL STRATEGIES

Related Diversification

Vertical Integration Acquisition Strategic Alliance

• Unitata Berhad – Palm-oil refinery• PT Surya Sawit Sejati & PT Surya Sawit Seberang (Indonesia) – Oil-palm plantation• Butterworth Bulking Installation Sdn. Bhd. – Oil-palm collection and transportation• Bernam Agencies Sdn. Bhd. – Sales and marketing• Aarhuskarlshamn – Sales and distribution in Europe

Oil-palm plantation Palm-oil refineryManufacturing of palm-oil based products

BUSINESS-LEVEL STRATEGIES

Broad Differentiation Strategy

UP’s Quality Philosophy:

To uphold the name and reputation of United Plantations as a top producer of premium quality palm products.

Product features and performance

Input quality

Quality control process

Customer service

Production R&D

Technology and innovation

Employee training, skill and experience

Sales & marketing

FUNCTIONAL-LEVEL STRATEGIES

R&D and Technology Production

OPERATIONAL-LEVEL STRATEGIES• Managers at the operational-level are required to engage in all aspects of

operation• Operational activities are conducted in one integrated place in Jenderata

Estate, Perak

• PROBLEM AND CHALLENGES• IMPLEMENTATION ISSUES• RECOMMENDATIONS• CONCLUSION

PROBLEM AND CHALLENGES

1) Issues concerning labor:

a. High turnover rate

b. Disciplinary issues for foreign workforce

c. Hiring talented workers

PROBLEM AND CHALLENGES

2) Issues concerning land:

a. Availability

b. Type/Quality

c. Irrigation

d. Transportation

IMPLEMENTATION ISSUES

• In solving the shortage of sales and marketing professionals.

• Other processes are better than competitors.

RECOMMENDATIONS

1. Hire talented sales and marketing

professionals.

2. Extend business operations to potential

new markets (e.g. Africa and the Middle East).

3. Acquire more of the plantable lands.

4. Seek more stable workforce.

5. Improve their R&D activities.

CONCLUSION

• Is UP’s strategy a Winning Strategy ?!– Fit test

(In Harmony with External Environment, Good management of Resources)– Competitive Advantage test

(distinctive quality, excellent at TQM & JIT)– Performance test

(financial strength / competitive strength and market standing)

THANK YOUQUESTIONS, COMMENTS & FEEDBACK

ARE MOST WELCOME

![Optical and Electrical Properties of TTF-MPcs€¦ · Optical and Electrical Properties of TTF-MPcs ... well as for organic solar cells (OSC) [2]. ... in many applications, such as](https://static.fdocuments.us/doc/165x107/5f0859bd7e708231d421939c/optical-and-electrical-properties-of-ttf-mpcs-optical-and-electrical-properties.jpg)