Mortgage Planning Guidemymortgageguydan.com/wp-content/uploads/2010/09/Dan... · 2017. 9. 12. ·...

20

Mortgage Planning Guide We Are Mortgage Planners We’ve developed a special process that simplifies getting approved for a home loan. Our unique Mortgage Planning Philosophy educates our clients on the ins-and-outs of the mortgage process, as well as explaining the total costs of ALL your options. Our vision is to guide you through the home buying process from start to finish so that you can make a SMART home purchase! “We work with FAMILIES, not files.” - Dan Keller Dan Keller Mortgage Advisor - MLO #115349 Direct: 425-350-7136 Office: 425-947-8533 [email protected] 12220 113th Ave NE Suite 120 Kirkland, WA 98034 As Seen On 2009—2014 Host of Seale Real Estate Radio

Transcript of Mortgage Planning Guidemymortgageguydan.com/wp-content/uploads/2010/09/Dan... · 2017. 9. 12. ·...

Mortgage Planning Guide

We Are Mortgage Planners

We’ve developed a special process that

simplifies getting approved for a home loan.

Our unique Mortgage Planning Philosophy educates our clients

on the ins-and-outs of the mortgage process, as well as

explaining the total costs of ALL your options.

Our vision is to guide you through the home buying

process from start to finish so that you can make a

SMART home purchase!

“We work with FAMILIES, not files.” - Dan Keller

Dan Keller Mortgage Advisor - MLO #115349

Direct: 425-350-7136 Office: 425-947-8533

12220 113th Ave NE Suite 120

Kirkland, WA 98034

As Seen On

2009—2014

Host of Sea�le Real Estate Radio

MORTGAGE TIMELINE SUNDAY WEDNESDAY MONDAY

APPLY FOR LOAN

Meet with your Dan

Keller to complete

your loan applica-

#on. Provide the

items listed on the

“What Items Are

Needed” handout.

TUESDAY FRIDAY THURSDAY SATURDAY

YOU’RE APPROVED

Congratula#ons!

Your loan is pre-

approved. The pre-

approval le�er will

be sent to you and

your agent.

YOU FOUND IT

Find the perfect

home and make an

offer.

OFFER ACCEPTED

Your agent will

forward the

Earnest Money

Agreement (sales

contract) to your

lender for review.

HOME INSPECTION

It’s #me to order

the home

inspec#on. Your

agent may have a

good referral if you

need one.

LOCK THAT LOAN

If you have not

discussed locking in

a rate with Dan

Keller, now is a

good #me to do so.

GREAT NEWS

The home

inspec#on is

complete.

Nego#ate any

necessary repairs

with the seller.

APPRAISAL

It’s #me for your

lender (Dan’s

Team) to order the

appraisal.

APPRAISER VISIT

The appraiser will

provide a property

value based on

comparable home

sales in the

neighborhood.

HOME INSURANCE

Contact a home-

owner’s insurance

agent and secure a

quote for the

premium.

APPRAISAL DONE

The appraisal will

be sent to Dan’s

Team for review.

MISSING ITEMS

Underwri#ng will

request any

missing items that

may be needed for

final loan approval.

FINAL REVIEW

The appraisal and

all updated income

and asset

documents will be

reviewed by the

underwriter.

FINAL APPROVAL

You receive final

loan approval!

Your lender will

now order loan

documents and

send them to the

#tle company.

TITLE COMPANY

The #tle company

will work up your

final “cash to

close” numbers

and schedule a

#me for you to

sign your loan

CASHIER’S CHECK

You will bring any

addi#onal required

funds to the sign-

ing in the form of a

cashier’s check.

You will sign loan

documents at the

#tle company.

CONGRATULATIONS

Your loan funds and

the mortgage is

recorded. You are

now a homeowner!

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

Your First Mortgage Payment

Once your loan funds, you will have between 30-60 days before your first payment is due. For example, a loan that funds September 18th will have a first payment due date of November 1st.

THE DAN KELLER Mortgage Planning Playbook

Hello! My name is Dan Keller. I am a residential mortgage

advisor, speaker, and writer (ok fine, blogger).

I’ve been originating mortgages since 2008, and have built my

mortgage practice upon Ken Blanchard’s book, “Raving Fans”.

The idea behind the book, “Ravings Fans” is to find out exactly

what your clients are looking for, and deliver above their

expectations. That is my goal—Every client gets our BEST!

What I’ve found over the years is that buying a home is the larg-

est financial transaction one will ever make, and therefore it’s

important that you integrate your mortgage decision into your

short-term and long-term financial goals.

What you’re about to see in in this Mortgage Planning Playbook is a formula I’ve created for

providing both a Raving Fans mortgage experience and the peace of mind that comes with

making an educated financial decision!

Who Is Dan Keller?

I’m a husband to Jenny. I’m a father to Ally and Hudson.

My family is everything to me. When I am not serving my clients

in the office, I am spending time on the Puget Sound fishing with

my son or vacationing to Lake Chelan with my family.

One of my favorite hobbies is supporting my wife’s business,

Jenny Cookies, or “baker to the stars”> www.Jennycookies.com

As a former college professor, I enjoy speaking and teaching on

the topics of mortgage, real estate and Dave Ramsey’s Financial

Peace Program.

I graduated with a Master's Degree from E. Washington Univ. in

2000, and was a collegiate all-American baseball player in 1998.

Yes, I like baseball... A lot.

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

THE DAN KELLER Mortgage Planning Playbook

The Dan Keller Team’s Service Commitment The Power of Teamwork

My mentor and one of the brightest men to ever walk this Earth, Jim Rohn once said, “You are

the average of the people you spend the most amount of time with.”

That is why I have spent the last couple of years growing my mortgage practice with these two

great people and the operations team at New American Funding!

Who Is Brie Sidener? She’s our Production

Manager and she is a 13-year veteran loan processor/loan officer

assistant to top producing loan officers. Since 2012, she has been

recognized as one of the top loan processors in the Puget Sound!

Brie will be your main point of contact after I have structured your

mortgage. She helps with securing your mortgage pre-approval and

navigates you into processing & underwriting.

Who Is Jason Hoskins? Jason is my

Production Partner and a veteran customer service

manager in the mortgage and auto sale industries.

Jason’s primary role is to assist you in gathering your initial loan

docs and prepare them for me to evaluate. He will also schedule

your mortgage planning meeting with me, while keeping both you

and your realtor proactively updated throughout the loan pre-

approval/home shopping stage.

Jason is a husband and father of two; and one of the most

customer-service focused individuals you’ll ever meet!

Brie’s primary role is to assist in pre-underwriting and processing your

loan pre-approval. Additionally, she will proactively keep you and your

Realtor updated throughout the loan process. Brie is famous for her detailed “Friday Status Up-

dates” that she sends to ALL parties! Brie completely understands the Raving Fans approach

to customer service, in fact, that is what makes her a champion!

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

Dan.Keller

Highlight

THE DAN KELLER Mortgage Planning Playbook

Items Necessary to Process Your Loan

We are genuinely interested in helping you obtain the financing necessary to acquire the home you

have selected or to refinance your current home without delay.

In order to expedite the processing of your loan, we request that you scan or fax the following items

to us for review within 24-hours of completing the secure online application.

� Pay stubs covering the most recent one month period (must be payroll or computer

generated and show the YTD earnings and deductions)

� W2s for the most recent two years

� 1040s (Personal Federal Tax Returns) for the most recent two years. All pages

(schedules) please.

� Photo copy of a valid U.S. picture ID (or bring the ID with you to your appointment for

photocopying)

� Bank statements for the most recent two months for all checking and savings accounts.

All pages please, must reference acct # and name.

� Asset account statements (IRA, 401K, investment accounts, etc.) for the most recent

two months

� Copy of your current lease agreement (if renting) or copy of mortgage statement (if you

have mortgages. Please provide a list of ALL properties owned.

If applicable:

� Bankruptcy papers (including all pages and discharge paperwork)

� Divorce decree or child support court order

If self-employed:

� Business Tax Returns for the most recent two years

� CPA letter documenting minimum two years of self-employment with positive continued

outlook for business.

� Business licenses for most recent two years

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

THE DAN KELLER Mortgage Planning Playbook

These DOs and DON’Ts will help avoid any delays with your loan approval.

Tips For a Smooth Loan Approval

MOST IMPORTANTLY: DO NOT GIVE YOUR SSN OUT FOR THE NEXT 30 DAYS!

DO continue making your mortgage or rent payments on time

DO stay current on all existing accounts (even if you’re paying them off)

DO continue to work for the same employer

DO continue to use the same insurance company

DO continue living at your current residence

DO continue to use your credit cards as normal

DO call us if you have ANY questions

DON’T make a major purchase (car, boat, furniture, jewelry, etc.)

DON’T apply for new credit (even if you’re pre-approved)

DON’T open a new credit card

DON’T transfer any balances from one account to another

DON’T pay off any collections or accounts without first consulting us

DON’T close any credit card accounts

DON’T change bank accounts or banks

DON’T max out or overcharge your credit cards

DON’T consolidate your debt onto fewer credit accounts

DON’T take out a new loan

DON’T start any home improvement projects

DON’T finance any elective medical procedure

DON’T open a new cell phone account

DON’T join a fitness club

If you encounter a special situation, it is best to mention it to us right away so we can help you determine the best way to handle it in order to achieve your financial goals.

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

Dan.Keller

Highlight

Dan.Keller

Highlight

THE DAN KELLER Mortgage Planning Playbook

Mortgage Planning Report - Total Cost Analysis

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

I see my job as an educator, a financial planner in nature. My vision is to help you integrate your

mortgage into your short-term and long-term financial goals. I want every single one of my clients to

get the BEST that I have to offer, that is why I present loan options much like a financial planner

would present investment options to you. Education - Communication - Execution!

Name(s):

Phone: 425-425-4250 Date

Email Address: [email protected]

Property Address:

Loan Program: Est Closing Date: TBD

Loan Purpose Purchase Origination Fee $0.00

Occupancy Primary Discount Points $0.00

Loan Type Conventional Appraisal Fee $525.00

Amortization Type Fixed Rate Credit Report $36.00

Lien Position 1st Tax Service Fee $77.00

Purchase Price $400,000.00 Settlement/Closing Fee $550.00

Interest Rate 4.125% Title Insurance (Lender's) $700.00

Number of Payments 360 Recording Fee $185.00

Amortization Term 360 Processing Fee $0.00

Loan To Value Ratio 95.00% Underwritng Fee $1,417.00

Combined Loan To Value Ratio 95.00% Flood Cert $7.50

Lender Courier Fee $0.00

Wire Transfer Fee $0.00

1st Lien P&I Payment $1,841.67 ReX loan fee $0.00

Other Financing Payment $0.00

Hazard Insurance $50.00 ---Estimated Closing Costs Total---

Property Taxes $333.33

Mortgage Insurance $171.00

HOA Dues $0.00 Est. Interest 1 days @ $42.95 / day

FHA/VA/USDA Funding Fee

---Estimated Monthly Payment--- $2,396.00

Hazard Insurance Annual Premium

Hazard Insurance Escrow (3 mos)

Estimated Base Loan Amount $380,000.00 Property Taxes Escrow (3 mos)

Upfront PMI Fee 0.00% $0.00

--- Estimated Total Loan Amount--- $380,000.00 ---Estimated Prepaids and Escrows Total---

Estimated Down Payment $20,000.00 * Closing Date: TBD

Prepaids (see "block 4") $1,792.94 * Title opened with:_____ Escrow is opened with: ______

Closing Costs (see "block 2") $3,497.50 * Pricing - 4.125% w/ cost of 0.00% discount points (01/12/16)

Estimated Total Cash Investment $25,290.44 * Septic or well? No

- Estimated Lender Credit $0.00 * Rate/PMI based on 740 credit score or higher

- Estimated Seller Credit $0.00 * PMI quote from Essent at .54% monthly

- Estimated Earnest Money $0.00 * Your interest rate is NOT currently locked.

* Real Estate Agent: _________

$25,290.44 * Condo or townhome? No

Loan Analysis Worksheet [Example report for MC Packet]

New American Funding

Dan Keller [MLO# 115349]

425-350-7136

Block 1. Proposed Loan Terms Block 2. Estimated Closing Costs

1/12/2016

Conventional - 30yr Fxd/5% Down

Johnny and Sally Homebuyer

Property TBD - Home Search In Process

This document is not a Good Faith Estimate of Settlement Costs and is intended solely for pre-qualification purposes. This document is a part of the mortgage planning process and does not constitute an

application or confirm the terms/rate are locked. The information above reflects proposed loan terms and estimated costs which are typical for this type of loan transaction. If you decide to proceed with these

loan terms, you will be provided with detailed loan disclosures including a Good Faith Estimate and Truth In Lending Disclosure.

---Estimated Total Funds To Close---

Block 5. Estimated Loan Amount

Block 3. Estimated Monthly Payment

Block 6. Estimated Cash To Close

$0.00

Block 4. Estimated Prepaids and Escrows

Comments/File Notes:

$999.99

$1,792.94

$600.00

$150.00

(0.000%)

(0.000%)

$3,497.50

$42.95

THE DAN KELLER Mortgage Planning Playbook

Shopping Around?

1. What Are Mortgage Interest Rates Based On?

The ONLY correct answer is MBS or Mortgage Backed Securities or Mortgage Bonds, NOT the 10-yr Treasury.

While the 10-yr Treasury Note often trends in the same direction as Mortgage Bonds, it is not unusual to see them

move in completely opposite directions. DO NOT work with a lender that has their eyes on the wrong indicators!

2. What Is the Next Economic Report or Event That May Cause An Interest Rate Movement?

A professional lender will have this information at their fingertips (or know off the top of their head). As host of

Seattle Real Estate Radio on KKOL 1300am Business Radio, I address these topics weekly keeping clients in the

KNOW when it comes to their mortgage! Tune in Monday’s at 3p or visit www.SeattleRealEstateRadio.com

3. When Janet Yellen and the FED “Change Rates”, What Does That Mean and What Impact

Does It Have On Mortgage Interest Rates?

The answer may surprise you (along with many others). When the FED makes a move, they are changing a rate

called the Fed Funds Rate. This is a very short term rate that affects credit cards, credit lines, and auto loans.

Mortgage rates often times end up moving in the opposite direction due to the dynamics of the financial markets

and economy. Many people (and loan reps) do not understand the difference here. Work with a pro that does!

4. What Is Happening In the Market Today, and What Is Happening In the Near Future?

If a mortgage lender cannot explain how Mortgage Bonds and interest rates are moving at the PRESENT moment

as well as what is coming up in the near future, you are talking with someone who is reading last week’s news,

and probably not a professional with whom to entrust your home financing.

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

Here’s The Inside Scoop On How To Do It Right!

First, Make sure that you are working with an experienced, professional loan officer. Large banks and credit un-

ions rely on volume and low wage earning employees to discount their rates. It is very important to understand that

the largest financial transaction of your life is far too important to place into the hands of someone not

capable of advising you properly and troubleshooting any issues that may arise along the way. Many reps

at banks are “order takers” and have no contact with an underwriter to get help if needed. But how can you tell?

Step One: Get the name and company of the loan officer and look them up on Yelp and Zillow. DO NOT engage

in business with a loan officer without checking references first. If you are considering a large bank, Google (for

example) “Wells Fargo Mortgage Approval Complaints”.

Next, here are FOUR SIMPLE QUESTIONS YOUR LENDER ABSOLUTELY MUST BE ABLE TO ANSWER

CORRECTLY. (The answers are given to you as I do not expect you to know) IF THEY DO NOT KNOW THE

ANSWERS5 RUN55 DON’T WALK, RUN TO A LENDER THAT DOES!

Be Smart; Ask Questions; Get Answers!

Dan Keller

Highlight

Dan Keller

Highlight

Dan Keller

Highlight

THE DAN KELLER Mortgage Planning Playbook

Shopping Around? (Part Two)

1. IF IT SEEMS TOO GOOD TO BE TRUE, THEN IT PROBABLY IS.

You probably didn’t need me to tell you that, did you? Mortgage rates and money ALL come from the same place.

So if something sounds really unbelievable, it’s better to ask a few more questions to find the “hook”. Is there a

pre-payment penalty? What is the term of the loan? How many points are required? What is the lock in period?

2. YOU GET WHAT YOU PAY FOR.

If you are looking for the cheapest deal out there, understand that you are placing a hugely important process into

the hands of the lowest bidder, that in the end, while saving you a couple of dollars could end up costing you thou-

sands. Worst case, expect that you don’t close at all and lose your Earnest Money deposit. All too often I see

this, clients don’t realize until it’s too late that the cheapest isn’t best. If you are looking for the cheapest “quote”,

head on out to the internet, and we wish you good luck.

Just remember - if you’ve heard of any horror stories from family members or friends about closing late, communi-

cation problems, and/or last minute changes to rates/fees<. These are often due to working with internet lenders

or large banks/credit unions who have a serious lack of guideline knowledge and experience in the local market

place. MOST IMPORTANTLY, REMEMBER THAT THE CHEAPEST RATE ON THE WRONG STRATEGY CAN

COST YOU THOUSANDS OF DOLLARS IN THE LONG-RUN. That being said, we are not the cheapest. Of

course our rates/fees are extremely competitive, but we have also invested in the systems and Team to ensure the

TOP quality experience that you DESERVE!

3. MAKE CORRECT COMPARISONS - RATES & CLOSING COSTS GO HAND-IN-HAND.

When looking at estimates, don’t simply look at the bottom line. This means that you may see the interest rate that

you want, but may have to pay higher costs to get it. On the other hand, you can pay lower fees or even no fees

at all - but understand , that comes at the expense of a higher interest rate. Either of these balances may be right

for you, or somewhere in between, it all depends on what your financial goals are. A professional lender will be

able to offer the best advice and options in terms of the balance between interest rate and closing costs that cor-

rectly fits your personal financial goals. This is a conversation we have in a Mortgage Planning Meeting.

4. UNDERSTAND THAT INTEREST RATES CHANGE DAILY, EVEN HOURLY.

This means that if you are comparing lender rates/fees - this is a moving target on an hourly basis. For example, if

you have two lenders that you want to compare, you must get the quote at the EXACT time on the EXACT day

with the EXACT same terms in order to make an accurate comparison. You must also consider the length of lock,

as that impacts the interest rate. Lastly, the lender must guarantee a 30-day close or you will pay points to extend.

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

Here’s The Inside Scoop On How To Do It Right!

Again, our advice to you is simple: Be Smart; Ask Questions; Get Answers!

As you can imagine, I wouldn’t be encouraging you to “shop around” if we weren’t very confident

that we feel that we can give you a great value and serve you the very BEST!

Dan Keller

Highlight

!"#$%#&'($"()$'*$(++$,-./0$1$

)#23-'/0$%.-*0(0#$(44-.5(+$(/&$

)(*')67'/0$2-#&'*$3/&#-,-'*'/0$

03'&#+'/#)$(-#$/.*$*"#$&'66'23+*'#)$

4+(03'/0$%.-*0(0#$2./)3%#-)8$9*:)$

'/$%##*'/0$*"#$-'0.-.3)$

&.23%#/*(*'./$-#;3'-#%#/*)$*"(*$

%.)*$4#.4+#$6(++$6+(*8$!"#$0..&$/#,)$

')<$*"#$6'=$')$)'%4+#8$>3)*$)2(/<$

4".*.2.47<$6(=<$(/&$&#+'5#-$#5#-7$

()4#2*$.6$7.3-$6'/(/2'(+$+'6#8$!"#/<$

)".-*+7$?#6.-#$2+.)'/0<$2"#2@$

#5#-7*"'/0$(0('/8$$$

A.-*0(0#$2./)3%#-)$,".$#/*#-$*"#$%.-*0(0#$(44-.5(+$4-.2#))$-#(&7$*.$

?(**+#$*"#'-$2".)#/$%.-*0(0#$+#/&#-$,'++$2.%#$.3*$,'*"$($/'0"*%(-#$)*.-7$*.$

*#++8$B)$*"#$4-.2#))<$-#;3'-#%#/*)<$(/&$03'&#+'/#)$(-#$*"#$)(%#$6.-$#5#-7?.&7<$

7.3-$%'/&)#*$')$*"#$0(%#C2"(/0#-8$B22#4*'/0$*"#$-#&3/&(/*$&.23%#/*(*'./$

/#2#))(-7$6.-$+#/&#-$(44-.5(+$,'++$%(@#$#5#-7./#:)$+'6#$#()'#-8$

D"#/$9$,()$($@'&<$%7$6(*"#-$.22()'./(++7$'))3#&$&'-#2*'5#)$*"(*$9$/(*3-(++7$

*".30"*$,#-#$)34#-6+3.3)<$(/&$,"#/$()@#&$,"7$9$/##&#&$*.$&.$,"(*#5#-$'*$

,()$"#$,(/*#&$%#$*.$&.<$"')$(/),#-$,()$.6*#/E$FG#2(3)#$9$)('&$).8H$!"')$

/#5#-$)##%#&$*.$(&&-#))$%7$;3#-7$?3*$(+,(7)$+#6*$%#$,'*".3*$($-#*.-*<$(/&$9$

,.3+&$3)3(++7$2.%4+78$!"')$')$#=(2*+7$,"(*$2./)3%#-)$)".3+&$&.$&3-'/0$*"#$

%.-*0(0#$(44-.5(+$4-.2#))8$D"#/$7.3-$+#/&#-$-#;3#)*)$,"(*$)##%)$*.$?#$

.5#-C&.23%#/*(*'./$(/&$7.3$,./&#-$,"7$7.3$/##&$'*<$(22#4*$*"#$)'%4+#$

#&'2*$1$F?#2(3)#$9$)('&$).8H$I.3$,'++$6'/&$*"#$%.-*0(0#$(44-.5(+$4-.2#))$%32"$

+#))$6-3)*-(*'/08$

J.<$,"(*:)$*"#$4#-6#2*$+.(/K$D#++<$'*:)$./#$*"(*$L(M$4(7)$?(2@$*"#$+#/&#-$(/&$

L?M$4(7)$?(2@$*"#$+#/&#-$./$*'%#8$N/&#-,-'*'/0$*"#$4#-6#2*$+.(/$')$/.*$*"#$

0.(+$*"(*$%.-*0(0#$+#/&#-)$()4'-#$*.$*.&(78$

!"#$-#(+$0.(+$')$*"#$4#-6#2*$+.(/$6'+#8$

A.-*0(0#$+#/&#-)$"(5#$)366#-#&$)*(00#-'/0$+.))#)$(/&$0./#$.3*$.6$?3)'/#))$

?#2(3)#$.6$*"#$&-#(&#&$+.(/$-#43-2"()#8$B)$%.-*0(0#$&#+'/;3#/2'#)$

'/2-#()#&<$O(//'#A(#$(/&$O-#&&'#A(2$?#0(/$*.$(3&'*$%.-*0(0#$+.(/)$*"#7$

"(&$43-2"()#&$(/&$&')2.5#-#&$)3?)*(/&(-&$(/&$6-(3&3+#/*$3/&#-,-'*'/0$

4-(2*'2#)$*"(*$5'.+(*#&$-#4-#)#/*(*'./)$(/&$,(--(/*'#)$%(&#<$)*(*'/0$*"#)#$

,#-#$"'0"$;3(+'*7$+.(/)8$O(//'#$(/&$O-#&&'#$?#0(/$6.-2'/0$*"#$.-'0'/(*'/0$

+#/&#-)$.6$*"#)#$F?(&H$+.(/)$*.$?37$*"#%$?(2@8$J.$($)%(++$2.--#)4./&#/*$

!"#$%&'()&'*""&+,(-(&./""0)12&3&4/15&6(&!*-&6,0&!(5-&7'&8(*)&!/)&9(/:&

&&&&

&&

;<=>7?@9&AB?@?!< C DEFGEHFIH&J&IF2HD@K& C ILMNOG&P#0Q5&

!"#$P#-6#2*$Q.(/$O'+#$&

ABR9ST$JUSJU$VO$IVNW$O9SBSXUJ$$

A./#7G3'+&#-&

!"#$%&#''('M&!(:-)#R*-()

)''%*+,-,)

Page 1 of 3The Perfect Loan File - Forbes

3/29/2012http://www.forbes.com/sites/moneybuilder/2012/03/09/the-perfect-loan-file-2/print/

dan keller

dan keller

dan keller

dan keller

%.-*0(0#$+#/&#-$')$6.-2#&$*.$?37$?(2@$($)'/0+#$%.-*0(0#$+.(/$'/$*"#$(%.3/*$

.6$YZ[\<\\\8$!"')$?#2.%#)$($YZ[\<\\\$+.))$*.$($)%(++$%.-*0(0#$?3)'/#))$6.-$

($)'/0+#$+.(/<$?#2(3)#$'*$,'++$/#5#-$?#$-#4('&8$

9*$&.#)/:*$*(@#$%(/7$.6$*"#)#$?(&$+.(/$?37?(2@)$*.$2+.)#$*"#$&..-)$./$%(/7$

)%(++$%.-*0(0#$.4#-(*'./)8$!"#$+#/&'/0$".3)#)$)366#-#&$?'++'./)$.6$&.++(-)$.6$

+.))#)$-#43-2"()'/0$+.(/)$6-.%$O(//'#$(/&$O-#&&'#<$(/&$?#0(/$*.$&.$*"#$

)(%#$*"'/0$6.-$+.(/)$*"#7$"(&$43-2"()#&$6-.%$)%(++#-$.-'0'/(*.-)8$

!"#$)%(++$(/&$%#&'3%$)']#&$%.-*0(0#$.-'0'/(*.-)$*"(*$)3-5'5#&$2-#(*#&$

3/&#-,-'*'/0$03'&#+'/#)$(/&$4-.2#&3-#)$*.$#+'%'/(*#$*"#$*"-#(*$.6$63*3-#$+.(/$

-#43-2"()#$+.))#)8$!"#$(/),#-K$!"#$4#-6#2*$+.(/$6'+#8$

9*:)$/.$+./0#-$/#2#))(-7$*.$"(5#$#=2#++#/*$2-#&'*<$($?'0$&.,/$4(7%#/*$(/&$

)*(?+#$#%4+.7%#/*$,'*"$'/2.%#$)366'2'#/*$*.$)344.-*$7.3-$&#?*$)#-5'2#$*.$

03(-(/*##$7.3-$+.(/$(44-.5(+8$^.,#5#-<$7.3$%3)*$"(5#$($?.--.,#-$4-.6'+#$

*"(*$%##*)$*"#$2-#&'*$3/&#-,-'*'/0$03'&#+'/#)$6.-$*"#$+.(/$7.3$(-#$-#;3#)*'/08$

B/&<$%.-#$'%4.-*(/*+7<$7.3$"(5#$*.$?#$(?+#$*.$"(-&C2.47C03'&#+'/#C

&.23%#/*$7.3-$4-.6'+#8$

U5#-7$/..@$(/&$2-(//7$.6$7.3-$6'/(/2'(+$+'6#$"()$*.$?#$2.--.?.-(*#&<$&.3?+#C$

(/&$*-'4+#C2"#2@#&<$(/&$-#5'#,#&$(0('/$?#6.-#$2+.)'/08$!"')$,(7<$'6$*"#$

.-'0'/(*'/0$+#/&#-$"()$2-#(*#&$($+.(/$6'+#$*"(*$')$#=(2*+7$2./)')*#/*$,'*"$

43?+')"#&$3/&#-,-'*'/0$03'&#+'/#)$(/&$"()$&.23%#/*#&$,"'+#$(&"#-'/0$*.$

*".)#$03'&#+'/#)<$*"#$2"(/2#)$(-#$*"(*$7.3-$+.(/$,'++$/.*$?#$)3?_#2*$*.$

-#43-2"()#8$

G.--.,#-)$(+).$/##&$*.$4-#4(-#$6.-$4-.2#))'/0$(/&$3/&#-,-'*'/08$P-.2#)).-)$

(/&$3/&#-,-'*#-)$(-#$*"#$4#.4+#$*-('/#&$(/&$2"(-0#&$,'*"$0(*"#-'/0$

L4-.2#)).-)M<$(++$.6$7.3-$-#;3'-#&C6.-C(44-.5(+$6'/(/2'(+$&.23%#/*)<$(/&$*"#/$

(44-.5'/0$L3/&#-,-'*#-)M<$7.3-$+.(/8$I.3$2(/$())3%#$*"#)#$4#.4+#$(-#$,#++$

*-('/#&$(/&$5#-7$#=4#-'#/2#&<$()$*"#7$(-#$*()@#&$,'*"$())#%?+'/0$(/&$

(44-.5'/0$($"'0"C;3(+'*7C*"#)#C4#.4+#C,'++C4(7C3)C?(2@$+.(/$6'+#8$G3*$_3)*$

".,$&.$*"#7$0.$(?.3*$*"(*K$

!"#$4-.2#))$?#0'/)$,'*"$*"#$6'+*#-$1$*"#$+.(/$.-'0'/(*.-$L(8@8($+.(/$.66'2#-<$

%.-*0(0#$2./)3+*(/*<$%.-*0(0#$(&5')#-<$#*28M$1$*()@#&$*.$%(*2"$*"#$

;3(+'6'2(*'./)$.6$($4(-*'23+(-$%.-*0(0#$&#(+$*.$*"#$(44-.4-'(*#$3/&#-,-'*'/0$

03'&#+'/#)8$9*$')$*"#$6'+*#-:)$_.?$*.$&#*#-%'/#$'6$($+.(/$)2#/(-'.$')$(44-.5(?+#$

(/&$*.$0(*"#-$*"#$&.23%#/*(*'./$*.$)344.-*$*"(*$&#*#-%'/(*'./8$9*$')$"#-#<$(*$

*"#$?#0'//'/0$.6$*"#$(44-.5(+$4-.2#))<$,"#-#$*"#$&#(+$')$%(&#$.-$?-.@#/8$!"#$

-#)*$.6$*"#$(44-.5(+$4-.2#))$')$_3)*$4(4#-'/0$*"#$6'+#8$

!"#$6'+*#-$&#*#-%'/#)$,"#*"#-$*"#$'/6.-%(*'./$4-.5'&#&$?7$*"#$?.--.,#-$2(/$

?#$5(+'&(*#&$(/&$&.23%#/*#&8$!"')$')$)'%4+#<$)'/2#$%.)*$%.-*0(0#)$(-#$

(44-.5#&$?7$(3*.%(*#&$3/&#-,-'*'/0$#/0'/#)$)32"$()$`#)@*.4$N/&#-,-'*#-<$

(/&$*"#$(3*.%(*#&$(44-.5(+$0#/#-(*#)$($+')*$.6$*"#$&.23%#/*)$/##&#&$*.$

4(4#-$*"#$+.(/$6'+#8$B/$3/&#-,-'*#-$2(/<$(*$*"')$)*(0#<$-#;3#)*$(&&'*'./(+$

)344.-*'/0$&.23%#/*(*'./$#5'&#/2#$(*$*"#'-$&')2-#*'./<$()$/.*$(++$

2'-23%)*(/2#)$/#(*+7$6'*$'/*.$*"#$4-#)2-'?#&$3/&#-,-'*'/0$?.=8$96$*"#$6'+*#-$

2-#(*#)$($+.(/$6'+#$,'*"$(223-(*#$'/6.-%(*'./<$*"#/$)#23-#)$*"#$&.23%#/*(*'./$

-#)3+*'/0$6-.%$*"#$(3*.%(*#&$3/&#-,-'*'/0$6'/&'/0)<$*"#$+.(/$,'++$2+.)#$

3/#5#/*63++78$

J.<$+#*:)$?#0'/$,'*"$*"#$4-#C(44-.5(+$2(++8$A.-*0(0#$4-#C(44-.5(+$')$*74'2(++7$

(22.%4+')"#&$,'*"$($*#+#4"./#$'/*#-5'#,8$B$4-.)4#2*'5#$?.--.,#-$2(++)$($

%.-*0(0#$-#4$L6'+*#-M<$(/&$*"#$;3#)*'./)$?#0'/8$!"#-#$,'++$?#$+.*)$.6$;3#)*'./)$

Page 2 of 3The Perfect Loan File - Forbes

3/29/2012http://www.forbes.com/sites/moneybuilder/2012/03/09/the-perfect-loan-file-2/print/

dan keller

dan keller

dan keller

dan keller

&&

&&

()$*"')$2-'*'2(+$4"()#$.6$*"#$4-.2#))$')$(@'/$*.$*"#$&')2.5#-7$4#-'.&$'/$($*-'(+$1$

7.3:++$/##&$*.$&')2+.)#$#5#-7*"'/08$U=4#2*$*.$(/),#-$;3#-'#)$./$,"(*$7.3$&.$

6.-$($+'5'/0<$".,$+./0$7.3:5#$?##/$#%4+.7#&$'/$7.3-$23--#/*$6'#+&<$(/&$,"(*$

7.3-$)(+(-7$')8$96$*"#-#$')$($2.C?.--.,#-<$*"#7$,'++$"(5#$*.$(/),#-$*"#$)(%#$

;3#)*'./)8$

U5#-7$&.++(-$'/$2"#2@'/0<$)(5'/0)<$'/5#)*%#/*)$(/&$-#*'-#%#/*$(22.3/*)<$(+).$

@/.,/$()$())#*)$*.$2+.)#<$()$,#++$()$0'6*)$6-.%$-#+(*'5#)$(/&$/./C4-.6'*$0-(/*)<$

"()$*.$?#$(22.3/*#&$6.-8$U))#/*'(++7$#5#-7*"'/0$(44#(-'/0$./$($?.--.,#-:)$

())#*C-(&(-C)2-##/$"()$*.$?#$&.23%#/*#&$(/&$#=4+('/#&8$

96$7.3$,#-#$4-#5'.3)+7$($".%#.,/#-$(/&$).+&$7.3-$".%#$'/$($)".-*$)(+#<$.-$'6$

7.3$.,/$($".%#$/.,$(/&$4+(/$*.$@##4$'*$()$(/$'/5#)*%#/*$.-$-#/*(+$4-.4#-*7<$

*"#-#$(-#$/#,$(/&$)4#2'6'2$3/&#-,-'*'/0$03'&#+'/#)$2-#(*#&$_3)*$6.-$7.38$9/$

*"#)#$2()#)<$63++$&')2+.)3-#$.6$7.3-$2-#&'*$(/&$".%#.,/#-)"'4$4()*$2(/$

4.*#/*'(++7$#+'%'/(*#$3/6.-#)##/$%.-*0(0#$(44-.5(+$,.#)8$O.-$'/)*(/2#<$

O(//'#A(#$"()$($/#,$3/&#-,-'*'/0$03'&#+'/#$2(++#&$FG37C(/&CG('+<H$6.-$

23--#/*$".%#.,/#-):$4+(//'/0$./$@##4'/0$*"#'-$#=')*'/0$".%#$()$(/$

'/5#)*%#/*a-#/*(+$4-.4#-*78$P-.4#-*'#)$/.*$%##*'/0$*"#$b\c$#;3'*7$*#)*$

6.-$FG37C(/&CG('+H$-#)3+*$'/$(&&'*'./(+$())#*$-#;3'-#%#/*)$*.$43-2"()#$($/#,$

".%#8$G37#-)$,'*"$($)".-*$)(+#$"')*.-7$%(7$"(5#$*.$,('*$*,.$*.$*"-##$7#(-)$

?#6.-#$*"#7$(-#$#+'0'?+#$6.-$%.-*0(0#$6'/(/2'/0$(0('/8$O3++$5#**'/0$.6$7.3-$

4-#5'.3)$%.-*0(0#$+'6#$,'++$)(5#$7.3$*"#$&-#(&#&$,#C"(5#C(C4-.?+#%$2(++$

6-.%$7.3-$%.-*0(0#$+#/&#-8$

9*$(++$2.%#)$&.,/$*.$7.3-$4-..68$96$*"#$+#/&#-$()@)$6.-$($)4#2'6'2$&.23%#/*<$

0'5#$*"#%$#=(2*+7$,"(*$*"#7$(-#$()@'/0$6.-<$/.*$,"(*$F)".3+&$?#$VR<H$1$

?#2(3)#$'*$,./:*$?#8$$!"')$')$,"#-#$*"#$(44-.5(+$4-.2#))$*#/&)$*.$0.$.66$*"#$

-('+)<$,"#/$*"#$+#/&#-$()@)$6.-$)4#2'6'2$&.23%#/*(*'./$(/&$*"#$?.--.,#-$

)344+'#)$).%#*"'/0$#+)#8$^#-#<$*..<$')$,"#-#$?.*"$)'&#)$0#*$6-3)*-(*#&8$J.$'6$

*"#$+#/&#-$()@)$6.-$($?(/@$)*(*#%#/*$(/&$*"#-#$(-#$[$4(0#)$6.-$*"(*$?(/@$

)*(*#%#/*<$)#/&$*"#%$(++$[$4(0#)<$(/&$/.*$_3)*$*"#$)3%%(-78$96$7.3$)#/&$

*"#%$*"#$)3%%(-7$4(0#$(/&$*"#7$()@$(0('/<$&./:*$2.%4+('/$*"(*$*"#$+#/&#-$

@##4)$()@'/0$6.-$*"#$)(%#$*"'/0$,"#/$7.3$/#5#-$)#/*$'*$'/$*"#$6'-)*$4+(2#8$!"')$

%(7$).3/&$#+#%#/*(-7<$?3*$*"#$5()*$%(_.-'*7$.6$%.-*0(0#$(44-.5(+$4-.2#))$

,.#)$)*#%$6-.%$)2#/(-'.)$_3)*$+'@#$*"')8$

!"#$-#()./$*"#$%.-*0(0#$(44-.5(+$4-.2#))$')$/.,$).$-'0.-.3)$')$)'%4+#8$

B5.'&'/0$(3+*)$(/&$+.(/$?37?(2@)$"()$?#2.%#$*"#$4-'%(-7$0.(+$.6$

%.-*0(0#$+#/&#-)8$$$^'0"#-$)*(/&(-&)$(-#$-#&32'/0$+.(/$(3+*)<$$,"'2"$

)".3+&$%#(/$6#,#-$6.-#2+.)3-#)$'/$*"#$63*3-#8$T.5#-/%#/*$&(*($)".,)$

*"(*$$+#))$*"(/$Zc$.6$+.(/)$.-'0'/(*#&$'/$Z\\d<$*"(*$,#-#$-#).+&$*.$O-#&&'#$

A(2$(/&$O(//'#$A(#$,#/*$'/*.$(3+*$(6*#-$ef$%./*")<$&.,/$6-.%$%.-#$

*"(/$ZZc$(3+*$-(*#)$6.-$Z\\g$+.(/)8$

J.$,"#/$7.3-$+#/&#-$-#;3#)*)$)4#2'6'2$&.23%#/*)$6-.%$7.3<$0'5#$'*$*"#%$

_3)*$F?#2(3)#$*"#7$)('&$).8H$

I.3$2(/$*"(/@$%7$&(&$6.-$*"(*8$

&.+/)%"#-/01'%/)%"2"/1"31'%,(1/('%"-4%%+--*45566678,#3')70,95)/-')59,(':3;/1<'#5=>?=5>@5>A5-+'B*'#8'0-B1,"(B8/1'B=5&&

Page 3 of 3The Perfect Loan File - Forbes

3/29/2012http://www.forbes.com/sites/moneybuilder/2012/03/09/the-perfect-loan-file-2/print/

dan keller

dan keller

dan keller

dan keller

WHAT’S IN YOUR MORTGAGE PAYMENT?

A mortgage payment consists of four components:

P

PRINCIPAL

The original amount of

money owed

I

INTEREST

The charge for the use

(loan) of money

T

$

TAXES

These are assessed by your

county; your lender typically

pays your taxes

I

INSURANCE

Your homeowners insurance;

you pay 1/12 the annual

premium each month

MORTGAGE PAYMENT BREAKDOWN

There are several factors, including how much of a down payment

you make and the program you choose that determine how much

your monthly mortgage payment will be.

EXAMPLES OF MORTGAGE LOAN OPTIONS:

1 2

3 4

Conven onal - 30-yr Fxd. Conven onal - 15-yr Fxd.

FHA – 30-yr Fxd. Conven onal - 5% Down

Home Price: $200,000

Down Payment: 20% ($40,000)

Program/Rate: 30 yr fixed @ 4.25%

Property Tax: 1%

Homeowners Insurance: $800/yr

PAYMENT BREAKDOWN:

Principal & Interest: $787.10

Property Taxes: $200

Homeowners Insurance: $67

Monthly Payment: $1,054.10

Home Price: $200,000

Down Payment: 20% ($40,000)

Program/Rate: 15 yr fixed @ 3.25%

Property Tax: 1%

Homeowners Insurance: $800/yr

PAYMENT BREAKDOWN:

Principal & Interest: $1,124.27

Property Taxes: $200

Homeowners Insurance: $67

Monthly Payment: $1,391.27

Home Price: $200,000

Down Payment: 3.5% ($7,000)

Program/Rate: 30 yr fixed @ 3.875%

Property Tax: 1%

Homeowners Insurance: $800/yr

PAYMENT BREAKDOWN:

FHA Private Mortgage Insurance: $212.74

Principal & Interest: $923.44

Property Taxes: $200

Homeowners Insurance: $67

Monthly Payment: $1,403.18

Home Price: $200,000

Down Payment: 5% ($10,000)

Program/Rate: 30 yr fixed @ 4.25%

Property Tax: 1%

Homeowners Insurance: $800/yr

PAYMENT BREAKDOWN:

Private Mortgage Insurance: $99.75

Principal & Interest: $934.69

Property Taxes: $200

Homeowners Insurance: $67

Monthly Payment: $1,301.44

Presented By:

Dan Keller MLO# 115349

Mortgage Advisor

- AND -

Private Mortgage Insurance.

This is required if you put down

less than 20% down payment.

$200,000

HOW CAN YOU FIND MONEY FOR THIS EXTRA PAYMENT?

I have designed a Debt-Analysis Worksheet with my financial planner to assist you in freeing up an addiDonal

mortgage payment per year. Contact your financial planner or let me know if I can help direct you!

THE SIZE OF YOUR DOWN PAYMENT

The amount of your down payment may impact how many loan program opDons are

available to you. In addiDon, depending on the amount of your down payment, you

may be required to have private mortgage insurance.

ADDITIONAL MORTGAGE PAYMENTS MATTER

Making one addiDonal mortgage payment per year can save you thousands of dollars and help you pay off your loan in less Dme.

12 Monthly Payments/Year 13 Payments/Year REPAYMENT EXAMPLE

Twelve payments each year will put

your total loan cost at $455,088.98

One addiDonal payment each year will save you

$55,990.06 and reduce your term by 6 years FACTORS

Original Payment

Total Loan Payment

Interest Rate

Term

Monthly Payment

Total Interest

$200,000 $200,000

30-year fixed 30-year fixed

4.25% 4.25%

$938.88 $938.88

$199,010 $255,000

$354,197 $286,597

Residen al Mortgage Advisor - MLO 115349

Direct 425-350-7136

Office 425-947-8533

www.thedankellergroup.com

12220 113th Ave NE Suite 120 Kirkland, WA

THE DAN KELLER Mortgage Planning Playbook

Read What Clients Are Saying About Dan Keller

See More Reviews Like This On Yelp - (Google “Dan Keller Mortgage Yelp Reviews”)

[Jonathan W.] “My wife and I are first �me home buyers who were slightly anxious about the unknowns in the process

of ge�ng a loan. A friend referred us to Dan Keller and his group, saying they had rates comparable to big banks but

were much more personable. Our first thought was that paying a bit more would be worth the answered ques�ons, so

we gave it a try. First of all, we were pleasantly surprised to see that they did not cost any more than big banks, but

actually saved us money by really trying to lock down our interest rate at the best �me during the month while the

house details were going through. On top of that, they were great about giving quick and detailed responses to any

ques�ons or concerns along the way. The several �mes that we met with Dan, he was clearly very knowledgeable and

made us feel like we were in good hands. Next �me we need a loan, I don't think we will hesitate to use Dan Keller's

group again. We recommend that you give them a try, especially if the whole loan process seems a bit over your

head.”

[Jillayne S.] “I'm an educator and a 30+ year veteran of the mortgage lending industry. I've known Dan for several

years now. This year, Dan was put in a posi�on of having to make an ethical choice. He chose to be honest. His choice

had an effect on me professionally, and I don't think he realized it at the �me. Dan works hard, takes care of his cus-

tomers, and understands that it takes a long �me of making solid, ethically jus�fiable choices, year a3er year, to build

a reputa�on in this industry. I know thousands of mortgage loan originators, and Dan Keller comes with my highest

recommenda�on.”

[Ed Finlan, Realtor] “Can't say enough about Dan and his team. I am a real estate broker in Northwest Washington

and encourage all of the buyers we are working with to contact Dan and use him if they are financing their home. I

could go on and on about how he has saved the day on different deals or pulled a rabbit of his hat at the last minute

when a different lender couldn't make it happen but in the end, the best way to see how good he is, is to contact him

and use him when you get a loan or refinance. Dan and I teach home buyer classes and help people become home

owners with the right home, the right loan and in the end the right deal. An honest to goodness "Nice guy” who is

good at what he does.”

[Sharath U.] Dan was referred to us by our real estate agent (Chris�an Nossum) and we are very glad we went with his

team. The quick closing promised by Dan's team was surely one of the reasons we won a very compe��ve, mul�-offer

scenario. Once our offer was accepted, the loan process was handled in a very professional & smooth manner. One

thing I was very amazed by was the use of latest technologies at their disposal to make the process super quick.

(425) 350-7136 Dan Keller mlo# 115349 [email protected]

W W W .T h e D a n K e l l e r G r o u p . C O M

HOME MORTGAGE CONCIERGE PROGRAM

For questions contact: Dan Keller cell: (425) 350-7136 / fax: (206) 339-6343 / [email protected]

Mortgage Planning Questionnaire 1

Purpose of Loan: PPuurrcchhaassee RReeffiinnaannccee ((ccaasshh oouutt)) RReeffiinnaannccee ((nnoo ccaasshh oouutt))

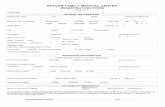

BBoorrrroowweerr CCoo--BBoorrrroowweerr FFuullll NNaammee ____________________________________________________________________________________________________ SSoocc.. SSeeccuurriittyy ##:: ____________________________________________ DDaattee ooff BBiirrtthh __________________________ PPhhoonnee ((cceellll)) ________________________________________________ ((ww))____________________________________________

mmaarrrriieedd uunnmmaarrrriieedd ddiivvoorrcceedd YYeeaarrss ooff sscchhooooll __________________________ ## ooff ddeeppeennddeennttss __________________________ AAggeess ______________________________________________________ PPrreesseenntt aaddddrreessss ____________________________________________________________________________________________ ________________________________________________________________________________________________________________________

oowwnn rreenntt YYeeaarrss aatt tthhiiss aaddddrreessss __________ RReenntt//MMoorrttgg.. PPmmnntt____________________ PPrreevviioouuss AAddddrreessss ((iiff lleessss tthhaann 22 yyrrss.. AAbboovvee)) ________________________________________________ ______________________________________________________________________________________________________________________ EEmmppllooyyeerr ______________________________________________________________________________________________________ AAddddrreessss ______________________________________________________________________________________________________ ______________________________________________________________________________________________________________________ PPoossiittiioonn ______________________________________________________ WWoorrkk PPhhoonnee____________________________ YYeeaarrss oonn tthhiiss jjoobb ________________________________ YYeeaarrss iinn tthhiiss lliinnee ooff wwoorrkk ________________ GGrroossss MMoonntthhllyy IInnccoommee ______________________________ AAnnnnuuaall BBoonnuusseess ______________________ CCuurrrreenntt HHoouussiinngg EExxppeennsseess:: RReenntt __________________________ MMoorrttggaaggee __________________________ TTaaxxeess ____________________________ IInnssuurraannccee __________________ MMttgg.. IInnssuurraannccee ____________________ HH--OO DDuueess __________________ AAsssseettss::

CChheecckkiinngg//SSaavviinnggss//OOtthheerr IInnvveessttmmeenntt AAccccoouunnttss BBaannkk NNaammee __________________________________________________ BBaallaannccee __________________________________ BBaannkk NNaammee __________________________________________________ BBaallaannccee __________________________________ BBaannkk NNaammee __________________________________________________ BBaallaannccee __________________________________ AApppprrooxx.. VVaalluuee ooff RReettiirreemmeenntt AAccccoouunnttss ((440011KK,, eettcc)) ______________________________________ AAuuttoommoobbiilleess oowwnneedd ((yyeeaarr,, mmaakkee,, mmooddeell)) ______________________________________________________ ________________________________________________________________________________________________________________________ PPlleeaassee lliisstt aannyy ootthheerr aasssseettss oowwnneedd,, rreeaall eessttaattee oowwnneedd,, oorr aaddddiittiioonnaall mmoonneeyy eeaarrnneedd ((ssttoocckkss,, bboonnddss,, rreeaall eessttaattee,, bbooaattss,, ttiimmee sshhaarreess,, cchhiilldd ssuuppppoorrtt,, eettcc)).. ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ EE--mmaaiill aaddddrreessss ______________________________________________________________________________________________

FFuullll NNaammee ____________________________________________________________________________________________________ SSoocc.. SSeeccuurriittyy ##:: ____________________________________________ DDaattee ooff BBiirrtthh __________________________ PPhhoonnee ((cceellll)) ________________________________________________ ((ww))____________________________________________

mmaarrrriieedd uunnmmaarrrriieedd ddiivvoorrcceedd YYeeaarrss ooff sscchhooooll __________________________ ## ooff ddeeppeennddeennttss __________________________ AAggeess ______________________________________________________ PPrreesseenntt aaddddrreessss __________________________________________________________________________________________ ______________________________________________________________________________________________________________________

oowwnn rreenntt YYeeaarrss aatt tthhiiss aaddddrreessss __________ RReenntt//MMoorrttgg.. PPmmnntt__________________ PPrreevviioouuss AAddddrreessss ((iiff lleessss tthhaann 22 yyrrss.. AAbboovvee)) ________________________________________________ ______________________________________________________________________________________________________________________ EEmmppllooyyeerr ______________________________________________________________________________________________________ AAddddrreessss ______________________________________________________________________________________________________ ______________________________________________________________________________________________________________________ PPoossiittiioonn ______________________________________________________ WWoorrkk PPhhoonnee____________________________ YYeeaarrss oonn tthhiiss jjoobb ________________________________ YYeeaarrss iinn tthhiiss lliinnee ooff wwoorrkk ________________ GGrroossss MMoonntthhllyy IInnccoommee ______________________________ AAnnnnuuaall BBoonnuusseess ______________________ CCuurrrreenntt HHoouussiinngg EExxppeennsseess:: RReenntt __________________________ MMoorrttggaaggee __________________________ TTaaxxeess ____________________________ IInnssuurraannccee __________________ MMttgg.. IInnssuurraannccee ____________________ HH--OO DDuueess __________________ AAsssseettss::

CChheecckkiinngg//SSaavviinnggss//OOtthheerr IInnvveessttmmeenntt AAccccoouunnttss BBaannkk NNaammee __________________________________________________ BBaallaannccee __________________________________ BBaannkk NNaammee __________________________________________________ BBaallaannccee __________________________________ BBaannkk NNaammee __________________________________________________ BBaallaannccee __________________________________ AApppprrooxx.. VVaalluuee ooff RReettiirreemmeenntt AAccccoouunnttss ((440011KK,, eettcc)) ______________________________________ AAuuttoommoobbiilleess oowwnneedd ((yyeeaarr,, mmaakkee,, mmooddeell)) ______________________________________________________ ________________________________________________________________________________________________________________________ PPlleeaassee lliisstt aannyy ootthheerr aasssseettss oowwnneedd,, rreeaall eessttaattee oowwnneedd,, oorr aaddddiittiioonnaall mmoonneeyy eeaarrnneedd ((ssttoocckkss,, bboonnddss,, rreeaall eessttaattee,, bbooaattss,, ttiimmee sshhaarreess,, cchhiilldd ssuuppppoorrtt,, eettcc)).. ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ ________________________________________________________________________________________________________________________ EE--mmaaiill aaddddrreessss ______________________________________________________________________________________________

W W W .T h e D a n K e l l e r G r o u p . C O M

HOME MORTGAGE CONCIERGE PROGRAM

For questions contact: Dan Keller cell: (425) 350-7136 / fax: (206) 339-6343 / [email protected]

Mortgage Planning Questionnaire 2

NEW LOAN INFORMATION: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11.

12. 13. 14. 15. 16. 17. 18.

Names (full) that will appear on title: _________________________________________________________ How do you wish to be communicated with: phone e-mail text mail / preferred_______________ Have you served in the US Armed Forced? yes no Are you a disabled Veteran? yes no Have you owned a home in the last 3 years? yes no Have you ever owned a home? yes no Are you wanting to purchase a home as: Primary residence 2nd Home Investment Property Term of mortgage that you request (30, 25, 20, 15, 10, 5 years): _______ or undecided _______________ Type of mortgage you prefer: Fixed ARM Interest Only Princ./Interest Pay-off Undecided Would you prefer to pay taxes and insurance with your monthly mortgage payment? yes no Do you prefer to have the seller pay your closing costs? yes no If you rent, please provide the following information: Name of Landlord_____________________________ Phone _______________________ Date of Current Lease____________________________________ Please rate your credit score as poor, just ok, excellent -__________________________________________ If applicable, would you like information on credit restoration yes no Have you had any judgments, lawsuits, bankruptcies (last 10 yrs.), foreclosures (last 7 yrs.)? yes no Purchase price range $_________________ Desirable monthly mortgage payment $__________________ Down payment amount $___________________ or percent down _______________% Down payment will come from ______________________________________________________________ (ex. checking, savings, investments, sale of stock, sale of home, 401(K) loan, gift funds, bonus, etc.) If owned, is your current resident listed for sale? yes no If listed, with whom ____________________ Under contract? yes no Sale price $______________ Original purchase price $______________ Year built ____________ Bedrooms _____ Bathrooms _____ Sq. Feet __________ Who can we thank for referring you to meet with Dan Keller and his team?____________________________ Is there anything that you would like to know about me before allowing us to serve you? ________________ _______________________________________________________________________________________

W W W .T h e D a n K e l l e r G r o u p . C O M

HOME MORTGAGE CONCIERGE PROGRAM

For questions contact: Dan Keller cell: (425) 350-7136 / fax: (206) 339-6343 / [email protected]

Mortgage Planning Questionnaire 3

MORTGAGE ANALYSIS

1.

2. 3.

4. 5. 6. 7. 8. 9. 10. 11.

As a Mortgage and Credit Consultant, my goal is to ensure that you and your realtor receive nothing less than an exceptional lending experience working with me and my team. In the end, I am confident that I will be able to help you to secure the best rate at the lowest cost. In saying that, what is most important to you in working with a mortgage and real estate professional? ________________________________________________________________________________________

________________________________________________________________________________________

________________________________________________________________________________________ Amount of monthly payment that you are comfortable with? $_______________________ What is the best estimate for how long you will have this loan or live in this home?

_____ 1-3 years _____ 3-5 years _____ 7-10 years _____10 years+ Do you currently have plans for a major purchase in the next 12 months including a car, college tuition, home improvements, or rental properties? yes no If yes to the above question, how much do you expect to need? $____________________________________ In how many years do you plan to retire? __________________ Are you working with an experienced realtor? yes no Name _________________________________ If no, would you like me to refer one? yes no Are you currently working with an experienced financial planner? yes no Name __________________________________ If no, would you like me to refer one? yes no Do you have insurance to protect your family and home? yes no If yes, what type of policy do you have and how much coverage do you have? _________________________

________________________________________________________________________________________ What are your hobbies? ____________________________________________________________________ Do you have children? If so, what are their names and b-days?______________________________________ What is your favorite restaurant? ______________________________________________________________

What is your favorite desert? _________________________________________________________________

To: From:

Company: Date: Total # of Pages:

Fax# Senderʼs Cell #:

Phone # Senderʼs Email:

RE: Mortgage Application Packet - Items RequestedThank you for taking the time to apply for a home loan with The Dan Keller Group! To expedite the approval of your loan approval, Iʼve provided documents and a short checklist for you to complete. This will help us get you prompt feedback and expedite the loan process! Thank you!

Completed Secure Online Mortgage Application - www.MyMortgageGuyDan.com/Apply Watch the “Perfect Mortgage Process” video series at www.MyMortgageGuyDan.com/Apply Review all pages in the enclosed “Mortgage Concierge Packet” Submit/Attach All Documents Requested On the “Items Needed Checklist”

Once you have submitted the above-mentioned items to me, we will make a best effort to return your completed mortgage pre-approval results within 24 hours.

I appreciate and value the opportunity to serve you in financing your home purchase! Please do not hesitate to contact me directly at (425) 350-7136 if you may have any questions!

Dan KellerDan Keller - MLO# 115349Mortgage AdvisorBrie Sidener/Office: 8a-4p: (425) 947-8533 / Dan Keller cell after hours (425) 350-7136

Dan Keller - [MLO# 115349] New American Funding 12220 113th Ave NE Suite 120 Kirkland, WA 98034

FAX TRANSMITTAL SHEET

Dan Keller Team

New American Funding

(425) 968-6382

(425) 947-8533