Morgan Stanley Industrials and Natural Resources … Stanley Industrials and Natural Resources...

32

www.thalesgroup.com Morgan Stanley Industrials and Natural Resources Summit London 10 September 2015

Transcript of Morgan Stanley Industrials and Natural Resources … Stanley Industrials and Natural Resources...

www.thalesgroup.com

Morgan Stanley Industrials and Natural Resources Summit London

10 September 2015

2

Thales at a glance

(*) Non-GAAP measure - Income from operations; plus the share of net income or loss of equity affiliates less: amortisation of intangible assets acquired (PPA) (**) Excluding the impact of the 35% share of net esult of DCNS (***) Based on foreign exchange rates as of February 2015

Aerospace

39%

Transport

11%

Defence & Security

50%

FY 2014 sales by segment

FY 2014 sales by geography

North America

11%

France

26%

United Kingdom

10%

Other Europe 23%

Australia 5%

Emerging Markets

23%

FY 2014 EBIT(*)

1.1

Employees

61,000

Global presence

56 countries

FY 2014 sales

13.0 billion euros

billion euros (**)

2015 objectives

Order

intake

Growing, beyond the high level

reached in 2014

Higher emerging markets

contribution

Sales Low single digit growth

EBIT(*) €1,130-1,150m (***)

2017/18 objectives

Sales Moderate growth

EBIT(*)

margin 9.5-10%

3

▌Aerospace

Avionics: continued positive dynamics for cockpit avionics

and IFEC

Space: telecom market remains highly competitive

▌ Transport

Strong demand in both emerging markets and Europe

▌Defence & Security

Elevated geopolitical tensions

Improved outlook in mature markets despite ongoing budget

pressures

Opportunities in emerging markets

H1 2015 business environment

4

▌Strong order intake

driven by emerging markets

▌Return to top line growth

▌ Further EBIT improvement

H1 2015 highlights

Continued focus on profitable growth

5

5,695

6,347

H1 2014 H1 2015

Sales

5,220

6,224

H1 2014 H1 2015

Order intake

402

473

H1 2014 (b) H1 2015

EBIT (a)

€m

(a) Non-GAAP measure: see definition in appendix

(b) In this presentation, H1 2014 EBIT has been restated to take into account the introduction of IFRIC 21

€m

€m €m

H1 2015 key figures

-535

-304

H1 2014 H1 2015

Free Operating Cash Flow

+19% +11%

+18%

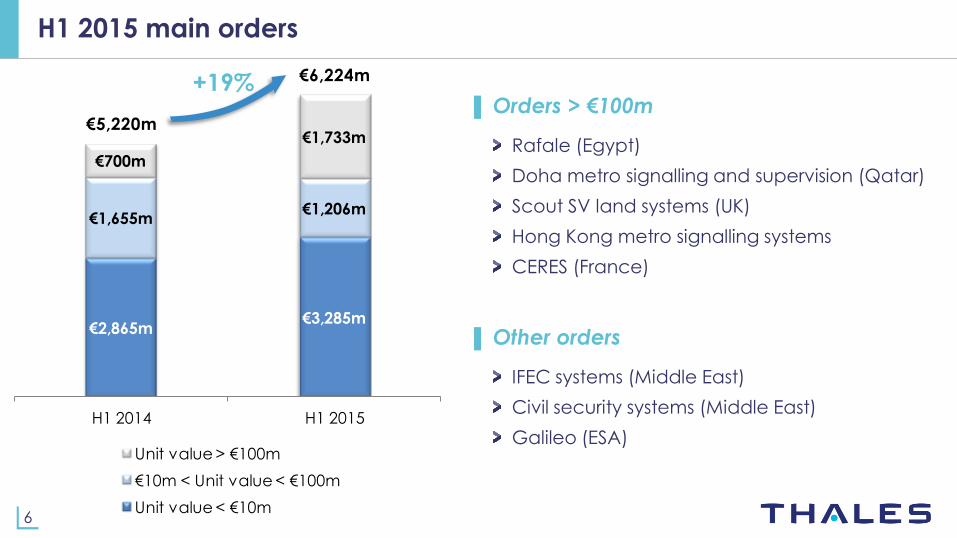

6

€2,865m€3,285m

€1,655m€1,206m

€700m

€1,733m€5,220m

€6,224m

H1 2014 H1 2015

Unit value > €100m

€10m < Unit value < €100m

Unit value < €10m

H1 2015 main orders

▌ Orders > €100m

Rafale (Egypt)

Doha metro signalling and supervision (Qatar)

Scout SV land systems (UK)

Hong Kong metro signalling systems

CERES (France)

▌ Other orders

IFEC systems (Middle East)

Civil security systems (Middle East)

Galileo (ESA)

+19%

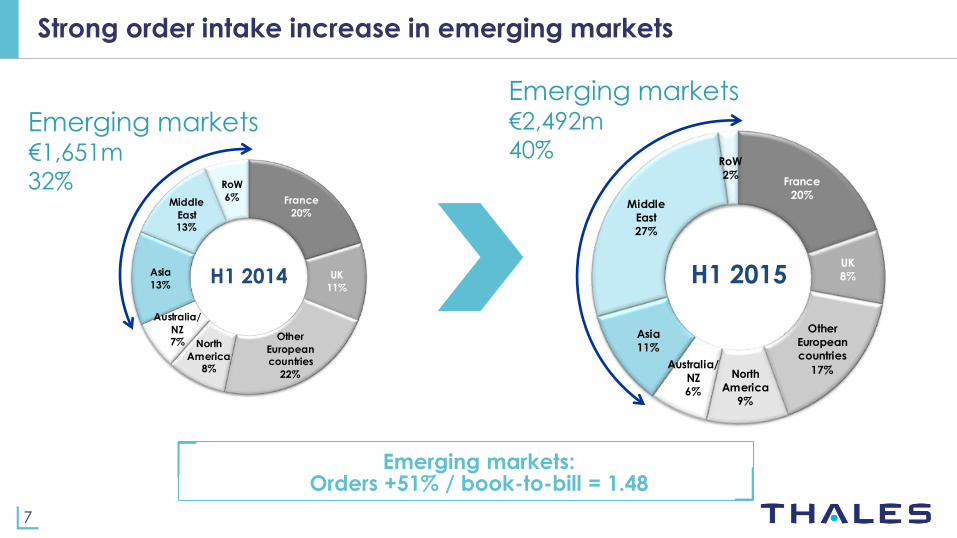

7

France

20%

UK

11%

Other

Europeancountries

22%

North

America8%

Australia/

NZ7%

Asia

13%

Middle

East13%

RoW

6%

H1 2014

France

20%

UK

8%

Other

European

countries

17%North

America

9%

Australia/

NZ

6%

Asia

11%

Middle

East

27%

RoW

2%

H1 2015

Strong order intake increase in emerging markets

Emerging markets €1,651m

32%

Emerging markets €2,492m

40%

Emerging markets: Orders +51% / book-to-bill = 1.48

8

Summary P&L: from sales to EBIT

(a) In this presentation, "organic" means "at constant scope and exchange rates"

(b) Non-GAAP measure: see definition in appendix.

Return to organic sales growth

Continued

EBIT improvement

€m

total organic

Sales 6,347 5,695 +11% +6%

Gross margin 1,520 1,399 +9% +4%

in % of sales 23.9% 24.6%

Indirect costs (1,064) (998) +7% +2%

in % of sales 16.8% 17.5%

o/w R&D expenses (310) (286) +9% +4%in % of sales 4.9% 5.0%

o/w M&S expenses (495) (456) +8% +4%in % of sales 7.8% 8.0%

o/w G&A expenses (259) (256) +1% -5%in % of sales 4.1% 4.5%

Restructuring costs (43) (53) -19% -19%

in % of sales 0.7% 0.9%

Share of net result of equity-accounted affiliates excl. DCNS 50 42 +19% -5%

EBIT (a)

excl. DCNS 463 391 +18% +11%

in % of sales 7.3% 6.9%

Share of net result of DCNS 10 10

EBIT (a) 473 402 +18% +10%

in % of sales 7.5% 7.1%

changeH1 2015 H1 2014

9

402

+29

+74+10

-10-13

-19

473

H1 2014

EBIT (a)

Scope

and FX

Organic

operationalperformance

Restructuring

charges

Pension

servicecosts

Add'l

expensedR&D

Add'l

expensedM&S

H1 2015

EBIT (a)

€m

(a) Non-GAAP measure: see definition in appendix.

+18%

EBIT bridge

Top line growth and efficiency measures drive EBIT increase

10

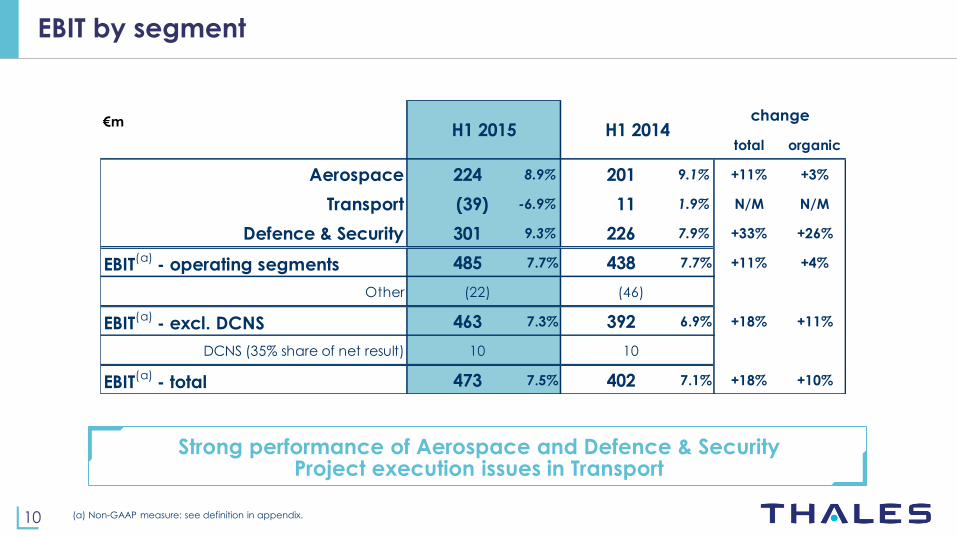

EBIT by segment

Strong performance of Aerospace and Defence & Security Project execution issues in Transport

(a) Non-GAAP measure: see definition in appendix.

€m

total organic

Aerospace 224 8.9% 201 9.1% +11% +3%

Transport (39) -6.9% 11 1.9% N/M N/M

Defence & Security 301 9.3% 226 7.9% +33% +26%

EBIT(a)

- operating segments 485 7.7% 438 7.7% +11% +4%

Other (22) (46)

EBIT(a)

- excl. DCNS 463 7.3% 392 6.9% +18% +11%

DCNS (35% share of net result) 10 10

EBIT(a)

- total 473 7.5% 402 7.1% +18% +10%

changeH1 2015 H1 2014

11

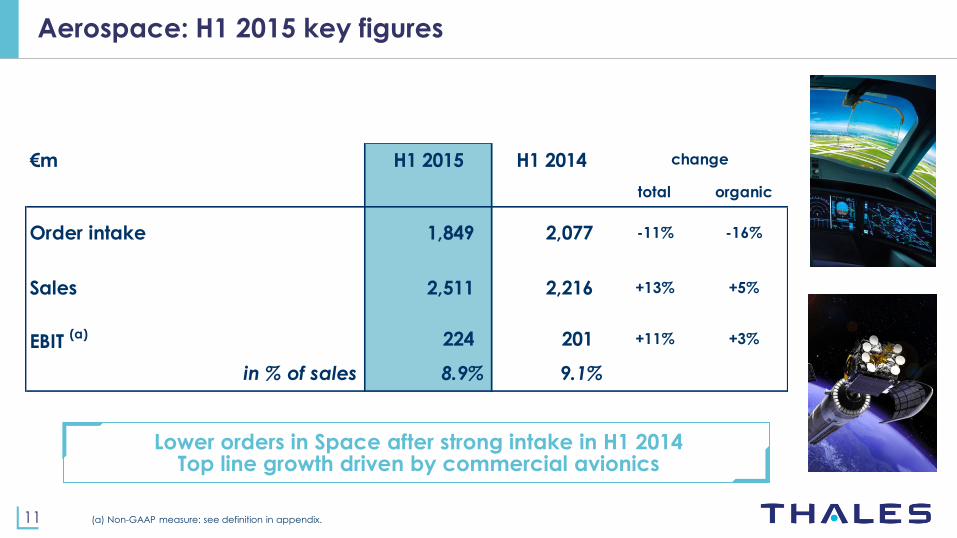

Aerospace: H1 2015 key figures

Lower orders in Space after strong intake in H1 2014 Top line growth driven by commercial avionics

€m H1 2015 H1 2014

total organic

Order intake 1,849 2,077 -11% -16%

Sales 2,511 2,216 +13% +5%

EBIT (a) 224 201 +11% +3%

in % of sales 8.9% 9.1%

change

(a) Non-GAAP measure: see definition in appendix.

12

Transport: H1 2015 key figures

Strong order intake momentum Project execution weighs on profitability, action plan underway

€m H1 2015 H1 2014

total organic

Order intake 1,197 637 +88% +80%

Sales 569 571 0% -6%

EBIT (a) (39) 11 N/M N/M

in % of sales -6.9% 1.9%

change

(a) Non-GAAP measure: see definition in appendix.

13

Defence & Security: H1 2015 key figures

Growing order intake (Rafale/Egypt) Higher profitability driven by top line growth and good project execution

€m H1 2015 H1 2014

total organic

Order intake 3,152 2,485 +27% +22%

Sales 3,229 2,873 +12% +9%

EBIT (a) 301 226 +33% +26%

in % of sales 9.3% 7.9%

change

(a) Non-GAAP measure: see definition in appendix.

14

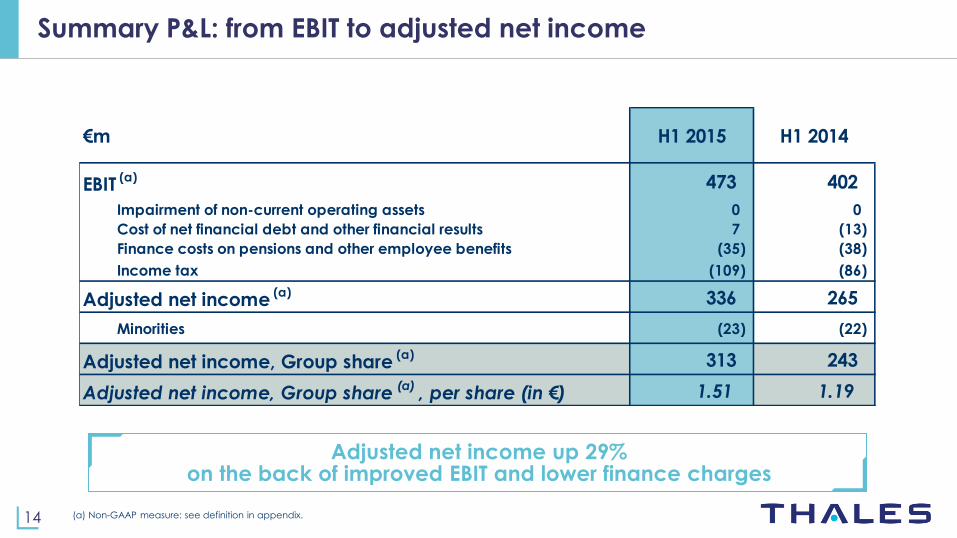

Adjusted net income up 29% on the back of improved EBIT and lower finance charges

Summary P&L: from EBIT to adjusted net income

(a) Non-GAAP measure: see definition in appendix.

€m H1 2015 H1 2014

EBIT (a) 473 402

Impairment of non-current operating assets 0 0

Cost of net financial debt and other financial results 7 (13)

Finance costs on pensions and other employee benefits (35) (38)

Income tax (109) (86)

Adjusted net income (a) 336 265

Minorities (23) (22)

Adjusted net income, Group share (a) 313 243

Adjusted net income, Group share(a)

, per share (in €) 1.51 1.19

15

Cash flow

Positive impact of downpayments on export contracts

(a) Non-GAAP measure: see definition in appendix.

€m H1 2015 H1 2014

683 582

Change in WCR & contingency reserves (697) (824)

Payment of contributions / pension benefits (60) (56)

Financial interest paid 10 (4)

Income tax paid (42) (44)

(106) (347)

Net operating investments (198) (188)

Free operating cash flow (a) (304) (535)

Net cash flows from operating activities

Operating cash flows before WCR changes

16

€m

Movement in net cash

Improved FOCF, strong net cash position

53

+1 036

-304

-81

-88

-231

+102

+104 +23 614

Net cash

30.06.2014

Free operating

cash flowH2 2014

Free operating

cash flowH1 2015

Deficit

paymentUK pensions

Disposals/

acquisitions

Dividends FX Stock options Other Net cash

30.06.2015

17

2015 priorities: a mid-year review

▌ What we said in February

Ambition Boost actions across all businesses and countries

Fixing issues in Transport

Monitoring and supporting DCNS

recovery

Deliver top line growth

Accelerate our globalisation

▌ Status

Ambition Boost delivers: EBIT(a) up 18% while keeping sustained R&D and commercial efforts

Comprehensive contract portfolio review by new management team

Recovery plan underway, drawing on resources from Aerospace and Defence & Security

DCNS on track to deliver breakeven

performance in 2015

Sales up 11% vs. H1 2014

EM orders up 51%, EM sales up 26%

vs. H1 2014

(a) Non-GAAP measure: see definition in appendix.

18

(a) Non-GAAP measure: see definition in appendix

(b) Based on foreign exchange rates as of February 2015

Order intake Growing – beyond the high level reached in 2014

Higher emerging markets contribution

Sales Low single digit growth

EBIT(a)

€1,130-1,150 m (b)

2015 objectives

Objectives confirmed

Appendix

20

▌Q3 and 9m 2015 sales 21 October 2015

▌2015 annual results 24 February 2016

Upcoming events

21

H1 2015 sales by destination

total organic

France 1,569 1,610 -3% -3%

United Kingdom 638 621 +3% -8%

Other European countries 1,263 1,232 +2% +1%

Europe 3,470 3,463 +0% -2%

North America 759 536 +42% +15%

Australia/NZ 365 327 +12% +7%

Asia 842 784 +7% +2%

Middle East 647 377 +71% +61%

Rest of the world 265 208 +27% +24%

Emerging markets 1,753 1,369 +28% +21%

Total 6,347 5,695 +11% +6%

€m H1 2015 H1 2014change

France

25%

UK

10%

Other

European

countries

20%

N America

12%

Australia/

NZ

6%

Asia

13%

Middle

East

10%

RoW

4%

H1 2015

22

H1 2015 adjusted net result

Sales 6,347 6,347 Cost of sales (4,827) (4,827)

R&D (310) (310)

SG&A costs (754) (754)

Restructuring costs (43) (43)

Amortisation of intangible assets (PPA) (53) 53 0

Income from operations 360 Impairment of non-current operating assets 0 --- (*)

Disposal of assets, change in scope and others (3) 3 0

Share in net income (loss) of equity affiliates 47 13 60

Income of operating activities

incl. share in net income of equity affiliates 404

EBIT 473 Impairment of non-current operating assets --- (*) 0

Cost of net financial debt 5 5

Other financial income (expense) (13) 15 2

Finance costs on pensions

and other employee benefits (25) (10) (35)

Income tax (88) (18) (1) (5) 3 (109)

Net income (loss) 282 48 2 10 7 335 Minorities (16) (6) (1) 1 (23)

Net income (loss), Group share 266 42 2 9 8 313

(*) included within "Income of operating activities incl. share in net income of equity affiliates" in the consolidated P&L and within "Net income" in the adjusted P&L

Adjusted

P&L

H1 2015

€m

Consolidated

P&L H1 2015

Amortisation of

intangible assets

(PPA)

Disposal of

assets and

others

Change in fair

value of

derivative FX

instruments

Actuarial

gains/losses

on other long

term benefits

23

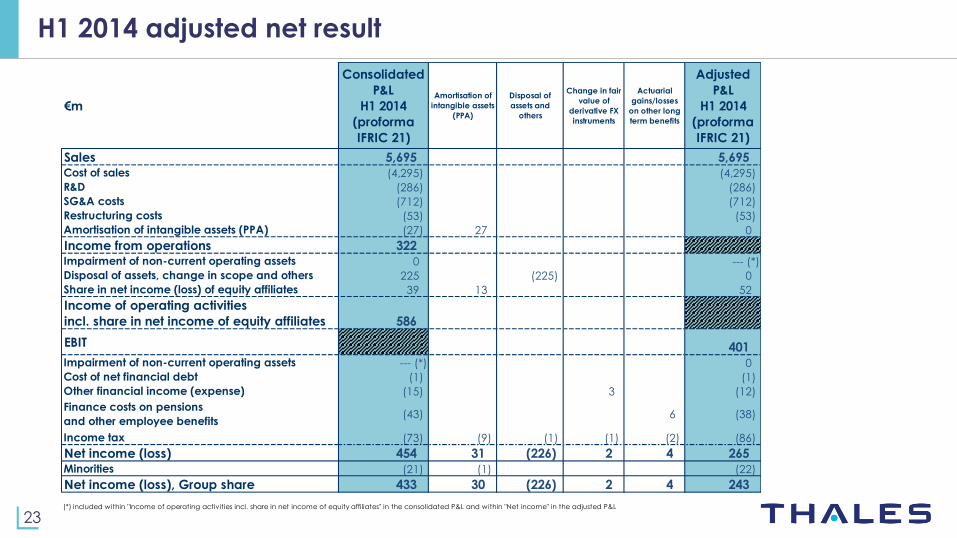

H1 2014 adjusted net result

Sales 5,695 5,695Cost of sales (4,295) (4,295)

R&D (286) (286)

SG&A costs (712) (712)

Restructuring costs (53) (53)

Amortisation of intangible assets (PPA) (27) 27 0

Income from operations 322Impairment of non-current operating assets 0 --- (*)

Disposal of assets, change in scope and others 225 (225) 0

Share in net income (loss) of equity affiliates 39 13 52

Income of operating activities

incl. share in net income of equity affiliates 586

EBIT 401Impairment of non-current operating assets --- (*) 0

Cost of net financial debt (1) (1)

Other financial income (expense) (15) 3 (12)

Finance costs on pensions

and other employee benefits(43) 6 (38)

Income tax (73) (9) (1) (1) (2) (86)

Net income (loss) 454 31 (226) 2 4 265Minorities (21) (1) (22)

Net income (loss), Group share 433 30 (226) 2 4 243

(*) included within "Income of operating activities incl. share in net income of equity affiliates" in the consolidated P&L and within "Net income" in the adjusted P&L

Actuarial

gains/losses

on other long

term benefits

Adjusted

P&L

H1 2014

(proforma

IFRIC 21)

€m

Consolidated

P&L

H1 2014

(proforma

IFRIC 21)

Amortisation of

intangible assets

(PPA)

Disposal of

assets and

others

Change in fair

value of

derivative FX

instruments

24

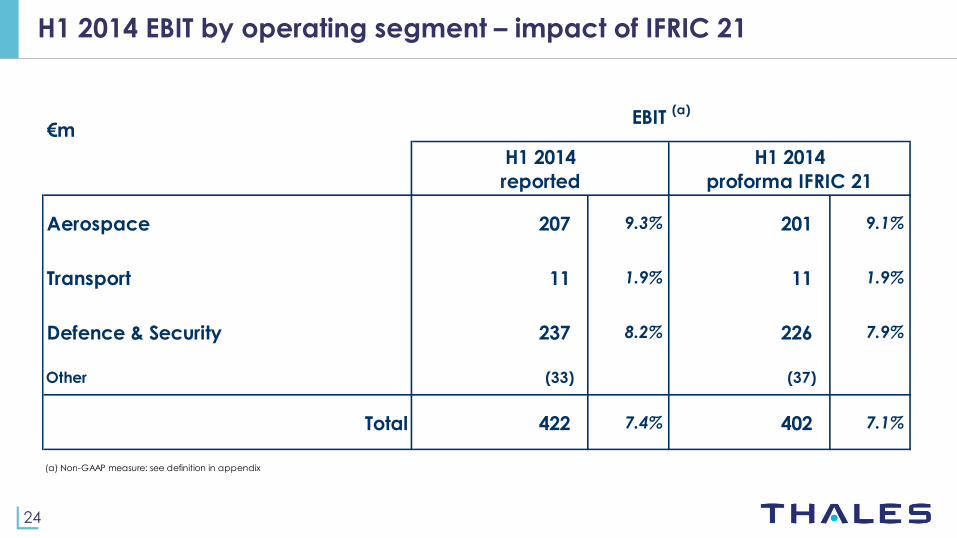

H1 2014 EBIT by operating segment – impact of IFRIC 21

€m

Aerospace 207 9.3% 201 9.1%

Transport 11 1.9% 11 1.9%

Defence & Security 237 8.2% 226 7.9%

Other (33) (37)

Total 422 7.4% 402 7.1%

(a) Non-GAAP measure: see definition in appendix

H1 2014

proforma IFRIC 21

EBIT (a)

H1 2014

reported

25

Q2 2015 order intake by sector

Q2 2015 Q2 2014

total organic

Aerospace 1,067 1,301 -18% -22%

Transport 735 380 +93% +83%

Defence & Security 1,586 1,461 +9% +4%

Other 13 3

Total 3,401 3,145 +8% +3%

change€m

26

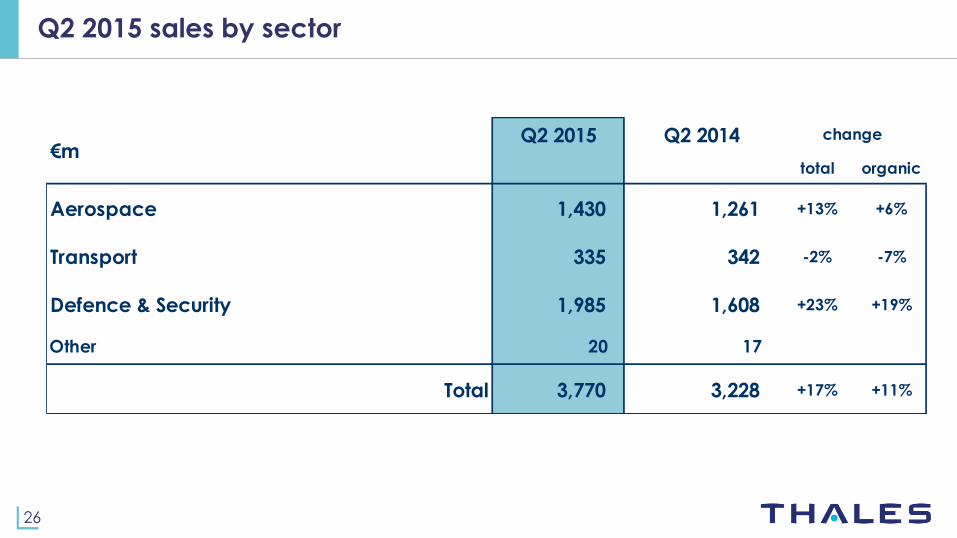

Q2 2015 sales by sector

Q2 2015 Q2 2014

total organic

Aerospace 1,430 1,261 +13% +6%

Transport 335 342 -2% -7%

Defence & Security 1,985 1,608 +23% +19%

Other 20 17

Total 3,770 3,228 +17% +11%

change€m

27

Thales on board Rafale

Thales =

about 25% of total aircraft value

28

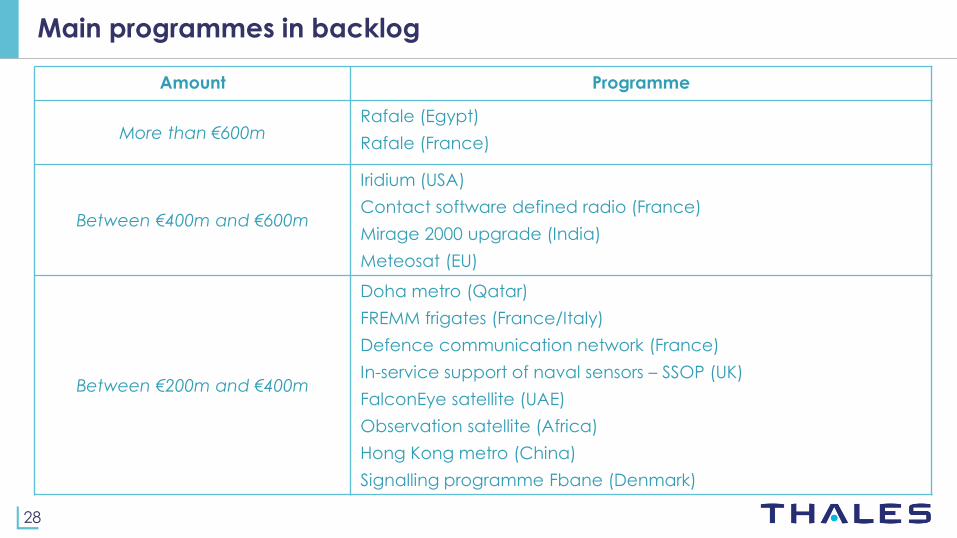

Amount Programme

More than €600m Rafale (Egypt)

Rafale (France)

Between €400m and €600m

Iridium (USA)

Contact software defined radio (France)

Mirage 2000 upgrade (India)

Meteosat (EU)

Between €200m and €400m

Doha metro (Qatar)

FREMM frigates (France/Italy)

Defence communication network (France)

In-service support of naval sensors – SSOP (UK)

FalconEye satellite (UAE)

Observation satellite (Africa)

Hong Kong metro (China)

Signalling programme Fbane (Denmark)

Main programmes in backlog

29 (a) French State shares are held directly and indirectly through TSA, a 100% state-owned holding company

Thales shareholding structure – June 2015

French

State (a)

26.1%

Dassault

Aviation

25.0%

Free float

48.9%

o/w

Employees

1.9%

Total share count as of 30 June:

210,162,630

30

Leadership Team

Alex Cresswell

Executive Vice-President

Land & Air Systems

Marc Darmon

Executive Vice-President

Secure Communications

and Information Systems

Pierre Eric Pommellet

Executive Vice-President

Defence Mission Systems

Gil Michielin

Executive Vice-President

Avionics

Jean-Loïc Galle

Executive Vice-President

Space

Millar Crawford

Executive Vice-President

Transportation Systems

Pascale Sourisse

Senior Executive

Vice-President

International Development

Michel Mathieu

Senior Executive

Vice-President

Chief Operating Officer and

Chief Performance Officer

David Tournadre

Senior Executive

Vice-President

Human Resources

Pascal Bouchiat

Senior Exective

Vice-President

Chief Finance Officer

Hervé Multon

Executive Vice-President

Strategy

Research and Technology

Patrice Caine Chairman and

Chief Executive Officer

Isabelle Simon Group Secretary & General

Counsel

31

This presentation contains non-Generally Accepted Accounting Principles (GAAP) financial measures. Thales regards such non-GAAP

financial measures as relevant operating and financial performance indicators for the Group, as they allow non-operating and non-

recurring items to be excluded. Thales definitions for such measures may differ from similarly titled measures used by other companies or

analysts.

▌Organic: at constant scope and exchange rates.

▌Book-to-Bill ratio: ratio of orders received to sales.

▌EBIT: income from operations; plus the share of net income or loss of equity affiliates less: amortisation of intangible assets acquired (PPA)

▌Emerging Markets: All countries in Middle East, Asia, Latin America and Africa

▌Adjusted net income: net income, less the following elements, net of the corresponding tax effects: (i) amortisation of intangible assets

acquired, (ii) disposal of assets, change in scope of consolidation and other, (iii) change in fair value of derivative foreign exchange

instruments (recorded in "other financial results" in the consolidated accounts), (iv) actuarial gains or losses on long-term benefits

(accounted within the "finance costs on pensions and employee benefits" in the consolidated accounts).

▌Adjusted EPS: ratio of adjusted net income (as defined above) to average number of shares outstanding.

▌Free Operating Cash Flow: net cash flow from operating activities, less: capital expenditures, less: deficit payments on pensions in the

United Kingdom.

Definition of non-GAAP measures

Thales – Tour Carpe Diem – 31 Place des Corolles – 92098 Paris La Défense – France www.thalesgroup.com

This presentation may contain forward-looking statements. Such forward-looking statements are trends or objectives, as the case may be, and shall not be construed as constituting forecasts regarding the Company’s results or any other performance indicator. These statements are by nature subject to risks and uncertainties as described in the Company’s registration document ("Document de référence") filed with Autorité des Marchés Financiers. These statements do not therefore reflect future performance of the Company, which may be materially different.