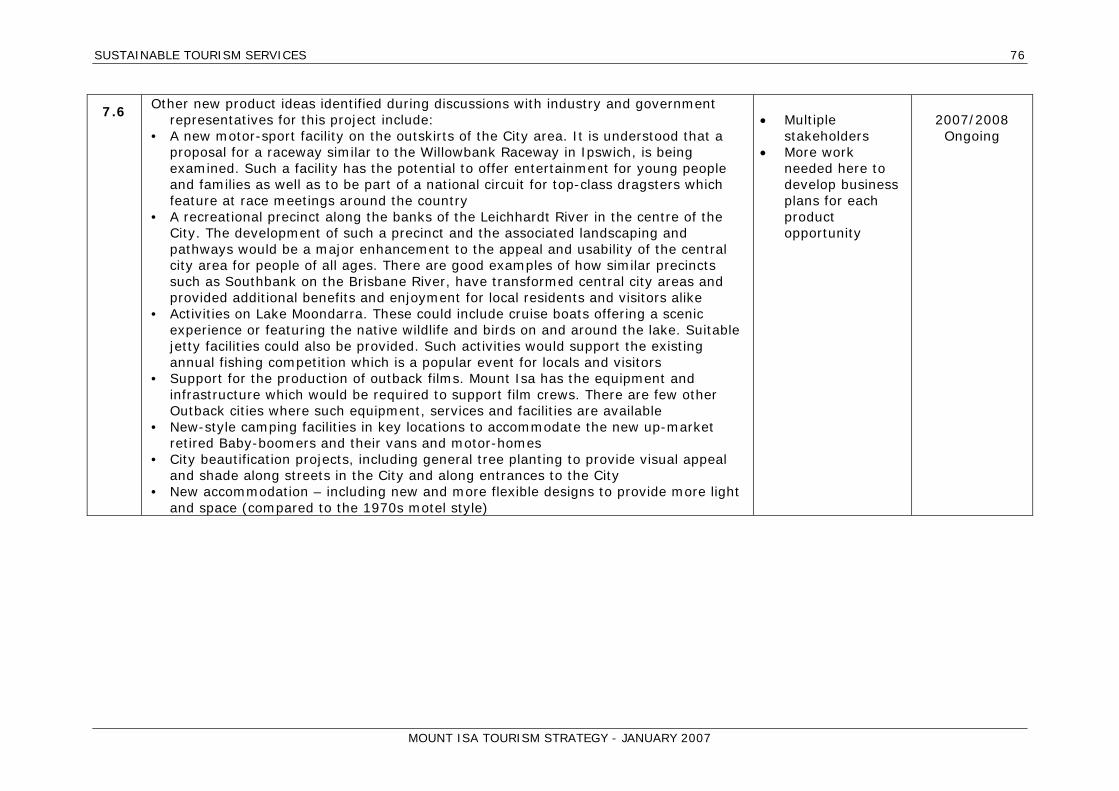

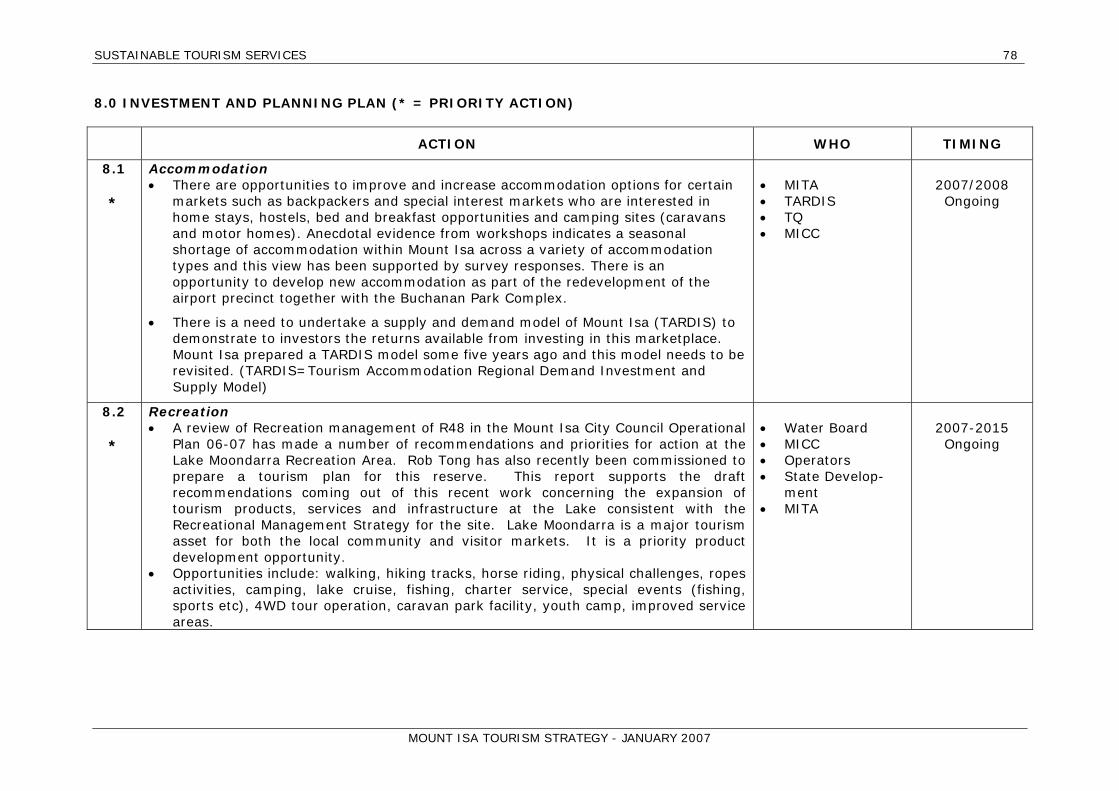

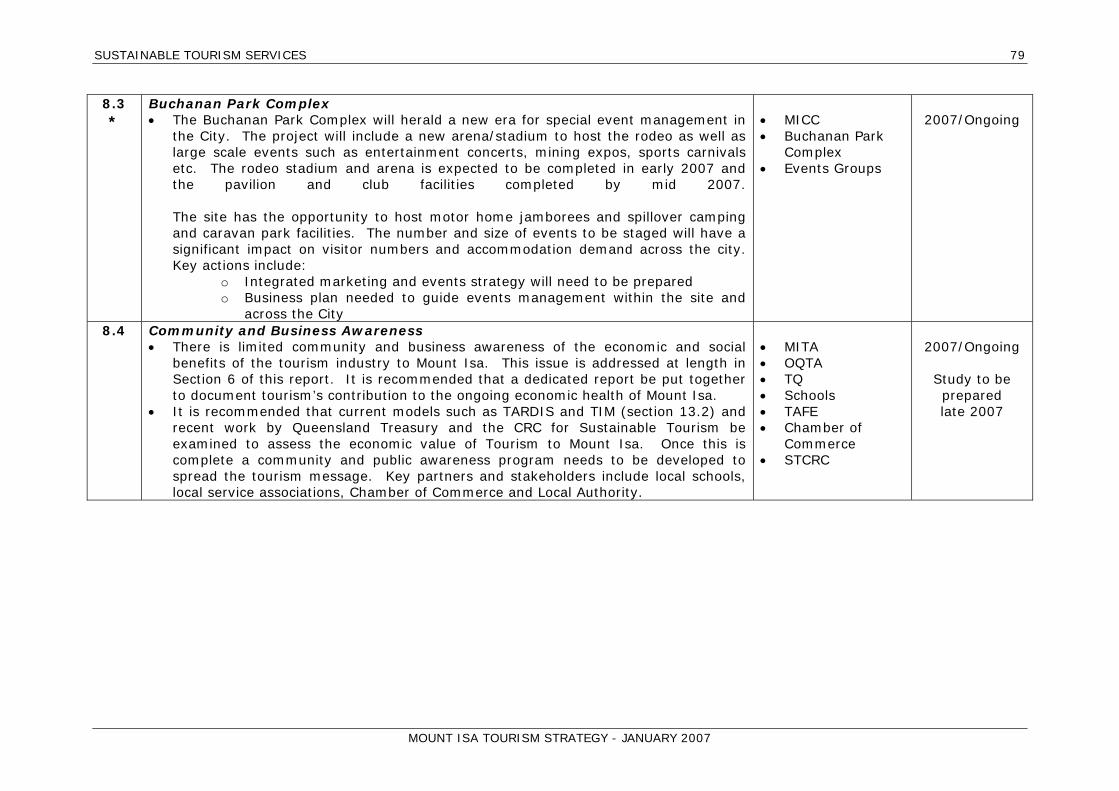

MOUNT ISA TOURISM STRATEGY 2007-2017

123

MOUNT ISA TOURISM STRATEGY - JANUARY 2007 Prepared for: Mount Isa City Council and Mount Isa Tourism Association MOUNT ISA TOURISM STRATEGY 2007-2017 Prepared by: National Centre for Studies in Travel and Tourism Pty Ltd A.C.N. 58 011 075 997 January 2007

Transcript of MOUNT ISA TOURISM STRATEGY 2007-2017

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

Prepared for: Mount Isa City Council

and Mount Isa Tourism Association

MOUNT ISA TOURISM STRATEGY

2007-2017

Prepared by: National Centre for Studies in Travel and Tourism Pty Ltd

A.C.N. 58 011 075 997

January 2007

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

ii

CONTENTS

1.0 EXECUTIVE SUMMARY .................................................................................. 1 1.1 SUMMARY OF RECOMMENDATIONS...................................................................2

2.0 BACKGROUND AND OBJECTIVES................................................................... 4 2.1 BACKGROUND................................................................................................4 2.2 OBJECTIVES ..................................................................................................4

3.0 PLANNING PROCESS..................................................................................... 7 4.0 CONTEXT ANALYSIS ..................................................................................... 8

4.1 LITERATURE SEARCH......................................................................................8 4.2 INDUSTRY MEETINGS .....................................................................................8

5.0 TOURISM OVERVIEW.................................................................................. 10 5.1 VISITOR MARKETS ....................................................................................... 10

5.1.1 Target Markets ................................................................................... 10 5.1.2 Visitor Characteristics (what do we know about these visitors?) ................. 11 5.1.3 Overall Motivations (why do they visit Mount Isa and the North West?)....... 11 5.1.4 The Journey (where do they come from and where do they go to?) ............ 12

5.2 VISITOR EXPENDITURE ................................................................................. 12 5.3 DOMESTIC VISITORS TO THE OUTBACK REGION AND MOUNT ISA ...................... 12

5.3.1 Age of Domestic Visitors ...................................................................... 14 5.3.2 Seasonality of Domestic Visitors............................................................ 14 5.3.3 Mount Isa Domestic Visitation............................................................... 15

5.4 INTERNATIONAL VISITORS TO THE OUTBACK REGION & MOUNT ISA .................. 17 5.4.1 Age of International Visitors ................................................................. 17 5.4.2 Seasonality of International Visitors....................................................... 18 5.4.3 Mount Isa International Visitation.......................................................... 18

5.5 SEASONALITY .............................................................................................. 20 5.6 CURRENT MARKET/EMERGING OPPORTUNITIES................................................ 20 5.7 VISITOR SATISFACTION................................................................................ 21

6.0 IMPORTANCE OF TOURISM TO MOUNT ISA................................................. 23 6.1 ESTIMATING TOURISM’S CONTRIBUTION TO AN ECONOMY................................ 23 6.2 TOURISM’S ECONOMIC CONTRIBUTION TO OUTBACK REGION & MOUNT ISA........ 24 6.3 ENVIRONMENTAL REVIEW ............................................................................. 26

7.0 COMMUNITY AND INDUSTRY FEEDBACK..................................................... 28 7.1 STAKEHOLDER FEEDBACK AND COMMENT ....................................................... 28 7.2 UNDERSTANDING OF TOURISM WITHIN MOUNT ISA ......................................... 29

8.0 CURRENT DELIVERY MODEL FOR MOUNT ISA TOURISM ............................. 30 8.1 OVERVIEW .................................................................................................. 30 8.2 THE ROLE OF MOUNT ISA CITY COUNCIL ......................................................... 31 8.3 THE STRUCTURE OF THE TOURISM INDUSTRY IN AUSTRALIA ............................. 31 8.4 THE CURRENT STRUCTURE OF TOURISM IN MOUNT ISA .................................... 32 8.5 TYPICAL ROLES AND RELATIONSHIPS OF A LOCAL TOURISM ORGANISATION....... 33

8.5.1 Port Douglas Daintree Tourism Association (PDDTA) ................................ 33 8.5.2 Tourism Noosa ................................................................................... 35

8.6 THE CURRENT ROLE OF MOUNT ISA TOURISM ASSOCIATION (MITA)................... 35 9.0 STRATEGIC DIRECTION AND OUTLOOK ...................................................... 36 10.0 TOURISM MARKETING AND DEVELOPMENT ................................................ 37

10.1 CONSUMER PERCEPTIONS OF MOUNT ISA ....................................................... 37

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

iii

10.2 MARKETING ACTIVITIES................................................................................ 37 10.3 ROLES AND RESPONSIBILITIES – PAST AND FUTURE ........................................ 38 10.4 EXPECTATIONS OF FUTURE GROWTH.............................................................. 39 10.5 PRODUCT DEVELOPMENT............................................................................... 40

10.5.1 Infrastructure and Attraction Projects .................................................... 41 10.5.2 Promotional Projects ........................................................................... 43 10.5.3 Product Development Projects .............................................................. 44

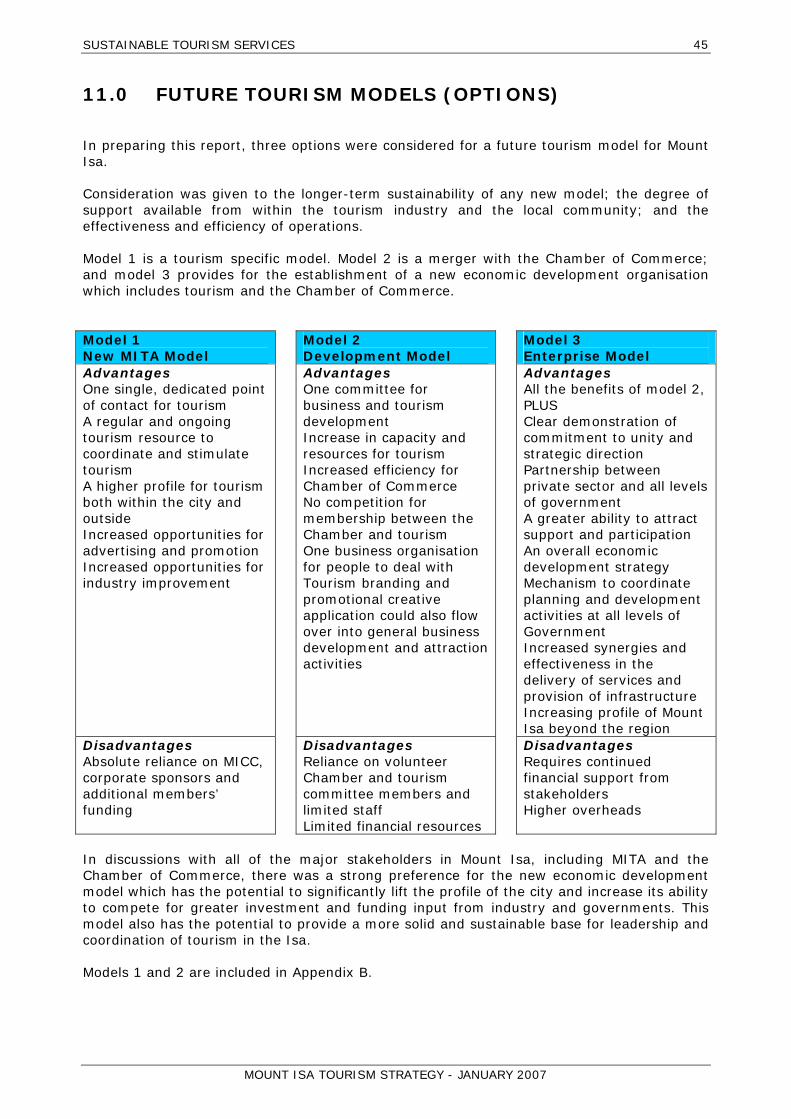

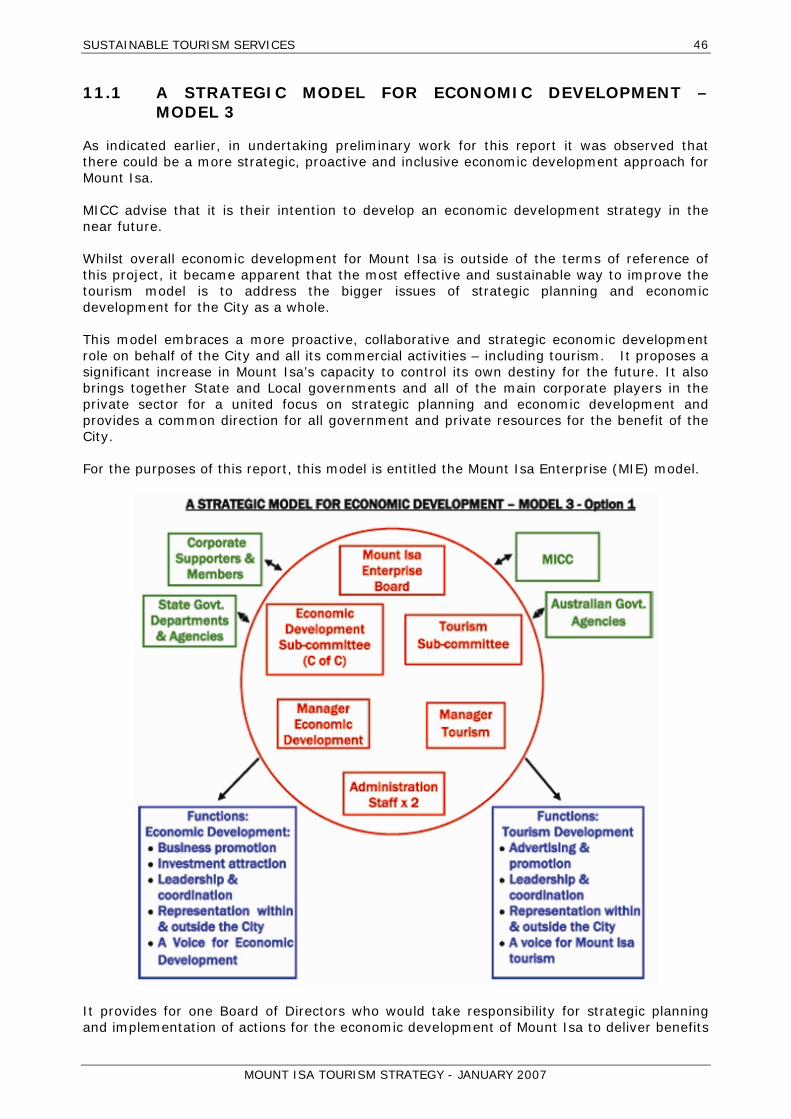

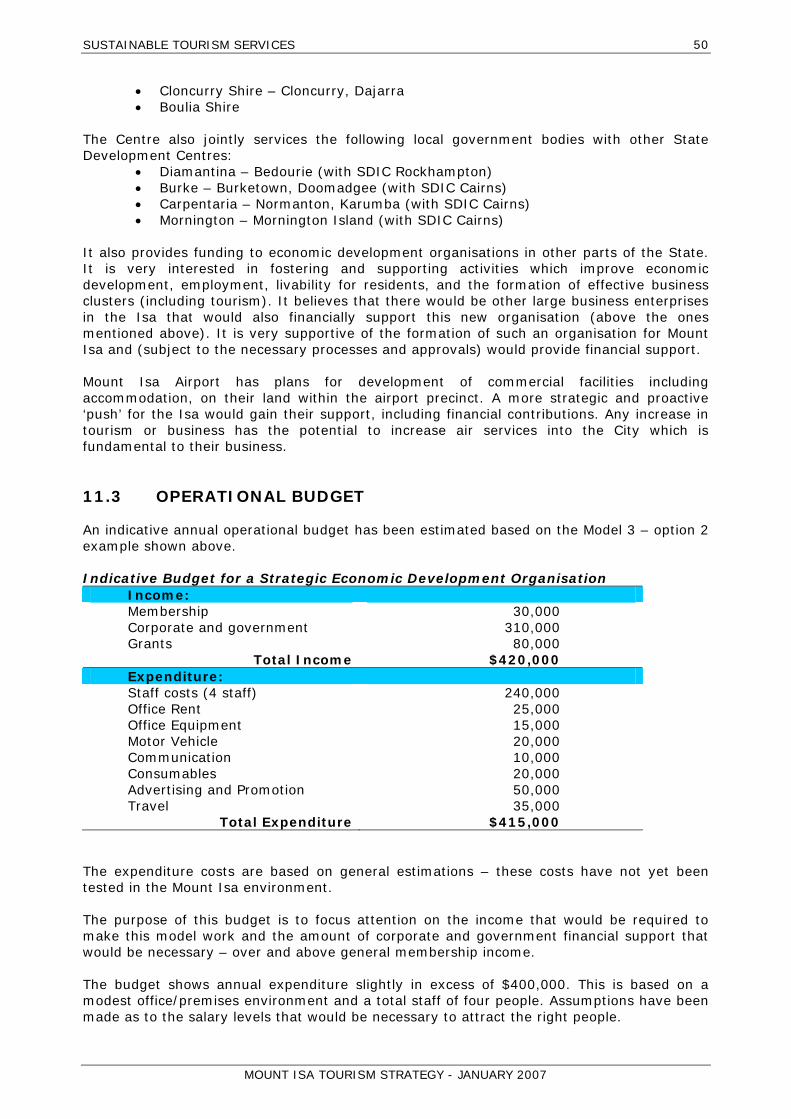

11.0 FUTURE TOURISM MODELS......................................................................... 45 11.1 A STRATEGIC MODEL FOR ECONOMIC DEVELOPMENT – MODEL 3 ....................... 46 11.2 SUPPORT FOR A STRATEGIC ECONOMIC DEVELOPMENT MODEL.......................... 49 11.3 OPERATIONAL BUDGET ................................................................................. 50 11.4 FUNCTIONS ................................................................................................. 51 11.5 ESTABLISHMENT AND OPERATIONS................................................................ 52

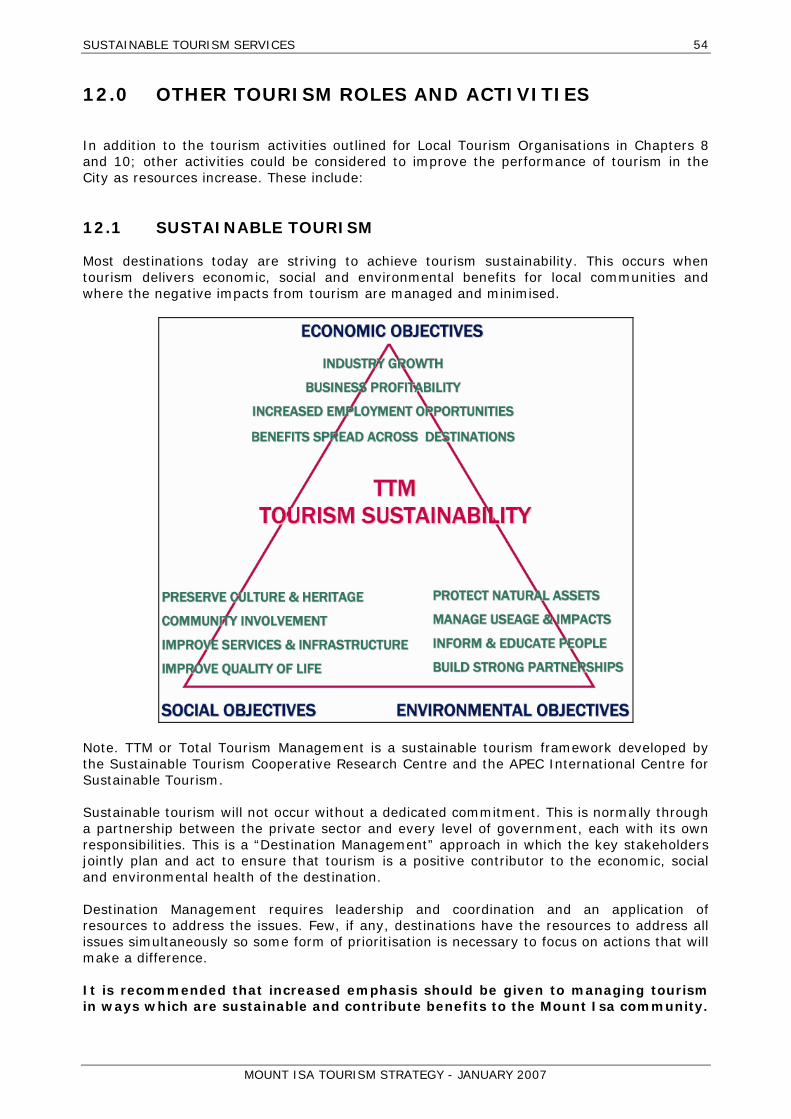

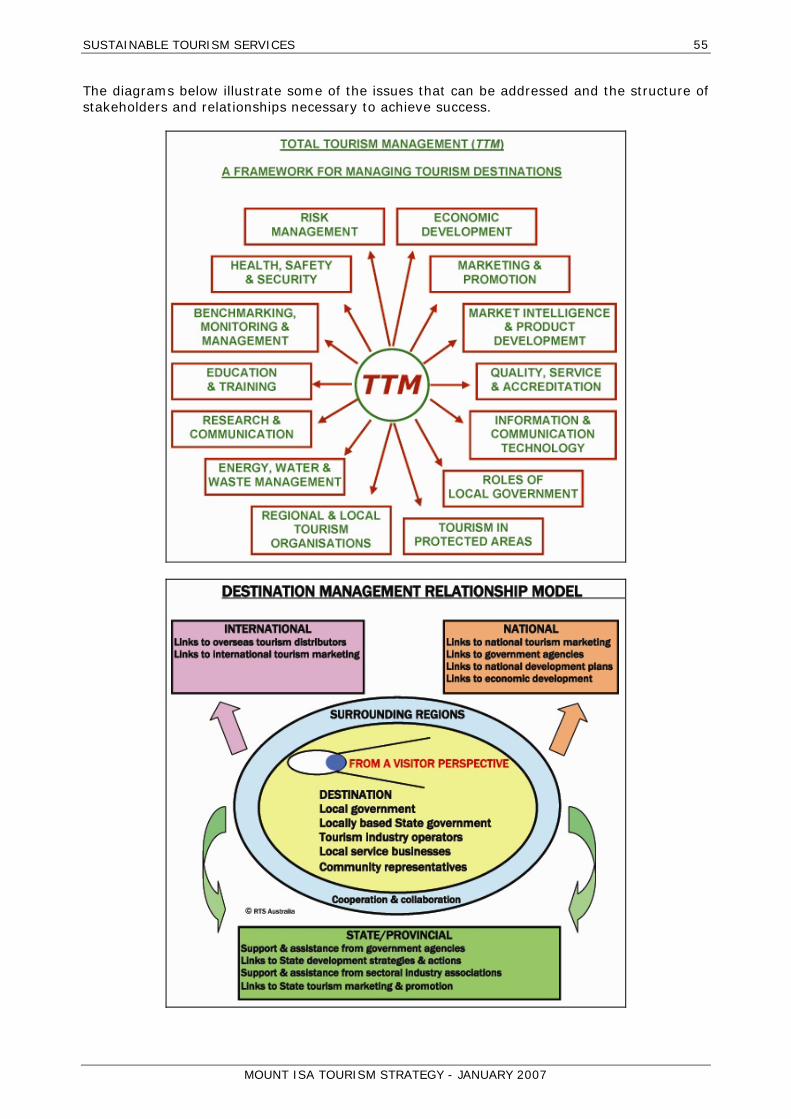

12.0 OTHER TOURISM ROLES AND ACTIVITIES .................................................. 54 12.1 SUSTAINABLE TOURISM................................................................................ 54

12.1.1 Communicating the Benefits of Tourism to Local Communities................... 56 13.0 IMPLEMENTATION OF NEW TOURISM MODEL............................................. 58

13.1 STAGE 1 – CONSULTATION............................................................................ 58 13.2 STAGE 2 – PREPARATION .............................................................................. 59 13.3 STAGE 3 – IMPLEMENTATION......................................................................... 60

14.0 SUMMARY OF RECOMMENDATIONS ............................................................ 61 APPENDIX A – TOURISM ACTION PLAN (TAP) .......................................................... 63 APPENDIX B – A NEW TOURISM MODEL (MODEL 1) AND AN AMALGAMATED MODEL FOR TOURISM & BUSINESS (MODEL 2) .................................................................... 81 APPENDIX C – FEEDBACK FROM CONSULTATION MEETINGS .................................... 85 APPENDIX D - CASE STUDIES OF SIMILAR ECONOMIC DEVELOPMENT (INCLUDING TOURISM) ORGANISATIONS IN OTHER REGIONS..................................................... 89 APPENDIX E – LIST OF EXISTING ACCOMMODATION, ATTRACTIONS AND EVENTS .. 93 APPENDIX F - THE RATIONALE FOR GOVERNMENT FUNDING OF TOURISM DESTINATION MARKETING....................................................................................... 95 APPENDIX G - CASE STUDY; LOCAL GOVERNMENT NEW ZEALAND TOURISM PARTNERSHIPS…………………………………………………………………………………97 APPENDIX H - LOCAL TOURISM FUNDING MECHANISMS.......................................... 98 APPENDIX I - CASE STUDIES FOR A DIFFERENTIAL RATE LEVY.............................. 102 APPENDIX I – SPECIAL RATES AND CHARGES ........................................................ 108 APPENDIX J – OUTBACK QUEENSLAND COOPERATIVE DOMESTIC MARKETING OPPORTUNITIES 2006/2007.................................................................................. 117

SUSTAINABLE TOURISM SERVICES 1

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

1.0 EXECUTIVE SUMMARY

In July 2006 Mount Isa City Council (MICC) and Mount Isa Tourism Association (MITA) contracted Sustainable Tourism Services (STS) to examine the effectiveness of the current management model for tourism in Mount Isa, identify priority action areas, and make recommendations as to how Mount Isa could best manage tourism over the next ten years. The name of Mount Isa is synonymous with mining on a large scale. ‘The Isa’ exists because of its mine and mining continues to influence almost every aspect of the city’s development. The size of the tourism industry is small and there are few resources to undertake tourism promotion and development initiatives that are needed to realise the tourism potential of the area. MICC has filled the leadership and resources gap by becoming the main coordinator of tourism activities in recent years. The private sector tourism body (MITA) is limited in its operations with no staff and a small funding base. Given the size of Mount Isa and its role as a transport and service hub the City has an opportunity to service a wider range of visitor markets than other towns in the North West/Outback Queensland. STS consulted with key industry stakeholders to identify issues and future options and reviewed best practice models in other areas which might be applicable to Mount Isa. In preparing this report, three options were considered for a future tourism model for Mount Isa. One was a tourism specific model, the second a merger with the Chamber of Commerce and the third was a new economic development model that included tourism and the Chamber of Commerce. In discussions with all of the major stakeholders in Mount Isa, including MITA and the Chamber of Commerce, there was a strong preference for the new economic development model which has the potential to significantly lift the profile of the city and increase its ability to compete for greater investment and funding input from industry and governments. This model also has the potential to provide a more solid and sustainable base for leadership and coordination of tourism development in The Isa. This Economic Development/Tourism model proposes a proactive, collaborative and strategic economic development role on behalf of the City and all its commercial activities – including tourism. It proposes a significant increase in Mount Isa’s capacity to control its own destiny for the future. It also brings together State and Local Governments and all of the main corporate players in the private sector for a united focus on strategic planning and economic development and provides a common direction for all government and private resources for the benefit of the City. The predominant reason for the perceived ineffectiveness of past tourism marketing has been the lack of resources. The new model provides for more funding and resources for planning and implementation of tourism marketing and development. This report also contains recommendations for implementation of the new Economic Development/Tourism Model.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

2

1.1 SUMMARY OF RECOMMENDATIONS

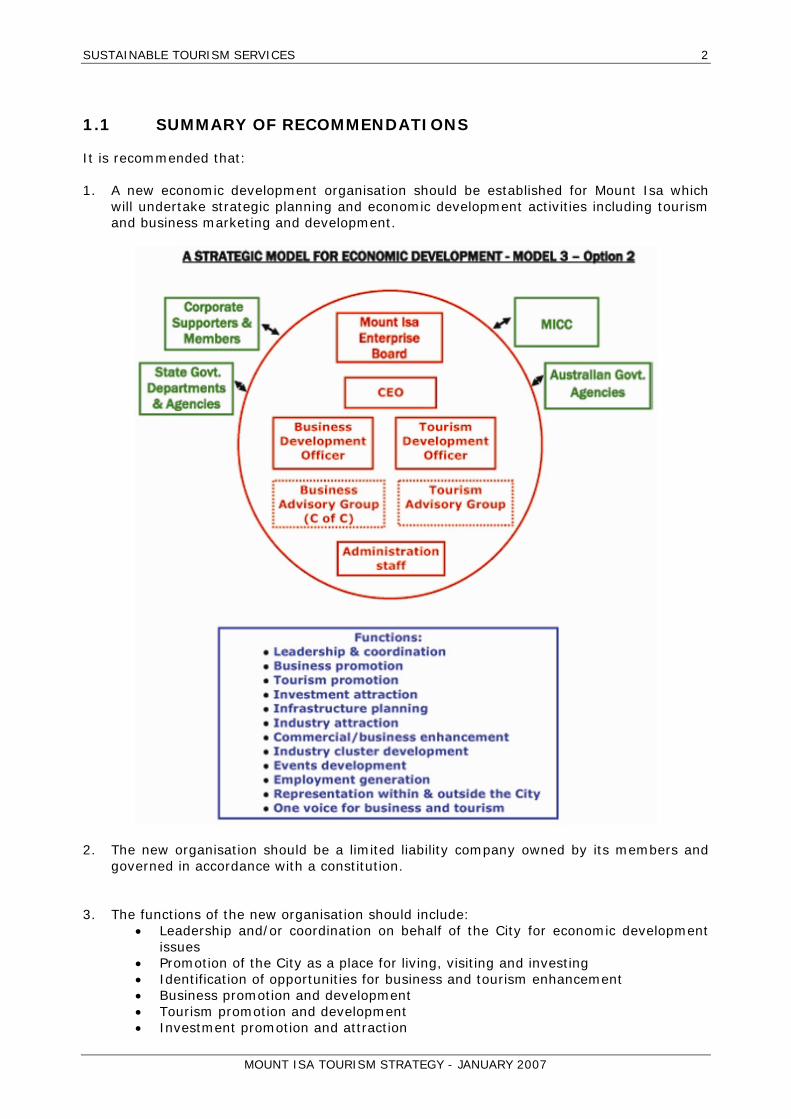

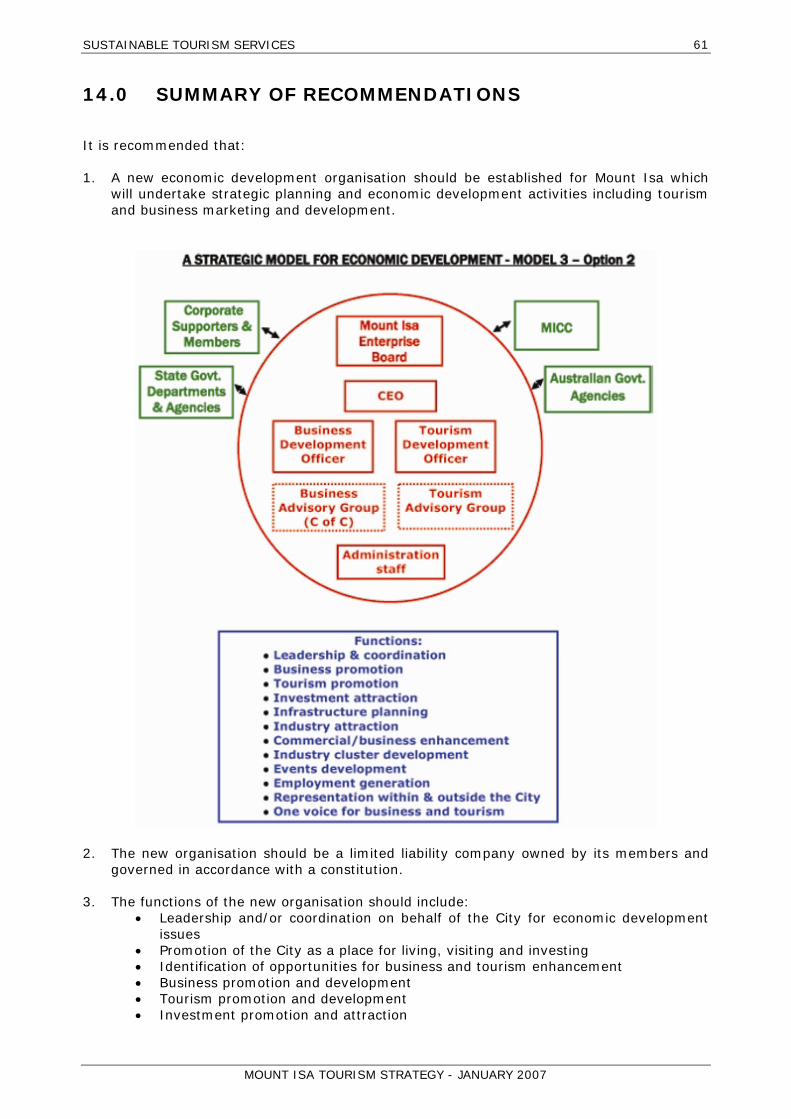

It is recommended that: 1. A new economic development organisation should be established for Mount Isa which

will undertake strategic planning and economic development activities including tourism and business marketing and development.

2. The new organisation should be a limited liability company owned by its members and

governed in accordance with a constitution. 3. The functions of the new organisation should include:

• Leadership and/or coordination on behalf of the City for economic development issues

• Promotion of the City as a place for living, visiting and investing • Identification of opportunities for business and tourism enhancement • Business promotion and development • Tourism promotion and development • Investment promotion and attraction

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

3

• Infrastructure planning and input into government planning processes • Industry attraction • Commercial/business enhancement • Industry cluster development (including tourism) • Events development and/or facilitation • Employment generation • Representation of the Isa within & outside the City • One voice for business and tourism – spokesperson role • Provision of business and tourism information to various internal and external

audiences • Community education of the benefits from business and tourism

4. An annual economic development strategy for Mount Isa is developed and implemented

by the new organisation on behalf of its stakeholders, containing action plans for both tourism and business marketing and development.

5. A dedicated tourism positioning and brand strategy should be prepared. This should

provide overall direction for all Mount Isa promotional activities.

6. MICC should be a major partner and financial contributor to the new Economic Development organisation. In this way, MICC will coordinate its support for tourism with other business and economic development activities.

7. An increased emphasis should be given to managing tourism in ways which are

sustainable and contribute benefits to the Mount Isa community. 8. A communication plan to increase the level of knowledge and understanding of tourism

in the City should be developed, including more comprehensive information on tourism’s contribution to Mount Isa’s economy.

9. Council and major stakeholders should adopt a staged implementation plan in relation to

the recommended actions contained in this report. (An implementation framework is enclosed.)

10. The main stakeholders (as listed below) should form an Implementation Taskforce which

will coordinate the preparation work and the implementation of the new organisation: • MICC • Xstrata Copper • Queensland Government Department of State Development and Innovation • Mount Isa Water • Mount Isa Airport • Mount Isa Chamber of Commerce • MITA

11. The Taskforce should be formed and the consultation period commence immediately

following acceptance of this report and be linked to a planned commencement date for the new organisation of 1 July 2007.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

4

2.0 BACKGROUND AND OBJECTIVES

2.1 BACKGROUND

The name of Mount Isa is synonymous with mining on a large scale. ‘The Isa’ exists because of its mine and mining continues to influence almost every aspect of the city’s development. Tourism in Mount Isa is highly seasonal with most visitors arriving between May and October each year. Most are escaping the colder weather in southern Australia to take advantage of the moderate, fine and sunny weather that prevails at this time of the year and to experience the unique outback areas of Queensland and the Northern Territory. Covering an area of 43,420 square kilometers, Mount Isa is strategically located in relation to the major highways linking Queensland and the Northern Territory. It is situated on the Overlander’s Way, the main east-west highway linking the Queensland north coast from Townsville through to Tennant Creek. The Matilda Highway, which links southern Queensland with the Gulf of Carpentaria, also runs through the city. The Savannah Way which runs all the way from Cairns in tropical north Queensland through to Broome in Western Australia passes close to the north. The city is isolated and remote from mainstream Australia with extreme environmental conditions. The east coast of Queensland is 900 kilometers to the east and Brisbane is 1900 kilometers away, to the south east. As noted above, Mount Isa has been, and is, predominately a mining town. With the current mining boom in Australia, the focus on tourism is not as high with many local businesses as it is for many other Outback towns. The size of the tourism industry is small and there are few resources to undertake tourism promotion and development initiatives that are needed to realise the tourism potential of the area. The Mount Isa City Council (MICC) has filled the leadership and resources gap by becoming the main coordinator of tourism activities in recent years. The private sector tourism body; the Mount Isa Tourism Association (MITA), is limited in its operations with no staff and a small funding base. A working group consisting of MICC and MITA representatives contracted Sustainable Tourism Services (STS) in July 2006 to undertake a review of possible options for a new tourism structure for Mount Isa and to prepare a tourism strategy identifying priority action areas in consultation with key industry groups. The aim of the project was to:

• Examine the effectiveness of the current management model for tourism in Mount Isa • Consult with key industry stakeholders to identify issues and future options • Review best practice models in other areas which might be applicable to Mount Isa, and • Recommend how Mount Isa could best manage tourism over the next ten years.

2.2 OBJECTIVES

A number of project outcomes were identified at the outset of the project. These include: • Assess the current situation and its effectiveness • Identify what stakeholders believe to be the best options for tourism in Mount Isa • Gauge an understanding of realistic expectations for future tourism growth in Mount

Isa • Examine and report on alternative structures/models and how they might be suitable

to Mount Isa, including how stakeholders can contribute to support the local tourism organisation

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

5

• Analyse existing marketing and consumer perceptions and provide recommendations for strategies to achieve improved outcomes

• Prepare an action plan including priority action areas and new or potential future projects for implementation

• Recommend how improved stakeholder relationships could be established for Mount Isa

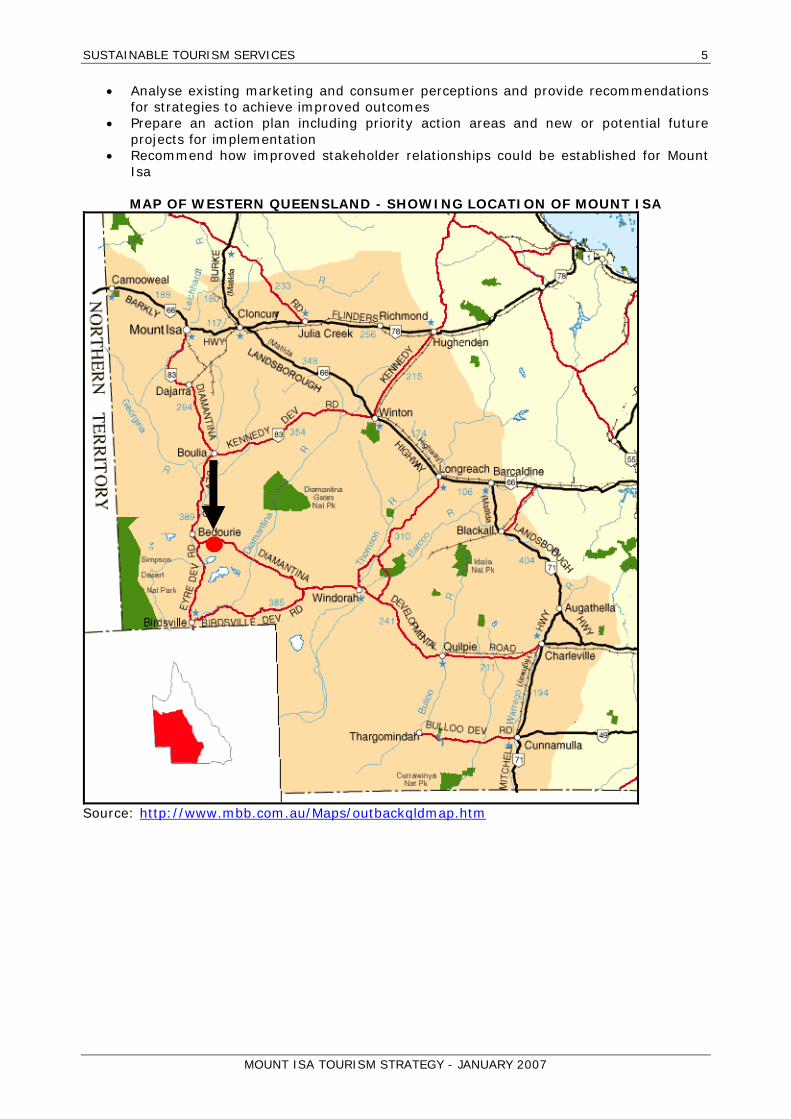

MAP OF WESTERN QUEENSLAND - SHOWING LOCATION OF MOUNT ISA

Source: http://www.mbb.com.au/Maps/outbackqldmap.htm

SUSTAINABLE TOURISM SERVICES 6

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

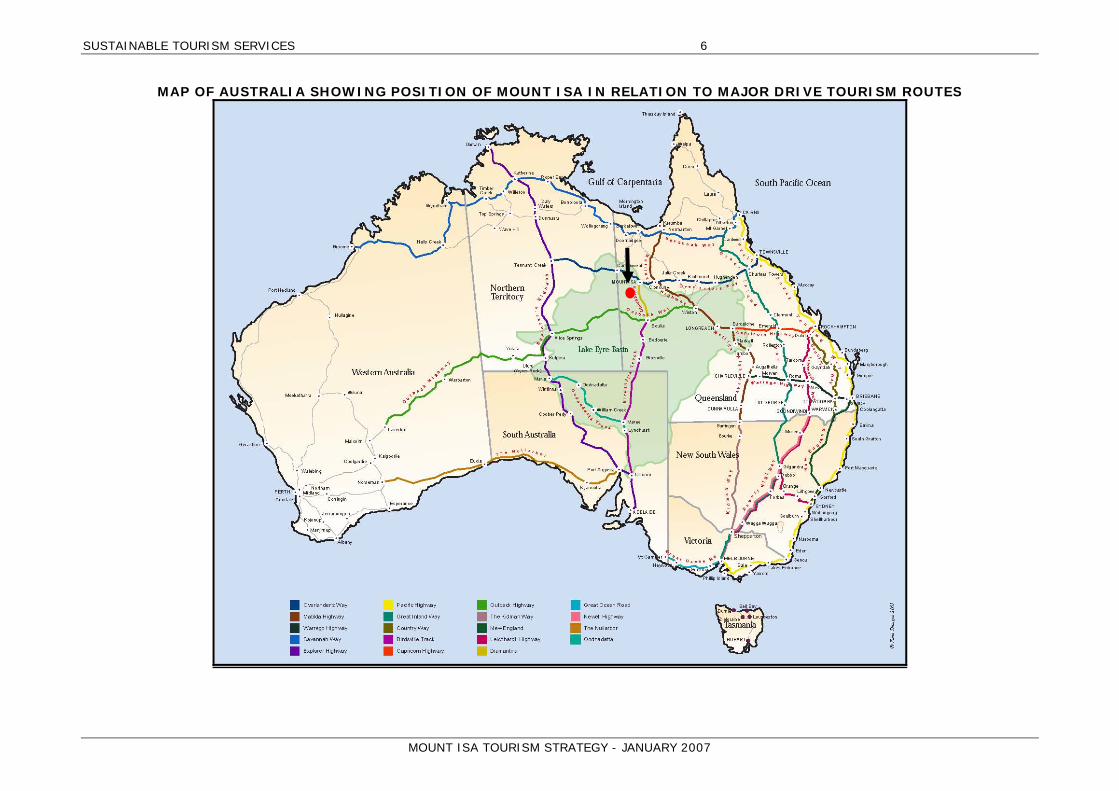

MAP OF AUSTRALIA SHOWING POSITION OF MOUNT ISA IN RELATION TO MAJOR DRIVE TOURISM ROUTES

SUSTAINABLE TOURISM SERVICES 7

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

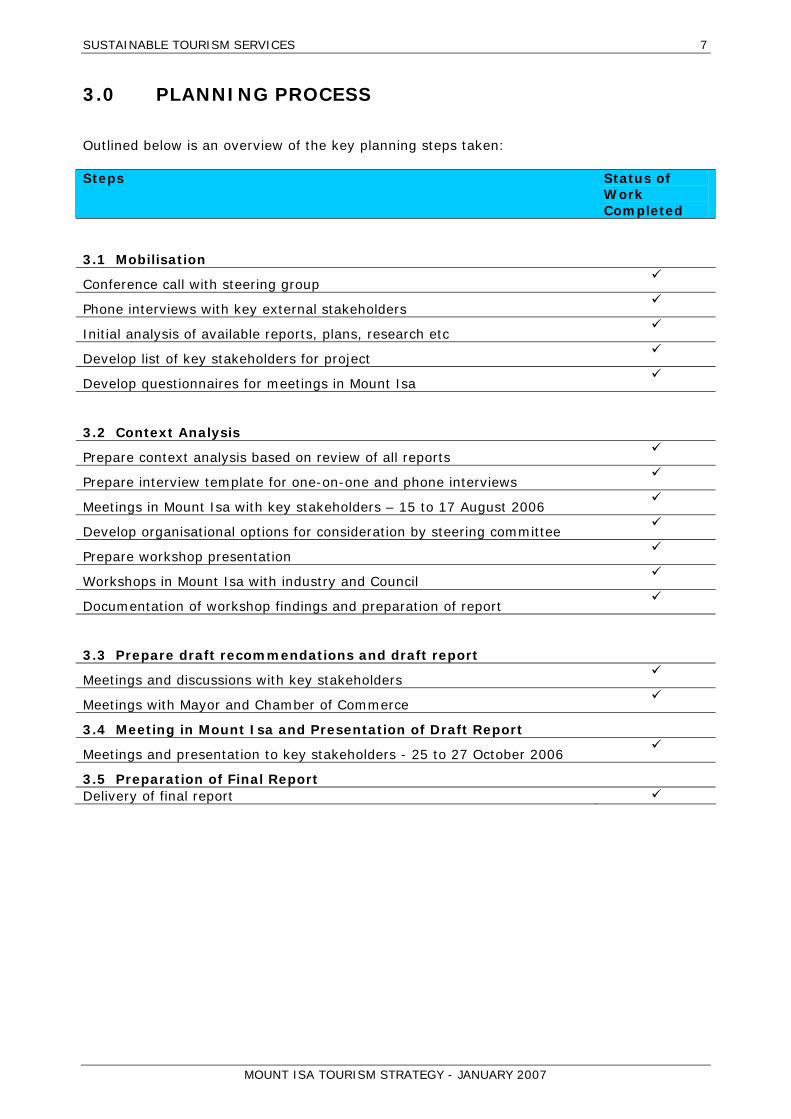

3.0 PLANNING PROCESS

Outlined below is an overview of the key planning steps taken: Steps Status of

Work Completed

3.1 Mobilisation

Conference call with steering group

Phone interviews with key external stakeholders

Initial analysis of available reports, plans, research etc

Develop list of key stakeholders for project

Develop questionnaires for meetings in Mount Isa

3.2 Context Analysis

Prepare context analysis based on review of all reports

Prepare interview template for one-on-one and phone interviews

Meetings in Mount Isa with key stakeholders – 15 to 17 August 2006

Develop organisational options for consideration by steering committee

Prepare workshop presentation

Workshops in Mount Isa with industry and Council

Documentation of workshop findings and preparation of report

3.3 Prepare draft recommendations and draft report

Meetings and discussions with key stakeholders

Meetings with Mayor and Chamber of Commerce

3.4 Meeting in Mount Isa and Presentation of Draft Report

Meetings and presentation to key stakeholders - 25 to 27 October 2006

3.5 Preparation of Final Report

Delivery of final report

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

8

4.0 CONTEXT ANALYSIS

4.1 LITERATURE SEARCH

A comprehensive range of available material on tourism relating to Mount Isa was analysed as part of this review. Documents examined included: Mount Isa

• Mount Isa Tourism Masterplan – Mount Isa City Council (MICC)/ATS - 2000 • Mount Isa Heritage Centre Report (Mount Isa Outback Centre) – Convergence Design

2001 • Mount Isa City Council 2003 - 2004 Annual Report • Mount Isa City Council Operational Plan 2005 - 2006 • Mount Isa City Council Corporate Plan 2005 – 2010 • Mount Isa Tourism Association’s Constitution - 2004

North-West Queensland

• Research Among Visitors to Sites, Attractions and Exhibits in North West Queensland – Tourism Queensland (TQ) – 1999

• North West Queensland Regional Tourism Action Plan – MICC/NCSTT – 2003 Outback Queensland

• Outback Queensland Regional Tourism Strategy 1996 – Outback Queensland Tourism Authority

• Outback Queensland Regional Tourism Strategy 2000 – Outback Queensland Tourism Authority

• Outback Domestic Leisure Marketing Strategy 2001–2004 – Tourism Queensland • Outback Marketing Report – MCR/Tourism Queensland – 2002 • The Outback Regional Summary – Tourism Queensland - 2002 • Pathway 2010 - A Marketing Plan – Outback Queensland Tourism Association/Best –

2004 • Pathway 2010 - A Business Plan – Outback Queensland Tourism Association/Best

Management Group/Executive Resource Group • Outback Destination Management Plan – Tourism Queensland – 2004 • Queensland Outback Demand Audit – Tourism Queensland – 2005 • Our Outback: Partnerships and Pathways to Success in Tourism – Desert Knowledge

Australia/Sustainable Tourism Services – 2005 • Outback Regional Update – Tourism Queensland - 2005

Queensland

• Queensland Heritage Trails Network Marketing Audit – Tourism Queensland/Economic and Market Development Advisors – 2001

• Overlander’s Way Marketing Plan – 2006-2007 Regional Tourism

• Funding Options for Regional Tourism Organisations – Sustainable Tourism Services 2004 (prepared for Tourism Queensland)

4.2 INDUSTRY MEETINGS

An extensive program of meetings was conducted to secure feedback and comment on the current situation and options for the future. A survey of all key stakeholders was also completed. Key interviews were undertaken with the following:

• The Mayor, Mount Isa City Council • Mount Isa City Council Councillors and Executives (presentation) • Chairman and committee members of Mount Isa Tourism Association (MITA)

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

9

• Chief Operating Officer of Xstrata Copper • President of the Chamber of Commerce • Several Queensland Government Department regional offices (in Mount

Isa/Brisbane) • Numerous tourism operators • Representatives of Brisbane based transport companies servicing Mount Isa • CEO of the Outback Queensland Tourism Association • Tourism Queensland/Tourism Australia • Mount Isa Airport • National Parks and Wildlife Service

(Feedback from these meetings is included as Appendix C.) A survey approved by the Steering Committee was also sent out to all key stakeholders. A workshop which was open to public attendance was conducted to obtain feedback and comment on the main issues facing tourism in Mount Isa. Best practice tourism models, structures and relationships were examined for their relevance to Mount Isa tourism. An overview of typical models is included in Chapter 8.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

10

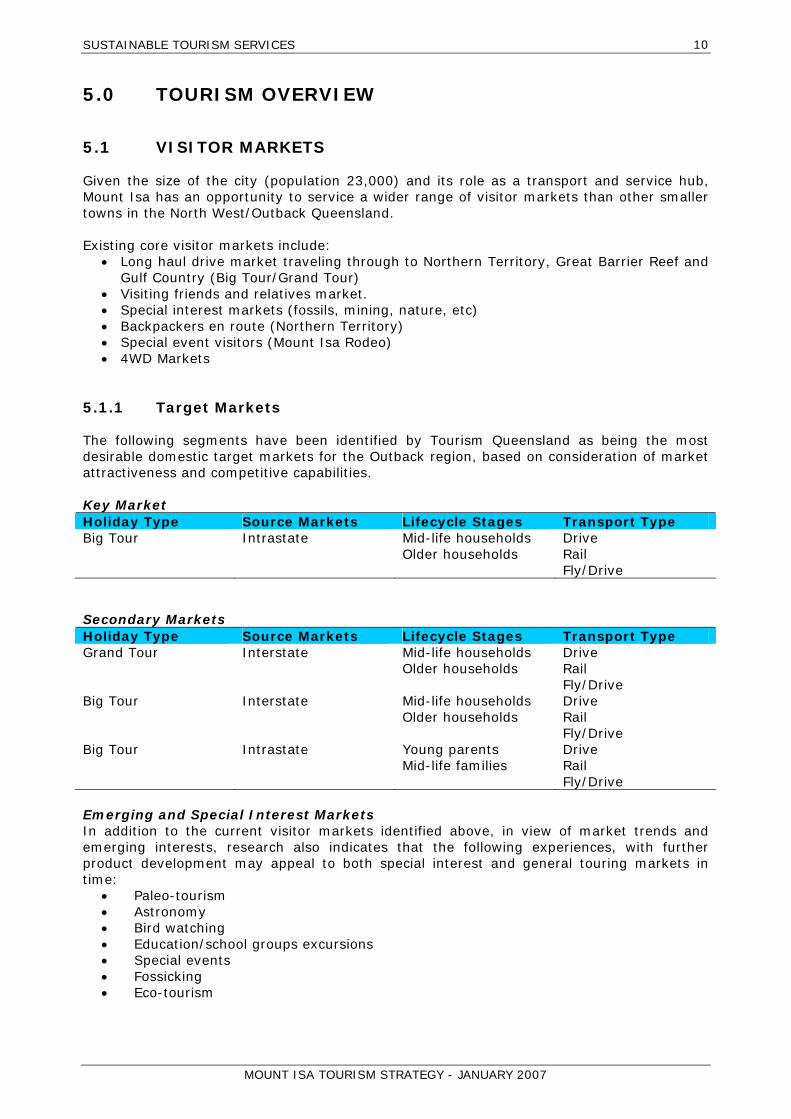

5.0 TOURISM OVERVIEW

5.1 VISITOR MARKETS

Given the size of the city (population 23,000) and its role as a transport and service hub, Mount Isa has an opportunity to service a wider range of visitor markets than other smaller towns in the North West/Outback Queensland. Existing core visitor markets include:

• Long haul drive market traveling through to Northern Territory, Great Barrier Reef and Gulf Country (Big Tour/Grand Tour)

• Visiting friends and relatives market. • Special interest markets (fossils, mining, nature, etc) • Backpackers en route (Northern Territory) • Special event visitors (Mount Isa Rodeo) • 4WD Markets

5.1.1 Target Markets

The following segments have been identified by Tourism Queensland as being the most desirable domestic target markets for the Outback region, based on consideration of market attractiveness and competitive capabilities. Key Market Holiday Type Source Markets Lifecycle Stages Transport Type Big Tour Intrastate Mid-life households

Older households Drive Rail Fly/Drive

Secondary Markets Holiday Type Source Markets Lifecycle Stages Transport Type Grand Tour Interstate Mid-life households

Older households Drive Rail Fly/Drive

Big Tour Interstate Mid-life households Older households

Drive Rail Fly/Drive

Big Tour Intrastate Young parents Mid-life families

Drive Rail Fly/Drive

Emerging and Special Interest Markets In addition to the current visitor markets identified above, in view of market trends and emerging interests, research also indicates that the following experiences, with further product development may appeal to both special interest and general touring markets in time:

• Paleo-tourism • Astronomy • Bird watching • Education/school groups excursions • Special events • Fossicking • Eco-tourism

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

11

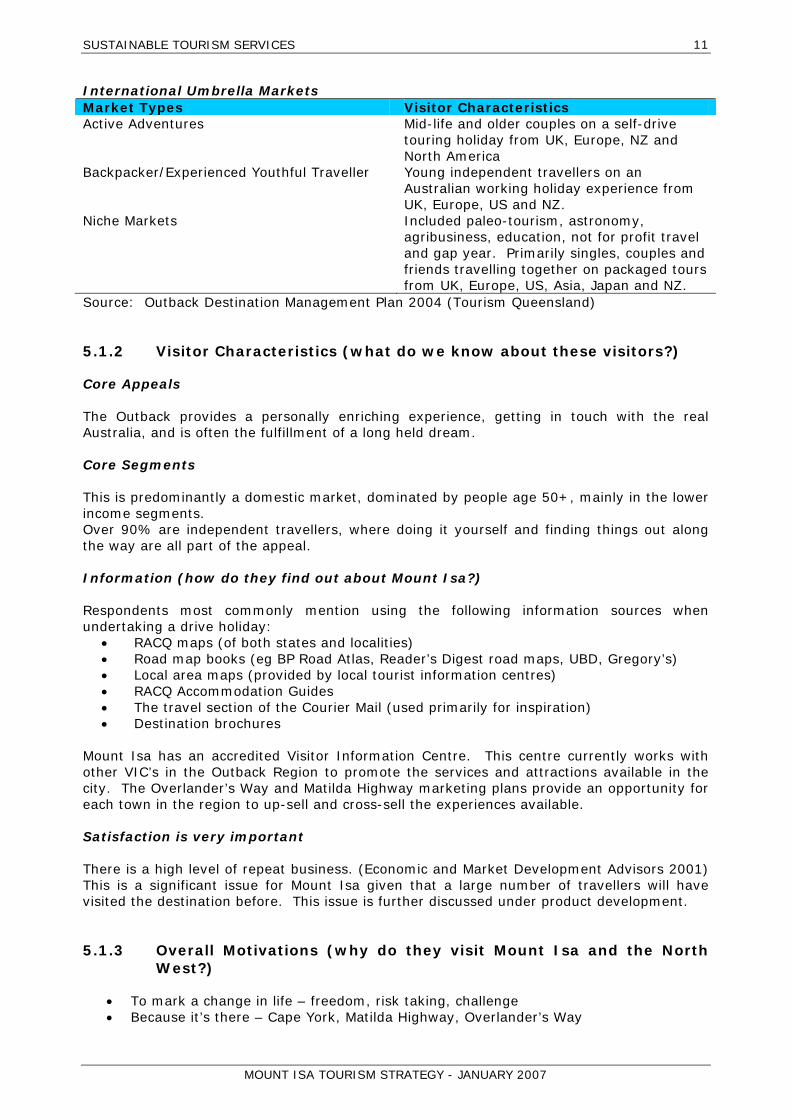

International Umbrella Markets Market Types Visitor Characteristics Active Adventures Mid-life and older couples on a self-drive

touring holiday from UK, Europe, NZ and North America

Backpacker/Experienced Youthful Traveller Young independent travellers on an Australian working holiday experience from UK, Europe, US and NZ.

Niche Markets Included paleo-tourism, astronomy, agribusiness, education, not for profit travel and gap year. Primarily singles, couples and friends travelling together on packaged tours from UK, Europe, US, Asia, Japan and NZ.

Source: Outback Destination Management Plan 2004 (Tourism Queensland)

5.1.2 Visitor Characteristics (what do we know about these visitors?)

Core Appeals The Outback provides a personally enriching experience, getting in touch with the real Australia, and is often the fulfillment of a long held dream. Core Segments This is predominantly a domestic market, dominated by people age 50+, mainly in the lower income segments. Over 90% are independent travellers, where doing it yourself and finding things out along the way are all part of the appeal. Information (how do they find out about Mount Isa?) Respondents most commonly mention using the following information sources when undertaking a drive holiday:

• RACQ maps (of both states and localities) • Road map books (eg BP Road Atlas, Reader’s Digest road maps, UBD, Gregory’s) • Local area maps (provided by local tourist information centres) • RACQ Accommodation Guides • The travel section of the Courier Mail (used primarily for inspiration) • Destination brochures

Mount Isa has an accredited Visitor Information Centre. This centre currently works with other VIC’s in the Outback Region to promote the services and attractions available in the city. The Overlander’s Way and Matilda Highway marketing plans provide an opportunity for each town in the region to up-sell and cross-sell the experiences available. Satisfaction is very important There is a high level of repeat business. (Economic and Market Development Advisors 2001) This is a significant issue for Mount Isa given that a large number of travellers will have visited the destination before. This issue is further discussed under product development.

5.1.3 Overall Motivations (why do they visit Mount Isa and the North West?)

• To mark a change in life – freedom, risk taking, challenge • Because it’s there – Cape York, Matilda Highway, Overlander’s Way

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

12

• To complete their knowledge of Australia • To revisit old haunts (Darwin, Mount Isa, Defence Force bases) • Enjoyment of heritage/history and ‘traditional Australian values’ (friendliness,

resourcefulness, enterprise, hospitality, company) • Peace and quiet, space

Specific interests: • Fossils, minerals, flora and fauna • The holiday in the Outback is perceived in terms of a total visitation experience.

Visits through individual towns or attractions build towards an overall and continuous experience. (Parfitt 1998, Economic and Market Development Advisors 2001, STS 2005).

5.1.4 The Journey (where do they come from and where do they go to?)

• There are three key end points – Darwin, Cairns/Cape York, Karumba • There are three key road corridors or entry points – the Overlander’s Way (East to

West), the Matilda Highway (North to South) and the Savannah Way (East to West – refer map in section 2.2)

• Rarely will the same route be used going and coming back • Most travellers have end and/or mid dates – eg bookings at Karumba, camel races at

Charleville, arranged meetings points with other travellers • Travelling is usually flexible, allowing for long stays in places of interest and/or

positive welcome. Extended stays in a particular location are usually compensated by shorter stays in less interesting or friendly places.

• Most travellers have a fairly precise idea of the overall time they will spend away from home and this is based on considerations of budget, climate and tolerance of living and traveling conditions.

Mount Isa needs to position itself as both a key service centre and as an activity focal point for all travel to north-western Australia. Feedback from operators indicates that at the moment the city is not keeping leisure visitors beyond 1-2 days stopover. It is perceived as a transit area, on the way to an end point, not a destination in itself.

5.2 VISITOR EXPENDITURE

Total visitor expenditure in Queensland for the 2005 year was $9.508 million from domestic visitors and $2.781 million from international visitors, making a total of $12.285 million. For the Outback Region, domestic visitors spent $207 million and international visitors $14 million, making a total of $221 million, for the 2005 year. These figures represent the actual expenditure by visitors. They do not fully reflect the effects on the State and Regional economies as this expenditure flows through the community.

5.3 DOMESTIC VISITORS TO THE OUTBACK REGION AND MOUNT ISA

Tourism Queensland, in their Outback Regional Update for 2005, provides details of visitors to the Outback Region. (This document is the source for all information in Section 5.3) In the 2005 year, 503,000 domestic visitors travelled to the region. They included 167,000 holiday visitors (33%), 149,000 Visiting Friends and Relatives (VFR) (30%), and 134,000 business visitors (27%).

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

13

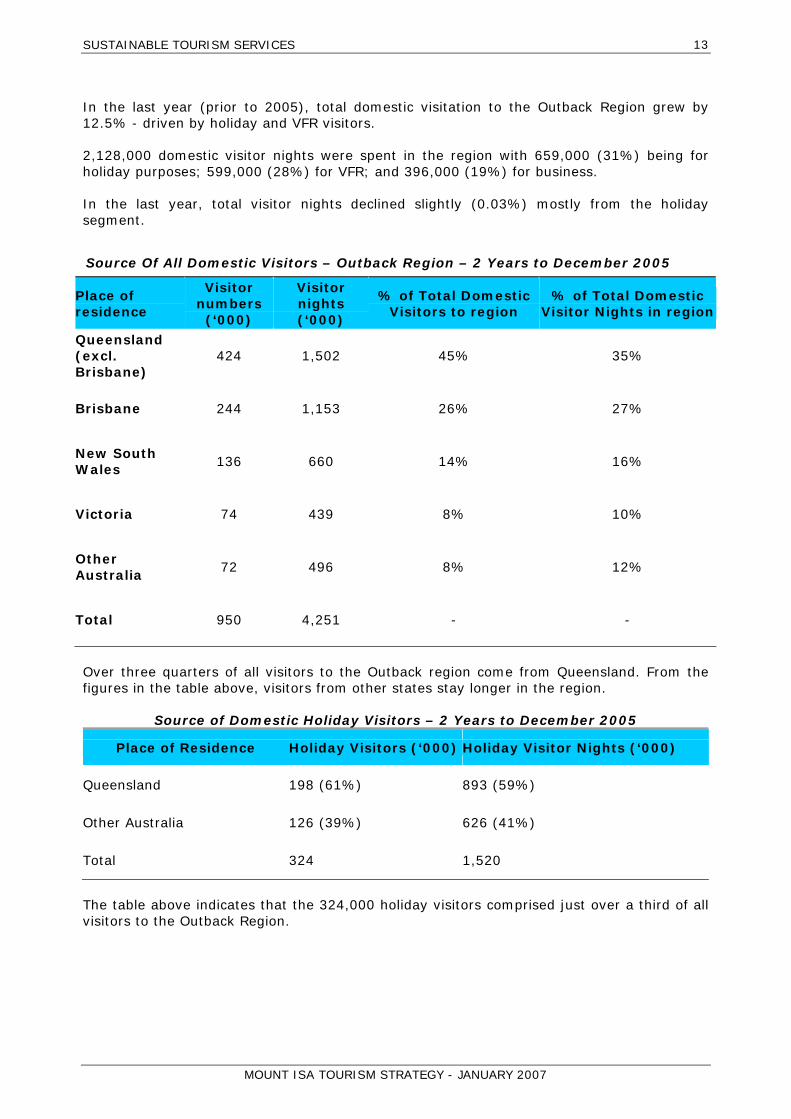

Source Of All Domestic Visitors – Outback Region – 2 Years to December 2005

In the last year (prior to 2005), total domestic visitation to the Outback Region grew by 12.5% - driven by holiday and VFR visitors. 2,128,000 domestic visitor nights were spent in the region with 659,000 (31%) being for holiday purposes; 599,000 (28%) for VFR; and 396,000 (19%) for business. In the last year, total visitor nights declined slightly (0.03%) mostly from the holiday segment.

Place of residence

Visitor numbers

(‘000)

Visitor nights (‘000)

% of Total Domestic Visitors to region

% of Total Domestic Visitor Nights in region

Queensland (excl. Brisbane)

424 1,502 45% 35%

Brisbane 244 1,153 26% 27%

New South Wales

136 660 14% 16%

Victoria 74 439 8% 10%

Other Australia

72 496 8% 12%

Total 950 4,251 - -

Over three quarters of all visitors to the Outback region come from Queensland. From the figures in the table above, visitors from other states stay longer in the region.

Source of Domestic Holiday Visitors – 2 Years to December 2005

Place of Residence Holiday Visitors (‘000) Holiday Visitor Nights (‘000)

Queensland 198 (61%) 893 (59%)

Other Australia 126 (39%) 626 (41%)

Total 324 1,520

The table above indicates that the 324,000 holiday visitors comprised just over a third of all visitors to the Outback Region.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

14

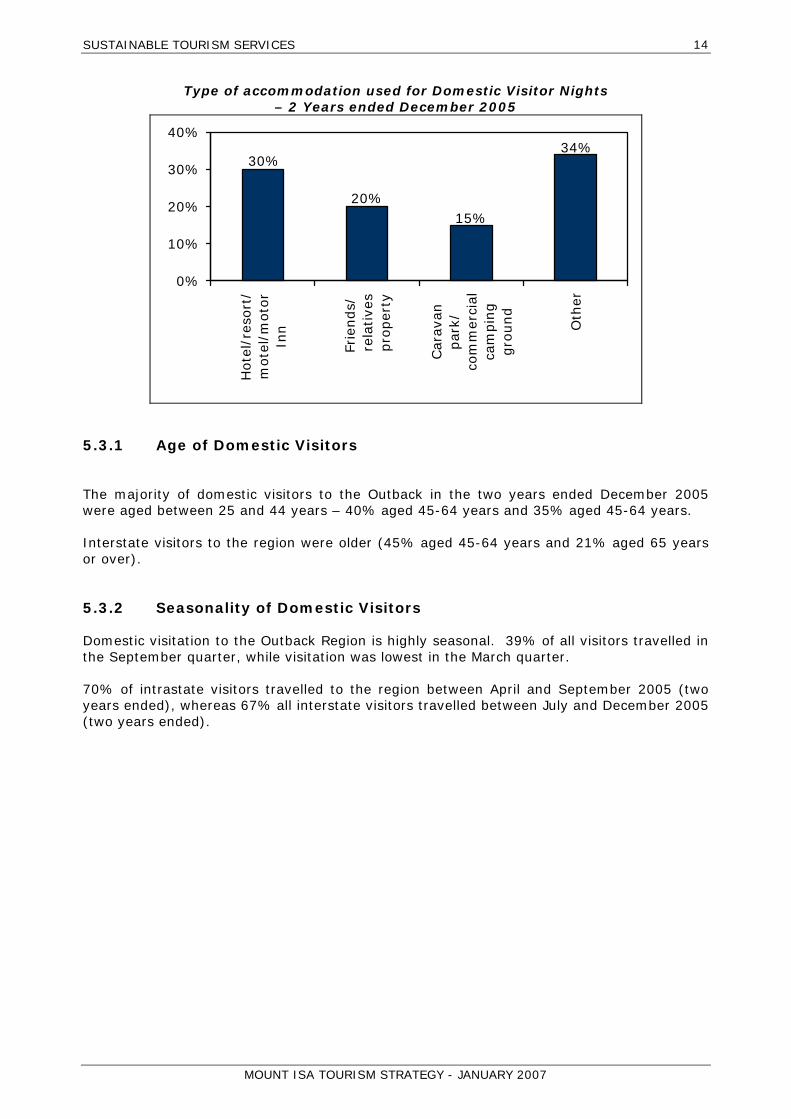

Type of accommodation used for Domestic Visitor Nights – 2 Years ended December 2005

34%

15%20%

30%

0%

10%

20%

30%

40%

Hote

l/re

sort

/m

ote

l/m

oto

rIn

n

Frie

nds/

re

lative

spro

per

ty

Car

avan

par

k/co

mm

erci

alca

mpin

ggro

und

Oth

er

5.3.1 Age of Domestic Visitors

The majority of domestic visitors to the Outback in the two years ended December 2005 were aged between 25 and 44 years – 40% aged 45-64 years and 35% aged 45-64 years. Interstate visitors to the region were older (45% aged 45-64 years and 21% aged 65 years or over).

5.3.2 Seasonality of Domestic Visitors

Domestic visitation to the Outback Region is highly seasonal. 39% of all visitors travelled in the September quarter, while visitation was lowest in the March quarter. 70% of intrastate visitors travelled to the region between April and September 2005 (two years ended), whereas 67% all interstate visitors travelled between July and December 2005 (two years ended).

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

15

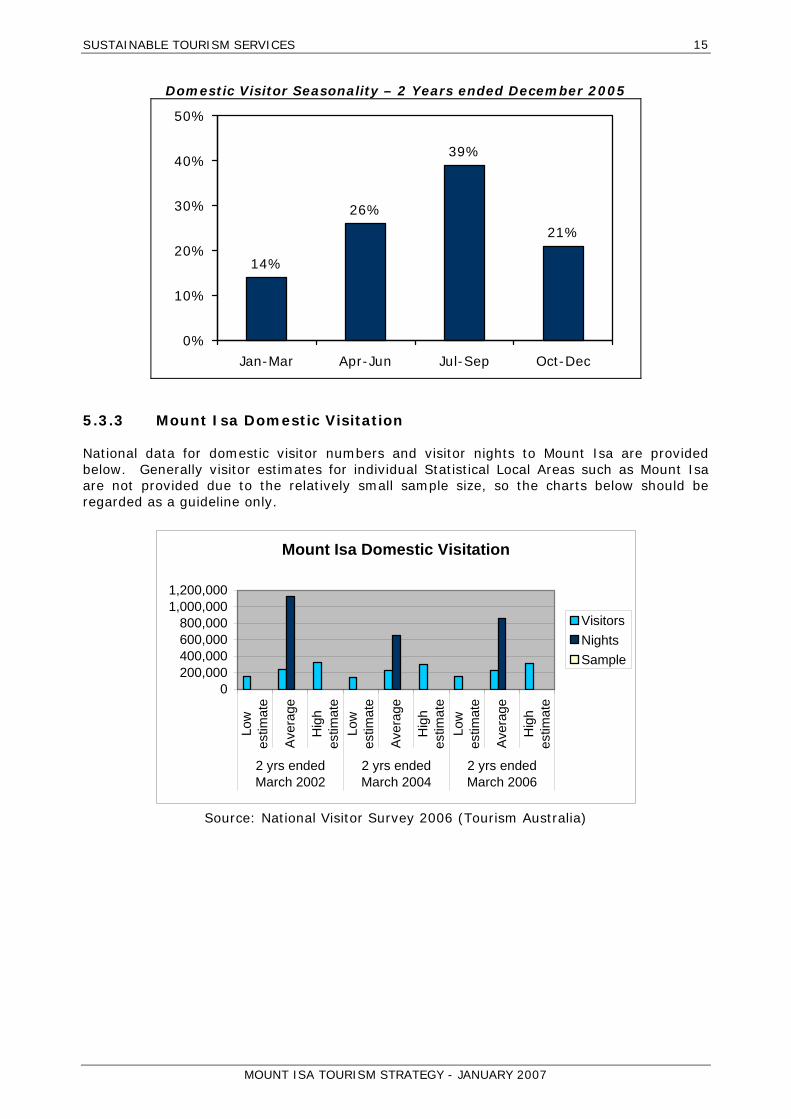

Domestic Visitor Seasonality – 2 Years ended December 2005

14%

26%

39%

21%

0%

10%

20%

30%

40%

50%

Jan-Mar Apr-Jun Jul-Sep Oct-Dec

5.3.3 Mount Isa Domestic Visitation

National data for domestic visitor numbers and visitor nights to Mount Isa are provided below. Generally visitor estimates for individual Statistical Local Areas such as Mount Isa are not provided due to the relatively small sample size, so the charts below should be regarded as a guideline only.

Mount Isa Domestic Visitation

0200,000400,000600,000800,000

1,000,0001,200,000

Low

estim

ate

Aver

age

Hig

hes

timat

eLo

wes

timat

e

Aver

age

Hig

hes

timat

eLo

wes

timat

e

Aver

age

Hig

hes

timat

e

2 yrs endedMarch 2002

2 yrs endedMarch 2004

2 yrs endedMarch 2006

VisitorsNightsSample

Source: National Visitor Survey 2006 (Tourism Australia)

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

16

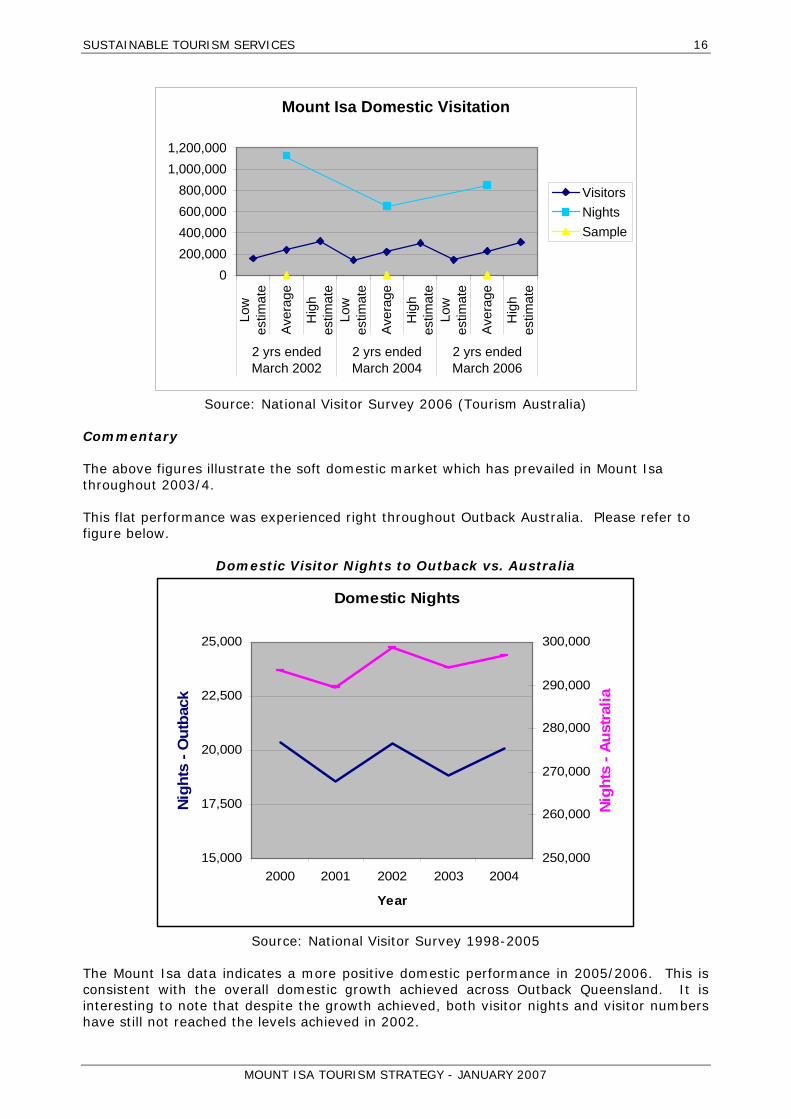

Mount Isa Domestic Visitation

0200,000400,000600,000800,000

1,000,0001,200,000

Low

estim

ate

Aver

age

Hig

hes

timat

eLo

wes

timat

e

Aver

age

Hig

hes

timat

eLo

wes

timat

e

Aver

age

Hig

hes

timat

e

2 yrs endedMarch 2002

2 yrs endedMarch 2004

2 yrs endedMarch 2006

VisitorsNightsSample

Source: National Visitor Survey 2006 (Tourism Australia)

Commentary The above figures illustrate the soft domestic market which has prevailed in Mount Isa throughout 2003/4. This flat performance was experienced right throughout Outback Australia. Please refer to figure below.

Domestic Visitor Nights to Outback vs. Australia

Domestic Nights

15,000

17,500

20,000

22,500

25,000

2000 2001 2002 2003 2004

Year

Nig

hts

- Out

back

250,000

260,000

270,000

280,000

290,000

300,000

Nig

hts

- Aus

tral

ia

Source: National Visitor Survey 1998-2005

The Mount Isa data indicates a more positive domestic performance in 2005/2006. This is consistent with the overall domestic growth achieved across Outback Queensland. It is interesting to note that despite the growth achieved, both visitor nights and visitor numbers have still not reached the levels achieved in 2002.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

17

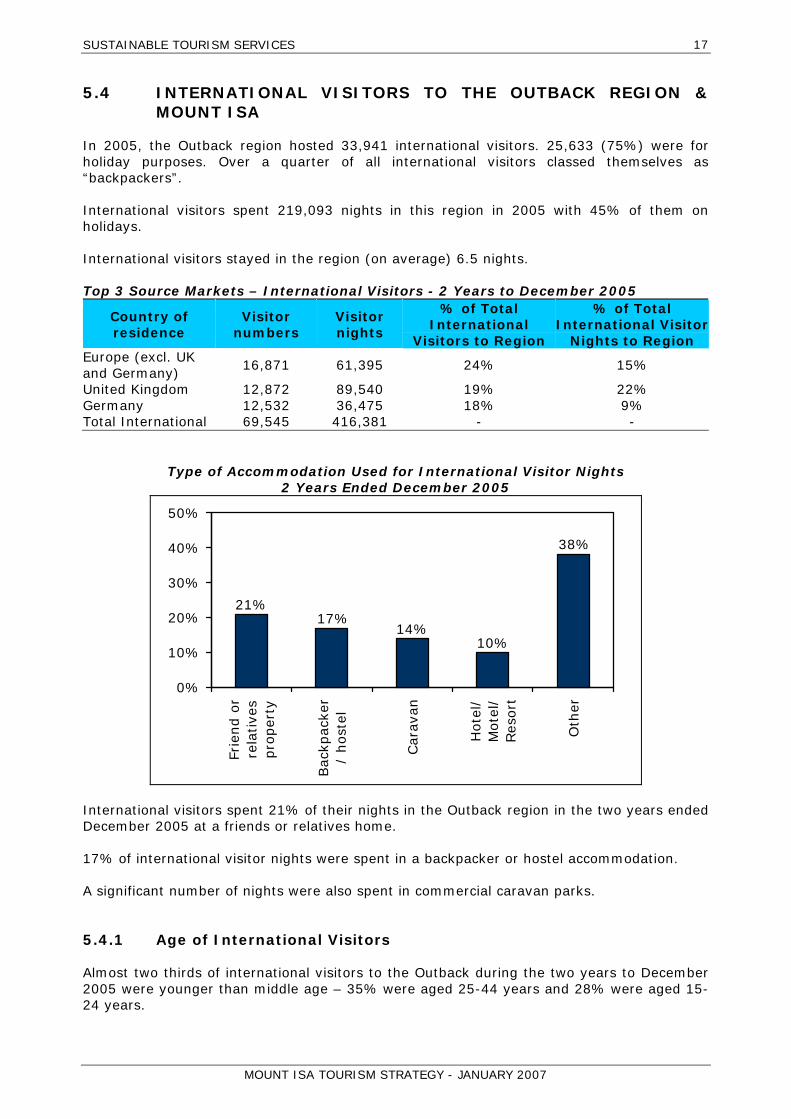

5.4 INTERNATIONAL VISITORS TO THE OUTBACK REGION & MOUNT ISA

In 2005, the Outback region hosted 33,941 international visitors. 25,633 (75%) were for holiday purposes. Over a quarter of all international visitors classed themselves as “backpackers”. International visitors spent 219,093 nights in this region in 2005 with 45% of them on holidays. International visitors stayed in the region (on average) 6.5 nights. Top 3 Source Markets – International Visitors - 2 Years to December 2005

Country of residence

Visitor numbers

Visitor nights

% of Total International

Visitors to Region

% of Total International Visitor

Nights to Region Europe (excl. UK and Germany)

16,871 61,395 24% 15%

United Kingdom 12,872 89,540 19% 22% Germany 12,532 36,475 18% 9% Total International 69,545 416,381 - -

Type of Accommodation Used for International Visitor Nights 2 Years Ended December 2005

38%

10%14%

17%21%

0%

10%

20%

30%

40%

50%

Frie

nd o

rre

lative

spro

per

ty

Bac

kpac

ker

/ host

el

Car

avan

Hote

l/M

ote

l/Res

ort

Oth

er

International visitors spent 21% of their nights in the Outback region in the two years ended December 2005 at a friends or relatives home. 17% of international visitor nights were spent in a backpacker or hostel accommodation. A significant number of nights were also spent in commercial caravan parks.

5.4.1 Age of International Visitors

Almost two thirds of international visitors to the Outback during the two years to December 2005 were younger than middle age – 35% were aged 25-44 years and 28% were aged 15-24 years.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

18

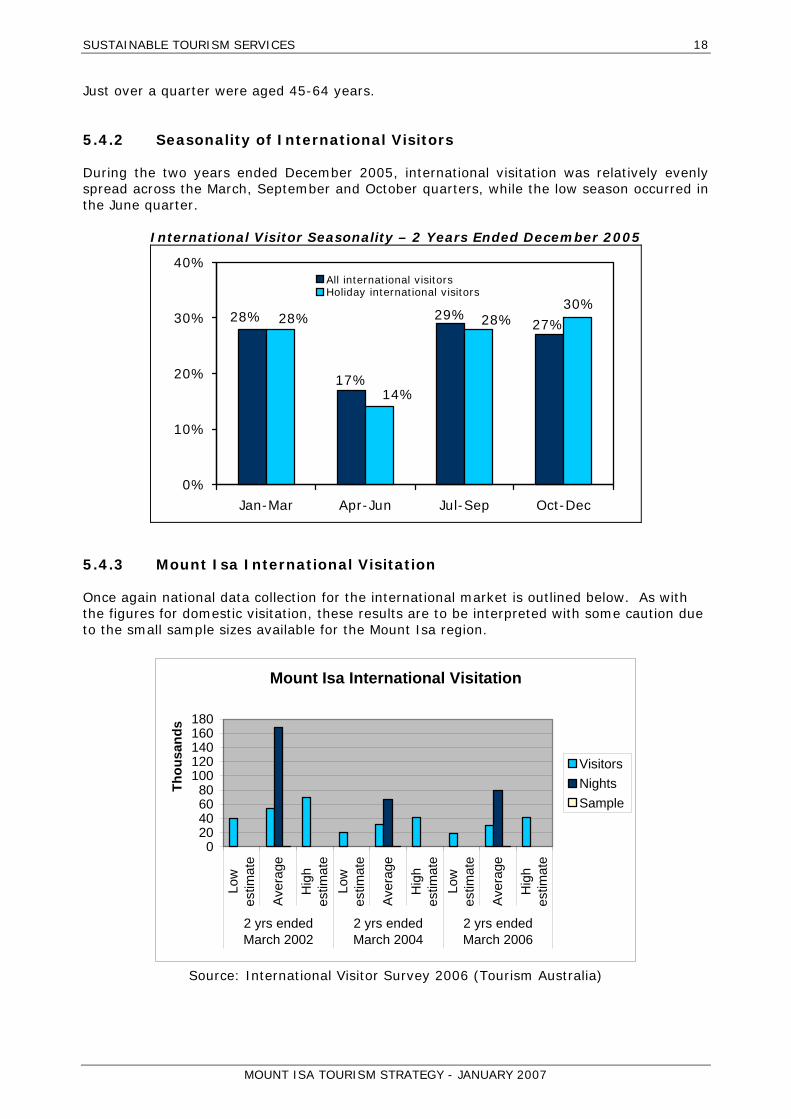

Just over a quarter were aged 45-64 years.

5.4.2 Seasonality of International Visitors

During the two years ended December 2005, international visitation was relatively evenly spread across the March, September and October quarters, while the low season occurred in the June quarter.

International Visitor Seasonality – 2 Years Ended December 2005

28% 27%29%

17%

28%30%

28%

14%

0%

10%

20%

30%

40%

Jan-Mar Apr-Jun Jul-Sep Oct-Dec

All international visitorsHoliday international visitors

5.4.3 Mount Isa International Visitation

Once again national data collection for the international market is outlined below. As with the figures for domestic visitation, these results are to be interpreted with some caution due to the small sample sizes available for the Mount Isa region.

Mount Isa International Visitation

020406080

100120140160180

Low

estim

ate

Ave

rage

Hig

hes

timat

eLo

wes

timat

e

Ave

rage

Hig

hes

timat

eLo

wes

timat

e

Ave

rage

Hig

hes

timat

e

2 yrs endedMarch 2002

2 yrs endedMarch 2004

2 yrs endedMarch 2006

Thou

sand

s

Visitors Nights Sample

Source: International Visitor Survey 2006 (Tourism Australia)

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

19

Mount Isa International Visitation

020406080

100120140160180

Low

estim

ate

Aver

age

Hig

hes

timat

eLo

wes

timat

e

Aver

age

Hig

hes

timat

eLo

wes

timat

e

Aver

age

Hig

hes

timat

e

2 yrs endedMarch 2002

2 yrs endedMarch 2004

2 yrs endedMarch 2006

Thou

sand

sVisitors Nights Sample

Source: International Visitor Survey 2006 (Tourism Australia)

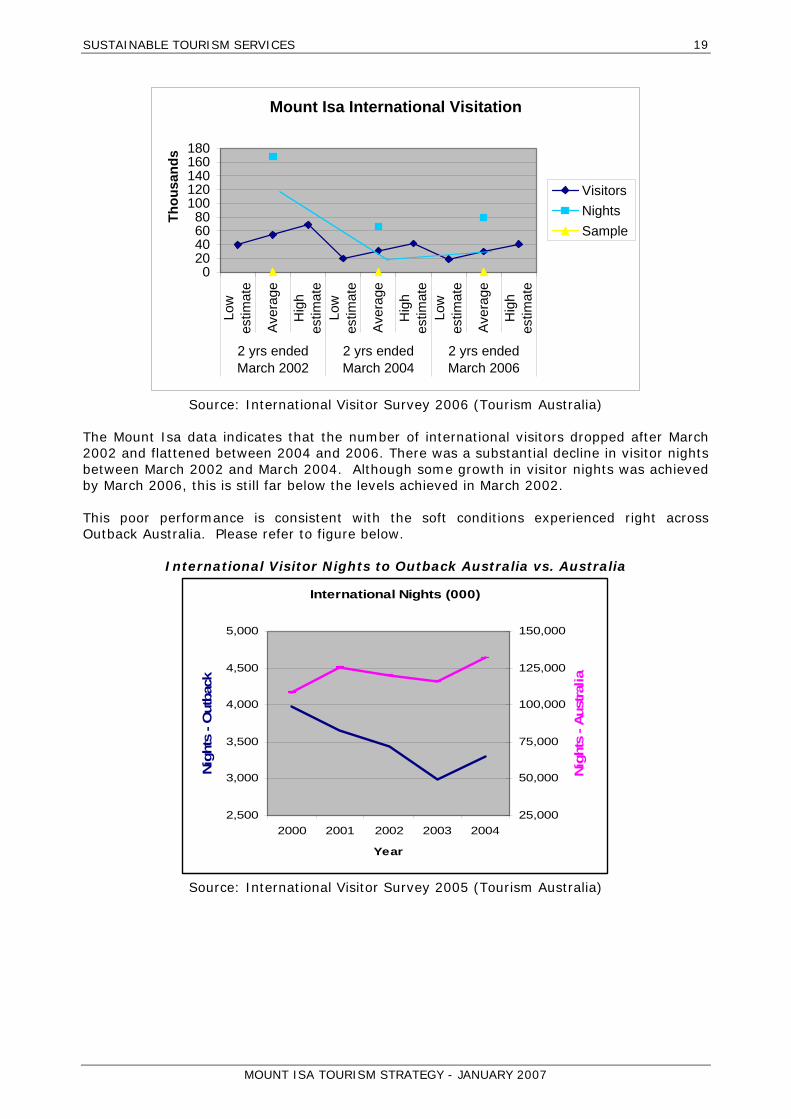

The Mount Isa data indicates that the number of international visitors dropped after March 2002 and flattened between 2004 and 2006. There was a substantial decline in visitor nights between March 2002 and March 2004. Although some growth in visitor nights was achieved by March 2006, this is still far below the levels achieved in March 2002. This poor performance is consistent with the soft conditions experienced right across Outback Australia. Please refer to figure below.

International Visitor Nights to Outback Australia vs. Australia

International Nights (000)

2,500

3,000

3,500

4,000

4,500

5,000

2000 2001 2002 2003 2004

Year

Nig

hts

- Out

back

25,000

50,000

75,000

100,000

125,000

150,000

Nig

hts

- Aus

tralia

Source: International Visitor Survey 2005 (Tourism Australia)

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

20

5.5 SEASONALITY

• Seasonality is quite dramatic in the Outback, with room occupancy fluctuating from approximately 30% in the low season to approximately 70% in peak season.

• Monthly occupancy levels for commercial accommodation in the Outback region are consistently highest between July and September and lowest between December and January.

• Over the two years ended December 2003, the peak season for all domestic visitors and holiday/leisure domestic visitors occurred from July to September (38% and 48% respectively). Domestic visitation was lowest between January and March (10% and 4% of the total domestic and holiday/leisure visitors to the region, respectively).

• Over the two years ending December 2003, international visitation to the Outback was lowest between January and June. International visitation was highest between July and September (31% and 33% of the total international and holiday/leisure international visitors respectively).

5.6 CURRENT MARKET/EMERGING OPPORTUNITIES

Tourism Queensland has identified the following market segments with varying growth and yield potentials: Domestic Markets Holiday Type

Geographic Source

Demographic Characteristics

Length of Stay

Travel Party

Type of Transport

Special Interest

Grand Tour

Interstate Intrastate

Mid-life households, Older households

15+ nights

Couple, Couples travelling together

Self-drive Culture/ heritage Nature Adventure Social Authentic experience

Big Tour – Couples Self-drive

Interstate Intrastate

Mid-life households, Older households

8-14 nights

Couple, Couples travelling together

Self-drive Culture/ heritage Nature Adventure Social Authentic experience

Big Tour – Couples Rail

Intrastate Mid-life households, Older households

5-10 nights

Couple, Couples travelling together

Rail Culture/ heritage Nature Adventure Social Authentic experience

Big Tour – Families Self-drive

Intrastate Young parents, Mid-life families

5-10 nights

Family and friends with children

Self-drive Education Culture/ heritage Nature Adventure Family Experience real Aust.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

21

Queensland’s Outback attracts mid-life and older couples from both intrastate and interstate on the self-drive Grand Tour/Big Tour holiday. This market represents a variable level of growth and yield potential for this destination. Anecdotal evidence suggests the latter two groups in the above mentioned table represent a comparatively small market with limited potential. It would appear that there are three segments with significantly greater potential for growth, including short-stay markets, backpackers and international/campervan segments. The “grey nomads” represent an ongoing source of visitation for Outback Queensland – the challenge is to attract new segments. Potential Domestic Visitor Markets In addition to the current visitor markets, the following experiences, with further product development, may appeal to special interest, short stay, backpacking, international/campervan and general touring markets in time:

• Paleo-tourism • Astronomy • Birdwatching • Education/school group excursions • Special events • Fossicking • Eco-tourism • Hunting/fishing • Bush walking

International While international markets do not currently constitute a significant component of visitation to the Queensland Outback, there is opportunity for international market growth from the self-drive segment and the special interest niche segments from the long-haul source markets. New Zealand also presents a good opportunity for growth. Queensland Outback is also showing embryonic appeal to the international education markets. OQTA is committed to:

• Maximising growth opportunities for the Big Tour and Grand Tour markets as its ‘core’/grey nomad market.

• ‘Corridor Coastal’ marketing to attract short stay/family markets • Initiatives to tap the backpacker market through employment arrangers, TNT

Magazine with emphasis in Cairns and Brisbane. • Cooperative activities with campervan operators, such as Britz. • Targeted initiatives to attract the special interest segments detailed above.

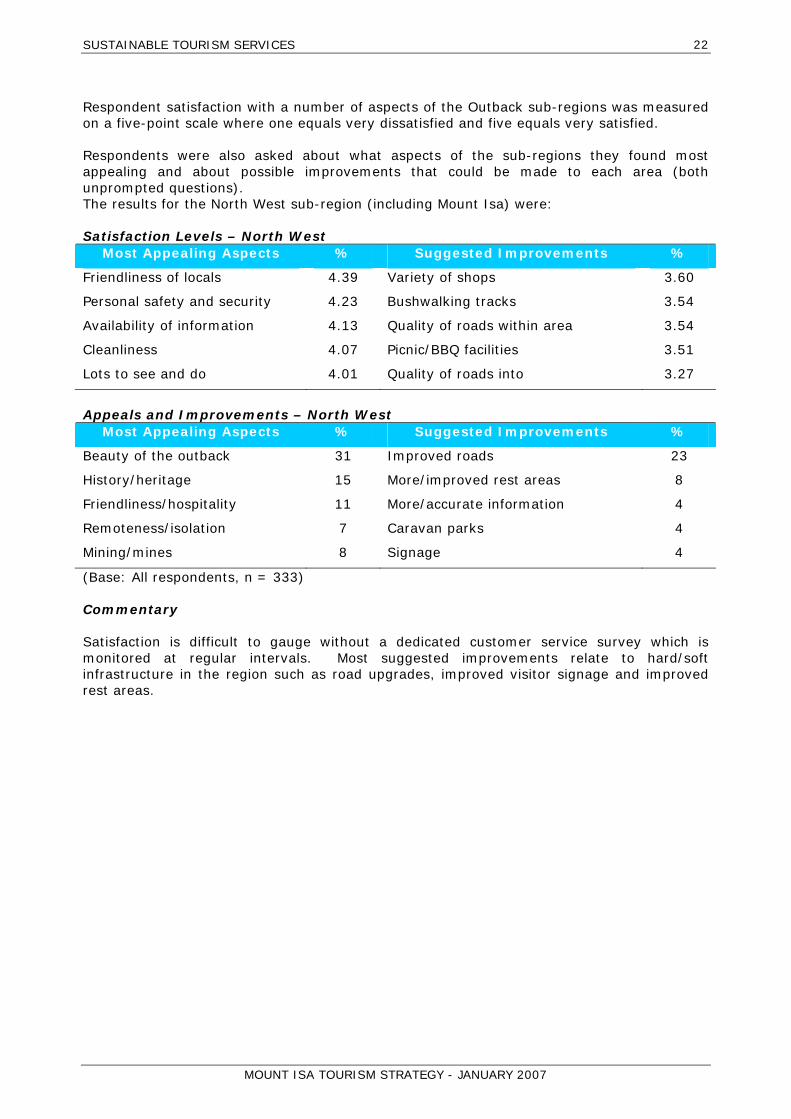

5.7 VISITOR SATISFACTION

Tourism Queensland has conducted the Standard Visitor Survey (SVS) in a range of areas throughout Queensland. The survey collects demographic data and information about the trip to/in the area. During the month of August 2002, a visitor survey was conducted in the three sub-regions of Queensland’s Outback (i.e. North West, Central West and South West). The data was collected by means of a self-completion questionnaire distributed to visitors at attractions and Visitor Information Centres throughout the regions. In total, 333 questionnaires were completed for the North West, 407 questionnaires for the Central West and 318 questionnaires for the South West.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

22

Respondent satisfaction with a number of aspects of the Outback sub-regions was measured on a five-point scale where one equals very dissatisfied and five equals very satisfied. Respondents were also asked about what aspects of the sub-regions they found most appealing and about possible improvements that could be made to each area (both unprompted questions). The results for the North West sub-region (including Mount Isa) were: Satisfaction Levels – North West

Most Appealing Aspects % Suggested Improvements %

Friendliness of locals 4.39 Variety of shops 3.60

Personal safety and security 4.23 Bushwalking tracks 3.54

Availability of information 4.13 Quality of roads within area 3.54

Cleanliness 4.07 Picnic/BBQ facilities 3.51

Lots to see and do 4.01 Quality of roads into 3.27

Appeals and Improvements – North West

Most Appealing Aspects % Suggested Improvements %

Beauty of the outback 31 Improved roads 23

History/heritage 15 More/improved rest areas 8

Friendliness/hospitality 11 More/accurate information 4

Remoteness/isolation 7 Caravan parks 4

Mining/mines 8 Signage 4

(Base: All respondents, n = 333) Commentary Satisfaction is difficult to gauge without a dedicated customer service survey which is monitored at regular intervals. Most suggested improvements relate to hard/soft infrastructure in the region such as road upgrades, improved visitor signage and improved rest areas.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

23

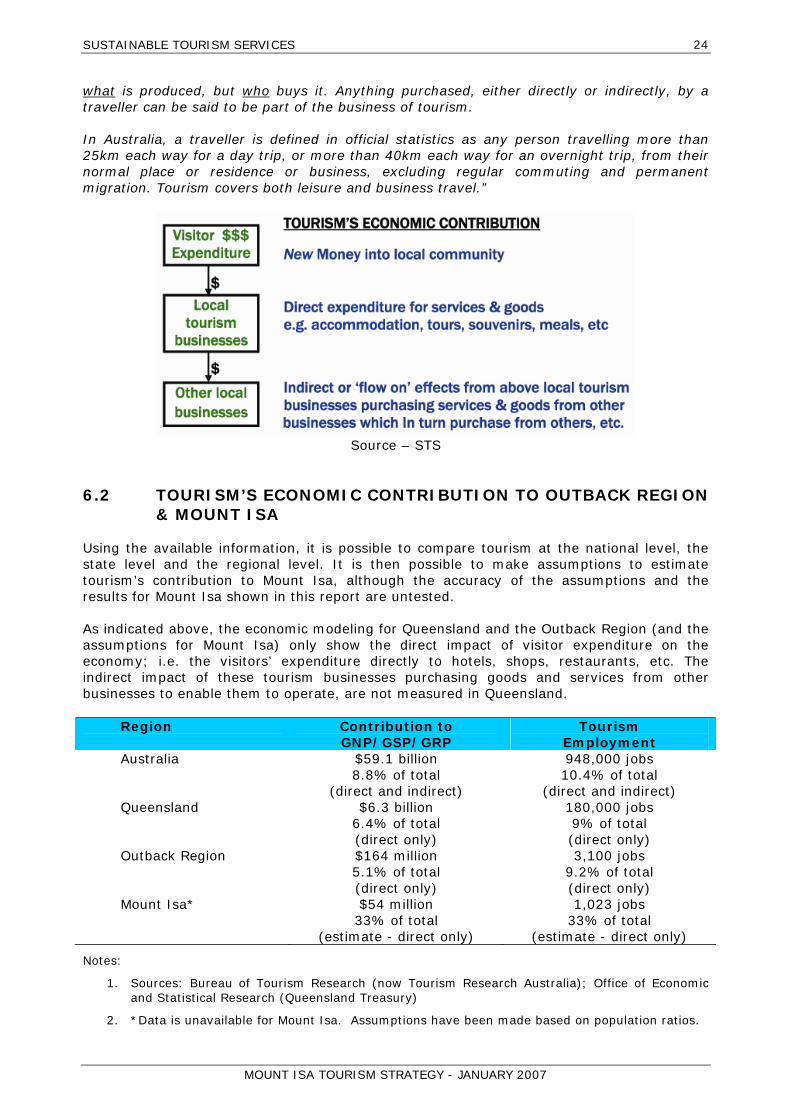

6.0 IMPORTANCE OF TOURISM TO MOUNT ISA

The MICC acknowledges that the local economy is underpinned by local and international major resource companies, with the pastoral industry and tourism being contributors. Whilst tourism is important to Mount Isa, there is no available data to measure exactly how important. One of the key issues identified in the Queensland Tourism Strategy and in local interviews was a general lack of understanding of the economic significance of the tourism industry and its relationship to other industry sectors and community development in general. The role of this section is to establish some context for the size of tourism in Outback Queensland in general, and Mount Isa in particular. This information is critical if tourism is to be taken seriously by other sections of the economy and to attract support from both big business and the community in the region and the City.

6.1 ESTIMATING TOURISM’S CONTRIBUTION TO AN ECONOMY

The Australian Bureau of Statistics (ABS) estimates the direct contribution of tourism to the national economy and employment in the Tourism Satellite Account (TSA). In 2002 the Bureau of Tourism Research (now Tourism Research Australia) stated that tourism’s total worth is greater than the direct contribution estimated by the TSA and they undertook further economic modeling to estimate the indirect effects as well. Their report indicated that for 2000/1 tourism directly contributed 4.7% GDP and indirectly contributed an additional 4.1%: estimating tourism’s total contribution to national GDP at 8.8%. It was also estimated that tourism’s direct contribution to national employment was 6% of total jobs and the indirect contribution added an additional 4.3% of all jobs, making a total of 10.4% of all jobs in Australia generated by visitors’ expenditure. These figures indicate that the direct economic contribution of tourism is only 50% of the total contribution; and for employment the direct contribution is only 60% of the total contribution (for Australia). In the tables below, the total effects (direct and indirect) are shown for Australia. Queensland Treasury’s Office of Economic and Statistical Research (OESR) also has an economic model which estimates the direct effects of tourism on the Queensland economy and employment. However there have been no studies undertaken to estimate tourism’s indirect effects in Queensland. In 2002, OESR estimated tourism’s contribution to each of the Regions in Queensland – again only for the direct contribution. Access Economics Pty Ltd in a 2002 report explained: “Tourism is not a conventional industry. Measuring its economic contribution properly and comprehensively requires a different approach. Conventional industries are defined, and their performance assessed, from a supply-side perspective. That is, the industry is classified by the goods and services it produces (such as meat, wool, coal, transport or health services), covering industry output, value-added, employment and the like. But tourism is a demand-side concept. The starting point is not

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

24

what is produced, but who buys it. Anything purchased, either directly or indirectly, by a traveller can be said to be part of the business of tourism. In Australia, a traveller is defined in official statistics as any person travelling more than 25km each way for a day trip, or more than 40km each way for an overnight trip, from their normal place or residence or business, excluding regular commuting and permanent migration. Tourism covers both leisure and business travel.”

Source – STS

6.2 TOURISM’S ECONOMIC CONTRIBUTION TO OUTBACK REGION & MOUNT ISA

Using the available information, it is possible to compare tourism at the national level, the state level and the regional level. It is then possible to make assumptions to estimate tourism’s contribution to Mount Isa, although the accuracy of the assumptions and the results for Mount Isa shown in this report are untested. As indicated above, the economic modeling for Queensland and the Outback Region (and the assumptions for Mount Isa) only show the direct impact of visitor expenditure on the economy; i.e. the visitors’ expenditure directly to hotels, shops, restaurants, etc. The indirect impact of these tourism businesses purchasing goods and services from other businesses to enable them to operate, are not measured in Queensland.

Region Contribution to GNP/GSP/GRP

Tourism Employment

Australia $59.1 billion 8.8% of total

(direct and indirect)

948,000 jobs 10.4% of total

(direct and indirect) Queensland $6.3 billion

6.4% of total (direct only)

180,000 jobs 9% of total (direct only)

Outback Region $164 million 5.1% of total (direct only)

3,100 jobs 9.2% of total (direct only)

Mount Isa* $54 million 33% of total

(estimate - direct only)

1,023 jobs 33% of total

(estimate - direct only)

Notes:

1. Sources: Bureau of Tourism Research (now Tourism Research Australia); Office of Economic and Statistical Research (Queensland Treasury)

2. *Data is unavailable for Mount Isa. Assumptions have been made based on population ratios.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

25

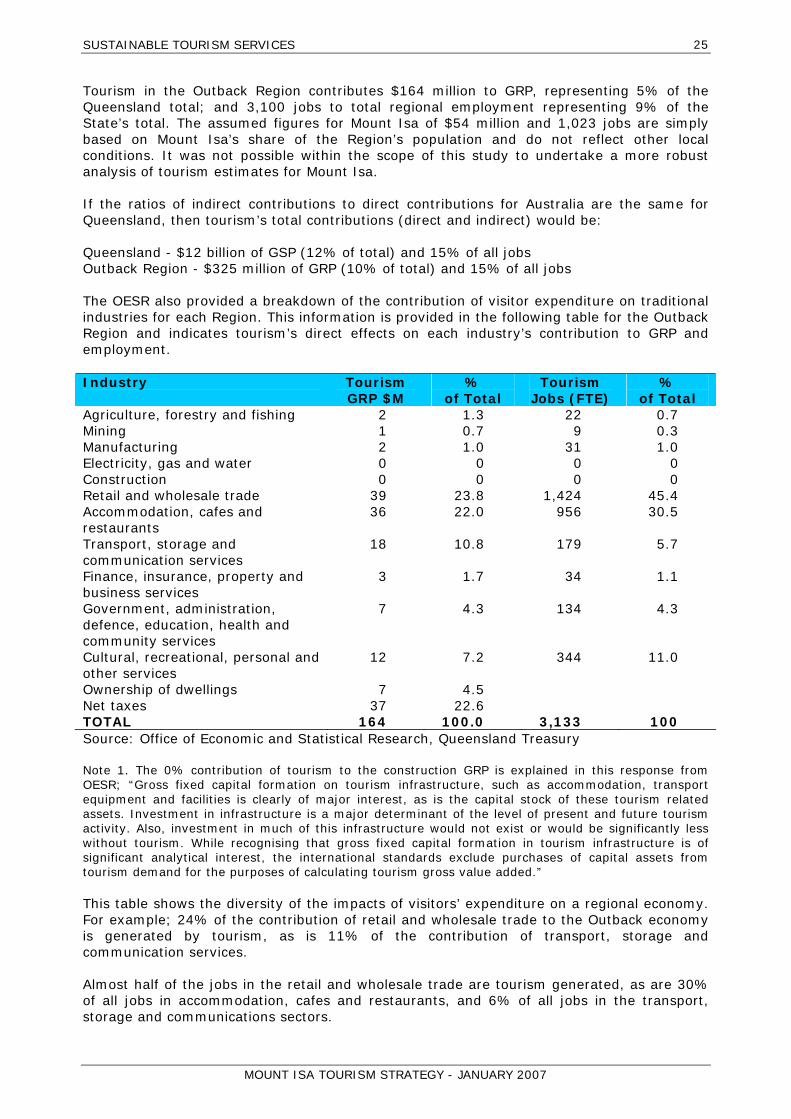

Tourism in the Outback Region contributes $164 million to GRP, representing 5% of the Queensland total; and 3,100 jobs to total regional employment representing 9% of the State’s total. The assumed figures for Mount Isa of $54 million and 1,023 jobs are simply based on Mount Isa’s share of the Region’s population and do not reflect other local conditions. It was not possible within the scope of this study to undertake a more robust analysis of tourism estimates for Mount Isa. If the ratios of indirect contributions to direct contributions for Australia are the same for Queensland, then tourism’s total contributions (direct and indirect) would be: Queensland - $12 billion of GSP (12% of total) and 15% of all jobs Outback Region - $325 million of GRP (10% of total) and 15% of all jobs The OESR also provided a breakdown of the contribution of visitor expenditure on traditional industries for each Region. This information is provided in the following table for the Outback Region and indicates tourism’s direct effects on each industry’s contribution to GRP and employment. Industry Tourism

GRP $M %

of Total Tourism

Jobs (FTE) %

of Total Agriculture, forestry and fishing 2 1.3 22 0.7 Mining 1 0.7 9 0.3 Manufacturing 2 1.0 31 1.0 Electricity, gas and water 0 0 0 0 Construction 0 0 0 0 Retail and wholesale trade 39 23.8 1,424 45.4 Accommodation, cafes and restaurants

36 22.0 956 30.5

Transport, storage and communication services

18 10.8 179 5.7

Finance, insurance, property and business services

3 1.7 34 1.1

Government, administration, defence, education, health and community services

7 4.3 134 4.3

Cultural, recreational, personal and other services

12 7.2 344 11.0

Ownership of dwellings 7 4.5 Net taxes 37 22.6 TOTAL 164 100.0 3,133 100 Source: Office of Economic and Statistical Research, Queensland Treasury Note 1. The 0% contribution of tourism to the construction GRP is explained in this response from OESR; “Gross fixed capital formation on tourism infrastructure, such as accommodation, transport equipment and facilities is clearly of major interest, as is the capital stock of these tourism related assets. Investment in infrastructure is a major determinant of the level of present and future tourism activity. Also, investment in much of this infrastructure would not exist or would be significantly less without tourism. While recognising that gross fixed capital formation in tourism infrastructure is of significant analytical interest, the international standards exclude purchases of capital assets from tourism demand for the purposes of calculating tourism gross value added.” This table shows the diversity of the impacts of visitors’ expenditure on a regional economy. For example; 24% of the contribution of retail and wholesale trade to the Outback economy is generated by tourism, as is 11% of the contribution of transport, storage and communication services. Almost half of the jobs in the retail and wholesale trade are tourism generated, as are 30% of all jobs in accommodation, cafes and restaurants, and 6% of all jobs in the transport, storage and communications sectors.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

26

Information is not available for Mount Isa specifically. However, the regional information will have some relevance to the local Mount Isa situation.

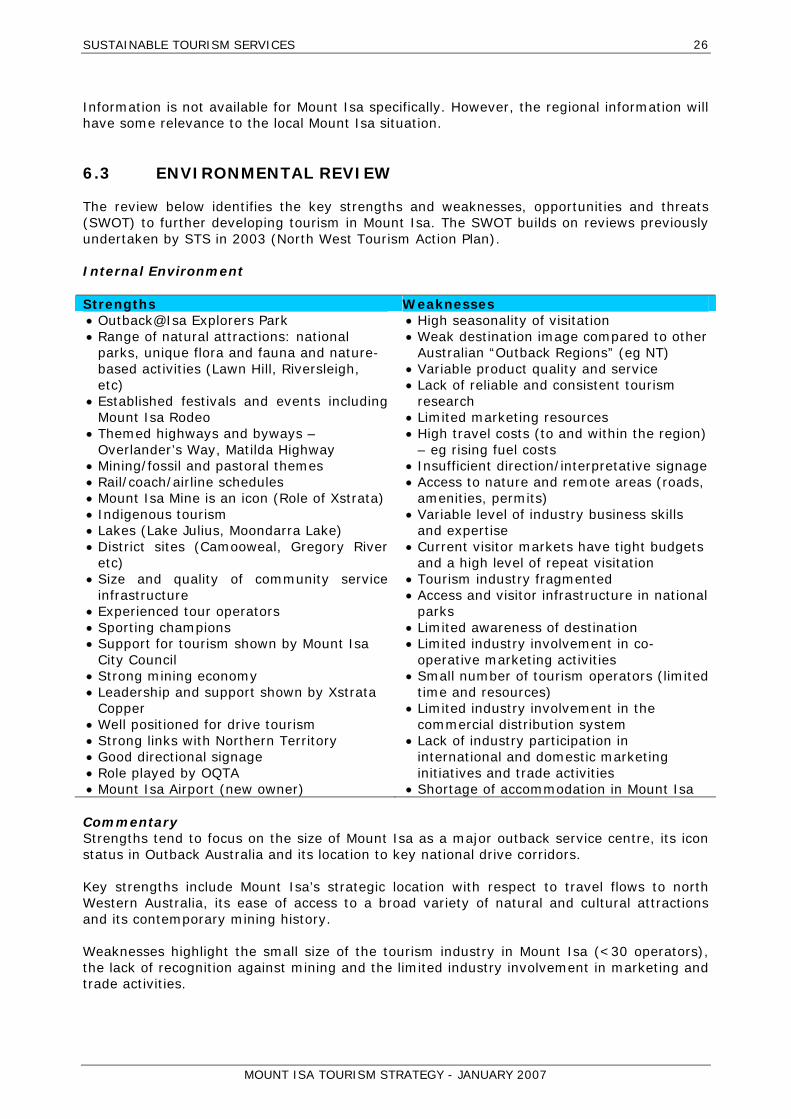

6.3 ENVIRONMENTAL REVIEW

The review below identifies the key strengths and weaknesses, opportunities and threats (SWOT) to further developing tourism in Mount Isa. The SWOT builds on reviews previously undertaken by STS in 2003 (North West Tourism Action Plan). Internal Environment Strengths Weaknesses • Outback@Isa Explorers Park • Range of natural attractions: national

parks, unique flora and fauna and nature-based activities (Lawn Hill, Riversleigh, etc)

• Established festivals and events including Mount Isa Rodeo

• Themed highways and byways – Overlander’s Way, Matilda Highway

• Mining/fossil and pastoral themes • Rail/coach/airline schedules • Mount Isa Mine is an icon (Role of Xstrata) • Indigenous tourism • Lakes (Lake Julius, Moondarra Lake) • District sites (Camooweal, Gregory River

etc) • Size and quality of community service

infrastructure • Experienced tour operators • Sporting champions • Support for tourism shown by Mount Isa

City Council • Strong mining economy • Leadership and support shown by Xstrata

Copper • Well positioned for drive tourism • Strong links with Northern Territory • Good directional signage • Role played by OQTA • Mount Isa Airport (new owner)

• High seasonality of visitation • Weak destination image compared to other

Australian “Outback Regions” (eg NT) • Variable product quality and service • Lack of reliable and consistent tourism

research • Limited marketing resources • High travel costs (to and within the region)

– eg rising fuel costs • Insufficient direction/interpretative signage • Access to nature and remote areas (roads,

amenities, permits) • Variable level of industry business skills

and expertise • Current visitor markets have tight budgets

and a high level of repeat visitation • Tourism industry fragmented • Access and visitor infrastructure in national

parks • Limited awareness of destination • Limited industry involvement in co-

operative marketing activities • Small number of tourism operators (limited

time and resources) • Limited industry involvement in the

commercial distribution system • Lack of industry participation in

international and domestic marketing initiatives and trade activities

• Shortage of accommodation in Mount Isa Commentary Strengths tend to focus on the size of Mount Isa as a major outback service centre, its icon status in Outback Australia and its location to key national drive corridors. Key strengths include Mount Isa’s strategic location with respect to travel flows to north Western Australia, its ease of access to a broad variety of natural and cultural attractions and its contemporary mining history. Weaknesses highlight the small size of the tourism industry in Mount Isa (<30 operators), the lack of recognition against mining and the limited industry involvement in marketing and trade activities.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

27

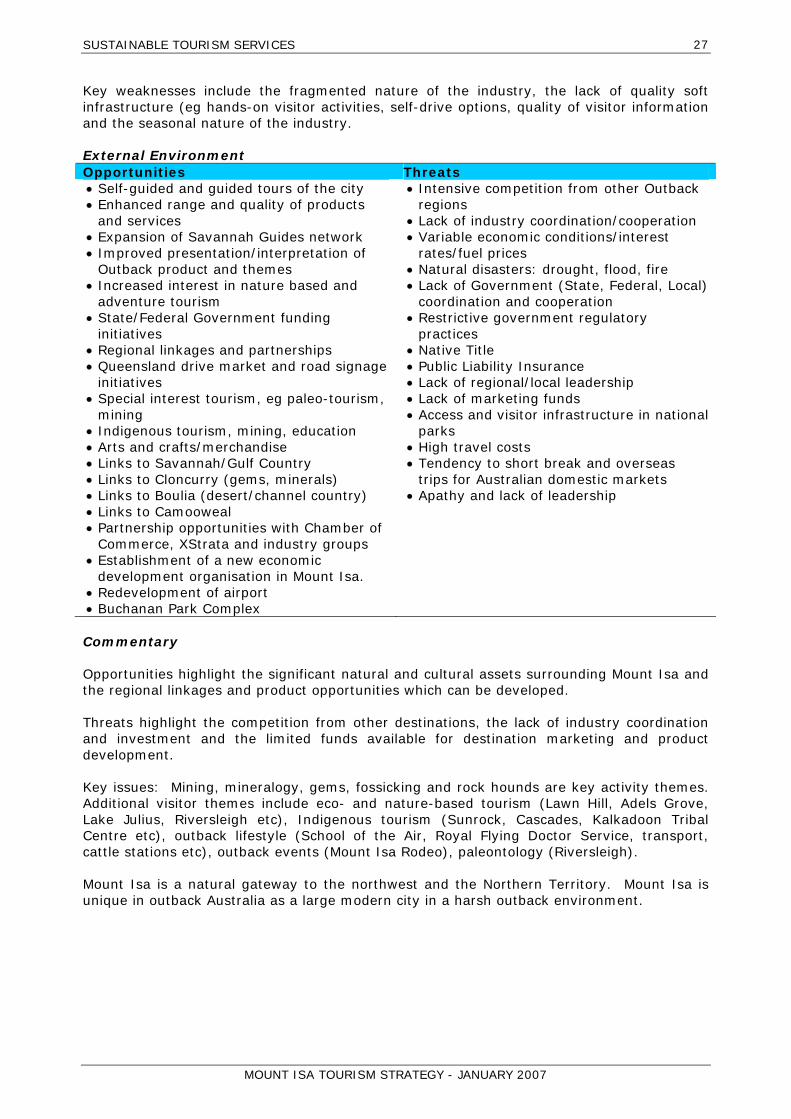

Key weaknesses include the fragmented nature of the industry, the lack of quality soft infrastructure (eg hands-on visitor activities, self-drive options, quality of visitor information and the seasonal nature of the industry. External Environment Opportunities Threats • Self-guided and guided tours of the city • Enhanced range and quality of products

and services • Expansion of Savannah Guides network • Improved presentation/interpretation of

Outback product and themes • Increased interest in nature based and

adventure tourism • State/Federal Government funding

initiatives • Regional linkages and partnerships • Queensland drive market and road signage

initiatives • Special interest tourism, eg paleo-tourism,

mining • Indigenous tourism, mining, education • Arts and crafts/merchandise • Links to Savannah/Gulf Country • Links to Cloncurry (gems, minerals) • Links to Boulia (desert/channel country) • Links to Camooweal • Partnership opportunities with Chamber of

Commerce, XStrata and industry groups • Establishment of a new economic

development organisation in Mount Isa. • Redevelopment of airport • Buchanan Park Complex

• Intensive competition from other Outback regions

• Lack of industry coordination/cooperation • Variable economic conditions/interest

rates/fuel prices • Natural disasters: drought, flood, fire • Lack of Government (State, Federal, Local)

coordination and cooperation • Restrictive government regulatory

practices • Native Title • Public Liability Insurance • Lack of regional/local leadership • Lack of marketing funds • Access and visitor infrastructure in national

parks • High travel costs • Tendency to short break and overseas

trips for Australian domestic markets • Apathy and lack of leadership

Commentary Opportunities highlight the significant natural and cultural assets surrounding Mount Isa and the regional linkages and product opportunities which can be developed. Threats highlight the competition from other destinations, the lack of industry coordination and investment and the limited funds available for destination marketing and product development. Key issues: Mining, mineralogy, gems, fossicking and rock hounds are key activity themes. Additional visitor themes include eco- and nature-based tourism (Lawn Hill, Adels Grove, Lake Julius, Riversleigh etc), Indigenous tourism (Sunrock, Cascades, Kalkadoon Tribal Centre etc), outback lifestyle (School of the Air, Royal Flying Doctor Service, transport, cattle stations etc), outback events (Mount Isa Rodeo), paleontology (Riversleigh). Mount Isa is a natural gateway to the northwest and the Northern Territory. Mount Isa is unique in outback Australia as a large modern city in a harsh outback environment.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

28

7.0 COMMUNITY AND INDUSTRY FEEDBACK

7.1 STAKEHOLDER FEEDBACK AND COMMENT

In addition to the project objectives outlined in Section 2.2, a further range of issues and desired outcomes were identified in the various meetings and workshops. Outlined below is an executive overview of key feedback received from workshops and interviews. Where possible, comments have been grouped under themed headings. Coordination

• There is a general lack of coordination in tourism marketing and promotional activities in Mount Isa. The major concern was the lack of a dedicated resource (staff member) to take forward initiatives on behalf of local operators.

Additional concerns included:

• The important role played by Council in providing continued financial support for tourism marketing and product development.

• The need for a more strategic approach to how tourism is promoted across the region.

• The limited financial and human resources available to MITA. • Tourism in Mount Isa does not have a dedicated point of contact. • The need for new leadership from business operators in the city (more people

‘putting up their hands’). • The importance of having an organisation with the skills and services to address and

take forward economic development issues for Mount Isa. • The need for a full time tourism resource to action initiatives.

Awareness/Destination Marketing There is a need to address the following issues:

• There is no effective brand or consistent promotional message for Mount Isa tourism. • Tourism promotion and marketing needs more effective coordination.

Product Development

• More product development is needed to provide opportunities for things to do and see around the city. This includes day trips (half day and full day) to surrounding attractions.

• It was also recognised that both soft and hard visitor infrastructure was needed. This includes suitable accommodation, caravan parks, signage, brochures, maps and visitor collateral

• Mining and the history of mining should be the main theme for Mount Isa. Partnerships/Linkages

• The significance of Mount Isa as the ‘Capital of Outback Queensland’ was recognised. Links and partnerships need to be made with the Northern Territory, the Gulf Savannah, the North West and strategic marketing initiatives such as the Overlander’s Way and the Matilda Highway.

• Further industry funding contributions to tourism promotion and marketing was needed.

• There are no champions pushing tourism in the local community. • There is a need for Council, tourism industry and general business community to

work together. A model which only includes tourism operators will not work. • There is an opportunity to establish a strong sense of unity and cooperation with the

Chamber of Commerce. There are an insufficient number of businesses and services within the city to support different associations.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

29

• Mount Isa needs a well resourced and supported local business organisation with a strong relationship with OQTA and strong links with Tourism Queensland and Tourism Australia.

Building a Profitable and Sustainable Tourism Industry

• The need to develop viable and profitable local businesses was considered as part of this project. Stakeholders agreed that while it was important to grow visitor numbers it was just an important to improve yield and return from visitors

• The need to establish partnerships with stakeholders such as the Chamber of Commerce was noted. It was agreed that the natural synergy which existed between both organisations should be explored. It was also noted that some ongoing education on the role that tourism played in business development needed to be addressed

Market Segmentation

• It is acknowledged that different products and service infrastructure were needed to service the needs of the different visitor markets to Mount Isa.

Implementation

• It was recognised that any plan for Mount Isa needed an implementation schedule to guide actions over a five to ten year period

• There was a general view that improvements could and should be made to the existing tourism delivery model and that it would require fundamental change to take advantage of the opportunities available, rather than tinkering at the edges. The point was also made that any significant changes would need to be phased in to allow all stakeholders to adjust and adapt

• A more complete description of the feedback obtained from the various individual meetings with stakeholders, is included in Appendix C.

7.2 UNDERSTANDING OF TOURISM WITHIN MOUNT ISA

Whilst no studies on this matter were undertaken for this project, it was the opinion of all persons interviewed, that tourism is not well understood within the Isa – by the resident and business communities and by some Councillors and staff. This view was supported by the observations of the STS team working on the project. Part of the reason is that there is a paucity of information available. This situation is not unique to Mount Isa. There is very little good data available on the economic contribution of tourism to all local areas in Australia. It is very difficult for Councillors, Council staff and the community to understand and appreciate tourism’s real contribution without good economic data and effective communication.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

30

8.0 CURRENT DELIVERY MODEL FOR MOUNT ISA TOURISM

8.1 OVERVIEW

The tourism industry in The Isa is characterised by a small number of very small businesses. It is estimated that the number of tourism operators providing services directly to visitors is less than 30 in total. There are no large private sector companies directly involved in tourism, based in Mount Isa. Tourism is seasonal, with seventy percent (64%) of all visitors arriving and departing between the months of April and September – 65% of domestic visitors and 46% of international visitors. Prior to 1994, Mount Isa was a major component of the Inland Tourism Region, one of the official RTOs of Queensland. The Shires of Cloncurry, McKinlay, Richmond and Flinders were also part of the Inland Tourism Region. There was an Inland RTO office in the Isa with full time staff. In 1994, this region was amalgamated with the Outback Region, and initially a local office and staff remained in Mount Isa. However in 1999, this office was closed as part of a major restructuring of the Outback Region administration and all staff was moved into one new office in Brisbane. Since that time, there has been no dedicated tourism resources in Mount Isa and the local tourism industry have struggled to maintain effective, coordinated marketing activities for the Shire. MICC filled the gap to some extent by dedicating council staff to coordinate marketing activities for the Shire. In addition to this role, council staff also managed the Riversleigh Centre, a local tourism attraction owned by Council. In 2003, with the impending opening of the new Council owned Outback at Isa tourism development, which included the Riversleigh Centre, Council took the decision to disband its own tourism unit and hand the role of marketing and promotion of Mount Isa to the new Board of Outback at Isa. This created a conflict for the Outback at Isa Board who were unwilling to assume the responsibility for overall promotion of Mount Isa in addition to their specific responsibilities for the Outback at Isa Centre. The local Mount Isa Tourism Association (MITA) has an active committee, but no staff. It has approximately 50 members who pay an annual membership fee. Total membership is approximately $7,000 per annum. It is now the principal body for promotion of Mount Isa, albeit with very limited resources. Mount Isa is part of the Outback Queensland Tourism Authority, the official Regional Tourism Organisation for the majority of Western Queensland. MICC pays a significant annual membership fee each year which is based on a population formula for each of the shires in the Outback Region. OQTA is supported by Tourism Queensland and is the main conduit for Outback Tourism Region members to participate in cooperative marketing activities with TQ. Currently, when there is a cooperative opportunity for the State’s tourism regions, TQ contacts OQTA who in turn contact each of their Shire members. In the case of Mount Isa, the contact is MITA. MITA then contact MICC to seek their support for matching funding to participate in each activity. Such activities include advertising, trade and consumer shows and brochures and collateral. As the funding from MITA and its members is minimal, many promotional opportunities are not taken up.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

31

8.2 THE ROLE OF MOUNT ISA CITY COUNCIL

The position adopted by MICC in 2003 is that the organisation of tourism activities, including marketing and product development, is principally the role of the local industry. It supports the local industry with promotional activities as indicated above, and facilitates the publication of a local visitors’ guide; which is produced by a commercial company at little or no cost to Council. Council funds some of the distribution costs for the guide. Council also contributes to promotional activities for the Overlander’s Way with the other Shires in the North West sub-region. In recent years, MICC has taken an active role in the development of infrastructure and facilities which increase Mount Isa’s tourism appeal. Besides the Outback at Isa Centre, a new $16 million Rodeo Centre and associated facilities is under construction at Buchanan Park, adjacent to the city area. When completed, this will be a very significant addition to tourism infrastructure at Mount Isa.

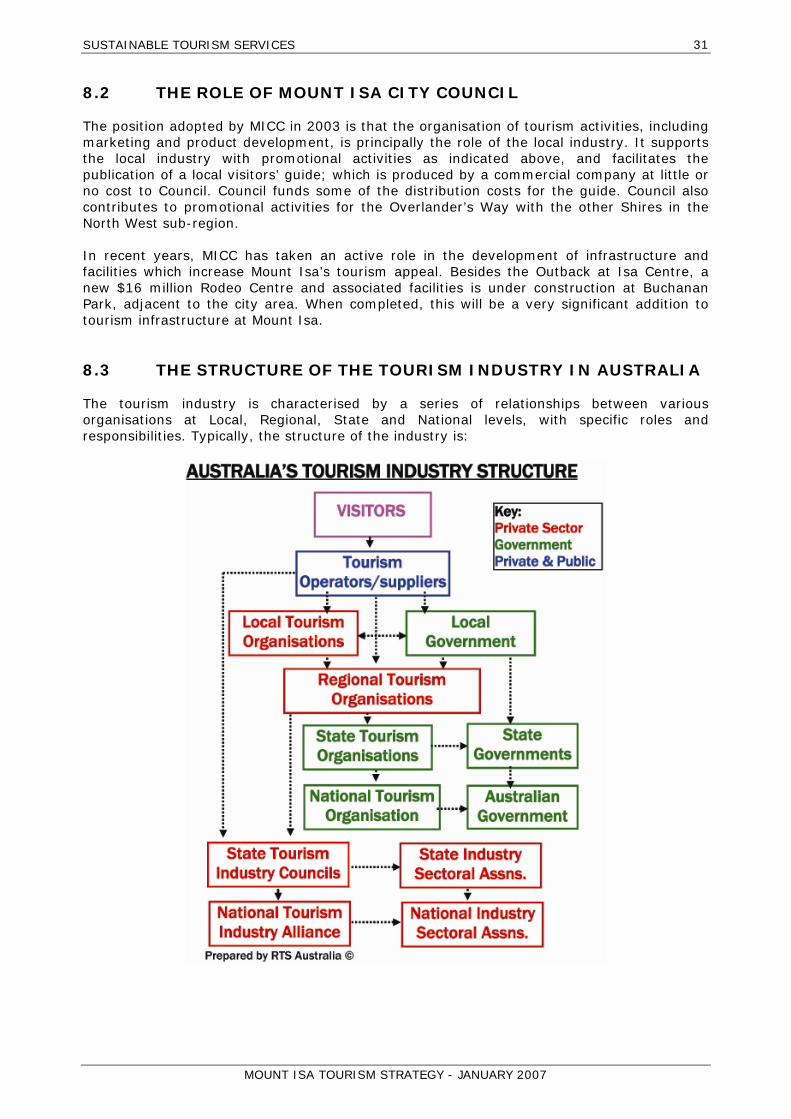

8.3 THE STRUCTURE OF THE TOURISM INDUSTRY IN AUSTRALIA

The tourism industry is characterised by a series of relationships between various organisations at Local, Regional, State and National levels, with specific roles and responsibilities. Typically, the structure of the industry is:

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

32

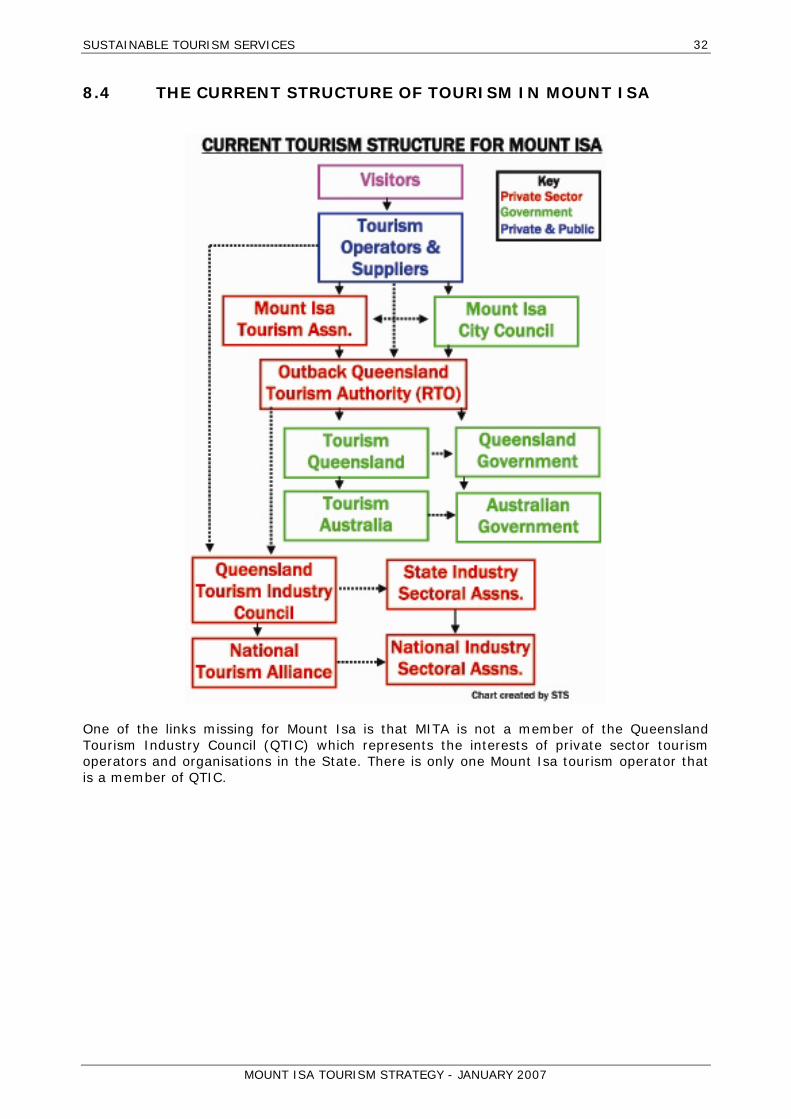

8.4 THE CURRENT STRUCTURE OF TOURISM IN MOUNT ISA

One of the links missing for Mount Isa is that MITA is not a member of the Queensland Tourism Industry Council (QTIC) which represents the interests of private sector tourism operators and organisations in the State. There is only one Mount Isa tourism operator that is a member of QTIC.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

33

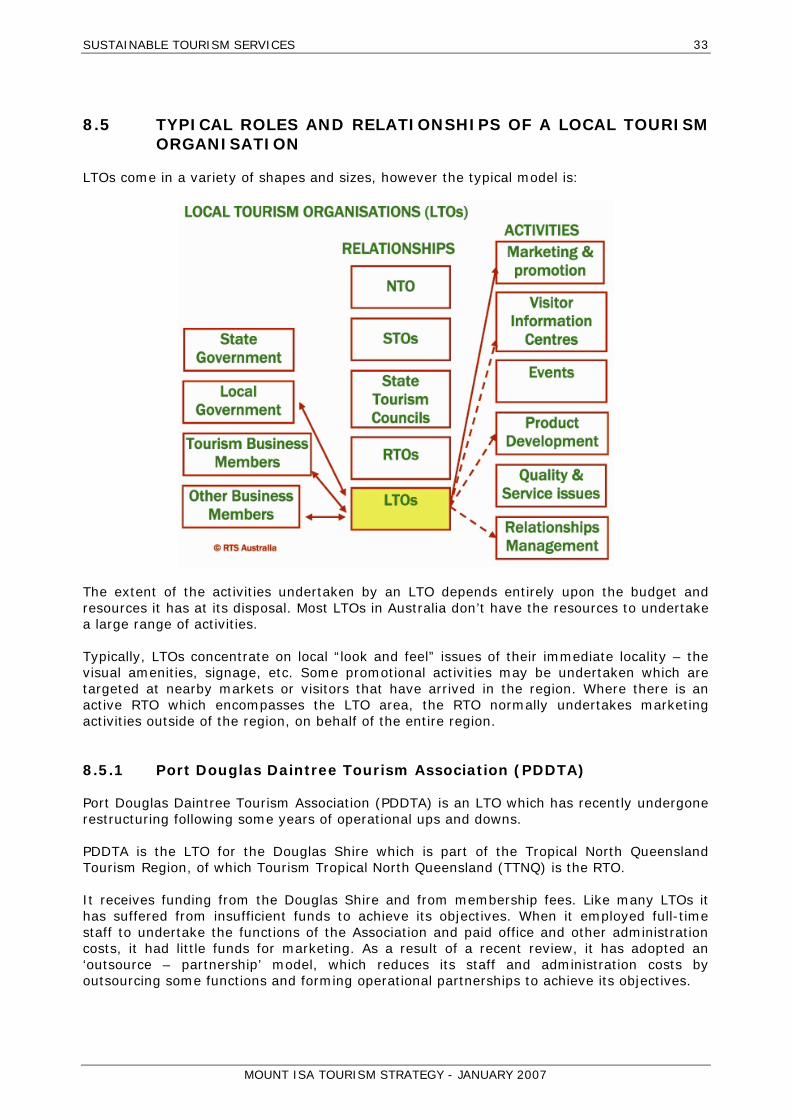

8.5 TYPICAL ROLES AND RELATIONSHIPS OF A LOCAL TOURISM ORGANISATION

LTOs come in a variety of shapes and sizes, however the typical model is:

The extent of the activities undertaken by an LTO depends entirely upon the budget and resources it has at its disposal. Most LTOs in Australia don’t have the resources to undertake a large range of activities. Typically, LTOs concentrate on local “look and feel” issues of their immediate locality – the visual amenities, signage, etc. Some promotional activities may be undertaken which are targeted at nearby markets or visitors that have arrived in the region. Where there is an active RTO which encompasses the LTO area, the RTO normally undertakes marketing activities outside of the region, on behalf of the entire region.

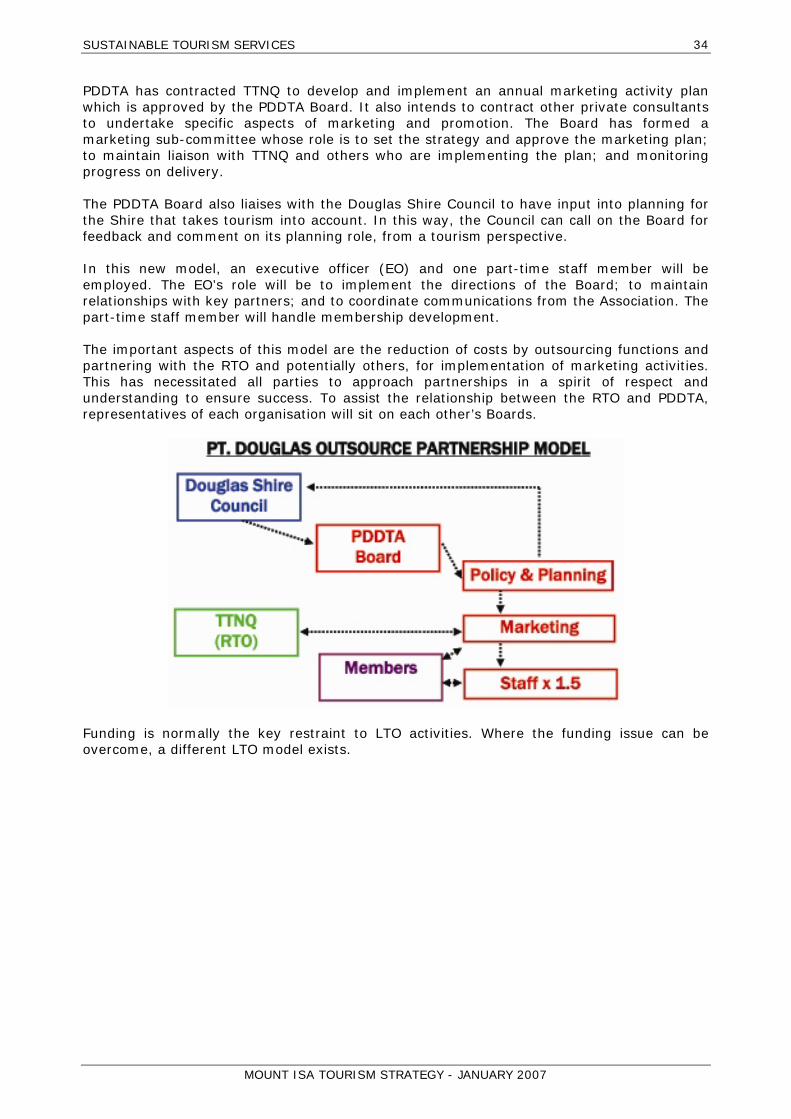

8.5.1 Port Douglas Daintree Tourism Association (PDDTA)

Port Douglas Daintree Tourism Association (PDDTA) is an LTO which has recently undergone restructuring following some years of operational ups and downs. PDDTA is the LTO for the Douglas Shire which is part of the Tropical North Queensland Tourism Region, of which Tourism Tropical North Queensland (TTNQ) is the RTO. It receives funding from the Douglas Shire and from membership fees. Like many LTOs it has suffered from insufficient funds to achieve its objectives. When it employed full-time staff to undertake the functions of the Association and paid office and other administration costs, it had little funds for marketing. As a result of a recent review, it has adopted an ‘outsource – partnership’ model, which reduces its staff and administration costs by outsourcing some functions and forming operational partnerships to achieve its objectives.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

34

PDDTA has contracted TTNQ to develop and implement an annual marketing activity plan which is approved by the PDDTA Board. It also intends to contract other private consultants to undertake specific aspects of marketing and promotion. The Board has formed a marketing sub-committee whose role is to set the strategy and approve the marketing plan; to maintain liaison with TTNQ and others who are implementing the plan; and monitoring progress on delivery.

The PDDTA Board also liaises with the Douglas Shire Council to have input into planning for the Shire that takes tourism into account. In this way, the Council can call on the Board for feedback and comment on its planning role, from a tourism perspective. In this new model, an executive officer (EO) and one part-time staff member will be employed. The EO’s role will be to implement the directions of the Board; to maintain relationships with key partners; and to coordinate communications from the Association. The part-time staff member will handle membership development. The important aspects of this model are the reduction of costs by outsourcing functions and partnering with the RTO and potentially others, for implementation of marketing activities. This has necessitated all parties to approach partnerships in a spirit of respect and understanding to ensure success. To assist the relationship between the RTO and PDDTA, representatives of each organisation will sit on each other’s Boards.

Funding is normally the key restraint to LTO activities. Where the funding issue can be overcome, a different LTO model exists.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007

35

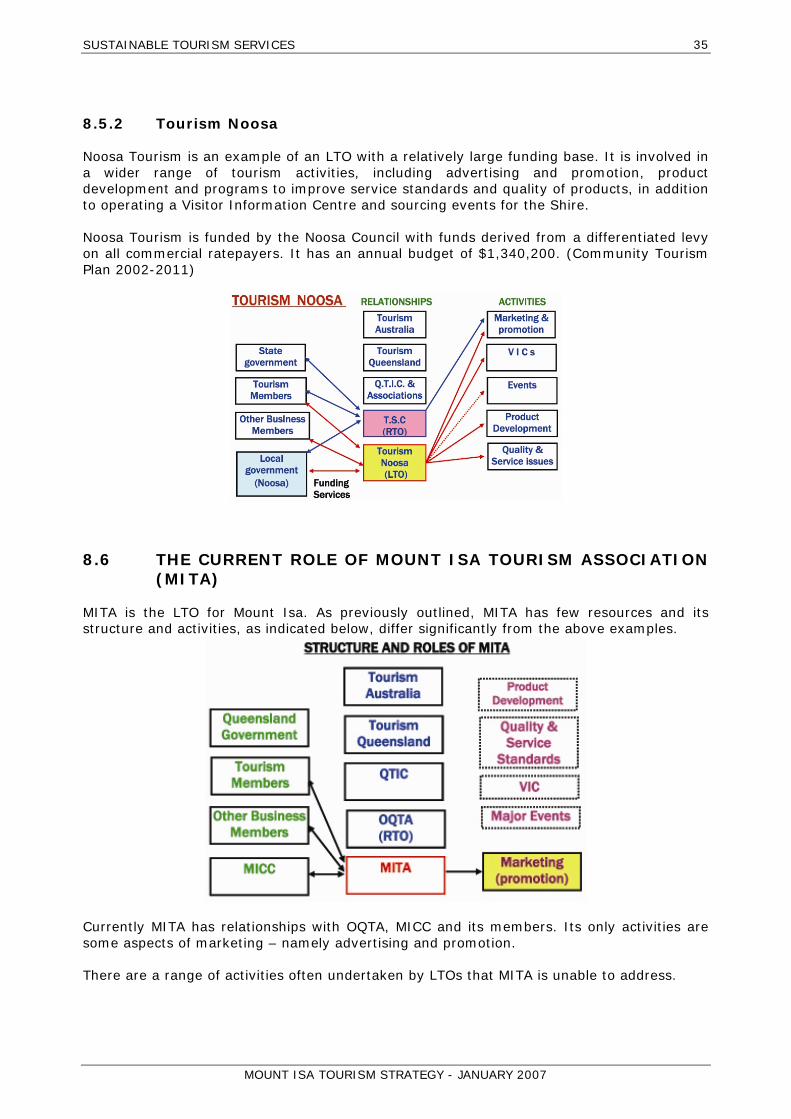

8.5.2 Tourism Noosa

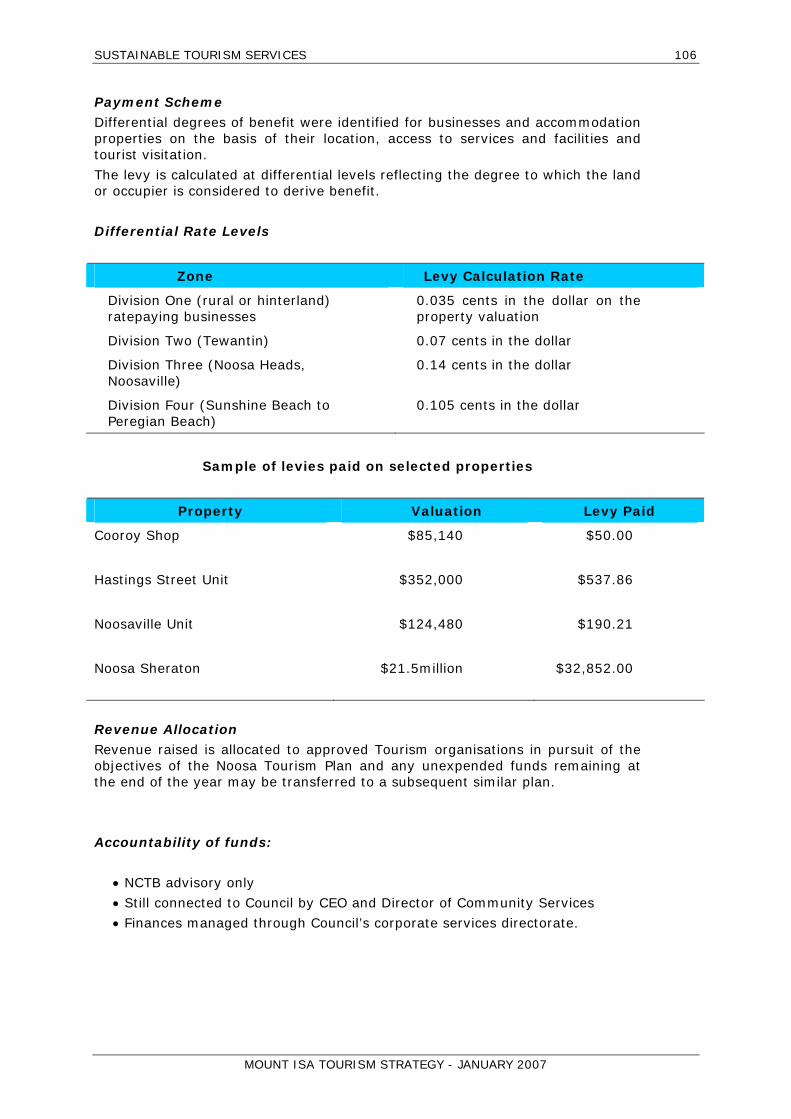

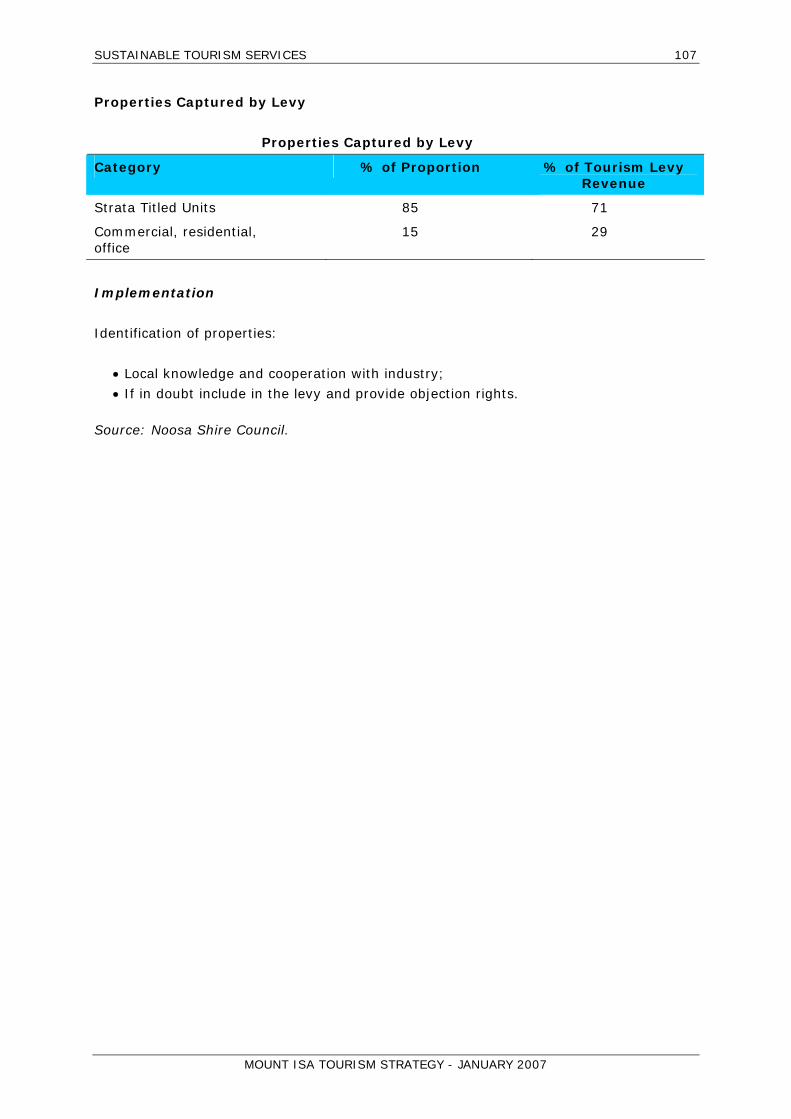

Noosa Tourism is an example of an LTO with a relatively large funding base. It is involved in a wider range of tourism activities, including advertising and promotion, product development and programs to improve service standards and quality of products, in addition to operating a Visitor Information Centre and sourcing events for the Shire. Noosa Tourism is funded by the Noosa Council with funds derived from a differentiated levy on all commercial ratepayers. It has an annual budget of $1,340,200. (Community Tourism Plan 2002-2011)

8.6 THE CURRENT ROLE OF MOUNT ISA TOURISM ASSOCIATION (MITA)

MITA is the LTO for Mount Isa. As previously outlined, MITA has few resources and its structure and activities, as indicated below, differ significantly from the above examples.

Currently MITA has relationships with OQTA, MICC and its members. Its only activities are some aspects of marketing – namely advertising and promotion. There are a range of activities often undertaken by LTOs that MITA is unable to address.

SUSTAINABLE TOURISM SERVICES

MOUNT ISA TOURISM STRATEGY - JANUARY 2007