Moving from R&D to Operations Chapter 11. Where we are Idea to Opportunity Assessing Technical And...

24

Moving from R&D to Operations Chapter 11

-

Upload

coleen-hubbard -

Category

Documents

-

view

213 -

download

0

Transcript of Moving from R&D to Operations Chapter 11. Where we are Idea to Opportunity Assessing Technical And...

Moving from R&D to Operations

Chapter 11

Where we are

Idea to Opportunity

Idea to Opportunity

Assessing TechnicalAnd Market Risks

Assessing TechnicalAnd Market Risks

Initial Proof Of Concept

Initial Proof Of Concept

Designing IP Strategy

Designing IP Strategy

Developing Business Model

Developing Business Model

Final FeasibilityAssessment

Final FeasibilityAssessment

Business PlanDevelopment& Resource Gathering

Business PlanDevelopment& Resource Gathering

License

Launch

TransitionTo

Operations

Transition Challenges

Technical specifications that don’t fit

Market expectations don’t match reality

Determination of first application is hard

First app versus killer app

Technical and process uncertainty

Initial assumptions about the market generally prove false

What Makes a Successful Transition?

People from the innovation team

People from the operations team

Transition management experts

A mission

Develop a Mission Statement

Contribution to

Performance

Contribution to

Performance

Components of the Mission

Statement

Components of the Mission

Statement

Phrasing of the Mission Statement

Phrasing of the Mission Statement

Communication to

Stakeholders

Communication to

Stakeholders

Construct a Process Flow Chart

Take a fantasy tour of the business to see how it works

Track an order

Note tasks, people, equipment

Gather Resource Pieces

Financial Capital

Cash needs assessment

Human Capital

Process flow chart and Founding Team

Assessment

Physical Capital

Process flow chart of business

Resources have Significant Implications for Survival and Growth

Bundles of resources create competitive advantages

Resources that are unique, rare, and valuable create wealth

Rapidly growing entrepreneurial firms require different resources at different times

Choose an Organizational Model

Engineering model: hire for technical skills

Star model: hire for long-term potential

Bureaucracy model: formal control procedures & employees hired for specific skills

Autocracy model: employees motivated by financial rewards

Commitment model: strong emotional bonds and informal peer-group control (best predictor of an IPO – Stanford Project on Emerging Companies

Choose Legal Form of Organization

Sole proprietorshipPartnershipCorporationHybrid form

How would you decide?

Criteria for Choice

Who will be the owners?

Level of liability protection required

Operating requirements and costs

Effect on the tax strategy of the

company & the founders

When do you expect to earn a profit?

How do you want to distribute

earnings?

Effect on financing plans

Summary of Forms

Legal Form

G en era l P artn e rsh ip

S -C orp

C -C orp F u ll C orp ora te N on -P ro fit

B rid g e F orm s L L C

P artn e rsh ip L im ited P artn e rsh ip

S o le P rop rie to r

Sole Proprietorship

76% of all businesses

Flexible, easy, inexpensive

Does not exist apart from the owner so pays no tax

Salary or draw not deductible as expense

Hobby rule (3 of 5 years)

Sole Proprietorship - Disadvantages

Unlimited liability

Difficult to raise debt capital

Lacks advantage of team

Survival dependent on owner

Partnership

Association of two or more persons as a business

Doctrine of ostensible authority

Specific property rights

Share in profit/loss according to contribution

Partnership Agreement

Duties and responsibilities

Profit/loss distribution

Transfer of interest

Duration and dissolution

Arbitration and dispute resolution

Type of partnership

general v. limited

secret, silent, dormant

C-Corporation

Legal entity

Survival of death and separation

Limited liability of shareholders

Issue different classes of stock

Raise capital by selling stock

More status

Benefit from retirement funds, profit sharing, stock options

Owners can lease their assets to the corporation

Disadvantages of Corporation

Complex and costs more

Stockholders do not have benefit of writing off losses

Double taxation (earnings and dividends)

Pay taxes on profits whether or not distributed as dividends

Accountable to board of directors

S-Corporation

Not a tax-paying entity

Owners taxed on corporate earnings

Deduct losses on personal income tax up to amount invested

No more than 75 stockholders, US citizens or legal residents

One class of stock

Disadvantages of S-Corp

Difficult to get loans if distributes earnings

No deductions based on medical reimbursements or health insurance plans

If not a cash business, may not be able to pay taxes out of business.

Must convert to C for IPO

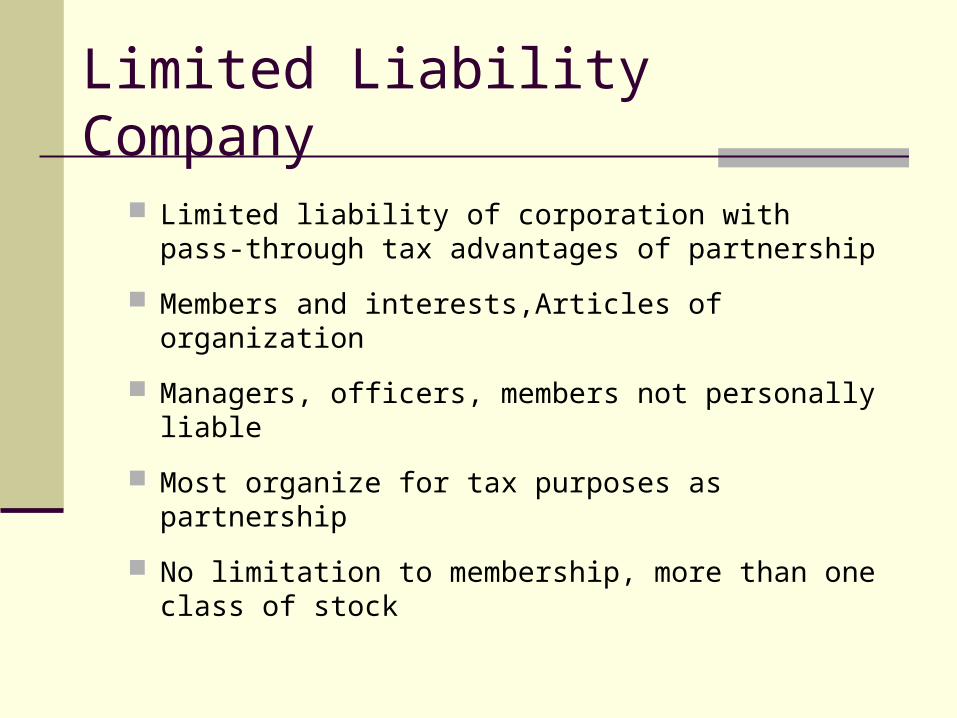

Limited Liability Company

Limited liability of corporation with pass-through tax advantages of partnership

Members and interests,Articles of organization

Managers, officers, members not personally liable

Most organize for tax purposes as partnership

No limitation to membership, more than one class of stock

Non-Profit

Established for charitable, public benefit, religious or mutual benefit

IRS 501(c)3 tax exempt

Limited liability

Owners give up proprietary interest

Perpetual existence

Apply for grants

Take-Aways

Add students’ comments here